the entrepreneurial development bank · source: banco de la ... working capital entrepreneurial...

TRANSCRIPT

THE ENTREPRENEURIAL DEVELOPMENT BANK

March 2013

COLOMBIA ECONOMIC OVERVIEW

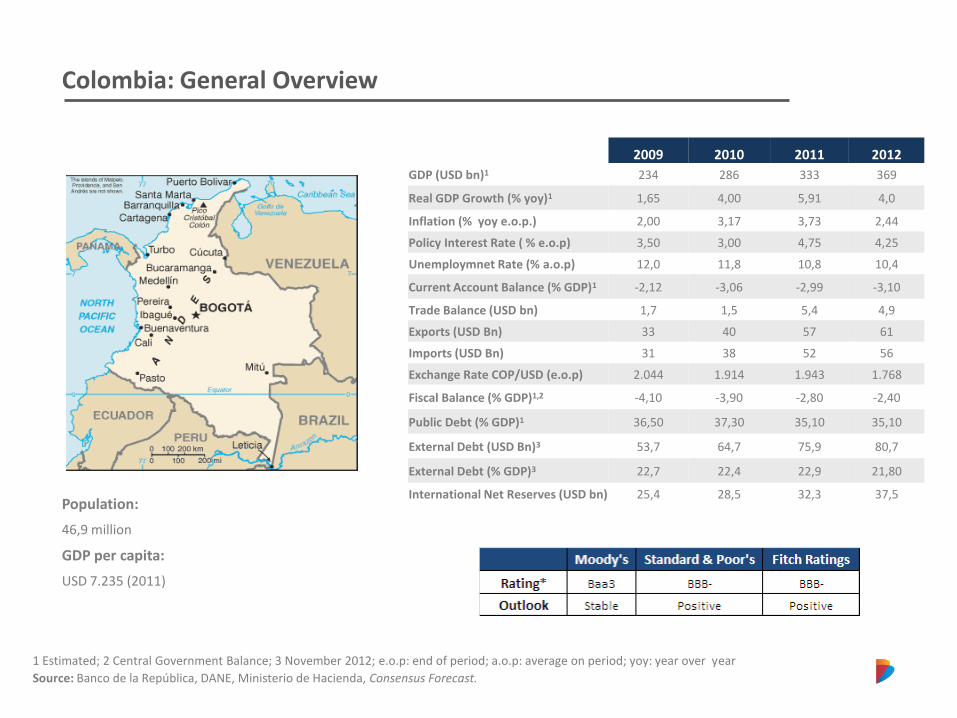

Colombia: General Overview

1 Estimated; 2 Central Government Balance; 3 November 2012; e.o.p: end of period; a.o.p: average on period; yoy: year over year

Source: Banco de la República, DANE, Ministerio de Hacienda, Consensus Forecast.

Population:

46,9 million

GDP per capita:

USD 7.235 (2011)

2009 2010 2011 2012

GDP (USD bn)1 234 286 333 369

Real GDP Growth (% yoy)1 1,65 4,00 5,91 4,0

Inflation (% yoy e.o.p.) 2,00 3,17 3,73 2,44

Policy Interest Rate ( % e.o.p) 3,50 3,00 4,75 4,25

Unemploymnet Rate (% a.o.p) 12,0 11,8 10,8 10,4

Current Account Balance (% GDP)1 -2,12 -3,06 -2,99 -3,10

Trade Balance (USD bn) 1,7 1,5 5,4 4,9

Exports (USD Bn) 33 40 57 61

Imports (USD Bn) 31 38 52 56

Exchange Rate COP/USD (e.o.p) 2.044 1.914 1.943 1.768

Fiscal Balance (% GDP)1,2 -4,10 -3,90 -2,80 -2,40

Public Debt (% GDP)1 36,50 37,30 35,10 35,10

External Debt (USD Bn)3 53,7 64,7 75,9 80,7

External Debt (% GDP)3 22,7 22,4 22,9 21,80

International Net Reserves (USD bn) 25,4 28,5 32,3 37,5

Colombian economy shows a positive trend

GDP (% yoy)

GDP per capita USD

3,9

5,3

4,7

6,7 6,9

3,5

1,7

4,0

5,9

4,3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012p

Average GDP growth rate 2003-2012: 4,2%

7235

0

1000

2000

3000

4000

5000

6000

7000

8000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

p

20

09

p

20

10

p

20

11

p

• Between 2000 – 2011 GPD per capita rose 158% (national currency COP)

• IMF estimated for 2012 GDP per capita in USD

7.842

Source: Banco de la República, DANE.

