the increased importance of earnings announcements...

TRANSCRIPT

The Increased Importance of Earnings Announcements after Regulation FD: Evidence from Revisions of

Analysts’ Forecasts and Pre-Announcements

Ron Lazer Stern School of Business

New York University 44 West 4th St. #10-184 New York, NY 10012

(212) 998 - 0036 [email protected]

Preliminary Draft – January 2004 Comments Welcome

Abstract

Regulation Fair Disclosure (Reg FD) was issued to prevent or mitigate the selective disclosure of material information to selected analysts and investors, beginning October 23, 2000. One expected effect of Reg FD is a reduction in private disclosure of material financial information to financial analysts before the earnings announcement. If analysts obtain less private information from management after Reg FD, they are more likely to depend on the subsequent public earnings disclosure in revising their forecasts. My results show a significant decrease in the time until analysts revise their forecasts after earnings announcements during the post-Reg FD period as compared to the period before Reg FD, and a significant increase in the absolute magnitude of these revisions. Also, forecast revisions prior to the earnings announcement in the post-Reg FD period, which are likely based on less private information conveyed by management to analysts, correspond less closely to the actual change in subsequent earnings than in the pre-Reg FD period. Finally, in the post-Reg FD period, I document an increase in the occurrence of voluntary disclosures issued by companies as pre-announcements – company disclosures during the reporting period, after controlling for changes in the economic environment between the pre- and post- Reg FD periods.

1

The Increased Importance of Earnings Announcements after Regulation FD: Evidence from Revisions of

Analysts’ Forecasts and Pre-Announcements

Regulation FD was issued to prevent or mitigate the widespread practice of

selective disclosure of material information by management to a restricted group of

analysts and influential investors. Its purpose was to level the playing field for all

market participants and prevent the loss of investor confidence in the integrity of

capital markets. The SEC was also concerned about the potential for management to

use material information as leverage on some analysts or investors, effectively

discouraging negative reports.1 The restrictions on this private channel became

effective October 23, 2000. After this date, financial analysts have less private

information provided to them by management, which is likely to cause changes in

their forecast revisions. Another expected effect is a shift in the content and

importance of companies’ announcements. Companies are expected to handle the

decrease in information conduits by finding alternative methods that are congruent

with the new rule. One such alternative could be additional public disclosures as pre-

announcements. Another could be enhanced disclosure during the earnings

announcements themselves. In this paper, I provide evidence for changes in attributes

of analyst forecasts and changes in corporate disclosures.

Assuming that companies behave according to the restrictions of Reg FD, that

analysts obtain less private information from management during the reporting period,

and that earnings are as informative post-Reg FD as before, I expect that the public

disclosure of earnings is likely to capture a larger component of the total information

1 http://www.sec.gov/rules/final/33-7881.htm.

2

that analysts use to forecast earnings for the next reporting period. Consequently,

analysts are expected to revise their forecasts closer after the earnings announcement

in the post-Reg FD period than before. Furthermore, the revisions after the disclosure

of earnings are expected to be larger in absolute magnitude during the post-Reg FD

period than before, because the actual earnings announcement provides a larger

amount of new information. Similarly, forecast revisions during the reporting period

are expected to be less consistent with the actual change in subsequent earnings

during the post-Reg FD period than before, because analysts are deprived of the

private information that management disclosed to them prior to Reg FD.

My results show a significant and overwhelming decrease in the time it takes

analysts to revise their forecasts immediately after the earnings announcement in the

post-Reg FD era. I also show that there is a significant increase in the magnitude of

forecast revisions issued immediately after earnings announcements during the post-

Reg FD period from the pre-Reg FD period. These results are consistent with the

increased role of earnings announcements in the later period. An analysis of forecast

revisions made during the reporting period reveals that in the post-Reg FD period

analysts made forecast revisions that are significantly less consistent with the actual

change in subsequent earnings than in the pre-Reg FD period. These results imply a

significant decrease in analysts’ private information.

To compensate for their inability to provide private information to selected

analysts and investors during the post-Reg FD period, companies may provide

additional public disclosures with and between earnings announcements. I examine

all public announcements made by a small sample of firms during the seven quarters

prior and post-Reg FD to assess changes in their disclosure behavior. This hand-

collected sample of forward-looking information and earnings pre-announcements

3

shows that, even after controlling for the deterioration in economic conditions during

the post-Reg FD period, companies made more frequent such disclosures.

The cumulative evidence in this study is generally consistent with Reg FD’s

living up to its objectives. The change in the information environment, designed to

curb selective disclosure practices and to “level the playing field,” seems to have had

significant real effects. Earnings announcements have reclaimed their informational

importance. Analysts’ behavior has changed, too, as seen in the reduced time taken to

issue revisions. Earnings announcements and other (voluntary) firm disclosures have

changed in character and content. Both include much more forward-looking

information post-Reg FD, to compensate for the sweeping restrictions imposed by the

rule.

This study contributes to the literature that examines the effects of Reg FD

along two major dimensions. First, it uses analyst forecast revisions to assess the level

of private information communicated to them by management, instead of employing

analyst forecast accuracy, dispersion, or stock market reactions to earnings

announcements. Second, I examine all public announcements made by a small sample

of firms to determine if there was an increase in forward looking information. Prior

studies have used samples of forward looking announcements, but not necessarily all

forward looking announcements made by those firms, and typically did not control for

the changes in the economic environment.

II. Prior Research:

Analysts’ Forecast Revisions

Analysts’ revisions have been of interest to current literature. Gleason and Lee

(2003) find that a substantial price adjustment occurs around forecast-revision dates.

4

Barron, Byard and Kim (2002) find that the commonality of information among

active analysts decreases around earnings announcements, and that the idiosyncratic

information contained in individual analysts' forecasts seems to increase immediately

after earnings announcements. Their results are more significant with the increase of

the number of forecast revisions. Zitzewitz (2002) examines the information content

of forecasts. He argues that Reg FD has been successful in reducing selective

disclosure of information about future earnings to individual analysts, without

reducing the total amount of information disclosed to the market. Mohanram and

Sunder (2001) explore the effects of Reg FD on the performance and behavior of

analysts, using forecast error and forecast dispersion. They find evidence consistent

with the objectives of Reg FD.

Voluntary Disclosure

With respect to voluntary disclosure, prior research has generally focused on

the motivation for companies’ pre-announcements, and on the market reaction to

these pre-announcements. Soffer et al. (2000) examine the factors influencing a firm’s

decision to voluntarily accelerate the release of earnings via a ”pre-announcement”.

They find that firms are more likely to pre-announce earnings if the consensus of

analysts’ forecasts is very different from actual subsequent earnings, if the dispersion

of these forecasts is high, and if the firm has negative news. Skinner (1994) argues

that managers pre-announce to prevent lawsuits caused by large stock price declines

at the bad earnings announcement, and to protect their reputation with analysts and

institutional investors by not delaying bad news. Using a random sample of 93

NASDAQ firms during 1981-90, he finds that earnings-related voluntary disclosure

occurs infrequently (on average, one disclosure for every ten quarterly earnings

announcements), and that good news disclosures tend to be point or range estimates of

5

annual earnings-per-share, whereas bad news disclosures tend to be qualitative

statements about the current quarter’s earnings. In his sample, quarterly earnings

announcements that convey large negative earnings surprises are preempted about

25% of the time by voluntary corporate disclosures, and other earnings

announcements are preempted less than 10% of the time.

Kasznik and Lev (1995) look at management’s discretionary disclosures for

firms that subsequently experience large earnings surprises. They find that less than

10% of their large-surprise firms publish quantitative earnings or sales forecasts (less

than 100 firms), and 50% provide no earnings guidance, although they subsequently

report very significant earnings surprises. Coller and Yohn (1997) use a sample of 278

quarterly earnings forecasts, including point estimates, range estimates, and upper and

lower bound estimates, to examine whether the decision to issue a management

earnings forecast is related to information asymmetry in the market for the firm’s

stock, and whether the forecasts reduce the information asymmetry. They find support

for the view that managers release forecasts to reduce information asymmetry.

Miller (2002) examines a sample of 80 companies experiencing an extended

period of seasonally adjusted earnings increases. Using 416 observations of forecasts

and earnings pre-announcements over a period of three years, he finds an increase in

disclosure during the period of increased earnings. The increase tends to be bundled

with earnings announcements, and the market responds positively to this disclosure.

