the journal of medical real estate

DESCRIPTION

Presented by Capital Markets Access Company & Swap NegotiatorsTRANSCRIPT

CAPITAL MARKETS ACCESS COMPANY ▶ 399 CAROLINA AvENuE, SuITE 250, WINTER PARK, FL 32789 ▶ OFFICE 407.264.7251 ▶ FAx 407.895.6001 ▶ CMACCAPITAL.COM

Volume III, Number IPresented By Capital Markets Access Company & Swap Negotiators

Are Your Retiring Partners Stealing Your Equity?They May Be If Your Swap Is Underwater

A North Georgia real estate LLC consisting of ten equal partners re-cently bought out three of the partners. Under the terms of the operat-ing agreement, the prop-

erty was appraised and the partners were paid their respective portions based on the equity available. The appraised value was $10,000,000 and the remaining debt was $7,000,000, leaving $3,000,000 of equity. Each partner received $300,000 (10% of the equity).

Sounds fair, right? Far from it. In this case, the outgoing partners received twice the amount that they would have real-ized had the building been sold and the equity distributed. This occurred because the calculation of equity failed to consider the worth of the interest rate swap at the time of valuation. In this example, the

interest rate swap had a mark-to-market (MtM) value of negative $1,500,000. If the partners had sold the building for the ap-praised value of $10,000,000, they would have had to repay the remaining debt of $7,000,000 and the termination of the swap of $1,500,000. Each partner would receive $150,000 from the sale as their portion of the equity…not $300,000.

Not only did they overpay the retir-ing partners a total of $450,000, but each remaining partner was left with only $85,714 in equity as opposed to $150,000. If the buyouts had been calculated with the all-in value considered, each remain-ing partner would have retained his true equity of $150,000. This pitfall can easily be avoided by obtaining an MtM value from a reputable third party such as Swap Negotiators. In this case, it’s a reversal of the old adage which should now read, “Let the sellers beware.”

By Shannon Stocker, M.D.

▶ Hidden Swap Charges Reach All-Time High Borrowers Paying As Much As 5% Of Loan Amount In Added Fees

ON THE INSIDE

▶ Maximizing Your Appraised value Advice From A Medical Building Appraiser

▶ ThreeTipstoRefinancingWhenYour Real Estate is upside Down Many Deals Being Done At 100%+ LTV

▶ Seven Quotes That Tell You All You Need to Know About Interest Rate Swaps

▶ Perfect Payers Penalized as Banks Review Loan Portfolios Beware The Technical Default

▶ Borrower Saves $75,000 in Hidden Swap Fees Last Minute Transparency Creates Reductions

▶ Bank Faces Allegations of Swap Overcharge Swap Negotiator’s Audit Uncovers Discrepancy

▶ Catch Me If You Can The Day Count Convention Maneuver

▶ Banks Holding Back Best Rates 3.95% Like Putting Lipstick On A Pig

▶OneDoctor’sJourneytoHellandBack

▶ Determined Ortho Executive Finds Lowest Rate Third Time's A Charm

Often times we are asked why, if there is an agreement on the spread, is it necessary to have a swap negotiator on the phone at the time of an interest rate swap trade. The answer is because the market never stops moving and, even if you have confirmed a rate going into a call, that rate can change dramatically by the time of execution.

You need only consider this excerpt from the recording of a recent interest swap execution. The swap was for an amount of $10,250,000 and the dollar value of each basis point was $10,502. On the call was the bank’s swap desk, the borrower and Swap

Negotiators.▶ We Pick Up The Call At 1:31:03…1:31:03—Bank: My trader is seeing 181.5 basis points. 1:31:08—Swap Negotiators: We are seeing the same level.1:31:11—Bank: Mr. Smith would you like to lock at 181.5?1:31:14.4—Swap Negotiators (interrupting): Let’s let the trader refresh his screen, we’re seeing movement.1:31:25—Bank: My trader is now seeing 179.0.

1:31:29—Swap Negotiators: We agree.1:31:33—Bank Mr. Smith would you like to lock at 179?1:31:36—Borrower: Chris?1:31:41—Swap Negotiators: Looks good.1:31:46—Borrower: Go ahead a lock at 179.0.▶ This Is Not An Anomaly. Markets Never Stop Moving. Hedge With Your Eyes Wide Open!

All was set to go on a $16,000,000 MOB to house four ophthalmology specialty practices in Colorado Springs. Gallacher Development, headed by Kelly and Kev-in Gallacher, had done a thorough job of negotiating the most favorable financing package possible among the banks in and

around the area. Then, just before signing the bank’s commitment letter, Gallacher learned of a similar deal that had closed in another area at even better terms.

Gallacher confirmed that CMAC had closed several deals that were substantial-ly more favorable than the market. In a

bold move, Gallacher recommended that the borrower hold off signing the com-mitment letter to allow CMAC an oppor-tunity to negotiate with the chosen lender.

CMAC found that the bank had pro-vided a rate and terms that were as good as had been seen in the Colorado Springs market, but not as good as what CMAC had achieved with this same bank in re-cent deals in other states. Once CMAC brought this additional information to the local bank, that banker was able to replicate the non-regional terms. The savings in interest and fees? More than $1,300,000.

“This is exactly why we chose this devel-oper,” said Dr. Dean Carlson of Ophthal-mology Associates. “They aren’t afraid to say that there might be someone out there with better tools. That’s what makes them exceptional developers.”

Construction is due to be completed in February of 2013.