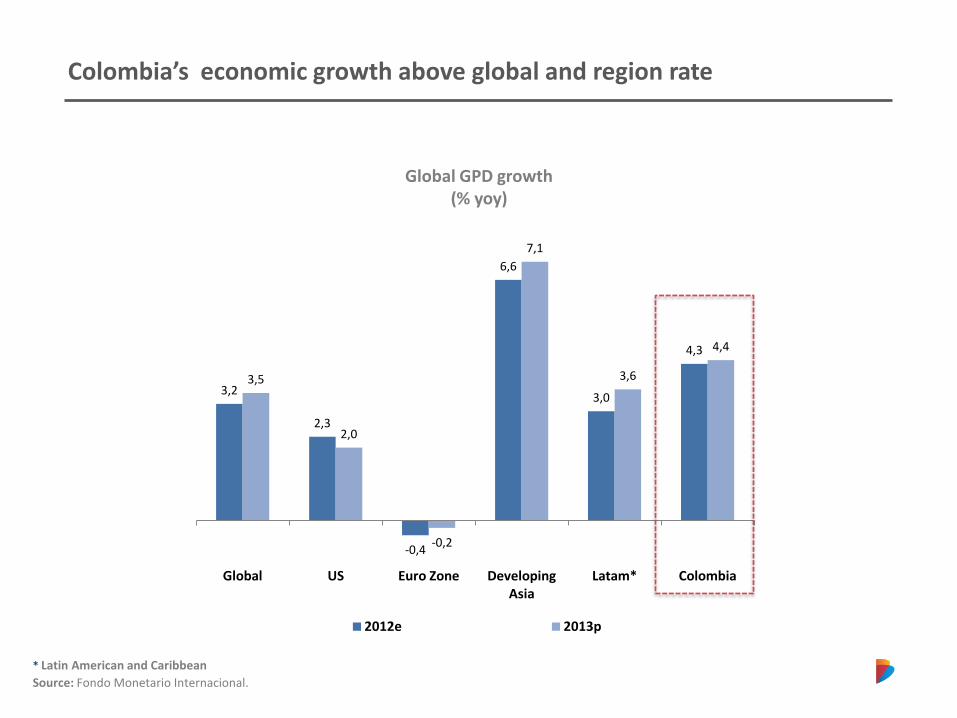

Colombia’s economic growth above global and region rate

Global GPD growth (% yoy)

* Latin American and Caribbean

Source: Fondo Monetario Internacional.

3,2

2,3

-0,4

6,6

3,0

4,3

3,5

2,0

-0,2

7,1

3,6

4,4

Global US Euro Zone Developing Asia

Latam* Colombia

2012e 2013p

GPD Demand Side (% yoy)

GDP Supply Side (% yoy)

Accumulated GDP growth from January - September

Source: DANE.

3,9%

10,1%

4,3%

5,7%

4,3%

4,5%

5,8%

21,5%

10,1%

16,7%

2,5%

6,6%

GDP

Imports

Exports

Investment

Goverment consumption

Household consumption

Jan - Sep 2011 Jan - Sep 2012

3,9%

5,5%

4,3%

4,2%

0,6%

0,0%

7,2%

2,1%

5,8%

5,6%

7,0%

6,2%

3,6%

4,3%

13,2%

3,4%

GDP

Financial Serv.

Transport

Retail

Construction

Manufacturing Ind.

Mining

Agricul/ farming

Jan - Sep 2011 Jan - Sep 2012

Exports is gaining momentum

Exports (USD million)

2012 Exports Evolution (% yoy)

Source: DANE.

61

6,6

40

10

3,4

57

7,1

38

10

2,8

Tota

l

Agr

icu

ltu

ral

Pro

du

cts

Fue

ls a

nd

m

inin

g

Man

ufa

ctu

res

Oth

er

2012 2011

4,8%

6,9%

-6,1%

5,7%

Manufactures

Fuels and mining

Agricultural products

Total

Source: DANE.

Colombian foreign trade By sector (% share) By country (% share)

Exp

ort

s Im

po

rts

Inflation (% end of period)

Reduction on inflation led an accommodative monetary policy

Central Bank Reference Rate (%)

Source: Banco de la República.

