the fundamentals of strategic logic and integration for merger and acquisition projects

DESCRIPTION

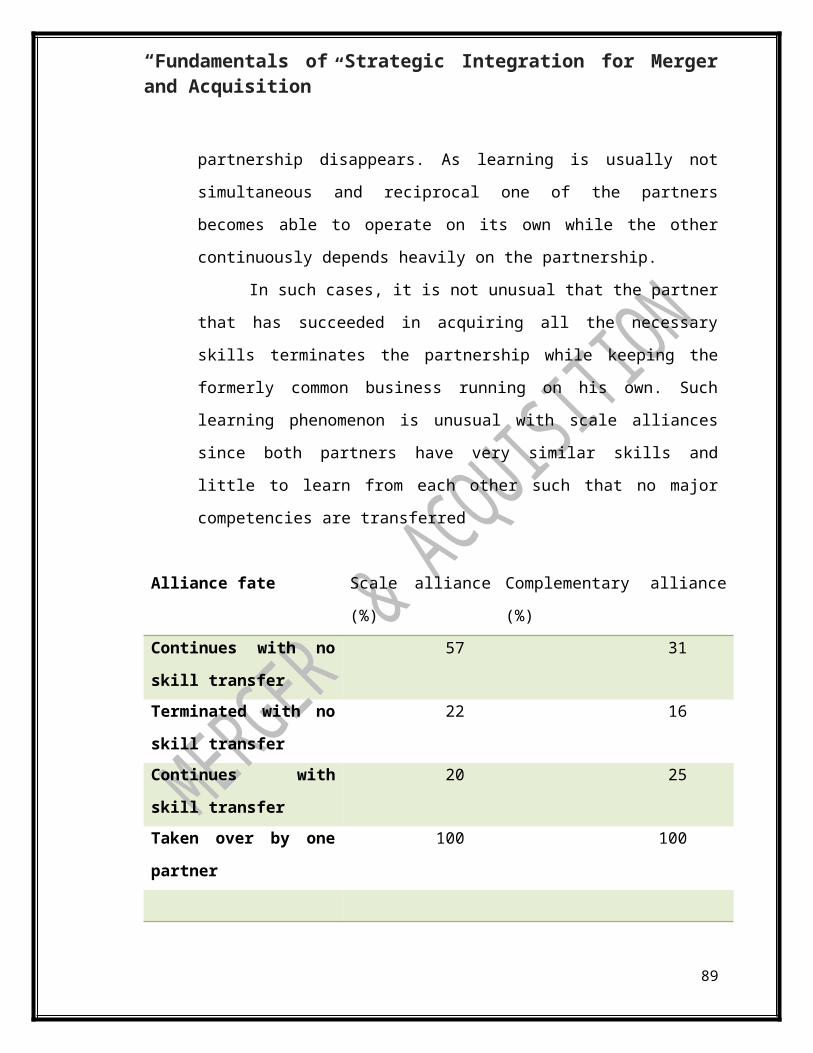

JKJKJKJTRANSCRIPT

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Fundamentals of Strategic Integration for Merger and Acquisition”.

PREPARED BY

SHASHANK MITTAL

ROLL NO. 581117084

UNDER THE GUIDANCE OF

Dr. Sanjna Jain

IN PARTIAL FULFILLMENT OF THE REQUIREMENTFOR THE AWARD OF

DEGREE OF

MBA (FINANCE)NIMACT INSTITUTE

(2011 – 2013)L.C. CODE:-01802

1

“Fundamentals of Strategic Integration for Merger and Acquisition ”

ABSTRACT

‘Mergers and Acquisitions’ (M&As) are strategically planned

transactions between two or more companies in which the target and

the acquiring firm jointly create a new entity to gain competitive

advantage in the market place. In other words, mergers and

acquisitions allow the purchase of assets that would be difficult, risky,

time-consuming or even impossible to obtain by other alternative

business collaborations or organic growth. ‘Merger and acquisition’, or

‘M&A’ is a field of study in which the definitions often vary in different

publications. The traditional framework how to distinguish between

‘mergers’ and ‘acquisitions’ is the perspective on the legal

independence of the business entities

There is lacking evidence on the correlation between the relative size

of the merging firms and long-term performance. Some researchers

have suggested that small mergers (mergers where the two firms are

very different in size) tend to produce higher performance than larger

mergers (mergers where the two firms are similar in size). They

attribute these performance differences to the ease of combining

operations. With smaller mergers the integration of the new entity is

more easily controlled and the disruption to the organization as a

whole is minimized. With a large merger, the integration problems are

multiplied and disruption can occur throughout the whole organization.

On the other hand, those researchers neglect the fact that a small

merger often provides also less significant gains to the large

organization.

A comprehensive introduction for practitioners to assess merger and

acquisition activity from an acquiring firm perspective – motives,

synergy realization, integration planning.

2

“Fundamentals of Strategic Integration for Merger and Acquisition ”

ACKNOWLEDGEMENT

IT IS THE MATTER OF GREAT PLEASURE AND PRIVILEGE TO BE ABLE

TO PRESENT THIS PROJECT REPORT ON FUNDAMENTAL OF STRATEGIC

INTEGRATION FOR MERGER AND ACQUISITION.

THE COMPILATION OF THE PROJECT IS A MILESTONE IN THE LIFE OF

THE MANAGEMENT STUDENT AND ITS EXECUTION IS INEVITABLE WITH THE

CO-OPERATION OF THE PROJECT GUIDE. I WISH TO RECORD A DEEP SENSE

OF RESPECT AND GRATITUDE TO MY PROJECT GUIDE, DR.. SANJNA JAIN FOR

HER ENCOURAGEMENT TO COURSE OF MY WORK. IT IS DUE TO THE

ENDURING EFFORT AND GUIDANCE OF MY GUIDE THAT ULTIMATELY MADE

IT SUCCESS.

I ALSO TAKE THIS OPPORTUNITY TO EXPRESS MY DEEP REGARDS AND

GRATITUDE AND WOULD LIKE TO THANK THE HEAD OF S.M.U. DEPARTMENT

WHO GAVE US GUIDANCE TO TAKE UP AND PURSUE THE PROJECT

I CANNOT JUST CONDONE THE VALUABLE OPPORTUNITY GIVE TO ME

BY THE SMU UNIVERSITY FOR COMPILING AND SUBMITTING THE PROJECT,

WHICH I FEEL IS AN OPPORTUNITY TO EXPRESS MY VIEWS ABOUT EXPORT

PROCEDURE AND DOCUMENTATION.

I ACKNOWLEDGE MY INDEBTNESS TO VARIOUS AUTHORS FOR

MAKING USE OF VALUABLE INFORMATION LIBERALLY.

IT IS MY PROUD PRIVILEGE TO EXPRESS MY DEEP SENSE OF

APPRECIATION AND GRATITUDE TO MY PARENTS AND FRIENDS FOR THEIR

SUPPORT AND CO-OPERATION IN THE COURSE OF THE PROJECT EITHER

DIRECTLY OR INDIRECTLY INVOLVED IN TIME WITH THEIR VALUABLE

CONTRIBUTION.

3

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Table of content

Abstract……………………………………………………………………………02

Acknowledgment…………………………………………………………….....03

1) Introduction.................................................................................07

1.1Motivation...................................................................................07

1.2 Objectives, perspective and limitations of this work....................08

1.2.1

Objectives ...................................................................................08

1.2.2

Perspective .................................................................................09

1.2.3Limitations...................................................................................09

1.3 Content description....................................................................09

2) Classification of mergers and

acquisitions..............................12

2.1 The merger ................................................................................13

2.2 The acquisition...........................................................................13

2.3 Classification according to companies’ relatedness ....................14

2.4 Other classifications...................................................................14

2.5 ‘Merger and acquisition’ as used throughout this work...............16

3) Post-M&A firm performance

studies........................................17

3.1 Motivation to consider performance studies ................................17

3.2 How is post-M&A firm performance measured? ..........................17

3.3 What is failure and success? ......................................................18

3.4 Factors with and without relationship to post-M&A performance.18

3.4.1 Positive or negative relationship to

performance .........................19

4

“Fundamentals of Strategic Integration for Merger and Acquisition ”

3.4.2 No significant relatedness to performance or conflicting

evidence21

3.5 M&A performance........................................................................23

3.6 Diversification .............................................................................24

3.7 Degree of integration ...................................................................26

3.8 Criticism on performance study methodology...............................26

4)Motives for merger and acquisition

activity..............................29

4.1 Exploitation (synergy motives) .....................................................30

4.1.1 What is

‘synergy’? .......................................................................30

4.1.2 Classification of

synergies ...........................................................31

4.1.3 Cost synergies

(‘rationalization’)...................................................32

4.1.4 Revenue

synergies........................................................................33

4.1.5 Synergies from

intangibles ..........................................................34

4.2 Exploration..................................................................................35

4.3 Preservation and survival.............................................................35

4.4 Managers’ self-interest and prestige ............................................37

4.5 Finance motives...........................................................................38

5) Post-M&A integration and

transformation................................40

5.1 What is an adequate level of integration? .....................................41

5.2 What are the difficulties and dangers during integration …..........41

5

“Fundamentals of Strategic Integration for Merger and Acquisition ”