Eleventh Hour Renegotiation Pays Big Dividends

Borrower Makes $26,255 in 3.4 SecondsA Great Lesson In Swap Market Movement

Developer Leverages $1,300,000 Rate Savings

▶ AND MuCH MORE!

PAGE 2 THeJOuRnalOfMeDicalRealesTaTe

Maximizing Your Appraised ValueAdvice From A Medical Building Appraiser

A building is not a building is not a building. And a medical building is far dif-ferent from all others. Too often, the owner of an MOB will be taken by surprise when an appraisal reports a market value that is substantially below what that owner paid for the building or what its income would support.

CMAC sat down with MAI Commercial Appraiser Loren Pipkin who specializes in medical properties to discuss this prob-lem. Loren gave us three points that she feels can create a big difference in making sure that you, as an owner, optimize the appraised market value.▶ Provide A Written Description Of The Building

Your description should include not only the building itself, but also focus on tenant improvements which can easily be overlooked in the appraisal process.

In unique medical buildings, there are often expensive building improvements that are not immediately apparent or hid-den from sight. Examples include: backup generators, dedicated HVAC for special-ized equipment, additional floor reinforce-ment, metal lining in walls for radiology areas, and alarm and monitoring systems for refrigerated storage.

Making sure your appraiser has a full list of building features is likely to benefit your value during the appraisal process. Keep in mind that this should include building features only and should exclude personal property.▶ Supply Historic Or Proposed Construction

Maintain historic building costs and provide them to the appraiser even if they are dated. If you have a new building, make sure the costs are provided in enough de-tail that the appraiser can see the fin-ish costs separate from the core and shell costs. Be sure to add to those finish costs features unique to your medical practice (like those noted above) that would not be typically found in standard office space. Take the time to have your construction company provide a separate breakout of core and shell versus finish costs for your records.

The same holds true if you have re-modeled an existing building and have costs beyond replacing carpet and paint. Provide your retrofit or new construction costs even if they are several years old. Don’t presume that the appraiser can ac-curately estimate your costs for construc-tion or renovation.

▶ Insist On An Appraiser With Experience In Medical Buildings Of Comparable Complexity

A bank will independently select the ap-praiser assigned to value your property, but you can and should insist that the bank se-lect an appraiser who can demonstrate that they have experience in valuing buildings of comparable complexity to your proper-ty. For a complex medical property, there are many features that the vast majority of experienced appraisers never encounter. Understanding the value of those unique medical features is an important sub-spe-cialization, not unlike medical practice.

Obviously, there are no guarantees. But some careful preparation will give you the best opportunity to have the outcome you are seeking.

Loren Pipkin is a Vice President with National Valuation Consultants, Inc., the largest private-ly held appraisal and consultant group in the United States. Pipkin has

a master's degree in Real Estate and Con-struction Management from Denver Uni-versity and has developed a specialization in medical office appraisal.

Interview With Loren Pipkin

Hidden Swap Charges Reach All-Time HighBorrowers Paying As Much As 5% Of Loan Amount In Added Fees

Based on a sampling of swap confirmations ex-ecuted during the last quarter of 2011, Swap Negotiators has report-ed a continuing trend in the widening of swap

spreads from all banks. It is now not unusual to find that banks

are imbedding up to 5% in undisclosed hidden fees into interest rate swaps where they are undetected by borrowers. This is particularly fertile ground for the bank to reap profits because the historically low swap rates give the banks the ability to add on basis points and still give the impres-sion of highly attractive rates.

Without the representation of a swap negotiator, the borrowers cannot see the true costs and the rates posted in The Wall Street Journal don’t apply to their own swaps because they are based upon several different factors. They are, in fact, sub-stantially higher than the swap applied to a monthly payment and based on 30-day

Libor. ▶ Here Is A Typical Example Of How The Banks Imbed These Profits…

A $10,000,000 borrower whose current floating rate is 30-day Libor plus 250 de-cides that he wants to hedge his interest rate risk and the bank offers a 10-year in-terest rate swap. When the borrower asks what that rate would be, the bank responds by telling him that they can fix at 4.98% (swap of 2.48% plus 2.50% loan spread). The bank tells the borrower that there will be no fees. The borrower agrees to the rate and assumes that his swap rate is whatev-er the cost of the swap was plus his loan spread of 2.50%. He is wrong and just end-ed up paying the bank the equivalent of an additional 5.01% in origination fees—more than a half million dollars! See Anatomy of a Price-Up box below.

Now, many informed borrowers are cre-ating transparency and negotiating their spreads by reaching out to swap negotiators who have the expertise to negotiate swap spreads and ensure the swaps are executed

By Greg Warren

How A Bank Hides $500,000 Of Undisclosed Fees

1. The borrower requests a swap to cover $10,000,000 for a 10-year term on an amortizing loan.2. The bank trades the swap at a cost of 1.92%.3. The bank quotes the borrower a price of 2.48%.4. The spread (0.56% in this example) is not disclosed to the borrower who assumes the bank passed on the swap without any additional fees and is making its money on the loan spread.5. Each 0.01% has a value of roughly $8,950. 6. Following GAAP, the bank recognizes an immediate profit on the transaction of $501,200.7. The borrower has just obligated himself to pay the equivalent of an added origination fee of 5.01%.

“You can clearly see that it's all pretty standard stuff.”

in accordance with the agreed pricing. While banks are due a fee when booking

a swap to cover the element of risk, the bor-rower should be represented so that he may

competently negotiate a reasonable price and then have access to live market data assuring that the contract is concluded in accordance with the negotiation.

