the global commodity trade finance industry report

TRANSCRIPT

The Global Commodity Trade Finance Industry Report

2 |

© TXF Limited 2020

The contents of this publication are protected by copyright. All rights reserved. The contents of this publication, either in whole or in part, may not be reproduced, without written permission of the publisher. The information set forth herein has been obtained from sources which we believe to be reliable, but this is not guaranteed. This publication is provided with the understanding that the authors or publisher shall have no liability for any errors, inaccuracies or omissions therein and, by this publication, the authors and publisher are not engaged in rendering consulting advice or other professional advice to the recipient regarding any specific matter. If consulting or other expert assistance is required regarding any specific matter, the services of qualified professionals should be sought.

The Global Commodity Trade Finance Industry Report

| 3

The Global Commodity Trade Finance Industry Report

4 |

ForewordI am delighted to present to you the 2020 edition of the TXF Research’s Global Commodity Finance Industry Report.

Through a difficult 2020, the TXF Research team has worked tirelessly to continue to invest in and bolster our research, and to make this survey not only more inclusive but as reflective of the fluctuating market as possible.

The commodity market since the end of last year has probably been through one of the toughest times we have seen in recent years. From my point of view, not since 1998 have I witnessed so many negatives impacting the market as a whole. At the end of 2019 we saw problems emerging with some of the smelters in China, but this was then totally dwarfed by the impact of the collapse of some of the local Singaporean commodity traders – most notably Agritrade International and Hin Leong. Then we also saw the dramatic collapse of Phoenix Commodities in Dubai.

The market has been hit by fraud and alleged fraud cases, which have impacted a significant number of banks considerably. There are many lawsuits in progress, and probably many more in the pipeline. Legal firms will be inundated. The impact has been significant, and a number of banking commodity units have closed, and numerous job losses have occurred at several leading banks.

Beyond this, earlier this year we saw the dramatic collapse in the crude oil price, and elsewhere dramatically increased volatility in commodity prices overall. In addition, commodity flows and prices continue to be impacted by the US-China trade war, sanctions, the random imposition of tariffs and of course China’s purchasing appetite. Some of these trends are revealed within this research report. But many other factors have also come to the surface.

As many people work remotely through the Covid-19 restrictions, compiling this report has arguably been challenging. Nevertheless, we have had some excellent responses across the commodity spectrum. Some 130 respondents have provided input, along with qualitative insights from 10 interviewees and market data using the TXF Data tool.

Thank you to everyone who spoke to us and took the time to input into the survey this year. Commodity finance is a niche business, but we at TXF have always felt that there is an opportunity for the product to play a more central role to a range of institutions, policy makers and the real economy in general.

With its independent position within the market, TXF continues to hone the intelligence it can provide, and ensure it is business critical information for our clients and the market in general.

Please do get in touch with your thoughts, and together we can continue this journey, and ensure commodity finance is publicised, scrutinised and analysed to an increasingly high standard in the years to come to help you take your business forward successfully.

We hope you enjoy the report.

Editor-in-Chief & Director

TXF

The Global Commodity Trade Finance Industry Report

| 5

ContentsExecutive summary 6Introduction 8 The perfect storm 8 Aims and objectives 9 Methods 9 The survey 9 The interviews 9

Findings 11 Background and demographics 12 Afocusedlookatthecommoditytradefinanceindustry 17 Past and present activity 18 Sustainability: climate change or climate colonialism? 20 Getting to grips with compliance and regulation 25 No more libor 26 Securities Financing Transactions Regulations (SFTR) 28 EU Benchmarks Regulation 29 Senior Management Certification Regime (SMCR) 31 The Covid-19 catalyst 35 “Uncertain, unprecedented and unbelievable” 36 The impact of Covid-19 on the commodity trade finance banks 39 Aforensiclookatthecommoditytradefinancebanks 41 A closer look at the financials 42 Basel and the banks 43 A growing threat from alternative finance? 47 Or a threat from global traders? 48 An insight into the traders’ and producers’ world 51 A growing need for alternative finance 52 The commodity trade finance banking heatmap 54

Concluding comments and recommendations 58List of figures 60Bibliography 62About TXF Research 64Acknowledgements 64

The Global Commodity Trade Finance Industry Report

6 |

Executive summaryThe Global Commodity Trade Finance Industry Report 2020 is based on data collected using a mixed methods design that combines quantitative data from 130 survey respondents spanning advisers, banks, brokers, law firms, private insurers, traders and producers with qualitative insights from 10 interviewees.

Over the next 12 months, 62% of the respondents said that they are going to become more active in the metals and mining industry, compared to 27% in agri/softs and energy/petrochemicals.

Views on sustainability are somewhat divided, with nearly half of the banking respondents, and a third of the traders and producers, showing an unwillingness to sacrifice economic returns in favour of ensuring deals remain sustainable.

Awareness of the new risk-free rates replacing LIBOR is relatively poor. Additionally, 53% and 57% of the total sample are unaware of the latest Securities Financing Transactions Regulations and EU Benchmarks Regulation, respectively.

2 3

1

The Global Commodity Trade Finance Industry Report

| 7

85% of the total sample think that Covid-19 will lead to a reduction in the availability of credit, with 68%, 56% and 54% of the sample citing cost of bank debt increases in agri/softs, energy/petrochemicals and metals and mining, respectively.

Structured commodity trade finance facilities are set to see a small increase over the next 12 months, particularly in pre-export financing, borrowing base loans, prepayment financing and reserve-based lending.

4

5

51% of the traders and producers noted that they are currently accessing alternative forms of finance, driven by an inability to access bank debt or because the cost of bank debt is too high.

6

The Global Commodity Trade Finance Industry Report

8 |

IntroductionThe perfect storm

“The commodity trade finance sector in 2020 has been hit by the perfect storm. Wave after wave of Covid-19, fraud, oil prices plummeting below $0 and a liquidity crisis have smashed the industry… I

imagine that no one will emerge unscathed from it.”

It is not normal practice to start a report with a qualitative quote from someone who took part in the research, but this year has been anything but normal. So much has been written on the trials and tribulations of the commodity trade finance industry in 2020, with adjectives such as ‘uncertain’ and ‘unprecedented’, exhausted across the ether. But the quote by the trader neatly sums everything up in one phrase – a perfect storm

Unexpected high-profile fraud cases, including Hin Leong, Agritrade International, ZenRock Commodities and Phoenix Commodities, have sent shockwaves through the industry. Hin Leong – arguably the most notorious collapse – ultimately led to ABN Amro, one of the stalwarts of the industry, retreating altogether – a move that exacerbated the growing liquidity crisis (Howse, 2020).

And then we have Covid-19, one of the most destructive pandemics of a generation. First and foremost, it is a humanitarian crisis, one which to date, has claimed the lives of more than one million people worldwide1 (European Centre for Disease Prevention and Control, 2020), and it is important to place this report into the context of the loss of life. However, from an industry perspective, global disruption in supply chains, coupled with massive shock in demand too, makes, for many, the current situation far more damaging for commodity trade finance than the 2008 financial crash – a largely demand-specific shock that was driven by systemic problems in the credit markets, leading to a liquidity crunch and the repricing of risk assets that spread across many financial markets.

To compound matters, the cessation of LIBOR at the end of 2021, the looming implementation

of Basel IV, and a wave of new compliance and regulatory changes are all making the commodity trade finance industry an increasingly more stringent and challenging place to operate.

The banks still left in the market are also having to contend with the emergence of alternative finance funds too – non-financial institutions that are less restricted by regulation, operate faster and with greater agility, and often have access to the latest technology that streamlines the supply chain and reduces the risk of fraud. The rise of funds makes it more important than ever to understand which are the best performing commodity trade finance banks. Having spoken to the market over the past six months, this report tackles all of these issues and presents the most in-depth primary research available to any individual or organisation active in the commodity trade finance industry.

For clarity, this report will use the term commodity trade finance when grouping the different types of financing available to borrowers. Commodity trade finance is an umbrella term that captures structured and unstructured (vanilla) financing.

