the israeli economy: challenges and opportunities objectives of economic policy for 2011-2012 state...

TRANSCRIPT

The Israeli Economy: Challenges and

OpportunitiesObjectives of Economic Policy for 2011-2012

State of IsraelMinistry of Finance

Click here for attached press release

Topics:

Israel’s economy: strengths, weaknesses, threats, and opportunities

Challenges of economic policy

Key points of economic policy

Challenges of Economic Policy

Resilience of the economic system to shocks

Increase in per-capita GDP and improvement of relative positioning

Strengthening disadvantaged population groups and reducing social inequalities

Key Points of Economic Policy

Chapter I – The future of human capital and the sophisticated industries

Chapter II – Infrastructure development and promotion of internal growth drivers

Chapter III – Addressing the labor market

Chapter IV – Responsible fiscal policies

Strengths and Opportunities

A tradition of structural reforms and responsible fiscal policies

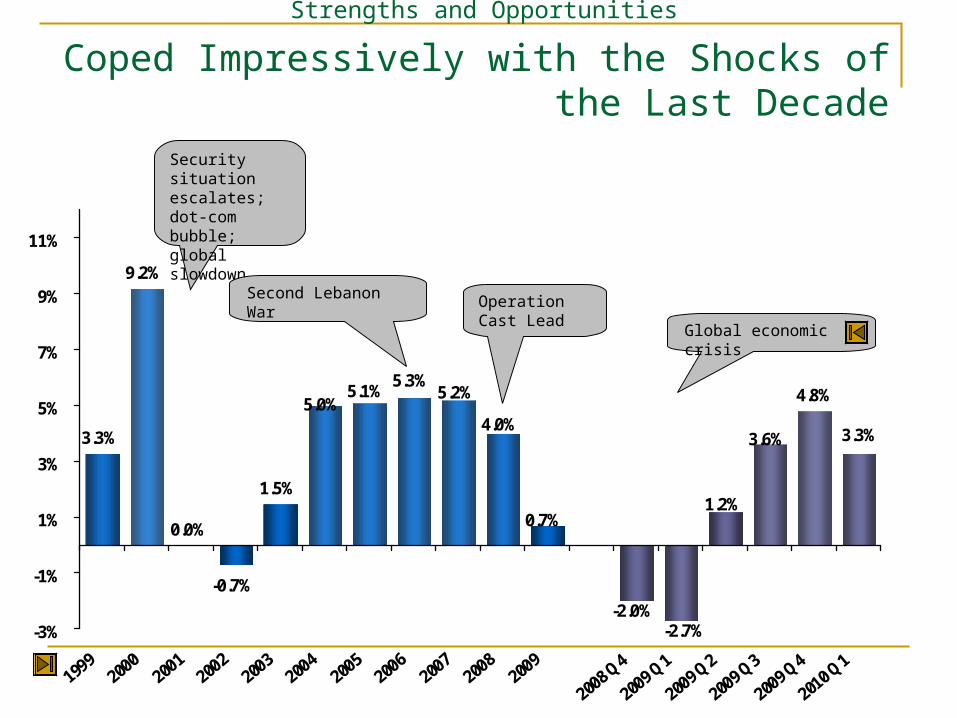

Coped impressively with the challenges of the last decade

Strong starting point compared to peer countries

The Israeli Economy: Strengths, Weaknesses, Threats, and Opportunities

A Tradition of Structural Reforms and Responsible Fiscal Policies

Five years of high growth rates (until the crisis) Consistent surplus in balance of payments; strong

currency Responsible, growth-supporting fiscal policies:

Gradual reduction of level of public expenditures Falling levels of deficit and debt Competitive tax rates Balance and stability in the public-sector wage system

