the institute of chartered accountants of · pdf file... sirc of icai & ex-officio of...

TRANSCRIPT

OFFICE BEARERS

FOR THE YEAR 2015-2016

CA. SRINIVAS AGNIHOTRAM

Chairman(O) 2439872, Cell: 94409 43129E-mail: [email protected]

CA. K. SIVA RAMA KUMAR

Vice Chairman(O) 08672-222373, Cell : 99596 99597

E-mail: [email protected]

CA. SREENIVASA RAO GODAVARTHI

Secretary(O) 2473164, Cell : 93462 22567

E-mail : [email protected]

CA. V. RAMA MOHAN REDDY

Treasurer(O) 2487600, Cell : 98484 83691

E-mail : [email protected]

CA. K.V.N. POORNA CHANDRA RAO

Chairman, SICASA(O) 2437887, Cell : 98490 90111

E-mail: [email protected]

CA. B. SHIVAJI PRASAD

Managing Committee Member(O) 2473393, Cell: 98482 90289

E-mail: [email protected]

CA. K.V. RAMESH BABU

Managing Committee Member(O) 2491365, Cell : 98491 94000

E-mail: [email protected]

CA. S. AKKAIAH NAIDU

Managing Committee Member(O) 2578801, 2578802, Cell: 94414 94415

E-mail: [email protected]

CA. E.PHALGUNA KUMAR

Secretary, SIRC of ICAI & Ex-Officio of Vijayawada BranchCell : 94418 86303

E-mail : [email protected]

For Private Circulation Only

The Institute of Chartered Accountants of India(Set up by an Act of Parliament)

EDITORIAL BOARD

Editor : CA. SRINIVAS AGNIHOTRAM

Members : CA. K. SIVA RAMA KUMAR, CA. V. RAMA MOHAN REDDY

website: www.vijayawada-icai.orgE-mail: [email protected]@gmail.com

Phone: 0866 - 2576666, 2575505, 2575506

October, 2015VOL - VIII

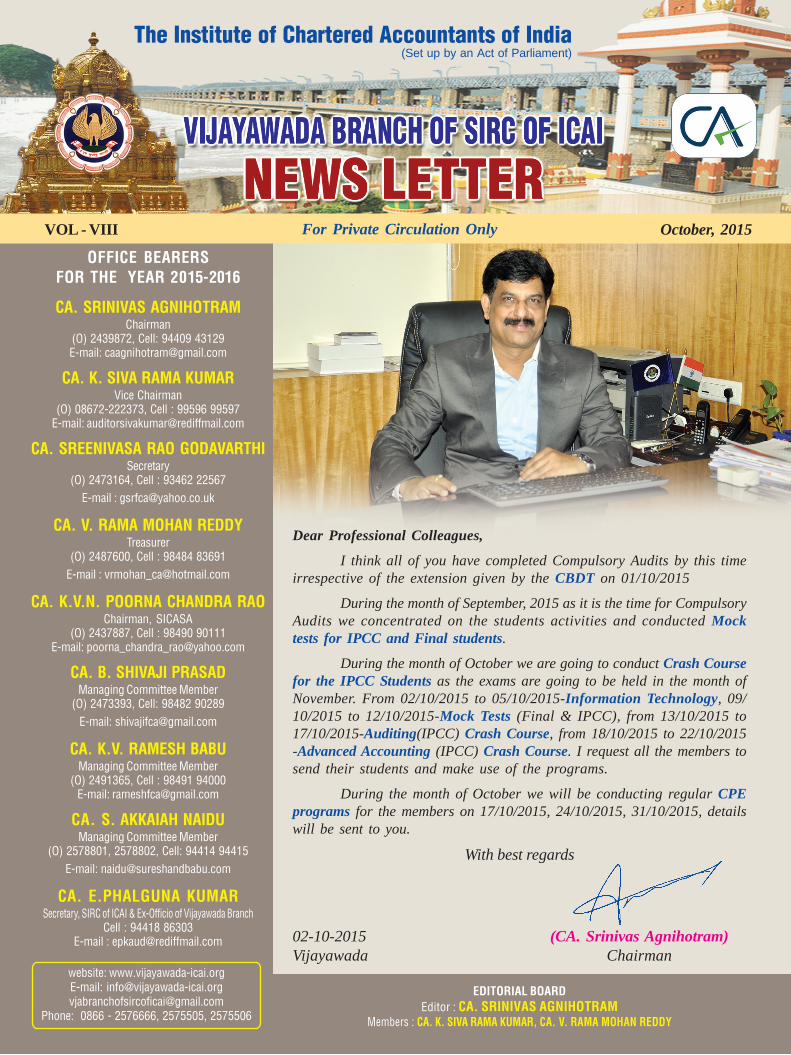

Dear Professional Colleagues,

I think all of you have completed Compulsory Audits by this timeirrespective of the extension given by the CBDT on 01/10/2015

During the month of September, 2015 as it is the time for CompulsoryAudits we concentrated on the students activities and conducted Mocktests for IPCC and Final students.

During the month of October we are going to conduct Crash Coursefor the IPCC Students as the exams are going to be held in the month ofNovember. From 02/10/2015 to 05/10/2015-Information Technology, 09/10/2015 to 12/10/2015-Mock Tests (Final & IPCC), from 13/10/2015 to17/10/2015-Auditing(IPCC) Crash Course, from 18/10/2015 to 22/10/2015-Advanced Accounting (IPCC) Crash Course. I request all the members tosend their students and make use of the programs.

During the month of October we will be conducting regular CPEprograms for the members on 17/10/2015, 24/10/2015, 31/10/2015, detailswill be sent to you.

With best regards

02-10-2015 (CA. Srinivas Agnihotram)Vijayawada Chairman

1. ON LIFE"My life is my message."

2. ON BEING A SOLDIER“I regard myself as a soldier, though a soldier of peace.“

3. ON FAITH IN HUMANITY“You must not lose faith in humanity. Humanity is an ocean; if a few drops of the ocean are dirty, the ocean doesnot become dirty."

