the iso’s guide to payfac-like customer...

TRANSCRIPT

The ISO’s Guide to

Payfac-like Customer Experience

E B O O K

Staying Afloat as an ISO

The volume of merchants is only increasing. In 2016, all micro, small and medium retailers (MSMR) had a global market size of $34 trillion in payments.1 Merchants are opening new doors and ecommerce sites every day and new transaction volume records are achieved each year. So nothing to worry about, right? There’s plenty of fish in the sea! Wrong.

The rules are changing. New business models, like those used by payment facilitators (payfacs), are changing merchant expectations by promising a lightning-fast, digital experience. They are powerboats in a world of canoes, and merchants are flocking

to their nets instead of your fishing rod. Sure, every large acquirer is busy building and rolling out custom-made vessels, but what’s an independent sales organization to do?

You might not be able to catch the same fish as the really big guys, but in reality, you’re fishing in a different lake. Take a glance at those motoring alongside you and read this eBook to learn how you can get faster and power ahead.

This is your guide to onboarding more merchants than the competition in a digital age by achieving payfac-like customer experience through efficiency.

The Merchant Acquiring industry is like a fishing business. Whether you’re a small ISO, a super ISO, or an acquirer, the same imperative applies. You must continuously acquire more merchants, or the competition will get them first. Catch fish, or go out of business.

Why Onboarding? Why now? 4

How onboarding will grow your business 7

ALL ABOARD: Turn nibbles to bites 8

CATCH MORE AT ONCE: Drive referrals 10

ALL IN A DAY’S WORK: Productivity is key 11

How to actually board more merchants 13

PREPARING YOUR VESSEL: Streamlined process 13

FISHING WITH A NET: Automation 15

BUILD, BUY, OR FRANKENSTEIN? 16

Platform 17

AGILE IMPLEMENTATION 18

EVALUATING A VENDOR 19

Conclusion 20

Contents

Why Onboarding? Why Now?

Consider this: Netflix put Blockbuster out of business because movie-lovers would rather stay home in their pajamas than drive to rent the movie they actually want to see. If you can save time and make life easier for the merchants and acquirers you work with, you stay in the game.

Including the ISO’s role, it takes the average merchant acquirer 3-5 days to get a new merchant fully set up and operating (or in other words, ‘onboarded’). Of course, there is massive variance here. The top 1-2% onboard same-day, and the slowest take upwards of 1-2 weeks.

In 2010, the Square crashed in like a tidal wave and began onboarding merchants in 15 minutes or less, from any device connected to the internet. At first, Square naysayers thought they’d never reach Netflix-level disruption,

Why is the merchant onboarding process important? Time-saving and convenience has become the ultimate value proposition, yet the merchant application and set-up process is one of the least convenient experiences in all of financial services.

but now the fact that they have seems like old news.

Square has completely overtaken the micro-merchant market and is almost synonymous with small business credit card acceptance. They haven’t removed the need for large acquirers because they serve different markets, similar to how Netflix hasn’t removed the movie theater market. They have, however, stolen the bottom of the market from underneath them.

Most importantly, Square has fundamentally changed merchant expectations for speed, convenience, and experience. Merchants now consider any application and approval process that takes more than a few hours frustrating, or even unacceptable. That’s why the rest of the industry, including those who didn’t think Square was their competition, are still scrambling to catch up several years later.

4

platforms, but those that do offer seamless integration to their merchant acquirer so no information has to be re-keyed twice. In some instances, merchant acquirers offer their ISOs digital platforms to make the entire onboarding process more convenient and so the acquirer can be more efficient.

World Bank Group noted that merchants are flocking to those who offer more services in one place, but are nearly ignoring those who don’t have frictionless onboarding experiences. Even if you don’t offer more services, you still need to be a player in the game. Small acquirers and ISVs (independent software vendors) that resemble payment facilitators have similar requirements from an onboarding perspective but very different approaches when it comes to managing risk.2 World Bank Group listed smooth onboarding as one of the top five things that merchants “need”, along with good salespeople, training, follow-up visits, customer service, and hardware or software installation and troubleshooting.

Enter, the payment facilitator. Square may not be the first ISO to act as a payment facilitator, but they have popularized the business model. Now, hundreds of companies are keen to offer their merchants a digital onboarding experience, in which they only need 6-8 pieces of KYC information up-front, and ask for more information as time goes on and more payments are processed. Payment facilitators also take on the risk and conduct their own underwriting so the merchant acquirer doesn’t have to. This domino approach of capturing small bits of data at a time and underwriting them as they go, means underwriting less information more frequently. Although this model is often perceived as being more risky to payment facilitators than the traditional model is to ISOs, it allows companies to get merchants processing payments faster.