Monetary stability

Strengths and Opportunities

3.3%

9.2%

0.0%

-0.7%

1.5%

3.3%3.6%

4.8%

0.7%

4.0%

-2.0%-2.7%

1.2%

5.0%

5.3%5.2%5.1%

-3%

-1%

1%

3%

5%

7%

9%

11%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2008 Q

4

2009 Q

1

2009 Q

2

2009 Q

3

2009 Q

4

2010 Q

1

Security situation escalates; dot-com bubble; global slowdown

Second Lebanon War

Operation Cast Lead

Global economic crisis

Coped Impressively with the Shocks of the Last Decade

Strengths and Opportunities

Strong Starting Point Compared to Peer Countries

Growth-supporting fiscal environment High national expenditure on R&D Outstanding knowledge-intensive industries High quality of human capital Flexible business-sector labor market

Strengths and Opportunities

Signs of Erosion and Threats Erosion of human capital and knowledge-intensive

industries Worsening competitive conditions in the global arena Rapid changes in composition of population – education

and employment Quality of services for citizens and businesses in need of

improvement Infrastructure gaps – overloaded transportation systems;

land and real estate Heavy burden of defense along with security risks Uncertainty in the global economy

The Israeli Economy: Strengths, Weaknesses, Threats, and Opportunities

Relative advantage in leading fields

Ongoing improvement in macro data

Good launching point at emergence from the crisis

High growth potential for the Israeli economy

Window of opportunity to take advantage of success

One Economy – Two Stories

Trend towards erosion of advantages Demographic scenario: decline in

employment and productivity, increase in social inequalities

Uncertainty in the global economy Regional / security-related instability

Doubts regarding growth potential; level of competition and level of inequality

Need to inject new fuel into growth engines

An opportunity to set the direction of the economy for the coming years

The Israeli Economy: Strengths, Weaknesses, Threats, and Opportunities

Challenges of the Economic Policy

Resilience of the economic system to shocks

Increase in per-capita GDP and improvement of relative positioning

Strengthening disadvantaged population groups and reducing social inequalities

Key Points of Economic Policy

Chapter I – The future of human capital and the sophisticated industries

Chapter II – Infrastructure development and promotion of internal growth drivers

Chapter III – Addressing the labor market

Chapter IV – Responsible fiscal policies

Chapter I – The Future of Human Capital and the Sophisticated

Industries Promotion and development of knowledge-intensive industries

Human capital – education and reform of higher education

Increasing the relative advantage of export industries while granting precedence to industry in peripheral regions

Key Points of Economic Policy

Chapter II – Infrastructures and Promotion of Internal

Growth Drivers Physical infrastructures – land, real estate,

transportation Improved services for citizens and reduced

bureaucracy Improved ability to do business More efficient court system Better management and execution capabilities in the

public sector Structural reforms – energy, ports, communications,

and defense industries

Key Points of Economic Policy

Chapter III – Addressing the Labor Market

Adoption of policy targets in the area of employment A national plan for employment of chronically

unemployed persons based on the “Employment Lights” format

Removal of barriers for Haredi (ultra-orthodox) men to seek work

Improvement of tools for the encouragement of employment of Arab women

Reduction of the number of foreign workers Addressing the problem of illegal entry

Key Points of Economic Policy

Section IV – Responsible Macro-Economic Policies

A continued responsible fiscal policy – a sustainable fiscal rule: Desirable government size Falling deficit trajectory Debt reduction

