the enterprise zone skill build basic business accounting jim mould teaching fellow sheffield...

TRANSCRIPT

THE ENTERPRISE ZONESKILL BUILD

BASIC BUSINESS ACCOUNTING

JIM MOULDTEACHING FELLOW

SHEFFIELD UNIVERSITY MANAGEMENT SCHOOLMARCH 2010

QUESTIONS

• IS MY BUSINESS MAKING A PROFIT?• WHY IS THE CASH RUNNING OUT?• WHAT IS MY BUSINESS WORTH?• WHAT DID THAT LAST ORDER COST

ME?• HOW SHOULD I PRICE MY

PRODUCTS/SERVICES?• ARE THINGS GOING ACCORDING TO

PLAN?

ANSWERS

• BASIC BUSINESS ACCOUNTING

• IN THE FORM OF :-

FINANCIAL ACCOUNTING

MANAGEMENT ACCOUNTING

FINANCIAL ACCOUNTING

• FOR EXTERNAL USE – ANNUALLY

- FOR TAX CALCULATIONS (whatever

the type of business organisation)

- TO COMPLY WITH COMPANIES ACT

REQUIREMENTS (companies only)

• FOR INTERNAL USE BY THE MANAGEMENT OF THE BUSINESS – SAY, MONTHLY.

MANAGEMENT ACCOUNTING

• FOR INTERNAL USE BY THE MANAGEMENT ONLY

• AS FREQUENTLY AS YOU WISH

• FOR ALL OR JUST PART OF THE BUSINESS

• IN THE FORM YOU NEED IT, FOR THE DECISIONS YOU NEED TO MAKE.

FINANCIAL ACCOUNTING

• KEEPING ACCOUNTING RECORDS IN ACCORDANCE WITH AN ACCOUNTING SYSTEM

• RECORDS OF “PRIME ENTRY”

• ACCOUNTS KEPT IN THE LEDGERS

• PRODUCING “THE FINAL ACCOUNTS”

RECORDS OF PRIME ENTRY• SALES DAY BOOK - Daily list of sales invoices issued to customers• PURCHASES/EXPENSES DAY BOOK - Daily list of invoices received from suppliers and other bills received• CASH BOOK - Daily record of receipts and payments• JOURNAL - to make adjustments as required

THESE RECORDS OF PRIME ENTRY WILL BE “POSTED” TO THE ACCOUNTS IN THE LEDGERS AT, SAY, THE END OF THE MONTH IF MONTHLY FINANCIAL ACCOUNTS ARE REQUIRED

