the israeli economy: still withstanding adverse global economic shocks december 2012

TRANSCRIPT

The Israeli Economy:Still withstanding adverse global economic

shocks

December 2012

The Israeli economy has experienced a drop in the GDP growth rate from over 5% to about 3%

Starting from mid-2013, natural gas will have a positive impact on Israel’s growth rate

4

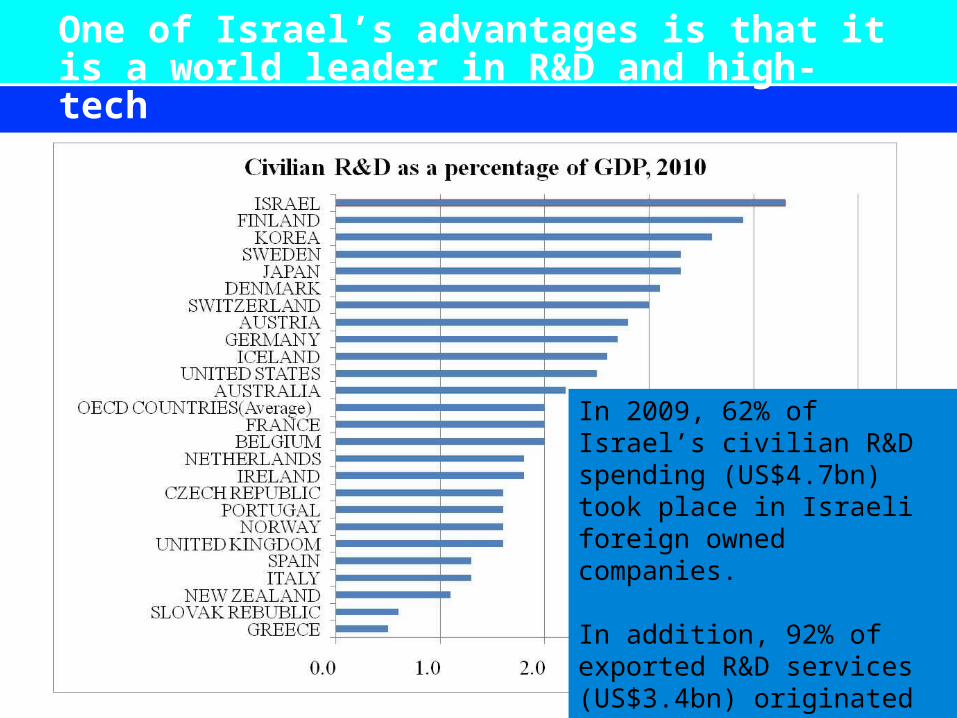

One of Israel’s advantages is that it is a world leader in R&D and high-tech

In 2009, 62% of Israel’s civilian R&D spending (US$4.7bn) took place in Israeli foreign owned companies.

In addition, 92% of exported R&D services (US$3.4bn) originated from these companies.

5

In “good periods”, Israel’s high-tech electronic goods exports tend to surge upwards more substantially than high-tech activity in the US

6

Exports of high-tech services have grown substantially and are now equivalent in volume to the export of high-tech goods

7

A balanced current account. There is no net foreign debt and there is a high level of FX reserves

8

FDI inflows have seen a rebound, but foreign party’s portfolio outflows have increased

