the impact of environmental reporting on firms’ performance · pharmaceutical sector of pakistan...

TRANSCRIPT

Page 275

International Journal of Accounting & Business Management

www.ftms.edu.my/journals/index.php/journals/ijabm

Vol. 4 (No.2), November, 2016

ISSN: 2289-4519 DOI: 10.24924/ijabm/2016.11/v4.iss2/285.301

This work is licensed under a Creative Commons Attribution 4.0 International License.

Conceptual Paper

The Impact of Environmental Reporting on Firms’ Performance

Fahria Tasneem

School of Accounting and Business Management FTMS College, Malaysia [email protected]

Sahibzada Muhammad Hamza

School of Accounting and Business Management FTMS College, Malaysia

Abdul Basit School of Accounting and Business Management

FTMS College, Malaysia [email protected]

ABSTRACT

This study has focused on assessing the impact of environmental reporting on the performances of the firms in the USA for the year 2015. The research has been undertaken onto the Manufacturing companies listed in the National Association of Securities Dealers Automated Quotations (NASDAQ). The study is a quantitative research with the adaptation of descriptive explanatory research design. Previous researches have assessed the firms’ performance from one or two dynamics of environmental reporting. However, based on the literature review, this study would be signifying itself through the implication of the three key issues in today’s time. Thereby, Greenhouse Gas Emission, Water Consumption and Waste Disposal have been utilized as independent variables, whilst Market Share has been implied as a measure of firms’ performances. Hence, in order to establish the hypotheses written on the basis of the literature review, a study must be carried out on the manufacturing companies listed in NASDAQ.

Keywords: Firms Performance, Environmental reporting, NASDAQ

Page 286

1. Introduction

The purpose of conducting this research is to study the impact of environmental reporting on the performance of the firms in the United States of America (USA). The study will be carried out with the reference to the firms in the manufacturing industry listed in the National Association of Securities Dealers Automated Quotations (NASDAQ). Environmental Reporting was first discussed by Emerson (1844) in his study where he elaborated the importance of green marketing; it was further flourished by authors like Lepold (1940) and Carson (1962), where they legitimized the concept through their publications of cultural movements (Feldman, 2007; Carson, 1962). However, the concept of Corporate Social Responsibility (CSR) was first discussed in the early 1930’s (Carroll, 1999). Carroll (1999) discussed CSR as a reference to the obligations of businessmen to pursue policies, make decisions and follow series of actions which are desirable in terms of the objectives and values of the society. Additionally, the first environmental reports were published by organizations during the late 1980s and early 1990s; these were prepared for a range of reasons but the main driver was the requirement of disclosing toxic emissions data, especially for US companies (Bennett and James, 1999). It is difficult for firms to operate in today’s business world where consumers have, and require, more knowledge regarding firms’ products and services, their ways of operating and about the firm itself. Consumers in today’s world are more aware and wide awake when it comes to their society and environment’s prosperity and how it is been treated by the firms (Khuntia, 2014). Thus, it is a huge responsibility for organizations to carry out their operations in a social and responsible manner as it not only affects the societies but also the consumer’s decision on involving themselves with the specific organizations (Wu, 2014). This is where the importance of Environmental Reporting strikes in, because if firms are unable to provide the community with a proper assessment of the measurements that they are taking towards preventing the destruction of the environment that they work in, it is likely for the society to lower their demand for the firms’ services; thus in return it results in lowered firm productivity and profitability (Lindgreen, Kotler, Vanhamme and Maon, 2012). Moreover, according to Ulusan and Ag (n.d.), Environmental Reporting has been a rising concern in today’s business era as it not only keeps the society aware of the ongoing social activities, but also works as a competitive advantage for today’s companies. Thereby, in this business world where companies are buried with neck to neck competition, it is highly important for firms to draw Environmental Reports for not only to track down their social performance, but also to attract more consumers towards them and survive in the market (Battaglia, Testa, Bianchi, Iraldo and Frey, 2014; Madueno, Jorge, Conesa and Martinez-Martinez, 2015). In order to assess how the firms’ performance is affected by environmental reporting, several theoretical models and frameworks have been built till now. The models and theories that have been applied by past researchers are UN Global Compact (UNGC) (Bratenius and Melin, 2015), Millennium Development Goals (Skare and Golja, 2012), Triple Bottom Line (Reddy and Gordon, 2010), and Carroll’s Pyramid of Responsibilities (Classon and Dahlstrom, 2006). As more businesses started to join the economy, the more the society started to become knowledgeable and concerned towards the environment that they reside in (Everett, Ishwaran, Ansaloni and Rubin, 2010). For a latest number of years, companies have begun to produce regular environment or sustainability reports which detail the company’s impacts upon the environment and the ways the impacts are measured and monitored. As the concept of ER is popularized by the organizations recently, it is been a difficult yet interesting topic to study about, and thus a significant number of researches have been carried out to assess the impact on the firms’ performances through environmental reporting in several countries such as the Oil and Gas Companies in Niger Delta of Nigeria (Bassey, Effiok and Eton, 2013), Public Listed Companies in India (Makori and Jagongo, 2007), Tannery, Cement, Ceramics, Engineering, Food and Beverages sectors of Bangladesh (Ahmad, 2010), Electronic sector of Brazil (Murica and

Page 287

Souza, 2007), Manufacturing sector of Sri Lanka (Larojana and Theyarubanb, 2007) and the Pharmaceutical sector of Pakistan (Malik and Kanwal, 2016). To explore the impact of environmental reporting with the dynamics of developed countries, researches were carried out on countries such as Japan’s Electronic sector (Cortez and Cudia, 2009), Australia’s Chemical, Forestry and Paper, Industrial Engineering, Industrial Transport and Mining sectors (Bhattacharyya, 2007), and United Kingdom’s Oil and Gas, Basic Material, Industrial Consumer Goods, Health Care, Consumer Services, Telecommunication and Technology sectors (Qiu, 2009). The common and major variables that were implied in order to assess the firms’ performances are ROI, Leverage, ROE, ROA, Net Profit Margin, Current Ratio and ROCE; while variables such as recycling, proactive waste reduction, environmental design, greenhouse emission control and waste management has been used to assess the environmental reporting (Delmas and Blass, 2009; Dozier, 2016; Koehler, 2009). Moreover, majority of the researches have been conducted in the African countries, especially Nigeria (Che-Ahmad and Osazuwa and Mgbame, 2012; Marfo, Xuhua, Antway and Yiranbon, 2014); the second highest number of researches done on this concept is Pakistan (Mujaheed and Abdullah, 2014; Awan and Akhtar, 2014); following by Malaysia at the third highest (Mustafa, Othman and Perumal, 2012; Saleh, Zulkifli and Muhamad, n.d.). Due to the recent development of its popularity, there still have not been many researches done in this field and especially on the field of manufacturing industry. Thereby, this research would be shedding lights on the newer dynamics and providing the readers with more knowledge of environmental reporting. This research will be further contributing to the corporate world by providing them with the vision of the aspects of gaining the benefits through the current trend of operating in a social and responsible manner. Moreover, this research will help the community to understand the concept and importance of environmental reporting and develop the consciousness of the significance of making their decisions based on it. It will furthermore assist the researchers, who will be willing to conduct their researches on this area, with this research’s result and framework to develop the foundation of their literature.

