the european petrochemical industry in challenging times · pdf filethe european petrochemical...

TRANSCRIPT

The European Petrochemical Industry in Challenging Times

Dorothee Arns, Executive Director Petrochemicals Europe

2

1. Petrochemicals Europe – who we are

2. The chemical industry – facts and figures

3. It all starts with the crackers …..

4. The competitiveness challenge

5. The regulatory landscape

6. Summary

3

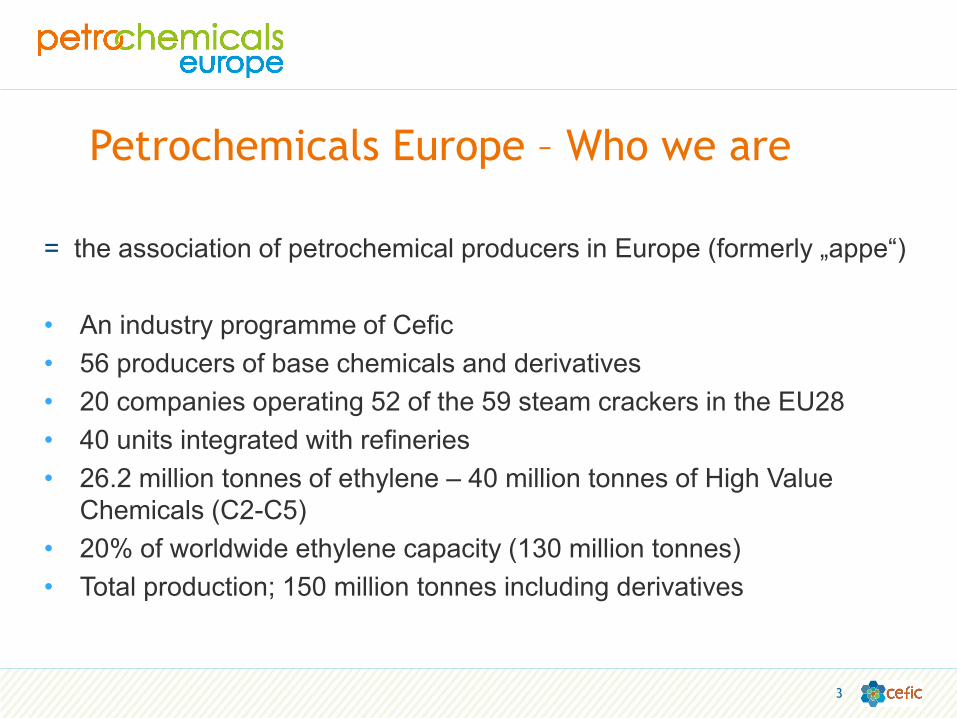

Petrochemicals Europe – Who we are

= the association of petrochemical producers in Europe (formerly „appe“)

• An industry programme of Cefic

• 56 producers of base chemicals and derivatives

• 20 companies operating 52 of the 59 steam crackers in the EU28

• 40 units integrated with refineries

• 26.2 million tonnes of ethylene – 40 million tonnes of High Value

Chemicals (C2-C5)

• 20% of worldwide ethylene capacity (130 million tonnes)

• Total production; 150 million tonnes including derivatives

4

Our VISION is for the petrochemical industry to be recognised as the

foundation of future economic success in Europe, fuelling innovation,

manufacturing and employment.

Our mission:

As the voice of the European petrochemical industry, we

Advocate for conditions that will allow the industry to operate successfully

in a highly competitive global environment

Raise awareness of the contribution of our industry to the European

economy which provides essential raw materials for thousands of

products produced by diverse industries, driving innovation and

creating employment

Engage continuously with all our stakeholders in the pursuit of

sustainable solutions.