4. ON NONVIOLENCE“Nonviolence is the first article of my faith. It is also the last article of my creed.”

5. ON THE SEVEN SINS“Seven social sins: politics without principles, wealth without work, pleasure without conscience, knowledgewithout character, commerce without morality, science without humanity, and worship without sacrifice."

6. ON TRUTH“An error does not become truth by reason of multiplied propagation, nor does truth become error becausenobody sees it. Truth stands, even if there be no public support. It is self sustained.”

7. ON THE "STILL SMALL VOICE"“The only tyrant I accept in this world is the 'still small voice' within me. And even though I have to face theprospect of being a minority of one, I humbly believe I have the courage to be in such a hopeless minority.”

8. ON LIBERTY“I’m a lover of my own liberty, and so I would do nothing to restrict yours.”

9. ON FORGIVENESS“The weak can never forgive. Forgiveness is the attribute of the strong.”

10. ON THE NATURE OF MAN“A man is but the product of his thoughts. What he thinks, he becomes."

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

5“Be the change that you wish to see in the world.” - Mahatma Gandhi

2015 (9) TMI 560 - KERLA HIGH COURT - Income Tax

THE COMMISSIONER OF INCOME TAX, COCHIN Versus M/s MERCHEM LIMITED

Disallowance under Sec.36(1)(va) r/w Sec.2(24)(x) - remittance of employees' contribution to Provident Fund and ESI hasbeen delayed beyond the due date of payment prescribed under the respective Acts - ITAT deleted the addition - Held that:-If the intention of a particular provision of a statute can be gathered from the language used by the legislation, then we arebound to abide by the language used therein in order to ascertain the intention. We are also of the opinion that there was aclear logic behind Sec.36(1)(va) and Explanation thereto since the Legislature intended that the amount received towardscontribution of the employee was money belonging to the employee and the assessee was not entitled to utilise the saidfund and enrich himself. So also, both the provisions supra will co-exist harmoniously without disturbing each other. Therefore,the distinction drawn to credit the amount of the employer and the employee was with a clear objective and there is noillegality or other legal infirmity in classifying the contributions of employees and employer in the matter of crediting thesame to the appropriate statutory authorities.

In that view of the matter, we are of the considered opinion that the view taken by the Tribunal which affirmed the decision ofthe 1st Appellate Authority that the Respondent was entitled to get deduction of the contributions received from the employeesif paid on or before the filing of the return under Sec. 139(1) was not correct. We are inclined to agree with the judgment ofthe Gujarat High Court in 'Gujarat State Road Transport Corporation's case (2014 (1) TMI502 - GUJARAT HIGH COURT)wherein held There is no amendment in Section section 36(1)(va) of the Income Tax Act and considering section 36(1)(va)of the Income Tax Act as it stands, with respect to any sum received by the assessee from any of his employees to whichthe provisions of clause (x) of sub-section (24) of section 2 applies, assessee shall not be entitled to deduction of suchamount in computing the income referred to in section 28 if such sum is not credited by the assessee to the employees'account in the relevant fund or funds on or before the due date as per explanation to section 36(1)(va) of the Act - By deletingSecond Proviso to section 43B by Finance Act, 2003, it cannot be said that Section 36(1) (va) is amended and/or explanationbelow clause (va) of sub-section (1) of section 36 is deleted, which is with respect to employees' contribution - Decided infavour of revenue.

2015 (9) TMI 559 - MADRAS HIGH COURT - Income Tax

M/s. Dharmapuri Paper Mills Pvt. Ltd. Versus The Joint Commissioner of Income Tax

Reopening of assessment - escaped income under Section 115JA - assessee had written back depreciation wrongly in theirprofit and loss account and that therefore the income chargeable to tax had escaped assessment - Tribunal held that booksprofit is not to be reduced by the excess provisions of depreciation credited in the profit and loss account? - Held that:- Theproviso under clause (i) of the Explanation makes it clear that in case where Section 115JA is applicable to an assessee inany previous year, the amount withdrawn from the reserves created or provisions made "in a previous year relevant to theassessment year commencing on or after the first day of April, 1997", shall not be reduced from the book profit unless thebook profit of such year has been increased by those reserves or provisions out of which the said amount was withdrawnunder the Explanation. It is not the case of the assessing officer that the provisions made by the assessee in this case wererelatable to a previous year relevant to the assessment year commencing on or after the first day of April, 1997.

Pointing out the object behind Section 115JA, it was contended by Mr.J.Narayanasamy, learned standing counsel that bya jugglery of the accounting methods, the assessee cannot always make it a "zero tax" company even while making profitsor at least showing profits to certain stakeholders. We appreciate the concern. But the law relating to income tax beingwhat it is, we do not think that the Court is entitled to go in for a purposive interpretation when the plain language of thetaxing statute is clear. Explanation (i) is very clear in its purport. The assessee may fall within the ambit of the mischiefsought to be undone by Section 115JA. But so long as the express language is in its favour, the mischief or no mischiefcannot be cured. - Decided in favour of assessee.

2015 (9) TMI 558 - DELHI HIGH COURT - Income Tax

Commissioner of Income Tax (Exemption) Versus Bhagwan Shree LaxmiNaraindham Trust

Scope of Section 115 BBC on trust - Registration under Section 12A denied - receipt of anonymous donations - whether thecase of the Assessee is clearly hit by the provision of Section 115BBC? - the case of the Assessee is not of public religioustrust but a case of spiritual organization as held by AO - Penalty proceedings under Section 271(1)(c) were directed to beinitiated separately - ITAT allowing the Assessee's appeal concluded that the Revenue had wrongly applied Section 115BBC of the Act to the case of the Assessee and accepting that the Assessee-Trust was carrying out various religiousactivities

Held that:- What can constitute religious activity in the context of the Hindu religion need not be confined the activitiesincidental to a place of worship like a temple. The Supreme Court in The Commissioner, Hindu Religious Endowments,Madras v. Sri LakshmindraThirthaSwamiar [1954 (4) TMI 29 - SUPREME COURT] held that "a religious denomination or

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

6“Live as if you were to die tomorrow. Learn as if you were to live forever.” - Mahatma Gandhi

organization enjoys complete autonomy in the matter of deciding as to what rites and ceremonies are essential accordingto the tenets of the religion they hold and no outside authority has any jurisdiction to interfere with their decision in suchmatters."