1.1 Research objectives

To analyze the impact of Greenhouse Gas Emission (GHG) on the firms’ Market Share. To analyze the impact of Water Consumption on firms’ Market Share. To analyze the impact of firms’ Waste Disposal on its Market Share.

2. Literature Review

As cited in Pramanik, Shil and Das’ (2007) research paper, according to Das (1972) Environmental Reporting is the process by which a corporation communicates its information regarding range of its environmental activities to a variety of stakeholders. While Holmes and Sugden (1998) defined Environmental Reporting as the assessment of the impact of environmental issues on the company’s financial performance and that it requires changes to the way company discloses environmental issues in their annual/financial report (Jones, 1999). Environmental reporting is to fulfill its accountability regarding environmental efforts in their activities, and to provide useful information to decision making of interested parties (Frost and English, 2002). Moreover, Welford (2005) has expressed the report as company’s way for the provision of information about environmental performance, and meeting the needs of the financial markets and at the same time providing itself with a positive environmental image. Additionally, Sarivudeen and Sheham (2013) have considered Environmental Reporting as a valuable evaluation tool for corporations and individuals investors, as well as financial institution, when making investment and financing decisions.

Page 288

As discussed earlier, several theoretical models and frameworks have been applied in past researches to have a better understanding of the relationship between the concept of environmental reporting and firms’ performances. The United Nations Global Compact (UNGC) happens to be the world’s largest voluntary corporate sustainability initiative (The Global Compact, 2007); it is a strategic policy initiative for businesses which are in a commitment for supporting the ten universally accepted principles for environment, anti-corruption, labor and human rights. In today’s business era, countless business practices have been using UNGC’s principles as their moral compass (OECD, 2005). As stated by Bandi (2007), the UNGC is by all means a social legitimacy to the global markets, as the corporate sector is in strong contact with the UN and NGOs emerging of the civil society, ending up making it more transparent and visible to the public. Moreover by taking the UNGC initiative, businesses which are stated as the primary driver of globalization, will be ensuring that markets, technology and finance advances in ways that will benefit economies and societies everywhere (Rasche and Waddock, 2012). Similarly, the Millennium Development Goals (MDG) are the quantified goals or targets which addresses extreme poverty in its many dimensions; such as income poverty, hunger and disease, lack of adequate shelter, while promoting gender equality, education and environmental sustainability (United Nations, 2015). The accomplishment of each of the targets that specifically define them is based on measurable indicators, generally altogether acceptable in themselves (Amin, 2006). The MDG has been appreciated by researchers such Davis (2011) who has pointed out that the target of halving the proportion of people without access to an improved drinking water source was achieved in 2010, five years ahead of schedule. In 2012, 89 per cent of the world’s population had access to an improved source, up from 76 per cent in 1990 (MDG Report, 2014). However, the Millennium Development Goals have been criticized for its several aspects. Mishra (2004) and Oya (2011) called the goals ‘unrealistic’ and happen to believe that the MDGs avoid the limited local capacities, mainly the governance capabilities. Moreover, Keyzer and Wesenbeeck (2006) believed that 15 years has been too short as a timeframe to see a development and its progress. However, criticism against the United Nations Global Compact was raised by many researchers as well. Knudsen (2011) argued that the ten principles of the UNGC are minimal standards. It rests upon documents which are already in the recognition in majority of states and already anchored in national lawmaking. Moreover, the challenge for many firms is that the UN Global Compact offers a ‘one size fits all’ solution regarding environmental reporting. This is a problem because many firms therefore undertake CSR initiatives that fit the UN Global Compact rather than focusing on the kinds of initiatives that could best benefit the company and the society in which it operates (Lalonde, 2016). Despite the criticism, UN Global Compact is more appreciated as one of the main factors that UNGC takes into consideration is ‘environment’, and assists a research with a better understanding of the environmental factors. While MDGs has been focusing more on other factors such as reducing extreme poverty, the Global Compact’s work on environment is designed to help companies develop a holistic and comprehensive strategy. It asks business to actively address environmental risks and opportunities, and have major efforts progressing with business in the areas of “Climate” and “Water” (UNGC, 2014). For instance, they are committed to set greenhouse gas emissions reduction targets, to work collaboratively with other companies and governments, and to publicly report on performance on an annual basis (Deloitte, 2013). While these goals/initiatives were developed in recent years, theories and models have been built in past years too in order to assess the impact of mainly corporate social responsibility (CSR). Triple Bottom Line (TBL) was introduced by John Elkington (1994) to measure sustainability and argues that companies should prepare three different and separate bottom lines (Slaper and Hall, 2011). The TBL consists of three factors; profit, people and planet. The aim of this concept is to give the measurement of the financial, social and environment performances of a corporation trough a certain period of time (Slaper and Hall, 2007). Arguments were made supporting the concept of the Triple Bottom Lines. Mirinda (2016) stated that companies which relies on the production of cheap products made from fossil fuels is increasing the scarcity of resources; thus using the TBL approach, they will be more likely to