Two-year budget

Key Points of Economic Policy

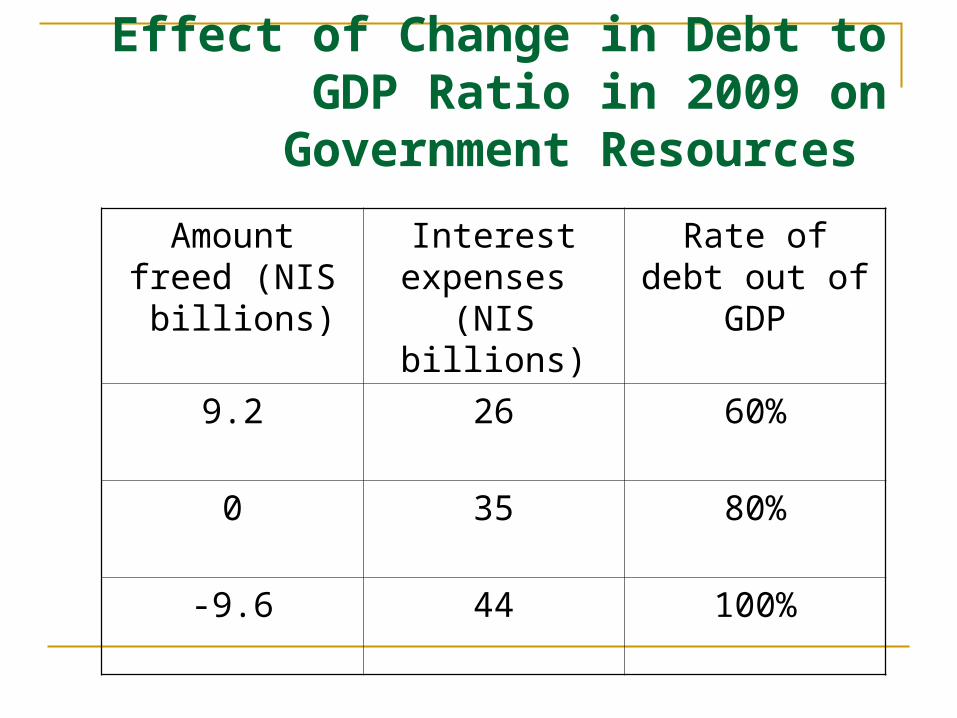

Maintaining fiscal credibility

Effect of Change in Debt to GDP Ratio in 2009 on

Government Resources

Rate of debt out of GDP

Interest expenses

(NIS billions)

Amount freed (NIS billions)

60%269.2

80%350

100%449.6-

Israel’s Credit Rating

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Moody's S&P Fitch

A1/A+

A2/A

A3/A-

Baa1/BBB+

Baa2/BBB

Baa3/BBB-

Aa3/AA-

Current credit rating Moody’s - A1 (Stable)

S&P – A (Stable)

Fitch – A (Stable)

Nov 2007S&P upgrade

Israel to A

Nov 2007S&P upgrade

Israel to A

Feb 2008Fitch upgrade

Israel to A

Feb 2008Fitch upgrade

Israel to A

April 2008Moody’s upgrade

Israel to A1

April 2008Moody’s upgrade

Israel to A1

All Three Credit Rating Agencies Re-affirmed

Israel’s Rating/Outlook in 2009

All Three Credit Rating Agencies Re-affirmed

Israel’s Rating/Outlook in 2009

End

Strengths: Indicators

Five years of high growth, rapid recovery from the crisis

3.3%

9.2%

0.0%

-0.7%

1.5%

3.3%3.6%

4.8%

0.7%

4.0%

-2.0%-2.7%

1.2%

5.0%

5.3%5.2%5.1%

-3%

-1%

1%

3%

5%

7%

9%

11%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2008 Q

4

2009 Q

1

2009 Q

2

2009 Q

3

2009 Q

4

2010 Q

1

Recovery Starting in Q2 2009

1999-2010, annual rates of change

-1.3%

-3.5%-4.3%

-4.9%

-3.0%

-0.9%-1.3%

-0.8%-1.0%-0.8%

3.7%

-5.0%

-2.1%

0.3%0.5% 1.2%

2.3%

3.1%

0.7%

2.9%

5.1%

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Confidence in the markets – a surplus in the current account of the balance of

payments

Percent of GDP (right axis)

In USD millions and in percent of GDP

Falling rates of debt

78.079.977.2

99.0

84.4

100.8

119.2

136.2

145.1

158.2

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010F

Source: CBS; Economics and Research Division, MOF

Reduction of Public Debt as a Percentage of GDP

40%

50%

60%

70%

80%

90%

100%

110%

2003 2005 2007 2009 2011 2013 2015

ʤʩʁʬʥʮʩɦ ʬʲ ʥɹʡ ʨʫʩyʨɦ ʠʮ̋ ʰʮʠ

Assuming growth rates of 4% in 2011-2013 and 3.5% from 2014 forward.

