the f&a humpty dumpty – putting the pieces together ( insights for the departmental...

Post on 21-Dec-2015

214 views

TRANSCRIPT

The F&A Humpty Dumpty – Putting the Pieces Together

(Insights for the Departmental Administrator)

National Council of University Research Administrators

Region VI-VII Meeting

April 2005

Session Panelists

Gary Chaffins - Director, Office of Research Services & Administration, University of Oregon

Stuart Laing – Manager, Cost Analysis Office for Research and Sponsored Projects Administration, Arizona State University

Facilities & Administrative Costs

Topics• F & A rates - Huh? • Departmental Involvement -

You mean I’m involved? • F&A Recovery – Is it worth

the effort?

F & A RatesWhat are they?

Facilities & Administrative Costs

• The “Rate” is really multiple rates added together; example:– Research rate components: On Campus Off

• Building use 2.7 points• Equipment use 3.6 points• Operations & Maintenance 15.3 points• Library 2.4 points• General Administration 6.2 points * 6.2• Department Administration 14.9 points * 14.9• Sponsored Project Administration 4.4 points * 4.4• Student Services Administration .5 points * .5• Total 50.0 points

** 26.0

* Administration components are “capped” at 26%.** Points a.k.a. percent.

Geez… this session is going to be worse than I

thought!

Facilities & Administrative Costs

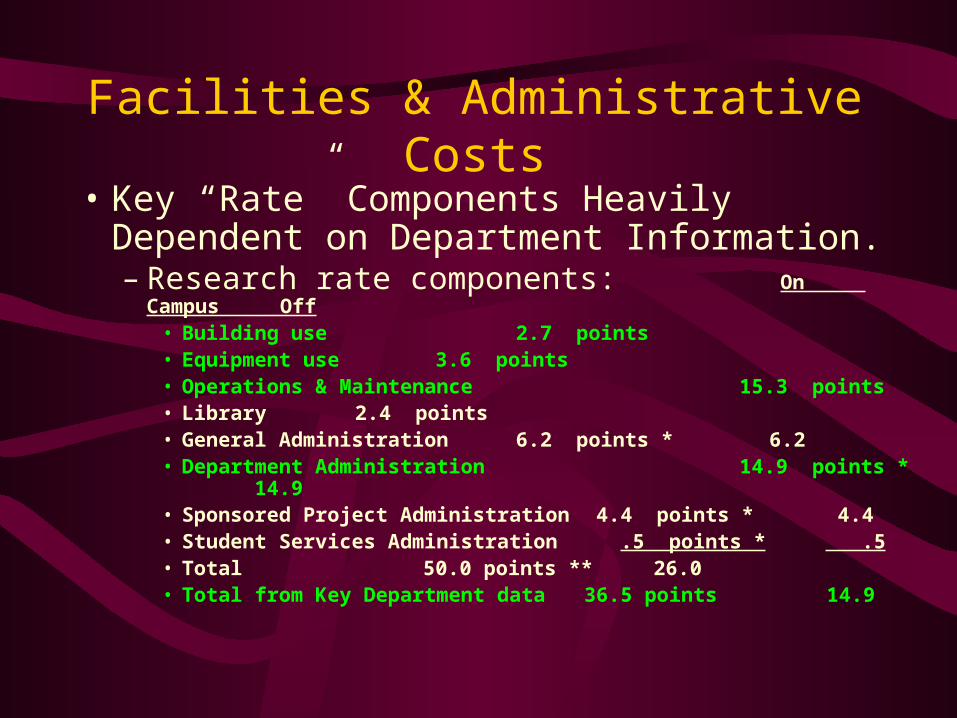

• Key “Rate” Components Heavily Dependent on Department Information.– Research rate components: On Campus Off

• Building use 2.7 points• Equipment use 3.6 points• Operations & Maintenance 15.3 points• Library 2.4 points• General Administration 6.2 points * 6.2• Department Administration 14.9 points * 14.9• Sponsored Project Administration 4.4 points * 4.4• Student Services Administration .5 points * .5• Total 50.0 points

** 26.0 • Total from Key Department data 36.5 points 14.9

Is it getting Better?

