the future of wind energy in denmark - reducing the … · the future of wind energy in denmark -...

TRANSCRIPT

The Future of Wind Energy in Denmark - Reducing the Cost and Increasing the Value of Wind

Martin Risum Bøndergaard

Policy Advisor – Energy and Economy

Danish Wind Industry Association

IEA Report Launch: Cost Reduction for Onshore Wind – Status and Perspectives

Copenhagen - 15 June 2015

Every wind power project is unique

• When communicating about LCOE it’s important to keep in mind that each wind power project is unique

• Significant variation in LCOE between projects within as well as between countries

• Important that framework conditions also in the future allow for utilization of the wind energy resources on relative low wind sites.

• That said it is cost effective to prioritize deployment on low cost locations

• Denmark has some of Europe’s best and cheapest wind energy locations.

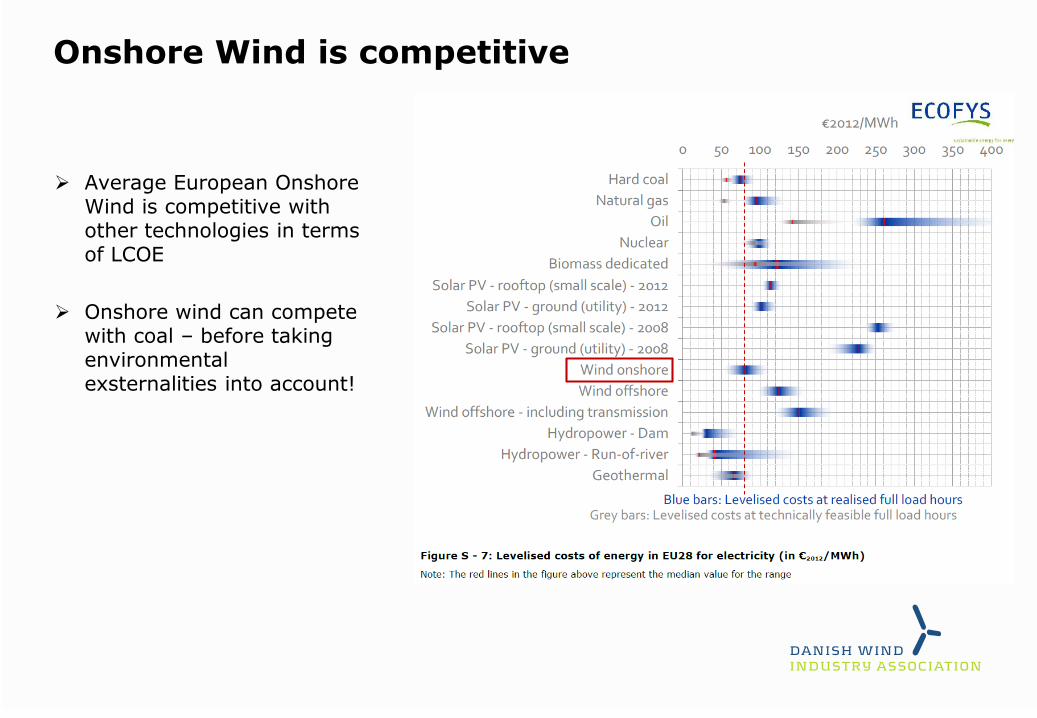

Onshore Wind is competitive

Average European Onshore Wind is competitive with other technologies in terms of LCOE

Onshore wind can compete with coal – before taking environmental exsternalities into account!