5.2.1 Under- and

overintegration...........................................................42

5.2.2 Post-merger management of positive and negative

synergies......43

5.2.3 Speed of integration ....................................................................

43

5.2.4 Communication to internal and external

stakeholders ................44

5.2.5 Cultural fit and anticipation of culture dissonance......................45

6) National and organizational culture and culture

clashes .........46

6.1 What is culture in the M&A context? ...........................................46

6.2 Which forms of acculturation exist……………………………………...47

6.3 Are cultural stereotypes a real assist or just convenience? ..........47

6.4 Can culture be ‘measured’? .........................................................48

6.5 What is the result of perceived culture dissonance…………….......50

6.6 How can one understand culture dissonance……………………......51

6.7 What can be learned for practice to anticipate culture……………..52

6.7.1 Avoid insurmountable integration

problems................................52

6.7.2 be aware of potential cultural dissonance ..................................53

7) Success factors, reasons for failure and

risks...........................54

7.1 Financial overextension and price premium.................................54

7.2 Realization of synergies................................................................55

7.3 Negative synergies .......................................................................56

7.4 An example on the difficulties of synergy

assessment………..........57

6

“Fundamentals of Strategic Integration for Merger and Acquisition ”

7.5 Strategic logic ..............................................................................58

7.6 Interview studies .........................................................................60

8) Alternatives to mergers and

acquisitions.................................61

9) Reasoning of M&A activity in an early project

phase ..............65

9.1 The acquiring company’s strategy................................................65

9.2 M&A motives...............................................................................65

9.3 Strategic fit between target and acquiring firm ............................66

9.4 Sources of synergies and price premium......................................66

9.5 Integration, transformation and culture.......................................67

9.6 Costs and negative synergies ......................................................68

9.7 Competition’s reaction ................................................................68

9.8 Alternative business collaborations .............................................69

10) A case study : HP COMPAQ Merger deal……………………………

70

11)

Conclusions...........................................................................8

3

Literature ..............................................................................

.....87

1) Introduction

7

“Fundamentals of Strategic Integration for Merger and Acquisition ”

‘Mergers and Acquisitions’ (M&As) are strategically planned

transactions between two or more companies in which the target and

the acquiring firm jointly create a new entity to gain competitive

advantage in the market place. The motives and objectives for M&A

activity are various. Competitive advantage could arise from synergies

due to economies of scale, an increase in market share, better access

to a customer base, ownership of distribution channels and access to

knowledge and technology to mention just a few. In other words,

mergers and acquisitions allow the purchase of assets that would be

difficult, risky, time-consuming or even impossible to obtain by other

alternative business collaborations or organic growth.

While strategic logic for M&A projects seems to be straightforward,

however, most empirical studies reveal that a majority of M&A projects

fails to reach their objectives

“[…] mangers generally want a company that is fully staffed, with a

general manager and all functional heads and, since it takes three to

five years to develop a good operating team, they want assurance that

these key people will stay on the job.” (Paine)

1.1 Motivation

The present work is conceptualized around the set of questions raised

above. The work is motivated by the recent necessity of the author’s

employer to obtain a comprehensive introduction to the field of

mergers and acquisitions that is of practical relevance in the

employer’s current economic context.

The Strategic Business Unit (SBU) Mat Char (Materials

Characterization)

Of METTLER TOLEDO AG faces a worldwide consolidation phase in the

field of Thermal Analysis and neighboring analytical lab techniques.

8

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Competitors’ mergers and acquisitions and the limited organic growth

potential due to harsh competition make it necessary to consider M&A

as a feasible mechanism for growth and protection. However, beside

financial analysis a systematic assessment concept and the

corresponding knowledge required in a pre-M&A phase are largely

missing.

Considering the fact that an M&A deal can be one of the biggest

decisions a company or business unit ever makes, missing

fundamentals for a proper decision put a high risk to the acquiring

company. Many managers however do not have adequate time and

knowledge to carefully evaluate merger and acquisition projects. Such

time pressure increases the chance of rushing headless into

unqualified decisions of poorly planned M&As, leaving important areas

of uncertainty unresolved and resulting in the widely reported

disappointing outcomes.

1.2 Objectives, perspective and limitations of this

work

1.2.1 Objectives

Indeed, research on M&A consists of two distinct categories: the

empirical performance literature and the post-merger integration and

culture literature. While these two very extensive areas of research

dominate the whole M&A literature, they are highly specialized

focusing mostly on very distinct subjects. As a consequence they

provide little guidance for managers due to their very fragment-like

research questions.

Interestingly, there is even very little literature on strategic concerns of

mergers and acquisitions not to mention a comprehensive (but still

trustworthy) introduction for practitioners.

9

“Fundamentals of Strategic Integration for Merger and Acquisition ”

As a consequence, the overall objective of this work is to

Provide a comprehensive introduction to subjects being relevant

in an early stage of a merger and acquisition project (before due

diligence) to increase the likelihood of M&A success.

Allow an informed decision on strategic logic and integration

matters of merger and acquisition projects and to sensitize to the

profound interdependence of these to subjects.

Introduce the prerequisites for a systematic assessment and

more objective comparison of potential target firms.

Evaluate alternative business collaborations.

Be a guide for practitioners enabling them to cope with the many

difficulties attached to M&A projects and to build awareness of

common pitfalls.

1.2.2 Perspective

The addressed readers of this work are managers of acquiring firms

and consultants that need to evaluate, advice on, decide on and

conduct merger and acquisition projects.

1.2.3 Limitations

Although the following matters find their reflection in this work it is not

a guide on how to:

Conduct a due diligence

Define and review a company’s strategy

Perform a market or company analysis

1.3 Content description

The first step towards the objectives defined above is to present

various definitions and categorizations of mergers and acquisitions

10

“Fundamentals of Strategic Integration for Merger and Acquisition ”

emphasizing the multifaceted and complex nature of such

undertakings (refer to chapter 2).

On this basis, the most often reported findings of empirical post-M&A

firm performance studies are reviewed to gain insight into why certain

M&A projects fail and others succeed and to discover universally valid

performance-enhancing key success factors that do not depend on the

specific characteristics of an M&A project (refer to chapter 3).

From the results of these performance studies and the critical review

of their methodology, a broader set of motives and objectives for

mergers and acquisition activity emerges and is discussed in the light

of multiple motive M&As. In particular, an extensive overview on the

manifold classical strategic motives like synergy is presented and

illustrated with a few examples. While considering a number of motives

that receive far less attention also irrational and illegitimate motives

find their reflection (refer to chapter 4). Once this basic framework is

established, various integration and transformation concerns are

discussed like the adequate level of target firm integration, generic

scenarios and the parameters determining the level of integration. In

particular, it is illustrated how M&A projects can be compromised to

reach their objectives, if post merger management fails to realize

positive synergies and does not foresee negative synergies. Beside

strategic considerations of the integration and transformation period,

determining national and corporate cultural fit between target and

acquiring firm, results of cultural dissonance and means of anticipation

for culture clashes and are deduce d from a group of surveys (refer to

chapters 5 and 6).

From all these areas under discussion, success factors, reasons for

failure and risks of an M&A project are figured out (refer to chapter 7).

As an addition, feasible alternative business collaborations are

11

“Fundamentals of Strategic Integration for Merger and Acquisition ”

contrasted with mergers and acquisitions in terms of strategic motives

and objectives to be realized (refer to chapter 8).

As a summary, a guide to reason M&A activity in an early project phase

is developed.

Without credible answers to these basic questions, acquirers are on

their way to losing the acquisition game from the beginning even

before the due diligence or even the integration starts to happen (refer

to chapter 9).

12

“Fundamentals of Strategic Integration for Merger and Acquisition ”