Page 289

diminish the risks by coming up with more sustainable options. Moreover, Carroll’s Pyramid of Responsibilities is been considered as one of the pioneer concept of Corporate Social Responsibility (Carroll, 1991). These responsibilities are such as Economical, Legal, Ethical and Philanthropic and are believed to be seen as together and not separated in order for a company to be profitable, minimize their cost, maximize their sales and improve their strategic decisions (Nalband and Kelabi, 2014). Meanwhile, Sridhar and Jones (2013) have criticized the measurement of TBL for being complex. They argued that the objectivity and reliability of the values obtained through measurement is doubtful, thus more attention should be given on the reliability of the obtained values than the ways it can be measured. Moreover, Alhaddi (2015) illustrated an argument stating the three Ps does not clearly address time as the fourth dimension. This dimension has its focus on preserving current values in all three other dimension for later, which indicates the short term and longer consequences of any action. In contrast, Hockerts et al. (2008) further argues that in Carroll’s CSR Pyramid, there is no need to represent CSR as a hierarchy (Dudovskiy, 2013). Unlike Maslow’s Hierarchy of Needs, there are weak or almost no relationships between CSR activities involved in each level in Carroll’s CSR Pyramid. Thereby, despite of having few drawbacks, Triple Bottom Line is an excellent match for collaborating with a study’s conceptual framework as two of the major issues that this model takes into account are “Waste Management” and “Greenhouse Emission” (WHO, 2013). Companies applying the TBL approach make an effort to reduce their ecological footprint by carefully managing its consumption of energy and non-renewable and reducing manufacturing waste as well as rendering waste less toxic before disposing of it in a safe and legal manner (Bradford, 2009). 2.1 Empirical Studies Rahman, Jauhari and Roslan (2013), carried out their research with the purpose of examining the link between environmental reporting practices and firm performance of Malaysia Public Listed Companies for the year 2009. They used content analysis to work on their framework which consists of independent variable, that is environmental reporting itself, and dependent variables, which are return on equity (ROE) and return on assets (ROA). In addition, control variables such as company size, leverage and industry sensitivity were used within the framework as well. The sample size was determined by using online sample size calculator by Raosoft. However, Rahman, Jauhari and Roslan (2013) concluded their research by revealing that 68.1% of 299 companies provide environmental information in their annual reports with an average of 7.82 sentences and 18.3% of the companies have separate environmental section in their annual reports. Moreover, insignificant relationship has been found between environmental reporting and ROA, while a significant relationship was found between environmental reporting and ROE, along with company size, leverage and industry sensitivity. Chetty, Naidoo and Seetharam (2014) carried out their research in South Africa to investigate the impact of environmental reporting on corporate financial performance (CFP). This is examined for a time period from 2004 to 2013, assessing the differences between short-term and long-term impact of CSR announcements on CFP of firms included in the Johannesburg Securities Exchange Socially Responsible Investment Index (JSE SRI). Regression analysis has been used as their methodology, and the framework included Corporate Social Responsibility Reports (CSR) as its independent variable, and their dependent variables consists of both Accounting-based measures (Return on Assets, Return on Equity and Earnings per Share) and Marketing-based measures (Market Capitalization and Risk). The research concluded with the finding that CSR activities lead to no significant differences in financial performances (Chetty, Naidoo and Seetharam, 2014). A research was conducted by Ahmad (2012) to find the significance of the environmental accounting and environmental reporting on Bangladeshi companies. This research was based on both primary and secondary data. The primary data were collected from the total number of 40 Chief Accountants and Senior Accountants, taking one from each company from different business sectors; while the secondary data were collected from the annual report s from the year 2010 of the companies. All the selected companies are listed companies of DSE. The

