the empowered investor part i - scorpiopartnership...

TRANSCRIPT

MARKETING COMMUNICATIONThis document is provided to you on a confidential basis. It must not be circulated, distributed, reproduced or disclosed to any other person without the prior written consent of BNP Paribas.The content of this document was prepared by Scorpio Partnership. This document has been produced by Scorpio Partnership in cooperation with BNP Paribas pursuant to an arrangement between the parties and this document may be distributed by BNP Paribas.

THE EMPOWERED INVESTOR PART I

The new rules of engagement for Asia-Pacific’s Wealth Managers

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS2

KEY ACTIONSFOR THE WEALTH MANAGEMENT INDUSTRY

1. GET TO KNOW A NEW CLIENTELEEmpowered Investors are the new generation of private banking client, defined not by demographics but by their drive. With distinct needs and preferences, advisors will need to spend time understanding their delivery expectations if they are to impress.

The new generation of private banking client, defined by their drive

“”

2. CREATE A FULLY-CUSTOMISED INVESTMENT JOURNEYHigh-net worth individuals want to see the benefits of mass customisation extended to their advisory relationships. Wealth Managers should apply this principle to all stages of the cycle, by providing customisable data and tools so that clients can evaluate portfolio performance.

Providing customisable data and tools

“”

3. EMBED KNOWLEDGE-SHARING TO FORM A TRUSTING PARTNERSHIPClients want more input in the investment process; Wealth Managers must enhance collaboration. They should provide more frequent, digestible market news and ac-cess to investor resources outside of meetings, so that clients feel comprehensively prepared.

more frequent, digestible market news and access to investor resources

“

”4. EMPOWER CLIENTS TO EXECUTE THEIR OWN IDEAS AND FOCUS ON

STRATEGY IN ADVISOR MEETINGSWealthy individuals in APAC are becoming increasingly self-directed. Platforms should be refashioned as ‘hubs’ where clients can conduct analysis and act upon their own ideas. Advisor meetings should be future-focussed, geared towards for-mulating strategy together.

Platforms should be refashioned as ‘hubs’ where clients can conduct analysis

“

”5. USE A MULTI-CHANNEL APPROACH TO IMPROVE THE PACE OF

INFORMATION EXCHANGEAsia’s wealthy clients are already using newer channels to engage effectively with advisors. Wealth Managers should craft a multi-channel approach that gives in-vestors more frequent snapshots of information, so they can nimbly monitor and rebalance portfolios.

clients are using newer channels to engage effectively with advisors

“”

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS3

FOREWORDSTEPHANE HONIG & KYOYA OKAZAWA

Asia-Pacific is now home to the world’s largest population of High Net Worth Individuals (HNWI), with the Wealth Management industry playing a critical role in the process of wealth creation, preservation and transmission.

At BNP Paribas, we believe that wealth preservation and growth spans the whole Wealth Management supply chain, covering investment banks, asset managers and insurance companies.

We take great pride in helping Asian private banks focus on their value propositions, in order to better serve their end clients.

Society at large is transforming and the investment patterns of Asian HNWI are no exception. A new generation of wealthy investors has emerged, with their own set of characteristics and expectations.

There are profound trends in place which shape how wealth managers interact with their clients, including:• New sectors driving wealth creation• Increasing influence of technology• Huge amounts of wealth being handed down the

generations• Growth of onshore private banking• Sustainability• The evolution of the role of private banks in the

investment decision making process

Helping private banks embrace this new paradigm is at the heart of our strategy and commitment.

BNP Paribas’s collaboration with Scorpio Partnership aims to build a collective understanding of the behavioral changes Asian HNWI have undergone, as well as their expectations surrounding private banks. This white paper leverages Scorpio Partnership’s extensive experience in the area of strategic research around client engagement and value proposition.

Our first edition highlights the new generation of private banking clients, or ‘Empowered Investors’, offering insights around successful investment journeys from building a trust-based relationship, to the role of digital tools.

We embrace the ‘Empowered Investor’ and look forward to navigating this exciting journey with private banks across the region, to serve Asian economies, entrepreneurs and successful individuals who dedicate their lives to great achievements.

Yours sincerely

Stephane Honig Head of Sales Wealth Management & Family OfficesGlobal Markets Asia PacificBNP Paribas

Kyoya Okazawa Head of Institutional ClientsGlobal Markets Asia PacificBNP Paribas

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS4

Customisation – the art of making a wide-ly-available product or service feel as if it has been designed with you in mind – is a pre-requisite for any wealth management of-fering. The sector rightly prides itself on being relationship-driven, with long-term loyalty

secured only through a years-long and painstaking ac-cumulation of client knowledge. The effort is colossal but the reward considerable: the resulting relationships are often very close, occasionally life-long.

Wealth Managers may therefore be forgiven for thinking that customisation is not just an area of strength but the defining hallmark of our industry, setting it apart from Retail counterparts. The value proposition is a dual ex-pertise, bringing together a deep understanding of cli-ents’ lives with knowledge of investing, to guide towards the right outcome for each individual. In a client-centric industry like Wealth, the conventional wisdom is that customisation has always been king.

But, interestingly for Wealth Managers, high net worth individuals (HNWIs) now appear to be scaling up their expectations in line with what is now considered the

‘normal’ customer experience in other industries. Their growing appetite for more and better customisation across the entire private banking journey is one of sever-al unifying trends in a diverse set of Asian financial hubs.

To respond effectively, advisors need to look for inspira-tion beyond the boundaries of Wealth.