67.8%

Test point

Trajectory for Reduction of Debt-to-GDP Ratio, 2003-2020

Responsible, balanced fiscal horizon

Simulation Actual

Maastricht Treaty

Gradual reduction of level of public expenditure

59.0

56.355.4

52.0

47.2

50.3

42.942.9

42.4

30

35

40

45

50

55

60

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010F

Source: CBS; Economics and Research Division, MOF

Reduction of Public Expenditure as a Percentage of GDP

35%

40%

45%

50%

55%

2003 2005 2007 2009 2011 2013 2015

סימולציה בפועל

Assuming growth of 4% in 2011-2013 and 3.5% from 2014 forward.

Responsible, balanced fiscal horizon

Trajectory for Reduction of Public Expenditure, 2003-2020

Simulation Actual

4.8%

3.3%

5.6%

-7.4%

0.7%

-2.0% -2.7%

1.2%

3.6%

-6.4%-5.4%

-2.7%

-0.7%

2.2%3.2%

-1.6%

-9.6%

-0.4%

1.6% 1.2%0.4%

-10%

-6%

-2%

2%

6%

2008-Q3 2008-Q4 2009-Q1 2009-Q2 2009-Q3 2009-Q4 2010-Q1

Israel

US

Eurozone

The economic crisis: Late, moderate damage; early

recovery

Quarterly growth, annualized rate

Growth of Gross Domestic Product, in Israel and Globally

Expenditure for Civilian R&D, 2007* (in percent of GDP)4.8

3.6 3.5 3.5 3.4

2.92.7 2.7 2.6 2.6 2.5

2.32.1 2.0 1.9 1.9 1.8 1.7 1.6 1.6 1.5

1.3 1.3 1.2 1.2 1.11.0

0.7 0.6 0.6 0.5

0

1

2

3

4

5

6

Isra

el

Swed

en

Finla

nd

Korea

Japan

Switz

erland

Icel

and

US

Austria

Denm

ark

Ger

man

y

Weig

hted a

vera

ge

France

Austra

lia

Canada

Belgiu

m

UK

Netherla

nds

Norway

Luxembourg

Czech

Rep

ublic

Irela

nd

Spain

New Z

ealan

d

Portugal

Italy

Hungary

Turkey

Gre

ece

Poland

Slovak

ia

* 2007 or latest year for which data are available.

High rates of expenditure on civilian R&D

Rate of Contribution of Technology Sector to Exports,

2001-2009

0.36

0.330.30

0.320.31

0.340.33 0.32

0.41

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2001 2002 2003 2004 2005 2006 2007 2008 2009