Johnson, Kasznik and Nelson (2001) use 1135 forecasts between 1994 and 1996 for

about 600 firms in industries with high risk of litigation, to evaluate corporate

voluntary disclosure of forward-looking information under the Safe Harbor provision

of the Private Securities Litigation Reform Act of 1995. They find that managers

6

engage in more disclosure after the rule, and that the increase in disclosure is an

increasing function of the firms’ ex ante risk of litigation.

Market Reactions to Voluntary Earnings Preannouncements:

Heflin, Subramanyam and Zhang (2003) examine voluntary disclosure after

the implementation of Regulation FD and find (a) lower return volatility around

earnings announcements; (b) some improvement in the speed with which the price

before the earnings announcement converges to its post-announcement level; (c) no

reliable evidence of changes in various aspects of analysts’ forecast bias, accuracy,

and dispersion; and (d) an increase in the quantity of firms’ voluntary forward-looking

disclosures.

Skinner (1994) shows that there is a substantially stronger market reaction to

negative news guidance (-6.1%) than to positive news (2.5%). Kasznik and Lev

(1995) observe that the market-adjusted return in the five-day window around the

earnings (sales) forecast was about 5.4% for positive news and about 5.3% for

negative news. Furthermore, they show that for companies with negative disclosures,

the total market-adjusted return in the five-day window around the warning and the

five-day window around the subsequent earnings release was significantly more

negative than for companies that provided no warnings before announcing a

significant negative decline in earnings.

Soffer et al. (2000) find that size-adjusted returns in the three-day window

surrounding the earnings guidance disclosure is significantly associated with the

surprise in the announcement relative to analysts’ forecasts before the announcement,

and is about 6.95% stronger (more negative) for negative guidance. However, they

also show that negative guidance announcements tend to preempt the entire negative

news that are subsequently disclosed in the earnings release, but only about 50% of

7

the subsequent positive news are reported by companies providing positive guidance.

Moreover, they find that trading based on the fact that positive guidance is likely to be

followed by an even greater positive surprise subsequently can be a profitable

strategy, earning about 2.6% size-adjusted returns, or even 3.4% for companies in

industries with a high risk of litigation.

Feldman, Lazer and Livnat (2003) examine a large sample of earnings

guidance disclosures based on identification of these announcements using text-

mining techniques. Their results indicate that guidance provided with the disclosure of

earnings is not associated with significant market reactions, but guidance provided

between earnings releases is associated with significant negative reactions.

III. Hypothesis Development

I first investigate whether the information content of earnings announcements

has changed in the post-Reg FD period. To answer this question, I use analysts’

revisions as an indicator of the information environment available to analysts. The

elimination of a major information channel is bound to have substantial implications

for the timing and form in which information is disseminated and processed (Heflin et

al. 2003). For example, earnings announcements are expected to reclaim their

informational importance, as private channels have been restricted. Moreover,

companies eager to convey relevant information to market participants may bundle it

in those earnings announcement events (Bailey, Li, Mao and Zohng, 2003). Thus,

overall, the importance of earnings announcements as a major event for information

users should increase. Evidence of this importance can be seen in the behavior of

financial information users, namely analysts. The speed with which analysts issue

their forecast revisions after any disclosure event is a strong indication of the amount

8

of information contained in that disclosure, in relation to the total information

available to them. The change in the length of time analysts take to process and issue

their revisions after earnings announcements indicates the change in the relative

amount of new information contained in the announcements. Given the deterioration

in the private information management can convey to analysts post-Reg FD, I expect

to find an increase in the sense of urgency with which analysts issue their revisions,

lending support to the hypothesis that the information contained in earnings has

increased from the pre-Reg FD period. Therefore, I postulate the following hypothesis

(stated in the alternate form):

H1: Analysts’ revisions are issued much more quickly since Reg FD.

Before Reg FD, many firms communicated privately with analysts during the

quarter. These analysts revised their forecasts during the quarter based on the

information supplied privately, resulting in reasonably accurate forecasts for the

subsequent quarters. When earnings were subsequently announced, the new

information contained in the release was typically smaller relative to the information

available to the analyst before the announcement, requiring a smaller forecast

revision. Analysts now face a different information environment and are likely to

behave differently. Their forecasting ability during the quarter and prior to the

earnings announcement may be substantially affected, as the stream of private

information is more limited and sparse. Therefore, the earnings announcement is

expected to convey significant new information and to yield revisions of a higher

magnitude in the post-Reg FD period. Therefore, I postulate the following hypothesis

(stated in the alternate form):

9

H2: Analysts’ forecast revisions post-Reg FD are larger in magnitude than such

revision pre-Reg FD.

The decrease in available information due to Reg FD is bound to have

additional repercussions on analysts’ behavior. If analysts now have less access to

private information, this should be reflected in their forecast revisions during the

quarter and before the actual earnings announcement date, a period in which

management is unlikely to disclose private information to analysts. Thus, I look at

forecast revisions made during the period starting 10 days after the issuance of

earnings announcements and ending right before the following quarter’s earnings

announcements (approximately 80 days). Assuming that revisions in analysts’

forecast imply availability of new information, I expect the forecast revision to be less

consistent with the actual subsequent change in earnings during the poorer

information environment post-Reg FD. Specifically, the magnitude of revisions for

firms with actual subsequent negative (positive) earnings surprises should be less

negative (positive) in the post-Reg FD period than in the pre-Reg FD period.

Therefore, I postulate the following hypothesis (stated in the alternate form):

H3: Analysts’ forecast revisions are less consistent with the actual subsequent

changes in earnings during the post-Reg FD.

The third research question I consider is whether there has been a change in

firms’ disclosure behavior post-Reg FD. To answer this question I use a hand-

10

collected sample of companies that made voluntary disclosures of forward-looking

information, either as part of an earnings announcement or separately.

Post-Reg FD, firms have fewer channels through which they can communicate

with the public and analysts. I therefore expect to see an increase in permissible

communications, such as pre-announcements and other forward-looking disclosures.

Previous researchers have found a positive correlation between the magnitude of the

negative earnings or sales surprises and the tendency of firms to use voluntary

disclosure (Skinner 1994; Kasznik and Lev 1995). I collect a sample of companies

that made voluntary disclosures of forward-looking information, either as part of an

earnings announcement or separately, between 1999 and mid-2002. During this period

the economy experienced both high growth and a recession. Based on prior literature,

I expect more pre-announcements in the recession period due to a higher occurrence

of negative changes in earnings. To control for changes in the economic environment

between the pre-Reg FD period and the post-Reg FD period, I examine the frequency

of voluntary disclosures while controlling for the actual earnings surprise. I expect to

find a higher frequency of voluntary disclosures in the post-Reg FD period for the

same level of an earnings surprise. Therefore, I postulate the following hypothesis

(stated in the alternate form):

H4: The frequency of voluntary disclosures of forward-looking information is

higher post-Reg FD.

I also use the hand-collected sample of companies that made voluntary

disclosures of forward-looking information to test for analysts’ forecast revisions

made during the period prior to the preannouncement. I examine the period starting

11

10 days after the issuance of earnings announcements and ending right before the

following quarter’s earnings pre-announcement if it occurred prior to the end of the

quarter. Assuming that revisions in analysts’ forecasts imply the availability of new

information, I expect these revisions to be less consistent with the actual changes in

earnings implied by the preannouncement during the poorer information environment

post-Reg FD. Specifically, I expect the magnitude of revisions for firms with actual

negative (positive) earnings surprises to be less negative (positive) in the post-Reg FD

period than before it. By testing this with the sample of firms that voluntarily

disclosed forward-looking information, I can capture the portion of the sample most

eager to disclose information to market participants. These firms are arguably also

more likely to try to circumvent and test the limits of Regulation FD. Therefore, I

postulate the following hypothesis (stated in the alternate form):

H5: Analysts’ forecast revisions during the quarter but prior to the

preannouncement of earnings are less consistent with the implied change in

earnings due to the announcement post-Reg FD.

IV. Research Design and Discussion of Results

To assess how quickly analysts’ revisions are issued after earning

announcements, I use the IBES detailed and actual files for all firms traded in the US.