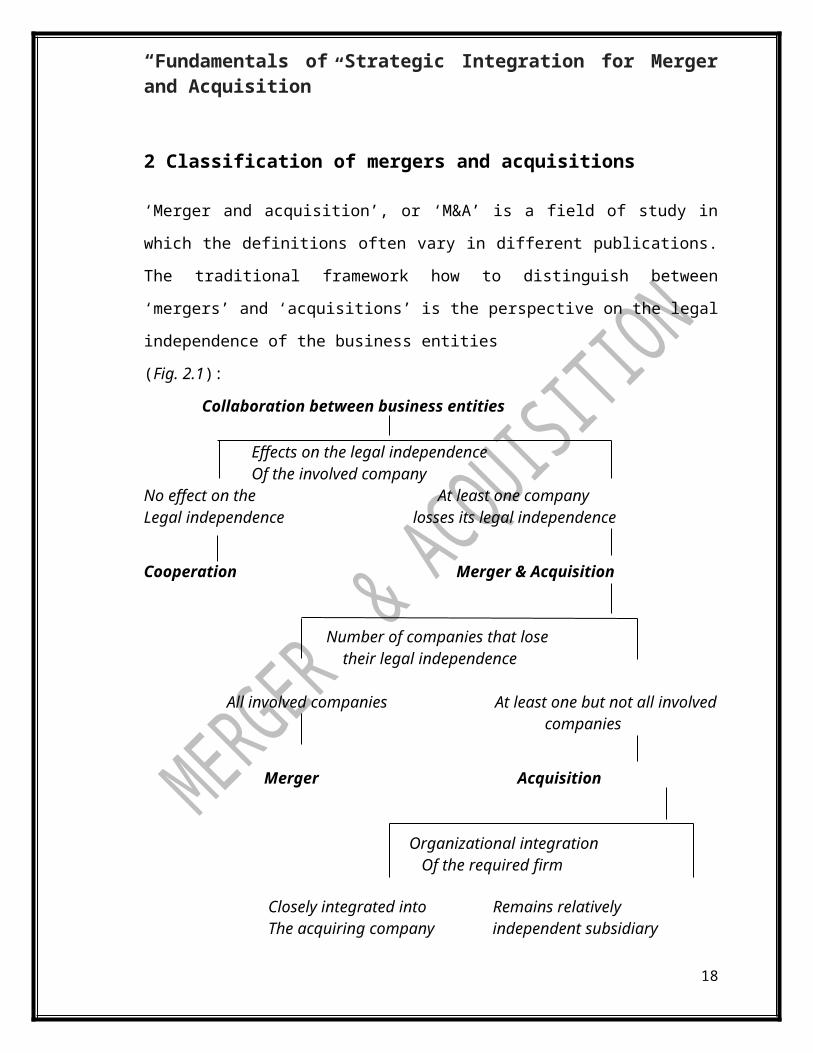

2 Classification of mergers and acquisitions

‘Merger and acquisition’, or ‘M&A’ is a field of study in which the

definitions often vary in different publications. The traditional

framework how to distinguish between ‘mergers’ and ‘acquisitions’ is

the perspective on the legal independence of the business entities

(Fig. 2.1):

Collaboration between business entities

Effects on the legal independence Of the involved companyNo effect on the At least one company Legal independence losses its legal independence

Cooperation Merger &

Acquisition

Number of companies that lose their legal independence All involved companies At least one but

not all involved companies

Merger

Acquisition

Organizational integration Of the required firm Closely integrated into Remains relatively The acquiring company independent subsidiary Of the acquiring firm

13

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Absorption Subsidiary company

In Corporate Group

Fig. 2.1: Types of collaboration between business entities categorized

by effect on legal independence (Metzenthin).

2.1 The merger

A ‘merger’ is a combination of assets of two previously separate firms

into a single new legal entity. All involved companies lose their legal

independence as all their assets become the pieces of a new firm. A

‘merger’ may be characterized by an equal rank of the involved firms

with respect to their sizes, resources and power. In this context, the

phrase ‘merger of equals’ is frequently used to refer to the equality of

the formerly independent companies. However, even when

theoretically and officially ‘mergers’ are supposed to be between equal

partners, most result in one partner dominating the other (Ghauri).

Terming the combination a ‘merger’ rather than an ‘acquisition’ thus

can be done purely for political or marketing reasons. The number of

‘real’ mergers in M&As is either way almost vanishingly small. Less

than 3% of cross border M&As by number are mergers (Ghauri).

2.2 The acquisition

‘Acquisition’ (or ‘takeover’) usually refers to a purchase of a smaller

firm or a part of a firm by a larger one. In an ‘acquisition’, the control

of assets is transferred from one company to another. The acquired

firm (target) loses its legal independence, while the acquiring firm is

not affected in that respect.

‘Acquisitions’ can be subdivided into full absorption or a subsidiary

status within a corporate group depending on the level of

organizational integration of the acquired firm (refer to chapter 5.1).

14

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Sometimes, however, a smaller firm acquires management control of a

larger or longer established company and keeps its name for the

combined firm. This is known as a ‘reverse takeover’.

2.3 Classification according to companies’ relatedness

While the traditional distinction between ‘mergers’ and ‘acquisitions’ is

mainly based on their differences in legal structure there exist many

other ways how to categorize M&As. One is to group M&As into four

categories with respect to the companies’ relatedness (Ghauri):

1) Horizontal: takes place where the two combining companies

produce similar Products in the same industry and/or are competitors.

2) Vertical: occur when two firms, each working at different stages in

the production of the same good (value chain), combine (e.g. buyer-

seller, client-supplier).

3) Conglomerate: takes place when the two combining firms operate

in unrelated businesses (unrelated diversification).

4) Concentric: occurs where two combining firms are in the same

industry (related diversification), but they have no customer or supplier

relationship (e.g. a merger between a bank and a leasing company).

2.4 Other classifications

Depending on the perspective on M&As other criteria for classification

are discussed in the literature. These perspectives are reflected in the

field of M&A performance studies (refer to chapter 3) to conclude on

the key success factors for mergers and acquisitions projects. Here, list

of some alternative classifications is given (Metzenthin; Ghauri):

15

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Management cooperation perspective:

M&As can be friendly or hostile. In the former case, the companies

cooperate in negotiations, finally agree to the transaction and ensure

that the deal is beneficial to both parties. In the latter case, the

acquiring company purchases the majority of outstanding shares of a

company in the open market while the takeover target is unwilling to

be bought or the target's board has no prior knowledge of the offer.

Stock market perspective:

‘Accretive’ mergers are those in which an acquiring company's

earnings per share (EPS) increase and/or in which a company with a

high price to earnings ratio (P/E) acquires one with a low P/E. ‘Dilutive’

mergers are the opposite of above, whereby a company's EPS

decreases. The company will be one with a low P/E acquiring one with

a high P/E.

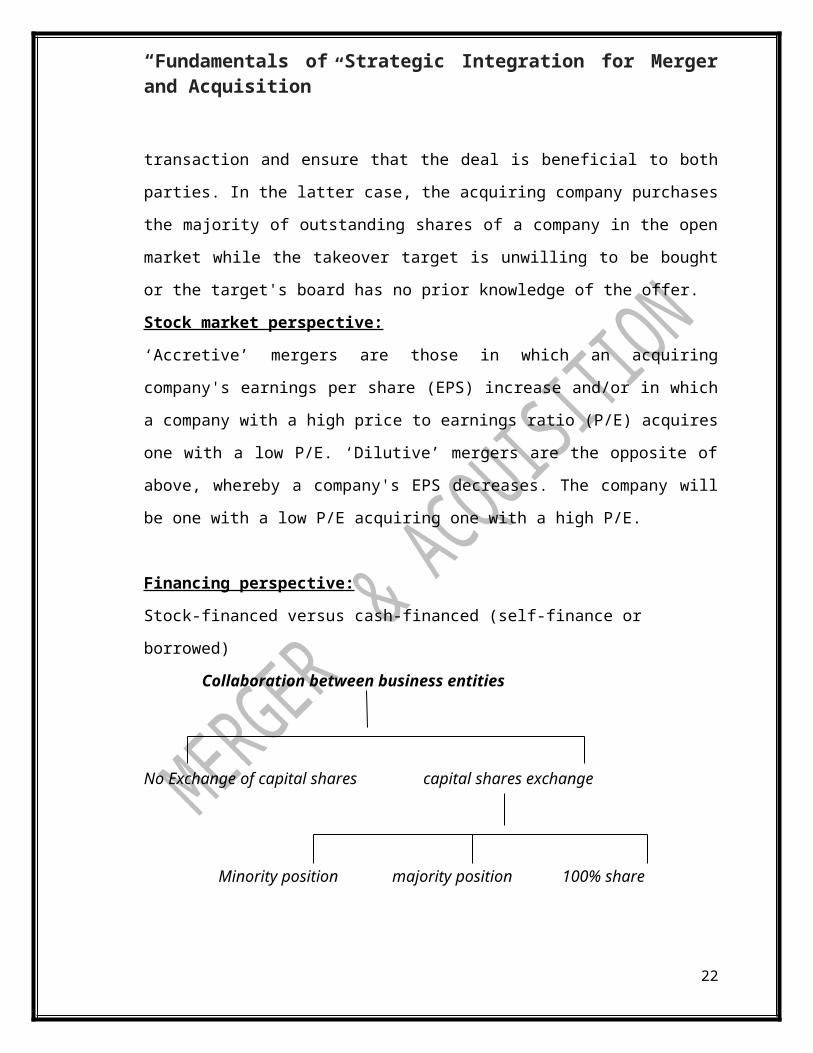

Financing perspective:

Stock-financed versus cash-financed (self-finance or borrowed)

Collaboration between business entities

No Exchange of capital shares capital shares exchange

Minority position majority position 100%

share

Fig. 2.2: Types of collaboration categorized on the basis of involved

capital investments (Metzenthin).

Market perspective:

16

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Both partners focus onto the same or different target customers,

distribution channels, technologies, products and services.

Motives perspective:

Similarity M&A versus complementary M&A

Geographic perspective:

Domestic versus cross-border M&As

Technology perspective:

Technology oriented enterprises versus non-technology firms

Strategic perspective:

Diversification (cross-industry, focus decreasing) versus concentration

(focus increasing)

Integration perspective:

Degree of loss of control or degree of integration of the target firm

2.5 ‘Merger and acquisition’ as used throughout this

work

The various perspectives on the field of M&A emphasize how

multifaceted and complex such an undertaking is. Since most of the

perspectives given above will find their discussion throughout this work

the terms ‘merger’ and ‘acquisition’ are not assigned to an specific

type of deal. In fact, the term ‘merger’ and ‘acquisition’ or ‘M&A’ is

generally used for a project where two firms (the target and the

acquiring company) combine to one legal entity or one or several parts

of a firm (target) change their belonging to the entity of the acquiring

17

“Fundamentals of Strategic Integration for Merger and Acquisition ”

firm. However, ‘merger and acquisition’ is clearly set apart from

collaborations as ‘alliance’, ‘co-operation’ or ‘joint venture’ (refer to

chapter 8).