Expectations are being set not by direct competitors, but by brands whose products manage to delight everyday – like Nike, whose NIKEiD collection allows clients to fully customise their footwear; or luxury boutique Atelier Co-logne, where an intimately personal giftset can be cre-ated within three clicks. In an industry that believes it already does ‘tailored’ and ‘bespoke’ well, there is a real risk that Wealth Managers will focus efforts on the wrong

HNWIs are scaling up their expectations in line with what is ‘normal’ in other industries.

EMERGENCEOF THE EMPOWERED INVESTOR

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS5

areas if they fail to first understand how clients them-selves are now defining these terms.

Responding to their personalisation demands means prioritising which areas are likely to impact strongly on HNW engagement – a critical decision in a tight-margin environment. To investigate the investor perspective, BNP Paribas Corporate and Institutional Banking (CIB) and Scorpio Partnership reached out to 1,020 HNWIs from eight leading Asian-Pacific markets: Australia, Chi-na, Hong Kong, Indonesia, Japan, Malaysia, Singapore and Taiwan.

What we increasingly observe is a new client profile in Asia-Pacific today: the ‘Empowered Investor’. Concerned that the knowledge gap with their advisors has grown too wide, Asia’s wealthiest now seek to improve their investment understanding. They want the playing-field to be levelled to foster genuine collaboration within the advisory relationship. They want to have more informed conversations with their Wealth Managers, believing that they will result in better outcomes. And they believe cus-tomisation should cover every stage of the investment cycle – and that it is part and parcel of offering a ‘be-spoke’ service.

The Empowered Investor quickly identifies opportunities

for their advisors to help improve their investment un-derstanding; for example, by reconfiguring online plat-forms, adapting communications and introducing smart ways to implement their ideas. They expect a holistic view of their investments, so that they can take their next steps with confidence.

The clamour for more customisation is not limited to a minority of investors but is evident in the views of core client segments, with the ultra-wealthy among the most vocal in their desire for change. These clients desire a shift in the current arrangement with advisors and are already redefining the role of private banks in their lives.

In a two-part series, BNP Paribas explores the success fac-tors for Wealth Managers in this changing environment. In Part I, we discuss the emergence of the Empowered Investor and why a renewed approach to customisation across the private banking experience will redress the balance. In Part 2, we will explore how to future-proof the Wealth advisory model.

from eight leading Asian-Pacific markets ‘believe customisation should cover every stage of the investment cycle’.

1,020 HNWIs

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS6

Across Asia-Pacific, a different kind of investor is on the rise. They are not defined by demo-graphic detail – in fact they are visible at all life-stages as well as up and down the wealth curve. They do not limit themselves to us-ing one specific product or having one type

of banking relationship. Instead they are distinguishable by their attitudes – most importantly, their high expecta-tions and hopes of the Wealth advisory relationship.

This new wave of clients is independent in spirit and wants resources to conduct research, execute investment ideas and re-balance portfolios where necessary. But they also hope to be a genuine partner to their advisor at all stages of the investment cycle. Their ambition is to de-velop a higher-value relationship, where both sides have access to self-directed instruments (including product access and trading services), but decisions are frequently mulled over and taken together.

In our study, we asked respondents to visualise what their dream private bank would look like. We then filtered re-sponses according to how they defined ‘value’ in Wealth Management: specifically, their expectations around cus-tomisation and self-service during various points of the client journey, and the type of interaction they seek with their advisors.

Using this approach, we found that just over half (529) of respondents in our 1,020-strong HNWI sample can be categorised as ‘Empowered Investors’. Their prevalence and profile [Figure 1] should act as encouragement to fi-nancial advisors across the Asia-Pacific region to re-think their engagement strategy to improve and impress.

The Empowered Investor mind-set can be found in every generation. The average age is 39 years old but this type of client is technically most likely to be part of the Baby Boomer cohort, representing 61% of the over-50 sample. A majority of millennials also exhibit their behaviours, with 52% falling into this category; and just under half of 35 to 49 year-olds fit this profile.

DEFININGA NEW CLIENTELE

TOTAL SAMPLE

MALE

AUSTRALIA

USD1M TO USD3M

UNDER 35

JAPAN

HONG KONG

USD5M TO USD10M

50 AND OVER

SINGAPORE

CHINA

USD3M TO USD5M

35-49

MALASYA

INDONESIA

USD10M AND OVER

FEMALE

NUMBER OF RESPONDENTS

GENDER

COUNTRY OF RESIDENCE

FINANCIAL ASSETS

AGE

TAIWAN

EMPOWERED INVESTOR REST OF SAMPLE

52%

49%

48%

51%

46%54%

33%67%

20%80%

63%37%

56%44%

67%33%

50%50%

33%67%

62%38%

48%52%

52%48%

39%61%

51%49%

61%39%

48%52%

44%56%

FIGURE 1: SAMPLE BREAKDOWN, EMPOWERED INVESTOR PROFILE

Source: BNP Paribas & Scorpio Partnership

Their wealth and age characteristics taken all together mean they are within the sweet-spot for Asian wealth managers. They are more likely to be part of the ul-tra-wealthy segment, with 56% of those with investable assets of USD$10 million+ fulfilling the criteria. On aver-age they have a net worth of USD$9.1 million, compared with USD$7.9 million for the rest of the sample.

is the average age of the Empowered Investor.