In this report, structured finance includes pre-export financing, pre-payment financing, borrowing base loans and reserved based lending2 where financing is tied to a physical asset. Unstructured (vanilla) financing includes revolving credit facilities (RCFs), transactional commodity trade finance3, unsecured debt and bonds – all of which are not generally tied to any sort of underlying asset.

1 Data quoted from the 11th October 2020.2 We acknowledge that reserve based lending is more niche than the other types structured finance but it has been included as it is still used by some commodity trade finance teams.3 We acknowledge that transactional commodity trade financing can be structured, but for the purpose of this report, it is assumed that is mostly unstructured debt that facilitates day-to-day operations

The Global Commodity Trade Finance Industry Report

| 9

Aims and objectives

There are two primary aims of this report:

1. To present a detailed overview of the commodity trade finance industry over the past 12 months, focusing on activity, the impact of Covid-19, compliance and regulation, the banking sector and the views of traders and producers.

2. To present a heatmap that compares the top 10 commodity trade finance banks across nine different attributes. The data that make up this heatmap comes from the clients (traders and producers) of the banks.

To meet these aims, the following objectives were undertaken:

• A quantitative survey of alternative financiers, banks, brokers, law firms, private insurers, producers and traders active in the commodity trade finance industry.

• Qualitative interviews with consenting participants to better understand the latest trends.

Methods

This report uses a mixed methodology research design that combines quantitative survey data with qualitative interviews.

The survey

The quantitative data were collected using an online platform (SurveyMonkey) with data being collected between March and September 2020. The survey was designed so that the respondents only answered questions that were relevant to them and their company. Consequently, ‘background and demographics’, ‘a focused look at the commodity trade finance industry’, ‘compliance and regulation’ and ‘the impact of Covid-19’ were answered by all respondents, the banking industry section was answered by the banks and the final section was for traders and producers only.

No duplicate data from the same institution were included. If more than one respondent answered from

the same institution, the scores were aggregated and then averaged. This approach ensures that every institution is weighted equally.

To provide additional context, closed deal data from TXF Data are included. TXF Data captures around 30% of all commodity trade finance deals. Consequently, where TXF Data is referred to, conclusions should be interpreted with a degree of caution, as the data is a partial snapshot of the market – much of which remains bilateral or hidden/confidential.

The interviews

To explain the quantitative trends, in-depth, semi-structured telephone interviews were conducted with 10 consenting respondents to understand why the quantitative trends occurred. Participants were identified through the survey.

The topic guide for each interview was based on their survey responses to ensure the conversation remained focused. Interviews were conducted between June and September 2020, lasted between 17 and 35 minutes, and were audio recorded for accuracy and further analysis. Any qualitative data used throughout this report has been anonymised to protect the identity of the interviewees.

The Global Commodity Trade Finance Industry Report

10 |

The Global Commodity Trade Finance Industry Report

| 11

Findings• Background and demographics• A focused look at the commodity trade finance industry• Getting to grips with compliance and regulation• The Covid-19 catalyst• A forensic look at the commodity trade finance banks• An insight into the traders’ and producers’ world

The Global Commodity Trade Finance Industry Report

12 |

43% Trader

25% Bank

17% Producer

9% Alternative financer

4% Insurance broker

1% Law firm

1% Private insurer

Figure 1: Type of institution

Background and demographics

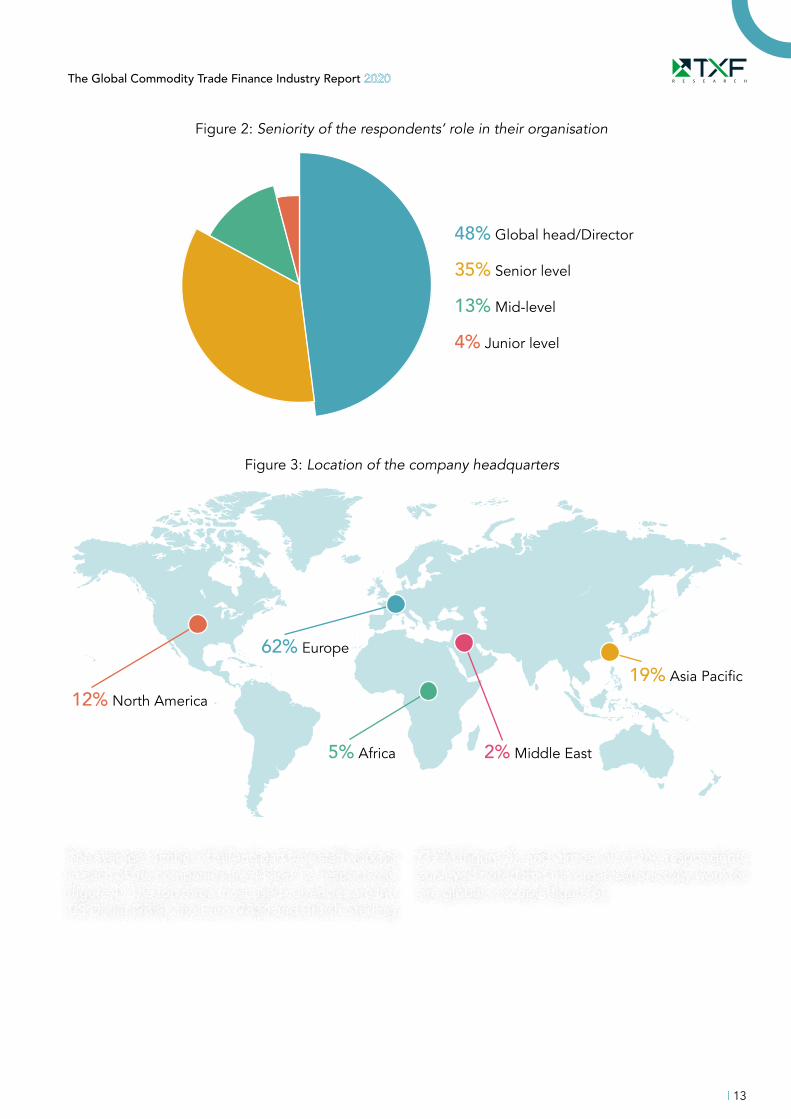

A total of 130 respondents took part in the survey. Figure 1 shows the proportion of respondents from each type of institution. There was a concerted effort in this year’s report to increase the proportional representation of traders and producers. The reason for this is because they provide a unique perspective on an industry that is continually changing and acutely sensitive to global disruption. This has been reflected in the traders and producers representing 60% of the total sample made up of traders (43%) or producers (17%) – higher than last year’s report (44% trader and producers).

This report also aimed to understand how companies and organisations have managed at a strategic,

decision-making level. Having representation from those who identified as a global head or director (48%) or as a senior member of staff involved in decision making (35%), ensures that the data presented in this report are from decision makers (figure 2).

Nearly two-thirds of the sample reported having headquarters in Europe, followed by Asia-Pacific (19%) and North America (12%) (figure 3), reaffirming the European-centric nature of commodity trade finance.

The Global Commodity Trade Finance Industry Report

| 13

48% Global head/Director

35% Senior level

13% Mid-level

4% Junior level

Figure 2: Seniority of the respondents’ role in their organisation

Figure 3: Location of the company headquarters

62% Europe

19% Asia Pacific

12% North America

5% Africa 2% Middle East

The average number of full and part time staff working in each of the companies are 44 and 12, respectively (figure 4). The top three most used currencies are the US Dollar (98%), the Euro (78%) and British Sterling

(31%) (figure 5), and almost all of the respondents surveyed noted that the organisations they work for are global in scope (figure 6).

The Global Commodity Trade Finance Industry Report

14 |

Figure 4: Number of full and part time staff working in the commodity trade finance team

44 Full time 12 Part time

98% US Dollar

78% Euro

31% British Sterling

14% Renminbi

7% Japanese Yen

4% Rupee

11% Other

Figure 5: Most used currencies by the respondents in commodity trade finance

The Global Commodity Trade Finance Industry Report

| 15

92% Global (operating across all continents)

7% Regional (across the continent within which you are located e.g. Asia-Pacific Europe, North America)

1% Just local (your home country and surrounding countries)

Figure 6: Geographic footprint of the respondents’ organisations

Across all of the survey respondents, the average rating for the current state of the commodity trade finance industry is 2 out of 5. Covid-19, the high-profile fraud cases that have been exposed by Covid-19, banks retrenching from the market, taking with them their substantial financial support, and the soaring costs of bank debt, have been very well documented over the past year. However, while the situation could get worse, one interviewee suggests that there are still positives to focus on:

“In all likelihood things will get much worse before they get better. A surge of defaults, insolvencies and insurance claims is almost certain to materialise in the next 6-12 months. While the size and scope are debatable, consolidation in some form or another seems to be a foregone conclusion at this point.