3 Post-M&A firm performance studies

The most often researched and reported findings of post-M&A firm

performance studies are described here focusing on those being of

strategic importance in a pre-M&A stage. A critical review on

performance study’s methodology is given and other sources of

evidence are discussed.

3.1 Motivation to consider performance studies

The surveys on acquiring firms’ post-M&A performance build the vast

majority of all research studies beside those focusing on M&A

integration matters (Paine). Thus, one could assume that performance

studies provide, first, insight into why certain M&A projects fail and

others succeed and, second, present universally valid performance

enhancing key success factors that do not depend on the specific

characteristics of an M&A project.

3.2 How is post-M&A firm performance measured?

In the literature manifold ways can be found how an acquiring firm’s

post-M&A performance is measured relative to its pre-M&A

performance:

Turnover and profit growth

Relative firm value

18

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Short- and long-term stock price (event study methodology)

Abnormal stock return (difference between actual returns and

the previously

Expected returns)

Present value of the post-M&A incremental cash flows

For a more complete understanding of different types of performance

studies and their characteristics (data collection, time horizon

considered, statistical evaluation, relative performance vs. absolute

performance methodology, definition of failure and success etc.) refer

to the corresponding literature. Beside the many performance studies

also a large number of reviews can be found of which those by Sirower

and Agrawal are the most complete and most recent.

3.3 What is failure and success?

Failure has been understood in terms as extreme as ‘resale’,

‘liquidation’ or ‘divestment’, or as conservative as “failing to reach

certain projected growth or profit” in benchmarking. As a result, the

definition of failure and success depends on the performance

measures applied and thus is exceedingly broad and almost a

peculiarity of every single performance study.

3.4 Factors with and without relationship to post-M&A

performance

This work distinguishes between factors having a positive/negative

impact and factors having no significant or a highly controversial

impact on a firm’s performance. Since there is mostly no agreement on

the extent of positive or negative impact no concrete figures are given

here.

19

“Fundamentals of Strategic Integration for Merger and Acquisition ”

The findings on the factors ‘M&A activity’, ‘Diversification’ and ‘Degree

of Integration’ have biggest significance for the validation of potential

firms to be acquired and thus are discussed in more detail

subsequently to the list below.

3.4.1 Factors for which a majority of empirical studies

found a positive or negative relationship to

performance of the acquiring firm:

1. M&A activity (e.g. Dyer)

Most studies report, on average, a negative long-run performance

following

M&A deals (see a more detailed discussion subsequent to this list).

2. Acquisition premium (e.g. Epstein)

The level of the acquisition premium (price paid) has a strong negative

effect on performance across most measures of shareholder

performance. The higher the premium is, the larger the subsequent

loss. Alberts and Varaiya (in Datta) conclude that post-acquisition gains

to most bidding firms were not adequate to cover the premiums paid

to acquire the targets.

Epstein reports that even if the price paid is not public, acquiring

companies experience a decrease in stock price when the market is

anxious that the bidder will overpay for growth opportunities of the

acquired firm.

3. Multiple bidders (e.g. Datta; Goergen)

The presence of multiple bidders has a negative impact on short- and

long-term acquiring firm performance. As a result, bidding firms should

20

“Fundamentals of Strategic Integration for Merger and Acquisition ”

avoid getting involved in tender offers. The vast majority of worldwide

M&As are single-bidder auctions (more than 72%). The increased

competitiveness in such cases tends to drive up acquisition premiums.

4. Means of payment (e.g. Loughran; Goergen)

An all-cash offer for acquisitions results in better performance than an

all-equity or a combination of cash and equity. The fact the takeover

will be paid with equity might signal to the market that the bidding

managers believe that their firm’s shares are overpriced or already

expect a subsequent long-term underperformance of the combined

firms.

5. Percentage of the target firm shares acquired (e.g. Sirower)

Majority holdings in the target firm correlate positively with the

acquiring firm’s long-term performance.

6. Managerial ownership (e.g. Goergen)

The fraction of managerial ownership (e.g. through equity stakes) in

the acquiring firm is found to be strongly significant for long-term

performance. This suggests that managers are more likely to

undertake value-destroying M&A deals, if they do not own equity in

their firm.

7. Type of takeover (e.g. Loughran; Goergen)

In comparison to friendly M&A offers, hostile bids trigger large positive

abnormal returns for the target shareholders but significant, negative

returns for the bidder.

21

“Fundamentals of Strategic Integration for Merger and Acquisition ”

The overwhelming proportion of M&As are friendly. In 1999, there were

only 30 hostile takeovers out of 17’000 friendly M&As.

8. Industry phase

A study by Kröger evaluating 30’000 firms over 15 years reports

successful M&A deals in almost 60 per cent of the cases across various

industries in their opening phase (Öffnungs phase) and accumulation

phase (Kumluations phase) of his model. In the subsequent focusing

phase (Fokussie rungs phase) the success rate diminishes to 30 per

cent and even less in the balance phase (Balance phase). The reason

for this decline in success rate is seen in the decreasing realizable

synergy potential due to the raising price premiums paid for target

firms and, when the industry matures, the value chains that are

already substantially optimized in the later phases of the model.

3.4.2 Factors for which no significant relatedness to

the acquiring firm’s performance or heavy conflicting

evidence is found:

1. Stock market behavior at announcement (e.g.

Goergen)

There is little consensus about the announcement effects for the

bidding firms. About half of the studies report small value-destructive

effects for the acquirers’ shareholders (Sirower) whereas the other half

finds zero or small positive abnormal returns. Considering that the

average target is much smaller than the average acquirer, the

combined net economic gain or loss at the announcement is expected

to be rather small. However, the literature findings for target firms’

returns are much more consistent. Goergen et al. in their extensive

22

“Fundamentals of Strategic Integration for Merger and Acquisition ”

empirical study across various industries find large announcement

effects of 9% for target firms, but the cumulative abnormal return that

includes the price run-up over the two-weekn period prior to the event

rises to 20%.

2. Acquisition experience

According to Straub the number of acquisitions in the years prior to the

relevant acquisition is not significantly related to performance while

Duncan identifies a company’s previous acquisition experience as a

factor for success.

Selden et al. (in Sirower) on the other hand find that most companies

outperforming the S&P500 have low M&A activity, and if, rather small

firms are acquired.

3. Diversification (e.g. King)

Strategic relatedness does not generally outperform strategic

unrelated M&As (see a more detailed discussion subsequent to this

list).

4. Size of merging firms

There is lacking evidence on the correlation between the relative size

of the merging firms and long-term performance. Some researchers

have suggested that small mergers (mergers where the two firms are

very different in size) tend to produce higher performance than larger

mergers (mergers where the two firms are similar in size). They

attribute these performance differences to the ease of combining

operations. With smaller mergers the integration of the new entity is

more easily controlled and the disruption to the organization as a

23

“Fundamentals of Strategic Integration for Merger and Acquisition ”

whole is minimized. With a large merger, the integration problems are

multiplied and disruption can occur throughout the whole organization.

On the other hand, those researchers neglect the fact that a small

merger often provides also less significant gains to the large

organization. However, as Lubatkin and Seth point out, the few studies

that have examined this size issue have found that larger mergers, on

average, tend to be more successful than smaller ones.

5. Degree of integration

The post-merger integration level (i.e. fully integrated versus not or

partially integrated) has no relationship with a firm’s performance (see

a more detailed discussion subsequent to this list).

Many other factors exist being reported in a smaller number of

studies, as for example the pre-merger book-to-market ratio (e.g. Rau

and Vermaelen in Megginson), the premerger financial performance

(e.g. Kruse), the net cash held by the target and growth potential of

target as central factors influencing long-term firm performance of the

merged firms.

3.5 M&A performance

Success and failure with M&A deals has been studied in the vast

majority of all surveys in terms of narrow measures as given in chapter

3.2 leading to the claims that most M&As fail. Acquiring firms loose, on

average, 10 per cent of stock value in a five years period as found by

Dyer in his study across various industries. Only about 35% of

acquisitions are met with positive stock market return. According to a

KPMG study (2000), 83% of recent deals failed to deliver shareholder

value and 53% actually destroyed value. Also Porter (in Datta), based

on an analysis of acquisitions made by 33 Fortune-500 firms, concludes

that acquisitions have been largely unsuccessful when one considers

that over half were subsequently divested.

24

“Fundamentals of Strategic Integration for Merger and Acquisition ”

When gains to targets and bidders are combined, most acquisitions are

wealth creating. Although Seth et al. (in Ghauri) find that positive total

gains occur in 74% of the acquisitions they estimate in their review

that total gains are only 7.6% of the pre acquisition value of the

combined firm. From a macroeconomic point of view one can argue

that acquisitions transfer resources from less to more productive

sectors of the economy. However, bidders have only minimal or no

incentives at all to be a participant in such transactions (Datta). Ghauri

claims that more than 50% of the mergers so far have led to a

decrease in share value of the bidder firm and another 25% have

shown no significant increase. Ghauri reports that targets realize the

majority of the gains, while acquirers appear to experience positive

effects on shareholder value only in about onethird of M&As and gain

nothing on average.