Not only has this emerging payment facilitators trend made it more convenient for merchants, but their digital platforms make sharing data with merchant acquirers much easier. Not all payment facilitators have open

5

“Not only is it relevant for non-traditional payment actors to play a part in the value chain, but it is also needed; in particular, they can have a competitive or complementary advantage for the value chain’s merchant onboarding and relationship management elements.” - World Bank Group, “Innovation in Electronic Payment Adoption”

This trend of emerging payment facilitators has made it clear that ISOs must get stronger on two fronts:

ISOs who automate their onboarding processes can achieve most, if not all of these things, and stay ahead of the competition, earn revenue faster than before, and in some cases increase their merchant volume.

Think of it as upgrading your canoe for a powerboat. If you’re not fast and easy to do business with, you won’t have the chance to fish at all.

6

merchants want a digital experience,

fast results, and more product

offerings in one place; and

merchant acquirers

want to work with businesses who have

open, integrated digital platforms

to share data easily and increase

efficiency.

Imagine for a moment that a merchant acquirer is a fish monger.

An ISO, a fisher, only spears and brings a few fish (merchants) to the

monger to sell in their store, but there’s a better chance they’re going

to be high-quality catches. It’s up to the monger, however, to clean

and prepare the fish to determine if they are actually good

enough to sell (i.e., conduct risk assessment or due diligence.)

If anyone who eats the fish sold at the monger’s store gets

sick (is fraudulent, launders money, or goes bankrupt),

the monger takes the blame (pays out). A payment

facilitator, on the other hand, fishes with a huge net

and catches many fish at once. They sell these on

behalf of the monger’s store at their own market stall.

Here, though, they clean and pick out the bad ones

as they’re selling them off their cart and give the

monger a cut of what they make. In some cases,

this can be riskier to the payfac, as they take

all the responsibility if someone gets sick,

but they have many more fish to sell. If

they get too many people sick though, the

monger’s reputation could bedamaged too.

If you were the fish monger, who would you

rather do business with?

How Onboarding Will Grow Your Business

We’re not talking about keeping up with Square and other payfacs or ISVs just for the sake of it.

Even if these industry disruptors were not threatening your business, using onboarding automation can drastically improve and enhance your efficiency and revenue. Imagine your sales team could ask merchants to click a link, fill out a digital form on the spot, and have an answer to the merchant almost instantly.

Next, we’ll explain why you can’t afford to have a slow, clunky, paper-based, error-ridden canoe. Or rather, onboarding process. Designing a better merchant onboarding experience will help you grow your business and cut costs. Any new project that doesn’t help you do one or both of those things is not worth your time.

7

Let’s say you get 500 applications per month, but only 40% of them actually board with you. That’s 3,600 merchants for the year. If each merchant was worth about $1,500, you’d make about $5.4M over the course of the year. If you boarded 99% of those applications, however, you’d get 5,940 new clients and $8.9M that year. Who doesn’t want an extra $3.5M?

8

Think about how many merchant applications you send out that you simply never get back. It’s like when you cast a fishing line and can feel some nibbles, but get no bites.

Most ISOs today have paper-based onboarding or, at best, siloed digital forms, separate from their automated systems. ISOs who also conduct KYC checks or full underwriting often do so manually. Therefore, there’s no empirical way to measure just how many merchants abandon ship during the application or later onboarding process.

After working with hundreds of payment service providers over the years, we estimate that most organizations are losing between 25-40% of merchants during the onboarding process. Of the merchants who get sent back their applications due to missing or incorrect information (not in good order), only about 50% of them submit a revised application. If you are only converting 50-75% of merchants who begin the onboarding process with you, you’re in serious trouble.

ALL ABOARD

To solve this problem, we need to understand why merchants abandon the signup process

• It’s slow

• It’s inconvenient

• It doesn’t meet them on their terms

• It’s filled with friction

• It’s filled with human error

• It doesn’t offer everything they need in one place

Other ISOs, payfacs, or ISVs offer them the opposite.

If you were asked, with your current sales team, to increase sales volume by 25-40% by the end of next quarter, you would balk.

“There’s only so much each sales person can do.”

But if you could reduce merchant onboarding abandonment to less than 5%, you would hit your goal.