Denmark has the cheapest Wind Power in Europe

Report by ECOFYS for the EC in 2014

This is confirmedby todays IEA Wind report with respectto the includedcountries

Source: IEA Wind Task 26 – Wind Technology, Cost, and performance

Trends in Denmark, Germany, Ireland, Norway, the European Union, and

the United States: 2007-2012

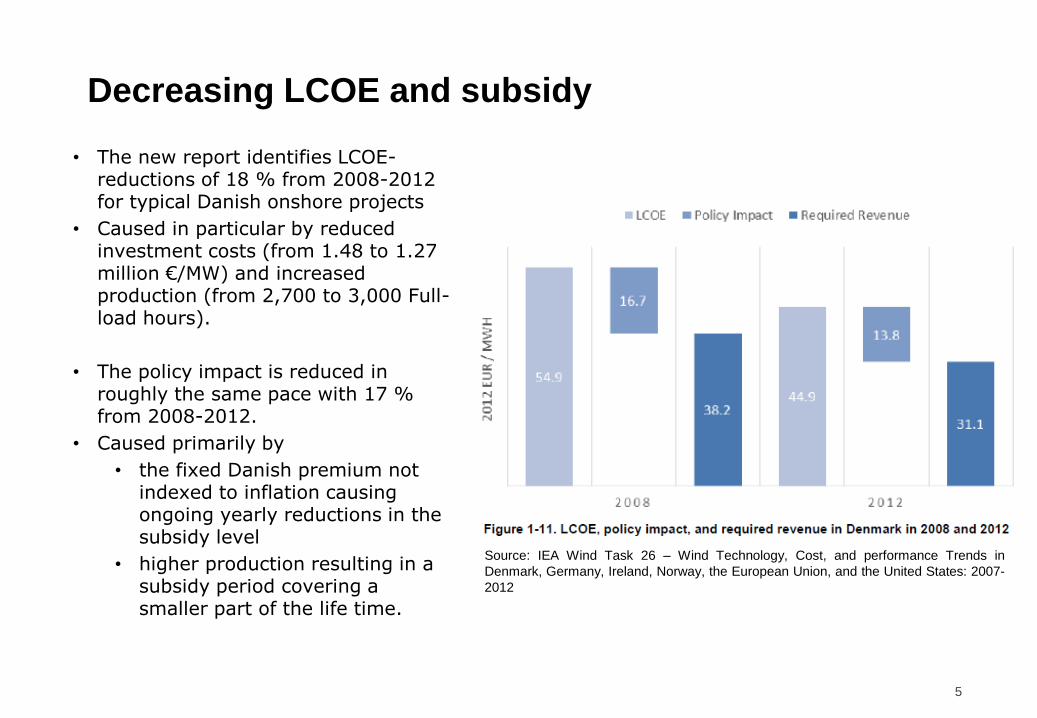

Decreasing LCOE and subsidy

• The new report identifies LCOE-reductions of 18 % from 2008-2012 for typical Danish onshore projects

• Caused in particular by reduced investment costs (from 1.48 to 1.27 million €/MW) and increased production (from 2,700 to 3,000 Full-load hours).

• The policy impact is reduced in roughly the same pace with 17 % from 2008-2012.

• Caused primarily by

• the fixed Danish premium not indexed to inflation causing ongoing yearly reductions in the subsidy level

• higher production resulting in a subsidy period covering a smaller part of the life time.

5

Source: IEA Wind Task 26 – Wind Technology, Cost, and performance Trends in

Denmark, Germany, Ireland, Norway, the European Union, and the United States: 2007-

2012

Current subsidy scheme is well functioning

As of January 2014 the Danish subsidy scheme was reformed:

• Maintaining the nominal premium level at 250 DKK/MWh (33.5 Euro/MWh) –not indexed to inflation

• FIP period now primarily depending on rotor size - incentivizing lower specific power (W/m2) and thus contributing to reducing the system integration cost

• Introduction of nominal price cap on the sum of the market price and premium of 580 DKK/MWh (77.8 €/MWh) – If electricity prices increase to above 44.2 €/MWh consumers get the up side.

• Overall the current Danish subsidy scheme is well functioning.

High exposure to electricity market prices

What we have seen since 2008 is a 40-50% decrease in electricity prices in Denmark (DK1 and DK2)

Only thanks to the cost reductions the Danish onshore market still holds a sound climate for investment

If electricity prices hadn’t plummeted it would have been possible to reduce the subsidy level also in nominal terms.

Onshore wind in Denmark is highly exposed to variations in the power market price:

Fixed premium resulting in variable revenue streams fluctuating with the market price

Short subsidy period of 6-8 years –2/3 of lifetime only receiving the market price

Increasing price gap

• When controlling for potential subsidy scheme overcompensation (Financial Gap) you can not simply use the same method across countries and electricity markets.

• In markets with high wind penetration it is important to take into account that the realized power price for wind turbines is below the average market price.

• We are seeing tendencies to increased price gap

• System modelling suggests that the price gap will increase (In Denmark from around 10 % today to between 15-30% in 2030).

Increasing the Value of Wind

If we want to phase out the support for onshore wind we need to succeed in increasing the value of wind.

Two steps are needed:

1) Domestic electrification – Creating an intelligent energy system

• We need to improve our domestic utilization of the wind energy

• Especially electrifying the heating sector by using heat pumps – individual as well as in district heating systems. Heat pumps in relation to existing gas CHP plants create both flexible power plants and flexible demand.

• Electric vehicles etc.

2) Integrating European electricity markets is the cheapest way to a sustainable and secure energy supply

• The continued deployment of wind has to be followed by better market integration – Both in terms of hardware (Interconnectors) and software (Market design)

• It is always windy somewhere. Connecting wind power across geographical distances allowing for cross-border balancing is the obvious way to minimize needs for expensive back-up capacity.