Page 290

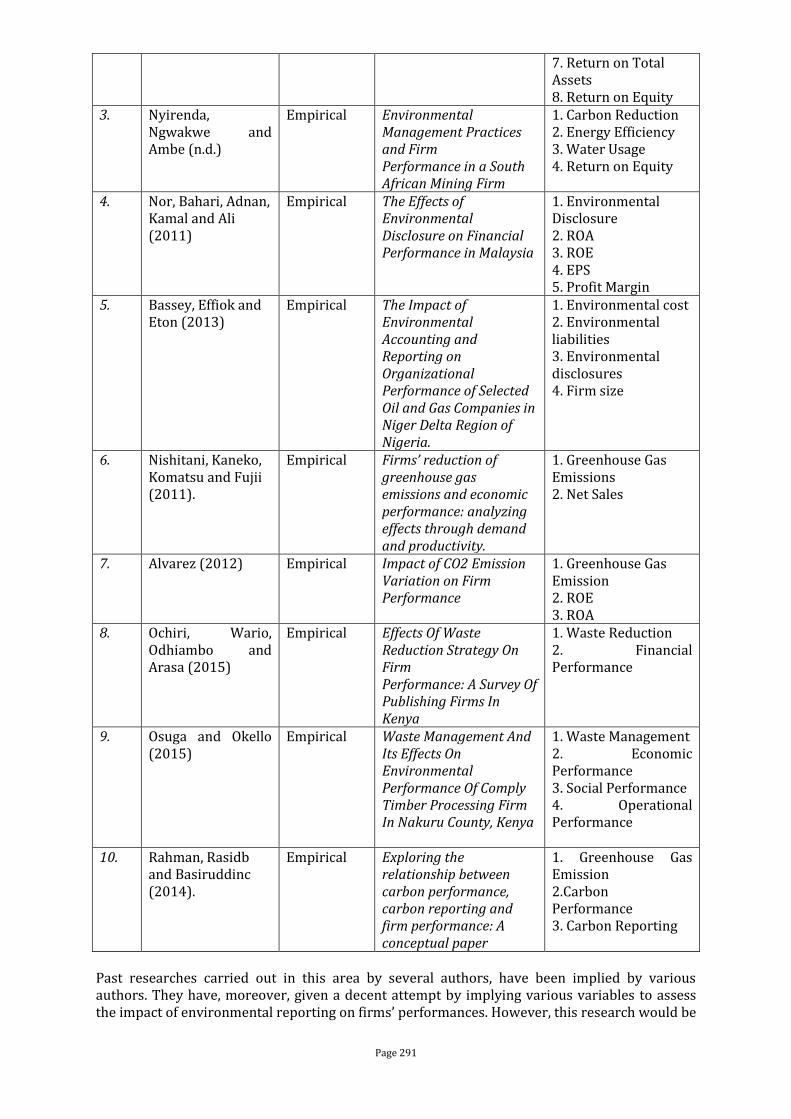

framework for this paper consists of two independent variables, Environmental Accounting and Environmental Reporting, while having Annual Reports as their dependent variable. The main findings of the study are: i) the respondents have felt the strong need for EA (Environmental Accounting) and ER (Environmental Reporting) in their Annual Reports, ii) as regards of nature of environmental disclosure, it is observed that only qualitative disclosures in positive sense have been provided in the Annual Reports either in Chairman or Managing Director statement, Directors’ reports and a separate section “Environmental Compliance”. Makori and Jagongo (2013) conducted their research in India with the objective of establishing whether there is any significant relationship between environmental reporting and profitability of selected firms listed in India. The data for this paper were collected from annual reports and accounts of 14 randomly selected quotes companies in Bombay Stock Exchange in India, and was analyzed using multiple regression models. His framework involved Environmental Accounting (amount spent on environmental protection) as its independent variable; and Return on Capital Employed (ROCE), Earnings per Share (EPS), Net Profit Margin and Dividend per Share as its dependent variables. The key findings of the study shows that there is significant negative relationship between Environmental Accounting and Return on Capital Employed (ROCE) and Earnings per Share (EPS) and a significant positive relationship between Environmental Accounting and Net Profit Margin and Dividend per Share. Murray, Sinclair, Power and Gray (2006) examined the relationship between social and environmental reporting and financial performance of Top 100 United Kingdom companies over the nine year period starting from the year 1989 to 1997. Total social and environmental, voluntary social and environmental and environmental disclosures were employed as the research’s independent variables; whereas just share price returns was employed as their dependent variable. Furthermore, content analysis was used for the data collected. According to their research, the relationships between share price returns and total social and environmental, voluntary social and environmental and environmental disclosures varied from year to year, varied across different forms of disclosure and swung between positive and negative over time. The table below shows the key summary of the variable identified.

Table 1: Empirical Studies and their Variables No. Authors Proposal Titles Measures/Variables

1. Rokhmawati, Sathye and Sathye (2015)

Empirical The Effect Of Greenhouse Gas Emissions On Financial Performance Of Listed Manufacturing Firms In Indonesia

1. Greenhouse Gas Emissions 2. Firm Social Performance 3. Firm Environmental Performance. 4. Return On Asset 5. Return On Equity 6. Return On Investment 7. Return On Investment Capital 8. Return On Sales 9. Tobin’s Q.

2. Ong, Teh and Ang (2014)

Empirical The Impact of Environmental Improvements on the Financial Performance of Leading Companies Listed in Bursa Malaysia

1. Materials Consumption 2. Energy Consumption 3. Water Consumption 4. Biodiversity 5. GHG Reduction 6. Waste Reduction

Page 291

7. Return on Total Assets 8. Return on Equity

3. Nyirenda, Ngwakwe and Ambe (n.d.)

Empirical Environmental Management Practices and Firm Performance in a South African Mining Firm

1. Carbon Reduction 2. Energy Efficiency 3. Water Usage 4. Return on Equity

4. Nor, Bahari, Adnan, Kamal and Ali (2011)

Empirical The Effects of Environmental Disclosure on Financial Performance in Malaysia

1. Environmental Disclosure 2. ROA 3. ROE 4. EPS 5. Profit Margin

5. Bassey, Effiok and Eton (2013)

Empirical The Impact of Environmental Accounting and Reporting on Organizational Performance of Selected Oil and Gas Companies in Niger Delta Region of Nigeria.

1. Environmental cost 2. Environmental liabilities 3. Environmental disclosures 4. Firm size

6. Nishitani, Kaneko, Komatsu and Fujii (2011).

Empirical Firms’ reduction of greenhouse gas emissions and economic performance: analyzing effects through demand and productivity.

1. Greenhouse Gas Emissions 2. Net Sales

7. Alvarez (2012) Empirical Impact of CO2 Emission Variation on Firm Performance

1. Greenhouse Gas Emission 2. ROE 3. ROA

8. Ochiri, Wario, Odhiambo and Arasa (2015)

Empirical Effects Of Waste Reduction Strategy On Firm Performance: A Survey Of Publishing Firms In Kenya

1. Waste Reduction 2. Financial Performance

9. Osuga and Okello (2015)

Empirical Waste Management And Its Effects On Environmental Performance Of Comply Timber Processing Firm In Nakuru County, Kenya

1. Waste Management 2. Economic Performance 3. Social Performance 4. Operational Performance

10. Rahman, Rasidb and Basiruddinc (2014).

Empirical Exploring the relationship between carbon performance, carbon reporting and firm performance: A conceptual paper

1. Greenhouse Gas Emission 2.Carbon Performance 3. Carbon Reporting

Past researches carried out in this area by several authors, have been implied by various authors. They have, moreover, given a decent attempt by implying various variables to assess the impact of environmental reporting on firms’ performances. However, this research would be

Page 292

taking the inspiration from previous researches and implying the variables which are most suitable for today’s business world. Moreover, also on the basis of the theoretical perspective such as UN Global Compact and Millennium Development Goals which have been focusing on helping businesses take initiatives in lowering environmental risks in the areas of “Climate” and “Water”, Greenhouse Emissions (Rokhmawati, Sathye and Sathye, 2015) and Water Consumptions (Ong, Teh and Ang, 2014) are believe to be more appropriate measures for this study (UNGC, 2014). While considering the fact that one of the major issues considered by Triple Bottom Line is “Waste Management”, Waste Disposal (Osuga and Okello, 2015) would be a fine choice for assessing the environmental impact (WHO, 2013). Thus, these three independent variables have been taken into account as the measurements for environmental reporting, while Market Share has been implied as to measure firms’ performances (Nishitani, Kaneko, Komatsu and Fujii, 2011).

H1: Greenhouse Gas Emissions have a positive significant impact on Market Share. Greenhouse gas emissions are the gaseous compounds which are found in atmosphere and have the capability to absorb infrared radiation by trapping the harmful heat in the atmosphere (EPA, 2014). The greenhouse emission has contributed a large share to global warming and thus it is believed to be one of the most concerned areas in the environmental aspects. When a firm, especially in the industry sectors whose energy production usage engages emissions of significant quantities of greenhouse gasses, has given a better environmental performance, it creates its image as an environmental friendly firm in the public’s eye; and thus it boosts their market share and even enable them to charge higher prices for their products (Nishitani, Kaneko, Komatsu and Fujii, 2011; Bradford and Fraser, 2008). Thereby, an effort in reducing greenhouse emissions will increase a firm’s added value as it will be increasing the demand for their offered product or services and hence improving their productivity (Ikkatai, Ishikawa, Ohori and Sasaki, 2008).

H2: Water Consumption has a positive significant impact on Market Share.

According to Hoekstra and Mekonnen (2011), the demand for freshwater has increased by 64 billion m3 per year. It is been recorded that worldwide, 70% water consumption has accounted for agriculture while 20% for industrial use and 10% for domestic (UN Water, 2015). It is been found that a positive link builds up between firms performance and natural resources, water consumption, when it is used efficiently (Ong, The and Ang, 2014). Due to cost saving solutions and water reduction plans, it directly increases the profitability of the company. This initiative not only reduces overall expenses but also gives the firms a “green image”, hence enhancing the public’s demands (Konar and Cohen, 2001). Thus, with reduced cost and increased demand, firms’ market share is enhanced as well.