There are some glimmers of hope, however. Prices for many commodities have remained strong, buoyed by

a weak dollar and expectations of recovery. Supply chains, for the most part, either have remained intact or have been restored – at least where end demand remains strong. Reinsurance markets, at least until now, appear to be functioning as normal. Plenty of capital sits on the side-lines, waiting to flow to opportunities (distressed or otherwise) as credit and commodity markets reprice, creating a potential buffer for the system to absorb future shocks.” [Alternative financier; North America]

It is important to remember that these views are subjective and that in places like Europe in particular, some may suggest that reinsurance markets are not performing ‘normally’. How the industry responds over the next few months remains to be seen, but the fundamental importance of all tradable commodities to the global economy is so great, that even in times of extreme stress, there will always be a need for commodity trade finance.

Figure 7: Average rating of the current state of the commodity trade finance industry

Negative Neither positive or negative Positive

2 out of 5

The Global Commodity Trade Finance Industry Report

16 |

The Global Commodity Trade Finance Industry Report

| 17

A focused look at the commodity trade finance industry• Past and present activity• Sustainability: climate change or climate colonialism?

The Global Commodity Trade Finance Industry Report

18 |

Past and present activity

Across the survey respondents over the past 12 months, energy/petrochemicals (57%), has been the most active sector, followed by agri/softs (44%) and metals and mining (43%) (figure 8). TXF Data shows that energy/petrochemicals was the most active sector by deal volume ($38.7 billion), followed by metals and mining ($18.5 billion) and agri/softs ($8.6 billion).

TXF Data also shows that so far in 2020, 74 commodity trade finance deals have closed with a total volume of $62 billion. Nearly 70% of this deal volume ($43 billion) is concentrated across just 14 borrowers (15 deals), a relatively precarious position for an industry that has experienced some major shockwaves during 2020, to be in.

Despite the current climate, all three sectors are set to see more or ‘about the same’ activity in each over the next 12 months, with metals and mining the standout sector with 62% of respondents expecting to do more activity (figure 8). This move likely reflects the fairly buoyant position that the metals and mining industry finds itself in.

More than any other sector, metals and mining has demonstrated a particularly strong resilience to the effects of Covid-19. The counter-cyclical nature of gold is driving its price up, making it a particularly

attractive alternative investment at the moment, and iron ore is starting to see a rapid recovery on the back of an economic rebound from China, and as Brazil’s largest mining company, Vale, begins to return to pre-pandemic volumes. China’s demand for copper too, is driving up its demand, coupled with a resurgence in copper mining in Peru as lockdowns as begin to ease, and the spot price of uranium, driven largely by the large supply correction in Kazakhstan, has risen 32% since January 2020 (McKinsey & Company, 2020)

In addition to its resilient nature, the metals and mining industry is also a hotbed for merger and acquisition (M&A) opportunities. For instance, in North America, Canada’s Endeavour Mining announced plans to merge with Semafo in a $690 million deal to create the largest gold mine in west Africa; Colorado-based Alacer Gold has also recently announced plans to merge with SSR Mining in a $1.7 billion deal, and; Canada’s Gran Colombia Gold is set to purchase Guyana Goldfields in an all-stock deal. In Asia-Pacific, China’s Shandong Gold has recently purchased TMAC Resources and Anil Agarwal has launched a $2 billion bid to take control of Vedanta (Hume & Sanderson, 2020)

Figure 8: Commodity trade finance activity over the past 12 months and predicted activity over the next 12 months, by sector

44%

57%

43%

27%

27%

62%

27%

22%

26%

9%

26%

14%

29%

21%

31%

64%

47%

23%

Very active

Very active

Less active

Less active

Somewhat active

Somewhat active

Past 12 months

Next 12 months

Agri/softs

Energy/petrochemicals

Metals and mining

Agri/softs

Energy/petrochemicals

Metals and mining

The Global Commodity Trade Finance Industry Report

| 19

In terms of which regions have seen most activity over the past 12 months, Europe (64%) leads the way (figure 9), a finding supported by TXF Data which found that Europe has been the most active region with $20.9 billion close across 27 deals. This represents more than a third of all activity just in this region. The standout deal was the $10 billion revolving credit facility (RCF) closed by Royal Dutch Shell.

Asia-Pacific (50%) and Africa (43%) have also seen high levels of activity over the past 12 months, with Trafigura’s $5.5 billion revolving credit facility (RCF) and Sonangol’s $2.5 billion pre-export finance deal, the standout deals in these regions, respectively.

Over the next 12 months, all regions are expected to see the same level of activity as they have done over the past 12 months (figure 9). One possible reason for this, one European banker commented, is because companies tend to consolidate and protect during times of stress:

“You have to focus on what you have. For banks, times of economic stress are often accompanied by losses from loan defaults and increases in risk-weighted assets… both of which deplete capital. It is vital to consolidate and protect what you have.” [Bank; Europe]

Figure 9: Commodity trade finance activity over the past 12 months and predicted activity over the next 12 months, by region

43%

50%

33%

64%

36%

33%

42%

37%

23%

30%

29%

17%

23%

12%

35%

11%

25%

36%

15%

11%

11%

8%

18%

19%

35%

38%

32%

25%

40%

31%

43%

52%

66%

62%

53%

64%

Very active

Very active

Less active

Less active

Somewhat active

Somewhat active

Past 12 months

Next 12 months

Africa (the whole continent)

Asia-Pacific

Central and South America

Europe (inc. Turkey and Russia)

Middle East

North America

Africa (the whole continent)

Asia-Pacific

Central and South America

Europe (inc. Turkey and Russia)

Middle East

North America

The Global Commodity Trade Finance Industry Report

20 |

Sustainability: climate change or climate colonialism?

Figure 10 shows the expected level of operation in the future, by the banks and traders and producers in the different sectors. For the agricultural and softs sectors, where their environmental and social impact is substantially lower than its energy and metals and mining counterparts, banks, traders and producers will mostly continue to operate as normal. Banks, traders and producers are also largely in agreement that they will no longer work in forest-related commodities or in more niche areas such as wool, the extraction of palm oil and rubber.

Metals and mining are also sectors where banks and traders and producers are likely to continue operating as normal, a move that reflects the potential opportunities that are to be gained there.

Coal presents a more mixed picture as the banks report a stronger desire to continue operating as normal (as opposed to reconsidering their position or retreating from the industry altogether), whereas traders and producers show a preference for

retreating from coal-related commodities altogether. While coal is acknowledged as a big contributor to climate change, there are repercussions for moving away from coal:

“The world still needs hydrocarbons. It is easy for people in the West to generate their own green energy, but we [the West] cannot start dictating to people in poorer countries that they cannot use hydrocarbons when they are such a rich source of fuel. It would be like climate colonialism, leaving billions in energy poverty.” [Lawyer; Europe]

The Global Commodity Trade Finance Industry Report

| 21

Figure 10: Anticipated level of sector involvement in the future, by institution type

85%

50%

42%

63%

18%

95%

65%

29%

73%

63%

24%

23%

25%

52%

48%

29%

0%

42%

32%

11%

55%

0%

24%

43%

27%

38%

56%

50%

65%

32%

39%

67%

15%

8%

26%

26%

27%

5%

12%

29%

0%

0%

20%

27%

10%

16%

13%

5%

Continue operating as normal

Continue operating as normal

No longer work in these

sectors

No longer work in these

sectors

Reconsidering

Reconsidering

Banks

Traders and producers

Agri/softs (grains/food/fibre)

Agri/softs (livestock and meat)

Coal (thermal)

Coal (metallurgical)

Forest products (hardwood/softwood pulp)

Metals and mining (industrial/commons

metals e.g. copper, lead and zinc)

Metals and mining (precious metals e.g.

gold, silver and platinum)

Other (palm oil, wool and rubber)

Agri/softs (grains/food/fibre)

Agri/softs (livestock and meat)

Coal (thermal)

Coal (metallurgical)

Forest products (hardwood/softwood pulp)

Metals and mining (industrial/commons

metals e.g. copper, lead and zinc)

Metals and mining (precious metals e.g.

gold, silver and platinum)

Other (palm oil, wool and rubber)

When banks were asked if they would provide more attractive loans for sustainability (where they would charge lower premiums and interest), 55% of the banks stated that they would. Conversely, when traders and producers were asked if they would pay more for green financial products, 68% of those surveyed stated that they would (figure 11). Moreover, the largest proportion of banks and traders and producers were in strong agreement that sustainability should be driven by compliance

and regulatory change, requires a better use of resources, is a cultural and behavioural change concept, and one that should be embodied by the whole commodity trade finance industry (figure 12).