39 years old

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS7

Empowered Investors are focussed on the value their Wealth relationships bring and are willing to find other partners if they are under-serviced. But they also reward good value with loyalty and are more likely to say they are satisfied with their current solutions than other in-vestors, giving an average performance score of 7.4 out of 10 (compared with 5.5 by the rest of the client sample).

They want a closer, more trusting advisory relationship – and would be willing to pay more to reap the rewards. Empowered Investors are on average +2.3 on a willing-ness-to-pay scale of -5 to +5, (compared with +1.1 for the rest of the sample), showing they are more comfortable with shouldering a higher fee if they receive gold-stand-ard service. Their motivation to become self-directed does not stem from dissatisfaction with the status quo, but a desire to make more of its ample opportunities.

For Wealth Managers across the Asian region the emergence of the Empowered Investor should be a game-changer. These clients want – and are willing to

pay a premium for – the bespoke experience that the in-dustry champions, if it can be reconfigured into a trans-parent partnership. Having greater autonomy would make them value their advisors more, firstly by creating trust within client engagement and in the longer-term by enabling them to close the knowledge gap.

By enacting their recommended changes to the invest-ment journey, financial advisors have an opportunity to bring long-lasting value to their relationships with Asia’s wealthy investors. But to do this, they will first need to take the time to really understand the Empowered In-vestor: their needs, their demands and their constraints.

is the average net worth of the Empowered Investor.

9.1 million USD

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS8

Mass personalisation has become, re-markably quickly, ubiquitous in modern life. Whether taking out an insurance policy, looking for a film or searching for news, consumers can now reason-ably expect businesses to capture their

behavioural data, learn from their past activity and use their current location to offer a tailored proposition.

The resulting customised approach has proved effective in making transactional, inhuman interactions feel like intimate and trusting customer relationships. Brands are transformed from sellers to advisors, not only helping people find what they want now but guiding on what they may need in the future. To do this they have relied heavily on powerful customer intelligence platforms to cultivate a credible image. Prominent examples include The Echo Nest (now owned by Spotify) for recommending music playlists and Google Now’s helpful ‘nudges’ towards local promotions, based on users’ search history.

Having experienced the benefits of mass personalisation in many other areas of their lives, HNWIs now want to

see this value delivered in their Wealth relationships too. For private banks already enjoying the status of trusted advisors, the challenge is to use client intelligence for more ambitious aspirations than product promotions; even using the opportunity to transform the overall client experience into a collaborative partnership.

Whereas in the past investors may have been comforta-ble entrusting major investment decisions predominantly to an expert, today there is a strong desire for more input and control of the process, with personalised portfolio information the natural starting-point [Figure 2].

CUSTOMISATION MUST BEA FUNDAMENTAL PRINCIPLE OF THE INVESTMENT JOURNEY

What is the one major action your current primary provider can take?“Give more customised input on my financial well-being.” Male, 35, Singapore

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS9

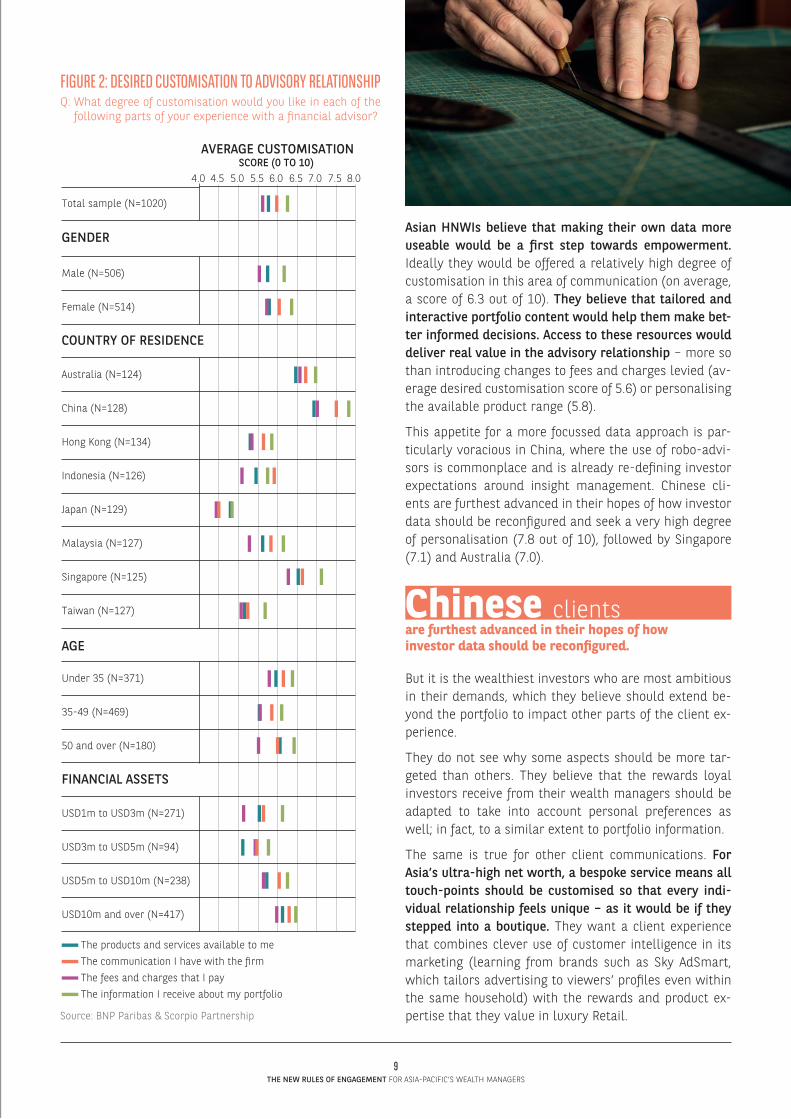

Asian HNWIs believe that making their own data more useable would be a first step towards empowerment. Ideally they would be offered a relatively high degree of customisation in this area of communication (on average, a score of 6.3 out of 10). They believe that tailored and interactive portfolio content would help them make bet-ter informed decisions. Access to these resources would deliver real value in the advisory relationship – more so than introducing changes to fees and charges levied (av-erage desired customisation score of 5.6) or personalising the available product range (5.8).