The sample period includes annual forecasts made between January 1998 and July

2003–approximately two and a half years pre- and post-Reg FD. For all the firms in

the IBES database, I identified a 120-day window (60 days before and 60 days after

an earnings announcement). To be included in the sample an analyst should have had

12

at least two EPS forecasts for the current year within the 120-day window–one

forecast before and one after the earning announcement.

I illustrate the construction of the variables using the following time frame:

60 days 60 days

Panel A of Table 1 reports the average number of days until the issuance of a

new annual forecast, following annual or quarterly earnings announcements. The

average number of days following earnings announcements is significantly shorter in

the post-Reg FD period. For example, the average number of days used by analysts to

update their annual EPS forecast went from 12.3 days in the pre-Reg FD period to 7.7

days in the post-Reg FD period. Thus, analysts react faster to earnings

announcements in the post-Reg FD period, implying an increase in the amount of

information conveyed in those announcements relative to available information prior

to the announcements. Forecast revisions following the announcement of previous

annual earnings results are slower than the revisions following quarterly earnings

announcements, but consistent with the decrease between the pre-Reg FD and the

post-Reg FD periods (there is a decrease of 5.6 days in the length of time analysts use

to revise their annual forecast following annual earnings announcements). The

difference between revisions following quarterly and annual results might be

explained by the greater amount of information conveyed in annual announcements.

T-60 To T+60

At least one

new forecast

for year 1 is announced

Earning

announcement

date for year 0 or

Q1/2/3 of year 1

results

At least one

new forecast

for year 1 is announced

13

Given the change in the economic environment between the pre- and post-Reg

FD periods, there is a need to control for differential levels of earnings surprises.

Panel B of Table 1 provides the difference in the average number of days until the

issuance of a forecast revision of the annual EPS, pre- and post-Reg FD, controlling

for the median forecast error in analysts’ forecasts for the current quarter. Median

forecast error is defined as the difference between the actual EPS (as reported by

IBES) and the median of all available forecasts (the last forecast of each analyst) 60

days before the earnings announcement, divided by the share price at the beginning of

the previous quarter. Post-Reg FD, there is a significant decrease in the average

number of days until the issuance of a new forecast for all levels of current-quarter

median error.

An additional way to control for both the change in the economic conditions

and the speed of forecast revisions is to control for the specific forecast error of each

analyst. Panel C of Table 1 presents the difference in the average number of days until

the issuance of a forecast revision of the annual EPS, pre- and post-Reg FD,

controlling for the specific forecast error in analysts’ forecasts for the current quarter.

The specific forecast error is defined as the difference between the actual EPS and the

last analyst forecast before the earnings announcement (less than 60 days before the

earnings announcement), divided by the share price at the beginning of the previous

quarter. As the panel shows, there is a significant decrease in the average number of

days for all levels of forecasts’ accuracy in the post-Reg FD period.

Further analysis of the average number of days until the issuance of forecast

revisions for the following quarter EPS provide similar results. The quarterly analysis

follows this timeline:

14

60 days 60 days

Figure 1 shows that the percentage of analyst revisions in quarterly forecasts

made one day after earnings announcement is higher in the post-Reg FD period than

before. Untabulated results similar to those in Table 1 also show that analyst forecast

revisions occur faster after Reg FD than before. Thus, the above results significantly

reject the null hypothesis corresponding to H1, indicating that during the post-Reg FD

period analysts revised their forecasts immediately after the earnings announcements

faster than in the pre-Reg FD period.

In Table 2, I analyze the size of the EPS forecast revisions. As mentioned

above, the information gap between analysts and firms that is decreased at the

earnings announcement event is expected to yield revisions of a higher magnitude in

the post-Reg FD period, because relatively more information is conveyed by the

earnings announcement post-Reg FD than before. The EPS forecast revision is

calculated as the difference between the first forecast following the earnings

announcement and the last forecast before that earnings announcement, divided by the

share price at the beginning of the quarter. Table 2 presents the average EPS forecast

revision, controlling for the median forecast error for the current quarter results (Panel

A), and for analysts’ specific forecast error (Panel B). The table shows that the

magnitude of forecast revisions post-Reg FD is significantly higher than in the pre-

Reg FD period. The positive difference holds for most levels of median or specific

forecast errors.

T-60 To T+60 T~+90

At least one new forecast

for quarter 1 is

announced

Earning announcement date

for quarter 0

results

At least one new forecast

for quarter 1 is

announced

Earning announcemen

t date for quarter 1

results

15

To further assess the difference in the magnitude of forecast revisions between

the pre- and post-Reg FD periods, I use the following multi-variable model, which

controls for the contemporaneous forecast error and the previous revision magnitude:

(1) ABS_Revt,i = a0 + a1 * ABS_FEt,i + a2 * ABS_Revt-1,i + a3 * Posti * ABS_FEt,i

+ a4 * Posti * ABS_Revt-1,i + ei

ABS_Rev – The absolute value of the revision of quarterly/annual analyst forecasts around the earnings announcement divided by the share price at the beginning of the quarter

ABS_FE – The absolute value of the difference between the actual quarterly EPS and the latest (specific) analyst forecasts divided by the share price at the beginning of the quarter

Post – A dummy variable indicating the period (1 for Post-Reg FD and 0 for Pre-Reg FD)

I expect to find a positive coefficient for the interaction between the period’s

dummy and the absolute value of the forecast error, indicating a bigger effect of

forecast errors in the post-Reg FD period. The absolute value of the previous quarter

analyst revision is introduced in order to control for autocorrelations in analysts’

forecast revisions.

Table 3 reports the estimation results for using analysts’ revisions of both

quarterly and annual forecasts. Consistent with my hypothesis, the coefficient on the

absolute forecast error (a3) post-Reg FD is positive and significant for two different

measures of forecast error. The first measure is the specific analyst forecast error,

which is the difference between the actual EPS and the specific analyst’s latest

forecast before the earnings announcement. This measure indicates the specific gap in

information between the analyst and the company. The second measure is the latest

analyst forecast error, which is the difference between the actual EPS and the latest

forecast before the earnings announcement. This measure indicates the overall gap

between the company and the capital market. Using the median forecast error, the

16

results (not reported) hold. Thus, the combined evidence in Tables 2 and 3 indicates

that the data reject the null hypothesis corresponding to H2, i.e., and that forecast

revisions immediately after earnings announcements are larger in magnitude after Reg

FD than before it, even after controlling for the forecast error and the previous analyst

revision.

To assess the relative amount of private information in analyst forecasts

during the reporting period, I compare whether the forecast revisions made during the

quarter are less consistent with the actual subsequent change in earnings during the

post-Reg FD period then before. This can be best illustrated with the following

timeline:

10 days ~80 days

By ten days after the quarter earnings announcement, most analysts have

already revise their forecast for current quarter EPS based on the information

provided in the earning announcement for the previous quarter. The forecast

revisions following those ten days are based on information available to analysts

during the remainder of the quarter. Companies may provide additional information,

and analysts gather new information on their own. This period, approximately 80 days