H3: Waste Disposal has a positive significant impact on Market Share. With the growing concern of waste disposal, firms have started to apply Waste Reduction Strategies. Applying these strategies turned out to be beneficial via not only reducing the waste produced, but also reducing storage space, reducing energy usage and also reduction in the cost of labour (Ochiri, Wario, Odhiambo and Arasa, 2015). Moreover, it also reduces the total waste sent to landfills, conserves natural resources and significantly brings a reduction in the greenshouse gas emissions. This initiative has turned out to be cost saving strategy too which enhances the company’s profitability (Lyson and Farrington, 2006). The Conceptual Framework as per this research is illustrated below:

Page 293

3. Methodology

This paper has adapted the descriptive explanatory research design and is based on the collection of secondary data. All the data would be extracted from the companies’ published annual reports, Corporate Social Responsibility (CSR) reports and Sustainability reports for the year of 2015. As mentioned earlier, this study is based on the US Manufacturing Industry within the time span of one year. For this research, the manufacturing industry is divided into 5 sub-sectors of Energy, Healthcare, Technology, Public Utilities and Capital Goods. Thus, as listed in the NASDAQ, the total population for this study is 2428 companies, while our sample size is 100 companies.

As per this research, within the 5 sub-sectors of the US manufacturing industry, we have taken 20 companies from each sector which equals to a total of 100 companies. Moreover, as not all companies have been producing or publishing their environmental reports, convenience sampling has been applied. This not only makes it easier to use but also eliminates the complications of using randomized sampling (Farrokhi and Hamidabad, 2012). Thereby, the collaboration of Convenience-Quota sampling technique is applied. 4. Conclusion

Based on the critical review of the empirical literature and theoretical perspectives of environmental reporting, it is concluded that the 3 independent factors (Greenhouse Gas Emissions, Water Consumption and Waste Disposal) considered in the conceptual framework are key indicators of environmental reporting which is been widely enlightened into the empirical frameworks of environmental reporting like UN Global Compact, Millennium Development Goals, Triple Bottom Line and Carroll’s CSR Pyramid. Further it was also been a hot consideration in the scholarly circles of the environmental practitioner which are impacting the financial and operating performance of the firms in current business world. Hence, this has convinced the researcher to include these independent factors in the designed conceptual

Page 294

framework for this study to see its impact on firm’s performance in the companies registered in NASDAQ.

Reference Ahmad, A., 2012. Environmental Accounting and Reporting Practices: Significance and Issues: A Case from Bangaldeshi Companies. Global Journal of Management and Business Research, [online] 12(14). Available at: <https://globaljournals.org/GJMBR_Volume12/10-Environmental-Accounting-and-Reporting.pdf> [Accessed 7 Sep. 2016]. Alhaddi, H., 2015. Triple Bottom Line and Sustainability: A Literature Review. Business and Management Studies, [online] 1(2). Available at: <https://www.google.com.my/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&cad=rja&uact=8&ved=0ahUKEwjQkqu0krHQAhUcTI8KHYJ0A4YQFggZMAA&url=http%3A%2F%2Fredfame.com%2Fjournal%2Findex.php%2Fbms%2Farticle%2Fdownload%2F752%2F697&usg=AFQjCNFwY0HqJVsn9W31vsu39hUBGB_J4A> [Accessed 10 Oct. 2016]. Alvarez, I., 2012. Impact of CO2Emission Variation on Firm Performance. Business Strategy and the Environment, [online] 21(7), pp.435-454. Available at: <http://onlinelibrary.wiley.com/doi/10.1002/bse.1729/abstract> [Accessed 9 Oct. 2016].

Page 295

Alvarez, I., 2012. Impact of CO2Emission Variation on Firm Performance. Business Strategy and the Environment, [online] 21(7), pp.435-454. Available at: <http://onlinelibrary.wiley.com/doi/10.1002/bse.1729/abstract> [Accessed 10 Oct. 2016]. Amin, S., 2006. The Millennium Development Goals: A Critique from the South. [online] 57(10). Available at: <http://monthlyreview.org/2006/03/01/the-millennium-development-goals-a-critique-from-the-south/> [Accessed 8 Aug. 2016]. Bandi, N., 2007. United Nations Global Compact: Impact and its Critics. [online] Available at: <http://www.ethicalquote.com/docs/UnitedNationsGlobalCompact.pdf> [Accessed 14 Aug. 2016]. Bassey, B., Effiok, S. and Eton, O., 2013. The Impact of Environmental Accounting and Reporting on Organizational Performance of Selected Oil and Gas Companies in Niger Delta Region of Nigeria. Research Journal of Finance and Accounting, [online] 4(3). Available at: <https://www.google.com.my/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&cad=rja&uact=8&ved=0ahUKEwiW75WHsLbQAhXLtI8KHUptD84QFgggMAE&url=http%3A%2F%2Fwww.iiste.org%2FJournals%2Findex.php%2FRJFA%2Farticle%2Fdownload%2F4962%2F5045&usg=AFQjCNGGOOB20cMizADI0kR4WM_NdJ08Tg&bvm=bv.139250283,d.c2I> [Accessed 10 Oct. 2016]. Battaglia, M., Testa, F., Bianchi, L., Iraldo, F. and Frey, M., 2014. Corporate Social Responsibility and Competitiveness within SMEs of the Fashion Industry: Evidence from Italy and France. Sustainability, [online] 6(2), pp.872-893. Available at: <http://eprints.lancs.ac.uk/73579/1/sustainability_06_00872.pdf> [Accessed 11 Jul. 2016]. Bennett, M. and James, P., 1999. Sustainable Measures: Evaluation and Reporting of Environmental and Social Perfromance. [online] Available at: <https://books.google.com.my/books?id=I0iChJeHaC4C&pg=PA76&lpg=PA76&dq=Bennett+and+James,+1999&source=bl&ots=4ic5ma_0FZ&sig=E-EcEIdhTCMThm7lcKDQiLHxpjY&hl=en&sa=X&ved=0ahUKEwjBoMux_rDQAhXFOY8KHT7iAlwQ6AEINTAI#v=onepage&q=Bennett%20and%20James%2C%201999&f=false> [Accessed 15 Jul. 2016]. Bradford, J. and Fraser, E., 2008. Local authorities, climate change and small and medium enterprises: identifying effective policy instruments to reduce energy use and carbon emissions. Corporate Social Responsibility and Environmental Management, [online] 15(3), pp.156-172. Available at: <http://onlinelibrary.wiley.com/doi/10.1002/csr.151/abstract> [Accessed 17 Nov. 2016]. Bradford, J., 2009. The Triple Bottom Line of Sustainable Agriculture. [online] Farmland LP. Available at: <http://www.farmlandlp.com/2009/11/triple-bottom-line-sustainable-agriculture/> [Accessed 15 Nov. 2016]. Bratenius, A. and Melin, E., 2015. The Impact of CSR on Financial Performance. [online] Available at: <http://studenttheses.cbs.dk/bitstream/handle/10417/5336/anna_linnea_helena_braatenius_og_emilie_josefin_melin.pdf?sequence=1> [Accessed 8 Aug. 2016]. Carroll, A., 1991. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, [online] 34(4), pp.39-48. Available at: <http://www.sciencedirect.com/science/article/pii/000768139190005G> [Accessed 16 Oct. 2016]. Carroll, A., 1999. Corporate Social Responsibility: Evolution of a Definitional Construct. Business & Society, [online] 38(3), pp.268-295. Available at: <http://bas.sagepub.com/content/38/3/268.abstract> [Accessed 8 Jul. 2016].