This appetite for a more focussed data approach is par-ticularly voracious in China, where the use of robo-advi-sors is commonplace and is already re-defining investor expectations around insight management. Chinese cli-ents are furthest advanced in their hopes of how investor data should be reconfigured and seek a very high degree of personalisation (7.8 out of 10), followed by Singapore (7.1) and Australia (7.0).

But it is the wealthiest investors who are most ambitious in their demands, which they believe should extend be-yond the portfolio to impact other parts of the client ex-perience.

They do not see why some aspects should be more tar-geted than others. They believe that the rewards loyal investors receive from their wealth managers should be adapted to take into account personal preferences as well; in fact, to a similar extent to portfolio information.

The same is true for other client communications. For Asia’s ultra-high net worth, a bespoke service means all touch-points should be customised so that every indi-vidual relationship feels unique – as it would be if they stepped into a boutique. They want a client experience that combines clever use of customer intelligence in its marketing (learning from brands such as Sky AdSmart, which tailors advertising to viewers’ profiles even within the same household) with the rewards and product ex-pertise that they value in luxury Retail.

4.0 4.5 5.0 5.5 6.0 6.5 7.0 7.5 8.0

Total sample (N=1020)

Male (N=506)

Female (N=514)

Australia (N=124)

China (N=128)

Hong Kong (N=134)

Indonesia (N=126)

Japan (N=129)

Malaysia (N=127)

Singapore (N=125)

Taiwan (N=127)

Under 35 (N=371)

35-49 (N=469)

50 and over (N=180)

USD1m to USD3m (N=271)

USD3m to USD5m (N=94)

USD5m to USD10m (N=238)

USD10m and over (N=417)

COUNTRY OF RESIDENCE

AGE

FINANCIAL ASSETS

AVERAGE CUSTOMISATIONSCORE (0 TO 10)

GENDER

The products and services available to me

The fees and charges that I pay The communication I have with the �rm

The information I receive about my portfolio

FIGURE 2: DESIRED CUSTOMISATION TO ADVISORY RELATIONSHIPQ: What degree of customisation would you like in each of the

following parts of your experience with a financial advisor?

Source: BNP Paribas & Scorpio Partnership

are furthest advanced in their hopes of how investor data should be reconfigured.

Chinese clients

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS10

EMBEDKNOWLEDGE-SHARING INTO THE CLIENT

EXPERIENCE TO BE A TRUE PARTNER

Driving the quest for data customisation is a straightforward client end-goal: a collabora-tive advisory relationship.

The first step in this direction is to build a better understanding of investment perfor-mance. But as information-sharing currently

tends to be provider-led and ad hoc, there is a strain in the delivery model, with clients eager to access market updates and news that may affect their portfolios.

What is the one major action your current primary provider can take?“Knowledge is power and the timely access to news and trends is vital.” Female, 43, Singapore

Overall 27% of APAC’s HNWIs currently views the con-fidence gained in their investments as the most impor-tant Wealth Manager attribute – a figure which rises to roughly a third in Australia, Hong Kong, Indonesia and Japan [Figure 3]. A fifth believes updates received on port-folio changes are their advisor’s defining responsibility. Clients are relying on their private banks to give them a view of market trends.

But they don’t expect to wait until scheduled touch-points for important updates from their primary advisors. They want immediate access to market knowledge so they can make their own judgements on their investments, in their own time. Inefficient information flow often re-sults in a frustrating knowledge gap between client and investment manager, with the former playing ‘catch-up’ during meetings rather than being able to discuss next steps together as a team.

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS11

GENDER

COUNTRY OF RESIDENCE

COUNTRY OF RESIDENCE

FINANCIAL ASSETS

AGE

TOTAL SAMPLE (N=688)

NUMBER OF RESPONDENTS

MALAYSIA (N=87)

INDONESIA (N=95)

TAIWAN (N=94)

HONG KONG (N=107)

HONG KONG (N=107)

USD5m to USD10m (N=176)

SINGAPORE (N=95)

JAPAN (N=59)

… makes me confident regarding my current investments

… provides active updates and information on portfolio and investment changes

… brings clarity to the decision making process

… invests time to counsel me in my investment plans and future opportunities

… helps me to create a strategy to improve my financial situation

… understands and adapts recommendations to my personal short term and long term needs

… gives me guidance I need to make good investment decisions

… introduces me to investment specialists

MALE (N=326)

AUSTRALIA (N=45)

AUSTRALIA (N=45)

USD1m to USD3m (N=161)

UNDER 35 (N=269)

FEMALE (N=362)

CHINA (N=106)

CHINA (N=106)

USD3m to USD5m (N=57)

35 - 49 (N=319)

FIGURE 3: VALUED WEALTH MANAGER ATTRIBUTESQ: Which of the following attributes and responsibilities do you value the most when

considering your current relationship with your primary contact at your Wealth Manager?