In summary, the aggregate evidence from the performance literature

is toward negative performance for acquiring firms in M&A deals.

Results indicate that while the target firm’s shareholders gain

significantly from M&As, those of the bidding firm do not. Moreover,

historical evidence documents that the returns to acquirers have

gotten progressively worse, on average, for acquisitions occurring in

the 1960s, 70s, 80s and 90s, respectively (Sirower). As a conclusion

one is tempted to claim that the M&A activity itself inherently is a

reason for under-performance or failure of M&A deals. Clearly this

negative evidence raises serious doubts over the massive and still

increasing size and number of M&A deals over the last 40 years (refer

to chapter 3.8).

3.6 Diversification

There is considerable disagreement in the literature about whether

strategically related acquisitions are more beneficial than strategically

25

“Fundamentals of Strategic Integration for Merger and Acquisition ”

unrelated acquisitions. However, most publications suggest from a

theoretical point of view that corporate focus is the primary

determinant of long-term M&A performance. Continuing to focus on the

acquiring firm’s core business should help to maintain its strengths and

to minimize the risks associated with acquiring a business in an

industry of which the firm may have only limited knowledge. However,

many studies document that relatedness (focus-preserving or focus-

increasing, FPI mergers) had a marginal positive effect on long-term

performance.

On the other hand, unrelatedness (focus-decreasing, FD mergers) is

often reported to result in significantly negative long-term performance

(e.g. Megginson; Duncan). To classify corporate diversification

Megginson uses the ‘Herfindahl Index’ (HI), which describes the

merger-related degree of change in corporate focus (Megginson). He

finds that every 10% reduction in focus results in a 9% loss in

stockholder wealth, a 4% discount in firm value, and a more than 1%

decline in operating performance. These results suggest that

companies should not attempt to do what investors can do better

them, i.e. creating a diversified portfolio.

However, several authors have found no significant effect of

relatedness on performance. Some researchers even have found that

acquiring firms making conglomerate (i.e. unrelated) acquisitions

outperform those making non-conglomerate acquisitions (Sirower;

Kruse; review in Megginson). They report advantages of unrelated M&A

to be improved cash management, more efficient allocation of

investment capital and reduced cost of debt capital.

In summary, although a majority of studies have found

overperformance of related M&A deals, the evidence is very vague.

Boutellier reminds that the decision for relatedness or un relatedness

26

“Fundamentals of Strategic Integration for Merger and Acquisition ”

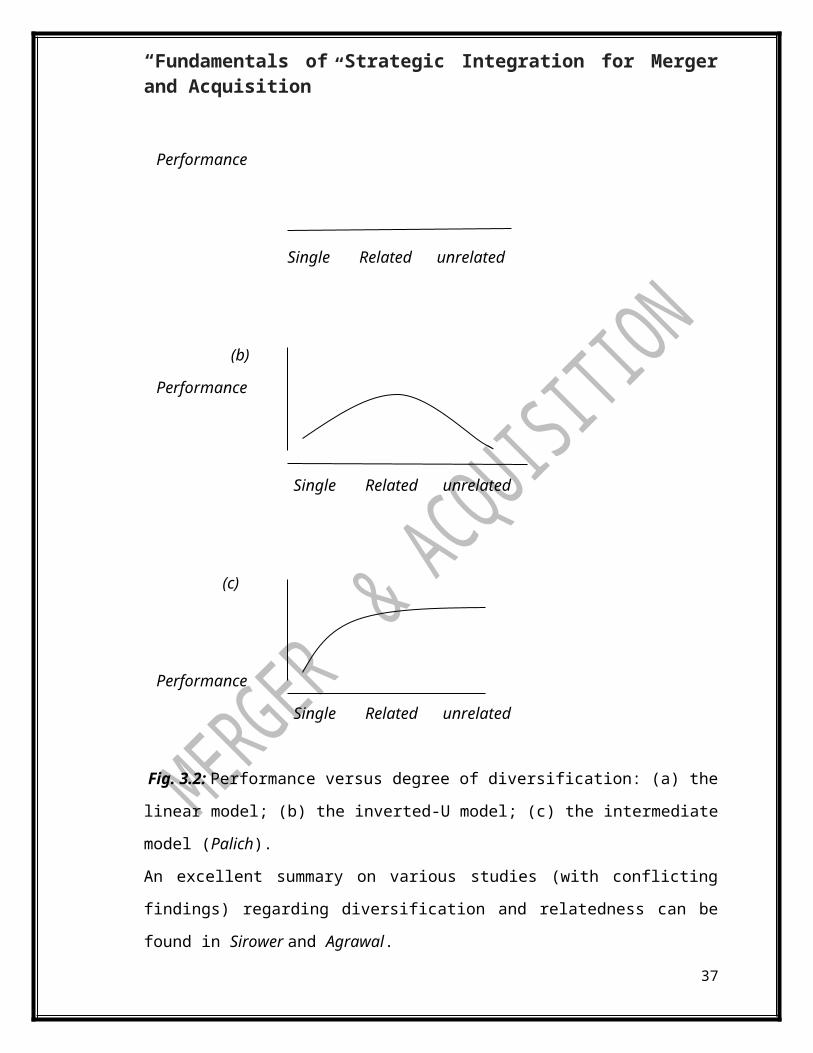

is very dependent on the industry within which the firms operate. This

matter of fact is visualized by Palich et al. (Fig. 3.2):

(A)

Performance

Single Related unrelated

(b)

Performance

Single Related unrelated

(c)

Performance

Single Related unrelated

Fig. 3.2: Performance versus degree of diversification: (a) the linear

model; (b) the inverted-U model; (c) the intermediate model (Palich).

An excellent summary on various studies (with conflicting findings)

regarding diversification and relatedness can be found in Sirower and

Agrawal.

3.7 Degree of integration

27

“Fundamentals of Strategic Integration for Merger and Acquisition ”

The finding that the degree of integration of the acquired into the

acquiring firm is a particularly interesting result because performance

gains presumably should be driven by some type of synergy realization

through integration. On the other hand, the level of integration is

assumed to be related to the number of integration difficulties limiting

the realization of the synergy potential. As a result one could conclude

that the advantages of a full or moderate integration are diminished by

the disadvantages such integration creates.

3.8 Criticism on performance study methodology

Empirical performance studies have almost exclusively concentrated

on whether M&A projects create abnormal shareholder value or

profitability for the acquiring and the target company and whether

strategically related acquisitions are more beneficial than strategically

unrelated acquisitions. The overall conclusion from hundreds of studies

is that most M&A fail. The vast majority of studies on M&A performance

in the last 40 years show failure rates for acquirers of between 40%

and 85% with an average of approximately 2/3 on a wide variety of

measures (Angwin). Despite considerable research effort being

devoted to assess M&A performance the findings of strategic

importance in a pre-M&A stage are mainly vague or inconsistent. That

fact is troubling since first, no significant success factors for M&A deals

that drive the returns can be extracted and second, a reasoning of the

findings in these studies seems to be inappropriate in the view of such

lacking evidence:

“[…] M&As’ influence on post-acquisition firm performance remains

inconclusive.

28

“Fundamentals of Strategic Integration for Merger and Acquisition ”

[…] the existing empirical post-acquisition performance studies have

not recognized any prerequisites that would be useful in forecasting

post-acquisition performance.” (Straub)

These findings raise a paradox: Why do managers continue to transact

M&A deals on such a massive scale in both number and monetary

terms, when there is little economic justification for M&As from the

bidding shareholders’ point of view? This difference between action

(the continued pursuit of mergers) and performance (the low rate of

successful mergers) are caused by:

Managers being overly optimistic, continuing to make estimation

errors in valuing target firms, thinking that they have learned

from past merger mistakes and that the next merger will be

successful (while in fact they continue to make the same merger

mistakes).

Past empirical studies being inaccurate because of data

collection, time-periods covered, statistical errors or aggregation

of different deal structures (e.g. size of merger, cross-industry

comparison etc.). Angwin states that too often M&A projects are

considered as whole homogeneous entity not taking into account

project-specific characteristics.

Managers pursuing goals other than shareholder wealth

maximization and, thus, empirical research is using an

inaccurate measure of performance (e.g. Angwin).

Some researchers raise the fundamental issue of whether the financial

markets are always best placed to value the actions of management.

For instance, a CEO embedded in an industrial context may be more of

an expert on how firms should be run and necessary investment

decisions which should be made (such as M&A) than financial analysts

and shareholders eventually far away from that context. The CEO may

take actions which may not result in positive shareholder returns in the

29

“Fundamentals of Strategic Integration for Merger and Acquisition ”

short run but could be of vital importance to the long-term success of

the firm.

Evaluation of long-term changes in stock price must be done with care

since merger strategies often require years of integration efforts

before potential benefits are reflected in stock price. And, changes in

stock price often tells little about the M&A and its motives but more

about the company overall and the economic context. If the existence

of multiple merger motives and motives other than share holder

wealth creation is correct, then past merger studies that attempt to

measure merger success by examining single financial indicators of

performance (most commonly profitability and share value) tend to

undervalue the achievement of other goals and may fail to provide an

accurate picture of M&A success. Thus, the results from performance

studies may be biased since many deals are being assessed on

motives which were never the main intention of management.