SOME OF OuR CLIENTS INCLuDE

Florida Heart Group Orlando, FL ▶ Orlando Heart Group Orlando, FL ▶ Bay Eyes Surgery Center Fairhope, AL ▶ Tallahassee Orthopaedic Clinic Tallahassee, FL ▶ Alabama Psychiatric Birmingham, AL ▶ Eye Associates Boca Raton, FL ▶ Wise Pembroke MOB Pembroke, MD ▶ Gastro Associates Baton Rouge, LA ▶ vero Radiology vero Beach, FL ▶ The Outpatient Center Delray Beach, FL ▶ North Carolina Eye Ear Nose and Throat Raleigh, NC ▶ Eye Center of North Florida Panama City, FL ▶ Alabama Gastro Birmingham, AL ▶ Eye Institute of West Florida Largo, FL ▶ South West Neurological Associates Ft. Myers, FL ▶ Cullman ASC Cullman, AL ▶ Huntsville Laser Center Huntsville, AL ▶ Foot and Ankle Clinic Ft. Myers, FL ▶ Kagan Surgical Suites Cape Coral, FL ▶ Kingsford and Rock Maitland, FL ▶ Cardiovascular and Interventional Consultants Clearwater, FL ▶ Triangle Orthopaedic Associates Raleigh, NC ▶ visual Health Lake Worth, FL ▶ Diaz Foods Atlanta, GA ▶ Orthopaedic Care Specialists Palm Beach, FL ▶ Charleston Radiology Charleston, SC ▶ Piedmont Health Group Greenwood, SC ▶ Ocala Endoscopy Ocala, FL ▶ Calvert Orthopaedic and Sports Medicine Prince Frederick, MD ▶ Pinnacle Financial Orlando, FL ▶ Laser Center of Palm Beach Palm Beach, FL ▶ Wake International Medicine North Raleigh, NC ▶ Athens Orthopedic Clinic Athens, GA ▶ Long Island Radiation Center Massapequa, NY ▶ Nicolitz Eye Center Jacksonville, fl ▶ Savannah Cardiology Savannah, GA ▶ Florida Imaging Acropolis Orlando, FL ▶ Orthopedic Center of Florida Ft. Myers, FL ▶ Cardiac Disease Specialists Atlanta, GA ▶ Interventional Cardiology Gainesville, FL ▶ Northeast Georgia Heart Gainesville, GA ▶ Bayside Orthopedics Fairhope, AL ▶ Central Park ENT and Associates Arlington, Tx ▶ Alabama Orthopedics Mobile, AL ▶ Massey Services Orlando, FL ▶ Commerce Parkway Wooster, OH ▶ Peace River Distributing Punta Gorda, FL ▶ Hilton Head Surgical Hilton Head, SC ▶ Bushwood Land Development Ft. Myers, FL ▶ North Carolina Surgical Hospital Durham, NC ▶ Ocala Eye Ocala, FL ▶ Same Day Surgery Center Zephyrhills, FL ▶ South West Florida Oral Surgery Ft. Myers, FL ▶ Athletic Orthopedic Reconstruction Center Ft. Myers, FL ▶ Southeastern urological Center Tallahassee, FL ▶ Carteret Surgical Associates Morehead City, NC ▶ Hughes & Coleman Law Bowling Green, KY ▶ Abilene Cardiology Abilene, Tx ▶ Ortho Tennessee Knoxville, TN ▶ Hillcroft Medical Houston, Tx ▶ Palmetto Surgery Center Columbia, SC ▶Kagan,JuganandassociatesFt. Myers, FL ▶ Southern Cardiovascular Gadsden, AL ▶ Clearwater Orthopaedic Clearwater, FL ▶ BoneandJointGroupClarksville, TN ▶ And More!