However, while the qualitative interviews supported these findings, one broker did issue a word of caution when attempting to integrate sustainable practices into existing business models:

The Global Commodity Trade Finance Industry Report

22 |

“Sustainable practices are important. However, the move to more sustainable financing must not, in my opinion, lead to a misallocation of capital or failure to appreciate the credit risks that are still prevalent in sustainable financing transactions. Reduced capital held against sustainable transactions to encourage sustainable lending doesn’t in my opinion seem sensible.

If sustainable transactions can be shown to have a lower probability of default or better loss given default, then of course a reduced capital weighting is equitable, but I don’t feel that it should be a blanket decision made to encourage financings.” [Broker; Europe]

This is perhaps why banks, traders and producers stated that sustainability has some influence over strategic and operational decision making but is not the defining factor (figure 13).

Figure 11: Willingness of the banks to provide more attractive financing and of traders/producers to pay more for green products

55% Yes 68% Yes

45% No 32% NoBanks

Traders and producers

The Global Commodity Trade Finance Industry Report

| 23

Figure 13: Influence of sustainability on decision making

Negative

Negative

Neither positive or negative

Neither positive or negative

Banks

Traders and producers

Positive

Positive

3 out of 5

3 out of 5

Figure 12: Respondents’ views on sustainability

40%

45%

60%

55%

10%

49%

47%

55%

55%

6%

30%

10%

5%

10%

75%

9%

4%

4%

9%

88%

30%

45%

35%

45%

15%

42%

49%

40%

36%

6%

Strongly agree

Strongly agree

Disagree

Disagree

Somewhat agree

Somewhat agree

Banks

Traders and producers

Compliance and regulatory change are the driving

force behind sustainability

Sustainability is not a new concept but one that

requires a redirecting of existing resources

Sustainability is a cultural and behavioural change

concept that must address socio-economic, eco-

economic and socio-environmental issues

Sustainability is a way of life that every institution

must adopt

Sustainability is not important for me

Compliance and regulatory change are the driving

force behind sustainability

Sustainability is not a new concept but one that

requires a redirecting of existing resources

Sustainability is a cultural and behavioural change

concept that must address socio-economic, eco-

economic and socio-environmental issues

Sustainability is a way of life that every institution

must adopt

Sustainability is not important for me

The Global Commodity Trade Finance Industry Report

24 |

The Global Commodity Trade Finance Industry Report

| 25

Getting to grips with compliance and regulation• No more LIBOR• Securities Financing Transactions Regulations• EU Benchmarks Regulations• Senior Management Certification Regime

The Global Commodity Trade Finance Industry Report

26 |

No more LIBOR

The London Interbank Offered Rate, better known as LIBOR, refers to a series of reference rates that are currently estimated to underpin $350 trillion dollars’ worth of contracts, including derivatives, bonds and loans (UK Finance, 2019). LIBOR is currently quoted in five different currencies (US Dollar, UK sterling, Euro, Japanese Yen and the Swiss Franc) and seven tenors (overnight/spot next, one week, one month, two months, three months, six months, and one year) but it is scheduled to end in December 2021 (Financial Conduct Authority, 2020).

Historically, LIBOR has been calculated based on banks’ submissions of their own interbank borrowing rates. However, following substantial market regulatory changes in the wake of the 2008 financial crash and the infamous LIBOR manipulation scandal, these submissions have drastically reduced in number. More recently, LIBOR has been based on banks’ judgement concerning their cost of borrowing, rather than transactional data, leaving it exposed to abuse (FCA, 2020).

LIBOR will be discontinued altogether in December 2021 and is set to be replaced by currency-specific risk free rates (RFRs). With this impending shift, it is encouraging that 77% of the banks, traders and producers are aware of LIBOR’s discontinuation (figure 14). However, when banks, traders and producers were asked to comment on their awareness of the new RFRs, it was generally low, with the Canadian Overnight Repo Rate Average (CORRA) scoring just 1 out of 5.

Awareness of the Secured Overnight Financing Rate (SOFR) for the US Dollar, the Sterling Overnight Interbank Average Rate (SONIA) and the Euro Short-Term Rate (ESTER) faired more favourably, scoring an average of 3 out of 5, but this still only reflects ‘some’ awareness (figure 15).

When asked about the greatest challenges in transitioning to the new RFRs, 55% of the banks, traders and producers cited difficulties in where to start, followed by changing the basis (38%) and identifying all impacted products (32%) (figure 16). A recent report by Deloitte concluded that LIBOR is so embedded in the day-to-day activities of providers

and users of financial services, both regulated and unregulated, the task of identifying a firm’s exposure is a monumental task (Deloitte, 2018).

To compound matters further, allowances for Covid-19 are not being considered to delay the cessation of LIBOR timeline (FCA, 2020), with the FCA, Bank of England and the Working Group on Sterling Risk-Free Reference Rates (RFRWG) stating “the central assumption is that firms cannot rely on LIBOR being published after the end of 2021.” (Bank of England, 2020).

Important context is needed here. For the banks, LIBOR transition is an industry-wide phenomenon and not specific to commodity trade finance teams. Moreover, with most commodity trade finance loans being short term, LIBOR also does not come into play too often.

However, there is more cause for concern for the traders and producers, who generally had a lower understanding of the RFRs (figure 15). Failing to transition to the new RFRs will have financial and legal ramifications on how contracts are priced and how associated risk is managed.

This could leave many borrowers of bank debt facing considerable financial losses, legal challenges, and reputational damage. With tackling Covid-19 being the main cause for concern, one trader noted: “we have not even started looking at LIBOR yet.” This places greater impetus on the banks to effectively work with their clients to transition any deal that still uses LIBOR.

The Global Commodity Trade Finance Industry Report

| 27

Figure 14: Banks’, traders’ and producers’ awareness of the cessation of LIBOR

77% Yes

23% No

Canadian Overnight Repo Rate Average (CORRA)

Secured Overnight Financing Rate (SOFR)

Sterling Overnight Interbank Average Rate (SONIA)

Swiss Average Rate Overnight (SARON)

Tokyo Overnight Average Rate (TONAR)

Euro Short-Term Rate (ESTER)

1 out of 5

3 out of 5

3 out of 5

2 out of 5

2 out of 5

3 out of 5

1 out of 5

2 out of 5

2 out of 5

2 out of 5

1 out of 5

3 out of 5

Banks, traders

and producers

Traders and

producers

Figure 15: Banks’, traders’ and producers’ awareness of the different risk free rate systems

The Global Commodity Trade Finance Industry Report

28 |

Identifying all products that are impacted

Accounting hedge accounting impact

Developing wider liquidity in the underlying markets

Client outreach

Other

The process of starting the transition to the new RFRs

Changing the basis

55%

38%

32%

29%

26%

26%

4%

Figure 16: Greatest challenges to transitioning to the new RFRs (banks, traders and producers only).

Securities Financing Transactions Regulations (SFTR)

The SFTR is a piece of legislation that is designed to increase transparency across securities financing transactions in the EU. It is designed to:

“Compel market participants to report all SFTs to an approved trade repository and to radically restructure their data architecture – integrating numerous, and often disparate, data sources to enhance transparency.” (European Commission, 2015)

Financial counterparties, non-financial counterparties, EU-based entities including their non-EU-based branches and non-EU entities where the transaction is concluded by an EU-based branch, all must comply with SFTR.