If your merchant onboarding platform is digital and all the information you capture can be seamlessly integrated into your acquirer’s systems, even better. They will get the full benefit of your sales conversion and be happier with your partnership as a result. By catering to both the merchant and the acquirer, you cover both sides of the business.

The merchant is happy with an easy, user-friendly experience. Reel them in.

The merchant acquirer is happy to work with your efficient, integrated systems. Sell like hotcakes.

9

The merchant application and onboarding is the first date. It’s the crucial first impression. Too many ISOs view the onboarding process as a formality that happens after the merchant has committed. That’s a mistake.

Referral marketing research tells us that 83% of customers are willing to refer your service if they are satisfied3. This is especially true in the Payments world, where a slow onboarding process will lose you business to the faster ISO or ISV.

And just to remove any ambiguity from the equation, “excellent” means 2 things:

• Fast

• Convenient

Yes, a powerboat. When merchants and merchant acquirers interact with a fast and easy system, they will recommend it to their colleagues. You’ll bring in more merchants by referral than you could by hiring more salespeople. To offer a streamlined experience, you don’t need a revolutionary app that makes headline news. All you need is a fast, convenient, digital process that fully boards merchants in under an hour. If you’re able to accomplish that, you’ll be catching fish by the netful, rather than one at a time.

The industry is fixated on same-day processing, same-day approvals, and same-day solutions. If you can’t receive a merchant application and provide approval within a day, your lure isn’t attractive enough. With Agreement Express, the basic onboarding workflow can take as little as 10 minutes.

CATCH MORE AT ONCE

10

Converting all your merchants and driving referrals is the heavy lifting that automated onboarding does for you. But there’s a critical third component of business growth that happens when you begin to build a more efficient onboarding and underwriting process: your sales team and back-office staff get twice as productive.

Your sales team excels at building trust with prospects quickly and convincing merchants their life would be better with the products and services you sell. They do not excel at wrangling paperwork, follow-up emails, and liaising with the back-office or merchant acquirer team to make sure they received the correct merchant application.

If your sales team received 95% of their merchant applications fully completed and correct the first time, and did not need to act as a middleman between the merchant and back-office, they would save hundreds of hours a year that they could use to focus on winning new clients. You would essentially win the equivalent of a doubled sales team.

One of our clients reduced the back-and-forth time spent with customers from 95 mins per customer to 5 mins per customer. This saved their team about 3,000 hours over the year, or 57 hours per week, that they could spend on more specialized tasks.The merchant acquirers you work with will be thrilled to not have to follow up with the merchant for missing information, or re-key merchant data into their systems. This saves an enormous amount of time on their end and this efficiency makes you more desirable to work with. It’s like

11

ALL IN A DAY’S WORK

offering the fish monger fish that have

already been cleaned.

Now, imagine running each merchant

application through an automated

risk assessment tool before passing

it to the merchant acquirer. Each time

you handed over an application, you

could also include a score indicating

how risky it is and all the data needed

to show why. This would be like doing

all the dirty work to prepare a fish for

market. Only you wouldn’t even have

to hire an underwriting team to offer

your merchant acquirers this perk and

make their underwriting process more

efficient. Take that, payfacs.

Electronic Cash Systems (ECS) is a merchant service provider who offers their customers access to a variety of products all in one place and deals with many processors and banks. This makes them unique in their industry, but also more complicated.

“We have to integrate with a lot of applications for our various products and partners, and Agreement Express helps us do that,” said CEO Fadi Cheikha

When a merchant fills in an application, Agreement Express tracks everything that ECS needs including their driver’s license, signature and acceptance of terms and conditions. Before automating this process, much of this application information would be missing upon first submission, so ECS had to go back to the customer to correct it or fill it in. In some cases, by the time they reached out a second time, the customer had changed their mind. The concern about merchants dropping out due to NIGO (not in good order) applications was only one of the reasons Cheikha adopted automation.

“Having an automated underwriting piece was also

important to us,” said Cheikha, “because

7

Case Study: Electronic Cash Systems

12

we were doing all of our underwriting and pulling all of our reporting manually before. The Agreement Express Risk Scorecard automates all of that for us.”

Cheikha shared that using Agreement Express is a differentiator for them to compete against their competition as it makes them even more unique.

“We can onboard customers, provide a risk assessment, underwrite and monitor them. We settle a lot of products

because of this back-end system.”

Eventually, ECS hopes to become a complete back-end system that conducts all merchant acquiring services themselves, cutting out the middleman.

“Agreement Express solves a big part of the challenges we face as we work toward our goals,” said Cheikha. “The best part about them is the increased

efficiency. It opens up huge growth opportunities for the organizations they work with, like us.”