PAGE 3THeJOuRnalOfMeDicalRealesTaTe

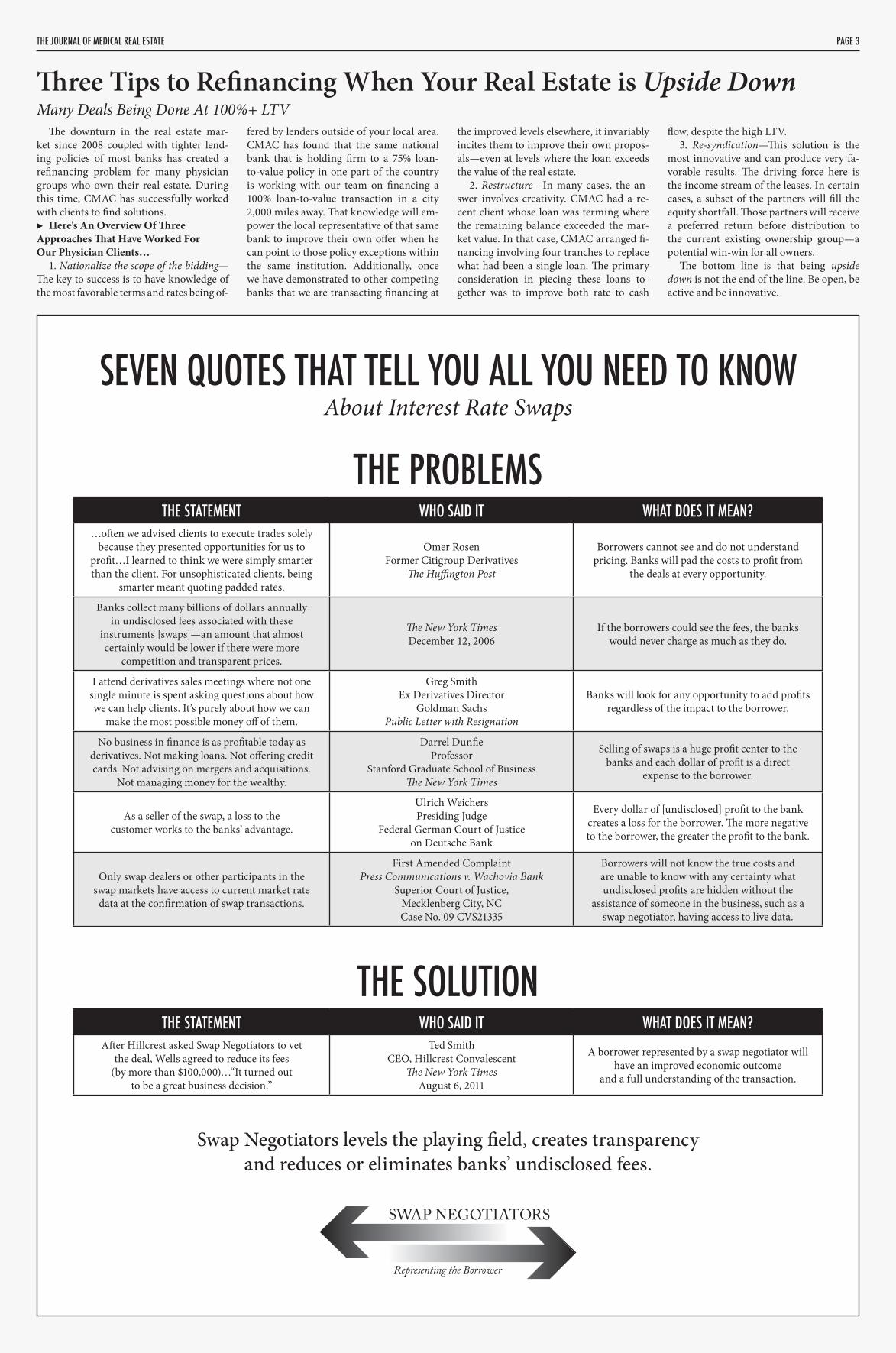

SEvEN QuOTES THAT TELL YOu ALL YOu NEED TO KNOWAbout Interest Rate Swaps

Swap Negotiators levels the playing field, creates transparencyand reduces or eliminates banks’ undisclosed fees.

THE STATEMENT WHO SAID IT WHAT DOES IT MEAN?…often we advised clients to execute trades solely

because they presented opportunities for us to profit…I learned to think we were simply smarter than the client. For unsophisticated clients, being

smarter meant quoting padded rates.

Omer RosenFormer Citigroup Derivatives

The Huffington Post

Borrowers cannot see and do not understand pricing. Banks will pad the costs to profit from

the deals at every opportunity.

Banks collect many billions of dollars annually in undisclosed fees associated with these

instruments [swaps]—an amount that almost certainly would be lower if there were more

competition and transparent prices.

The New York TimesDecember 12, 2006

If the borrowers could see the fees, the banks would never charge as much as they do.

I attend derivatives sales meetings where not one single minute is spent asking questions about how we can help clients. It’s purely about how we can

make the most possible money off of them.

Greg SmithEx Derivatives Director

Goldman SachsPublic Letter with Resignation

Banks will look for any opportunity to add profits regardless of the impact to the borrower.

No business in finance is as profitable today as derivatives. Not making loans. Not offering credit cards. Not advising on mergers and acquisitions.

Not managing money for the wealthy.

Darrel DunfieProfessor

Stanford Graduate School of BusinessThe New York Times

Selling of swaps is a huge profit center to the banks and each dollar of profit is a direct

expense to the borrower.

As a seller of the swap, a loss to the customer works to the banks’ advantage.

Ulrich WeichersPresiding Judge

Federal German Court of Justiceon Deutsche Bank

Every dollar of [undisclosed] profit to the bank creates a loss for the borrower. The more negative to the borrower, the greater the profit to the bank.

Only swap dealers or other participants in the swap markets have access to current market rate

data at the confirmation of swap transactions.

First Amended ComplaintPress Communications v. Wachovia Bank

Superior Court of Justice, Mecklenberg City, NC Case No. 09 CVS21335

Borrowers will not know the true costs and are unable to know with any certainty what undisclosed profits are hidden without the

assistance of someone in the business, such as a swap negotiator, having access to live data.

THE PROBLEMS

THE STATEMENT WHO SAID IT WHAT DOES IT MEAN?After Hillcrest asked Swap Negotiators to vet

the deal, Wells agreed to reduce its fees (by more than $100,000)…“It turned out

to be a great business decision.”

Ted SmithCEO, Hillcrest Convalescent

The New York TimesAugust 6, 2011

A borrower represented by a swap negotiator will have an improved economic outcome

and a full understanding of the transaction.