long, is a period with limited private communications between the company and

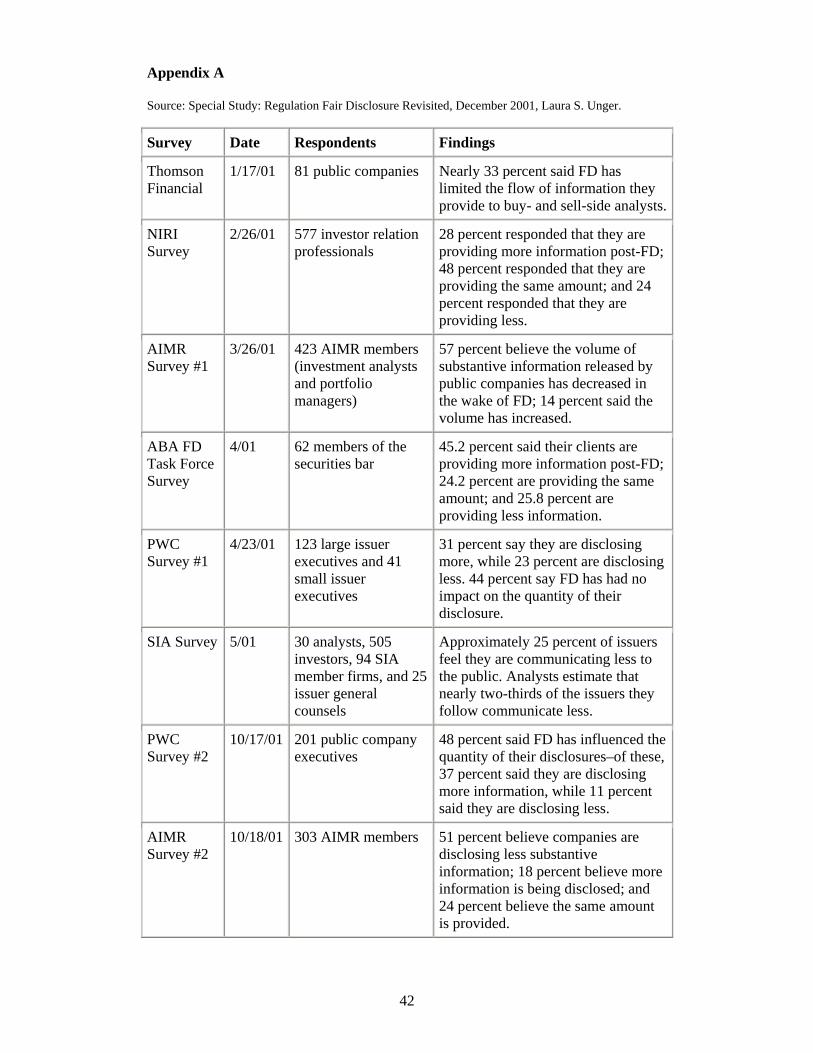

analysts post-Reg FD. Several surveys (Appendices A and B) show a decrease in the

amount of information available to analysts during the quarter after Reg FD. To assess

T0 T+10 T~+90

Earning announcement

date for quarter 0 results

Consensus analysts’ forecast based on quarter 0 results is available

At least one new forecast

for quarter 1 is

announced

Earning announcement

date for quarter 1 results

17

the impact of the change in private information available to analysts post-Reg FD, I

examine forecast revisions during the roughly 80-day period prior to the subsequent

earnings announcement. Table 4 reports the difference between the pre- and post-Reg

FD periods in forecast revisions during this period, controlling for the earnings

surprise in the subsequent quarter. EPS forecast revision is the difference between the

last forecast in the quarter and the forecast issued in the first ten days after the

previous quarter’s earnings announcements, scaled by the share price at the beginning

of the previous quarter. The EPS surprise is the actual (IBES) EPS minus actual

(IBES) EPS for the same quarter of the prior year, divided by the share price at the

beginning of the quarter.

In the pre-Reg FD period, negative (positive) earnings surprises are

accompanied by negative forecast (positive) revisions during the quarter, indicating

analysts’ ability to gather new information during the quarter which is consistent with

the actual subsequent earnings changes. In the post-Reg FD period, forecast revisions

are negative for both positive and negative surprises, indicating a lower ability to

gather information about companies’ performance during the quarter. For very

negative surprises, there are larger negative forecast revisions in the pre-Reg FD

period than in the post-Reg FD period, indicating better knowledge and information

regarding the negative surprise during the 80-day period prior to the subsequent

earnings announcement. For positive earnings surprises, the forecast revisions in the

pre-Reg FD period are in the right direction (positive); post-Reg FD, these revisions

are in the wrong direction (negative). Table 5 replicates the analysis for the revision in

next quarter analysts’ forecasts and provides similar results. Using a different

measure of earnings surprise based on analysts’ forecasts at the beginning of the

quarter generates similar results, indicating that analysts had a better ability to update

18

their forecasts during the quarter in the pre-Reg FD period. The combined evidence in

Tables 4 and 5 significantly rejects the null hypotheis corresponding to H3, showing

that analysts’ ability to revise their forecasts during the period in a manner that would

be consistent with the actual subsequent change in earnings deteriorated in the post-

Reg FD period from before.

To assess the changes in firms’ disclosure behavior in the post-Reg FD period,

I collected a sample of forward-looking voluntary disclosures provided by companies

during earnings announcements and between earnings announcements dates. For a

sample of 80 companies, during the period between 1999 and mid-2002, I examined

all press releases issued by the companies indicating present or future results. I

collected forward-looking information provided by companies in the form of

EPS/Earnings/Sales point estimates or ranges (some of the information in the press

releases, was given as percentage of changes and was transformed to point estimates

and ranges).

Table 6 reports the number of voluntary forward-looking disclosures provided

by the companies in the sample. The table shows the number of days with forward-

looking information that accompany earnings announcements, and the number of days

with forward-looking information during the quarter–between earnings

announcements. Some of the days include more than one item of forward-looking

information; for example, the company may provide new EPS estimates for both the

current quarter and the year. Panel C details the number of forward-looking

information items, separating them to annual and quarter financial results.

I examine the number of firm quarters with voluntary disclosures relative to

the total number of firm quarters in the period. I expect the percentage of firm

quarters with voluntary disclosure to be higher in the post-Reg FD period, consistent

19

with previous studies (Heflin et al., 2003). Previous studies that addressed the

question of change in voluntary disclosure did not control for the change in the

economic conditions between the pre- and the post-Reg FD periods. An economic

downturn can cause an increase in voluntary disclosures (Skinner 1994). To control

for economic changes, I examine the percentage of voluntary disclosures for different

levels of earnings surprises. An increase in the percentage of voluntary disclosures for

a given level of an earnings surprise indicates the impact of Reg FD, after controlling

for the economic conditions that caused the earnings surprise. Table 7 provides the

percentage of quarterly voluntary disclosures for four different levels of EPS

surprise. The EPS surprise is the change in EPS in the quarter relative to the

equivalent quarter in the previous year divided by that previous quarter’s price per

share. The proportion of negative surprises is higher in the post-Reg FD period

(consistent with the actual changes in economic conditions), but the percentage of

voluntary disclosures is higher for each level of EPS surprise. Panel B of Table 7

provides similar results with respect to sales surprises for the quarter. Table 8 reports

the percentage of annual voluntary disclosures for four different levels of EPS (sales)

surprises Panel A (B). The percentage of annual voluntary disclosures is higher in the

post-Reg FD period and is consistent with the quarterly findings. The combined

evidence in Tables 6-8 significantly rejects the null hypothesis corresponding to H4,

showing that companies attempted to compensate for their inability to communicate

with selected analysts and investors by issuing more public disclosures, even after

controlling for the deteriorating economic conditions after Reg FD became effective.

20

V. Summary and Conclusions

Reg FD is an important effort to curb the practice of private disclosure of

material information by management to selected analysts and investors. This

restriction of a substantial information channel can be expected to bring a shift in the

content and the importance of companies’ announcements. Financial analysts are

expected to have less private information available to them after Reg FD and to rely

more on public earnings announcements. Companies are expected to handle the

decrease in information conduits by finding alternative methods to disseminate

information. By examining the characteristics of revisions of analysts’ forecasts, I test

for an increase in the relative magnitude of new information conveyed by the

earnings announcements, as manifested by an increase (after Reg FD) in revisions

issued immediately after an earnings announcement. My results show a significant

decrease in the time until analysts revise their forecasts after earnings announcements.

I also find a significant increase in the magnitude of these revisions after earning

announcements. When controlling for the level of earnings surprise, I find analyst

revisions prior to the earnings announcement to be less consistent with the subsequent

actual change in earnings, in line with less private information available to analysts

during the quarter. I explore an increase in the occurrence of pre-announcements–

voluntary disclosures made during the reporting period. Further analysis shows a

clear increase in companies’ tendency to provide additional information and forecast

estimates, both in their earnings announcements and in their pre-announcements, in

the post-Reg FD period, consistent with the expected implications of Reg FD.

21

The combined evidence in this paper indicates that the data are consistent with

Regulation FD living up to regulators’ expectations. The change in the information

environment brought about by Regulation FD seems to have had significant real

effects in reducing selective disclosure practices and “leveling the playing field”. The

evidence on analyst forecast revisions indicates clearly that earnings announcements

have reclaimed at least some of their previous informational importance. Analysts’

behavior has changed, too, as seen in the reduced time taken to issue revisions, and

earnings announcements, and other voluntary firm disclosures have changed in

character and content. Both include much more forward-looking information post-Reg

FD, to compensate for the restrictions imposed by the rule.

22

References:

Ajinkya, B. and M. Gift. “Corporate Managers’ Earnings Forecasts and Symmetrical Adjustments of Market Expectations.” Journal of Accounting Research 22 (1984): 425-444.

