the euroindia summit fernando guedán pecker director of investment projects ferrovial servicios sa...

TRANSCRIPT

The EuroIndia Summit

Fernando Guedán PeckerDirector of Investment Projects Ferrovial Servicios SA

Valladolid, 5th of October of 2009

Financing Financing Urban development projectsUrban development projects

The EuroIndia Summit

Public vs PPP/PFI

Madrid Calle 30

Conclusions

2

Agenda

The EuroIndia Summit

Definitions- Public vs PPP/PFI

3

“PPP (Public Private Partnership) is basically just a different method of procuring public services and infrastructure by combining the best of the public and private sectors with an emphasis on value for money and delivering quality public services. .” Irish Government Public Private Partnership (PPP) website

South African law defines a PPP as a contract between a public sector institution/municipality and a private party, in which the private party assumes substantial financial, technical and operational risk in the design, financing, building and operation of a project.

“One of the key requirements for PFI schemes is that they offer the public sector value for money (VFM). The Government, and indeed the private sector, demand high quality services, delivered on time and to budget. Historically, major investment projects built purely under public finance have failed to keep within the initial schedule and funding constraints. PFI has proven to be substantially more cost-effective and reliable.”

The EuroIndia Summit

Public vs PPP/PFI

4

• Execution on time.

• Quality assurance in construction and operation

• Less risk of extra-cost and delays

• The Risk is transferred to the best managers

• Payment either by the final user or deferred Public payment

• No payments until the service beginning

Advantage PPP/PFI Advantages of Public Financing

• Economically Not Profitable but necessaries from the social point of view

• Country Strategic services

• Can assume level of risk unacceptable for private sector

• Urgent Projects

• Lower Financial cost

Services economically unacceptable, Strategic or

Urgent

Greater security in PRICE and QUALITY

The EuroIndia Summit 5

There wont be considered as Public Debt when the PPP Mixed economy

company:

Assume the majority of the Investment / Construction risk

Assume the majority of the Service risk, the Operating risk or both

o Service Risk: automatic penalties that affect significantly the private rent ability as result of the service level provided

o Operating Risk: Significant decrease in private rent ability because the low level of infrastructure use although the cause of that doesn't depend of private management

Eurostat: According with the Public Accounting criteria, the major factor to classify an active and its debt as public or private is the level of risk transference of the project

Public vs PPP/PFI

The EuroIndia Summit 66

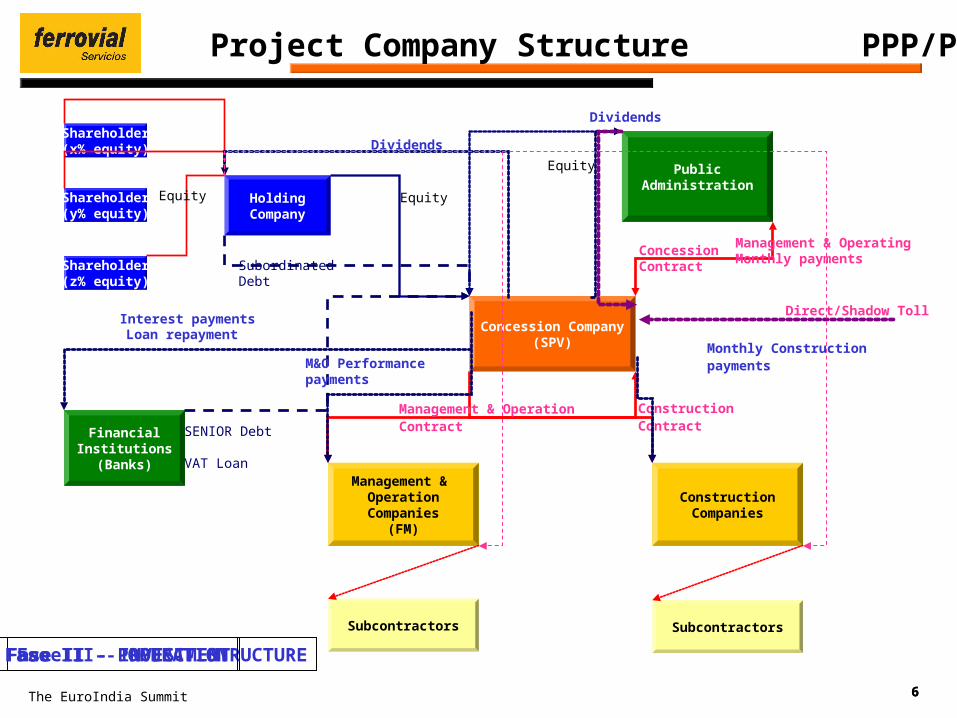

Project Company Structure PPP/PFI

Shareholder(x% equity)