4,9 4,5

5,7

7,7

2,0

3,2 3,7

2,4

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

2005 2006 2007 2008 2009 2010 2011 2012

Inflation Lower band Target Upper band

3,75

2

4

6

8

10

12

feb

-06

feb

-07

feb

-08

feb

-09

feb

-10

feb

-11

feb

-12

feb

-13

Main figures financial intermediaries (USD Billion)

Financial system size

Profits financial intermediaries (USD Billion)

Source: Superfinanciera

140

120

19

177

152

25

206

176

30

Assets Liabilities Equity

Dec-10 Dec-11 Dec-12

2,0 2,1

2,6

3,1

3,7

4,1

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

Crisis did not affected significantly the banking system

Financial Intermediaries: banks, financial corporation and others

*Includes provisions

Source: Superfinanciera

Loan portfolio growth (% yoy)

Total loans* & performing loans growth (% yoy)

15%

12%

18%

-10%

0%

10%

20%

30%

40%

50%

60%

De

c-0

4

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

Total loan Commercial Consumption

15%

31%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Total Loan Non performing loans

Fiscal policy soundness continues in 2012

CPS: Combined Public Sector

NPS: Nonfinancial Public Sector Balance

CG: Central Government Balance

2012 estimated

Source: Ministerio de Hacienda

Fiscal Balance (% GDP)

-2,0

-0,1

-1,8

-1,2

-2,8

-2,4

-5,0

-4,5

-4,0

-3,5

-3,0

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012e

CPS NPS CG

Colombian public debt remains at the same levels in adverse international scenario

Public Debt* (% GDP)

External Debt (% GDP)

35,1

0

5

10

15

20

25

30

35

40

45

50

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

p

*Central Government Public Debt

Source: Banco de la República, Ministerio de Hacienda

12,2 9,4

22,9 21,7

0

5

10

15

20

25

30

35

40

45

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

No

v-1

2

Public Private Total

Favorable sovereign risk perception

Sovereign CDS 5 YR (USD)

CDS: Credit Default Swaps

*Foreign Currency Long Term

Source: Bloomberg

Sovereign Ratings*

295

108

98

97

96

91

72

394

162

154

172

156

222

132

Spain

Brazil

Mexico

Peru

Colombia

France

Chile

Dic-11 Dic-12

Country Moody's S&P

Fitch Ratings (selection)

Thailand Baa1 BBB+ BBB

Italy Baa2 BBB+ A-

South Africa Baa1 BBB BBB

Mexico Baa1 BBB BBB

Russia Baa1 BBB BBB

Brazil Baa2 BBB BBB

Panama Baa2 BBB BBB

Peru Baa2 BBB BBB

Bulgaria Baa2 BBB BBB-

Colombia Baa3 BBB- BBB-

Island Baa3 BBB- BBB-

Spain Baa3 BBB- BBB

India Baa3 BB+ BBB-

Indonesia Baa3 BB+ BBB-

In 2012 FDI flows reached a new record

Foreign Direct Investment Flows (USD Billions)

Source: Banco de la República

16,7

-

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2008 2009 2010 2011 2012

Alianza del Pacífico: Chile, Colombia, México y Perú

CAN: Bolivia, Ecuador y Perú

CARICOM: Comunidad del Caribe

EFTA: Islandia, Liechtenstein, Noruega y Suiza

North Triangle: El Salvador, Guatemala y Honduras

Mexico

CAN

North Triangle of Central America

Mercosur Chile

Canada

EFTA

US

Panama

Korea

Turkey

Israel

Costa Rica

EUROPEAN UNION

SIGNED IN NEGOCIATION

Source: Ministerio de Comercio, Industria y Turismo

Free Trade Agreements

Japan

IN FORCE

Alianza del Pacífico

Summary

•Colombian economy shows a sustained growth above global and region rate.

•Exports expanded in adverse international scenario.

•Inflation expectation is within Central Bank’s medium term target.

•The current interest rate levels will help to sustainable economic growth.

•Financial system is solid and financial institutions will remain with high levels of liquidity.

•Prudence in fiscal and monetary policy will continue.

•A better risk perception (investment grade) will lead to a local investment growth.

•The main downside risks to economic growth are lead by external conditions.

•For 2013 is expected a GDP rate growth above 4,0%.

ABOUT BANCÓLDEX

Ownership structure

Ownership structure As of December 2012

Bancoldex strategic allies

Bancóldex is supervised by the Colombian Financial Superintendence

www.superfinanciera.gov.co

Ministry of Trade,

Industry and Tourism 91.9%

Ministry of Finance 7.9% Others 0.2%

49.63%

30.21%

86.55% 89.17%

ORGANIZATIONAL STRUCTURE

Organization chart

STRATEGIC FRAMEWORK 2010-2014

Evolución de Bancóldex

2007 2012 2010 2009 2008 2006 2005 2003 1992-2002

Banco de comercio exterior

IFI´s Assets and Libabilities adquisition

• Broad attention to domestic market • Focusing on SME • Beginning of the territorial agreement

schemes

“aProgresar” Program

Banca de las Oportunidades Program

Contraciclic Program Economic slowdown

Private Equity Funds

Microinsurance Futurex Program

National Development Plan 2010-2014 Special Programs

Emergency Plan

Revaluation

Entrepreneurial training program

Focusing on foreign trade products and

services

Mission- Vision

Mission

As a development bank, we drive the Colombian entrepreneurial sector

productivity through innovation, modernization and internationalization, with

financial sustainability and commitment of our human capital, within the

framework of social responsibility.

