the global economic and financial outlook and challenges ... · consensus on need for coordinated...

TRANSCRIPT

1

Astana, Kazakhstan May 28-31, 2009

The Global Economic and Financial Outlook and Challenges for Emerging Economies

Takatoshi

KatoDeputy Managing Director

International Monetary Fund

2

Structure of PresentationStructure of Presentation

The Global Economy and OutlookThe Global Economy and OutlookThe Road to Recovery will be ProtractedThe Road to Recovery will be ProtractedChallenges for Emerging MarketsChallenges for Emerging MarketsOutcome of GOutcome of G--20 Summit20 SummitRole of the IMFRole of the IMF

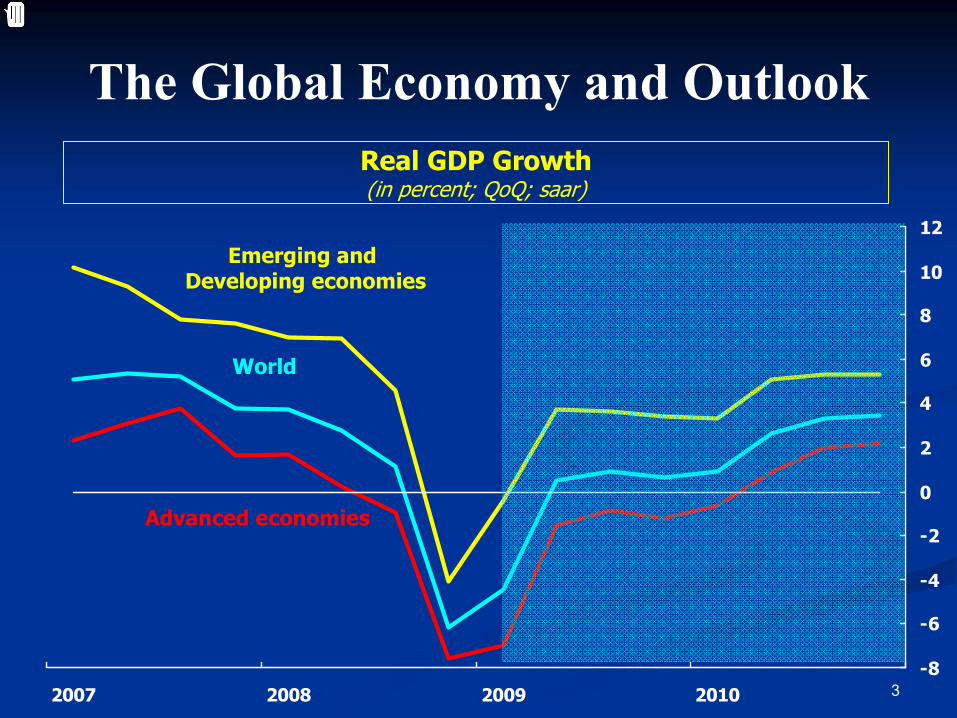

3-8

-6

-4

-2

0

2

4

6

8

10

12

2007 2008 2009 2010

Real GDP Growth(in percent; QoQ; saar)

World

Emerging and Developing economies

Advanced economies

The Global Economy and Outlook

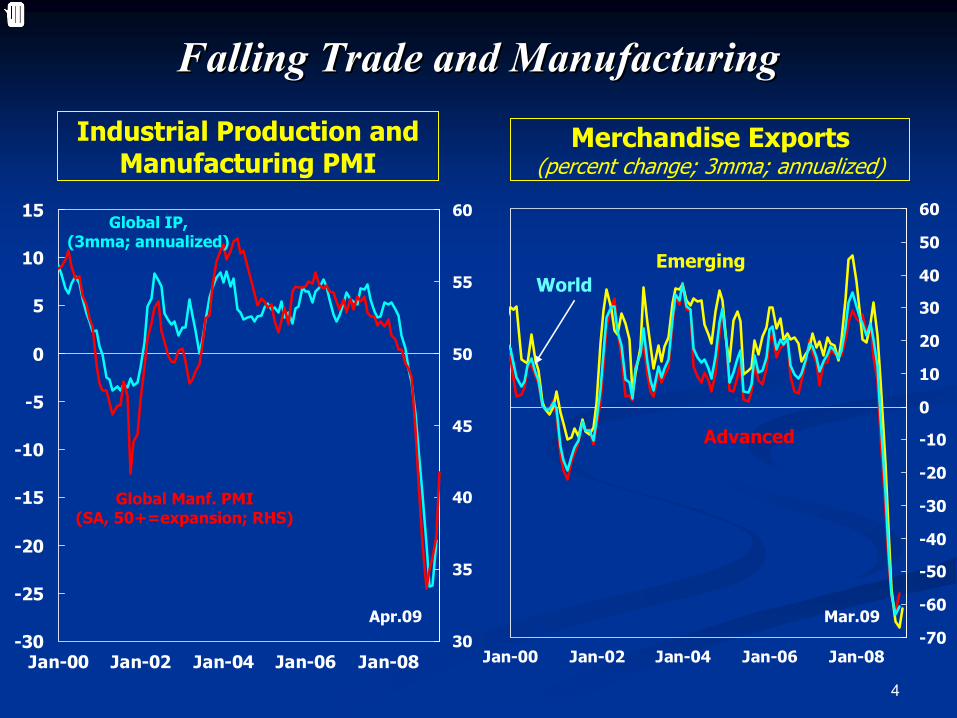

4

Merchandise Exports(percent change; 3mma; annualized)