How to Actually Onboard More Merchants

Now that you’re convinced onboarding automation is the silver bullet for growth (or at least, a silver bullet) let’s dig into how you can begin to onboard merchants faster and better.

There are essentially two components to designing a better onboarding and risk assessment process:

• Creating a minimum viable onboarding process

• Automating that process

PREPARING YOUR VESSEL STREAMLINED PROCESSIn truth, creating a digital merchant application form isn’t that hard. The hard part is creating the flow of the merchant onboarding process and figuring out what to do with the merchant data.

The very first step in creating a faster, more delightful, cost-efficient onboarding process is to design a minimum viable process. This involves doing the least work possible to achieve the most effective result. It’s always important to consider your return on investment, regardless of whether it’s time, money, or people resources you’re investing in. Think about designing a slick powerboat rather than fishing out of a canoe. Removing operational inefficiencies is like patching holes in your fishing boat, and cutting cost inefficiencies is using diesel fuel.

13

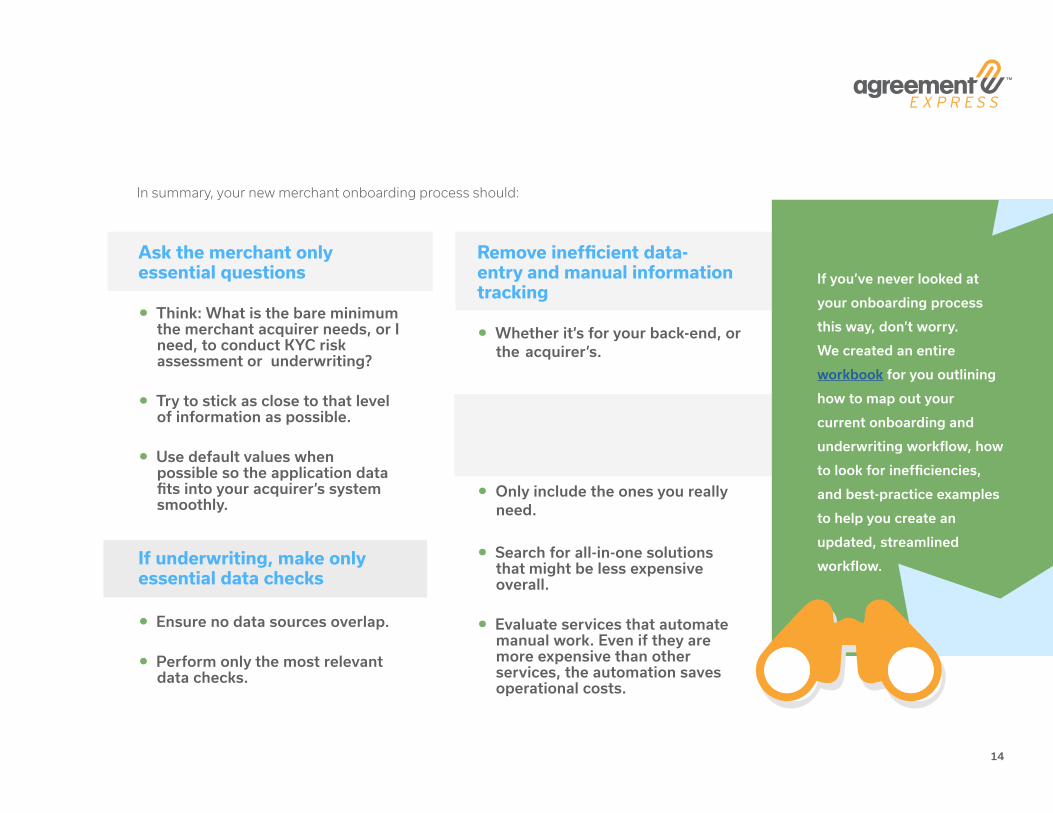

Ask the merchant only essential questions

• Think: What is the bare minimum the merchant acquirer needs, or I need, to conduct KYC risk assessment or underwriting?

• Try to stick as close to that level of information as possible.

• Use default values when possible so the application data fits into your acquirer’s system smoothly.

If underwriting, make only essential data checks

• Ensure no data sources overlap.

• Perform only the most relevant data checks.

14

Remove inefficient data-entry and manual information tracking

• Whether it’s for your back-end, or the acquirer’s.

Structure any third-party services involved from least to most expensive

• Only include the ones you really need.

• Search for all-in-one solutions that might be less expensive overall.