Bailey W., H Li, C.X. Mao, and R. Zhong. “Regulation Fair Disclosure and Earnings

Information: Market, Analyst, and Corporate Responses”. The Journal of Finance, Volume 58 Issue 6 - December 2003

Barron, O. E., D. Byard and O. Kim, 2002, “Changes in Analysts’ information around

Earnings Announcements”. The Accounting Review, October 2002. Barron, O. E., and Pamela S. Stuerke, 1998, “Dispersion in analysts earnings forecasts

as a measure of uncertainty”, Journal of Accounting, Auditing, and Finance 18, 235-270.

Bushee, B., J. Dawn, A. Matsumoto, and G. S. Miller, 2002, “Managerial and investor

responses to disclosure regulation: The case of Reg FD and conference calls”, Working paper, University of Pennsylvania.

Coller, M. and T.L. Yohn. 1997. “Management forecasts and information asymmetry:

An examination of bid-ask spreads”. Journal of Accounting Research 35, 2 (1997).

Dontoh, A. “Voluntary Disclosure.” Journal of Accounting, Auditing & Finance; Fall

1989. Eleswarapu, V. R., R. Thompson, and K. Venkataraman, 2002, “Measuring the

fairness of Regulation Fair Disclosure through its impact on trading costs and information asymmetry”, Journal of Financial and Quantitative Analysis, forthcoming.

El-Gazzar, S. M., 1998, “Predisclosure information, firm capitalization, and security

price behavior around earnings announcements”, The Accounting Review 73, 119-129.

Feldman R., R. Lazer, and J. Livnat ,”Earnings Guidance after Regulation FD, Journal

of Investing”, Winter 2003. Foster, G. “Stock-Market Reaction to Estimates of Earnings-Per-Share by Company

Officials.” Journal of Accounting Research 11 (1973): 25-37. Gadarowski, C., and P. Sinha, 2002, “On efficacy of Regulation Fair Disclosure:

Theory and evidence”, Working paper, Cornell University. Gintschel, A., and S. Markov, 2002, “The effectiveness of Reg FD”, Working paper,

Emory University.

23

Gleason, C.A., and C.M.C. Lee. 2003. “Analyst forecast revisions and market price discovery”. The Accounting review 78, 1, (January): 193-225.

Heflin, F., K. R. Subrahmanyman, and Y. Zhang, 2003, “Regulation FD and the

financial information environment: Early evidence”, The Accounting Review 78, 1-37.

Irani, A., 2003, “The Effect of Regulation Fair Disclosure on the relevance of

conference calls to financial analysts”, Working paper, University of New Hampshire.

Irani, A., and I. Karamanou, 2002, “Regulation Fair Disclosure, analyst following,

and analyst forecast dispersion”, Accounting Horizons, forthcoming. Johnson, MF, R. Kasznik, and K.K. Nelson, “The impact of securities litigation

reform on the disclosure of forward-looking information by high technology firms” Journal of Accounting Research 39 (2) (2001): 297-327.

Kasznik, R., and B. Lev. “To Warn or Not to Warn: Management Disclosures in the

Face of an Earnings Surprise.” Accounting Review 70 (1995): 113-134. Kile, C., G. Pownall, and G. Waymire. “How Frequently Do Managers Disclose

Prospective Earnings Information?” The Journal of Financial Statement Analysis (1998).

Kim, O., and R. E. Verrecchia, 1994, “Market liquidity and volume around earnings

announcements”, Journal of Accounting and Economics 17, 41-67. Kim, O., and R. E. Verrecchia, 1997, “Pre-announcement and event period private

information”, Journal of Accounting and Economics 24, 395-419. Lev, B. and S. Penman. “Voluntary Forecast Disclosure, Nondisclosure, and Stock

Prices.” Journal of Accounting Research 28 (1990). Miller, G. S. “Earnings Performance and Discretionary Disclosure” Journal of

Accounting Research 40 (1) (2002): 173-204

Monhanram, P., and S. V. Sunder, 2001, “Has Regulation Fair Disclosure affected

financial analysts' ability to forecast earnings?” Working paper, New York University.

Securities and Exchange Commission. “Selective Disclosure and Insider Trading.”

17 CFR Parts 240, 243, and 249. Release Nos. 33-7881, 34-43154, IC-24599, File No. S7-31-99 RIN 3235-AH82

Skinner, D. “Earnings Disclosures and Stockholder Lawsuits.” Journal of Accounting

and Economics 23 (1997): 249-282.

24

Skinner, D. “Why Firms Voluntarily Disclose Bad News.” Journal of Accounting Research 32 (1994): 38-60.

Soffer, C.L., S.R. Thiagarajan and B.R. Walther. “Earnings Preannouncement

Strategies.” Review of Accounting Studies, 5 (2000): 5-26 Straser, V., 2002, “Regulation Fair Disclosure and information asymmetry”, Working

paper, University of Notre Dame. Sunder, S. V., 2002, “Investor access to conference call disclosures: Impact of

Regulation Fair Disclosure on information asymmetry”, Working paper, New York University.

Verrecchia, R.E., “Discretionary Ddisclosure and Information Quality.” Journal of

Accounting and Economics 12 (1990): 179-194. Zitzewitz, E., 2002, “Regulation Fair Disclosure and the private information of

analysts”, Working paper, Stanford University.

25

Table 1 – Number of Days to Revise This Year’s Annual EPS Forecast After Earnings Announcements Panel A – By QTR Post FD Pre FD Significance

Period

No. of Days Until

Revision No. of Obs.

No. of Days Until

Revision No. of Obs. Difference t-test Wilcoxon

Third Qtr Results 8.0 22560 11.0 19669 -3.0 <0.0001 <0.0001

Second Qtr Results 6.1 23374 11.0 23930 -5.0 <0.0001 <0.0001

First Qtr Results 7.7 25467 12.3 25053 -4.6 <0.0001 <0.0001

Previous Annual Results 10.0 21028 15.6 19274 -5.5 <0.0001 <0.0001

Total 7.9 92429 12.4 87926 -4.5 <0.0001 <0.0001 Panel B – By Size of Absolute Median Forecast Error Post FD Pre FD Significance

Absolute Value of Median FE

No. of Days Until

Revision No. of Obs.

No. of Days Until

Revision No. of Obs. Difference t-test Wilcoxon

1 – Low 8.4 19468 12.5 19317 -4.1 <0.0001 <0.0001

2 7.4 20262 11.0 18513 -3.6 <0.0001 <0.0001

3 6.7 21070 11.1 17720 -4.3 <0.0001 <0.0001

4 – High 7.1 21162 11.6 17621 -4.5 <0.0001 <0.0001

Total 7.4 81962 11.6 73171 -4.2 <0.0001 <0.0001 No. of Days Until Revision – the number of days from the earnings announcement and the first revision of the annual EPS forecast. Median Forecast Error – the difference between the actual quarterly EPS and the median analyst forecast prior to the earnings announcement, divided by the beginning of the quarter share price

26

Table 1 (Continued) – Number of Days to Revise This Year’s Annual EPS Forecast After Earnings Announcements Panel C – By Size of Absolute Specific Forecast Error Post FD Pre FD Significance

Absolute Value of Specific FE

No. of Days Until Revision

No. of Obs.

No. of Days Until Revision

No. of Obs. Difference t-test Wilcoxon

1 – Low 8.8 15465 12.0 14187 -3.2 <0.0001 <0.0001

2 6.7 16409 9.6 13245 -2.9 <0.0001 <0.0001

3 6.2 16596 9.6 13058 -3.4 <0.0001 <0.0001

4 – High 6.7 16958 10.5 12695 -3.9 <0.0001 <0.0001

Total 7.1 65428 10.5 53185 -3.4 <0.0001 <0.0001 No. of Days Until Revision – the number of days from the earnings announcement until the first revision of the annual EPS forecast Specific Forecast Error – the difference between the actual quarterly EPS and the latest specific analyst forecast prior to the earnings announcement, divided by the beginning

of the quarter share price

27

Table 2 – Current Year EPS Forecast Revision After Earnings Announcements Panel A – By Size of Absolute Median Forecast Error Post FD Pre FD Significance

Absolute Value of Median FE

EPS Forecast Revision No. of Obs.