-30

-25

-20

-15

-10

-5

0

5

10

15

Jan-00 Jan-02 Jan-04 Jan-06 Jan-0830

35

40

45

50

55

60

Industrial Production and Manufacturing PMI

Global IP, (3mma; annualized)

Global Manf. PMI(SA, 50+=expansion; RHS)

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08

Apr.09

World

Mar.09

Advanced

Emerging

Falling Trade and ManufacturingFalling Trade and Manufacturing

5

GDP Slowdown in Selected Countries with a GDP Slowdown in Selected Countries with a High Share of Manufacturing ExportsHigh Share of Manufacturing Exports

R2 = 0.47

-30-25-20-15-10-505

10

0 5 10 15 20 25 30 35 40Share of advanced manufacturing in GDP

2008

Q4

GD

P gr

owth

(SA

AR)

Share of Advanced Manufacturing in GDP and 2008Q4 GDP Growth1

(In percent)

Sources: UNIDO database; and IMF staff calculations. 1 Advanced manufacturing is high-and-medium-technology manufacturing as defined in UNIDO Industrial Development Report , 2009.

Thailand

SingaporeKorea

Malaysia

Japan

Taiwan Province of China Ireland

GermanyFinland

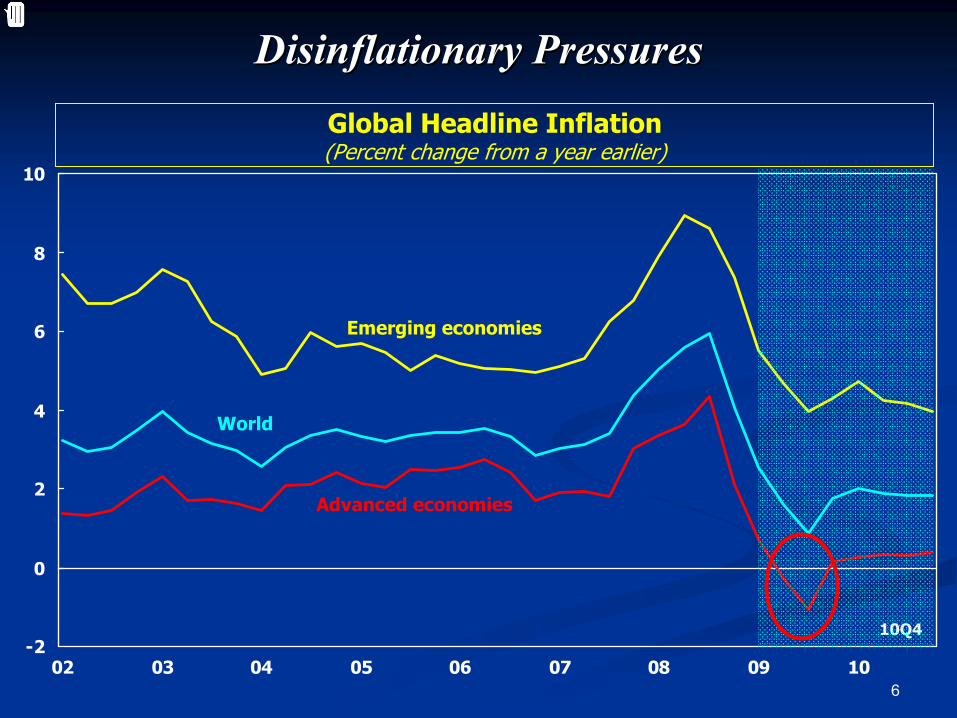

6

-2

0

2

4

6

8

10

02 03 04 05 06 07 08 09 10

Global Headline Inflation(Percent change from a year earlier)

World

Advanced economies

Emerging economies

10Q4

Disinflationary PressuresDisinflationary Pressures

7

Unemployment Rate ProjectionsUnemployment Rate Projections

2

4

6

8

10

12

2006 2007 2008 2009 2010

U.K.U.K.

U.S.U.S.