It might well be that a Hindu religious institution like the Assessee is also engaged in charitable activities which are verymuch part of religious activity. In carrying on charitable activities along with organising of spiritual lectures, the Assessee byno means ceases to be a religious institution. The activities described by the Assessee as having been undertaken by itduring the AY in question can be included in the broad conspectus of Hindu religious activity when viewed in the context ofthe objects of the Trust and its activities in general.

No legal infirmity in the conclusion of the ITAT that for the purpose of Section 115 BBC (2) (a) anonymous donations receivedby the Assessee would qualify for deduction and it cannot be included in its assessable income. - Decided against revenue.

2015 (9) TMI 557 - BOMBAY HIGH COURT - Income Tax

The Commissioner of Income Tax - 1 Versus M/s. BFIL Finance Ltd.

Income on account of short term capital gains on sale of property - selection of assessment year for taxation - Tribunalaccepting the additional evidences setting aside the entire issue of Short Term Capital Gain - Held that:- Even where anassessee has offered tax in the subject assessment year, it was open to the assessee before the Appellate Authority toraise additional grounds to the effect that same should not be included in the total income for the purposes of taxation. Theentire issue is with regard to the year of taxability has been restored to the Assessing Officer for fresh consideration.Therefore, the issue raised herein would also be a subject of consideration of the Assessing Officer while passing the orderon remand. In fact, the chargeability to tax as shortterm capital gain is not in dispute, only the year of taxability is to beexamined. The Assessee itself has offered the above amount to tax as short-term capital gain - No substantial questions oflaw. - Decided against revenue.

Depreciation on leased assets - Tribunal restoring the issue - Held that:- CIT(A) while following the order for the AssessmentYear 1995-96 has not followed the same in its entirety. The CIT(A) after holding that the assessee is not entitled to its claimfor depreciation as the lease transactions under reference, were not genuine did not consider the alternative submissionmade with regard to Finance Transaction. Besides, the order passed by the CIT(A) for the Assessment Year 1995-96, hadnot dealt with the genuineness of the lease transaction. Nevertheless, for the subject Assessment Year, he holds, it is notgenuine without giving any notice to the Respondent-Assessee. Therefore, by the impugned order, the Tribunal held thatCIT(A) has decided on the issue of the lease transaction not being genuine without having given a hearing to theRespondentAssesee. The CIT(A) ought to have given Respondent-Assessee an opportunity to meet the same.It is in theabove view that the impugned order of the Tribunal has restored the issue as raised in Question No.3 to the AssessingOfficer for fresh consideration - No substantial questions of law. - Decided against revenue.

2015 (9) TMI 556 - ITAT BANGALORE - Income Tax

M/s Subex Ltd. Versus Commissioner of Income Tax-III

Revision u/s 263 - as per CIT(A) AO did not verify the claim of the Assessee for deduction u/s.35D of the Act, by taking noteof the definition of capital employed and as to whether share premium can be considered as part of the capital employedand whether FCCBs can be considered as debentures and taken as part of capital employed for the purpose of allowingdeduction u/s.35D of the Act - Held that:- In the present case, the 1st year in which relief was allowed u/s.35D of the Act hassince been modified. Though such modification happened after the order u/s.263 of the Act, which order is impugned in thisappeal, it cannot be said that the 1st year of allowance of deduction u/s.35D of the Act stands allowed as claimed by theAssessee. In none of the decisions relied upon by the Assessee, it has been held that even if the 1st year of allowance ofa claim is withdrawn at a later point of time, still the revisional order would be bad in law on the ground that the 1st year aclaim had been allowed. We are of the view in such circumstances, the exercise of jurisdiction cannot be attacked on theground that it is only in the 1st year of allowance of a claim which is to be allowed over a period of time that jurisdiction u/s.263 can be exercised. We therefore reject this argument of the learned counsel for the Assessee. - Decided againstassessee.

Relief on the basis of "Cost of Project" u/s.35D(3)(a) - Held that:- It is only the fixed assets, being land, buildings, leaseholds,plant, machinery, furniture, fittings and railway sidings (including expenditure on development of land and buildings), whichare acquired or developed in connection with the extension of the industrial undertaking or the setting up of the newindustrial unit of the Assessee that should be considered. The Assessee issued GDRS and FCCBs and incurred expenditurein this regard. The proceeds of the issue were used to acquire shares of two foreign companies and thereby gain control ofthe two foreign companies. Therefore there were no fixed assets that were acquired or developed in connection with theextension of the industrial undertaking or setting up of the new industrial unit of the Assessee. The argument of the learnedcounsel for the Assessee cannot therefore be sustained and shares acquired cannot be treated by any stretch of imagination

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

7“An eye for an eye will only make the whole world blind.” - Mahatma Gandhi

as land or building, plant or machinery etc., and treated as "cost of project" for the purpose of allowing deduction u/s.35D- Decided against Assessee.

Share Premium - whether can be regarded as part of the Issued Share capital while computing "Capital Employed"? - Heldthat:- Sec.254(2) and the regular assessment proceedings, cannot be applied in the context of provisions of Sec.263 of theAct. The power u/s.263 of the Act is a supervisory power and protection of the interest of the revenue owing to an erroneousorder is the salutary purpose of those provisions. The provisions of Sec.78 of the Companies Act, 1956 on which thedecision of Sirhind Steel Ltd. (2005 (9) TMI 218 - ITAT AHMEDABAD-D) proceeded provides for a limited fiction of treatingshare premium as part of paid up capital for the purpose of reduction of the same. Sec.78(2) of the Companies Act, 1956prohibits use of share premium for any purpose other than the purposes set out therein. Can it be said that share premiumcould be employed in the business of the Assessee as share capital? In our view therefore there is no merit in the contentionof the learned counsel for the Assessee that share premium should be regarded as part of the "issued share capital" forallowing deduction u/s.35D of the Act - Decided against the Assessee.