0

5

10

15

20

25

30

35

Norway

United

Stat

es

Nether

lands

Israe

l

Icelan

d

Canad

a

New Z

ealan

d

Denmar

k

Korea

Austra

lia

Japa

n

Sweden

United

King

dom

Estonia

Russia

n Fed

erati

on

Irelan

d

Finlan

d

Switzer

land

Spain

OECD ave

rage

Poland

Luxe

mbour

g

Hunga

ry

Franc

e

Germ

any

Greec

e

Mex

ico

Belgium

Portu

gal

Czech

Rep

ublic

Italy

Slovak

Rep

ublic

Sloven

ia

Turke

y

Austria

Chile

Brazil

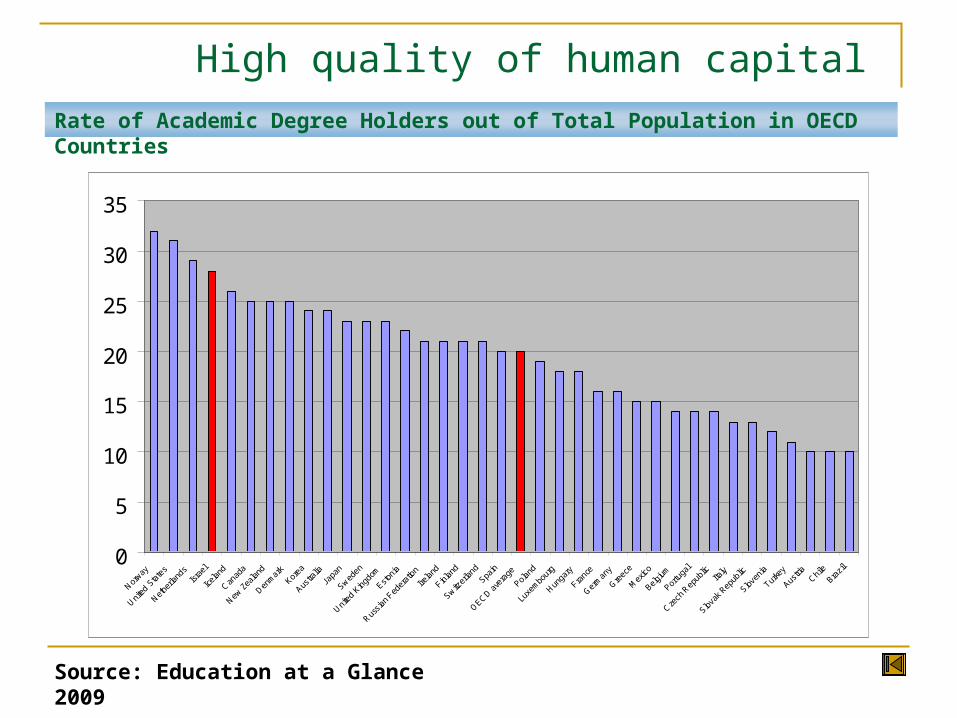

Source: Education at a Glance 2009

High quality of human capital Rate of Academic Degree Holders out of Total Population in OECD Countries