Petrochemicals Europe – Vision and Mission

5

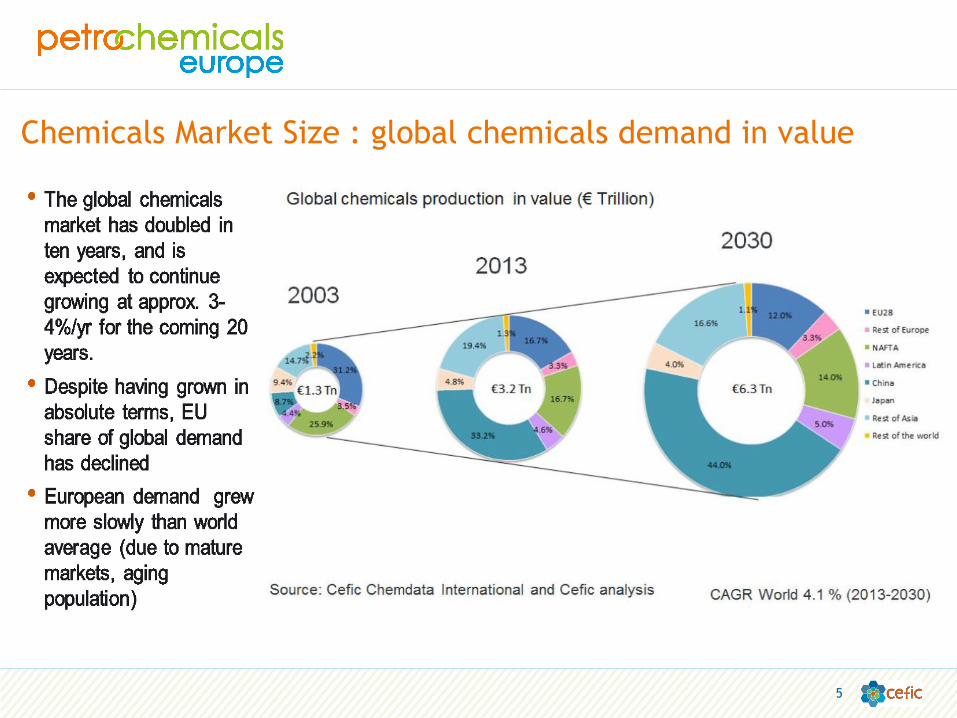

Chemicals Market Size : global chemicals demand in value

6

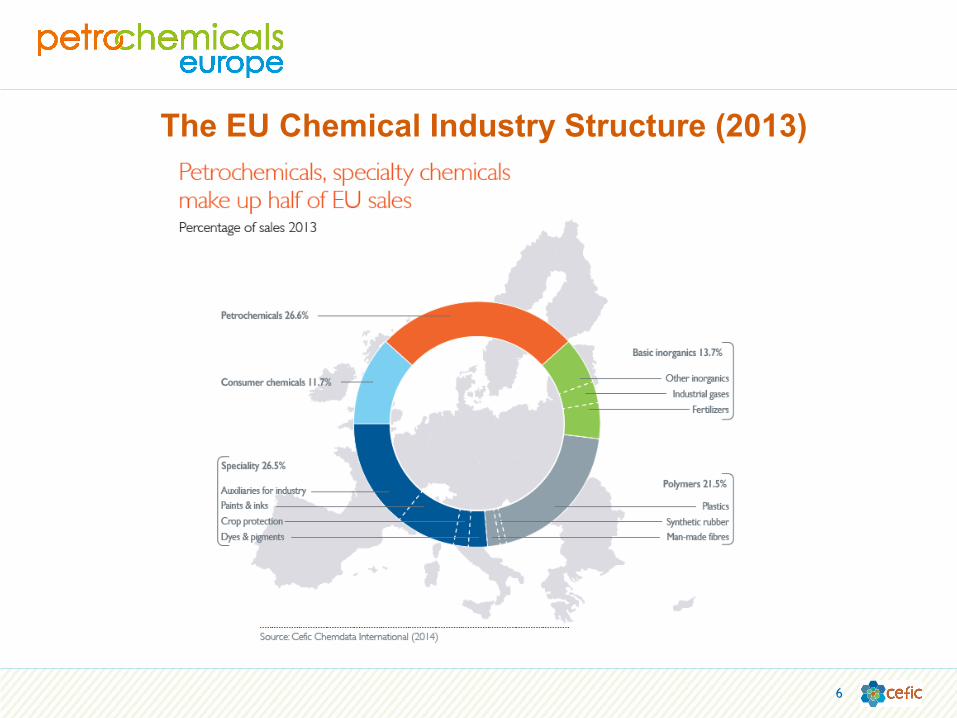

The EU Chemical Industry Structure (2013)