Shareholder(y% equity)

Shareholder(z% equity)

HoldingCompany

PublicAdministration

Concession Company(SPV)

FinancialInstitutions

(Banks)

ConstructionCompanies

Subcontractors

Management & Operation

Companies(FM)

Subcontractors

Equity

SubordinatedDebt

Equity

ConcessionContract

SENIOR Debt

VAT Loan

Construction Contract

Monthly ConstructionpaymentsM&O Performance

payments

Interest payments

Dividends

Dividends

Management & OperationContract

Management & OperatingMonthly payments

Direct/Shadow Toll

Equity

Loan repayment

Fase II - INVESTMENTFase I – PROJECT STRUCTUREFase III - OPERATION

The EuroIndia Summit

-80,0

-60,0

-40,0

-20,0

0,0

20,0

40,0

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

Milo

nes

€

Ingresos Inversión

Financieros Operacionales

77

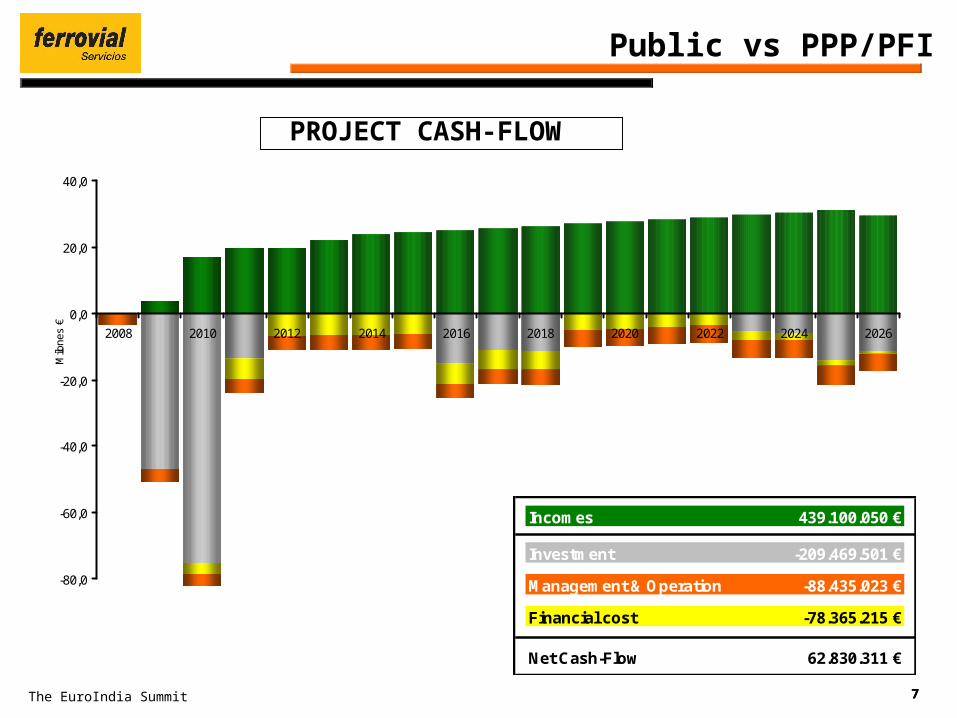

Public vs PPP/PFI

PROJECT CASH-FLOW

Incomes 439.100.050 €

Investment -209.469.501 €

Management & Operation -88.435.023 €

Financial cost -78.365.215 €

Net Cash-Flow 62.830.311 €

The EuroIndia Summit 88

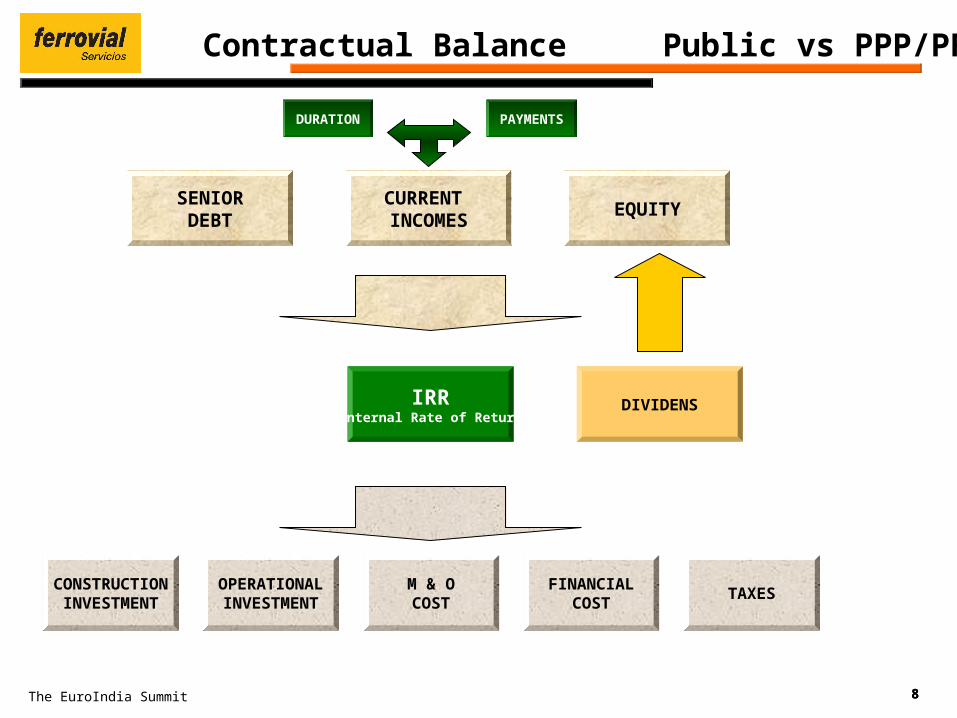

Contractual Balance Public vs PPP/PFI

CONSTRUCTIONINVESTMENT

CURRENT INCOMES

M & OCOST

OPERATIONALINVESTMENT

SENIORDEBT

EQUITY

PAYMENTSDURATION

FINANCIALCOST