Vision

In 2014, to become the leading Bank implementing entrepreneurial

development instruments to promote productivity of Colombian enterprises.

Bancóldex, an entrepreneurial ally

Entrepreneurial Modernization Financing

Entrepreneurial Innovation Support

MORE COMPETITIVE AND PRODUCTIVE COMPANIES

LEADS TO JOB CREATION

Growth National Market International Markets

Bancóldex offers instruments for all entrepreneurial development stages

BANCÓLDEX AS A SECOND TIER BANK

Second tier bank

Second tier loans Direct loans

Rediscount Application

Rediscount credit Direct credit

Credit Application

Company- entrepreneur Financial Insititution

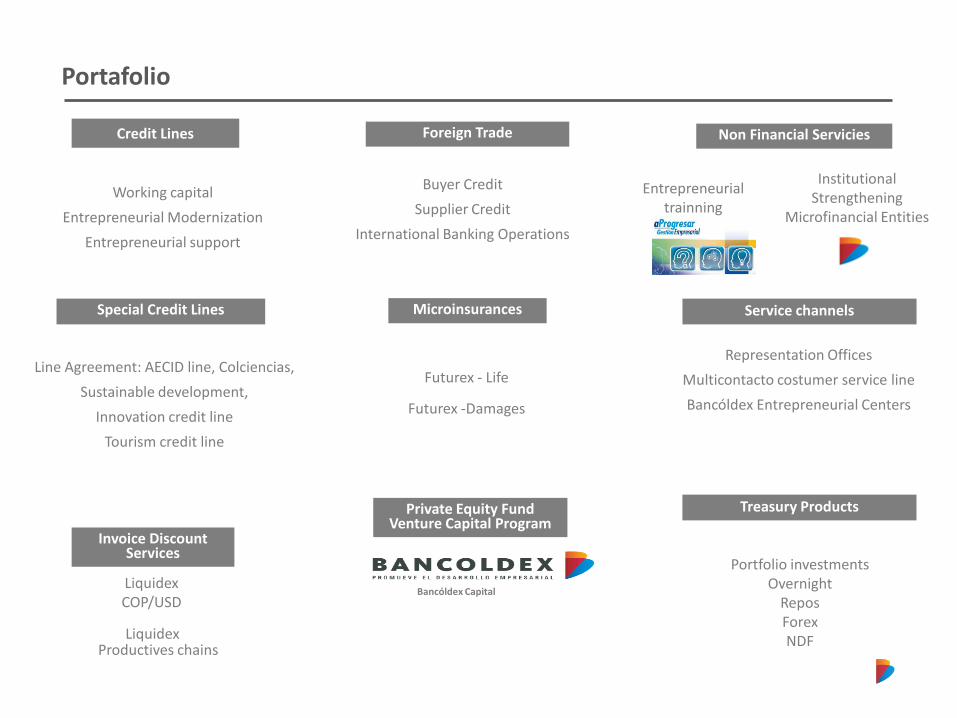

Portafolio

Entrepreneurial trainning

Line Agreement: AECID line, Colciencias,

Sustainable development,

Innovation credit line

Tourism credit line

Buyer Credit

Supplier Credit

International Banking Operations

Working capital

Entrepreneurial Modernization

Entrepreneurial support

Credit Lines

Liquidex Productives chains

Special Credit Lines Service channels

Institutional Strengthening

Microfinancial Entities

Non Financial Servicies

Microinsurances

Private Equity Fund Venture Capital Program

Foreign Trade

Liquidex COP/USD

Representation Offices

Multicontacto costumer service line

Bancóldex Entrepreneurial Centers

Invoice Discount Services

Treasury Products

Portfolio investments Overnight

Repos Forex NDF

Futurex - Life

Futurex -Damages

Bancóldex Capital

Bancóldex services and programs

BUSINESS PLAN

UNDER EXPANSION

VENTURE CAPITAL

“START UP”

MATURITY PRIVATE EQUITY

CONSOLIDATION

STOCK MARKET

SEED CAPITAL

ANGELS

Entrepreneurial development stages

Tip

e o

f Fi

nan

cin

g (

sou

rce

s)