9

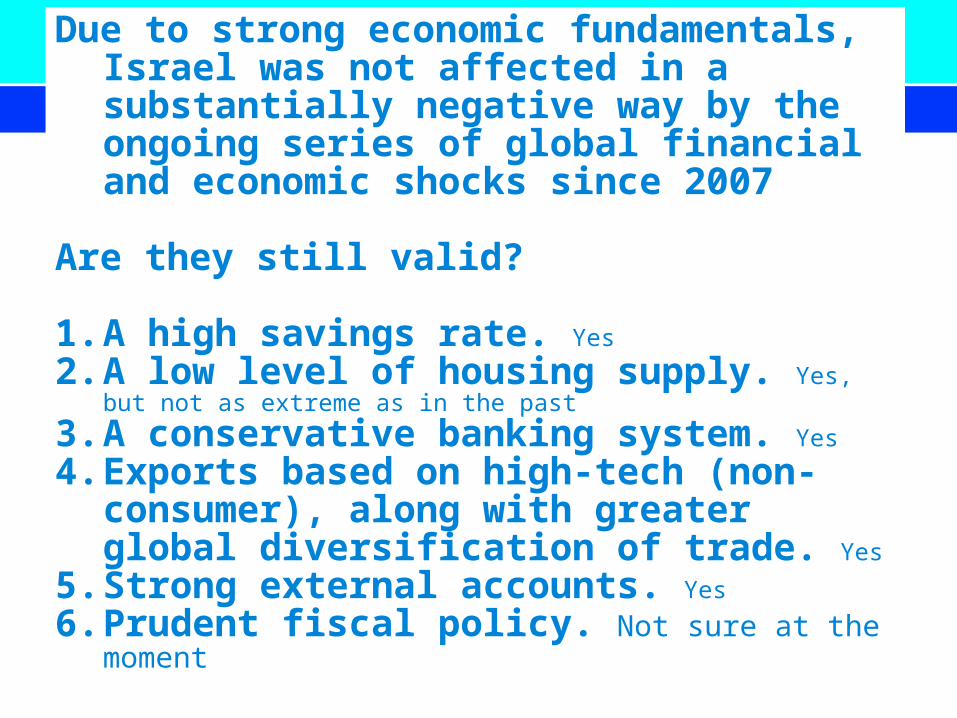

Due to strong economic fundamentals, Israel was not affected in a substantially negative way by the ongoing series of global financial and economic shocks since 2007

Are they still valid?

1. A high savings rate. Yes

2. A low level of housing supply. Yes, but not as extreme as in the past

3. A conservative banking system. Yes

4. Exports based on high-tech (non-consumer), along with greater global diversification of trade. Yes

5. Strong external accounts. Yes

6. Prudent fiscal policy. Not sure at the moment

10

The resilience of Israel’s private sector is related to a high savings rate

Household

11

The labor force participation rate is low; this has an impact on the Israel’s growth potential and on the dependency ratio

12

Israel’s unemployment rate is low; slow GDP growth is likely to result in an increase of unemployment in 2013