• Evaluate services that automate manual work. Even if they are more expensive than other services, the automation saves operational costs.

In summary, your new merchant onboarding process should:

If you’ve never looked at

your onboarding process

this way, don’t worry.

We created an entire

workbook for you outlining

how to map out your

current onboarding and

underwriting workflow, how

to look for inefficiencies,

and best-practice examples

to help you create an

updated, streamlined

workflow.

AUTOMATIONEvaluate services that automate manual work. Before defaulting to the least costly option, consider the operational costs automation will save. Developing a streamlined onboarding process is only step one. Step two is where you can begin to reach Square-level onboarding speeds with automation. If your minimum viable process is your fishing vessel and removing inefficiencies is filling holes and choosing diesel, automation is the motor that gets you going and allows your net to catch as many fish as possible.

A good onboarding software platform will remove all extraneous data channels including emails, physical paper, and spreadsheets. This frees up your sales team to focus on finding and securing new deals, rather than chasing paperwork.

Regulators are increasingly pushing ISOs of all sizes to at least conduct some KYC practices on merchant applications before sending them off to underwriting. A good automated onboarding software will have the option to add-on an automated KYC or underwriting tool to see the application all the way through from initial data collection, to verification, underwriting, and final approval. 15

The risk assessment platform will automatically complete relevant data checks and complete straight-through-processing, depending on your merchant acquirer’s specific risk guidelines and rules, freeing up the underwriters to focus on the more complex cases and do what they do best, not making data calls and collating information into spreadsheets.

When you offer a merchant experience that easy and fast, you’ll be bringing in fish by the netful while your peers continue to fish out of canoes with a rod.

Automation is no longer simply an option. If you want to compete with payment facilitators, you have to have a central onboarding platform. Regulators would argue each ISO should have their own KYC risk assessment platform incorporated in this too. It’s the only way you’ll begin to consistently onboard more merchants than your competition as you scale and the industry continues to change. Those who don’t have fast, digital boarding will become as outdated as Blockbuster.

Next, we’ll dive into the specifics of how to implement a merchant onboarding automation platform.

FISHING WITH A NET

16

At this point, you might be wondering what the options are to get a solution like this in place. Large ISOs might consider hiring a development team to build a system in-house. Small to mid-sized ISOs might wonder if they could afford to buy a solution like this, or perhaps cobble together individual, separate systems with their existing legacy systems. A digital signature product here, a data warehouse there, and a digital forms application here. We call this approach, “Frankenstein.”

It’s important to consider all three options, so you understand what you’re getting into. Onboarding and KYC automation is a big undertaking, and you need to count not just cost, but other factors as well.

BUILD VS. BUY VS. FRANKENSTEIN

PROS

Annual license feesVery high up-front cost

No expertise on best practices

High failure rate

Slow times to market

Difficult to scale as your company grows

Difficult to iterate for new compliance regulation needs

No external support or troubleshooting

Non-integrated solution to an integrated problem

Not reliable

Very difficult to troubleshoot

Reliance on APIs to keep system working System won’t scale with your company

Very difficult to maintain fully auditable records

Reliably working aspects of onboarding Less expensive than purchasing an enterprise solution

Lower up-front cost

Working with onboarding and underwriting experts Fast time to market Reliable, end-to-end platform

Fully scalable Immediate and long term success Easily auditable records

Iterates automatically for new regulation compliance needs

No annual license fees

You can take your time

CONS

BUY BUILD FRANKENSTEIN

Platform

Once you have either built, bought, or mashed your automation platform together, you should have the following components:

This simplifies just how complex the onboarding and risk assessment process can be, but if you have deeply thought through how you can compress your process and use automation to power it, you will be onboarding your merchants in under one hour. Some of our ISO customers have achieved onboarding in under 10 minutes!

17

It’s not enough to simply create a minimum viable merchant onboarding process. Just collecting less information through the same paper process, and potentially having the same underwriters conducting slightly fewer data checks isn’t going to make you competitive against payment facilitators. Without automation, you may make your back-office more efficient, but you won’t offer the end-user a digital customer experience with a “wow” factor and speed that will drive referrals and make them choose you over another payfac or ISV.

If you do not implement a central automated onboarding platform, the tack you used to fill holes in your boat will simply fall away to your old processes as salespeople choose to operate out of their email inbox, underwriters begin to do some extra Googling, and administrative staff decide to work from print-outs because it’s what they’re used to. You may have a boat and a net, but no motor to put them to good use.