Page 296

Carson, R., 1962. Silent Spring. [online] Available at: <http://library.uniteddiversity.coop/More_Books_and_Reports/Silent_Spring-Rachel_Carson-1962.pdf> [Accessed 15 Sep. 2016]. Chetty, S., Naidoo, R. and Seetharam, Y., 2015. The Impact of Corporate Social Responsibility on Firms’ Financial Performance in South Africa. 9, [online] 2. Available at: <https://www.google.com.my/url?sa=t&rct=j&q=&esrc=s&source=web&cd=3&cad=rja&uact=8&ved=0ahUKEwjXjsO9qLbQAhUIuo8KHfNmDdUQFggvMAI&url=http%3A%2F%2Fwe.vizja.pl%2Fen%2Fdownload-pdf%2Fid%2F394&usg=AFQjCNHQO_iwLINQJG7hggPx2g4Ky0Kd7g&bvm=bv.139250283,d.c2I> [Accessed 7 Sep. 2016]. Classon, J. and Dahlstrom, J., 2006. How can CSR affect company performance?. [online] Available at: <http://www.diva-portal.org/smash/get/diva2:6476/fulltext01> [Accessed 12 Nov. 2016]. Davis, K., 2016. A Successful Failure: The Millennium Development Goal Project in Tanzania. [online] Available at: <http://crhsgg-studentresources.wikispaces.umb.edu/file/view/Kirsten+Davis+Capstone+2011.pdf> [Accessed 23 Aug. 2016]. Delmas, M. and Blass, V., 2009. Measuring Corporate Environmental Performance: The Trade-Offs Of Sustainability Ratings. [online] Available at: <http://www.environment.ucla.edu/perch/resources/delmas-doctori-blass-bse-1.pdf> [Accessed 12 Aug. 2016]. Deloitte, 2013. Global Impact Report. [online] Available at: <https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/gx-gr13-main-report.pdf> [Accessed 23 Sep. 2016]. Dozier, B., 2016. Effect of Corporate Social Responsibility on Firms Performance Telecommunication Industry in USA. [online] Available at: <https://barbradozier.wordpress.com/2016/05/30/effect-of-corporate-social-responsibility-on-firms-performance-telecommunication/> [Accessed 11 Aug. 2016]. Dudovskiy, J., 2013. Carrol’s CSR Pyramid and It’s Relation to Modern Environment - Research Methodology. [online] Research Methodology. Available at: <http://research-methodology.net/carrols-csr-pyramid-and-its-relation-to-modern-environment/> [Accessed 16 Oct. 2016]. EPA, 2014. Global Greenhouse Gas Emissions. [online] Available at: <https://www3.epa.gov/climatechange/pdfs/print_global-ghg-emissions-2014.pdf> [Accessed 17 Nov. 2016]. Everett, T., Ishwaran, M., Ansaloni, P. and Rubin, A., 2010. Economic Growth and the Environment. Defra Evidence and Analysis Series. [online] Available at: <https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/69195/pb13390-economic-growth-100305.pdf> [Accessed 8 Aug. 2016]. Farrokhi, F. and Hamidabad, A., 2012. Rethinking Convenience Sampling: Defining Quality Criteria. TPLS, [online] 2(4). Available at: <http://www.academypublication.com/issues/past/tpls/vol02/04/20.pdf> [Accessed 14 Oct. 2016]. Feldman, J., 2007. Public opinion, the Leopold Report, and the reform of federal predator control policy. 1, [online] 1. Available at: <http://digitalcommons.unl.edu/cgi/viewcontent.cgi?article=1119&context=hwi> [Accessed 3 Sep. 2016].