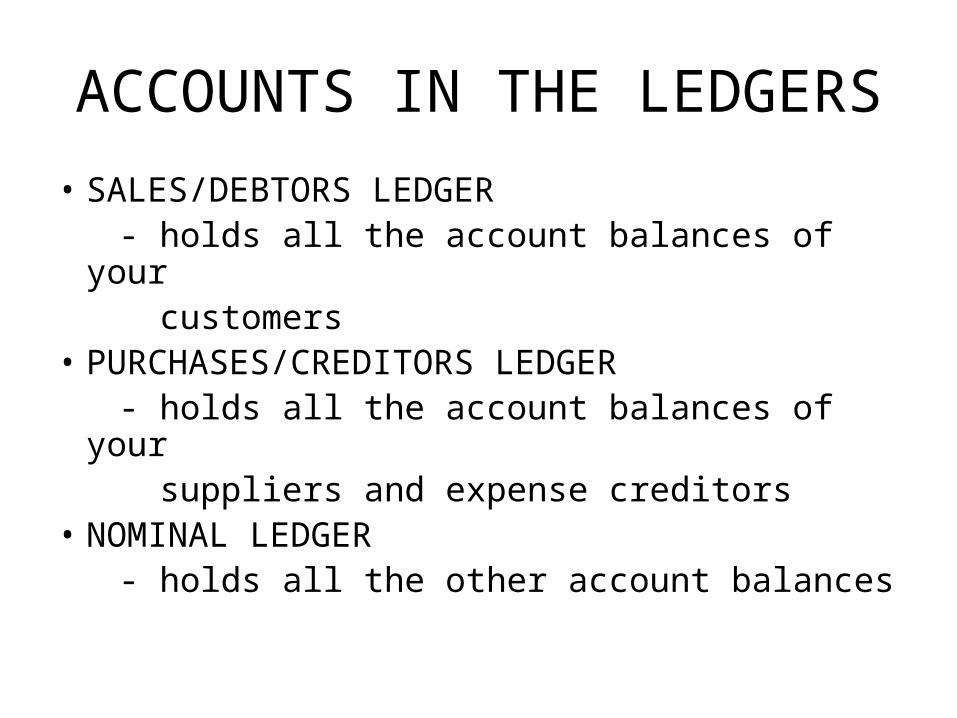

ACCOUNTS IN THE LEDGERS

• SALES/DEBTORS LEDGER - holds all the account balances of your customers• PURCHASES/CREDITORS LEDGER - holds all the account balances of your suppliers and expense creditors• NOMINAL LEDGER - holds all the other account balances

ACCOUNTS IN THE LEDGERS

• KEPT ON THE “DOUBLE ENTRY “ BOOKKEEPING SYSTEM

• BASED ON THE PRINCIPLE THAT EVERY BUSINESS TRANSACTION HAS TWO EFFECTS ON THE ACCOUNTS

i.e.

“for every debit there’s a credit”

“DEBITS AND CREDITS”

• DEBIT BALANCES CREDIT BALANCES for for

Cash In Cash out Cost of Sales Sales Expenses Other Income Assets Liabilities Drawings Capital Introduced

FINANCIAL ACCOUNTING

• FINANCIAL ACCOUNTS ARE KEPT ON AN “ACCRUALS” BASIS

- i.e.

“Sales” achieved in the period, whether

paid for of still owing

“Expenses” incurred in a period, whether

paid for or still owing

FINANCIAL ACCOUNTING

• AT THE MONTH END THE BALANCE ON EACH ACCOUNT IN THE LEDGERS WILL BE CALCULATED.

• THESE BALANCES WILL BE SUMMARISED ON A “TRIAL BALANCE” PRIOR TO THE PRODUCTION OF THE “FINAL ACCOUNTS”

THE “FINAL ACCOUNTS”

• Consist of :-

• THE TRADING AND PROFIT & LOSS ACCOUNT

THE BALANCE SHEET

THE CASHFLOW STATEMENT

THE TRADING AND PROFIT & LOSS ACCOUNT

• SALES less COST of SALES = GROSS PROFIT

• GROSS PROFIT plus OTHER INCOME less EXPENSES = NET PROFIT

THE BALANCE SHEET

• Consists of :-

“ THE ACCOUNTING EQUATION”

i.e.

ASSETS = CAPITAL + LIABILITIES

Or ASSETS – LIABILITIES = CAPITAL

What the Business Owns (its Assets) less what is owed to third parties (its liabilities) belongs to the Owner of the Business (the Capital)

THE ASSETS

• FIXED ASSETS - Land and Buildings - Plant and Machinery - Office Equipment - Vehicles

• CURRENT ASSETS - Stock - Debtors - Cash

THE LIABILITIES

• NON-CURRENT LIABILITIES

- LOANS

• CURRENT LIABILITIES

- Trade Creditors

- Expense Creditors

- Bank Overdraft

THE CAPITAL ACCOUNT

• CAPITAL INTRODUCEDAdd(less)• NET PROFIT(LOSS) for the Yearless• DRAWINGS (withdrawals of capital during