SME and Large Companies financing

Entrepreneurial modernization Working capital Sustainable development- green lines

International Banking Operations Supplier credit, buyer credit and correspondent banking

Invoice Discount Liquidex Foreign Trade

Micro - financing

Entrepreneurial training

Microinsurances

Private Equity Fund Program

Bancóldex special programs

• Futurex Microinsurance Program

• “aProgresar” Training Program

• Bancoldex Capital Program

• “Banca de las Oportunidades” Program

• Development &Innovation Unit

• Productive Transformation Program

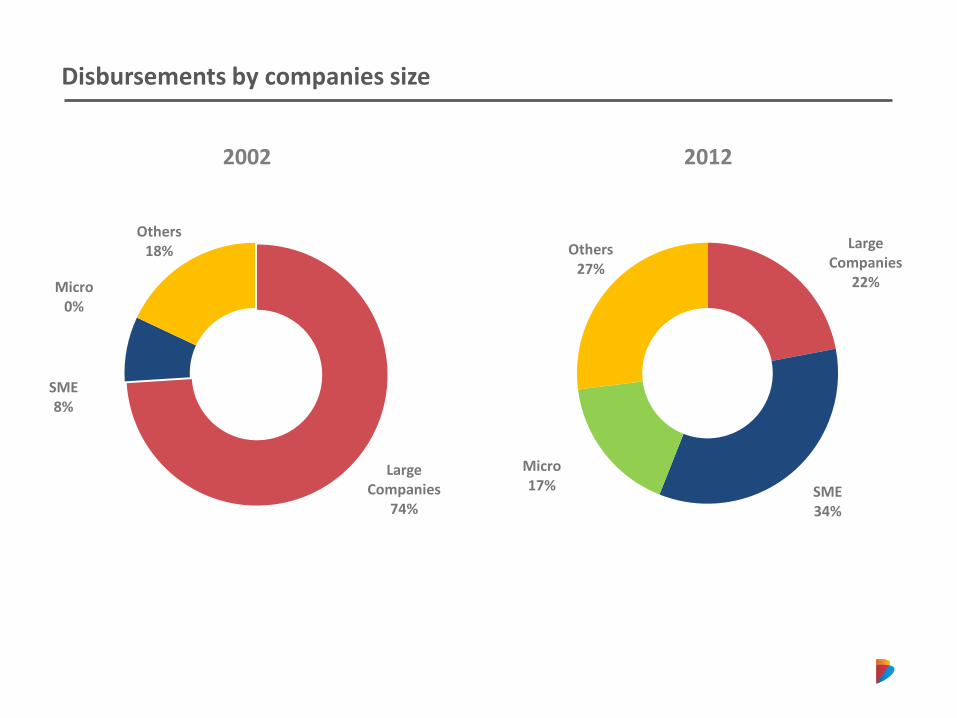

Disbursements by companies size

2002

Large Companies

74%

SME 8%

Micro 0%

Others 18% Large

Companies 22%

SME 34%

Micro 17%

Others 27%

2012

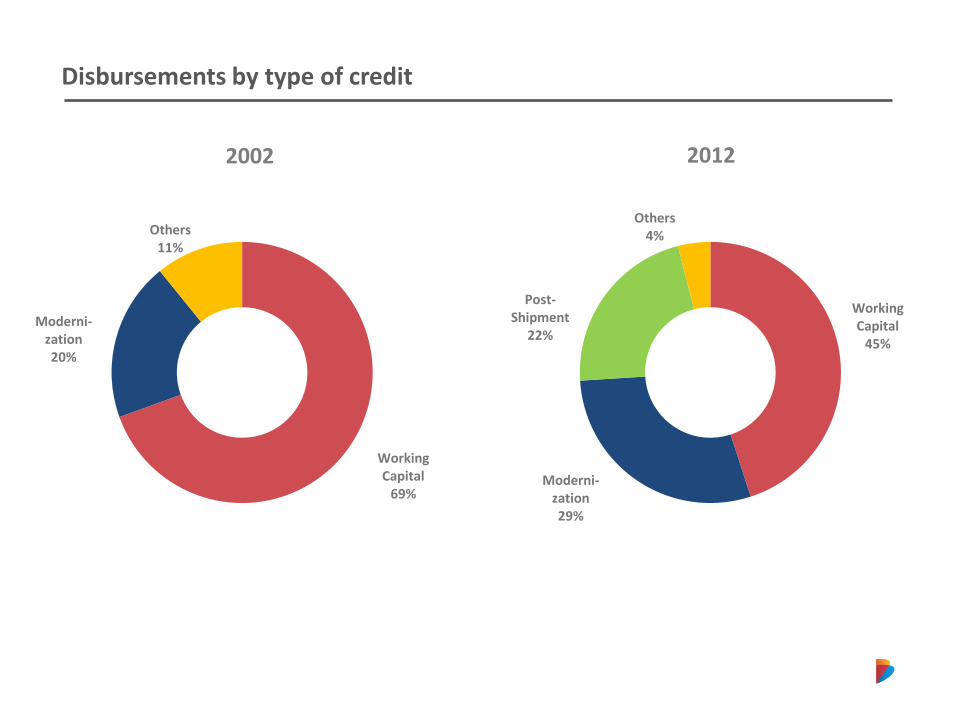

Disbursements by type of credit

Working Capital

69%

Moderni-zation 20%

Others 11%

Working Capital

45%

Moderni-zation 29%

Post- Shipment

22%

Others 4%

2002 2012

Disbursements by credit term

Short 57%

Medium 26%

Long 17%

Short 47%

Medium 29%

Long 24%

2002 2012

Impact analysis of Bancoldex

•Impact evaluation carried out for Bancoldex by the IDB under the coordination of Mr. Fernando De Olloqui in Alliance with the economists Ms Marcela Eslava and Marcela Meléndez. The study covered the period between 2000 and 2009

Main Results : Impact analysis of Bancoldex credit activity on performance of enterprises, emphasizing the effect of credit lines modernization.

Production 24%

Employment 11%

Investment 70%

Productivity 10%

PRIVATE EQUITY AND VENTURE CAPITAL INDUSTRY PROGRAM

Actively investing in private equity and venture capital funds

Since 2009, 33 funds have been analyzed by Bancoldex. Five investment commitments (USD