13

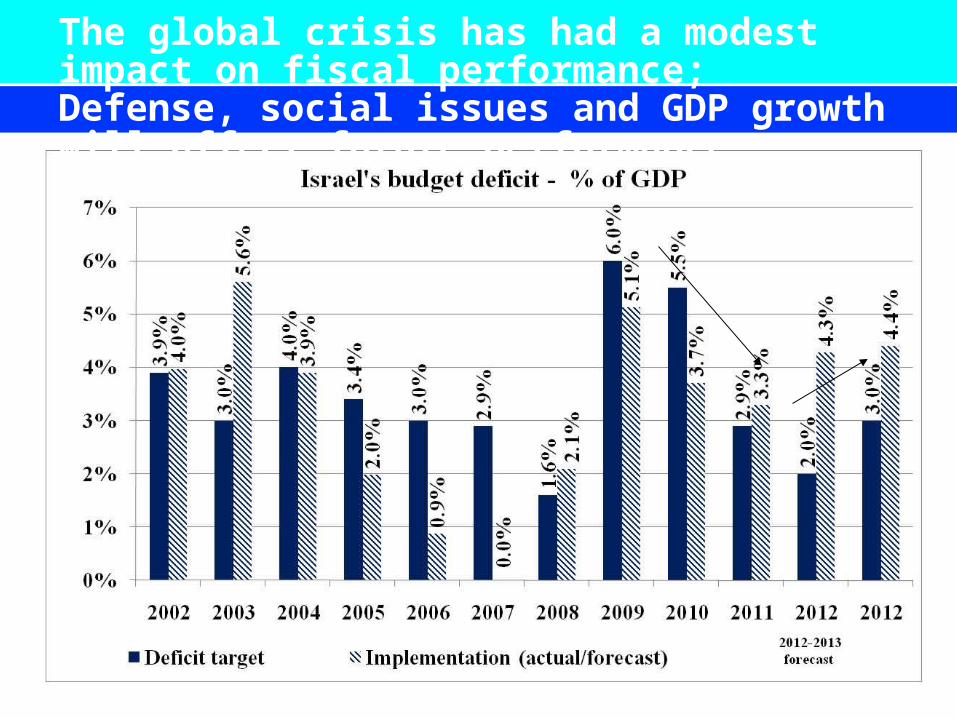

The global crisis has had a modest impact on fiscal performance; Defense, social issues and GDP growth will affect future performance

14

An undesired change in the debt/GDP trend

15

The BoI adopted a flexible approach towards inflation targeting

16

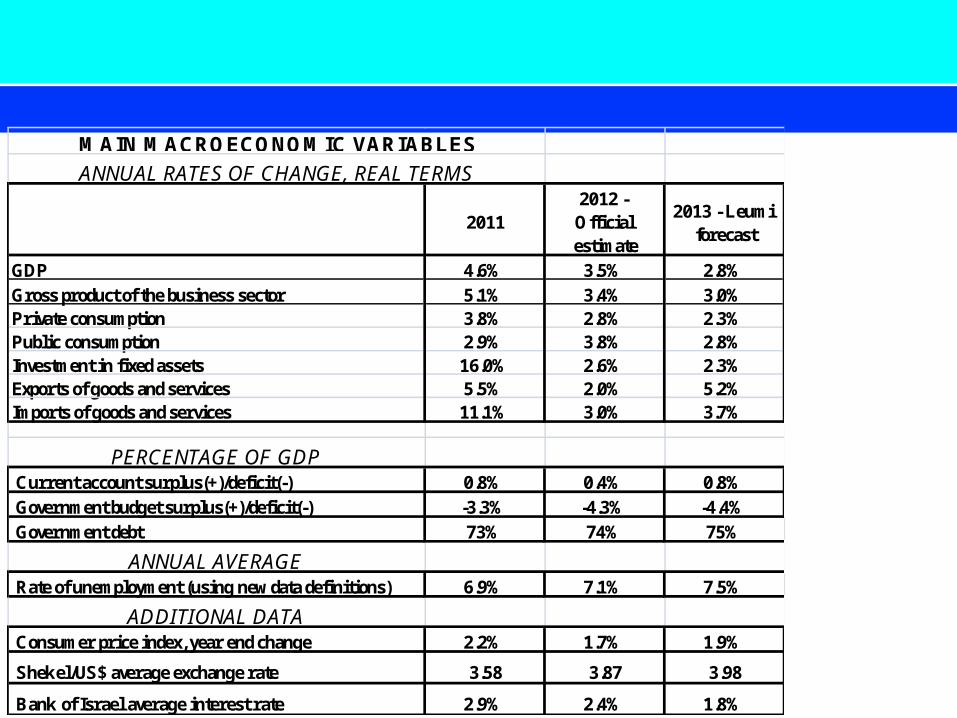

20112012 - Official estimate

2013 - Leumi forecast

GDP 4.6% 3.5% 2.8%Gross product of the business sector 5.1% 3.4% 3.0%Private consumption 3.8% 2.8% 2.3%Public consumption 2.9% 3.8% 2.8%Investment in fixed assets 16.0% 2.6% 2.3%Exports of goods and services 5.5% 2.0% 5.2%Imports of goods and services 11.1% 3.0% 3.7%

PERCENTAGE OF GDPCurrent account surplus(+)/deficit(-) 0.8% 0.4% 0.8%Government budget surplus(+)/deficit(-) -3.3% -4.3% -4.4%Government debt 73% 74% 75%

ANNUAL AVERAGERate of unemployment (using new data definitions) 6.9% 7.1% 7.5%

ADDITIONAL DATAConsumer price index, year end change 2.2% 1.7% 1.9%

Shekel/US$ average exchange rate 3.58 3.87 3.98

Bank of Israel average interest rate 2.9% 2.4% 1.8%

MAIN MACROECONOMIC VARIABLES

ANNUAL RATES OF CHANGE, REAL TERMS

Residential construction has come out of a cyclical low, recovered quickly, and contributed to growth in 2010-2011

Immigration wave

18

Housing prices peaked; Are the current market dynamics sufficient in order to sustain a gradual decline of prices?