4. Motives for merger and acquisition activity

Categorization of mergers and acquisitions according to the

management’s motives is fairly generic since motives can have

manifold facets, overlapping each other or even belong to several

categories. While it is attractive to categorize M&A deals into single

motives research studies show that this would be an oversimplification.

A survey from Angwin in 2000 involving CEOs of 100 domestic

acquirers in the UK about their motivations for carrying out a specific

M&A transaction reveals up to seven reasons in some instances, 45%

gave three or more reasons and 71% of CEOs gave two or more

reasons.

30

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Angwin in his survey groups motives into four categories:

Exploitation of the target through synergies to increase acquirer

value with a high degree of certainty (classical motivation)

Exploration of new territories of latent value and for future

opportunities with low certainty of improving returns to the

acquirer but with a big potential

Preservation (‘stasis’) attempting to defend the acquirer’s

competitive situation through control of potential new competitors

Survival attempting to prevent the acquirer’s end through being

acquired itself

The payoffs for these different types of motives are different. From

‘exploitation’ deals there should be reasonable certainty about value

created. ‘Exploration’ deals may have the potential for much greater

returns than exploitation deals as well as much higher risk about

whether those returns will be achieved and how far into the future. For

‘preservation’ deals the acquirer may not receive any direct benefit,

with neutral or even mildly negative returns but the negative threat of

severe future change may be reduced.

‘Survival’ deals are not so much about increasing value as to survive

potential takeover threat or current demise of the firm. For

‘preservation’ and ‘survival’ type deals, value creation maybe an

inappropriate way of viewing performance. Instead ‘worse off test’

should be applied answering the questions “would the acquirer be

substantially worse off if it did not transact a particular acquisition?”

4.1 Exploitation (synergy motives)

Synergy motives are widely seen as the most frequently mentioned

motives when managers argue for an M&A project (Schweiger).

Synergies are accepted as a legitimate reason for such undertakings

31

“Fundamentals of Strategic Integration for Merger and Acquisition ”

since their realization appears to directly correlate with the

enhancement of economic performance of a firm.

4.1.1 What is ‘synergy’?

A target firm has an intrinsic value that is based on what a firm is

worth as a stand-alone entity. This value is typically based on the

expected stream of cash flows it can produce as a going concern. If an

acquirer pays more than this value (price premium), value is likely to

be destroyed. However, a buyer can utilize the acquisition to improve

cash flows of either the target, itself or both such that value still can be

created. This concept is known as ‘synergy realization’.

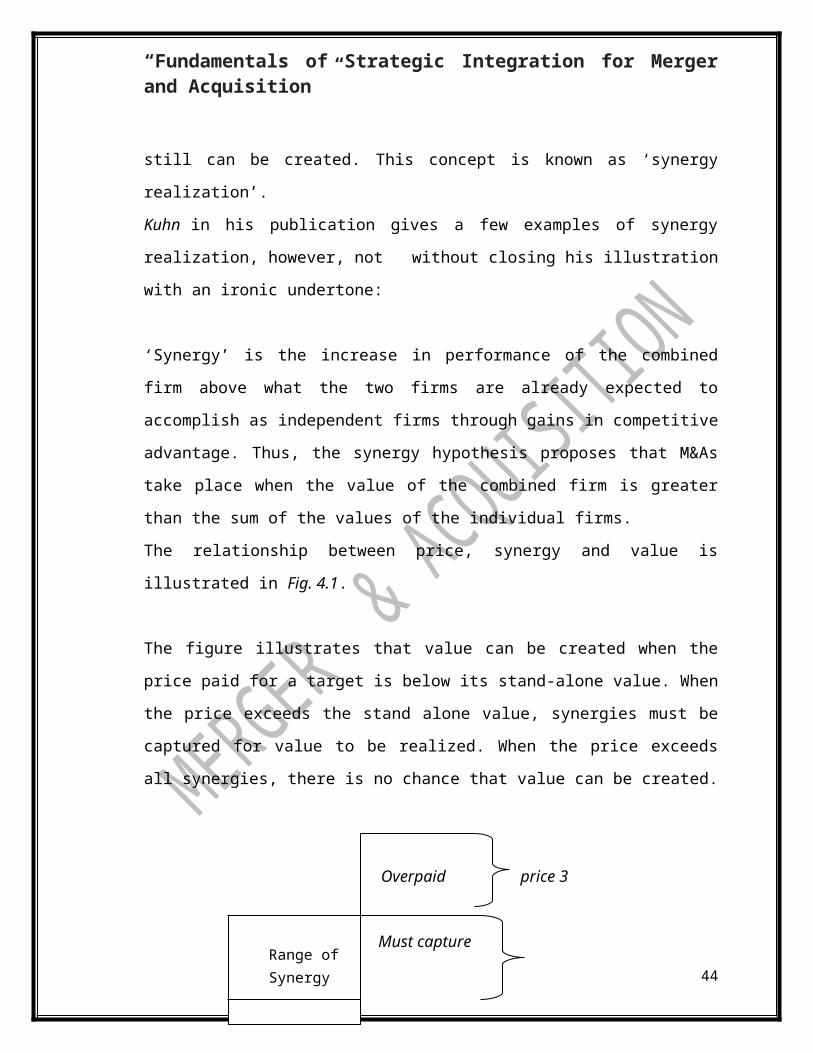

Kuhn in his publication gives a few examples of synergy realization,

however, not without closing his illustration with an ironic undertone:

‘Synergy’ is the increase in performance of the combined firm above

what the two firms are already expected to accomplish as independent

firms through gains in competitive advantage. Thus, the synergy

hypothesis proposes that M&As take place when the value of the

combined firm is greater than the sum of the values of the individual

firms.

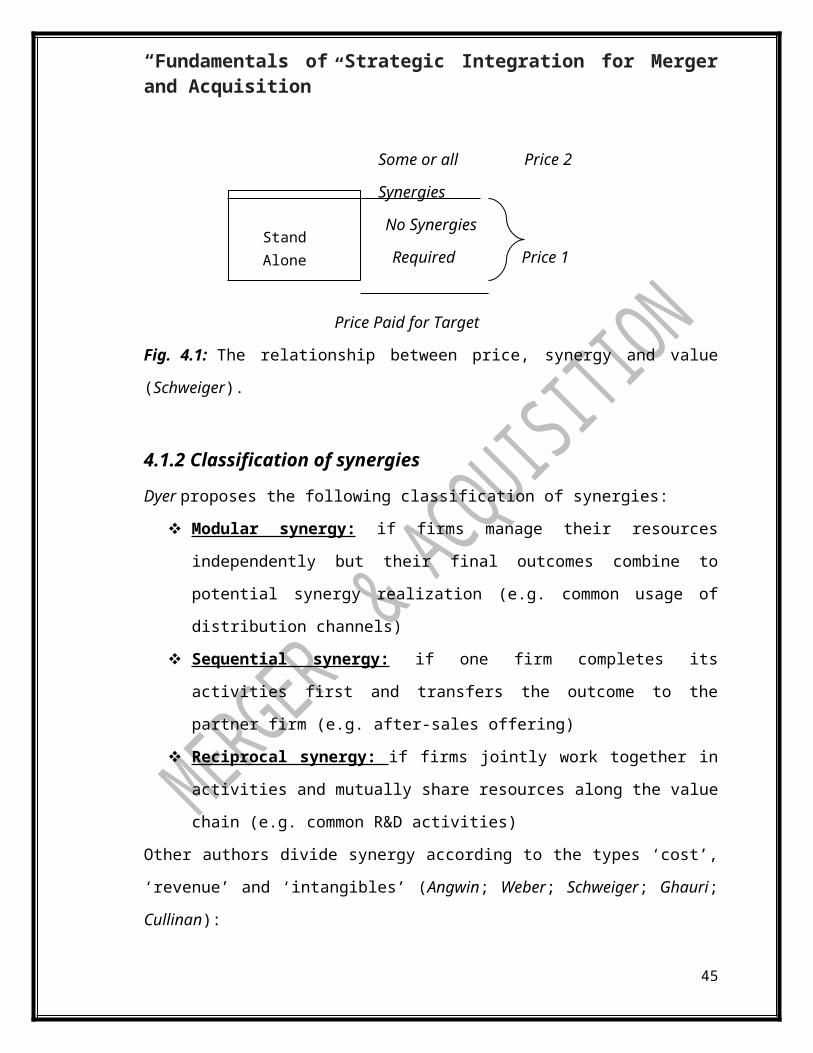

The relationship between price, synergy and value is illustrated in Fig.

4.1.

The figure illustrates that value can be created when the price paid for

a target is below its stand-alone value. When the price exceeds the

stand alone value, synergies must be captured for value to be realized.

When the price exceeds all synergies, there is no chance that value

can be created.

32

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Overpaid price 3

Must capture

Some or all Price 2

Synergies

No Synergies

Required Price 1

Price Paid for Target

Fig. 4.1: The relationship between price, synergy and value

(Schweiger).