Page 297

Frost, G. and Englsih, L., 2002. Mandatory corporate environmental reporting in Australia. [online] Australianreview.net. Available at: <http://www.australianreview.net/digest/2002/11/frost.html> [Accessed 8 Aug. 2016]. Herrera Madueño, J., Larrán Jorge, M., Martínez Conesa, I. and Martínez-Martínez, D., 2015. Relationship between corporate social responsibility and competitive performance in Spanish SMEs: Empirical evidence from a stakeholders’ perspective. BRQ Business Research Quarterly, [online] 19(1), pp.55-72. Available at: <http://ac.els-cdn.com/S2340943615000699/1-s2.0-S2340943615000699-main.pdf?_tid=17e46684-ad24-11e6-a4fd-00000aacb360&acdnat=1479428301_1c862a784a4f526d6c183e158b9e9a37> [Accessed 11 Jul. 2016]. Hoekstra, A. and Mekonnen, M., 2012. The water footprint of humanity. Proceedings of the National Academy of Sciences, [online] 109(9), pp.3232-3237. Available at: <http://www.pnas.org/content/109/9/3232.full> [Accessed 15 Nov. 2016]. Ikkatai, S., Ishikawa, D., Ohori, S. and Sasaki, K., 2008. Motivation of Japanese companies to take environmental action to reduce their greenhouse gas emissions: an econometric analysis. Sustainability Science, [online] 3(1), pp.145-154. Available at: <http://link.springer.com/article/10.1007/s11625-008-0048-y> [Accessed 17 Nov. 2016]. Jones, K., 1999. Study on Environmental Reporting by Companies. [online] Available at: <http://edz.bib.uni-mannheim.de/www-edz/pdf/1999/environreport.pdf> [Accessed 14 Nov. 2016]. Keyzer, M. and Wesenbeeck, L., 2006. The Millennium Development Goals, How Realistic Are They?. [online] 154(3), pp.443-466. Available at: <http://link.springer.com/article/10.1007/s10645-006-9019-9> [Accessed 6 Aug. 2016]. Keyzer, M. and Wesenbeeck, L., 2006. The Millennium Development Goals, How Realistic Are They?. De Economist, [online] 154(3), pp.443-466. Available at: <http://link.springer.com/article/10.1007/s10645-006-9019-9> [Accessed 24 Sep. 2016]. Khuntia, R., 2014. Corporate Environmental Reporting: A Changing Trend In The Corporate World For Sustainable Development. Impact Journals, [online] 2(10). Available at: <http://file:///C:/Users/User/Downloads/--1414671727-3.Management-CORPORATE%20ENVIRONMENTAL%20REPORTING%20A%20CHANGING%20TREND%20IN%20THE%20CORPORATE%20WORLD%20FOR%20SUSTAINABLE%20DEVELOPMENT%20(1).pdf> [Accessed 16 Aug. 2016]. Knudsen, J., 2011. Which Companies Benefit Most from UN Global Compact Membership?. [online] The European Business Review. Available at: <http://www.europeanbusinessreview.com/which-companies-benefit-most-from-un-global-compact-membership/> [Accessed 14 Aug. 2016]. Koehler, D., 2009. Capital Markets and Corporate Environmental Performance: Research in Untied States. [online] Available at: <http://opim.wharton.upenn.edu/risk/downloads/archive/arch33.pdf> [Accessed 9 Aug. 2016]. Lindgreen, A., Kotler, P., Vanhamme, J. and Maon, F., 2012. A Stakeholder Approach to Corporate Social Responsibility. [online] Available at: <https://books.google.com.my/books?id=DAzACwAAQBAJ&pg=PA385&lpg=PA385&dq=Garcia-Castro+et+al,+2010&source=bl&ots=gCT70eUtMs&sig=46EL1WSoO8uEa2lvf2GI_pQeU3s&hl=en&sa=X&ved=0ahUKEwi9iZjJ0c7PAhXFt48KHc3mAwMQ6AEIJDAB#v=onepage&q=Garcia-Castro%20et%20al%2C%202010&f=false> [Accessed 19 Sep. 2016].

Page 298

Makori, D. and Jagongo, A., 2013. Environmental Accounting and Firm Profitability: An Empirical Analysis of Selected Firms Listed in Bombay Stock Exchange, India. International Journal of Humanities and Social Science, [online] 3(18). Available at: <http://www.ijhssnet.com/journals/Vol_3_No_18_October_2013/24.pdf> [Accessed 8 Sep. 2016]. Miranda, C., 2016. The Triple Bottom Line and Why It's Crucial for Businesses. [online] Cultivating Capital. Available at: <http://www.cultivatingcapital.com/business-sustainability-triple-bottom-line/> [Accessed 3 Sep. 2016]. Murray, A., Sinclair, D., Power, D. and Gray, R., 2005. Do Financial Markets Care About Social And Environmental Disclosure? Further Evidence And Exploration From The UK. [online] Available at: <https://www.st-andrews.ac.uk/media/csear/discussion-papers/CSEAR_dps-finance-dofinmar.pdf> [Accessed 8 Aug. 2016]. Murray, A., Sinclair, D., Power, D. and Gray, R., 2005. Do Financial Markets Care About Social And Environmental Disclosure? Further Evidence And Exploration From The UK. Centre for Social and Environmental Accounting Research. [online] Available at: <https://www.st-andrews.ac.uk/media/csear/discussion-papers/CSEAR_dps-finance-dofinmar.pdf> [Accessed 8 Sep. 2016]. Nalband, N. and Kelabi, S., 2014. Redesigning Carroll’s CSR Pyramid Model. JOAMS, [online] 2(3), pp.236-239. Available at: <http://www.joams.com/uploadfile/2014/0217/20140217024434433.pdf> [Accessed 19 Sep. 2016]. Nishitani, K., Kaneko, S., Komatsu, S. and Fujii, H., 2011. Firms' reduction of greenhouse gas emissions and economic performance: analyzing effects through demand and productivity. [online] Available at: <http://ir.lib.hiroshima-u.ac.jp/files/public/3/31636/20141016182116634025/IDEC-DP2_01-1.pdf> [Accessed 22 Oct. 2016]. Nishitani, K., Kaneko, S., Komatsu, S. and Fujii, H., 2011. Firms’ reduction of greenhouse gas emissions and economic performance: analyzing effects through demand and productivity. [online] 1(1). Available at: <http://ir.lib.hiroshima-u.ac.jp/files/public/3/31636/20141016182116634025/IDEC-DP2_01-1.pdf> [Accessed 10 Oct. 2016]. Nor, N., Bahari, N., Adnan, N., Kamal, S. and Ali, I., 2016. The Effects of Environmental Disclosure on Financial Performance in Malaysia. Procedia Economics and Finance, [online] 35, pp.117-126. Available at: <http://www.sciencedirect.com/science/article/pii/S2212567116000162> [Accessed 10 Oct. 2016]. Nyirenda, G., Ngwakwe, C. and Ambe, C., n.d. Environmental Management Practices and Firm Performance in a South African Mining Firm. Managing Global Transitions, [online] 11(3), pp.243–260. Available at: <http://www.fm-kp.si/zalozba/ISSN/1581-6311/11_243-260.pdf> [Accessed 8 Oct. 2016]. Ochiri, G., Wario, G., Odhiambo, R. and Arasa, R., 2015. Effects Of Waste Reduction Strategy On Firm Performance: A Survey Of Publishing Firms In Kenya. International Journal of Economics, Commerce and Management, [online] 3(5). Available at: <http://ijecm.co.uk/wp-content/uploads/2015/05/3581.pdf> [Accessed 10 Oct. 2016]. OECD, 2005. The UN Global Compact And The Oecd Guidelines For Multinational Enterprises: Complementarities And Distinctive Contributions. [online] Available at: <http://www.oecd.org/investment/mne/34873731.pdf> [Accessed 16 Sep. 2016]. Ong, T., Teh, B. and Ang, Y., 2014. The Impact of Environmental Improvements on the Financial Performance of Leading Companies Listed in Bursa Malaysia. International Journal of Trade, Economics and Finance, [online] 5(5), pp.386-391. Available at: <http://www.ijtef.org/papers/403-C3003.pdf> [Accessed 16 Nov. 2016].