19

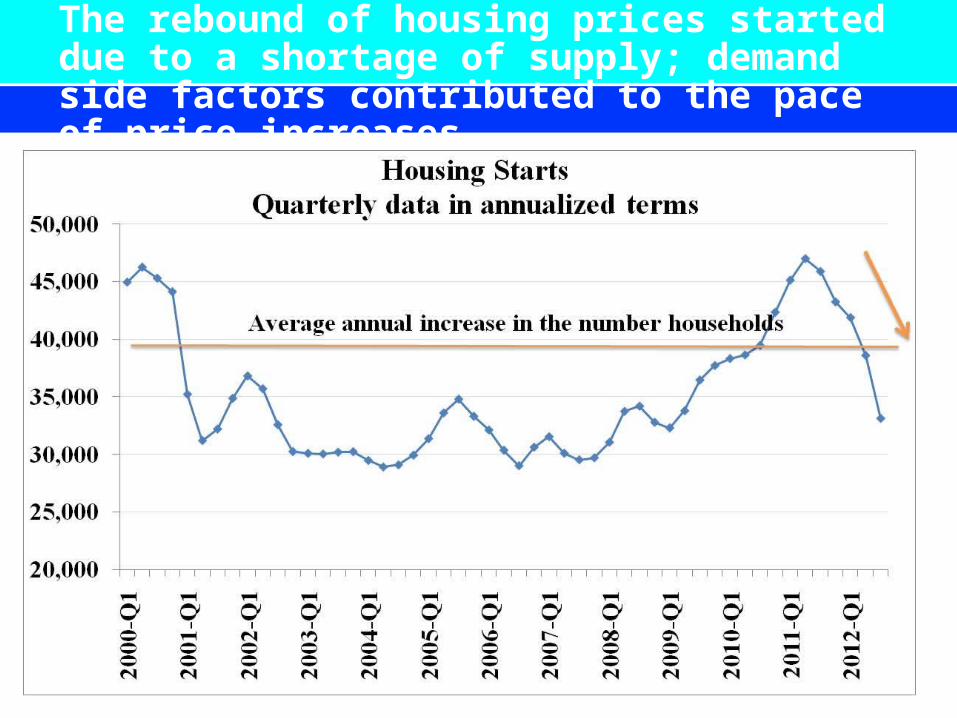

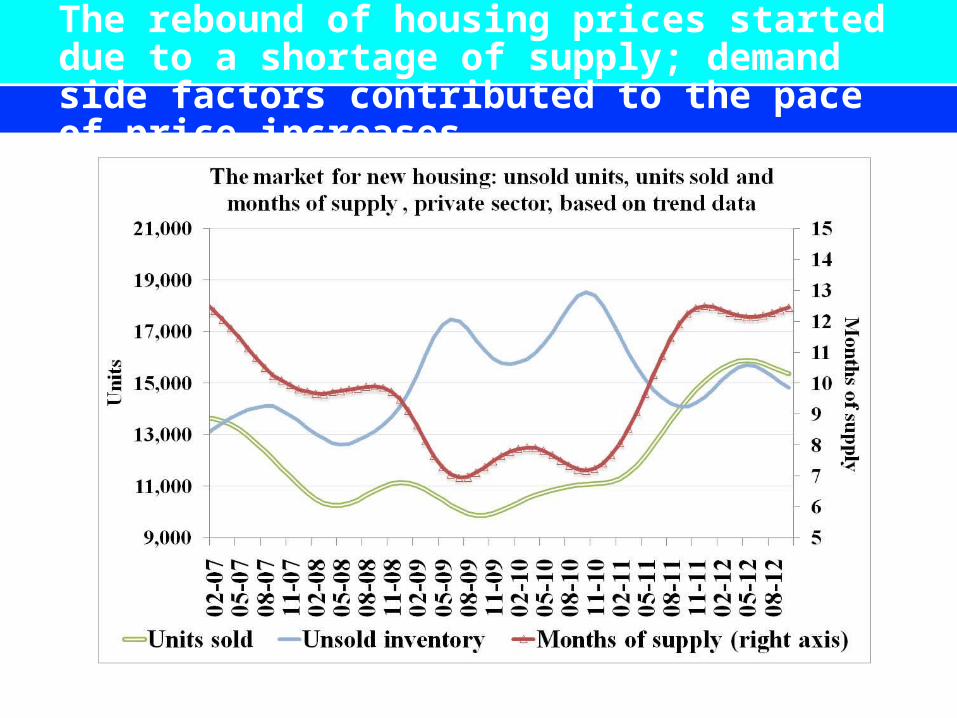

The rebound of housing prices started due to a shortage of supply; demand side factors contributed to the pace of price increases

20

The rebound of housing prices started due to a shortage of supply; demand side factors contributed to the pace of price increases

21

Despite a substantial increase in Israeli mortgage credit during 2007-2011, household leverage is still comparatively modest

22