THE SOLuTION

The downturn in the real estate mar-ket since 2008 coupled with tighter lend-ing policies of most banks has created a refinancing problem for many physician groups who own their real estate. During this time, CMAC has successfully worked with clients to find solutions. ▶ Here's An Overview Of Three Approaches That Have Worked For Our Physician Clients…

1. Nationalize the scope of the bidding—The key to success is to have knowledge of the most favorable terms and rates being of-

fered by lenders outside of your local area. CMAC has found that the same national bank that is holding firm to a 75% loan-to-value policy in one part of the country is working with our team on financing a 100% loan-to-value transaction in a city 2,000 miles away. That knowledge will em-power the local representative of that same bank to improve their own offer when he can point to those policy exceptions within the same institution. Additionally, once we have demonstrated to other competing banks that we are transacting financing at

the improved levels elsewhere, it invariably incites them to improve their own propos-als—even at levels where the loan exceeds the value of the real estate.

2. Restructure—In many cases, the an-swer involves creativity. CMAC had a re-cent client whose loan was terming where the remaining balance exceeded the mar-ket value. In that case, CMAC arranged fi-nancing involving four tranches to replace what had been a single loan. The primary consideration in piecing these loans to-gether was to improve both rate to cash

flow, despite the high LTV. 3. Re-syndication—This solution is the

most innovative and can produce very fa-vorable results. The driving force here is the income stream of the leases. In certain cases, a subset of the partners will fill the equity shortfall. Those partners will receive a preferred return before distribution to the current existing ownership group—a potential win-win for all owners.

The bottom line is that being upside down is not the end of the line. Be open, be active and be innovative.

Three Tips to Refinancing When Your Real Estate is Upside DownMany Deals Being Done At 100%+ LTV

PAGE 4 THeJOuRnalOfMeDicalRealesTaTe

WINTER PARK, Fla.—“I wish I could lower my rate right now, but I’m stuck because I’m up-side-down on my swap.”

“I’ve read through the documents a dozen

times, but there’s no way around my pre-payment penalty.”

There are many variations on these ob-jections, all of which are valid concerns for today’s borrower. But they are not nec-essarily roadblocks that cannot be over-come.

Take the orthopaedic group in Hicko-ry, North Carolina with several proper-ties. They had a prepayment penalty of 3% and an average interest rate of 6.11%. Once CMAC analyzed the numbers, they showed the group that a rate reduction to match other similar clients would leave them with a savings of nearly $300,000 over the term of the loan—net of all fees, including the prepayment penalty. CMAC was engaged, and the anticipated savings was surpassed.

Or consider a cardiology group in Or-lando, Florida. They were dissatisfied with their rate and their banking relationship had deteriorated with the exodus of famil-

iar faces and the influx of new staff. The group felt they were handcuffed because they had three swaps in place, and they were over $1,000,000 upside-down on those swaps.

Instead of staying the course, waiting for the swaps to term and having to refi-nance at whatever rates the market would bear at that time, CMAC and Swap Nego-tiators helped the group blend and extend the swaps so the rate was both reduced and fixed for a longer period of time.

It may seem impossible to leave a loan that has a hefty prepayment penalty or un-wind fee, but it is important to remember that this fee may quite simply be an invest-ment that can be quickly recouped. Rates are lower today than they have ever been before, and the only way to know with cer-tainty that your loan cannot be improved is to have an expert run the numbers.

A group like CMAC that has access to rates and terms given both to your other businesses locally and to other similar groups across the country can be your most valuable asset. Let them compare what you have now with what you could have, consider the costs of getting there, and then you can let the numbers speak for themselves.

By Steve Pishko

Prepayment Penalties and SwapsAre You Sure You’re Stuck?

Mortgage loan docu-ments often contain lots of pages of legal mumbo-jumbo detailing Events of Default, but most bor-rowers think they are safe as long as they never

miss a payment. Think again!Recently, many perfect payers have been

thrown into technical default for a breach of a covenant that would have never been noticed in past years. ▶ These Breaches Have Included…1. A reduction in property value (less than the approved LTV).2. A missed deadline in reporting—even a single partner being late with his personal financial statement.3. A loss of owner-occupied status.

The last on the list has really taken many by surprise. It generally occurs when a practice merges, sells or integrates with a hospital. Once that occurs, the operating entity and the real estate entity do not share common ownership and the covenant that requires the business of the operating en-

tity can no longer be met. Planning for this issue during the negotiation of the practice can often avoid unpleasant endings.

Once the default is declared, banks can charge the default rate of interest as de-fined in the note—often 15% or 18%. Also, many clients are finding their account transferred from their local banker to a Special Assets department of the bank—sometimes across the country. Generally, the job of the Special Assets department is to transition the client out of the bank as quickly as possible, with little thought given to customer service. The local loan officer’s hands are tied.

Why is this happening? Banks and their loan portfolios are now being carefully monitored by regulators who insist that the bank’s overall loan portfolio stays in compliance with established benchmarks. Regulators will review bank files with no true knowledge of your business and its place in the community. Just another case where a regulation has an unintended con-sequence —in this case penalizing a perfect payer.

By Elizabeth Allport

Perfect Payers Penalized as Banks Review Loan PortfoliosBeware The Technical Default

BOCA RATON, Fla.—The Greenfield Group, a Florida medical office building developer, executed two swap modifica-tions that enabled them to extend the fixed rates on their properties and, at the same time, improve cash flows.

The trades, commonly known as blend and extends, allowed Greenfield to incor-porate the negative value of the existing swaps into the value of the longer-term re-placement swaps. Because swap rates had declined substantially from the time that

the original swaps had been executed, the new longer-term rates (even after blend-ing) were lower.