DIVIDENSIRRInternal Rate of Return

TAXES

The EuroIndia Summit

Public vs PPP/PFI

Water

Energy

Roads

Public Transport

Hospitals

Education

Prisons

ConferenceCentres

Justice

PoliceStation

Sport and leisure

Traditional Sectors New Sectors

INVESTMENT + -PUBLIC SERVICE +-

The EuroIndia Summit

PPP in Penitentiary Centres

Construction

RoutineMaintenance

ExtraordinaryMaintenance

Laundry &Cleaning

Catering

Sanitary Assistance

Education andRehabilitation

Techno - Surveillance

Penitentiary ServicesPen

iten

tiar

y C

entr

es –

Lev

el o

f S

ervi

ces

un

der

co

nce

ssio

n

Sp

ain

Ch

ile

UK

, Sh

ou

t A

fric

a &

Au

stra

lia

INV

ES

TM

EN

T+

-

-

+

PU

BLI

C S

ER

VIC

E

The EuroIndia Summit 11

Public vs PPP/PFI

Madrid Calle 30

Conclusions

The EuroIndia Summit 12Tunnels

M-30Sections of the works

12

14

1

2

3

4

5

7.1

7.2

8

11.2

11.1

10.29

10.1

River

Project

ByPass

Surface Projects

Projected ByPassRemodelling of the roads and the area occupied by M-30 ring-road.

Road surface refurbishment. Mainly intersections

Reroute major sections through tunnels under the city areas

Allow the surface areas to be redeveloped into green park areas

Project Objective

Compromise:

All the works must be finalized in 48 months

The EuroIndia Summit 1313

Barrier effect suppression

The EuroIndia Summit 1414

Barrier effect suppression

The EuroIndia Summit

Año MesJuly

August

September

October

November

December

January

February

March

April

Mayo

Jun

July

August

September

October

November

December

January

February

March

April

Mayo

Jun

July

August

September

October

November

December

January

February

March

April

Mayo

Jun

July

August

September

October

November

December

January

February

March

April

Mayo

2005

2006

2007

2003

20041

year

Des

ign

an

d P

roje

cts

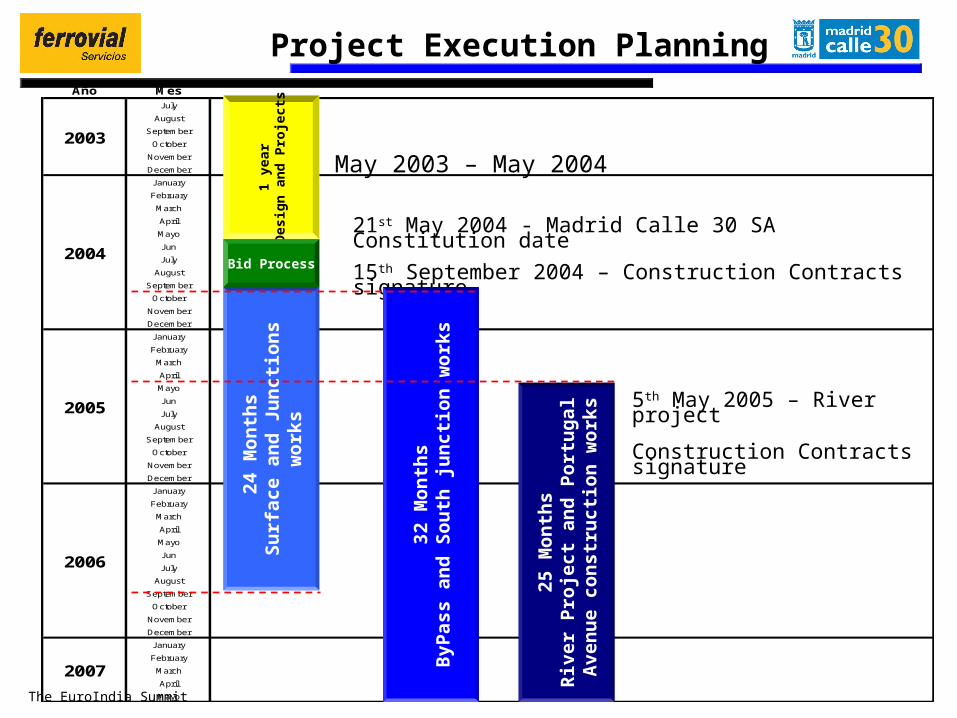

May 2003 – May 2004

21st May 2004 - Madrid Calle 30 SA Constitution date

Bid Process 15th September 2004 – Construction Contracts signature24

Mo

nth

s

Su

rfac

e an

d J

un

ctio

ns

wo

rks

32 M

on

ths

ByP

ass

and

So

uth

ju

nct

ion

wo

rks

25 M

on

ths

Riv

er

Pro

jec

t a

nd

Po

rtu

gal

Ave

nu

e co

nst

ruct

ion

wo

rks

5th May 2005 – River project

Construction Contracts signature

Project Execution Planning

The EuroIndia Summit 1616

Project - General Figures

EVOLUCIÓN OBRAS - MC30

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sep Dic Mar J un Sep Dic Mar J un Sep Dic Mar J un