Treatment to FCCB - whether FCCBs can be considered as "Debentures" and taken as part of capital employed for allowingdeduction u/s.35D? - Held that:- Conclusions of the CIT are unsustainable. In the light of the definition of Debentures ascontained in the Companies Act, 1956 to include Bonds and in the light of the fact that the FCCBs in question are in thenature of bonds as defined in the Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository ReceiptMechanism) Scheme, 1993 wherein the meaning FCCBs is given as "bonds issued in accordance with the said schemeand subscribed by a non-resident in foreign currency and convertible into ordinary shares of the issuing company in anymanner, either in whole, or in part, on the basis of any equity related warrants attached to debt instruments, we are of theview that FCCBs are to be regarded as debentures and consequently be considered as part of "capital Employed" forallowing deduction u/s.35D of the Act. - Decided in favour of the Assessee.

Unrealised foreign exchange gain - Whether should be treated as "Income" or not? - Held that:- In our view the facts of thecase in the decision of the Madras High Court in the case of PVP Ventures Ltd. (2012 (7) TMI 696 - MADRAS HIGH COURT), is identical to the facts of the case of the Assessee in this appeal. FCCBs are instruments issued to investors for raisingfunds which is repayable after certain period. It is a debt instrument. The increase or decrease in liability on account offluctuation in foreign exchange as on the date of the Balance sheet would increase or decrease the liability of the Assesseeand such liability would be on capital account. Therefore the gain or loss would be on capital account and not taxable. -Decided in favour of the Assessee.

2015 (9) TMI 555 - ITAT BANGALORE - Income Tax

Pole to Win India (P.) Ltd. Versus Deputy Commissioner of Income-tax, Circle 11 (3) , Bangalore

Transfer pricing adjustment - selection of comparable - Held that:- Maple eSolutions Ltd. be excluded from the set ofcomparable companies as objection of the assessee with reference to this company is with regard to the financials of thecompany, on the ground of unreliability of data being acceptable.

Vishal Information Technological Services Ltd., Asit C Mehta Financial Services Ltd. (earlier known as Nucleus Netsoft&GIS (India) Ltd.) - Admittedly, as pointed out by the ld. D.R., there is no disputing the fact that the assessee had neverobjected to the inclusion of these companies in the set of comparables in earlier proceedings both before the TPO and theCIT(A). It is also seen that even in the grounds of appeal raised before us, the assessee has not raised any grounds or anyadditional grounds of appeal challenging the inclusion of these two companies in the list of comparables. In this factualmatrix, since no cause of grievance arises to the assessee from the impugned order, on the inclusion of these companiesas comparables, this claim of the assessee is not maintainable as there is no adverse finding in the impugned orders callingfor or requiring us to adjudicate thereon. We, therefore, finding that the contentions raised by the learned AuthorisedRepresentative of the assessee in respect of these companies are not maintainable, reject the same. Consequently, theinclusion of these two companies i.e. Vishal Information Technological Services Ltd. and Asit C Mehta Financial ServicesLtd. in the final list of comparables is upheld.

Computation of Operating Cost of the assessee - assessee's claim for treating its claim for additional depreciation to betreated as an item of extra-ordinary expenditure and therefore should be reduced from operating cost - Held that:- If, ascontended by the assessee, this expenditure pertains to earlier assessment year's also, then in the fitness of things thisissue ought to be re-examined afresh by the TPO to ascertain whether and how the assessee's claim has been applied tothe comparable companies also so that there will be parity when the said expenditure is proportionately applied to theoperating cost of the assessee and comparable companies. In this view of the matter, we set aside the issue of theassessee's claim of additional depreciation being an item of extra-ordinary expenditure to the file of the TPO for freshexamination and adjudication thereon in the light of our observations above, after affording the assessee adequate opportunityof being heard and to file details/submissions required.

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

8“Happiness is when what you think, what you say, and what you do are in harmony.” - Mahatma Gandhi

Contingent expenses in the nature of provision for telecom expenses - Held that:- As it is seen that the assessee has itselfdisallowed these expenses in the computation of taxable income on the ground that it is contingent liability. We find that theassessee's reliance on the decision in the case of Haworth India Pvt. Ltd. (2013 (8) TMI 421 - ITAT DELHI), wherein it hasbeen held that expenses disallowed should be excluded from operating cost, is well placed and therefore agree with theassessee's contention that expenses disallowed in computation of taxable income should be excluded from operatingcost.- Decided in favour of assessee.

Foreign exchange income/loss to be non-operating income/loss and excluded the same while computing the margins in thecase of comparables - it is submitted that on grounds of parity the same should be excluded from operational income/losswhile computing the margins of the assessee also - Held that:- On consideration we are unable to accept the assessee'sclaim. We find that there are several decisions of this and other Tribunals which hold that foreign exchange gain/lossesrelated to the assessee's business activities are to be treated as operating income/expense for computing the operatingmargins of both the assessee and the comparable companies and therefore, we uphold the TPO's action in including thesame while computing the assessee's margins - we direct the TPO to recompute the margins of both the assessee and thecomparable companies by treating the foreign exchange gain/loss as operating income and to compute the margins of boththe assessee and the comparable companies accordingly - Decided against assessee.

Deduction under Section 10A - assessee contended that the Assessing Officer erred in not appreciating that income whichis eligible for exemption under Section 10A of the Act does not form part of total income at all and therefore does not enterthe normal computation mechanism so as to enable a reduction of business losses and unabsorbed depreciation of otherSTP units - Held that:- The Hon'ble High Court of Karnataka in the case of CIT v. Yokogawa India Ltd. [2011 (8) TMI 845 -Karnataka High Court] has held that deduction under Section 10A of the Act is to be given without setting off the unabsorbedbrought forward losses. In the case on hand, the Assessing Officer has computed the eligible deduction under Section 10Aof the Act after setting off brought forward unabsorbed business losses. Respectfully following the decision of the Hon'bleHigh Court of Karnataka in the case of Yokogawa India Ltd. (supra), we direct the Assessing Officer to allow the deductionunder Section 10A of the Act without setting off the brought forward unabsorbed business loses.- Decided in favour ofassessee.