46M) in multi sector funds, tourism, venture capital and infrastructure.

16

8

4

5

2009 2010 2011 2012

Funds under Preliminary Due Diligence (33)

4

8

3

2009 2010 2011 2012

Funds under Due Diligence (18)

Funds’ portfolio companies in diverse sectors

Outsourcing Services, Information Technology, Biotechnology, Clean Energy, Digital Animation, Tourism, Power generation , Logistics are some of the sectors backed by Bancoldex investments in funds

27 companies have been backed, 17 of

them are in Colombia

21% of the capital have been invested in

service companies

17 in Information technology and

telecommunications companies

There is a successful exit of a

biotechnology firm (agribusiness)

ITC; 75.303;

17%

Housing;

18.958; 4%

Retail; 39.975;

9%

Tourism;

15.510; 3%

Services;

96.522; 21% Oil&Gas

Services;

50.365; 11%

Energy; 22.317;

5%

Biotechnology;

3.684; 1%

Dining; 27.876;

6%

Health; 14.550;

3%

Port; 39.731;

9% Storage;

51.800; 11% Highway

Concession;

750; 0%

Fund investments by sector

Financial Structure

Financial structure

2.764 2.898

3.069

3.752

Dec-09 Dec-10 Dec-11 Dec-12

USD

Mill

ion

Assets COP 6.63 billion*

2.110 2.176 2.375

2.920

Dec-09 Dec-10 Dec-11 Dec-12

USD

Mill

ion

Liabilities COP 5.16 billion*

654 722 694

832

Dec-09 Dec-10 Dec-11 Dec-12

USD

Mill

ion

Equity COP 1.47 billion*

Dec 2012 exchange rate COP/USD: 1.768,23

Assets

Dec-09 Dec-10 Dec-11 Dec-12

Loans Investments* Others

* Investments Break-down: Securities, investments in private equity, equity investment (shares).

Break-down USD 3.752 million*

25%

69%

Dec-09 Dec-10 Dec-11 Dec-12

COP USD

USD 267 million abroad, which represents 38% of the total USD loan portfolio.

Loans

COP 74%

USD 26%

USD 702 mill

USD 2.012 mill

(COP 3.55 bill)