Typically, without the intervention of a swap negotiator on a blend and extend, a bank will add profit to both the existing value and the new trade. With Swap Ne-gotiators handling the transaction, there was no profit added to the blended value and the new swap spread was half of what was charged on the original trade that had been executed without Swap Negotiators.

The Greenfield Group Executes Swap Modifications at Low SpreadsTransparency Just A Part Of The Transaction

It was your standard transaction—a borrower refinancing its loan. In this case, the borrower had to also unwind a swap with SunTrust Bank and enter into a new swap with BB&T. Alpha Omicron Pi na-tional sorority was aware of all the fees and charges that had been disclosed by the banks, but was unaware of the hidden fees that were not being disclosed…until its at-torney decided to take an extra step and do some research.

As a result of that research, the attor-ney and CPA for AOPi decided to engage Swap Negotiators. Once Swap Negotiators reviewed the documents, two facts became apparent. First, that SunTrust Bank was charging nearly $50,000 more than the actual par value on the unwind and that BB&T was charging more than $100,000 of undisclosed fees on the new swap. By this time, the parties were virtually at the point of no return. It was too late to start the bidding process over in order to seek com-

petitive pricing on the swap, and it was far too late to do anything about the SunTrust swap documents that allowed SunTrust to be the calculation agent.

In this case, it was a combination of transparency and reasonableness by the banks that created the savings. Once the added profit on the termination became public knowledge, SunTrust agreed to re-duce that fee to a more acceptable level. BB&T then agreed to a spread that was more reflective of the risk associated with the transaction rather than an arbitrary number that was unilaterally applied with-out the borrower’s knowledge.

In all, AOPi saved more than $75,000 in fees and has new documents that will give them better controls should they ever ter-minate their new swap. Most importantly, AOPi and the clients of this attorney and CPA will have a great knowledge advantage that will convert to savings the next time they need to enter into a swap.

Borrower Saves $75,000 in Hidden Swap FeesLast Minute Transparency Creates Reductions

Goldman Sachs Ex Blows Lid Off Bank SecretsProfits Are First, Clients Are A (Distant) Second

The next time a banker tells you that fixing your rate with a swap is pretty stan-dard stuff and puts some boilerplate docu-ments in front of you to sign, think about this…

In March 2012, Greg Smith, an execu-tive director of Goldman Sachs and head of its derivatives operations ended his 12-year career after penning a candid exit let-ter à la Hollywood’s Jerry Maguire.

Called Why I Am Leaving Goldman Sachs, it was published by The New York Times Op-Ed and promptly caused a fire-storm. The director cited a “toxic and de-structive” work environment. He summa-rized, “To put the problem in the simplest terms, the interests of the client continue to be sidelined.”

Smith asserted that the executive focus was on making the most possible money, even if it meant pushing the clients into bad products or giving bad advice. He wrote, “I attend derivatives sales meetings where not one single minute is spent ask-ing questions about how we can help cli-ents. It’s purely about how we can make

the most possible money off of them.” Is this an isolated problem at the world’s

third largest investment bank? Or is the same profit-over-ethics mentality cel-ebrated at many other banks and finance companies today?

If the motto on Wall Street is “caveat emptor,” then borrowers need to level the playing field by having advisors who un-derstand the many tricks played by the fi-nance industry.

Anyone entering into or terminating an interest rate swap needs to worry about the possibility that the bank derivatives desks will attempt to take undue profits or steer them in the wrong direction.

Borrowers can protect themselves by hiring swap negotiators who present the unbiased pros and cons, negotiate fair pricing and monitoring the trade to en-sure you don’t get fleeced.

Smith stated in his letter, “It makes me ill how callously people talk about ripping their clients off.” You can take steps to make sure you are not the next subject of bragging rights by the bank.

By Elizabeth Allport

Swap Negotiators levels the playing field.

PAGE 5THeJOuRnalOfMeDicalRealesTaTe

Raleigh Ortho Scores Triple Double in $30 Million Financing100% LTV—3.18% 7-Year Fixed—Limited Guarantees

RALEIGH, N.C.—Raleigh Orthopae-dic Clinic (ROC) has started development of an 83,000-square-foot medical office building and ambulatory surgery center. The surgery center will take approximate-ly 22,000 square feet of the new facility, which is partially-owned by Rex Hospital.

The new building will be built with no cash out of pocket by the physicians, low limited personal guarantees and a 7-year fixed rate of 3.18% under a loan agreement negotiated by CMAC that was nearly two years in the making.

As ROC expanded its operations and added doctors, it needed to enlarge its facilities to accommodate the additional patient flow and surgical procedures. The financing for the project was complicat-ed by the initial plans to build separate buildings in two stages. According to Karl Stein, the group’s CEO “This project was

a major undertaking. I not only needed a team that could secure the most favorable financing rate and terms, but I needed the confidence that someone could help me navigate the complexities that come with a project like this.”

CMAC’s team is comprised of a physi-cian and a former Wall Street banker, a combination that understands the busi-ness of healthcare while providing ex-pertise in negotiating with commercial banks.

“Not only did they save our group a tremendous amount of money from a rate standpoint, but the time-value benefit cannot be understated. CMAC’s involve-ment allowed me to focus on the practice’s day-to-day operations,” said Stein.