2015 (9) TMI 554 - ITAT BANGALORE - Income Tax

Mac Charles India Ltd Versus Deputy Commissioner of Income-tax, Circle -12 (1) , Bangalore

Disallowance of depreciation on land on which assessee had leasehold rights - alternate claim of assessee that thepayment had to be allowed as revenueHeld that:- As decided in assessee's own case for AY 2006-07 to 2008-09 the leaserent paid for acquiring leasehold rights over the land can never be treated as cost of the plant (windmill). The functional testcannot be extended to a case of lease rent for acquiring leasehold rights over the land, whatever be the technical requirementof erecting a plant. The law is well settled that no depreciation is to be allowed on land. By placing reliance on the functionaltest, it is not possible to allow depreciation on land indirectly. If such a claim were to be allowed, then it could be extendedto a case of a land over which a shopping mall is constructed. A shopping mall requires a good area/location, main road forgood business. Can it be said that the rent paid for the land over which the shopping mall is constructed is part of thebuilding on which depreciation is to be allowed? In our view, by applying the functional test, it is possible to contend in all thecases that the land is a tool of trade and has to be regarded as plant or building. We therefore decline to accept theproposition canvassed on behalf of the assessee.

Hon'ble High Court of Karnataka in the case of HMT Ltd. (1992 (11) TMI 37 - KARNATAKA High Court), has considered thepremium for acquiring leasehold rights as nothing but rent paid in advance. The rent paid in advance was for acquiringleasehold rights over the land. Such payment had been considered by the Hon'ble Court as revenue expenditure. In view ofthe aforesaid decision of the Hon'ble High Court which is in parimateria with the facts of the present case, we are of the viewthat the lump sum rent paid for the entire period of 30 years has to be considered as revenue expenditure. The CIT(A)wrongly distinguished this decision as a case of lease of factory building. We therefore accept the alternative prayer of theassessee. - Decided partly in favour of assessee.

Disallowance u/s.14 of the Act read with Rule 8D - Held that:- It is crystal clear that assessee had a number of transactionsin mutual fund units and equity shares during the relevant previous year. It would be naive to presume that assessee wouldnot have incurred any expenditure, but for the brokerage. Claim of the assessee that no indirect expenditure was incurredand there was no necessity of any management inputs in taking decisions regarding the investment portfolio that were to bemaintained during the year, cannot be believed.The rule of preponderance of probability can be applied in such circumstances,and the onus to show that no expenditure was indeed incurred falls back on the assessee. The circumstances here aresuch that the note given by the assessee before the AO was prima-facie incorrect and unbelievable. At the same time it istrue that the AO had not called upon the assessee to prove its claim that no expenditure was indeed incurred by it forearning the exempt income. We set aside the orders of authorities below and remit the issue regarding disallowance under

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

9“First they ignore you, then they ridicule you, then they fight you, and then you win.” - Mahatma Gandhi

Section 14A back to the file of AO for denovo consideration after obtaining the explanation of the assessee. - Decided infavour of assessee for statistical purposes.

Interest u/s.234B - assessee contested as paid advance-tax of more than 90% of the assessed tax - Held that:- It is clearthat if the assessee had paid more than 90% of the assessed tax, then levy of interest u/s.234B cannot be done. Assessedtax has also been defined in the said section - In our opinion none of the lower authorities had applied their mind to therelevant section before charging interest u/s.234B of the Act. CIT (A) had considered it simply as a consequential ground.We set aside the issue of levy of interest u/s.234B of the Act, back to the file of the AO for consideration afresh inaccordance with law. - Decided in favour of assessee for statistical purposes.

2015 (9) TMI 553 - ITAT BANGALORE - Income Tax

Sri LaxmidasBapudasDarbar Versus The Income Tax Officer, Ward 1, Bagalkot.

Income under the head "Long Term Capital Gain" (LTCG) on surrender of tenancy rights - Whether the CIT(Appeals) wasright in coming to the conclusion that there was no transfer of leasehold rights by the assessee in favour of the lessors? -Held that:- Admittedly, the compromise decree was registered and a sum of ? 8,49,639 was incurred as stamp duty andregistration expenses in registering the compromise decree. A further sum of ? 5,81,090 had also been incurred to demolishthe structure on the area surrendered to the lessors by the Assessee. It may be true that the compromise decree does notrefer to the payment of the sum of ? 33 lacs as a payment for surrender of leasehold rights by the Assessee, but thecircumstances of the case clearly show that the said payment was towards surrender of leasehold rights. The only modificationis that the said sum of ? 33 lacs was to be taken by the Assessee after incurring expenses for registration of compromisedecree and expenses of demolition of structures. The sum of ? 33 lakhs is therefore rightly assessable to tax u/s. 45 of theAct and not under the head 'income from other sources. The fact that the compromise decree does not refer to the paymentof ? 33 lacs cannot be the basis to hold that the said sum is not towards surrender of leasehold rights. There was nonecessity for the lessors to pay the aforesaid sum but for the Assessee relinquishing leasehold rights over part of theproperty in favour of the lessors. We therefore hold that the sum of ? 33 lacs was paid in lieu of the Assessee surrenderinghis leasehold rights in favour of the lessors subject to certain directions for incurring of certain expenses by the Assesseeand therefore the said receipt by the Assessee is attributable to release of leasehold rights in favour of the lessors.Consequently the sum of ? 33 lacs is assessable to tax under the head "Capital Gains" subject to the computationprovisions of Sec.48 of the Act. We hold accordingly.