Dec 2012 exchange rate COP/USD: 1.768,23

Asset quality

0,186%

0,049%

0,018% 0,009%

Dec-09 Dec-10 Dec-11 Dec-12

Non Performing Loans Ratio

22

83

227

469

Dec-09 Dec-10 Dec-11 Dec-12

Non Performing Loans Coverage

Loan Portfolio Provision / Non performing loans

Liabilities

Dec-09 Dec-10 Dec-11 Dec-12

USD

Mill

ion

COP USD

Evolution

22%

78%

USD 2.920 million*

Dec-09 Dec-10 Dec-11 Dec-12

CDT's Bonds Repos Other Banks Others

USD

Mill

ion

Break-down

22%

21%

52%

Capital Ratio

22,52% 21,11%

0%

10%

20%

30%

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

Dec-09 Dec-10 Dec-11 Dec-12

USD

Mill

ion

Risk-weighted assets Capital Ratio

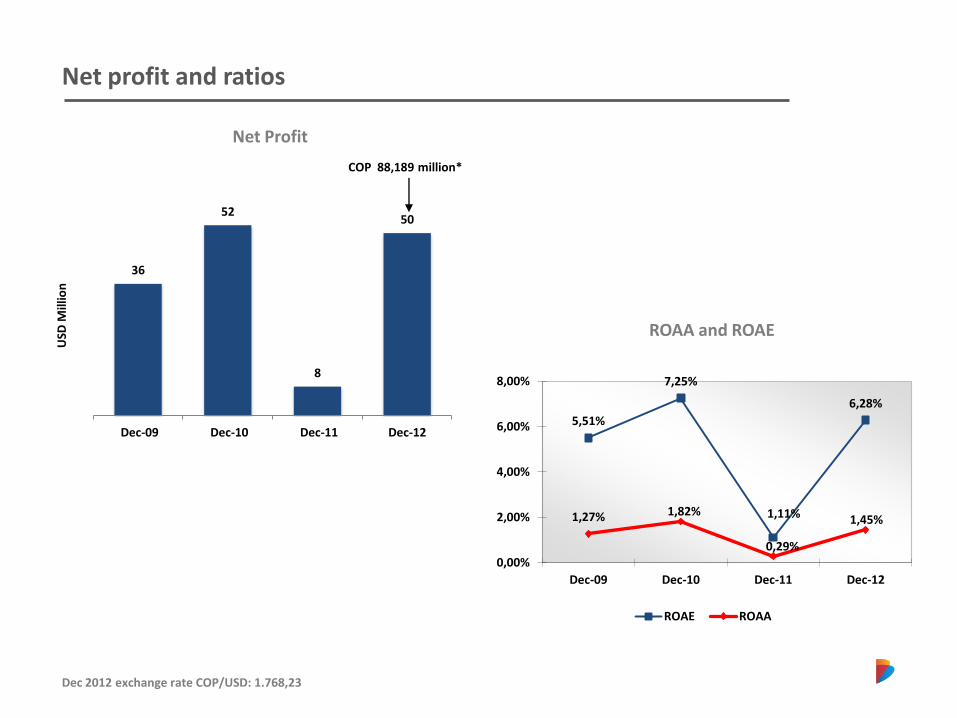

Net profit and ratios

36

52

8

50

Dec-09 Dec-10 Dec-11 Dec-12

USD

Mill

ion

Dec 2012 exchange rate COP/USD: 1.768,23

COP 88,189 million*

5,51%

7,25%

1,11%

6,28%

1,27% 1,82%

0,29%

1,45%

0,00%

2,00%

4,00%

6,00%

8,00%

Dec-09 Dec-10 Dec-11 Dec-12

ROAE ROAA

Net Profit

ROAA and ROAE

Credit Ratings Investment Grade

International

Debt instruments

Latest ratings 08/12 06/12 07/12

Long-term liabilities (Foreing currency) BBB-/Positive Short-term liabilities (COP) F 1+ BRC1+ Long-term liabilities (COP) AAA AAA

Local

* On Aug. 17, 2012, Standard & Poor's Ratings Services revised its long-term rating outlook on Bancoldex to positive from stable and affirmed its 'BBB-' ratings on the bank.

BANCÓLDEX AS A SPECIAL PROGRAMS MANAGER

Dynamic Innovative

Entrepreneurship

Matching grant fund for SMEs

Innovation

and

Entrepreneurship

in Large

Firms

Regional capacity building for

innovation and competitiveness

Mentality

and

Culture of

Innovation and

Entrepreneurship

Strategic work areas

The objective of the Modernization and Innovation Fund for Micro, Small and Medium

Enterprises is to strengthen this entrepreneurial segment. The Fund, operates through

open counter invitation based on the demand of non reimbursable confined resources,

namely permanent invitations up to the exhaustion of resources, shall focus such

resources for the development of projects oriented towards entrepreneurial

innovation, whether during the development of new products and/or services,

development of new processes, and in association schemes such as development of

suppliers, distributors or cross linking.