More than half of the respondents in this survey said that they do not know what SFTR is (figure 17). For European respondents only, this number rises to 57%. This is likely why more than half of the respondents do not know how difficult it is to identify all the necessary data to be SFTR compliant (figure 18).

Looking at what is required to be SFTR compliant, it is an incredibly data-intensive undertaking, which creates several challenges. First, beyond sole transaction data, half of the fields to be reported require counterparty data. Additionally, as a duel-sided reporting requirement, most fields must be reconciled with the counterparty. Second, there are 153 data fields to complete, half of which require providing enough information for counterparties so they can enable sufficient reporting. There is very little room for discrepancy, so data quality is vitally important.

Third, much of the data is not compatible with current trading technologies, making it very difficult to access. Finally, reporting the timing of deals is complex, as there are currently no established market practices on when to record booking times (Carrere, 2019).

These challenges will be particularly daunting for most traders, producers, financial and non-financial institutions, as the sheer task in providing the depth

The Global Commodity Trade Finance Industry Report

| 29

23% Yes

24% No

53% I do not know what SFTR reporting is

Figure 17: Ability to provide all necessary data to be compliant with SFTR reporting

Figure 18: Perceived difficulty in providing all necessary data to be compliant with SFTR reporting

Very difficult

Somewhat difficult

Not difficult

Don’t know

6%

25%16%

53%

EU Benchmarks Regulation

The EU Benchmarks Regulation (BMR) came into effect in 2018 to combat the manipulation of certain benchmark indices, as evidenced by the LIBOR and EURIBOR scandals. The BMR is defined as:

“Regulation on indices used as benchmarks in financial instruments and financial contracts or to measure the performance of investment funds.” (FCA, 2016).

Its aim is to restore confidence in the accuracy and integrity of benchmarks by ensuring that pricing accurately reflects the actual market or economic

reality they are intended to measure (Ashurst, 2018). Consequently, a ‘benchmark’ refers to any index that is regularly determined by the application of a formula, calculation, assessment, or is based on the value of an underlying asset. For example, regulated data benchmarks such as the FTSE 100 index, commodity benchmarks or an interest rate benchmark are examples of accepted indices. Under the new BMR, only authorised entities can be a benchmark administrator or contributor (Ashurst, 2018).

and breadth of data is likely insurmountable. Even for the largest trading houses such as Archer Daniels Midland, Bunge, Cargill, Glencore, Gunvor, Koch Industries, Louis Dreyfus, Mercuria, Trafigura and

Vitol, while they may have the resources to undertake SFTR reporting, they will likely have contracts that go back decades, making it data that are very difficult to locate.

The Global Commodity Trade Finance Industry Report

30 |

For the commodity trade finance industry sector, where prices have historically been set by price reporting agents acting on expert judgement rather than real transactional data, the BMR will have a significant impact on how commodities are priced.

On average, survey respondents think that the BMR will lead to some improvement in the transparency of how commodities are priced (figure 19) but the survey found that more than half of the sample do not know what BMR is (figures 20 and 21). One interviewee suggested that this might be because BMR is still not well established:

“The regulations are certainly well intentioned, but they are relatively new and not particularly well known. Some effort to improve transparency and limit the potential for manipulation in commodities pricing is long overdue. Indeed, benchmarks are perhaps one of the few areas of the financial markets where prescriptive regulation is a more appropriate and effective approach to preventing market manipulation than ex post, enforcement-only regulation. However, implementation is key and only time will tell whether the BMR scheme is under- or overbroad in its application.” [Broker; North America]

Figure 19: Impact of the new benchmark regulations to improve transparency in the pricing of commodities with indexes from price reporting agents

Negative Neither positive or negative Positive

3 out of 5

25% Yes

18% No

57% I do not know what the new BMR system is

Figure 20: Possibility for price reporting agents to have non-transparent index prices of commodities after the introduction of the new BMR system

The Global Commodity Trade Finance Industry Report

| 31

Figure 21: Likelihood of respondents’ continuing to use an index which does not fall under the scope of the new BMR system to finalise the price of commodities

SeniorManagementCertificationRegime(SMCR)

The primary goal of the SMCR is:

“Reduce harm to consumers and strengthen market integrity by creating a system that enables firms and regulators to hold people to account.” (FCA, 2019). It is for FCA-regulated companies only and aimed at people defined as ‘senior managers’ – those defined as the most senior people in the company who have the potential to do most harm (FCA, 2019). Of the total sample surveyed, 24% of the respondents identified as working in a company that is FCA regulated (figure 22) and, encouragingly, the introduction of this piece of governance-focused legislation is not making most of these companies reconsider their position as an FCA regulated company (figure 23).

However, for those companies that are not FCA regulated, 90% stated that the tighter governance and reporting standards brought in by the introduction of the SMCR, would not encourage them to become FCA regulated (figure 24).

The main goal of SMCR is to hold people accountable for their actions. It is difficult to speculate how a comparable piece of legislation in Singapore and the Middle East might have influenced the actions of senior personnel at Hin Leong, Agritrade International, ZenRock Commodities and Phoenix Commodities, but what is certain, is that the legislation would hold the responsible people to account.

19% Yes

19% No

61% Don’t know

The Global Commodity Trade Finance Industry Report

32 |

Figure 22: Proportion of respondents working in an FCA regulated company

24% Yes

76% No

Figure 23: If yes, will the introduction of the Senior Management Certification Regime (SMCR) cause you to rethink your position as an FCA regulated company?

16% Yes

84% No

The Global Commodity Trade Finance Industry Report

| 33

Figure 24: If no, will the introduction of SMCR make you think about becoming an FCA regulated company?

10% Yes

90% No

The Global Commodity Trade Finance Industry Report

34 |

The Global Commodity Trade Finance Industry Report

| 35

The Covid-19 catalyst• “Uncertain, unprecedented and unbelievable”• The impact of Covid-19 on the commodity trade finance banks

The Global Commodity Trade Finance Industry Report

36 |

“Uncertain, unprecedented and unbelievable”

More than two-thirds of the sample believe that the Covid-19 pandemic is worse than the 2008 financial crash, principally, because every part of the demand and supply chain has been impacted (figure 25). One interviewee notes:

“The Covid-19 pandemic is quite different to the GFC [global financial crash] in that both supply and demand have been hugely affected. Unlike the 2008 GFC where supply was not as heavily impacted, over the past several months we have seen significant disruption in many supply chains, from manufacturing to consumer goods and beyond.

The fact that the uncertainty and fear that were present with respect to demand in 2008 are now present with respect to both demand as well as supply today, creates the potential for the situation to become substantially worse.

Moreover, the effect of this dual-front dynamic is not easy to quantify since the overall system is highly complex: it is highly unlikely that we are dealing with a linear system here, in the sense that a demand and supply shock is twice as bad as demand shock alone; rather, the effect is more likely to be exponential.” [Alternative financer, North America]

For the commodity trade finance industry, the impact of Covid-19 is largely negative (figure 26), with the most severe consequences being felt by the smaller and medium sized traders and producers, as one producer from Asia-Pacific commented:

“I think that my view is in line with most commentators that agree that the larger traders will get bigger and the smaller entities will struggle to survive. This will push costs up the supply chain on to the producers, who will have less flexibility to improve terms due to a smaller number of buyers existing for their materials.” [Producer; Asia-Pacific]

The consolidation of traders in the commodity finance

industry is a fairly common sight. However, unlike previous economic crises, the current pandemic has led to a shock in supply chains and an unprecedented drop in demand, coupled with rising unemployment and a global humanitarian crisis (Barbosa, Bresciani, Graham, Nyquist & Yanosek, 2020).

One trader explained that the commodity trade finance industry in 2020 is best characterised as “uncertain, unprecedented and unbelievable” with no ending to the pandemic in sight. The quantitative data supports this statement as more than three-quarters of the total sample said that the impact of Covid-19 on the sector would be long-term (figure 27).