Tax the FMV of 42 guntas of land & building obtained by the assessee under compromise decree in the form of perpetualleasehold right under the head 'income from other sources' - Held that:- As far as the assessment of FMV of 42 guntas ofland & building which was given on a permanent lease to the assessee under the compromise decree as income from othersources, we are of the view that the assessee was already having leasehold interest over the said area of the land and thecompromise decree only reaffirms the said position. The assessee has not acquired any right whatsoever over this propertyby virtue of compromise decree. Therefore, conclusion of the CIT(Appeals) to tax the FMV of this property is without anybasis. There is no provision under the Act, under which the sum in question can be brought to tax. U/s. 56(2)(vii) which wasinserted by the Finance Act, 2009 w.e.f. 1.10.2009, the FMV of immovable property which is transferred without consideration,can be brought to tax in the hands of transferee. Even assuming that there was a transfer of leasehold rights in favour of theassessee by virtue of compromise decree, the provisions of section 56(2)(vii) are not applicable for the assessment year2006-07 and therefore assessment directed by the CIT(Appeals) cannot be sustained and the same is hereby deleted.

Expenses towards dismantling structures of leasehold property - Held that:- U/s. 48 of the Act, there is no requirement thatexpenditure incurred wholly and exclusively in connection with the transfer, has to be incurred only by the assessee. Sincethe factum of expenditure having been incurred is not disputed and since, admittedly, this was an expenditure incurredwholly and exclusively in connection with such transfer, the deduction claim, in our view, had to be allowed. We hold anddirect accordingly. We also find merit in the contention of the learned counsel for the Assessee that since this expenditurewas specifically required to be incurred by the Assessee under the receipt cum acknowledgement dated 27.6.2006, itconstitutes a diversion of income at source and cannot be construed as income that accrued to the Assessee.

Deduction being the indexed cost of acquisition of the structure - Held that:- We are of the view that the said claim fordeduction is unsustainable for the reason that the subject matter of transfer by assessee in favour of the lessors did notinclude any structure and therefore the claim would fail to satisfy the test as laid down in section 48(ii) of the Act.

Cost of acquisition of leasehold rights disallowed - Held that:- The capital asset transferred was a leasehold right. Evidenceon record goes to show that leasehold rights have been acquired by the assessee's predecessors in interest in the year1907 i.e., 07.12.1907 by paying a sum of ? 8,500. The assessee would therefore be entitled to claim deduction of cost ofacquisition of leasehold interest as on 1.4.1981. The assessee will also be entitled to benefit of indexation of this cost uptothe date of transfer of the leasehold rights. The assessee has not quantified this sum and therefore, in our view, it would bejust and proper to direct the assessee to make a claim before the AO in this regard. The AO is directed to examine such aclaim and allow deduction in accordance with law. - Decided partly in favour of assessee.

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

10“I like your Christ, I do not like your Christians. Your Christians are so unlike your Christ.” - Mahatma Gandhi

CHAPTER 8

1. Low class men desire wealth; middle class men both wealth and respect;but the noble, honour only; hence honour is the noble man's true wealth.

2. The lamp eats up the darkness and therefore it produces blackened lamp; inthe same way according to the nature of our diet (sattva, rajas, or tamas) weproduce offspring in similar quality.

3. O wise man! Give your wealth only to the worthy and never to others. Thewater of the sea received by the clouds is always sweet. The rainwater enlivensall living beings of the earth both movable (insects, animals, humans, etc.) and immovable (plants, trees, etc.), andthen returns to the ocean where its value is multiplied a million fold.

4. The wise who discern the essence of things have declared that the yavana (meat eater) is equal in baseness to athousand candalas (the lowest class), and hence ayavana is the basest of men; indeed there is no one more base.

5. After having rubbed oil on the body, after encountering the smoke from a funeral pyre, after sexual intercourse, and afterbeing shaved, one remains a chandala until he bathes.

6. Water is the medicine for indigestion; it is invigorating when the food that is eaten is well digested; it is like nectar whendrunk in the middle of a dinner; and it is like poison when taken at the end of a meal.

7. Knowledge is lost without putting it into practice; a man is lost due to ignorance; an army is lost without a commander;and a woman is lost without a husband.

8. A man who encounters the following three is unfortunate; the death of his wife in his old age, the entrusting of moneyinto the hands of relatives, and depending upon others for food.

9. Chanting of the Vedas without making ritualistic sacrifices to the Supreme Lord through the medium of Agni, andsacrifices not followed by bountiful gifts are futile. Perfection can be achieved only through devotion (to the SupremeLord) for devotion is the basis of all success.

10. There is no austerity equal to a balanced mind, and there is no happiness equal to contentment; there is no diseaselike covetousness, and no virtue like mercy.

11. Anger is a personification of Yama (the demigod of death); thirst is like the hellish river Vaitarani; knowledge is like akamadhenu (the cow of plenty); and contentment is like Nandanavana (the garden of Indra).

12. Moral excellence is an ornament for personal beauty; righteous conduct, for high birth; success for learning; and properspending for wealth.

13. Beauty is spoiled by an immoral nature; noble birth by bad conduct; learning, without being perfected; and wealth bynot being properly utilised.

14. Water seeping into the earth is pure; and a devoted wife is pure; the king who is the benefactor of his people is pure;and pure is the brahmana who is contented.

15. Discontented brahmanas, contented kings, shy prostitutes, and immodest housewives are ruined.

16. Of what avail is a high birth if a person is destitute of scholarship? A man who is of low extraction is honoured even bythe demigods if he is learned.

17. A learned man is honoured by the people. A learned man commands respect everywhere for his learning. Indeed,learning is honoured everywhere.

18. Those who are endowed with beauty and youth and who are born of noble families are worthless if they have nolearning. They are just like the kimshukablossoms( flowers of the palasa tree) which, though beautiful, have no fragrance.

19. The earth is encumbered with the weight of the flesh-eaters, wine-bibblers, dolts (dull and stupid) and blockheads, whoare beasts in the form of men.