A digital forms interface

A merchant onboarding document management dashboard

A risk scorecard (for KYC or underwriting)

An underwriting work queue (if you do KYC or underwriting)

Data, analytics, and reporting dashboard

Connectivity to your system of record and/or to your merchant acquirers’ system

Whether you choose to build, buy, or Frankenstein, how you choose to implement your new automated process is crucial to its future success. Rather than coming up with a master plan and taking 1-2 years to execute it, we’ve found that agile implementation is faster and more efficient. This method involves getting the bare bones of your streamlined merchant onboarding process up and running first. Following this method, you could be ready to digitally board merchants as soon as two weeks after signing with a vendor.

What’s agile about it? As the plans get built out, it’s easy to iterate and remain flexible for changes along the way. You can add more, but only necessary, complexity to the process as you go. Think of starting with the shell of a powerboat and adding insulation, seating, and rigs as you go. In payments language, maybe a new regulation came into play since you signed the deal, or you realized you need a KYC check that you didn’t need before. This can easily be incorporated into the platform as you implement, rather than having to wait a year or two after the platform has been built to start fishing or start making changes.

18

AGILE IMPLEMENTATION

“Tomorrow’s technology stack is... composed of open and flexible systems. It is inherently agile and can reorganize to predict and meet market needs on short notice. A must for payments players today and in the future.”

-Accenture, “Driving the Future of Payments”4

19

In your search for the best merchant onboarding vendor to partner with, evaluate results that they have had with existing clients. In particular, we recommend looking into results such as:

98%6WEEKS

Software implementation time of 6 weeks or less achieved through agile activation methodology

Near elimination of application errors with real-time data

validation and error checking

Increase client application return rate to more than

98%

Near elimination of all data entry (in the back-office or for the

merchant acquirer) through data reuse and external data capture

and verification

Reduction of average onboarding time to less than 30 minutes (no underwriting) or an

hour (including underwriting)

Instant risk assessment and decisioning through

automated underwriting (if applicable)

Straight-through processing from

merchant application to underwriting to acquirer

Sales and underwriting departments productivity

increases greater than 40%, allowing for scale

%+40

EVALUATING A VENDOR

This decision criteria will help you weed out traditional BPM-oriented vendors who may have succeeded in major software implementations for some of these specific criteria, but will not be able to help your independent sales organization achieve an end-to-end digital transformation of the merchant boarding process. They might be good at building charter ships, not the powerboat you need.

Conclusion

A minimum viable merchant onboarding process is a sturdy boat from which to fish for merchants and automation is the motor that gets you out to sea. You can’t compromise either of these components in your quest to compete against payment facilitators with a fast, easy, digital experience for both your merchants and acquirers.

What are your next steps?

Take stock of your current processes. Decide how many holes you need to fill, then get to work automating your new process. If you follow the principles in this short guide, you will be well on your way to onboarding more merchants than your competition. They won’t know what hit them.

You’re in Good Company

Still confused about where to start or what the best practices are to onboard merchants in under 10 minutes? Try out our streamlined onboarding process workbook, or give us a call and tell us about your processes and needs. We can give you advice and tell you where we might fit in.

Email us to book a call or directly ask one of our onboarding experts any questions at [email protected].

1 Innovation in Electronic Payment Adoption: The case of small retailers. The World Bank Group, June 2016. http://www3.weforum.org/docs/Innovative_Solutions_Accelerate_Adoption_Electronic_Payments_Merchants_report_2016.pdf

2 Fitzpatrick, Peter for Laszig, Dale and Murphy, Patti. November 2017. The Green Sheet. “From acquiring to facilitating: How payfacs are changing the acquiring market - Part 2.” Source: http://www.greensheet.com/emagazine.php?article_id=5545

3 Why Referral Marketing Works and How to Use It. Texas Tech University, 2015. http://today.ttu.edu/posts/2015/04/why-referral-marketing-works

4 “Driving the Future of Payments: 10 Mega Trends,” Accenture, November 2017

ABOUT AGREEMENT EXPRESS Agreement Express enables merchant acquirers and ISOs worldwide to offer their customers best-in-class experiences. The platform makes the merchant application process easier and completely digital. It is the first solution to help top performing financial institutions gather, use, and reuse customer data to make subsequent product applications easier.

The Agreement Express Risk Scorecard is used to achieve instant approvals by automating the KYC and underwriting process. The platform calculates an amalgamated risk score using data collected on the merchant application and from third party data services. This score determines if the account can be automatically approved or if it requires underwriter review, in accordance with the organization’s risk thresholds.