Page 299

Osuga, V. and Okello, B., 2015. Waste Management And Its Effects On Environmental Performance Of Comply Timber Processing Firm In Nakuru County, Kenya. International Journal of Economics, Commerce and Management, [online] 3(6). Available at: <http://ijecm.co.uk/wp-content/uploads/2015/06/3619.pdf> [Accessed 10 Oct. 2016]. Post, J., 2012. The United Nations Global Compact: A CSR Milestone. Business & Society, [online] 52(1), pp.53-63. Available at: <http://bas.sagepub.com/content/52/1/53.short> [Accessed 13 Aug. 2016]. Pramanik, A., Shil, N. and Das, B., 2007. Environmental accounting and reporting with special reference to India. [online] Available at: <https://mpra.ub.uni-muenchen.de/7712/1/Environmental_Accounting_and_Rep> [Accessed 8 Aug. 2016]. Rahman, N., Jauhari, H. and Roslan, N., 2013. An Empirical Examination of the Relationship between Environmental Disclosure and Financial Performance in Malaysia. Journal of Contemporary Issues and Thought, [online] 3. Available at: <https://www.google.com.my/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&cad=rja&uact=8&ved=0ahUKEwjwgcWvp7bQAhVMvo8KHRWwAb4QFggZMAA&url=http%3A%2F%2Fwww.mycite.my%2Fen%2Ffiles%2Farticle%2F83987&usg=AFQjCNHvuNkZlUQQB9hMF15izHfKduqhfA&bvm=bv.139250283,d.c2I> [Accessed 7 Sep. 2016]. Rahman, N., Rasid, S. and Basiruddin, R., 2014. Exploring the Relationship between Carbon Performance, Carbon Reporting and Firm Performance: A Conceptual Paper. Procedia - Social and Behavioral Sciences, [online] 164, pp.118-125. Available at: <http://repo.uum.edu.my/13368/1/18.pdf> [Accessed 14 Nov. 2016]. Rahman, N., Rasid, S. and Basiruddin, R., 2014. Exploring the Relationship between Carbon Performance, Carbon Reporting and Firm Performance: A Conceptual Paper. Procedia - Social and Behavioral Sciences, [online] 164, pp.118-125. Available at: <http://repo.uum.edu.my/13368/1/18.pdf> [Accessed 10 Oct. 2016]. Rasche, A., Waddock, S. and McIntosh, M., 2012. The United Nations Global Compact: Retrospect and Prospect. Business & Society, [online] 52(1), pp.6-30. Available at: <http://bas.sagepub.com/content/52/1/6.abstract> [Accessed 9 Aug. 2016]. Reddy, K. and Gordonb, L., 2010. The Effect of Sustainability Reporting on Financial Performance: An Empirical Study Using Listed Companies. [online] Available at: <http://researchcommons.waikato.ac.nz/bitstream/handle/10289/7658/Reddy%202010%20Effect.pdf?sequence=1> [Accessed 15 Nov. 2016]. Rokhmawati, A., 2015. The Effect Of Greenhouse Gas Emissions On Financial Performance Of Listed Manufacturing Firms In Indonesia. [online] Available at: <http://www.canberra.edu.au/researchrepository/file/663069a2-7059-465a-bca6-1eaaca26ff42/1/full_text.pdf> [Accessed 5 Nov. 2016]. Rokhmawati, A., Sathye, M. and Sathye, S., 2015. The Effect of GHG Emission, Environmental Performance, and Social Performance on Financial Performance of Listed Manufacturing Firms in Indonesia. Procedia - Social and Behavioral Sciences, [online] 211, pp.461-470. Available at: <http://www.sciencedirect.com/science/article/pii/S1877042815054014> [Accessed 10 Oct. 2016]. Sarivudeen, A. and Sheham, A., 2013. Corporate Governance Practices and Environmental Reporting: A Study of Selected Listed Companies in Sri Lanka. [online] Available at: <https://www.researchgate.net/publication/294882734_Corporate_Governance_Practices_and_Environmental_Reporting_A_Study_of_Selected_Listed_Companies_in_Sri_LankaEnter_title> [Accessed 12 Aug. 2016].

Page 300

Skare, M. and Golja, T., 2012. Corporate Social Responsibility And Corporate Financial Performance Is There A Link? Economic Research, [online] 25(1). Available at: <https://www.google.com.my/url?sa=t&rct=j&q=&esrc=s&source=web&cd=9&cad=rja&uact=8&ved=0ahUKEwiuifzviq7QAhVJrI8KHeu0AxIQFghVMAg&url=http%3A%2F%2Fhrcak.srce.hr%2Ffile%2F151814&usg=AFQjCNFJ4AZNFf5TgAkdKFsDnyQyBqzOHw&bvm=bv.139138859,d.c2I> [Accessed 15 Nov. 2016]. Slaper, T. and Hall, T., 2011. The Triple Bottom Line: What Is It and How Does It Work?. [online] Available at: <http://www.ibrc.indiana.edu/ibr/2011/spring/pdfs/article2.pdf> [Accessed 9 Aug. 2016]. Sridhar, K. and Jones, G., 2013. The three fundamental criticisms of the Triple Bottom Line approach: An empirical study to link sustainability reports in companies based in the Asia-Pacific region and TBL shortcomings. Asian Journal of Business Ethics, [online] 2(1), pp.91-111. Available at: <http://link.springer.com/article/10.1007/s13520-012-0019-3> [Accessed 19 Sep. 2016]. Ulusan, H. and Ag, Y., n.d. Environmental Reporting for Companies. [online] Available at: <http://www.academia.edu/2452171/Environmental_Reporting_For_Companies> [Accessed 18 Jul. 2016]. UN Global Compact, 2007. UN Global Compact Annual Review: 2007 Leaders Summit. [online] Available at: <https://www.unglobalcompact.org/docs/news_events/8.1/GCAnnualReview2007.pdf> [Accessed 8 Aug. 2016]. UN Water, 2016. UN-Water. [online] United Nation Water. Available at: <http://www.unwater.org/> [Accessed 14 Nov. 2016]. United Nations, 2014. The Millennium Development Goals Report 2014. [online] Available at: <http://www.un.org/millenniumgoals/2014%20MDG%20report/MDG%202014%20English%20web.pdf> [Accessed 10 Aug. 2016]. United Nations, 2015. The Millennium Development Goals Report 2015. [online] Available at: <http://www.un.org/millenniumgoals/2015_MDG_Report/pdf/MDG%202015%20Summary%20web_english.pdf> [Accessed 15 Sep. 2016]. Welford, R., 2005. Editorial. Corporate Social Responsibility and Environmental Management, [online] 12(2), pp.61-61. Available at: <http://onlinelibrary.wiley.com/doi/10.1002/csr.90/abstract> [Accessed 11 Aug. 2016].

Page 301