50 AND OVER (N=100)

TAIWAN (N=94)

USD10m and OVER (N=294)

33% 20% 16% 9% 9% 7% 4% 2%

33% 20% 16% 9% 9% 7% 4% 2%

20% 26% 23% 13% 8% 6% 2%2%

20% 26% 23% 13% 8% 6% 2%2%

27% 20% 11% 13% 9% 12% 8% 0%

26% 16% 11% 13% 10% 11% 11% 2%

31% 21% 16% 10% 7% 9% 5% 2%

27% 20% 13% 11% 10% 9% 8% 1%

32% 19% 12% 9% 10% 10% 8% 1%

23% 20% 15% 13% 10% 9% 9% 2%

32% 19% 14% 9% 8% 11% 7% 0%

32% 19% 14% 9% 8% 11% 7% 0%

23% 20% 15% 13% 10% 9% 9% 2%

23% 20% 15% 13% 10% 9% 9% 2%

23% 20% 15% 13% 10% 9% 9% 2%

25% 19% 14% 13% 8% 12% 6% 3%

24% 19% 12% 5% 11% 14% 14% 1%

28% 18% 13% 10% 10% 9% 10% 2%

26% 21% 14% 11% 10% 9% 7% 2%

24% 19% 12% 5% 11% 14% 14% 1%

20% 18% 12% 12% 18% 10% 11% 0%

33% 26% 11% 9% 2% 9% 11% 0%

Source: BNP Paribas & Scorpio Partnership

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS12

The ideal private banking relationship looks quite differ-ent to the current client experience. In the desired sce-nario, the value in the client-advisor model stems from having two partners working together to confirm a strat-egy. Advisors operate with full transparency, offering in-vestors portfolio data in raw format in advance of meet-ings, so that they can complete independent analysis, as well as in a customisable, easy-read format for quick re-view. With both sides having access to the same market data, the quality of discussion is high and conversations forward-looking, rather than an analysis of past events. The investment plan is grounded in a comprehensive understanding of the client’s goals. By contrast, tactical questions – such as being introduced to specialists or other banking needs – are deprioritised.

The desire for higher quality conversations is evident. Cli-ents across Asia-Pacific believe improving interactions with their advisor would mean discussions become solu-tions-oriented. Fifty-five percent of respondents would like to be using meetings to review overall progress to-wards their objectives [Figure 4], a proportion that rises to nearly two thirds of HNWIs in China and Indonesia. Similarly, a majority views discussing new aims and de-

ciding upon required portfolio changes as integral topics to be debated with advisors.

Baby boomer investors have the most ambitious view of what they want these interactions to be like. Those over 50 are considerably more likely to look to discuss new investment opportunities with their Wealth Managers (58%), than millennials (36%) or Generation X (42%) in-vestors. Their vision for the advisory relationship is for both sides to have a sophisticated market understand-ing, so that meetings can be future-focussed rather than reactive.

In their personal lives wealthy investors are continuously reminded by brands across other industries that they are focussed on the future to anticipate client needs. From the excitement of potential driverless technology in cars, to the more prosaic use of telematics for fairer premiums in insurance, to the helpful daily recommendations from Netflix and Amazon Prime, businesses prove to their cus-tomers every day that they can use their data intelligent-ly to add value to their lives.

The same expectations are now being applied to Wealth. Across ages and wealth bands, high-net worth individu-als want to experience the value that they have come to expect from other brands. They want their advisors to use different data sources not only to evaluate the past, but to forecast and plan for the future together.

of investors would like to be using meetings to review overall progress towards their objectives.

55 percent

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS13

FIGURE 4: IDEAL WEALTH MANAGER CONVERSATION TOPICSQ: In your ideal relationship with a personal advisor, which of the following key areas would be included in your interactions and

conversations with him / her?

We establish if new goals are required

We discuss relevant changes to my portfolio

We have a detailed discussion about every element of my wealth strategy

We discuss my broader banking needs (e.g. savings, mortgage)

We review overall progress towards my existing goals

I receive specialised advice related to a niche product

We discuss new investment opportunities

We discuss my broader wealth needs (e.g. tax planning, philanthropy)

I am introduced to other specialists

PERC

ENTA

GE

OF R

ESPO

NDE

NTS

0%

10%

20%

30%

40%

50%

60%

70%

Total sample(N=1020)

Australia(N=124)

China(N=128)

Hong Kong(N=134)

Indonesia(N=126)

Japan(N=129)

Malaysia(N=127)

Singapore(N=125)

Taiwan(N=127)

Under 35(N=371)

35-49(N=469)

50 and over(N=180)

COUNTRY OF RESIDENCE AGE

Source: BNP Paribas & Scorpio Partnership

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS14

INVESTOR PLATFORMSSHOULD SUPPORT INDEPENDENT ANALYSIS AND EXECUTION

Given the focus these investors place on hav-ing a customised advisor experience, it is little wonder that they expect technology to augment their engagement. They seek a closer relationship with their Wealth Man-agers that is geared towards discussing and

collaborating on new ideas. They also want access to products and trading instruments in order to act auton-omously upon their decisions, once made.

High-net worth individuals in Asia-Pacific already spend an average of 5.3 hours per week1 managing their wealth online. An integrated channel experience to support their activities is not only desirable, it is vital to the endur-ing advisor relationship: 83% of investors say they would leave their Wealth Manager if they were dissatisfied with their experience2. Expectations of what this platform needs to be are high.