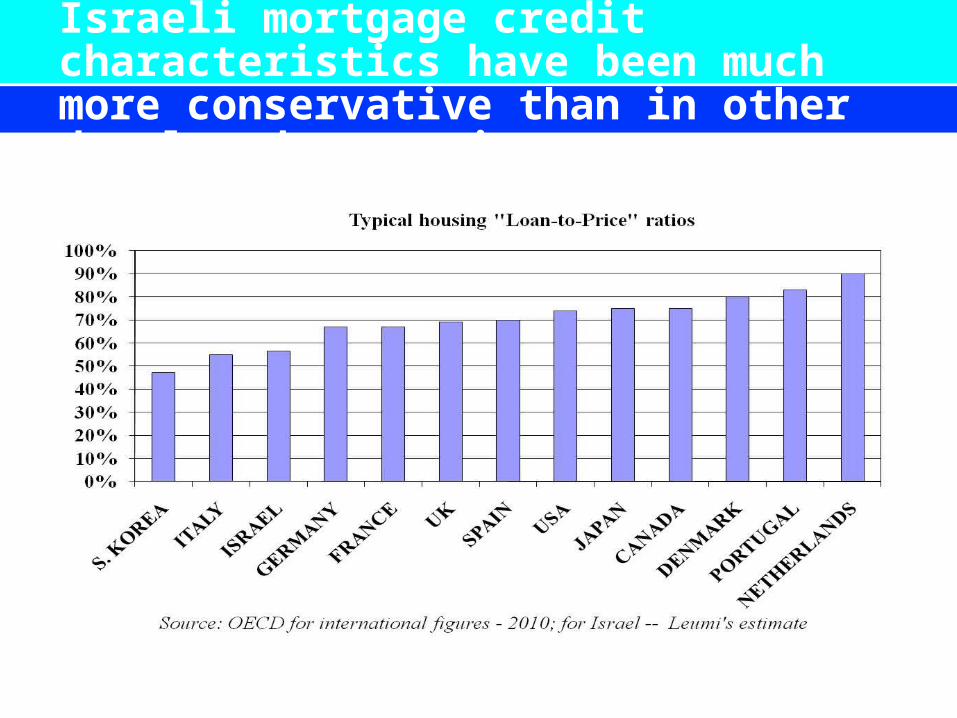

Israeli mortgage credit characteristics have been much more conservative than in other developed economies

23

Risks to the forecasts

•A Western world led global recession with renewed volatility in global financial markets.

•Changes in the regional geopolitical outlook.

•A prolonged deterioration of the security situation.

•A regulatory and risk aversion led credit crunch in Israel

24

The Israeli Economy:Still withstanding adverse global economic

shocks

December 2012