Figure 25: Will the covid-19 pandemic be worse than the 2008 financial crash for the commodity trade finance sector?

68% Yes

33% No

The Global Commodity Trade Finance Industry Report

| 37

Looking in more detail at how Covid-19 will impact the different sectors, the energy/petrochemicals sector (74%) is expected to be the most severely affected sector, followed by metals and mining (51%) (figure 28). This report found that agri/softs will be the least impacted sector, with 19% of the overall sample expecting no impact in the sector at all. While it is unlikely that no impact will be felt across the agricultural world, recent academic literature has found considerable resilience in these markets.

This is largely because food consumption is relatively inelastic, meaning that it can take several years for production to adjust fully to price change, ensuring that any shock to global GDP, results in a relatively modest impact on global production and consumption (Elleby, Perez Dominguez, Adenauer & Genovese, 2020).

Severe impact No impactModerate impact

Metals and mining

Agri/softs

Energy/petrochemicals

Figure 28: Impact of Covid-19 on each sector

27%

74%

51%

54%

26% 0%

0%

19%

49%

Figure 26: Perceived impact of Covid-19 on the commodity trade finance industry

Negative Neither positive or negative Positive

2 out of 5

Figure 27: Length of time that Covid-19 will impact the commodity trade finance industry

0% Short term (0-3 months)

23% Medium term (4-6 months)

78% Longer term (7 months and beyond)

The Global Commodity Trade Finance Industry Report

38 |

A considerable 85% of the total sample expect Covid-19 to lead to a reduction in the credit availability of banks (figure 29), which is expected to lead to an increase in the cost of bank debt for all of the sectors (figure 30). One interviewee explained why:

“A reduction in credit availability will lead to a drop in volumes. This means producers will have to curtail productions and capacity utilisation, which will impact commodity prices and their revenues, profitability and recovery of overheads. The producers will have to reduce capex, restructure, reorganise, and realign their business to make their resources more efficient, effective and productive. I fear that for those

producers who can’t effectively utilise technology, digitisation and AI will struggle to survive as they will not be able to do more, and make more, with less investments.” [Producer; Asia-Pacific]

The prevailing literature suggests that the hardest hit companies will be the mid-sized traders, principally, because they will struggle to find banking support to fill the liquidity gap left by the likes of ABN AMRO, BNP Paribas and Societe Generale either scaling back or leaving the industry altogether (Wass, 2020).

Increase Stay the sameDecrease

Metals and mining

Agri/softs

Energy/petrochemicals

Figure 30: Will a reduction in credit availability lead to an increase in the cost of bank debt over the next 12 months?

68%

56%

54%

8%

36% 8%

24%

35% 11%

Figure 29: Impact of Covid-19 on the credit availability of the banks

85% Yes

15% No

The Global Commodity Trade Finance Industry Report

| 39

TheimpactofCovid-19onthecommoditytradefinancebanks4

Nearly 60% of the banks surveyed noted that they think Covid-19 will be used as a smokescreen for already failing businesses (figure 31), a finding supported by the qualitative data:

“Everyone in the [commodity trade finance] industry got very overconfident… very low interest rates and huge liquidity at the start of the year [before Covid-19].” [Bank; Europe]

The respondent goes on to note:

“If Covid-19 had not happened, Hin Leong could have gone on for years. The stress that Covid-19 has put on the commodities sector has brought to light a raft of fraudulent companies that need making an example of.”

A considerable amount of news and information has been published over the past few months on the demise of Hin Leong, Agritrade International, ZenRock Commodities and Phoenix Commodities, driven by alleged or actual premeditated acts of document forgery, fraudulent use of invoices, fake trades, double financing and deception, compounded by poor governance, poor vigilance by the banks and auditors and market volatility which stressed aggressive and/or weaker players.

Yet, it is important to remember that the cause of these cases was not Covid-19, but the environment in which they were allowed to prosper.

4 The figures in this subsection are based on data provided by the banks only.

Figure 31: Banks’ perception of Covid-19 being used as a smokescreen for already failing businesses

58% Yes

42% No

Of the banks that took part in this survey, 42% noted that their clients have fully drawn down on their RCFs (figure 32), a move that reflects businesses entering survival mode as they look to combat the sudden drop in economic activity.

However, the qualitative data suggests that economic downturn is not the only reason for RCF drawdowns:

“It is true that many are drawing down to relieve stress or to combat anticipation of breaking covenants, but some companies are drawing down even if their operations have not been too severely impacted to ensure they have enough cash for future operations.” [Bank; Europe]

The Global Commodity Trade Finance Industry Report

40 |

Figure 32: Proportion of clients who have fully drawndown on their revolving credit facilities

42%

To support their clients, almost all of the banks (93%) stated that they would provide temporary waivers in the event of default (figure 33). This was welcomed by all of the traders and producers interviewed for

this research, as it helped to remove part of the uncertainty. It is also a stark reminder of the hardship that a huge majority of traders and producers have faced over the past few months.

Figure 33: Willingness of banks to provide temporary waivers to all clients that default payment

93% Yes

7% No

The Global Commodity Trade Finance Industry Report

| 41

A forensic look at the commodity trade finance banks• A closer look at the financials• Basel and the banks• A growing threat from alternative finance?• Or a threat from global traders?

The Global Commodity Trade Finance Industry Report

42 |

Acloserlookatthefinancials5

Of those banks surveyed, over the next 12 months, bank portfolios look set to be mostly made up of transactional commodity trade financing (53%), reflecting the need for banks to be able to operate on a day-to-day basis, most likely without structure (although some of it could be backed by securities such as warehouse receipts for example) (figure 34). Banks expect to see a small increase in their structured commodity trade facilities over the next 12 months, with pre-export finance (19% to 22%), borrowing base loans (16% to 19%), prepayment finance (15% to 25%), and reserve-based lending (4% to 9%) all set to make up slightly larger portions of the overall portfolio (figure 34). With access to liquidity and risk mitigation fundamental during times of stress, it is unsurprising that the respondents are opting for structured commodity trade finance options.

Survey data suggests that RCFs are set to decline over the next 12 months (a drop of 9% based on our survey data), a trend that is tentatively supported by TXF Data, which shows a decline in RCFs, from a total of $66 billion in 2019 to $26 billion in 2020. With the banks reporting that, on average, more than 40% of their clients have already fully drawn down on their RCFs (see figure 32), it stands to reason that banks will reduce this capital heavy product.

These data on RCFs should be interpreted with caution. The survey data presented here is from a small cross section of the industry, and the TXF Data only captures publicly available deals, most of which are structured commodity finance and does not include bilateral or confidential deals.

Nearly a combined 70% of the bankers who took part in this survey expect an increase in their loan loss provisions (LLP) over the next 12 months (figure 35). This quantitative indicator suggests that the banks anticipate a greater probability that loans will not be repaid in full, driven almost entirely by Covid-19.

To compensate, all of the banks also anticipate an increase in their margins and fees over the next 12 months (figure 36) as one possible way to counter market volatility and any potential downturn in financial performance.

Transactional commodity trade finance

Revolving credit facilities

Pre-export financing

Borrowing base loans

Prepayment financing

Unsecured debt

Reserve based lending

Bonds

49%

26%

19%

16%

15%

14%

4%

4%

53%

15%

22%

19%

25%

13%

9%

3%

Proportion of banks

using each type of facility

over the past 12 months

Proportion of banks

using each type of facility

over the next 12 months

Figure 34: Commodity trade finance banks’ portfolio breakdown over the past and next 12 months

5 The data in this section is based on banking respondents only.

The Global Commodity Trade Finance Industry Report

| 43

We expect to see a big increase

We expect to see a small increase

We expect to see a small decrease

We expect to see a big decrease

We do not expect any change

21%

47%11%

5%16%

Figure 35: Anticipated changes in loan loss provision (LLP) over the next 12 months

Figure 36: Anticipated changes in the banks’ margins and fees over the next 12 months

100%Increase

0%Decrease

0%Stay the same

Basel and the banks

The 2008 global financial crash caused shockwaves throughout the financial world, with most banks experiencing huge financial and reputational damage. In the wake of the crisis, the Basel accords have sought to prevent a repeat of the banking collapse by introducing a raft of increasingly stringent regulatory, compliance and governance structures, that mandate banks to have sufficient levels of capital to withstand extreme levels of stress.