7

Source: Petrochemicals Europe

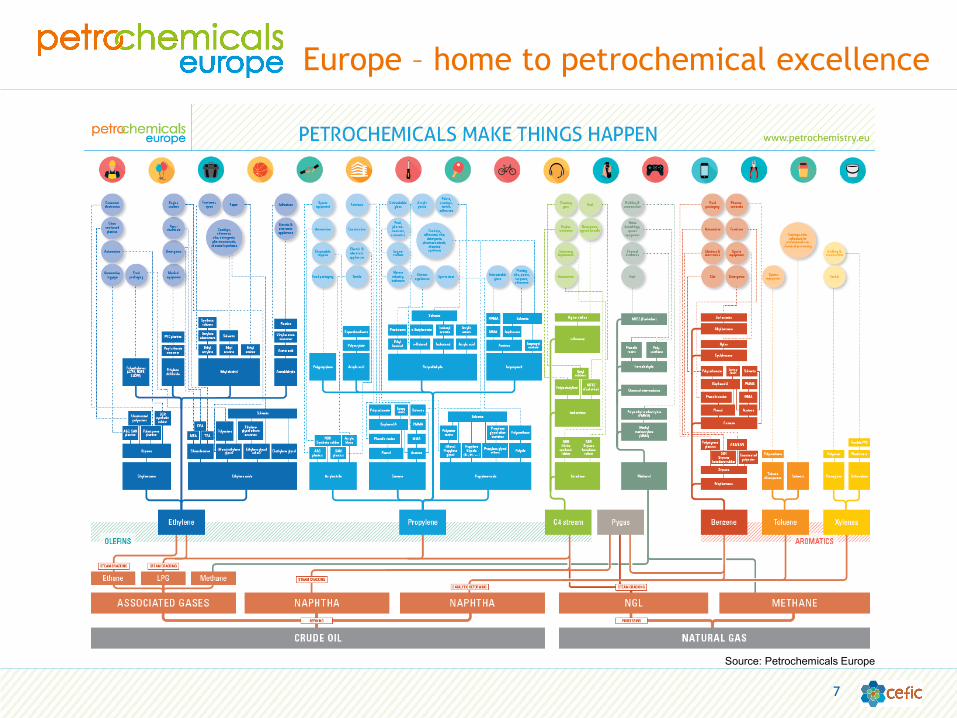

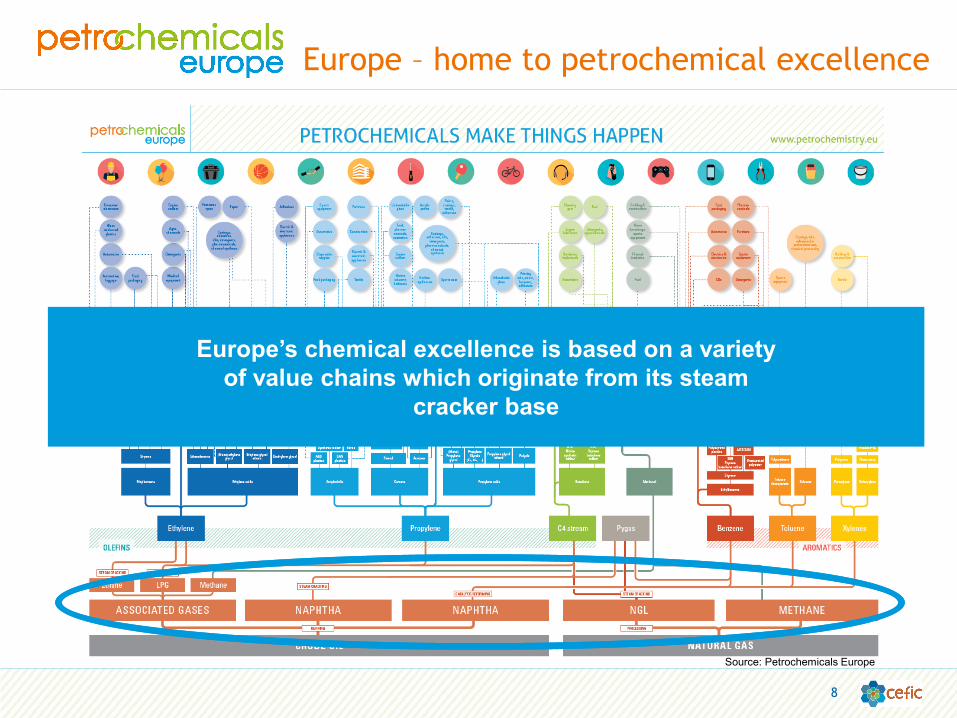

Europe – home to petrochemical excellence

Source: Petrochemicals Europe

Europe’s chemical excellence is based on a variety

of value chains which originate from its steam

cracker base

Europe – home to petrochemical excellence

8

9

59 steam crackers in operation in EU 28

Homogenous geographic coverage

Transform crude oil and natural gas into high value materials

> 80% of all value chains start from steam crackers

> 300,000 direct employees + huge multiplying effects

contribution to overall European GDP: 155,000,000,000 € (155 bn €)

Crackers´ derivatives and polymers provide sustainable

solutions to energy savings and confort such as insulation,

durable, light-weight and resistant composites, etc.

95% of all manufactured goods are based on petrochemicals, such

as electronics, furniture, appliances, textiles, and many more

Highly exposed to international competition (commodity business)

Highly exposed to energy and feedstock costs

Crackers initiate the value chains

10

Global drivers EU Mid-East US Asia

• Crude oil & Feedstock costs

• Market demand

• World scale capacity plants

• Credit rate (Capex)

• Currency (€/$)

Regional drivers

• Energy costs

• Labour cost

• Regulatory costs

• Infrastructure

Operator specific

• Integration & client proximity

• Energy efficiency

• Feedstock flexibility

• Product portfolio (technology)

Strength Weakness Neutral

Competitiveness Drivers for Petrochemicals

11

80% of manufacturing costs of petrochemicals are related to feedstock and

energy

85% of European crackers use naphtha as main feedstock

Units are capital intensive (2,5 to 4 billion €)

the price of both naphtha and natural gas remains correlated to the price of

Brent oil

in the value chain products derived from crackers are traded globally at a

market value set by global economics

Shale gas is a game changer for petrochemicals and creates substantial

opportunities for investments in the US

The Key Global Competitiveness Challenge –

Europe is losing ground

Ethylene Cash Cost of Regional Steam Crackers (US$/tonne C2)