20. There is no enemy like a yajna (sacrifice) which consumes the kingdom when not attended by feeding on a large scale;consumes the priest when the chanting is not done properly; and consumes the yajaman (the responsible person)when the gifts are not made.

BEST CHANAKYA QUOTES

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

11“Freedom is not worth having if it does not include the freedom to make mistakes.”- Mahatma Gandhi

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

12345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012345678901234567890123456789012123456789012345678901234567890121234567890123456789012345678901212345678901234567890123456789012123456789012345678901234567890

VIJAYAWADA BRANCH OF SIRC OF ICAI — News Letter OCTOBER, 2015

12“Nobody can hurt me without my permission.” - Mahatma Gandhi

|ü+#·<ës¡ s¡T∫ì e÷Á‘·yT ø±<äT... n+<ëìï ≈£L&Ü Á|ükÕ~düTÔ+~...

‹j·T´ì |ü+#·<ës¡ $$<Ûä s¡ø±\ ‹qTã+&Üsê\≈£î s¡T∫ì n+~düTÔ+~. Ç< |ü+#·<ës¡ n+<ëìï ≈£L&Ü Á|ükÕ~düTÔ+~.

á $wüj·T+ #ê˝≤ eT+~øÏ ‘Ó*j·T<äT. e+{Ï+{À¢ ñ+& |ü+#·<ës¡ #ùd nHø£ s¡ø± …’q ñ|üjÓ÷>±\qT ‘Ó\TdüT≈£î+fÒ

Çø£ n+<ä+ MT kı+‘·yT...

kÕ<Ûës¡D+>± Á|ü‹ ˇø£ÿs¡÷ ‘·eT ej·TdüT‡ø£+fÒ ‘·≈£îÿe>± ø£ì|æ+#ê\ì ø√s¡Tø√e&É+ düVü≤»+. BìøÏ |ü+#·<ës¡

#·ø£ÿ>± |üì #düTÔ+~. #·¬øÿs¡ À j·÷+{° @õ+>¥ z ø±s¡ø£+>± |üì #düTÔ+~. #·s¡à+ eTè<äTe⁄>± e÷sê\+fÒ

ns¡ø£|ü |ü+#·<ës¡ì bÕe⁄ø£|ü ø=ã“]q÷HÓ À ø£\|ü+&ç. Bì˝À ¬s+&ÉT #·Tø£ÿ\ ìeTà>∑&ç¶ q÷HÓ yj·÷*. á

$TÁXe÷ìï >±* Á|üy•+#·ì &Éu≤“˝À b˛dæ ø±e\dæq|ü&É ≤¢ ˇ+{ÏøÏ |ü{Ϻ+∫ u≤>± s¡T<ä›+&ç. Ç˝≤ #j·T&É+‘√ eTè‘·ø£D≤\T ‘=\–b˛sTT #·s¡à+

yÓT]dæb˛‘êsTT.

ydü$ ø±\+˝À m+&É Á|üuÛ≤e+‘√ bÕ≥T <äTeT÷à... <Ûä÷[\ Á|üuÛ≤e+ m≈£îÿe>± ñ+≥T+~. Bìe\¢ #·s¡à+ô|’ eTT]øÏ ù|s¡T≈£î b˛‘·T+~. Ç˝≤+{Ï

düeTj·T+˝À ø£|ü #·¬øÿs¡qT, ns¡ø£|ü Ä*yé ÄsTT Ÿ q÷HÓì, ¬s+&ÉT #Ó+#ê\ ìeTàs¡kÕìï ø£\T|ü⁄ø√yê*. á $TÁXe÷ìï ˇ+{ÏøÏ sêdüT≈£îì

ø±ùd|ü⁄ s¡T<äT›≈£î+fÒ q\T|ü⁄<äq+ ‘·>∑TZ‘·T+~.

eTTK+ u≤>± n\dæb˛sTT ø£ì|ædüTÔ+fÒ ø£|ü #·¬øÿs¡ À bÕe⁄ø£|ü Ä*yé q÷HÓ ø£*|æ <ëì˝À ˇø£ Á^Hé {° u≤´>∑T bı&çì ø£\T|ü⁄ø√yê*. á

$TÁXe÷ìï ø£ s√»+‘ê |üø£ÿqô|{Ϻ eTsêï{Ï qT+∫ Bìï eTTU≤ìøÏ sêdüT≈£îì XóÁuÛÑ|üs¡T#·T≈£î+fÒ eTTK+ô|’ ñ+& eTè‘·ø£D≤\˙ï ‘=\–b˛‘êsTT.

@ |ü+&ÉT ‹+fÒ @+{Ï Á|üjÓ÷»q+...?

ø=ìï s¡T>∑à‘·\ ìyês¡D˝À ø=ìï s¡ø±\ |ü+&ÉT¢ Ç‘√~Ûø£+>± yT\T #kÕÔsTT. @ s¡ø£+ |ü+&ÉT¢ m˝≤+{Ï yT\T

#kÕÔjÓ÷ ‘Ó\TdüTø√yê\+fÒ á ø£<∏äq+ #·<äe+&ç. >∑T+&ÓqT |ü]s¡øÏå+#·Tø√yê\+fÒ Á<ëø£å |ü+&É¢qT rdüTø√yê*.

Á<ëø£å, *N |ü+&É¢ À >∑T+&Ó≈£î Äs√>±´ìï Ç#à bÕ*|æHê Ÿ‡ n~Ûø£+>± ñ+{≤sTT. ø±´q‡sY e+{Ï yê´<ÛäT\qT

n]ø£≥º&É+˝À bÕ*|òæHê Ÿ‡ u≤>± |üì #kÕÔsTT.