FIGURE 5: IDEAL ONLINE PLATFORM – BANKING ADVISORY SERVICESQ: Which of the following banking / advisory services would you consider to be essential to offer as part of your online platform at

your ideal financial advisor institution?

Source: BNP Paribas & Scorpio Partnership

Hong Kong (N=134)

Indonesia (N=126) Taiwan (N=127)

Singapore (N=125)

Malaysia (N=127)

Japan (N=129) Australia (N=124)

China (N=128)

PERC

ENTA

GE

OF R

ESPO

NDE

NTS

0%

10%

20%

30%

40%

50%

60%

70%

Accountstatements

Ability to transfer money

between my accounts

Ability to make

payments

A dashboard that details

all the accounts I hold with the �rm

Interactive wealth

planning tools

Ability to apply for

credit

Trading and brokerage

tools

‘Chat’ functionality

with my relationship

manager

Access to client chat

forums

Portfolio performance

analysis

Financial research

1 Scorpio Partnership report: Future Advisor Asia – Embracing digital: a high stakes revolution in high net worth client management2 Global HNWI Insights Survey, Capgemini, RBC Wealth Management, and Scorpio Partnership (2014)

Asked to imagine their dream online portal, individuals first and foremost identify everyday features as essential: access to account statements and transfer capabilities are the most critical components across Asia, being core to any online banking proposition.

But importantly their ideal advisory platform would also incorporate self-directed tools [Figure 5], permitting their own investment execution.

Investors strongly desire a clearer line of sight into port-folio performance. More advanced analytical functional-ity holds strong appeal, particularly in relation to under-standing the overall investment position. A large minority – 40% of the overall sample – believe performance analy-sis is a vital tool. This drive for an independent evaluation is strongest in Singapore (54%) and Taiwan (49%), where such features are often viewed as standard elements of

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS15

FIGURE 6: MOST IMPORTANT ACCOUNT FEATURESQ: Which three of these are your preferred sections of content that you would like to see on your home screen at your ideal financial

advisor?

Source: BNP Paribas & Scorpio Partnership

Fee Summary

Risk exposure

Portfolio Overview

Personal Goals and Ambitions Socially Responsible Investments

PERC

ENTA

GE

OF R

ESPO

NDE

NTS

0%

10%

20%

30%

40%

50%

60%

70%

80%

Australia(N=124)

Totalsample

(N=1020)

China(N=128)

Hong Kong(N=134)

Indonesia(N=126)

Japan(N=129)

Malaysia(N=127)

Singapore(N=125)

Taiwan(N=127)

USD1m toUSD3m

(N=271)

USD3m toUSD5m(N=94)

USD5m toUSD10m(N=238)

USD10mand over(N=417)

COUNTRY OF RESIDENCE FINANCIAL ASSETS

an online wealth platform.

Sizeable minorities (over 40%) in Singapore, Malaysia, Indonesia and Australia believe the option to conduct fi-nancial research must also be offered by their advisors. A similar trend is observable in the same geographies to-wards interactive wealth planning, trading and brokerage tools, where about 40% wishes for autonomous execution.

These demands for self-direction also reflect an am-bition to be better informed in advisory meetings. For Asia’s wealthy, a fundamental function of an online plat-form is access to information outside of contact points, with several core segments admit they need reminders of their own investment strategy. Forty percent say they want a summary of their personal goals and ambitions to be made available, and this increases to nearly two thirds of HNWIs in China.

Wealthy clients are also clear on what account features they want to see in the ideal scenario. There is strong de-mand (from 62% of the overall sample) for a holistic over-view of portfolios, for instance [Figure 6]. HNWIs would gain clarity of their own market position if this informa-tion were easily at hand, on a platform they frequently used. Middle net worth (USD$1–3 million) individuals

appear to want this knowledge most of all, with 70% se-lecting this option.

The data reflects the beginning of a shift in investor per-ceptions: in several APAC markets, the balance is tipping in favour of considering the self-directed approach to be obligatory, not optional. The implications for private banks are considerable, extending beyond platforms across to other aspects of engagement, such as investor resources, portfolio data and client marketing.

Ultra-high net worth respondents are most likely to feel having visibility here is crucial (48%), strengthening the power of the message to the Wealth industry.

Viewed holistically the demands of Asia’s investors are loud and clear: Wealth Managers must give HNWIs the means to understand and respond to the dynamics of their portfolio independently of their advisors. Online portals should be refashioned as investor hubs, with ana-lytical tools, market data and investment information all readily available. Personal objectives should be captured on a cloud-based platform. Execution capabilities must also be offered.

Only through access to a range of self-directing capabili-ties will clients feel adequately equipped to execute their chosen ideas.

What is the one major action your current primary provider can take?“Dynamic analysis and timely market data tables.” Female, 35, China

of investors say they would leave their Wealth Manager if they were dissatisfied with their channel experience.

83 percent

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS16

High-net worth individuals want to feel con-fident that they have the resources to un-derstand past performance. But the ideal advisory relationship would be strongly fu-ture-focussed, with both partners working together to define the optimal strategy.

Currently however Asia’s wealthy lack visibility of im-portant investor resources outside of meetings. Contact time is often used to discuss this information, rather than focusing on the bigger strategic questions and looking to the future. More frequent touch-points with advisors would allow both sides to use their time together more productively.