Crude drop has brought some relief but only vs US

12

Source: ICIS Consulting

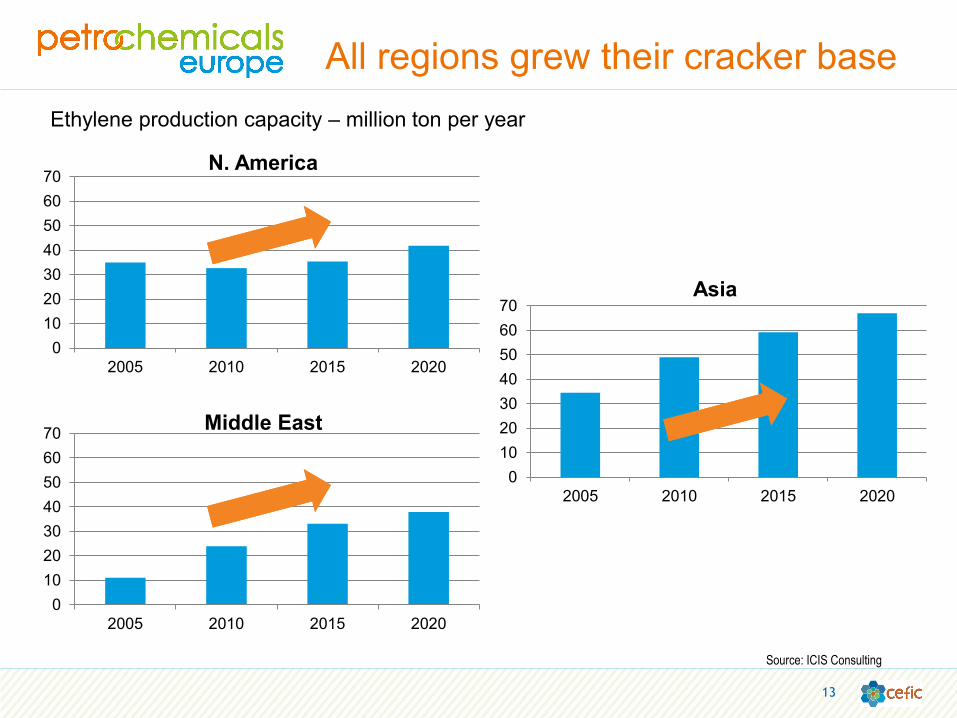

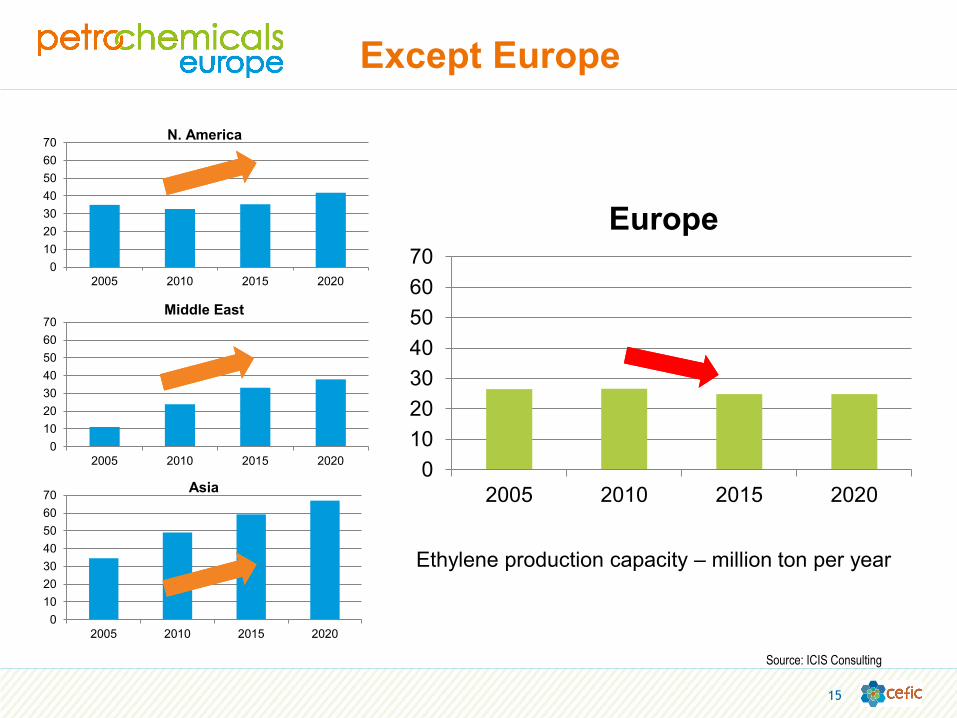

All regions grew their cracker base

Source: ICIS Consulting

Ethylene production capacity – million ton per year

0

10

20

30

40

50

60

70

2005 2010 2015 2020

N. America

0

10

20

30

40

50

60

70

2005 2010 2015 2020

Middle East

0

10

20

30

40

50

60

70

2005 2010 2015 2020

Asia

13

With ethane but also naphtha as feedstock

Naphtha remains dominant feedstock

14

Source: ICIS Consulting

0%

20%

40%

60%

80%

100%

2010 2015 2020

Ethylene production by feedstock

Other Naphtha LPG Ethane

0%

10%

20%

30%

40%

50%

2010 2015 2020

Ethylene production by feedstock

Ethane LPG Naphtha Other

0

10

20

30

40

50

60

70

2005 2010 2015 2020

Europe

Except Europe