FACILITIES & ADMINISTRATIVE COST CALCULATION – OVERVIEW

Space

Space

Space

MTC

Cross Allocations

Building andEquipment

Depreciation

Building andEquipment

Depreciation

InterestInterest

Operations andMaintenance

Operations andMaintenance

GeneralAdministration

GeneralAdministration

DepartmentAdministrationDepartment

Administration

Sponsored ProjectsAdministration

Sponsored ProjectsAdministration

Library1Library1

Student Services2Student Services2

F&A Cost Pools

OtherSponsoredActivities

OtherSponsoredActivities

Instruction andDepartmental

Research

Instruction andDepartmental

Research

OrganizedResearch

OrganizedResearch

OtherInstitutional

Activities

OtherInstitutional

Activities

F&A Costs Allocated To

MTDCOther

SponsoredActivities

MTDCOther

SponsoredActivities

MTDCInstruction andDepartmental

Research

MTDCInstruction andDepartmental

Research

MTDCOrganizedResearch

MTDCOrganizedResearch

Distribution Base

%%

%%

%%

F&A Cost Rates

Allocation Bases

Space

Space

Space

MTC

MTDC

MTDC

Pop/FTE

Instruc

=

=

=

1 Population including students/FTE of employees

2 Generally allocated to the Instruction function

1 Population including students/FTE of employees

2 Generally allocated to the Instruction function

/

/

/

Nope…

Departmental Involvement and

Impact

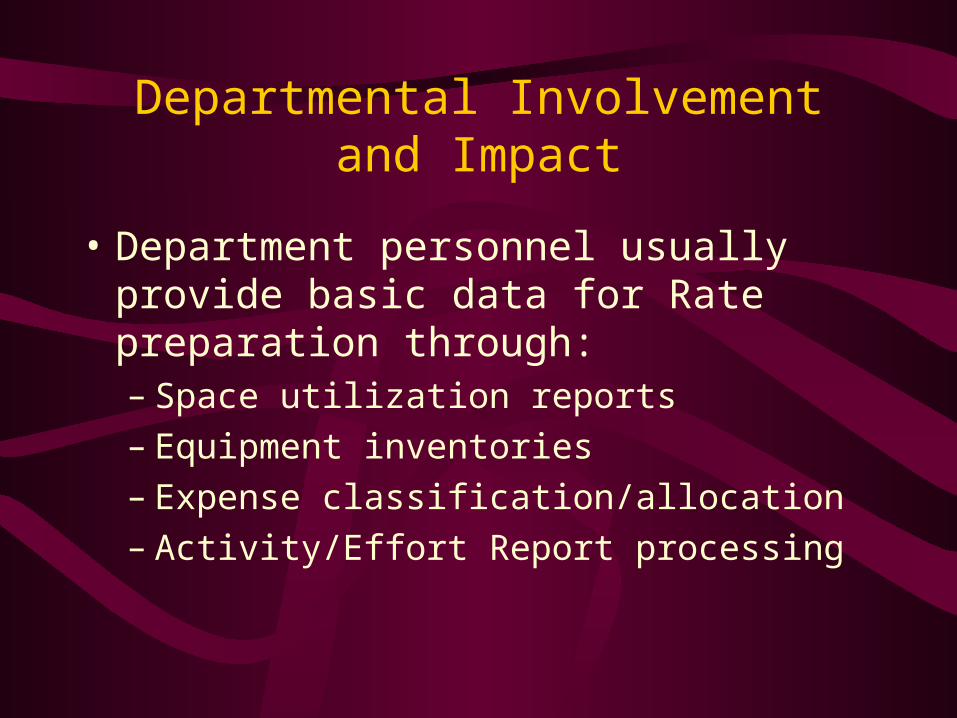

Departmental Involvement and Impact

• Department personnel usually provide basic data for Rate preparation through:– Space utilization reports – Equipment inventories– Expense classification/allocation– Activity/Effort Report processing