• Therefore market integration is a precondition for a cost-effective maximization of the possible and adequate wind energy share in the future energy system.

Significant steps in this direction can and should be taken within the next 5 years

Danish Wind Power Perspectives – Current Energy agreement

0

10

20

30

40

50

60

70

0

1000

2000

3000

4000

5000

6000

7000

%MW Danish wind capacity and wind power share 1990-2021

Onshore Offshore Wind power share of total electricity consumption

60 pct. wind by

2021

What about post-2020?

Do we really believe that we can run an entire society on wind energy alone? – No, of course not!

The Danish Energy Transition has only just begun

In 2020 Wind power is expected to provide about 8% af the entire energyconsumption.

Further wind energydeployment is needed post-2020!

DWIA’s vision: At least 20% by 2030

Which path to choose post-2020?

• 100% RES can be reached in different ways – 2 main scenarios are the biomass-based and the wind energy based.

• Denmark is a small country with high interconnectivity.

• No matter what Danish politicians prefer – Denmark is already in a high wind penetration area. This will only increase in the coming years.

• As shown in the ‘Energy Concept 2030’:

• It’s a ‘no regrets option’ for Denmark to design an energy system that is capable of utilizing the huge volume of wind energy in the Nordic system.

• To optimize the value of these investments it’s a rational choice for Danish politicians to continue along the wind energy path post-2020

• Denmark should continue to go for both on- and offshore wind energy.

• Onshore wind can not cover the needed volume in the long term so development of offshore wind should be prioritized in order to bring down cost.

• Onshore is cheapest -> potential should be utilized as much as publicly acceptable.

• We welcome the analysis carried out by Energinet.dk finding a technical potential of 12.000 MW – but the question is what is the publicly acceptable volume ?

• Size of the potential is determined by the planning regulation.

Planning regulation can constrain onshore potential and LCOE-reductions

Minimum distance to the nearest neighbour is 4 times the total height of the turbine

If the distance should be increased then the onshore potential is reduced and the expenses to acquisition of houses and thus the LCOE will increase.

If noise regulation is tightened e.g. with requirements leading to constrained production at night time then the LCOE will go up.

Due to current environmental and civil aviation regulations wind turbines in Denmark are limited to a maximum total height of 150m.Elsewhere in Europe there is a trend towards taller turbines. If the Danish regulation is not adapted to this trend, it will put constraints on the future cost reduction potential

LCOE will continue to drop as a result of technology improvements and increased industrialization and economics of scale – but the planning regulation can constrain this

Thank you for your attention

Martin Risum Bøndergaard

Policy Advisor – Energy and Economy

Back up slides

Energistyrelsen juli 2014: Vind er billigst!

LCOE resultat og sammenligning

0

5

10

15

20

25

30

35

40

45

IEA 2008* IEA 2012* EA energianalyse2014

Energistyrelsenteknologikatalog

2015

Energistyrelsenteknologikatalog

2020

øre

/kW

h (

20

14

)

LCOE estimater for landvind 2008-2020

*IEA 2008 og IEA 2012 er opgjort i 2012-priser

Hvorfor faldende pris i DK og hvorfor DK billigst?

DK have experienced decreasing investment cost because of:

1. Technology improvements / more effective tyrbines

2. Improved competition between OEM’s and in the value chain

3. Trend towards larger projects with more turbines

Om hvorfor DK har lavere investeringsomkostninger end andre lande:

1. One possible reason is that Denmark have very easy locations in terms of logistics and geotechnical conditions (no need for high towers in forrest and easy transportation)

2. Could also be due to differences in national subsidy schemes

PricesModTrans xx €/MWhHighTrans xx €/MWh

High RES and High Transmission

High RES deployment creates low prices to the benefit of consumers

High Transmission scenarios lead to price convergence / Higher prices in the Nordics. The advantage is a better utilizationof RES and that wind energy in the nordics will need less support

Resource sharing across regions for back-up and ancillary services – the possible need for capacity mecanisms / support to thermal power plants to act as back-up will be reduced.

2530

2830

3131

5151

4246

High RE

The Wind Industry is bringen down cost

We need stable political frameworks

• Stady hand on the weel – avoid sudden disruptive policy changes – ‘stop-go’ policies

• A market size allowing for economies of scale as well as healty competition – especially important for offshore wind energy

• A level playing field – fase out fossil fuel subsidies and implement the poluter pays principle (CO2-emisions, general airpolution etc. But also water consumption, land use and biodiversity loss etc.)

• In many markets wind energy is already competitive

• Integrated energy markets …