EPS Forecast Revision No. of Obs. Difference t-test Wilcoxon

1 – Low 0.0081 19468 0.0056 19317 0.0026 0.0007 <0.0001

2 0.0039 20262 0.0035 18513 0.0004 <0.0001 <0.0001

3 0.0065 21070 0.0064 17720 0.0002 0.1591 <0.0001

4 – High 0.0322 21162 0.0310 17621 0.0012 0.5756 <0.0001

Total 0.0129 81962 0.0114 73171 0.0015 0.0084 <0.0001 EPS forecast revision – the difference between the first forecast following an earnings announcement and the last forecast prior to that earnings announcement, divided by

the beginning of the quarter share price Median Forecast Error – the difference between the actual quarterly EPS and the median analyst forecast prior to the earnings announcement, divided by the beginning of the

quarter share price

28

Table 2 (Continued) – Current Year EPS Forecast Revision After Earnings Announcements Panel B – By Size of Absolute Specific Forecast Error Post FD Pre FD Significance

Absolute Value of Specific FE

EPS Forecast Revision No. of Obs.

EPS Forecast Revision No. of Obs. Difference t-test Wilcoxon

1 – Low 0.0069 15465 0.0047 14187 0.0022 0.0013 <0.0001

2 0.0036 16409 0.0032 13245 0.0005 <0.0001 <0.0001

3 0.0062 16596 0.0058 13058 0.0003 0.0061 <0.0001

4 – High 0.0331 16958 0.0262 12695 0.0069 0.0006 <0.0001

Total 0.0127 65428 0.0097 53185 0.0030 <0.0001 <0.0001 EPS forecast revision – the difference between the first EPS forecast following an earnings announcement and the last forecast prior to that earnings announcement, divided

by the beginning of the quarter share price Specific Forecast Error – the difference between the actual quarterly EPS and the latest specific analyst forecast prior to the earnings announcement, divided by the beginning

of the quarter share price

29

Table 3 – Forecast Revision Regression Estimation Panel A – Revisions of Quarterly Earnings Forecasts Using Forecast Error from Last Forecast

ABS_Revt,i = a0 + a1 * ABS_FEt,i + a2 * ABS_Revt-1,i + a3 * Posti * ABS_FEt,i

+ a4 * Posti * ABS_Revt-1,i + ei

Variable Expected Sign Absolute value

of revision Absolute value

of revision Intercept ? 0.0015 0.0015 (0.0000) (0.0000)

ABS_FEt,i + 0.3757 0.3658 (0.0000) (0.0000)

ABS_Revt-1,i + 0.2902 0.3052 (0.0000) (0.0000)

Post * ABS_FEt,i + 0.0243 0.0412 (0.0459) (0.0001)

Post * ABS_Revt-1,i + 0.0268 (0.0067) Adjusted R2 0.24 0.24 N 34009 34009

ABS_Rev – The absolute value of the revision of quarterly analyst forecasts around the earnings announcement divided by the share price at the beginning of the quarter

ABS_FE – The absolute value of the difference between the actual quarterly EPS and the latest analyst forecasts divided by the share price at the beginning of the quarter

Post – A dummy variable indicating the period (1 for Post-Reg FD and 0 for Pre-Reg FD)

30

Table 3 (Continued) – Forecast Revision Regression Estimation Panel B – Revisions of Quarterly Earnings Forecasts Using Analysts' Specific Forecast Errors

ABS_Revt,i = a0 + a1 * ABS_FEt,i + a2 * ABS_Revt-1,i + a3 * Posti * ABS_FEt,i

+ a4 * Posti * ABS_Revt-1,i + ei

Variable Expected Sign

Absolute value of revision

Absolute value of revision

Intercept ? 0.0014 0.0014 (0.0000) (0.0000)

ABS_FEt,i + 0.4396 0.4212 (0.0000) (0.0000)

ABS_Revt-1,i + 0.2608 0.2877 (0.0000) (0.0000)

Post * ABS_FEt,i + 0.0083 0.0391 (0.5183) (0.0004)

Post * ABS_Revt-1,i + 0.0475 (0.0000) Adjusted R2 0.26 0.26 N 30640 30640

ABS_Rev – The absolute value of the revision of quarterly analyst forecasts around the earnings announcement divided by the share price at the beginning of the quarter

ABS_FE – The absolute value of the difference between the actual quarterly EPS and the latest specific analyst forecast divided by the share price at the beginning of the quarter

Post – A dummy variable indicating the period (1 for Post-Reg FD and 0 for Pre-Reg FD)

31

Table 3 (Continued) – Forecast Revision Regression Estimation Panel C – Revisions of Annual Earnings Forecasted Using Analysts’ Median Forecast Errors

ABS_Revt,i = a0 + a1 * ABS_FEt,i + a2 * ABS_Revt-1,i + a3 * Posti * ABS_FEt,i

+ a4 * Posti * ABS_Revt-1,i + ei

Variable Expected Sign Absolute value

of revision Absolute value

of revision Intercept ? 0.0017 0.0017 0.0014 0.0012

ABS_FEt,i + 1.2331 1.1843 0.0000 0.0000

ABS_Revt-1,i + 0.9033 1.1049 0.0000 0.0000

Post * ABS_FEt,i + 0.3641 0.4504 0.0001 0.0000

Post * ABS_Revt-1,i + 0.3650 0.0162 Adjusted R2 0.03 0.03 N 48696 48696

ABS_Rev – The absolute value of the revisions of analyst forecasts around the earnings announcement divided by the share price at the beginning of the quarter ABS_FE – The absolute value of the difference between actual EPS and median analyst forecasts divided by the share price at the beginning of the quarter

Post – A dummy variable indicating the period (1 for Post-Reg FD and 0 for Pre-Reg FD)

32

Table 3 (Continued) – Forecast Revision Regression Estimation Panel D – Revisions of Annual Earnings Forecasts Using Analysts' Specific Forecast Errors

ABS_Revt,i = a0 + a1 * ABS_FEt,i + a2 * ABS_Revt-1,i + a3 * Posti * ABS_FEt,i

+ a4 * Posti * ABS_Revt-1,i + ei

Variable Expected Sign Absolute value

of revision Absolute value

of revision Intercept ? 0.0017 0.0017 (0.0036) (0.0037)

ABS_FEt,i + 1.1182 1.1260 (0.0000) (0.0000)

ABS_Revt-1,i + 0.7473 0.7141 (0.0000) (0.0000)

Post * ABS_FEt,i + 0.8971 0.8841 (0.0000) (0.0000)

Post * ABS_Revt-1,i + -0.0604 (0.7146) Adjusted R2 0.04 0.04 N 42872 42872

ABS_Rev – The absolute value of the revision of analyst forecasts around the earnings announcement divided by the share price at the beginning of the quarter

ABS_FE – The absolute value of the difference between the actual quarterly EPS and latest specific analyst forecasts divided by the share price at the beginning of the quarter

Post – A dummy variable indicating the period (1 for Post-Reg FD and 0 for Pre-Reg FD)

33

Table 4 – Revision in Current Quarter Analyst Forecasts During the "Low Information Period" Post FD Pre FD Significance

EPS Surprise

EPS Forecast Revision N

EPS Forecast Revision N

Expected Sign of

DifferenceDifference (Post-Pre) t-test Wilcoxon

1 – Negative -0.0072 6053 -0.0099 2721 + 0.0027 <0.0001 <0.0001

2 -0.0033 5784 -0.0038 2984 + 0.0005 0.0001 <0.0001

3 -0.0019 5731 -0.0018 3054 ? -0.0001 0.0940 0.0001

4 -0.0009 4467 -0.0005 4307 ? -0.0004 <0.0001 <0.0001

5 -0.0008 5250 -0.0005 3522 - -0.0004 <0.0001 <0.0001

6 – Positive -0.0003 5798 0.0008 2977 - -0.0010 0.0712 <0.0001

Total -0.0025 33083 -0.0023 19565

Low Information Period – the period starting 10 days after the issuance of the earnings announcement and ending right before the following quarter’s earnings announcement (approximately 80 days).

EPS Surprise – the actual EPS random walk divided by the share price at the beginning of the quarter

EPS Forecast Revision – the difference between the latest analyst forecast for the current quarter and the analysts’ consensus from 10 days after the previous quarter’s earnings announcement, divided by the share price at the beginning of the quarter

N – the number of analyst forecast revisions

Significance – the significance level obtained in a t-test and two-sided Wilcoxon test that the difference is zero.