4.1.2 Classification of synergies

Dyer proposes the following classification of synergies:

Modular synergy: if firms manage their resources

independently but their final outcomes combine to potential

synergy realization (e.g. common usage of distribution channels)

Sequential synergy: if one firm completes its activities first

and transfers the outcome to the partner firm (e.g. after-sales

offering)

Reciprocal synergy: if firms jointly work together in activities

and mutually share resources along the value chain (e.g.

common R&D activities)

Other authors divide synergy according to the types ‘cost’, ‘revenue’

and ‘intangibles’ (Angwin; Weber; Schweiger; Ghauri; Cullinan):

4.1.3 Cost synergies (‘rationalization’)

Reducing costs is one clear way to increase cash flows and has been

the most common form of synergy. If synergies are expected to come

from cost savings for price and/or cost structure competitiveness, they

33

Range of Synergy valve

Stand Alone Value

“Fundamentals of Strategic Integration for Merger and Acquisition ”

must emerge from eliminating duplication due to similarities between

the firms. Synergistic benefits from potential duplicated resources can

come as fixed or variable cost synergies:

Economies of scale i.e. increasing volume of production/sales

reduces costs per unit

Economies of scope i.e. spreading or shearing resources

across more business activities

Examples: sharing of products/services, marketing/advertising and

brand development efforts

Bargaining power along the value chain i.e. increasing

power over suppliers

(Purchasing efficiency) and distributors to reduce transaction

costs

Elimination of redundant functions i.e. reduction of

overlapping work force (administration, overhead, corporate staff

like finance, IT, human resources etc.) and rationalization of

processes

Control over value chain i.e. vertical integration Such moves

are made to increase value added into the business, to gain

control over more aspects of the business (supply, distribution)

and to reduce transaction costs in the value chain.

Examples: Lower variable costs of raw material through control

over raw materials, lower overall costs through improved product

development and manufacturing interfaces.

Flexibility of capacity i.e. using excess capacity of one firm to

fill the other firm’s excess demand (improved agility).

4.1.4 Revenue synergies

34

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Typically, revenue synergies are associated with complementary (i.e.

non-overlapping) activities resulting in higher volume and revenue

sales:

New customer base i.e. increase sales coverage or acquire

new distribution network or new sales channel that can result, for

example, in more profitable or loyal customers.

Cross-selling of products or services through complementary

sales organizations or distribution channels that serve different

geographic regions, customer groups or technologies (increased

sales productivity by selling more volume with the same number

of sales people).

Broadening a company’s products and services portfolio

to provide needed bundling or a more complete/full offering.

Internationalization i.e. increase sales volume and market

share through geographic extension and access to new

customers M&As are means to expand internationally more

rapidly or they make it possible to enter new markets using the

distribution network and the specific knowledge of local partners.

Thanks to the contributions of these partners, the foreign

company is offered a geographic presence, less effort and time

has to be put into learning how to succeed in very different local

environments (Garrette).

Internationalization can also foster a company’s responsiveness

by moving production processes, distribution, warehousing,

and after-sales activities closer to customers. This can result in

increased competitiveness by being better able to serve

customers with needs for broader geographic coverage.

4.1.5 Synergies from intangibles

This type of synergy results from the acquisition of immaterial goods or

goods that hardly can be acquired in the market:

35

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Access to brands, reputation and intellectual property

Example: increase appeal to more and better distributors,

suppliers and employees.

Access to human resources i.e. people, knowledge, experience,

skills, brainpower (talent-based M&A).

Access to technology and the attached knowledge,

innovation and product development efforts i.e. create new

business opportunities or enhance a firm’s core business.

Knowledge often cannot be acquired in the market as it is

bundled with other assets. Due to the asymmetric information

regarding knowledge and technology the valuation of this asset

is extremely difficult however important as it the key reason for

an acquisition is very often.

Access to superior managerial practices, business models and

operational excellence (e.g. quality control system, delivery

concepts, after-sales service…).

The reverse is ‘victim infusion’ (Ghauri): a firm can infuse the

‘victim’ with better management, organization skills, or superior

marketing.

4.2 Exploration

There are motives other than synergy realization which receive far less

attention:

Greenfield entry

As new markets and knowledge emerge there will always be a

need to engage in these areas. By definition there will be

significant uncertainty since acquirers cannot know the future.

They can form views about whether the potential of an M&A deal

maybe high, but in new unfamiliar areas (geographic,

36

“Fundamentals of Strategic Integration for Merger and Acquisition ”

technological etc.) the information available maybe extremely

unreliable or difficult to interpret.

Learning prologue i.e. sequential M&A to learn about a sector as

a prologue to a later larger M&A deal (e.g. a common practice

amongst Japanese firms in cross-border M&As) (Ghauri).

4.3 Preservation and survival

This type of synergy results from the elimination of competitors from a

market and to gain a more dominant position in an industry:

Affecting competitive dynamics

M&A deals can be used as a weapon to harm the actions of

competitor firms. Here performance is less about the

contribution of the target firm to the new parent, but more in

terms of the damage done to the competitor and prevention of

unpleasant challenges in an industry (e.g. Angwin; Ghauri).

Overcapacity reduction i.e. purchasing competitors and closing

them down to gain market share or critical mass

Pricing flexibility i.e. elimination of capacity from the market

place allowing an acquirer to maintain or increase prices in the

market thereby improving margins and cash flows.

Innovation quenching (Angwin)

The acquisition is intended to suppress rather than develop the

competitive potential of the acquired firm (Ghauri). For instance,

buying infant firms and closing them down prevents any possible

takeoff of that firm which could change industry dynamics. An

alternative to closure is to purchase infant firms so that the

acquirer can control the rate of innovation leakage into an

industry. Such acquisitions itself may not result in positive

returns, but may be less damaging than allowing the firm to

emerge.

37

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Competitor actions

The actions of a competitor may induce a firm into engaging in

M&A. It is known that when an industry begins to consolidate

there is a rush of other firms to follow. The motive here is the

fear of being taken over (M&A as a defense mechanism) or the

fear of no suitable targets being left for an M&A deal.

Customer / supplier pressure

Powerful customers or suppliers can force firms making M&A

deals. For instance, in the IT industry Nokia brought pressure on

one of its suppliers to purchase a high tech firm as they wanted

aspects of this technology integrated into the components they

were sourcing, but they did not want to purchase the firm

themselves. The supplier, wanting to keep its main client had no

choice. It may not have benefited from the actual M&A but to

lose Nokia as its primary customer would have been a far worse

outcome.

Political persuasion

Governments can bring substantial pressure upon top

management to act in a way which would further the national

interest. For instance, in France there has repeatedly been

pressure upon firms to merge rather than accept approaches

from Italian, Spanish and Swiss firms.

4.4 Managers’ self-interest and prestige

All of the above motives for M&A assume rational managerial

motivation based upon improving firm performance. However, not all

motives can be considered rational from the business perspective:

‘Agency’ motive (self-interest, greed motive)

38

“Fundamentals of Strategic Integration for Merger and Acquisition ”

In the context of M&A the agency motive suggests that

takeovers occur because they enhance the acquirer

management’s welfare at the expense of acquirer shareholders

(e.g. Angwin; Brouthers).

Hubris motive (prestige motive)

The hubris hypothesis suggests that managers make mistakes in

evaluating target firms (excess confidence) and engage in M&As

even when there is no synergy potential or other legitimate

motive (Berkovitch). Diversification of management’s personal

portfolio, managerial challenge, the increase of the firm size and

prestige, the increase of the firm’s dependence on the

management (empire building) and fashion (Ghauri) are

manager motives summarized under the hubris hypothesis.

The agency problem and hubris motive receive support from studies

reporting that acquirer returns from M&A deals are positively related to

the level of management ownership in the acquiring firm (Berkovitch;

refer to chapter 3.4.1).

Considering the increase in shareholder wealth as the primary reason

for any M&A and taking into account that most M&As fail, Berkovitch

jumps to the conclusion that many M&A deals are motivated by agency

and hubris. However, the huge variety of motives different from

shareholder wealth creation as the primary motivation for M&A puts

some doubt on that straight conclusion. “If all takeovers were

motivated by synergy only, one would never observe negative gains.”

Here, Berkovitch does not take into account that there are many other

issues except the motivation that decide upon M&A financial success.

4.5 Finance motives

The main motives cited in the finance literature:

39

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Improving stock market measures (classical motive referred as

‘exploitation’ or ‘synergy’ motive)

Reducing cost of capital (e.g. through reducing firm risk by

stabilizing earnings due to diversification or buying a listed

company)

Reduction of tax liabilities (e.g. through benefits achieved in

cross-border M&As)

Adjusting the debt profile of the company

Accessing cash or other financial resources in the target

company

Generate cash flow from the break-up of the target firm (e.g.

Megginson)

Move capital to higher valued uses / Reinvestment of financial

resources (e.g. firms with poor investment opportunities acquire

firms with outstanding growth opportunities; Goergen), in the

extreme case: Replace a business with a new one (respond to

market failures)

Asset stripping

Speculative transactions driven by the intention to buy shares in

companies solely to resell them at a profit in future.

The vast majority of M&A literature assumes that M&A deals must

improve returns to shareholders. However, this ignores many other

‘legitimate’ and ‘illegitimate’ motives for M&A activities and ownership

structures other than public companies. The broad set of\ motivations

presented here now, first, allows a much more subtle assessment of

post-

M&A firm performance while the lack thereof was criticized in the

chapter ‘Performance studies’ (refer to chapter 3), second, simplifies a

sound review of strategic logic and reasoning for M&A activity and,

40

“Fundamentals of Strategic Integration for Merger and Acquisition ”

third, opens a much broader view on upcoming integration and

transformation difficulties like negative synergies and culture issues.