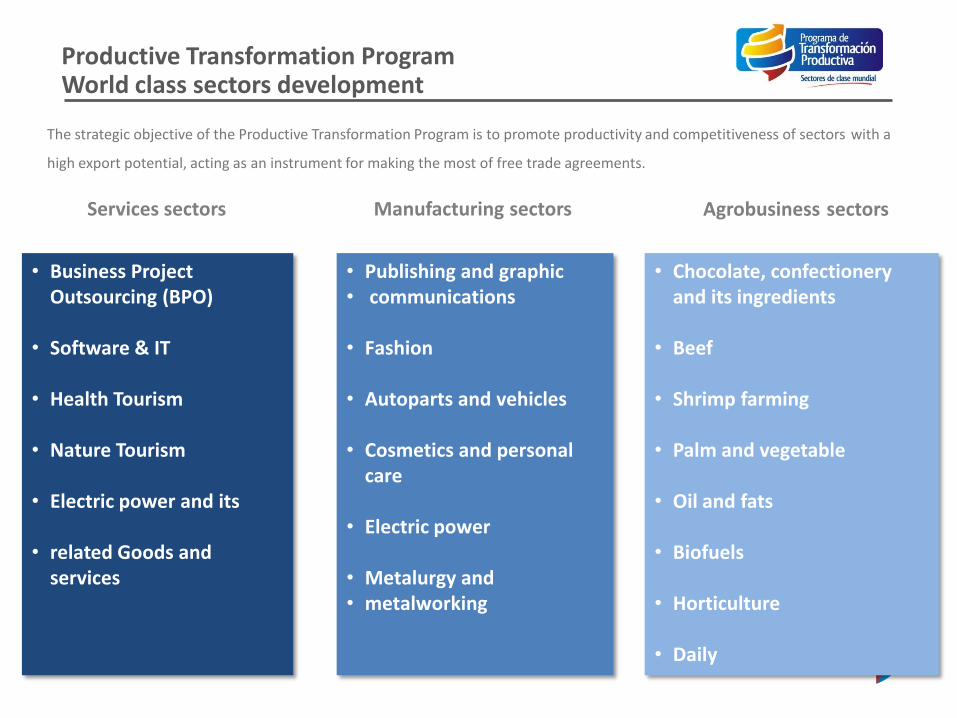

Productive Transformation Program World class sectors development

Services sectors Manufacturing sectors Agrobusiness sectors

• Business Project Outsourcing (BPO)

• Software & IT • Health Tourism • Nature Tourism • Electric power and its • related Goods and

services

• Publishing and graphic • communications • Fashion • Autoparts and vehicles • Cosmetics and personal

care

• Electric power • Metalurgy and • metalworking

• Chocolate, confectionery and its ingredients

• Beef • Shrimp farming • Palm and vegetable • Oil and fats

• Biofuels • Horticulture

• Daily

The strategic objective of the Productive Transformation Program is to promote productivity and competitiveness of sectors with a

high export potential, acting as an instrument for making the most of free trade agreements.

Mission – Banca de las Oportunidades

Encourage access to financial services to the unbanked colombian

population, specially to the low-income families, with the purpose of

enhancing the country s development and promote social equity.

Contact us

International Contacts

Fernando Esmeral

Chief Commercial Officer

(57-1) 486 30 00 ext. 2400

Alejandro Contreras

International Banking Director

(57-1) 486 30 00 ext. 2450

Alfonso Carreño

International Executive

(57-1) 486 30 00 ext. 2453

Treasury contacts

Beatriz Arbeláez

Chief Financial Officer

(57-1) 486 30 00 ext. 2701

Claudia González

Treasury Director

(57-1) 486 30 00 ext. 2471

Guillermo Puentes

Head of Trading Desk

(57-1) 486 30 00 ext. 2472

María Carvajal

Financial Markets Officer

(57-1) 486 30 00 ext. 2457

Maria. [email protected]

Miguel Angulo

Junior Financial Markets Officer

(57-1) 486 30 00 ext 2457

Operations contacts

Jorge García

Chief Operations Officer

(57-1) 486 30 00 ext 2500

Marcela González

Operations Director

(57-1) 486 30 00 ext 2550

Risk contact

Mauro Sartori

Risk Chief Officer

(57-1) 486 30 00 ext 2800

Contact us

Bogotá :

Calle 28 No 13A-15, floors 38 to 42

Phone: (57-1) 486 30 00

Fax: (57-1) 286 24 51 / (57-1)286 0237

Working Hours (monday to friday): from 8:00 a.m. to 5:00 p.m.

E-mail web master: [email protected]

www.bancoldex.com

_________________________________

SWIFT: BCEXCOBB

_________________________________

Contact us

Call Center Multicontacto Bancóldex

Bogotá: (57-1) 6 49 71 00