the year)=• CAPITAL BALANCE AT THE YEAR END

THE CASHFLOW STATEMENT

• SUMMARISES THE CASH INFLOWS AND CASH OUTFLOWS DURING THE YEAR TO EXPLAIN THE CHANGE IN THE CASH BALANCE

• THIS STATEMENT IS THEREFORE ON A “RECEIPTS AND PAYMENTS” BASIS

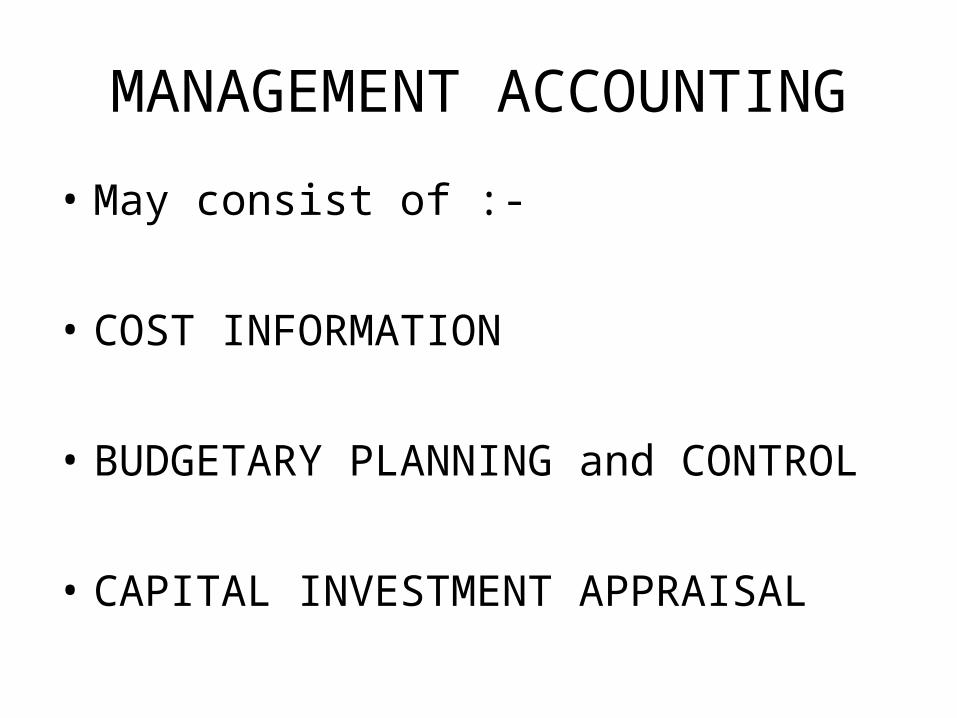

MANAGEMENT ACCOUNTING

• May consist of :-

• COST INFORMATION

• BUDGETARY PLANNING and CONTROL

• CAPITAL INVESTMENT APPRAISAL

EXAMPLES OF COST INFORMATION

• Identify which costs in your Business are :-

FIXED COSTS (they do NOT vary with changes in the level of activity)

and which are

VARIABLE COSTS (they DO change with the level of activity)

FIXED & VARIABLE COSTS

• SALES – VARIABLE COSTS = CONTRIBUTION

• TOTAL CONTRIBUTION – FIXED COSTS = NET PROFIT

• FIXED COSTS = SALES LEVEL Contribution per unit at BREAK-EVEN POINT of sales

BUDGETS

• PLAN - TARGET SALES - TARGET PROFIT ON SALES - PRODUCTION BUDGETS - STOCK REQUIREMENTS - MAJOR “CAPITAL EXPENDITURE” - CASHFLOW IMPLICATIONS/FUNDING REQUIREMENTS - RESULTS IN A BUDGET SET OF “FINAL ACCOUNTS”

BUDGETS

• CONTROL

BY COMPARING ACTUAL RESULTS TO THE BUDGET AND TAKING ACTION TO GET BACK ON BUDGET (or beat it if possible)

CAPITAL EXPENDITURE APPRAISAL

• How can we fund the Project?• When will we get our money back? (payback period)• What value do we get back for investing our funds in it? (Return on Investment)• Have we put the business at risk with this project and/or

has it provided a great opportunity for the development of the business?

• ANSWERS TO THE ABOVE REQUIRE FINANCIAL and MANAGEMENT ACCOUNTING INFORMATION TO HELP IN MAKING THE DECISION TO PROCEED WITH THE PROJECT OR NOT.