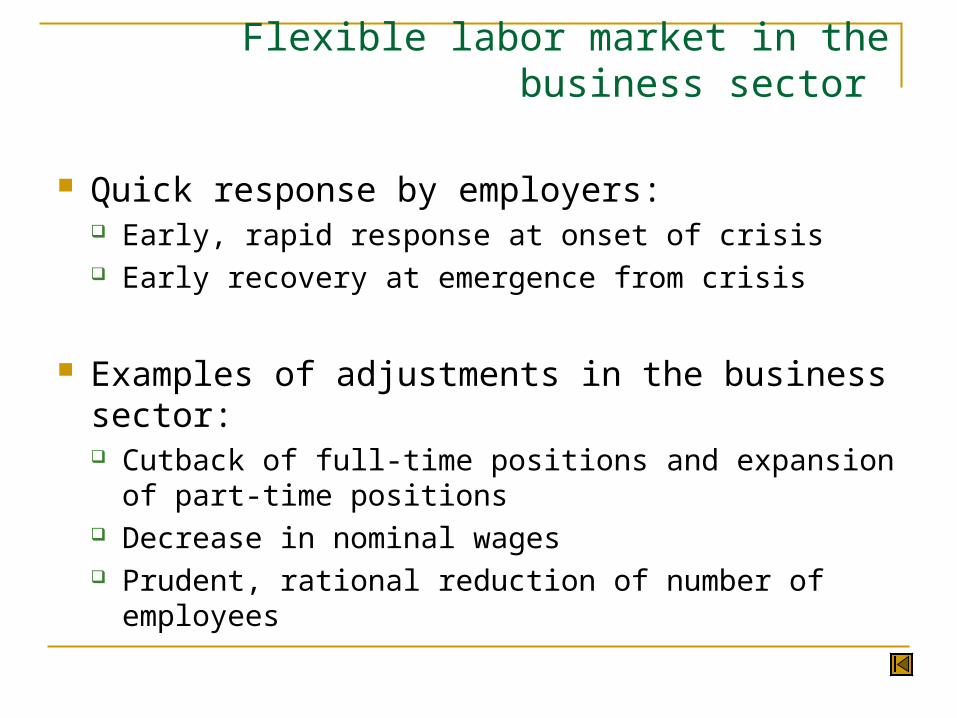

Flexible labor market in the business sector

Quick response by employers: Early, rapid response at onset of crisis Early recovery at emergence from crisis

Examples of adjustments in the business sector: Cutback of full-time positions and expansion of part-

time positions Decrease in nominal wages Prudent, rational reduction of number of employees

Signs of Erosion and Threats:

Indicators

Low achievement at all levels, including excellent

Pisa 2006

Signs of Erosion and Threats

Level 6

Level 5

Level 4

Level 3

Level 2

Level 1

Below Level 6

Israel OECD average

Aging of academic staff, moving away from optimal academic productivity age

Average age of senior academic

staff in Israel, 2010

Source: B. Jones, “Age and great Invention”, Review of Economics and Statistics, January 2010

Signs of Erosion and Threats

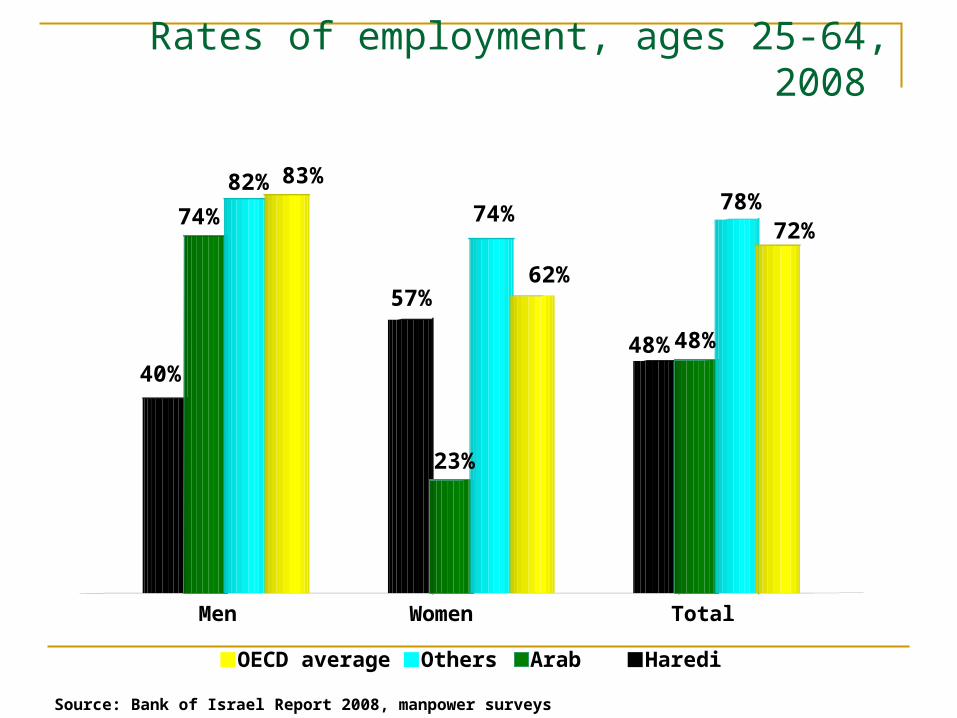

Rates of employment, ages 25-64, 2008

Source: Bank of Israel Report 2008, manpower surveys

83%82%

74%

40%

62%

74%

23%

57%

72%78%

48%48%

TotalWomenMen

OECD average Others Arab Haredi

Gender differences in wages Average Wages, in NIS per Employee Position,

2007

Source: Karnit Flug, “The Israeli Labor Market: An International Comparison,” Sept. 2009. Calculations based on CBS data.