Based on previous experience, ROC en-gaged CMAC to put the financing pieces together. When the new project came up,

there was no question that they wanted the market fully vetted. Because CMAC has relationships with most every major commercial banking institution across the nation and sees thousands of proposals, it constantly knows where the market is at any point. CMAC uses the market knowl-

edge to leverage the best deal possible. According to Liz Allport, CMAC’s Di-

rector of Finance “as a former banker, I know the pressure the local relationship bankers are getting from their superiors to squeeze as much profit out of a deal. It’s my job to squeeze back."

Bank Faces Allegations of Swap OverchargeSwap Negotiator’s Audit Uncovers Discrepancy

A large national bank headquartered in the Southeast has yet to address the ques-tion of whether it overcharged a borrower on a swap transaction by modifying the scheduled amortization. The discrepancy in the rate used to calculate the amorti-zation was discovered during a post-ex-ecution audit of the documents by Swap Negotiators and would likely have gone undetected by the borrower. The bank’s amortization rate in question increased the spread and the commensurate profit to the bank. The rate was stated in a recorded call. Yet, when Swap Negotiators asked the bank to release the recordings for review, the bank refused.

Swap Negotiators has repeatedly offered to select a mutually agreeable third party to value the transaction and the bank has again refused each offer. Once the over-charge was found, Swap Negotiators is-sued a check to the borrower to make the borrower whole and continues to work with the bank to resolve the problem.

▶ Not The First Time…Swap Negotiators had found that this

same bank and same banker had made a similar unauthorized term adjustment on an earlier transaction that, again, would have resulted in higher profits to the bank had it not been caught prior to execution and the pricing adjusted. In that case, the bank changed the fixed-rate day count convention from a previous term sheet from 30/360 to Actual/360. This added more days of interest, thereby raising the effective interest rate; something that would have gone unnoticed except for Swap Negotiators review. See Catch Me If You Can below.

It is the hope of Swap Negotiators that as more borrowers find representation with qualified swap negotiators, unscru-pulous bankers will be less inclined to look for opportunities to take advantage of borrowers…an act that damages the reputation of the many trustworthy bank-ers that execute swaps every day.

Banks Holding Back Best Rates3.95% Like Putting Lipstick On A Pig

Banks today are on the offensive. Bor-rowers are aware that rates have dropped substantially and are, or will soon be, seek-ing lower rates. In an effort to retain or im-prove profits, banks have become proactive. They are either approaching or responding to their borrowers with “substantial” rate reductions. The problem is defining “sub-stantial.”

In September, 2011, a surgical hospital in Arkansas renegotiated a “substantial” rate reduction for its real estate loan. The hos-pital’s administrative team had been timely in their negotiations and saved hundreds of thousands of dollars in interest expense over the remaining term. Four months later, how-ever, CMAC negotiated a further reduction that nearly tripled the initial improvement, creating an additional savings of roughly $2,000,000. ▶ How Did This Happen?

In truth, banks are making greater prof-its than they have in decades. And they are depending upon the borrower’s lack of in-formation and skewed perception of interest rates to do so.

The phrase everything is relative has never been truer. To those commercial real estate

borrowers who have been paying interest rates of between 6% and 8%, a 4% rate is a vast improvement. But in today’s economy, a rate of 4% may well be leaving considerable money on the table.▶ How Much Lower?

In a sampling of 14 CMAC loans financed in 2011, where a benchmark had been estab-lished prior to CMAC’s engagement, the av-erage difference in rates was 71 basis points, or 0.71%. If considering a $10,000,000 loan, this difference would amount to a savings of over $500,000 in 10 years, a true substantial difference.

There is only one way to be reasonably certain that you, as a borrower, are not making an excess contribution to fund the bank’s new courtyard fountain—you must completely test the market over a wide geo-graphic footprint, and then have a compe-tent financial analyst compare all aspects of the various proposals (rate, fees, term, amortization, loan-to-value, debt service, etc.).

Without that ability, you are operating within a virtual vacuum and are more likely to accept a “substantial” reduction that is not nearly as “substantial” as it might appear.

In this example, the bank changed the Fixed Rate Day Count Convention from 30/360 (top) to Actual/360 (bottom) without telling anyone about it.

Because the actual results in more days of interest, the effective rateis increased. The bank would have profited by nearly $100,000

had it not been caught by Swap Negotiators.

The Day Count Convention ManeuverCATCH ME IF YOu CAN

ORIGINAL

CHANGED

THeJOuRnalOfMeDicalRealesTaTePAGE 6

One Doctor’s Journey to Hell and Back

Determined Ortho Executive Finds Lowest RateThird Time's A Charm

Over the last 24 months, Orthopaedic Specialists of the Carolinas (OSC) dra-matically improved its building loan rate, creating savings of nearly $1,000,000 over the term, but it didn’t come all at once. Only a CEO who had a rare combination of persistence and humility made it pos-sible. ▶ Here’s The Story…

In 2010, CMAC met with the CFO of OSC and advised her that they felt they could reduce OSC’s rate. OSC had a good relationship with its bank and discussed that possibility directly with its bank. As a result, the CFO negotiated a rate modi-fication that saved them several hundred thousand dollars over the term of the loan.

It looked like a very good deal to OSC, but, in reality, the bank had given the CFO a rate that was nowhere near the bottom of the market, and CMAC let her know that.

Once again, the story repeats. Back to the bank directly for another drop. And, again, CMAC knew there was money left

on the table.It wasn’t until a year later that the CEO

of OSC, after hearing reports of what CMAC had achieved for other ortho-paedic clients, interceded and engaged CMAC to find the real bottom of the mar-ket.