Space Utilization Reports

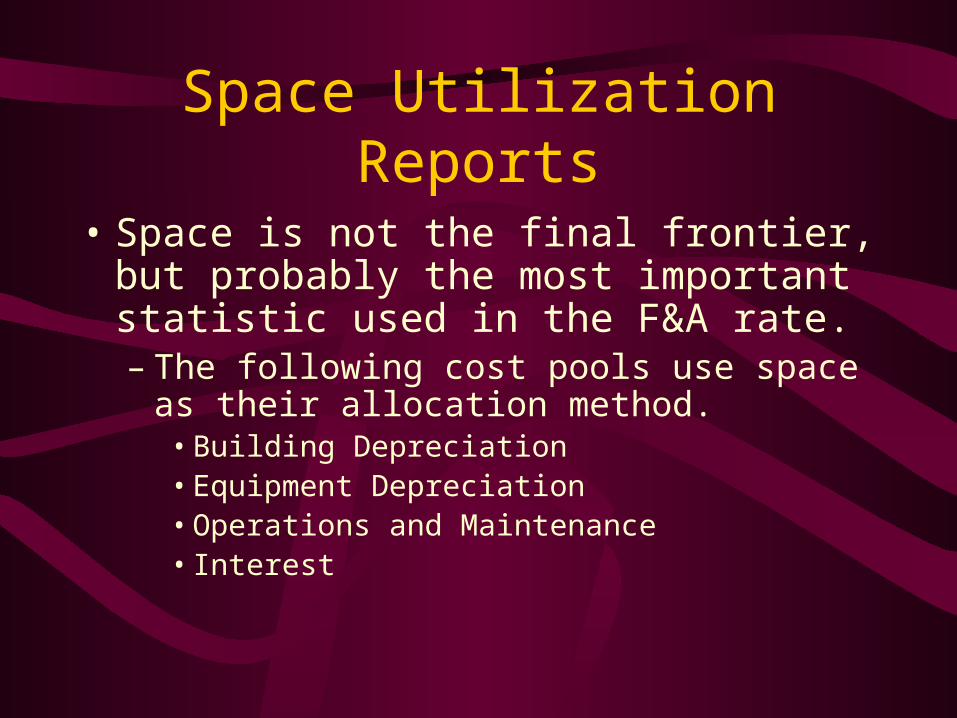

• Space is not the final frontier, but probably the most important statistic used in the F&A rate.– The following cost pools use space as their

allocation method.• Building Depreciation• Equipment Depreciation• Operations and Maintenance• Interest

Are you lost yet????

Space Utilization Reports

• It is critical that the departmental space coordinator know their department space, how generally how it’s used, and how it should be coded.

• No single person should decide how each room is being used, but the space coordinator should walk the space and talk to the occupant.

Space Utilization Reports

• A room that is 100% Organized Research (OR) with 1,000 square feet would equate to 1,000 square feet of OR space.

• Care should be taken not to code rooms incorrectly, one issue - 100% Organized Research Labs. Instruction does go on in labs.

Equipment Inventories

• Equipment used by the university is depreciated depending on the capitalization threshold.

• Equipment being depreciated is calculated into the F&A rate proposal.

• It is critical that each piece of equipment be mapped to a room, so depreciation can be allocated to the activities conducted in that room.

Expense classification/allocation

• How can you assist in this process?

• Each expense during a “Base Year” is used to calculate the F&A rate.

• It is critical that each expense be coded correctly in your financial system.

• Cost transfers must be completed by June, 30. Critical correct cost on correct account.

Activity/Effort Reporting

• Not only is this a hot topic in the eyes of A-133 Auditors and Federal Sponsors, but it is used in the F&A rate.

• You must include in the base (OR, Instruction, Other) all the MTDC Expenditures and Cost Share.

• PI Effort used as Cost Share is documented on the Effort Reports.

Activity/Effort Reporting

• Certifying Effort validates the expense to the sponsored account.

• Some Institutions still use Effort reports as a method to calculate the DA cost pool. You might think of switching to the DCE

Any questions so far?

F&A Recovery – Is it worth the effort?

Simple Answer…..YES!!

A Point is a Point

• A point is a percent of the F&A rate. So 50% is 50 points.

• A point to a University can range from $200K to well over $1M per year worth of recovery.

F&A Recovery

• Institutions have unrestricted use of F&A recovery (except those listed in Exhibit A of A-21).

• Pay for Buildings, Equipment, Cost Share etc.

• Return portions to the Colleges and Departments to help cover Administrative costs.

The Problem: Identify the Direct and the F&A Costs

Expense type:Salaries & Wages

Fringe benefits

Services

Supplies

Travel

Equipment

Subcontracts

Interest

Rent

Utilities

Direct F&A

X X

X X

X X

X X

X X

X X

X X

X X

X X

X X

Facilities & Administrative Costs (Order of Distribution)

• Depreciation and Use AllowancesOperation and Maintenance Expenses

General Administration & Expense

Departmental Administration

Sponsored Projects Administration

Student Administration and Services

Library

Instruction

Organized Research

Other Sponsored Programs

Other Institutional Activities

F&A Recovery- The Institutional

Perspective

Now’s The Time For Some Real Discussion…...