4 , 279 ) 72(%

4 , 351 ) 73(%

6, 154 ) 103(% 5,957

6 , 582 ) 71(%

5 , 759 ) 62(%

10,085) 108(%

9,263

₪0

₪2,000

₪4,000

₪6,000

₪8,000

₪10,000

₪12,000

Women MenHaredi Arab Non-Haredi Jews Average wages

Source: CBS Statistical Almanac, 2009. Calculations by Taub Center.

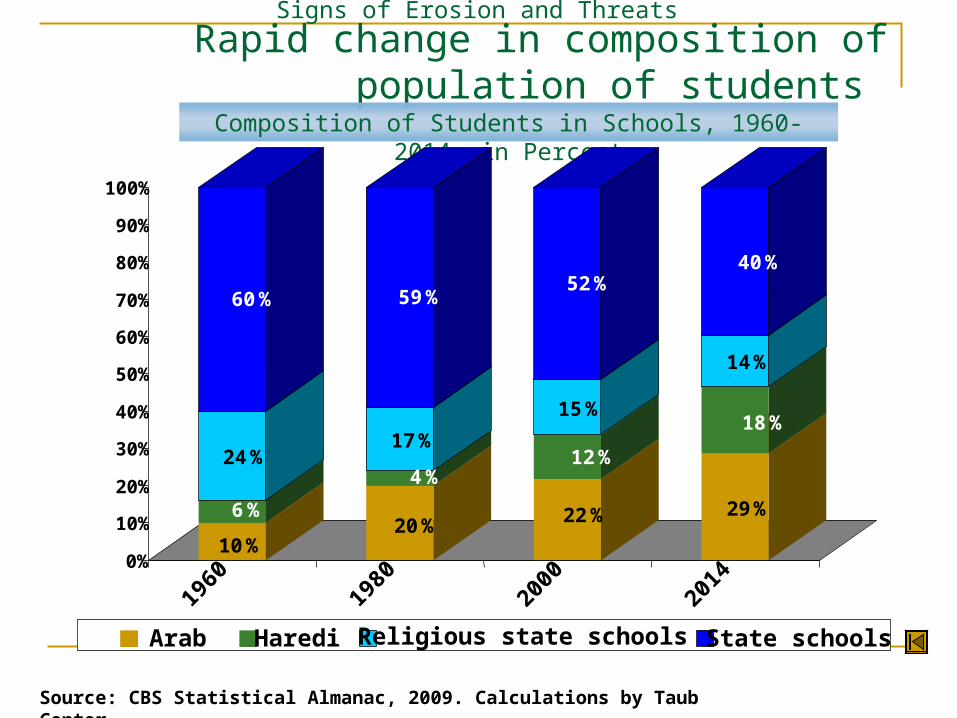

Rapid change in composition of population of students

Composition of Students in Schools, 1960-2014, in Percent

Signs of Erosion and Threats

10%

6%

24%

60%

20%

4%

17%

59%

22%

12%

15%

52%

29%

18%

14%

40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1960

1980

2000

2014

Arab Haredi Religious state schools State schools

Gap between supply and demand in the housing market

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

התחלות בנייה

גידול משקי הבית

Source: CBS

Cumulative gap over one decade: 116,000 housing units, ~10,000 units per year

Signs of Erosion and Threats

Construction startsIncrease in households

תקציב מקורי

49,033

38,708

35,000

37,000

39,000

41,000

43,000

45,000

47,000

49,000

51,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

תקציב מקורי

Original budget

26.6% growth within a decade!