The latest risk-based Basel IV reforms to credit, market and operational risk, the output floor and the credit valuation adjustment, will increase the weighted average Tier 1 minimum risk-based capital requirement of international EU banks and global systemically important banks (G-SIBs) by 23% and 26%, respectively (KPMG, 2018).

Just over half of the banking respondents said that these reforms will have a negative impact on resilience and confidence in the commodity trade finance banking industry (figure 37), with changes in the credit risk standardised approach (65%), removal of the internal ratings based (IRB) approach for low default portfolios (53%) and the number of reviews that banks have to go through (47%) the three most challenging aspects of Basel IV (figure 38).

Major banks are particularly critical of the reforms that limit the extent to which the banks can rely on internal models – rather than the standard tool of regulators – to calculate their risk-weighted assets and the amount of core capital they need to hold against these risks; a move that will limit profitability and competitiveness (Storbeck, 2017).

The Global Commodity Trade Finance Industry Report

44 |

The number of reviews that we have to go through

An aggregated IRB risk weighted assets output floor of 75%

The implementation of new impairment standards as set out under the International Financial Reporting Standards (IFRS) 9

Revisions to operational risk

Application of standardised approach risk weights for exposures to sovereigns

Changes in the credit risk standardised approach

Removal of the internal ratings based (IRB) approach for low default portfolios

Figure 38: Banks’ perception of the most challenging Basel IV initiatives for commodity trade finance banks to negotiate

65%

53%

47%

41%

35%

18%

12%

Figure 37: Perceived impact of Basel IV on bank resilience and confidence in the commodity trade finance banking industry

47% Yes, it will have a positive impact

53% No, it will have a negative impact

The Global Commodity Trade Finance Industry Report

| 45

The commodity trade finance banks surveyed in this report noted that over the next two years, changes in the requirements for capital, stress testing, liquidity, large exposures and improved reporting (67%), credit risk management (44%) and employing digitisation throughout transactional banking processes (39%) are the three most important areas for the sector to focus on (figure 39).

A recent news article published by TXF points to digitisation fast becoming a mainstay on the commodity trade finance world, with a growing number of banks, corporates and insurance companies adopting the SWIFT MT 798 standards; a move that will improve connectivity and the exchange of large amounts of information and data (Katsman, 2020).

The Global Commodity Trade Finance Industry Report

46 |

Changes in the requirements for capital, stress testing, liquidity, large exposures and improved reporting

Credit risk management

Properly employing digitisation throughout transactional banking processes

Improving the knowledge and processes to monitor transactions

Recruiting of third party risk managers to detect the risk of fraud

Improved protocols to detect financial crimes (e.g. money laundering and financing terrorism)

Improving and updating banking technology (e.g. the cloud and application programming interfaces (APIs)

Improving operational resilience (e.g. to disruptions in the bank, their clients and the wider industry)

A focus on optimising across three lines of defence (3LOD)

Refining their governance frameworks to identify weaknesses

Improving data management facilities

Improved privacy and cybersecurity protocols

A focus on nonfinancial risk (e.g. employee misconduct, and customer protection)

Figure 39: Banks’ perception of the most important factors to focus on over the next two years

67%

44%

39%

33%

22%

17%

17%

11%

11%

11%

6%

6%

6%

The Global Commodity Trade Finance Industry Report

| 47

Agrowingthreatfromalternativefinance?

With banks scaling back, reviewing their role or retreating altogether from the commodity trade finance industry, the trade finance liquidity gap is growing, with the latest estimates placing it between $2 trillion and $5 trillion (World Trade Organisation, 2020).

Alternative trade finance is gaining momentum as a viable way to fill at least part of the gap, with recent estimates suggesting that alternative investments have grown from just 6% ($4.8 trillion) of the global investible market in 2004, to 12% ($13.4 trillion) in 2018, and a predicted 18% to 24% (approximately $20 trillion) by 2025 (Chartered Alternative Investment Analyst Association, 2020). While these figures extend beyond commodity trade finance, they do highlight the growing role of alternative finance.

However, more than two-thirds of the banks surveyed said that they do not see any increased competition from non-banking trade finance funds (figure 40). For those types of alternative finance that the banks do come across, funds (63%), private equity funds (35%) and pension funds (12%) are the most common type (figure 41)6.

Comparing this to the trader and producer-specific data, 51% said that they are currently using some form of alternative finance fund (see figure 44).

Alternative forms of finance are more agile than banking finance, with the ability to operate in a more relaxed regulatory landscape and are able to adopt the latest technology to streamline the supply chain and reduce the risk of fraud (Lenney, 2020). This could make them particularly attractive to mid-sized corporates that are most harshly feeling the effects of low levels of liquidity.

With these benefits, however, often come higher prices to compensate for the increased risk involved in the deals, inadequate regulatory oversight that could precipitate fraudulent activity and higher risk of losses.

Figure 40: Are you seeing increased competition from alternative sources of financing?

32% Yes

68% No

6 The survey did also ask about a number of other types of alternative finance options, including hedge funds, private equity direct investments, mutual funds, and funds of funds but they all scored 0%.

The Global Commodity Trade Finance Industry Report

48 |

63% Funds

25% Private equity funds

12% Pension funds

Figure 41: Banks’ perception on the most prevalent sources of alternative finance in the commodity trade industry

Or a threat from global traders?

As well as the emergence of alternative funds, banks are also facing competition from the largest trading houses on-lending their own lines of credit to smaller and mid-sized traders, a move which 63% of the banks are in favour of (figure 42).

This is likely why almost the same proportion of banks said that they currently have co-lending facility agreements in place, where the banks and traders lend side-by-side, to other traders and producers (figure 43).

One banker commented, however, that co-lending will not benefit everyone:

“The industry is going to see more of this [co-lending between banks and traders]. It will allow the banks to be more selective in who they finance… but second and third tier traders will still not get a look in… there will still be a preference for the largest traders as they pose the least risk.” [Bank; Europe]

With Covid-19 threatening to loom large for quite some time, banks’ risk appetite is likely to be low for the foreseeable future. One possible way for the banks to reduce the risk is to co-lend with traders.

The Global Commodity Trade Finance Industry Report

| 49

Figure 43: The percentage of banks that current co-lend with traders, side-by-side, to other traders and producers (where you all sign the facility agreement as lenders)

65% Yes

35% No

Figure 42: Banks’ perception on whether or not global trading houses should lend to smaller traders and producers

63% Yes, global traders should lend to smaller traders and producers

37% No, global trading houses should not lend to smaller traders and producers

The Global Commodity Trade Finance Industry Report

50 |

The Global Commodity Trade Finance Industry Report

| 51

An insight into the traders’ and producers’ world• A growing need for alternative finance • The commodity trade finance banking heatmap

The Global Commodity Trade Finance Industry Report

52 |

Agrowingneedforalternativefinance

All of the data in this subsection is based on trader and producer survey responses and quotes only.

Across the traders and producers who took part in this survey, just under half noted that they are not currently using any form of alternative finance (figure 44). While this suggests that banks may still provide the preferred source for finance, over a third reported that they are accessing funds (36%) or private equity funds (34%) with just under a third also utilising private equity, direct investments (30%). Far fewer traders and producers reported using the global trading houses as a source of financing (figure 45). For many traders and producers, their options for financing are becoming increasingly limited. Covid-19 has caused a global wave of defaults in the industry, prompting the likes of BNP Paribas and Societe Generale to scale back their involvement and Rabobank to consider their current position (Howse, 2020). Coupled with the pandemic has been a raft of unexpected high-profile fraud cases – the $3.8 billion Hin Leong default perhaps being the most notorious – which led to ABN AMRO retreating altogether (Payne, 2020).