JapanJapan

Euro areaEuro area

Unemployment RateUnemployment Rate((in percent)in percent)

8

The Road to Recovery The Road to Recovery Will be ProtractedWill be Protracted

World economy affected by two opposing World economy affected by two opposing forcesforcesDownward force from crisisDownward force from crisisUpward force from policies and natural Upward force from policies and natural stabilizersstabilizers

9

-4

-2

0

2

4

6

8

10

90 95 00 05 10

Growth Rates and Output GapsGrowth Rates and Output GapsReal and Potential GDP Growth 1/

(percent change from a year earlier)

Advanced

World

Output Gaps(percent of potential GDP)

Emerging

-6

-4

-2

0

2

4

90 95 00 05 10

Emerging

World

Advanced

1/ Estimates of the output gap, in percent of potential GDP, are based on IMF staff calculations.

GDP growth rates of actual (solid line) versus potential (dashed line) for advanced economies. For emerging economies, Hodrick-Prescott filter applied for potential GDP.

10

What are the Policy Challenges?What are the Policy Challenges?

Implement forceful financial sector policiesImplement forceful financial sector policiesApply accommodative monetary policyApply accommodative monetary policyContinue fiscal stimulusContinue fiscal stimulusAnchor fiscal policy in a credible mediumAnchor fiscal policy in a credible medium--term term framework that addresses sustainability concernsframework that addresses sustainability concerns

11

Fiscal Stimulus in GFiscal Stimulus in G--20 in 2009 and 201020 in 2009 and 2010

0

1

2

3

4

5

Sout

h Af

rica

Ital

yTu

rkey

Indi

aBr

azil

Fran

ceU

nite

d St

ates

Saud

i Ara

bia

Uni

ted

King

dom

Indo

nesi

aAu

stra

liaAr

gent

ina

Mex

ico

Ger

man

yCa

nada

Japa

nCh

ina

Kore

aR

ussi

a

G-20: Discretionary Fiscal Measures, 20091

( In percent of GDP)

Source: IMF, staff estimates. 1 Defined as fiscal impulses in each year (yearly changesin structural fiscal balances related to measures taken in response to the current crisis).

Average

-3

-2

-1

0

1

Rus

sia

Kore

aSo

uth

Afri

caIn

done

sia

Uni

ted

King

dom

Japa

nAu

stra

liaCh

ina

Turk

eyCa

nada

Uni

ted

Stat

esIt

aly

Indi

aFr

ance

Braz

ilSa

udi A

rabi

aG

erm

any

G-20: Discretionary Fiscal Measures, 20101

( In percent of GDP)

Source: IMF, staff estimates. 1 A negative entry implies withdrawal of fiscal stimulus.

Average

12

Challenges for Emerging MarketsChallenges for Emerging Markets

DeleveragingDeleveraging is likely to weigh heavily on credit is likely to weigh heavily on credit creation and capital flowscreation and capital flowsMounting bank writeMounting bank write--downsdownsEmerging Europe has been particularly hit hardEmerging Europe has been particularly hit hardAsia and Latin America face less acute external Asia and Latin America face less acute external funding needsfunding needs

13

International Credit ProvisionInternational Credit Provision

-240

-180

-120

-60

0

60

120

04Q1 05Q1 06Q1 07Q1 08Q1

Net derivatives

Direct investment

Other investment

Portfolio investment

Total

Emerging Economies: Net Capital Flows Emerging Economies: Net Capital Flows ((US$ billions)US$ billions)

08Q408Q4

14

Sovereign Debt IssuesSovereign Debt Issues

Partial restoration of access to capital marketsPartial restoration of access to capital marketsRisks to financing the needs of emerging Risks to financing the needs of emerging markets aboundmarkets aboundDebt sustainability concerns may keep some Debt sustainability concerns may keep some emerging markets outemerging markets outPrudent debt management is all the more Prudent debt management is all the more importantimportant

15

Trade Finance and the Protectionist ThreatTrade Finance and the Protectionist Threat

Worrying signs of an increase in trade protectionWorrying signs of an increase in trade protectionRevival of trade is key to support global Revival of trade is key to support global economic recoveryeconomic recoveryTightening of lending standards constraining Tightening of lending standards constraining trade financetrade finance

16

Changes in the Pricing and Availability Changes in the Pricing and Availability of Trade Financeof Trade Finance

17

Outcome of GOutcome of G--20 Summit20 Summit

Consensus on need for coordinated global fiscal Consensus on need for coordinated global fiscal and monetary policiesand monetary policiesBoost in IMF resources and strengthening of its Boost in IMF resources and strengthening of its role in global economyrole in global economyNeed to strengthen financial regulatory systemsNeed to strengthen financial regulatory systems

18

Role of the IMFRole of the IMF

Continuation of efforts to adapt lending Continuation of efforts to adapt lending facilitiesfacilitiesCandid evenCandid even--handed and independent handed and independent surveillance, including the monitoring of fiscal surveillance, including the monitoring of fiscal and financial policy implementationand financial policy implementationDevelopment of early warning systemDevelopment of early warning systemAcceleration of reform of Acceleration of reform of IMFIMF’’ss governance governance structurestructure