Áu…dtº ø±´q‡sY≈£î #Óø ô|{≤º\+fÒ *N\T ñ|üj·TTø£ÔyÓTÆq$. Bì˝À j·÷+{° Äøχ&Ó+{Ÿ j·÷øϺ${° m≈£îÿe>± ñ

+≥T+~. u§bÕŒsTT, |ü⁄#·Ã|ü+&É¢ À ;{≤ ÁøÏbıø±‡+~∏Hé >∑TD≤\T m≈£îÿe>± e⁄+{≤sTT. Ç$ \+>¥ ø±´q‡sY qT+∫

ø±bÕ&É‘êsTT. Ç‘·s¡ s¡ø±\ ø±´q‡s¡¢ qT+∫ ø±bÕ&ç *ø√ô|qT¢ \_ÛkÕÔsTT.

u§bÕŒsTT˝Àì |üô|sTTHé m+C…’yéT Js¡íXøÏÔøÏ u≤>± düVü≤ø£]düTÔ+~. ˇø£ ø£|ü C≤eT|ü+&ÉT eTTø£ÿ˝À¢ \_Û+# $≥$THé dæ s√EyêØ nedüsêìø£+fÒ

◊<äT ¬s≥T¢ m≈£îÿe e⁄+≥T+~. eT<Ûä düÔ+>± ñ+& ø£eT˝≤|ü+&ÉT˝À ø£+fÒ Ç~ m≈£îÿe>± ñ+≥T+~.

$≥$THé dæ n~Ûø£+>± e⁄+& |ü+&ÉT¢ ‹H eTVæ≤fi˝À¢ #·s¡à+ô|’ eTT&É‘·\T e#·Ã neø±XÊ\T $T>∑‘ê yê]ø£+fÒ ‘·≈£îÿe>± e⁄+{≤sTT. u≤´ø°º]j·÷qT

m<äTs=ÿH XøÏÔ ≈£L&Ü \_ÛdüTÔ+~. s¡ø£Ôb˛≥TqT ‘·–Z+#·>∑\ bı{≤wæj·T+ n‹Ô, ns¡{Ï|ü+&É¢ À \_ÛdüTÔ+~.

ø= …ÅkÕº ŸqT ‘·–Z+#·>∑\ |”#·T|ü<ës¡ú+ >∑+>∑πs>∑T |üfifl˝À, j·÷|æ Ÿ‡˝À m≈£îÿe>± \_Û+#·>∑\e⁄. s√E≈£î nedüs¡yÓTÆq |”#·T˝À q\u…’ XÊ‘·+ á

|ü+&É¢qT+∫ \_ÛdüTÔ+~. |”#·T |ü<ësêú\T m≈£îÿe>± ‹Hyê]˝À ø= …ÅkÕº Ÿ kÕúsTT ‘·≈£îÿe>± ñ+{≤sTT.

|üs¡>∑&ÉT|ü⁄q ˙fió¢ ‘ê–‘ ãs¡Te⁄ ‘·>=Z#·TÃ...

|üs¡>∑&ÉT|ü⁄q eT+∫˙s¡T ‘ê>∑&É+ e\¢ nkÕ<Ûës¡DyÓTÆq nHø£ Äs√>∑ Á|üjÓ÷»Hê\T ñHêïsTT. mH√ï nHês√>∑

düeTdü \≈£î ìyê]DÏ>± |üì #düTÔ+~. ñ<äj·÷Hï ìÁ<ä Òe>±H ø£ dü+ ˇø£ ©≥s¡T ˙{Ïì ‘ê>∑&É+ eT+∫<äì

yÓ’<äT´\T dü\Vü‰ ÇdüTÔHêïs¡T. nsTT‘, s¡T ‘ê–q ‘·sê«‘· ø£ dü+ z >∑+≥ es¡≈£î m˝≤+{Ï ÄVü‰s¡+ rdüTø√≈£î+&Ü

ñ+&É≥+ eT+∫~.

n+‘ø±≈£î+&Ü, |üs¡>∑&ÉT|ü⁄q ˙s¡T ‘ê>∑&É+ e\¢ ô|<ä›Áù|>∑T XóÁuÛÑ|ü&ç eT]ìï b˛wüø±\qT Á>∑Væ≤düTÔ+~. n˝≤π>,

ø=‘·Ô s¡ø£Ô+ ‘·j·÷ØøÏ, ø£+&És¡ ø£DC≤\ n_Ûeè~ΔøÏ m+‘·>±H√ <√Vü≤<ä|ü&ÉT‘·T+~. ñ<äj·÷Hï ˙{Ïì ‘ê>∑&É+ e\¢

20 qT+∫ 25 XÊ‘·+ yTs¡≈£î XØs¡ yÓT≥u≤*C≤ìï ô|+#·T≈£î+~. Ç~ XØs¡ ãs¡Te⁄qT ‘·–ZdüTÔ+~. XØs¡+˝À Á<äe|ü<ësêúìï ø√˝ÀŒ≈£î+&Ü,

ÇHÓŒ¤ø£åHé‡ <ä]#s¡≈£î+&Ü b˛sê&ÉT‘·T+~.

j·÷<˚M düs¡« uÛÑ÷‘˚wüß

X¯øÏÔ s¡÷ù|D dü+dæú‘·

qeTdüÔôd’à qeTdüÔôd’à qyÓ÷ qeT:

<˚$ Äd”düT‡\‘√ MTs¡+<äs¡÷

düTK XÊ+‘·T\‘√ Äq+<ä+>± ñ+&Ü\ì ø√s¡T≈£î+≥T....

MT

lìyêdt n–ïVü≤√Á‘·+

$»j·T<äX¯$T X¯óuÛ≤ø±+ø£å\T

BOOK - POST PRINTED MATTER To

Contents of this News Letter do not necessarily represent the views of Vijayawada Branch of SIRC of ICAI unless otherwise statedEdited and published by the Editorial Board of the Branch & DTP at Akshaya Graphics & Printers, Vijayawada.

IF UNDELIVERED PLEASE RETURN TO :

VIJAYAWADA BRANCH OFSOUTHERN INDIA REGIONAL COUNCIL OFTHE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

D.No. 27-12-63, 64,65, Alibaig Street, Governorpet,VIJAYAWADA - 520 002. Ph: 0866 - 2576666

Glimpses of Mock Test for Final & IPCC Students