% a

van

ce d

e O

bra

Superficie Nudo Sur Madrid Rio

Ejercicio 2004 Ejercicio 2005 Ejercicio 2006 Ejercicio 2007

Ap

ert

ura

Tú

nele

s

Media monthly

Duration works payments

Junctions and Surface works 266,13 8,4% 24 months 11,09

ByPass and South contion 1.331,25 41,9% 32 months 41,60

River Project 1.582,62 49,8% 25 months 63,30

TOTAL PROJECT VALUE 3.180,00 33 months 96,36

Budget

The EuroIndia Summit 1717

Equi

tyEquity

Senior Debt

VAT Loan

Interest & Loan repayment

Subordinated Debt

Monthly paym

ents of O

perating & M

anagement

Performance PaymentsInterest & subordinated loan repayment

Dividen

ds

ConstructionConstructionCompaniesCompanies

ConstructionConstructionCompaniesCompanies

Monthly construction

payments

Bank Syndicate

Project Company Structure

Dividends

The EuroIndia Summit 1818

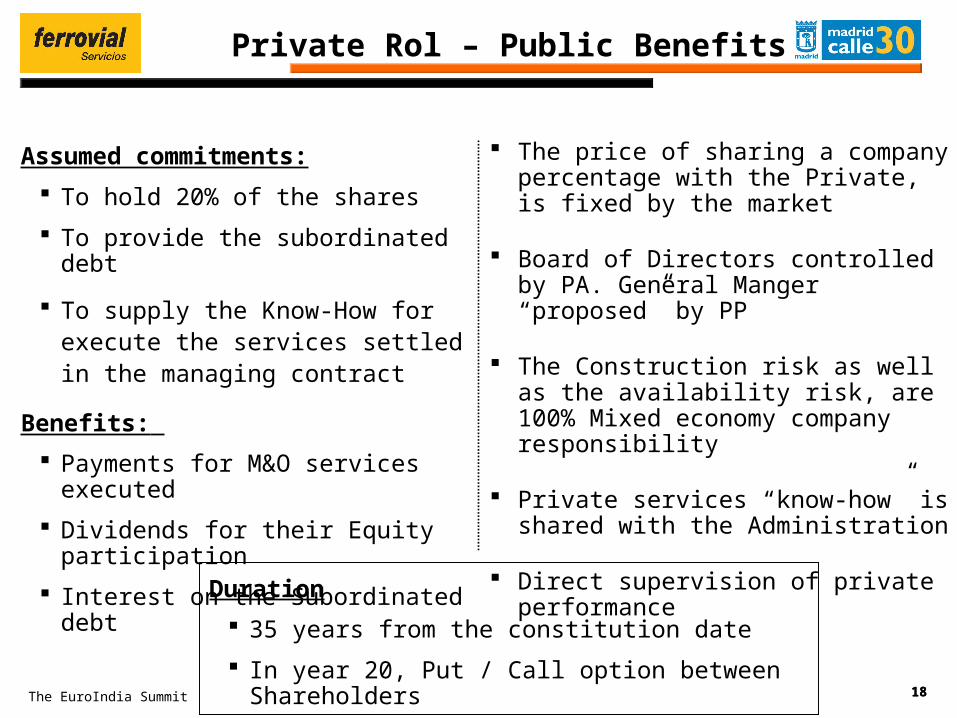

Assumed commitments:

To hold 20% of the shares

To provide the subordinated debt

To supply the Know-How for execute the services settled in the managing contract

Benefits:

Payments for M&O services executed

Dividends for their Equity participation

Interest on the Subordinated debt

Private Rol – Public Benefits

The price of sharing a company percentage with the Private, is fixed by the market

Board of Directors controlled by PA. General Manger “proposed” by PP

The Construction risk as well as the availability risk, are 100% Mixed economy company responsibility

Private services “know-how” is shared with the Administration

Direct supervision of private performance

Duration

35 years from the constitution date

In year 20, Put / Call option between Shareholders

The EuroIndia Summit19

Ratio Senior Debt / Own Resources 80/20 636,2 x 80/20 = 2.545,0

(4)202,3 Mill.€

Subordinated Debt 20%F

INA

NC

ING

SO

UR

CE

S 1

00%

(100)

Share Capital 80%

509,0 Mill.€ (16)

Madrid City Council 80% (407,2)

Private partner 20% (101,8)

Facility A = 1.350 Mill.€ • Term 30 years, Grace period 5 years• Guarantee: Basic Payment

Facility B = 1.150 Mill.€ • Term 20 years, Grace period 3 years• Guarantee: Additional payment

Senior Debt

80%

2.500 Mill.€

OwnResources

20%

636,0 Mill.€

Inve

stm

ent

– C

on

stru

ctio

n c

ost

3.18

0,00

+ 75,0 Mill.€

Ratio Municipality / Private Partner 80/20 509,0 x 80% = 407,2

Equity / Investment cost 16% 3.180,0 x 16% = 509,0

Ratio Share Capital / Subordinated Debt 80/20 509,0 x 20/80 = 127,2

Senior Debt

The EuroIndia Summit 2020

Contractual conditions

Payments are only based on the Service level.

There is no contractual relation between Payments and Traffic intensity

It was NEVER considered the Direct or the Shadow toll as an alternative concesional model. Who will pay for the lost of traffic in the M30 due to a traffic jam inside Madrid?

MC30 is responsible for the Management and Operation services

Technical and Quality standards were fixed by the Administration and assumed by the Company in the bid proposal

Risk and Venture is fully accepted by MC30 SA

Service Payment

The EuroIndia Summit 2121

Annual Payment

266,68

(Millions Euros of 2005)

Initially fixed (at contract date) and constant.