As banks retreat, competition will fall, and the cost of debt will increase – the underlying reason why traders and producers in this report sought funding from alternative sources (figure 46). The largest global trading houses will be largely immune from this, but the smaller and mid-sized traders will need to act fast to access trade finance, as one trader noted:

“The Vitols, Glencores and Trafis [Trafigura] of this world will be fine. They may even benefit from the banks leaving as they can provide their own financing… I don’t see many of the smaller and even mid-sized traders, lasting” [Trader; Europe]

While alternative finance has a role to play, it certainly cannot provide the debt volumes or lower pricing, to fill the funding gap. One possible solution might be a collaboration between banks and funds, but collaboration and patience will be key for such a partnership to work effectively with such a widening trade finance gap (Howse, 2020a)

The Global Commodity Trade Finance Industry Report

| 53

Private equity funds

Private equity, direct investments

Funds of funds

Mutual funds

Hedge funds

Pension funds

Other

I do not use any alternative source of funding

Funds

Figure 44: Traders’ and producers’ use of alternative funds

49%

36%

34%

30%

13%

13%

13%

6%

4%

Figure 45: Traders and producers currently utilising financing from global trading houses

24% Yes

76% No

The Global Commodity Trade Finance Industry Report

54 |

Figure 46: Reason for accessing alternative funds

There are too many regulatory and compliance issue around bank funding

Other

I can get bank funding, but the cost of debt is too high

Banks will not give me access to funds

43%

26%

15%

16%

Thecommoditytradefinancebankingheatmap

Of the traders and producers who took part in this report, the top three most used banks were UBS (54%), BNP Paribas (52%) and ING Bank (50%) (figure 47).

The banking heatmap7 shows that across the commodity trade finance banks, the average score for each attribute ranged from between 3.0 (pricing) and 3.8 (industry expertise), with an average overall total of 3.5 (figure 48). While it is encouraging that seven of the attributes had a highest score of 4.0 or more, suggesting that the top performing banks for each attribute have demonstrated strong expertise and guidance to the clients, the relatively modest overall average (3.5) suggests that the clients of the banks are only ‘somewhat satisfied’ with how the banks have performed during 20208.

Industry expertise had the highest overall average score (3.8). Interestingly, the standard deviation9

across the banks for this attribute is small (0.19), demonstrating that the banks’ clients consider there to be little variation between the banks’ knowledge of the commodity industry. This suggests that the banks have been providing comparable and consistent advice to all of their collective clients, a particularly positive attribute for one trader:

“We need up-to-date and consistent information on the markets. Now, more than ever, do we need reliable information to navigate the markets we are active in.” [Trader; Europe]

Pricing had the lowest average score of 3.0 and was one of only two attributes (the other being risk appetite), where no banks scored above 4.0. Pricing also had a relatively low standard deviation (0.22), highlighting that banking clients’ views on how debt has been priced over the past 12 months is relatively similar.

The data in this report suggest that across all of the banks, their clients were less satisfied with how the banks priced their debt. The driving reason for this – Covid-19.

Figure 35 shows a combined 68% of the banks surveyed in this report expect an increase in their loan loss provision (LLP) statements, with one banker pointing to Covid-19 as the cause for this:

“Covid-19. Simple. We have to cover losses somehow and we are seeing more and more of our clients defaulting on payments.” [Bank; Europe]

7 The wider heatmap captured data on 31 commodity trade finance banks. However, many of these did not have enough data to be included in the heatmap. The banks shown in figure 57 are those that had a minimum of 20 survey respondents. 8 Each of the commodity trade finance banks were rated on a scale of 1 to 5 across nine different attributes, where 1, 3 and 5 represented ‘very dissatisfied’, ‘somewhat satisfied’ and ‘very satisfied’, respectively. The respondents were asked to rate each bank based on their own experiences and how each bank compared with one another. 9 In statistics, standard deviation is used to measure the variation of data from the mean (average). A small standard deviation means that the data is centred close to the mean. A large standard deviation means that the data is spread far from the mean. Neither should be interpreted as ‘good’ or ‘bad’ but as a description of how dispersed the data is.

The Global Commodity Trade Finance Industry Report

| 55

One way for a bank to recoup costs from LLP and to generate more revenue is by increasing the cost of their debt, a move that all of the banks surveyed in this report say is happening or predict will happen (see figure 36).

Consequently, with the cost of bank debt increasing, coupled with banks predicting an increase in their LLP, it is possible that the clients of the banks are already experiencing the costs being passed on to them. It remains to be seen how high the pricing of bank debt will go over the next few months, but with the threat of national lockdowns looming large across Europe in particular (Ellyatt, 2020), the outlook is bleak for borrowers. One other attribute to note is awareness of sustainability. With an average score of 3.5, the clients of the banks are somewhat satisfied with the banks’ awareness of sustainability. The small standard deviation (0.22) also shows that the banks are perceived by their clients as having a fairly consistent awareness of sustainable issues.

When figure 13, the influence of sustainability on strategic and operational decision making (see page 23), is filtered by bank respondents only, the score remains three out of five; reflecting a position where sustainability has a ‘somewhat important’ role in banks’ decision-making procedures.

Taking the somewhat satisfied score for awareness of sustainability from the heatmap, combined with the somewhat important influence of sustainability on banks’ decision making process, these data suggest that the commodity trade finance banks’ awareness of sustainability has room for improvement.

Sustainable deals tend to be less attractive from a pricing perspective for banks and are often accompanied with higher levels of due diligence and higher costs to set up. This makes them less attractive to finance in times of stress. With Covid-19, high-profile fraud cases, banks retrenching from the market and ongoing geopolitical tensions, it could be that the banks have shifted their attention away from sustainable deals, to more traditional sectors such as oil and gas, where deal structuring is less costly. TXF Data tentatively supports this picture as 2020 has seen the oil and gas industry close $33.8 billion

worth of deals, while renewables is just a fraction of this.

Looking closer at how the banks have performed, for a second year in a row, UBS have been rated as the best commodity trade finance bank across all of the attributes with an average overall score of 4.0. While UBS does top score in five of the attributes, Rabobank (industry expertise, pricing and how well they understand their clients’ business), Credit Agricole (capacity) and UniCredit (customer service) also feature as industry leaders.

It is important to contextualise these findings in order to understand why UBS, a bank that, according to TXF Data league tables, ranks as 33rd, comes out on top of this heatmap. The main reason is because of the different types of data that make up TXF Data and the heatmap.

The banking heatmap is based on market sentiment data collected directly from the clients of the banks. These scores have no relationship to deal volume or wider commodity trade finance activity. In this report, where there is a larger representation of European respondents (an outcome that reflects the European-centric nature of the commodity trade finance markets), it is understandable why all but one of the top 10 banks (HSBC being the exception) score well.

Conversely, TXF Data is based on closed deal data, submitted by the banks on all the commodity trade finance deals they are prepared to disclose. Moreover, TXF Data only holds deal information on publicly available deals, almost all of which are structured commodity financed deals and not bilateral or confidential/hidden deals. These data hold no relationship to market sentiment, and therefore, should not be viewed in tandem.

The need for both types of data is because together, they present a more complete understanding of the commodity trade finance industry. Without the banking heatmap, it might be logical to conclude that the banks that close the largest volumes are also the best for more nuanced, qualitative traits such as customer service and awareness of sustainability. Equally, without TXF Data, it might be logical to draw the conclusion that the top performing banks in the heatmap are also the ones who close most deals.

The Global Commodity Trade Finance Industry Report

56 |

Figure 47: Most used commodity trade finance banks

54%

35%

28%

24%

13%

11%

52%

35%

26%

24%

13%

11%

50%

33%

26%

22%

13%

9%

2%

50%

30%

26%

22%

13%

9%

43%

30%

26%

17%

13%

7%

The Global Commodity Trade Finance Industry Report

| 57

Figure 48: The commodity trade finance banking heatmap

UBS

Rabobank

Credit Agricole CIB

Credit Suisse

UniCredit

ING Bank

Societe Generale

BNP Paribas

Deutsche Bank

HSBC

Difference between highest and lowest

score

Average score across the banks

Top performing bank

4.0

3.7

3.8

3.5

3.5

3.7

3.6

3.1

3.2

3.2

0.9

3.5

UBS

1.4

3.5

Credit Agricole

1.2

3.7

UBS and UniCredit

1.0

3.6

UBS

1.6

3.8

Rabobank

1.3

3.0