Many clients are switching to non-traditional channels in an effort to improve the exchange of information [Fig-ure 7]. Over two thirds of investors in Malaysia and Sin-gapore regularly communicate with their private bankers via SMS; a majority in Taiwan and three quarters in China opt for social networking. WhatsApp is now more often used than not to engage with advisors in Singapore, Indo-nesia and Malaysia.

In half of the APAC markets surveyed, HNWIs are at-tempting to increase the overall level and frequency of interaction outside of formal review points. Traditional engagement (such as face-to-face meetings, letters and emails, etc.) still dominates, but investors are also ac-tively opening up new lines of communication with their Wealth Managers. In doing so, they favour channels that are more likely to secure a rapid response to their ques-tions.

This shift in communication preferences reflects a latent need for frequent investor updates from financial advi-sors. Asian consumers are used to accessing any infor-mation they want at the touch of a Smart device. They expect to interact with investment data in the same way, picking and choosing strands of relevant insight instantly and on-the-go.

NEW CHANNELS SHOULD BEHARNESSED TO ACCELERATE THE PACE OF INFORMATION EXCHANGE

is now more often used than not to engage with advisors in Singapore, Indonesia and Malaysia.

WhatsApp messaging

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS17

FIGURE 7: CURRENT WEALTH MANAGER COMMUNICATION CHANNELSQ: Thinking about your primary contact point at your Wealth Manager, how do you currently interact and communicate with him /

her?

Source: BNP Paribas & Scorpio Partnership

Malaysia (N=127)

Hong Kong (N=134) China (N=128)

Taiwan (N=127) Singapore (N=125)

Australia (N=124)

Indonesia (N=126) Total sample (N=1020)

Japan (N=129)

PERC

ENTA

GE

OF R

ESPO

NDE

NTS

IN

DICA

TIN

G C

HAN

NEL

AS

A CO

NTA

CT M

ETH

OD

0%

20%

40%

60%

80%

100%

Telephonecalls

Meetingface-to-face

SMS/textmessages

Socialnetworking

Mobile chatapplications

(such asWhatsapp)

Video calls(such asSkype)

Chatfunctionalityon a secureweb portal

Email Writtencommunica-

tions(I.e. letters)

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS18

Unsurprisingly, clients worry that any communication de-lays with advisors will negatively impact their portfolios. And while real-time market updates may be desirable in everyday interactions, they become absolutely critical when an extraordinary event occurs. Without them, many do not feel they can be nimble and respond effectively when the tide turns in order to re-balance in time.

Concerned at the current pace of information exchange, 87% state they would want some kind of communication from their advisors after the occurrence of a market event [Figure 8]. Nearly half of respondents would prefer imme-diate contact, regardless of the impact on their portfolio.

Anxiety about being left out of the loop is highest in Indo-nesia (68%) and Malaysia (57%); in Japan, Australia and Hong Kong, investors tend to expect advisor contact only if action is needed. The ultra-wealthy are the most likely of all to seek an immediate explanation from their private banks, irrespective of whether changes are required.

In a fast-moving market environment, real-time updates are the best way to support Asia’s investors with moni-toring and re-balancing in time. But in order for clients to feel confident that they have the full picture from the outset, changes must be made to communication across the private banking experience, with more frequent con-tact and better information-sharing priority areas. Only then will the partnership model that clients envisage – collaborative, customised and future-focussed – become possible.

of investors want their advisors to communicate with them after a market event.

87 percent

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS19

FIGURE 8: PREFERRED ADVISOR RESPONSE, AFTER A MARKET EVENTQ: Imagine that a market event happens which you believe will have a material im-

pact on the value of your investments. How would you like your primary personal advisor to react?

TOTAL SAMPLE (N=1020)

NUMBER OF RESPONDENTS

I prefer my primary personal advisor to contact me immediately regardless its impact on my investments

I prefer my primary personal advisor to contact me only if there is action to be taken on my investments

I am confident in the longer term plan of my investments and am happy to not be contacted by my primary personal advisor

I want an email/ SMS alert with an explanation of what is happening

I prefer to receive a call from a relevant market specialist - not my primary personal advisor

Source: BNP Paribas & Scorpio Partnership

COUNTRY OF RESIDENCE

FINANCIAL ASSETS

MALAYSIA (N=127)

INDONESIA (N=126)

TAIWAN (N=127)

HONG KONG (N=134)

SINGAPORE (N=125)

JAPAN (N=129)

AUSTRALIA (N=124)

CHINA (N=128)

USD3M to USD5M (N=94)

USD5M to USD10M (N=238)

USD1M to USD3M (N=271)

USD10M and OVER (N=417)

47% 40% 8% 4% 1%

39% 35% 13% 12% 1%

47% 39% 6% 7% 1%

53% 38% 5% 2% 1%

49% 38% 7% 5% 1%

37% 46% 10% 5% 1%

68% 23% 2% 6% 1%

38% 39% 12% 8% 4%

57% 33% 5% 5% 0%

54% 38% 6% 2% 1%

50% 31% 12% 6% 0%

54% 42% 2% 2% 0%

32% 55% 6% 4% 2%

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS20

CONCLUSION

Our research indicates a shift in investor atti-tude is on the horizon, as individuals across Asia-Pacific enhance their delivery expecta-tions. The new generation of private banking clients isn’t defined solely by one character-istic; it transcends demographic divides and

is distinguished by a common mind-set.