Annually updated by CPI

Can be considered as a Minimum Guaranteed Revenue

Guarantee the Senior Debt Facility A repayment

Payments: The annual payment is split in two components:

The amount directly depends on service level

Can present discounts

Depends on the results of the biannual M&O audit program

Basic Payment

95,98

AdditionalPayment170,70

Service Payment

The EuroIndia Summit 22222222

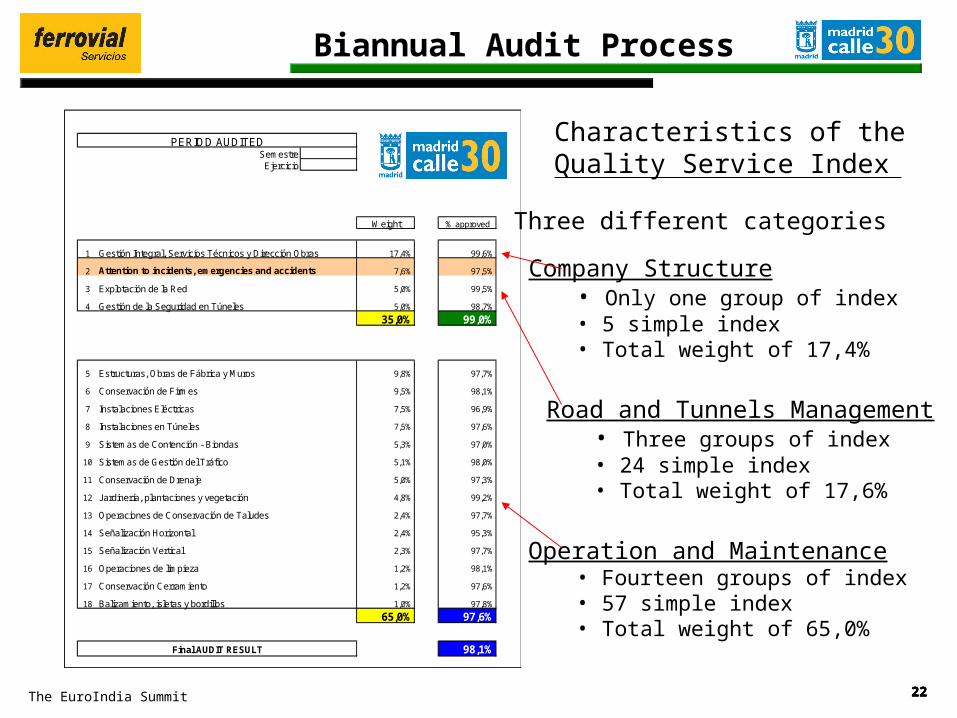

Biannual Audit Process

Characteristics of the Quality Service Index

Three different categories

Company Structure• Only one group of index• 5 simple index• Total weight of 17,4%

Road and Tunnels Management• Three groups of index• 24 simple index• Total weight of 17,6%

Operation and Maintenance• Fourteen groups of index• 57 simple index• Total weight of 65,0%

SemestreEjercicio

Weight % approved

1 Gestión Integral, Servicios Técnicos y Dirección Obras 17,4% 99,6%

2 Attention to incidents, emergencies and accidents 7,6% 97,5%

3 Explotación de la Red 5,0% 99,5%

4 Gestión de la Seguridad en Túneles 5,0% 98,7%

35,0% 99,0%

5 Estructuras, Obras de Fábrica y Muros 9,8% 97,7%

6 Conservación de Firmes 9,5% 98,1%

7 Instalaciones Eléctricas 7,5% 96,9%

8 Instalaciones en Túneles 7,5% 97,6%

9 Sistemas de Contención - Biondas 5,3% 97,0%

10 Sistemas de Gestión del Tráfico 5,1% 98,0%

11 Conservación de Drenaje 5,0% 97,3%

12 Jardinería, plantaciones y vegetación 4,8% 99,2%

13 Operaciones de Conservación de Taludes 2,4% 97,7%

14 Señalización Horizontal 2,4% 95,3%

15 Señalización Vertical 2,3% 97,7%

16 Operaciones de limpieza 1,2% 98,1%

17 Conservación Cerramiento 1,2% 97,6%

18 Balizamiento, isletas y bordillos 1,0% 97,8%

65,0% 97,6%

98,1%

PERIOD AUDITED

Final AUDIT RESULT

The EuroIndia Summit 23232323

2 Incidents, Emergencies and Accidents attention 7,60% 1.796,57

Appraisal Weight Value DiscountIndicador de resultado

2.1 % incidents, accidents or emergencies attended in time 97,9% 40% 703,18 15,45

2.2 Procedures and Action plans 95,8% 20% 344,34 14,97

2.3 Frequency of Surveillance periods fulfilled 97,6% 20% 350,69 8,62

2.4 24 hours Call Center correctly attended 99,2% 10% 178,16 1,50

2.5Possibility of Madrid City Council to have access to the register of notifications of incidents, emergencies and accidents

98,0%10% 176,06 3,59

97,5% 1.752,43 44,14

Audit procedures should be:

• Has to take into account not only the general figures but also the particular ones.