5 Post-M&A integration and transformation

Independent of the underlying motives for an M&A project, during post-

merger integration many different matters must be carefully blended

such as for example different strategies, brands, product portfolios,

production processes, knowledge and technology, pricing policy,

support functions, sourcing and distribution partners, administrative

policies and processes including the management of human resources,

technical operations, marketing activities and customer relationships.

Depending on the level of integration such a blending imposes many

difficulties and pitfalls for synergy realization and for reaching other

M&A objectives. The lacking awareness of those difficulties (fostering

positive synergy realization and anticipating negative synergies) are

seen as prominent reasons why M&A projects can be compromised to

41

“Fundamentals of Strategic Integration for Merger and Acquisition ”

reach their goals, in particular when not considered at a very early

stage in the M&A project (e.g.Datta; Haspeslagh). Mace and

Montgomery already noted in 1964:

„The values to be derived from an acquisition depend largely upon the

skill with which the […] problems of integration are handled. Many

potentially valuable acquired corporate assets have been lost by

neglect and poor handling during the integration process. “

As a consequence, besides recognizing the strategic logic that predicts

value creation the processes through which the M&A’s objectives come

to be realized must be taken into account and planned in detail.

Management must find the appropriate integration practice (e.g.

procedural, physical, and socio-cultural) given the motives and

characteristics of the acquiring and acquired firms (Marks).

5.1 What is an adequate level of integration?

There are several possible generic scenarios how a company can be

integrated in the post-M&A phase (Sirower; Duncan), although, hybrid

and intermediate forms may exist:

1. The company is acquired as a stand-alone (total autonomy).

2. The company is acquired as stand-alone but with a change in

strategy (e.g. restructuring followed by financial control).

3. The target company is to become part of the acquirer’s operations

(e.g. centralization of key functions).

4. The target and acquirer are to be completely integrated (full

integration).

5. The target takes over the acquirer’s existing business and the

acquirer is integrated into the target’s operations (reverse integration).

42

“Fundamentals of Strategic Integration for Merger and Acquisition ”

5.2 What are the difficulties and dangers during

integration?

Difficulties and dangers during the integration process are manifold

and widely discussed not only in the M&A literature but generally in the

transformation literature. Here the most often cited issues in the M&A

context and those of major relevance for the pre-M&A phase are

discussed. To foster a positive attitude in an often negatively charged

environment success factors are presented instead of a list with

frequent reasons for integration failure (no particular order):

a. Choice of appropriate level of integration

(2)Post-merger management of projected positive and negative

synergies

(3)Speed of integration

(4)Communication to internal and external stakeholders

(5)Cultural fit and anticipation of culture dissonance

(6)Experience with transition structures and transformation

management (Reimus)

(7)Avoidance of leadership vacuum (Duncan)

(8)Choice of top management positions reflecting the values being

applied in the merged firm and the true distribution of power

between the former firms (Trauth).

(9)All parts of the organization have the knowledge and resources,

and give their commitment for the integration efforts (Epstein).

5.2.1 under- and overintegration – or the appropriate level

of integration

An acquired firm must be aligned to a certain extent to the

requirements of the acquiring company. The accomplishment of

43

“Fundamentals of Strategic Integration for Merger and Acquisition ”

integration, however, requires that target-specific bases of critical

resources and skills be kept intact. The organizational task therefore is

the preservation of any unique characteristics of an acquired firm that

are a source of key strategic capabilities. Pablo advises against “fixing

things that aren’t broken”.

However, under- or overintegration has been cited as one of the

leading causes of M&A failure (Pablo). The realization of potential

synergies can be short-circuited given an insufficient level of

integration, but excessive integration (reconfiguration) can hinder the

development of fruitful conditions (e.g. when executives depart,

expertise is lost etc.).

Management of the acquiring firm has the tendency to over-integrate

the target firm, means to completely change the whole setup and the

processes. These practices (besides demotivating the employees) can

result in the loss of the firm’s success factors before the M&A deal

5.2.2 Post-merger management of projected positive

and negative synergies

Acquiring companies must view potential synergies in the light of

realization problems:

“When two previously sovereign organizations come together under a

common corporate umbrella, the result is a hybrid organization in

which value creation depends on the management of

interdependencies through the facilitation of firm interactions and the

development of mechanisms promoting stability.” (Pablo)

Specifically, management should:

44

“Fundamentals of Strategic Integration for Merger and Acquisition ”

Have an integration plan in considerable detail on how to

implement the strategy (e.g. integration of sales force,

distribution system, information systems, R&D processes,

marketing efforts, reward and incentive systems).

Examine how different issues impact the success of changes

needed in the acquirer, the target, or both firms and the impact

they can have on positive potential but also negative synergies

(value leakage e.g. through reduction in cash flows and earning

during integration period).

Develop different integration scenarios leading to a series of

realistic M&A evaluation.

5.2.3 Speed of integration

Angwin in his studies argues:

“[…] the first 100 days is when all the critical actions should be

launched, as this is the outer limit of employee enthusiasm, customer

tolerance and Wall Street patience”.

Early wins to convince internal and external stakeholders keep the

momentum of positive attitude while sustained uncertainty, not only

amongst employees, is seen as one of the most corrosive elements of

the soundness of post-acquisition integration.

Faster integration may reduce the length of time to experience

uncertainty as well as reduce the effects of the rumor mill.

An organization, Angwin then argues, benefits from well planned and

thus shorter integration periods in several ways:

Spending less time in a sub-optimal condition

Less costly readjustments and iterations

Cuts time for competitors’ reactions to the new organization

Favorable response of financial markets to quick wins

45

“Fundamentals of Strategic Integration for Merger and Acquisition ”

5.2.4 Communication to internal and external

stakeholders

The preparation during the period leading up to the merger

announcement is vital to success since it is critical to present the

merger to key constituencies with confidence.

During this period, the integration process is formulated and key

decisions should be made in the areas of leadership, structure, and

timeline. Unprofessional communication to employees, clients,

shareholders, suppliers and the media fosters uncertainty, mistrust

and rumors. Thus, it is necessary that the companies and their

stakeholders involved understand the advantages associated with the

merger.

The communication should generate a culture where employees see

the merger as enabling them to develop the business rather than

inhibiting them from progress.

Employees then can concentrate on reaching the objectives of the

whole M&A project or the integration process in particular.

Management must define the necessary changes that will bring a

successful transaction. It is important to establish clarity in roles and

responsibilities for those involved in the integration process, versus

those in operating businesses. And, the final authority and

responsibility should be communicated on all levels.

This chapter on ‘communication’ passes into to the subject of ‘culture

dissonance’ since Communication is an inherent part of culture and

lacking or unprofessional Communication shares the same set of

human reactions to culture dissonance.

46

“Fundamentals of Strategic Integration for Merger and Acquisition ”

5.2.5 Cultural fit and anticipation of culture

dissonance

For Ansoff citing Machiavelli “[…] resistance to change is proportional

to the degree of discontinuity in the culture and power structure

introduced by the change”. Resistance comprises cultural and social

aspects, at both the individual and collective level.

Culture dissonance, which might be real or just perceived, is a major

risk for M&A integration success and thus is widely discussed in the

literature and is treated in a separate but complementary chapter in

this work (refer to chapter 6).

6 National and organizational culture and culture

clashes

Numerous authors have discussed the potential troubles of culture

dissonance (culture clashes) between merging organizations and

report culture dissonance to be one major source of conflict that can

undermine potential synergistic effects and endanger a whole

M&A project. Duncan found that 65 per cent of those acquirers who

had experienced serious problems with post-acquisition integration

said that these difficulties had been due to cultural differences.

Cultural fit is therefore a vital success factor for international and

domestic M&As. The interesting point is that many studies show that

47

“Fundamentals of Strategic Integration for Merger and Acquisition ”

culture is an important issue even when the firms come from the same

country and the same industry Ghauri). On the other hand, culture

issues are worth to shed light into them since they can be used as

almost uncontroversial alibi for anything that goes wrong with M&As

(Sirower).

6.1 What is culture in the M&A context?

There exist various definitions of ‘culture’, but a classic definition is a

“shared set of norms, values, beliefs, and expectations” which are

translated into behaviors. A ‘corporate culture’ includes this shared set

but also implies incentive and reward systems, performance

evaluation, chain of command, leadership styles, information and

decision processes, operating procedures etc. (Veiga).

However defined, organizational culture is seen as being important in

determining an individual’s commitment, satisfaction, productivity, and

permanence within an organization. This is because individuals tend to

select groups that they perceive as having values similar to their own

while trying to avoid dissimilar others (Veiga).

6.2 Which forms of acculturation exist?

Similarly to the possible integration scenarios (refer to chapter 5.1)

Jöns defines different degrees of acculturation between the acquiring

and acquired firm while the degree of integration and degree of

acculturation do not necessarily correspond to each other. This is due

to the fact that the acculturation depends on the way companies

manage the formal (organizational aspects) and informal (socialization

aspects) integration process:

48

“Fundamentals of Strategic Integration for Merger and Acquisition ”

1. Integration is characterized by cultural and structural changes on

the part of both partners without a dominant culture.

2. Assimilation is a one-sided process where the acquiring company

fully absorbs the acquired one.

3. Separation means minimal cultural exchange; the acquired