As a result, CMAC obtained an even lower rate that doubled OSC’s previous savings. However, the premium paid for the prior year’s interest was lost.

In today’s rate environment, borrow-ers need a little help to find where the real bottom of the market is located. Substan-tially depressed rates have given banks the opportunity to improve their own profits by passing on only a portion of the avail-able savings to borrowers. Because all of today’s rates look good in comparison to pre-2008 rates, a borrower is quite willing to take the offer from his bank and think that he has obtained the best possible rate. The lesson to take away—banks put their own profits first, and borrowers must be prepared to take all necessary steps to validate their rate.

I get the question all the time…Why aren’t you practicing medicine? It’s a simple question, and it deserves a simple answer. But there are no simple answers to life-changing

events. Not in my estimation, anyway.Turn the clock back to 1999. I was a

fourth-year medical school student look-ing forward to a career as a pediatrician when I began having symptoms of persis-tent pain in my right arm. Nothing seemed to help, and no one seemed able to find the source of my problem. Knowing the inten-sity that would be required by a looming residency, I decided to focus on my health after graduation and pursued answers in-stead of pediatrics.

Shortly after graduation, an isolated tumor was discovered strangling a tiny sensory nerve in my right arm. I followed the recommended course of action and the tumor was surgically removed. The pain, however, persisted and even grew worse. Much, much worse.

Over the course of the next five years, I met with over two dozen physicians who callously diagnosed me as a head case. A drug seeker. One by one, they told me my symptoms were psychosomatic. And with

By Shannon Stocker, M.D.

each analogous diagnosis, my world crum-bled a little more.

Eventually, open neuropathic ulcers formed on my right arm that could be nei-ther controlled nor denied. My weight had deteriorated to a meager 85 pounds and it hurt so much to walk that I was forced to use a wheelchair or a cane. I constantly felt as if someone had doused me in gasoline and lit me on fire. My husband and I made the decision to visit Mayo in Rochester where, after a week of grueling tests in-cluding thermography, MRIs, a nerve con-duction study and a spinal tap, I was finally diagnosed with RSD (Reflex Sympathetic

Dystrophy), a disorder of the autonomic nervous system that produces unrelenting pain. Although a diagnosis was clear, the treatment options offered were antiquated and unreliable at best.

Years earlier, I had read about a ket-amine coma trial in Germany for people with pain symptoms similar in quality to mine. I remember shaking my head in pity for those patients having to choose such a terrifying path in the hopes of living a pain-free life. Yet now, here I was…facing the same choice. I knew I could die, but was living with my life as it was really an option?

After further research, my husband and I learned the coma trials had just begun in Monterrey, Mexico. We lived in Orlando and, ironically, the coordinating physician for the study was less than two hours away in Tampa. The decision for us was an easy one. I met with the doctor and, only three short weeks later, we flew to Mexico. Two days after arriving in Monterey I lay in my hospital bed being prepped for the in-duction. I cried with my husband one last time, thanked him for his unconditional love and support, and then, never know-ing if I would see him again…kissed him goodbye.

Some people ask me if I miss medicine,

and my answer is always the same—I miss the kids who would have been my patients. I miss their gratitude and their honesty, and the intense satisfaction that comes with helping a child feel better. But not a day goes by when I wish I would have cho-sen a different path. Six months after the coma I became pregnant with my daugh-ter and 22 months later I gave birth to my son. My husband remains my rock and my best friend. I have a job that I believe in and teammates that stuck with me through hell.

And now I’m back. Right where I’m sup-posed to be.

New York Times Article Praises Swap Negotiators“It turned out to be a great business decision.” Ted Smith, CEO, Hillcrest Convalescent Center

With those nine words printed in The New York Times, Ted Smith may have her-alded a great awakening by commercial borrowers. Finally, borrowers will know that banks are charging hidden fees and those fees can be negotiated and substan-tially reduced.

The Times’ Chief Financial columnist, Gretchen Morgenson, put her national spotlight on a bank practice that had been well hidden in the shadows—charging commercial borrowers between 1% and 5%

of the value of their loan. Banks are able to do this without ever disclosing these fees by burying them in the borrowers’ fixed rates.

Morgenson went on to detail how Swap Negotiators was hired by Hillcrest after it had been quoted a fixed interest rate by Wells Fargo, and through negotiation, saved Hillcrest nearly $100,000.

This article may be read in its en-tirety on Swap Negotiators' Web site at swapnegotiators.com.

Too often we look at bank statements, not quite understanding some of the mysterious calculations, and assume the banks must know what they are doing. That isn’t always the case. As the CEO of SW Florida Neurosurgical, Bob O’Grady was not satisfied with the muddled re-sponses he received from his loan officer at Bank of America. As a former client, Bob turned back to CMAC for some bet-ter answers.

As CMAC delved into these statements, it was discovered that Bank of America

had used an improper benchmark that was not consistent with the language in the loan documents. Because of the size of the loan and the small difference in the benchmark deviation, the error was dif-ficult to detect. However, the cumulative impact over nearly a two-year period had added up to more than $54,000.

After some prolonged negotiations with Bank of America, the bank agreed with CMAC’s interpretation and calcu-lations and refunded the overcharge plus interest to the borrower.

Bank of America Returns Overcharges to NeurosurgeonsCMAC Audit Discovers $54,000 Bank Error

399 Carolina Avenue, Suite 250Winter Park, FL 32789Office 407.264.7251 Fax [email protected]

Published By…