Ethylene production capacity – million ton per year

Source: ICIS Consulting

0

10

20

30

40

50

60

70

2005 2010 2015 2020

N. America

0

10

20

30

40

50

60

70

2005 2010 2015 2020

Middle East

0

10

20

30

40

50

60

70

2005 2010 2015 2020

Asia

15

Declining cracker base

Europe is only region in the world where no new cracker capacity was built

this decade. On the contrary: by 2016, capacity will be reduced by almost

10% vs. 2008 peak

Source: ICIS Consulting

21

22

23

24

25

26

27

28

2000 2005 2010 2015

million ton per year

European Ethylene Production Capacity

16

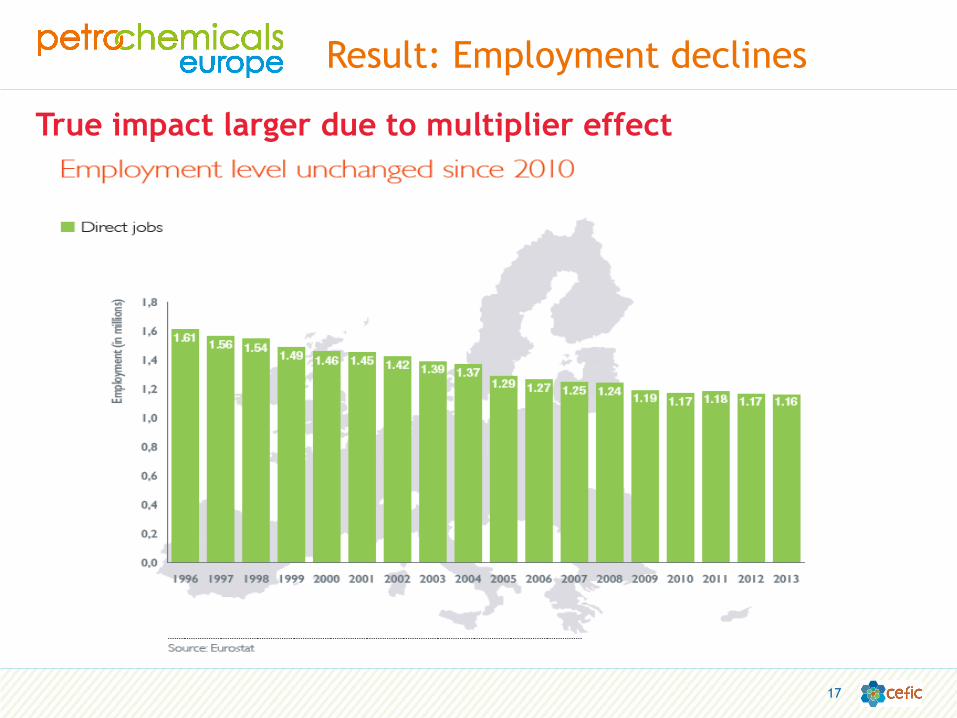

Result: Employment declines

True impact larger due to multiplier effect

17

The regulatory landscape

18

19

Cumulated number of EU regulations on Health,

Safety and Environment (net of abrogation)