34

Table 5 – Revision in Next Quarter’s Analyst Forecasts During the "Low Information Period" Post FD Pre FD Significance

EPS surprise EPS forecast

revision N EPS forecast

revision N Expected Sign of

Difference Difference (Post-Pre) t-test Wilcoxon

1 – Negative -0.0110 8059 -0.0127 4233 + 0.0017 0.0001 <0.0001

2 -0.0035 7584 -0.0045 4698 + 0.0010 <0.0001 <0.0001

3 -0.0018 7362 -0.0020 4937 ? 0.0002 0.0083 0.0069

4 -0.0009 5709 -0.0005 6577 ? -0.0004 <0.0001 <0.0001

5 -0.0003 6758 -0.0003 5523 - 0.0000 0.4473 0.2127

6 – Positive -0.0031 43053 -0.0028 30682 - -0.0003 0.2808 <0.0001

Total -0.0025 33083 -0.0023 19565

Low Information Period – the period starting 10 days after the issuance of the earnings announcement and ending right before the following quarter’s earnings announcement (approximately 80 days). EPS Surprise – the actual EPS random walk divided by the share price at the beginning of the quarter EPS Forecast Revision – the difference between the latest analyst forecast for the next quarter and the analysts’ consensus from 10 days after the previous quarter’s earnings announcement, divided by the share price at the beginning of the quarter N – the number of analyst forecast revisions

Significance – the significance level obtained in a t-test and two-sided Wilcoxon test that the difference is zero.

35

Table 6 – Voluntary Disclosure Sample Panel A – Number of Firms with at Least One Voluntary Disclosure Pre-Regulation FD 15 Post-Regulation FD 72 Panel B – Number of Days with Voluntary Disclosure Period

Pre-FD Post-FD

Earnings Announcement Days 10 169

Other 37 195

Total 47 364 Panel C – Number of Voluntary Disclosure Items

Pre-FD

Annual Quarter Total

Earnings announcement days 51 49 100

Other 15 38 53

Total 66 87 153

Post-FD

Annual Quarter Total

Earnings announcement days 173 191 364

Other 164 179 343

Total 337 370 707

36

Table 7 – Frequency of Quarterly Voluntary Disclosure in Post- vs. Pre-Reg FD Periods Panel A – Control by Random Walk of EPS Surprise

Post-FD Pre-FD

EPS Surprise

Firm quarters with no voluntary disclosure

Firm quarters with voluntary disclosure

Total number of firm quarters

Percentage of firm quarters with voluntary disclosure

Firm quarters with no voluntary disclosure

Firm quarters with voluntary disclosure

Total number of firm quarters

Percentage of firm quarters with voluntary disclosure

Total number of firm quarters

Difference in percentage of voluntary disclosure

1 – Positive surprise 130 35 165 21.2% 106 7 113 6.2% 278 15.0%

2 77 17 94 18.1% 170 14 184 7.6% 278 10.5%

3 59 33 92 35.9% 181 6 187 3.2% 279 32.7%

4 – Negative surprise 141 66 207 31.9% 70 1 71 1.4% 278 30.5%

Total 407 151 558 27.1% 527 28 555 5.0% 1113 22.0% Notes: EPS surprise is the change in EPS in the quarter relative to the equivalent quarter in the previous year divided by that previous quarter’s price per shareTo be considered a "Firm quarter with voluntary disclosure," at least one disclosure is required The sample period is January 1999 to June 2002 Voluntary disclosure includes any forward-looking disclosure outside of an earnings announcement

37

Table 7 (continued – Frequency of Quarterly Voluntary Disclosure in Post- vs. Pre-Reg FD Periods Panel B – Control by Random Walk of Sales Surprise

Post-FD Pre-FD

Sales Surprise

Firm quarters with no voluntary disclosure

Firm quarters with voluntary disclosure

Total number of firms’' quarters

Percentage of firm quarters with voluntary disclosure

Firm quarters with no voluntary disclosure

Firm quarters with voluntary disclosure

Total number of firm quarters

Percentage of firm quarters with voluntary disclosure

Total number of firm quarters

Difference in percentage of voluntary disclosure

1 – Positive surprise 66 18 84 21.4% 155 5 160 3.1% 244 18.3%

2 90 22 112 19.6% 123 9 132 6.8% 244 12.8%

3 102 44 146 30.1% 92 4 96 4.2% 242 26.0%

4 – Negative surprise 120 62 182 34.1% 61 1 62 1.6% 244 32.5%

Total 378 146 524 27.9% 431 19 450 4.2% 974 23.6% Notes: Sales surprise is the change in sales in the quarter relative to the equivalent quarter in the previous year divided by that previous quarter’s sales To be considered a "Firm quarter with voluntary disclosure," at least one disclosure is required The sample period is January 1999 to June 2002 Voluntary disclosure includes any forward-looking disclosure outside of an earnings announcement

38

Table 8 – Frequency of Annual Voluntary Disclosure in Post- vs. Pre-Reg FD Periods Panel A – Control by Random Walk of EPS Surprise

Post-FD Pre-FD

EPS Surprise

Firm years with no voluntary disclosure

Firm years with voluntary disclosure

Total number of firm years

Percentage of firm years with voluntary disclosure

Firm years with no voluntary disclosure

Firm years with voluntary disclosure

Total number of firm years

Percentage of firm years with voluntary disclosure

Total number of firm years

Difference in percentage of voluntary disclosure

1 – Positive surprise 20 26 46 56.5% 25 8 33 24.2% 79 32.3%

2 9 20 29 69.0% 47 1 48 2.1% 77 66.9%

3 8 37 45 82.2% 30 2 32 6.3% 77 76.0%

4 – Negative surprise 29 38 67 56.7% 10 1 11 9.1% 78 47.6%

Total 66 121 187 64.7% 112 12 124 9.7% 311 55.0% Notes: EPS surprise is the change in the actual annual EPS relative to the previous year divided by the share price at the end of the previous year To be considered a "Firm year with voluntary disclosure," at least one disclosure is required The sample period is January 1999 to June 2002 Voluntary disclosure includes any forward-looking disclosure outside of an earnings announcement

39

Table 8 (continued) – Frequency of Annual Voluntary Disclosure in Post- vs. Pre-Reg FD Periods Panel B – Control by Sales Surprise

Post-FD Pre-FD

Sales Surprise

Firm years with no voluntary disclosure

Firm years with voluntary disclosure

Total number of firm years

Percentage of firm years with voluntary disclosure

Firm years with no voluntary disclosure

Firm years with voluntary disclosure

Total number of firm years

Percentage of firm years with voluntary disclosure

Total number of firm years

Difference in percentage of voluntary disclosure

1 – Positive surprise 10 14 24 58.3% 38 6 44 13.6% 68 44.7%

2 11 31 42 73.8% 23 2 25 8.0% 67 65.8%

3 12 35 47 74.5% 18 2 20 10.0% 67 64.5%

4 – Negative surprise 14 43 57 75.4% 8 1 9 11.1% 66 64.3%

Total 47 123 170 72.4% 87 11 98 11.2% 268 61.1% Notes: Sales surprise is the change in annual sales relative to the previous year divided by the previous year’s sales To be considered a "Firm year with voluntary disclosure," at least one disclosure is required The sample period is January 1999 to June 2002 Voluntary disclosure includes any forward-looking disclosure outside of an earnings announcement

40

Figure 1

Revisions in Quarterly Forecasts After a Quarterly Earnings Announcement

0%5%

10%15%20%25%30%35%40%45%

0 1 2 3 4 5 6 7-59

Days

% o

f Rev

isio

ns

Post Pre

41

Figures 2 & 3

Revisions in Annual Forecasts After a Quarterly Earnings Announcement

0%5%

10%15%20%25%30%35%40%45%

0 1 2 3 4 5 6 7-59

Days

% o

f Rev

isio

ns

PostPre

Revisions in Annual Forecasts After an Annual Earnings Announcement

0%

10%

20%

30%

40%

50%

60%

0 1 2 3 4 5 6 7-59

Days

% o

f Rev

isio

ns

PostPre

42

Appendix A

Source: Special Study: Regulation Fair Disclosure Revisited, December 2001, Laura S. Unger.

Survey Date Respondents Findings

Thomson Financial

1/17/01 81 public companies Nearly 33 percent said FD has limited the flow of information they provide to buy- and sell-side analysts.