The emergence of this new client should make Wealth Managers pause for thought. Their circumspection needn’t be pessimistic. Our conclusions indicate Empow-ered Investors are an exciting prospect: ambitious, en-gaged and committed to the idea of working collabora-tively with their advisors. But at its heart, the challenge Wealth Managers face is how to deliver value to these clients as they prefer to become increasingly self-direct-ed.

Our recommendation to this industry is to focus on deliv-ering the area of value that clients themselves identify: customisation across every stage of the cycle.

Empowered Investors are an exciting prospect: ambitious, engaged and committed to the idea of working collaboratively with their advisors.

Advisors will first need to invest the time to understand this individual: their goals, their ambitions, their prefer-ences. A more substantial financial commitment will then be needed to respond to their desires, including re-con-figuring investor data and analysis tools, the communi-cation of market updates and bespoke investment tools. Change will feel disconcerting at first, but over time more transparency and autonomy should mean a higher-value relationship, with contact points freed up for more stra-tegic, future-focussed conversations.

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS21

By empowering investors in these ways, clients will not only gain the understanding they desire of their portfolios right now, they will be able to take any next steps with greater confidence. The benefits are likely to be long-last-ing and felt on both sides.

Focus on delivering the area of value that clients themselves identify: customisation across every stage of the cycle.

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS22

METHODOLOGY

This research was designed by BNP Paribas and Scorpio Partnership. The participants were independently sourced mass affluent, high-net-worth and ultra-high-net worth investors living in eight Asian-Pacific markets: Australia, China, Hong Kong, Indonesia, Japan, Malaysia,

Singapore and Taiwan.

Our respondents had an average net worth of USD$8.5 million and more than a third were millennial investors under the age of 35. Ultra-high net worth investors (UH-NWIs) with more than USD$10million in investable as-sets were the best represented segment in the sample (40%), providing rich insight into the needs of Asia’s most valuable wealth management clients.

The methodology was a 15 minute online survey with 1,020 respondents. Below is an illustration of the sample breakdown.

506

514

124

128

134

126

129

127

125

127

371

469

180

271

94

238

417

TOTAL SAMPLE

NUMBER OF RESPONDENTS

GENDER

MALE

FEMALE

COUNTRY OF RESIDENCE

AGE

MALAYSIA

INDONESIA

TAIWAN

HONG KONG

SINGAPORE

JAPAN

AUSTRALIA

CHINA

35 - 49

UNDER 35

FINANCIAL ASSETS

USD3M to USD5M

USD5M to USD10M

USD1M to USD3M

50 AND OVER

USD10M and OVER

1020

THE NEW RULES OF ENGAGEMENT FOR ASIA-PACIFIC’S WEALTH MANAGERS23

Scorpio Partnership is a leading insight and strategy consultancy to the global wealth in-dustry.

The firm specialises in understanding the wealthy and the financial institutions they in-teract with. We have developed four transfor-

mational disciplines – SEEK, THINK, SHAPE and CREATE – each designed to enable business leaders to strategi-cally assess, plan and drive growth. These include mar-ket research initiatives, client engagement programmes, value proposition and brand assessments and strategic business intelligence initiatives.

Scorpio Partnership has conducted more than 450 global assignments across wealth for institutions in the banking, fund management, family offices, law, trusts, regulation, IT and technology, insurance and charity sectors. In the course of these assignments, the firm has interviewed over 60,000 private investors and advisors.

For more information go to www.scorpiopartnership.com

ABOUT USSCORPIO PARTNERSHIP

IMPORTANT NOTICE:

The information included in this document is confidential and is provided to you for information purposes only. BNP Paribas is not providing any financial consulting service or investment advice to you. You should obtain independent legal, financial and other professional advice and make your own decision as to whether or not you wish to enter into any of those transactions with any person. Any information set out in this document is for reference only and should not be relied upon by you in any circumstances. BNP Paribas shall not have any liability to you or any of your affiliates (whether in contract, in tort or otherwise whatsoever) for any loss, damage, cost or expense that you or any of your affiliates may have suffered or incurred arising out of any of those transactions.

The information in this document has been obtained from published or unpublished sources which Scorpio Partnership and BNP Paribas reasonably believe to be complete, reliable and accurate, neither Scorpio Partnership nor BNP Paribas do represent or warrant, whether expressly or implicitly, and accept any responsibility for, its exhaustiveness, reliability or accuracy; any opinion expressed in this document is subject to change without notice. Scorpio Partnership and BNP Paribas accept no liability whatsoever for any consequences that may arise from the use of information, opinions or projections contained herein. This document does not constitute a prospectus or other offering document or an offer or solicitation to buy any securities or other investment. Information and opinions contained in this document are published for the assistance of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient; they are subject to change without notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein. Any reference to past performance should not be taken as an indication of future performance. No BNP Paribas Group Company accepts any liability whatsoever for any direct or consequential loss arising from any use of material contained in this document. All estimates and opinions included in this document constitute our judgments as of the date of this document.

This document is prepared by Scorpio Partnership in cooperation with BNP Paribas Hong Kong Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas Hong Kong Branch is registered as a Licensed Bank under the Banking Ordinance and regulated by the Hong Kong Monetary Authority. BNP Paribas Hong Kong Branch is also a Registered Institution regulated by the Securities and Futures Commission for the conduct of Regulated Activity Types 1, 4 and 6 under the Securities and Futures Ordinance. This document may not be circulated, distributed, reproduced or disclosed (in whole or in part and in any manner whatsoever) to any other person without the prior written consent of BNP Paribas Hong Kong Branch.

© BNP Paribas 2017. All rights reserved.