20

Competitiveness Pros and Cons for Europe

Summary

Large integrated domestic market with strong customer industry clusters

High international orientation and global network to external customer industries

Until now availability of skilled and motivated workers and scientists

Continued strategic restructuring efforts (flexibilty to globalised markets)

Strong innovation efforts will generate new growth clusters: Efficient Energy use, health and new materials which could solve upcoming societal mega challenges

Low “new consumers” population growth in the EU => low demand growth for chemicals in general - elderly population, shrinking working age classes, high saturation levels.

High energy and feedstock costs vs Middle East and now the US => EU is facing an upcoming wave of petrochemical capacity additions, especially in Middle East and US

High Regulatory Compliance Costs (e.g. REACH, Seveso, IED, 7th EAP…)

Non-energy raw material availability and cost issues (eg. biobased feedstock, rare earths, minerals)

Lack of a “Common Industrial Policy” or a “Common Energy Policy”

a „walk the talk“ approach is urgently needed from EU politicians!

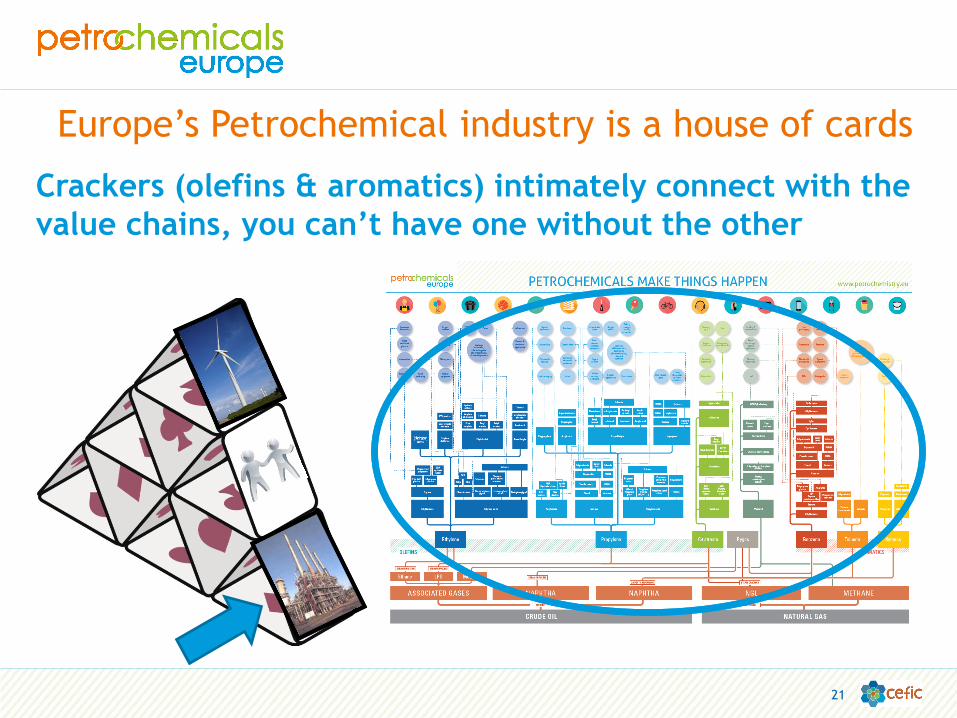

Crackers (olefins & aromatics) intimately connect with the

value chains, you can’t have one without the other

Europe’s Petrochemical industry is a house of cards

21

22

Thank you for your attention!

Please visit us at

www.petrochemistry.eu

and at our table outside …

… or follow us on : /eupetro