NIRI Survey

2/26/01 577 investor relation professionals

28 percent responded that they are providing more information post-FD; 48 percent responded that they are providing the same amount; and 24 percent responded that they are providing less.

AIMR Survey #1

3/26/01 423 AIMR members (investment analysts and portfolio managers)

57 percent believe the volume of substantive information released by public companies has decreased in the wake of FD; 14 percent said the volume has increased.

ABA FD Task Force Survey

4/01 62 members of the securities bar

45.2 percent said their clients are providing more information post-FD; 24.2 percent are providing the same amount; and 25.8 percent are providing less information.

PWC Survey #1

4/23/01 123 large issuer executives and 41 small issuer executives

31 percent say they are disclosing more, while 23 percent are disclosing less. 44 percent say FD has had no impact on the quantity of their disclosure.

SIA Survey 5/01 30 analysts, 505 investors, 94 SIA member firms, and 25 issuer general counsels

Approximately 25 percent of issuers feel they are communicating less to the public. Analysts estimate that nearly two-thirds of the issuers they follow communicate less.

PWC Survey #2

10/17/01 201 public company executives

48 percent said FD has influenced the quantity of their disclosures–of these, 37 percent said they are disclosing more information, while 11 percent said they are disclosing less.

AIMR Survey #2

10/18/01 303 AIMR members 51 percent believe companies are disclosing less substantive information; 18 percent believe more information is being disclosed; and 24 percent believe the same amount is provided.

43

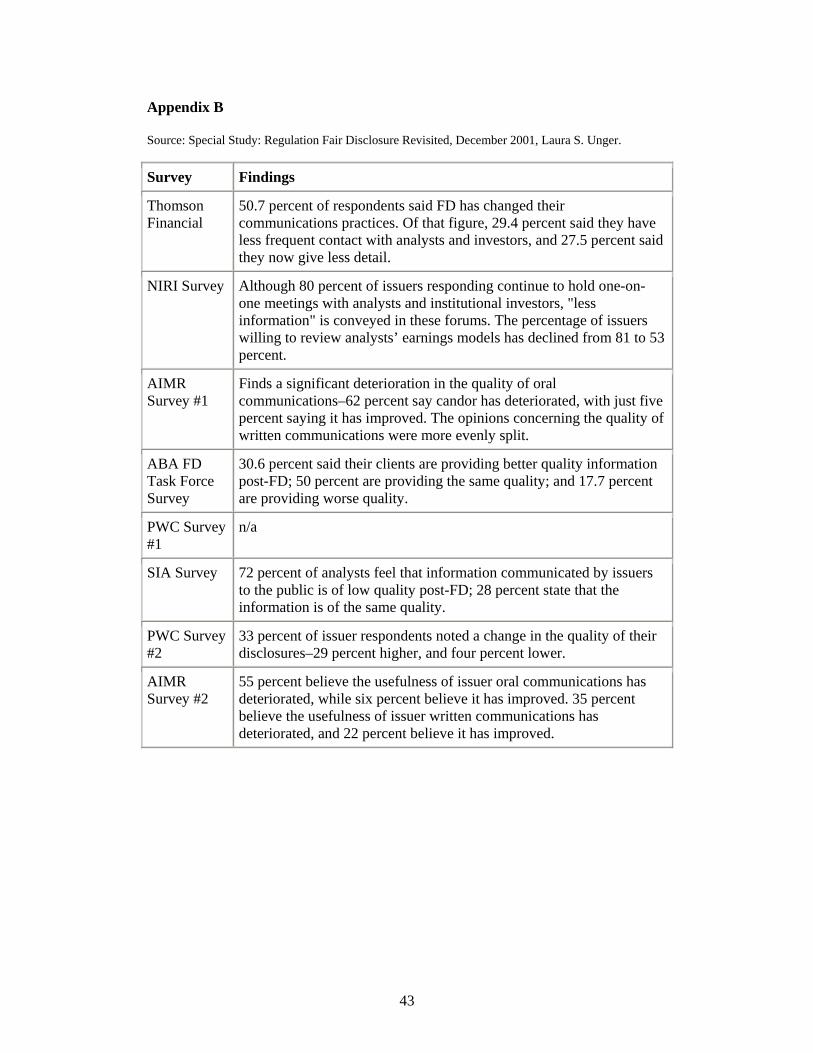

Appendix B

Source: Special Study: Regulation Fair Disclosure Revisited, December 2001, Laura S. Unger.

Survey Findings

Thomson Financial

50.7 percent of respondents said FD has changed their communications practices. Of that figure, 29.4 percent said they have less frequent contact with analysts and investors, and 27.5 percent said they now give less detail.

NIRI Survey Although 80 percent of issuers responding continue to hold one-on-one meetings with analysts and institutional investors, "less information" is conveyed in these forums. The percentage of issuers willing to review analysts’ earnings models has declined from 81 to 53 percent.

AIMR Survey #1

Finds a significant deterioration in the quality of oral communications–62 percent say candor has deteriorated, with just five percent saying it has improved. The opinions concerning the quality of written communications were more evenly split.

ABA FD Task Force Survey

30.6 percent said their clients are providing better quality information post-FD; 50 percent are providing the same quality; and 17.7 percent are providing worse quality.

PWC Survey #1

n/a

SIA Survey 72 percent of analysts feel that information communicated by issuers to the public is of low quality post-FD; 28 percent state that the information is of the same quality.

PWC Survey #2

33 percent of issuer respondents noted a change in the quality of their disclosures–29 percent higher, and four percent lower.

AIMR Survey #2

55 percent believe the usefulness of issuer oral communications has deteriorated, while six percent believe it has improved. 35 percent believe the usefulness of issuer written communications has deteriorated, and 22 percent believe it has improved.

44

Appendix C

Examples of differences in earnings guidance practices

Example 1:

On Oct. 17, 2000, Intel Corp. (“Intel”) announced record results for the third

quarter of 2000 and revised its outlook publication procedures in connection with the

adoption of Regulation FD. Intel said it would keep its Outlook forward-looking

statements and risk factors statements publicly available on its web site. Toward the

end of each fiscal quarter, it would have a “Quiet Period” when it would not update

Outlook, but before the start of the Quiet Period, the public could continue to rely on

the Outlook as reflecting Intel's most current expectations. The Quiet Period extends

to the day when Intel's next quarterly earnings release is published. Six months later,

on April 17, 2001, Intel announced: “Beginning this quarter (second quarter, 2001)

Intel will have a mid-quarter Business Update to the Outlook provided…”. Currently,

during Intel’s earnings quarterly press releases, Intel also announces the date for its

mid-quarter update. On July 17, 2001, Intel announced the results for the second

quarter of 2001 and its business outlook for the third quarter of 2001: “Revenue in

the third quarter of 2001 is expected to be between $6.2 billion and $6.8 billion.” In

addition, Intel announced that it planned “to provide a mid-quarter Business Update

to the Outlook provided below on Sept. 6”. On Sept. 6, 2001, Intel announced the

mid-quarter update, stating that it “expect[ed] revenue for the third quarter to be

within the previous expectation and slightly below the midpoint of the range provided

on July 17.” The release included updates regarding other expenses and capital

expenditures. Thus, Intel provides systematic forecasts with the earnings release, and

an update between earnings releases with a known date for the update.

45

Example 2:

On Oct. 29, 2001, FedEx Corp. (“FedEx”) updated its earnings outlook for

the second quarter, ending Nov. 30, 2001. In its press release, FedEx announced it

“expect[ed] to earn 40 cents to 45 cents a share excluding its slice of the aid package

and 61 cents to 66 cents a share including the $101 million in government

assistance.” On Dec. 19, 2001, FedEx reported the results for the second quarter

(ending Nov. 30, 2001). Earnings per share (not including the compensation from the

Air Transportation Safety and System Stabilization Act) were 57 cents per share. In its

press release, FedEx also included earnings forecasts for the third and fourth

quarters: “[W]e now expect earnings for the third quarter to be $0.25 to $0.35 per

diluted share, and earnings for the fourth quarter to be $0.70 to $0.80 per diluted

share”. The first announcement, on October 29, 2001, occurred between earnings

announcements and was intended to provide investors with a profit warning. The

second guidance coincided with the earnings announcement. Investors could not have

anticipated when the first announcement would be made, if at all.