Development of IDF/Defense Ministry Budget

NIS millions, 2010 budget prices (net budget)

Heavy burden of defense budget

Original budget

Changes in Net Defense Budget for 2006-2009 (2010 prices)

39.9 40.643.4

47.81.9

2.4

1.8

2.0 3.72.5

2.0

4.1

35.0

40.0

45.0

50.0

55.0

2006 2007 2008 2009

תקציב מקורי שינויים במהלך השנה הוצאות לחימה

46.048.

346.2

51.6

Original budget Changes during the year

Combat expenses

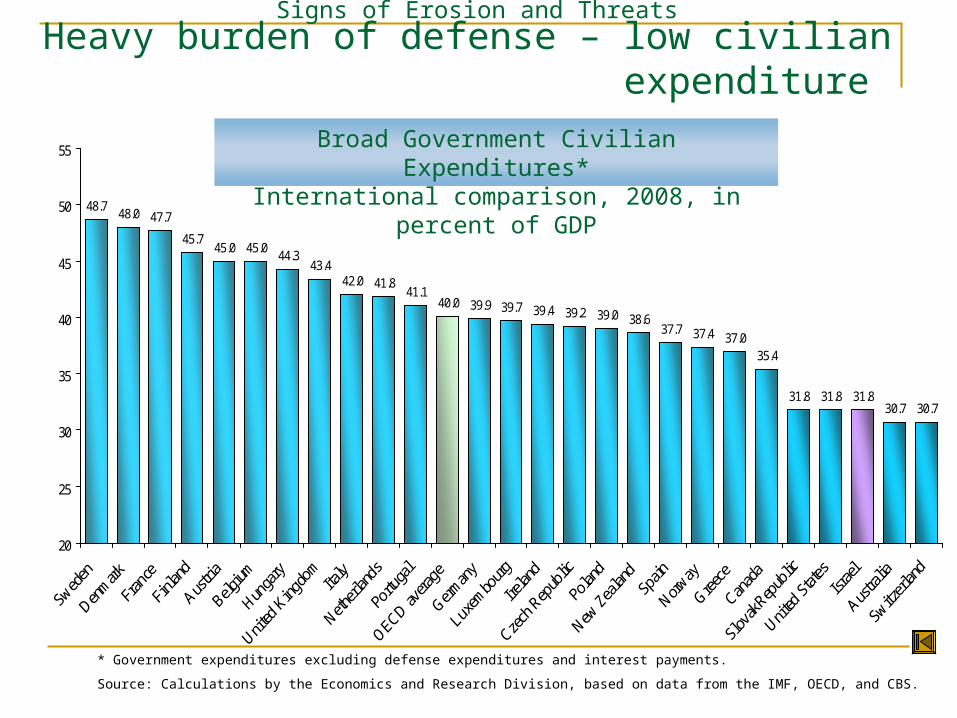

48.748.0 47.7

45.745.0 45.0

44.343.4

42.0 41.841.1

40.0 39.9 39.7 39.4 39.2 39.0 38.637.7 37.4 37.0

35.4

31.8 31.8 31.830.7 30.7

20

25

30

35

40

45

50

55

* Government expenditures excluding defense expenditures and interest payments.

Source: Calculations by the Economics and Research Division, based on data from the IMF, OECD, and CBS.

Heavy burden of defense – low civilian expenditure

Broad Government Civilian Expenditures*International comparison, 2008, in percent of GDP

Signs of Erosion and Threats

94.2%

89.3%

86.3%

78.8%

91.7%

88.2%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

שיעור תעסוקה פריון למבוגר 20+ שכר למועסק

Source: Dr. Michael Sarel, Israel Economic Association conference, May 2010.

In the “business as usual” scenario – a negative demographic effect at an annual rate

of 0.45% (per-capita GDP)Men: Effect of Demographic Composition for Ages 20+

Analysis of the “business as usual” trend with regard to the adoption of employment and wage patterns in the non-Haredi Jewish population .

One Economy, Two Stories

Employment rate

Productivity for adults (20+)

Wages per employee