Procedures

• Simples and well known for all the stakeholders

• Easy to put in practice

• Objective. Facts and registers are the principal sources.

• Achievable. 100% should be possible.

• Based only over relevant information.

2 Attention to incidents, emergencies and accidentsSemester

Year

2.1 % incidents, accidents or emergencies attended in time

1 2 3 4 5 6

100 105 142 112 121 99 679

4 4 4 4 4 4 24

0 0 1 0 2 0 3

Time for the application of the necessary measures in case external helps are needed Weight90,0%

1 2 3 4 5 6 TOTAL15 minutes surfice8 minutes tunnel

15' for derrick

15' for resolution

Weight10,0%

1 2 3 4 5 6 TOTAL

Observations

97,9%

A

B

C

D

95%

96,9%

40%

10%

25%

25%

100%

95%

95%

95%100% 95% 95%

100,0% 96,3% 96,3%

95% 100%

100% 95% 95% 100% 100% 95%

100% 95%

RANDOM STUDY OF THE INCIDENTS ATTENDED IN THE SEMESTERINCIDENTS

100% 100% 95% 95% 95% 95%

97% 98% 99% 98,0%TOTAL 99% 96% 100%

98% 98% 100% 98,5%Time for the application of the necessary measures in case external helpsare needed

98% 97% 100%

96% 100% 98% 97,7%Time of resolution in case that external helps are not needed 15 minutes surfice 97% 95%

97,5%

Time needed to establish the necessary signposting 10 minutes 98% 100% 100% 100% 100% 97% 99,2%

Accidents with dead people

100% 95% 100%

R E S U L T S

Month

MONTHLY ACCIDENTS

Time needed to arrive at the incident place

Total

Total Number of incidents attendedNumber of incidents fully analysed

96,3% 96,3% 96,3%

Period

95% 95% 100%

100%

Biannual Audit Process

The EuroIndia Summit 2424

Time needed to arrive at the incident place

0

5

10

15

20

1º Sem 06 2º Sem 06 ene-07 feb-07 mar-07 abr-07 may-07 jun-07 jul-07 ago-07 sep-07 oct-07 nov-07 dic-07

Va

ria

ble

Pa

yme

nt

Gu

ara

nte

ed

Contractual Limit

Time needed to establish the necassary signposting

0

5

10

15

1º Sem 06 2º Sem 06 ene-07 feb-07 mar-07 abr-07 may-07 jun-07 jul-07 ago-07 sep-07 oct-07 nov-07 dic-07

Va

ria

ble

Pa

yme

nt

Gu

ara

nte

ed

Contractual Limit

• Every single parameter must be fulfil

• In the 2º semester of 2006 the added value of

Arrive = 5,8 minSignal = 3,4 minResolution = 21,2 min

30,4 min

is less than the added contractual limit value (40 min)

• Nevertheless, MC30 was fined because Resolution time exceed the Contractual limit.

• Rules must be clear, understandable and easy to put in place.

Time of resolution in case that external helps are not needed

0

5

10

15

20

25

30

35

1º Sem 06 2º Sem 06 ene-07 feb-07 mar-07 abr-07 may-07 jun-07 jul-07 ago-07 sep-07 oct-07 nov-07 dic-07

Variable Payment Guaranteed

Contractual Limit

Biannual Audit Process

The EuroIndia Summit 25

Allow to achieve the best of both worlds. Roles must be clear, well defined and agreed

There are few sectors where PPP structure is not viable

The ratio between M&O cost and Investment project value, it is not a restriction for the implementation of PPP structures.

Risk and Benefit are two factors of the same equation. The higher the Risk, the higher the Benefit.

Tax structure (VAT, Corporation tax) must be carefully analyzed. From the Public point of view, PPP company structure is frequently inefficient in tax issues.

Conclusions

The EuroIndia Summit

Thank you very much for your

attention

26

Fernando Guedán PeckerDirector de Proyectos de InversiónFerrovial [email protected]