the legal and regulatory environment for credit reporting systems financial sector policy global...

TRANSCRIPT

The Legal and Regulatory Environment for

Credit Reporting Systems

Financial Sector Policy Global Dialogue Series # 7Sponsored by the Financial Sector Vice Presidency and

the World Bank Institute

Washington, D.C.

June 18, 2001

Organization of today’s eventI. Introduction

- Ms. Margaret Miller, Senior Economist, World BankII. Presentation of Legal Issues for Credit Reporting

- Ms. Peggy Twohig, Federal Trade Commission- Diputada Maria Teresa Gomez Mont y Ureta, Mexican Congress

Short BreakIII. Importance of Credit Data and the Regulatory Framework

- Mr. Michael Staten, Professor, Georgetown University- Mr. Vanio Aguiar, Director of Off-Site Supervision, Central Bank of Brazil

Elements of a Credit Reporting System

• the public credit registry, if one exists• private credit registries, including chambers of commerce, and

banking associations• the legal framework for credit reporting• the legal framework for privacy, as it relates to this activity• the regulatory framework for credit reporting• the characteristics of other pertinent borrower data available in

the economy• the use of credit data in the economy, by financial intermediaries

and others• the cultural context for credit reporting

Results of 1999-2000 World Bank survey of public and private credit registries

Survey sample by countryRegion Public CIR Private CIRNumber of obs by: Country Country Firms

Latin America 26 17 29Africa(includes 8 nations in BCEAO)

13 1 1

W. Europe 12 7 7E. Europe 4 6 8Asia Pacific 6 4 5Other 5 1 2TOTAL 66 36 52

The credit reporting industry is in transition, with many new entrants

• The median age of private registries in the survey sample is 10 years. Thirty percent of the private registries were established since 1995.

• Latin America led all other regions in the 1990s in the establishment of public credit registries.

• Legal issues contributed to the creation of the public credit registry in approximately half of the countries – and legal issues are still pending in about half the countries with public registries

Public vs. Private Credit Registries

Feature Public PrivateSource ofinformation

Supervisedinstitutions

Varied sources

Participationmandatory?

Yes No

Positive Info? Yes In some cases

Borrowers assigneda rating?

Yes No

Minimum loan size In some countries No

Fee for service No charge orminimal charge

Yes

Institutional Arrangements for Private Credit Registries

Institutional Type Pros Cons

Private firm w/nobank ownership

All types of data,independence

No automaticaccess to data

Private firm w/ bankownership

All types of data,Special access tobank data

Independence maybe questioned

Bank association Access to bank dataIntegrity

Only bank data,only bank access

Chamber ofCommerce

Retail & non-bankdata, broad cover,historical record

No bank data,Limited funds formodernization

Commercial &Credit insurancefirms

In-depth data oncommercial sector

Limited coverage,High cost per entry

Who submits information to public and private registries?

0

5

10

15

20

25

30

35

priv com bank

pub com bank

pub devt bank

cred union/coop

finance corp

/leasing

cred card

issuers

firms pro

vd'g loans

retail & m

erchants

No.

of r

egis

trie

s

Public (of 29,w orldw ide)

Private (of 28 inLAC)

Firm data collected by public and private registries

0

5

10

15

20

25

30PublicCreditRegistries(30worldwide)

PrivateCreditBureaus(26 in LatinAmerica)

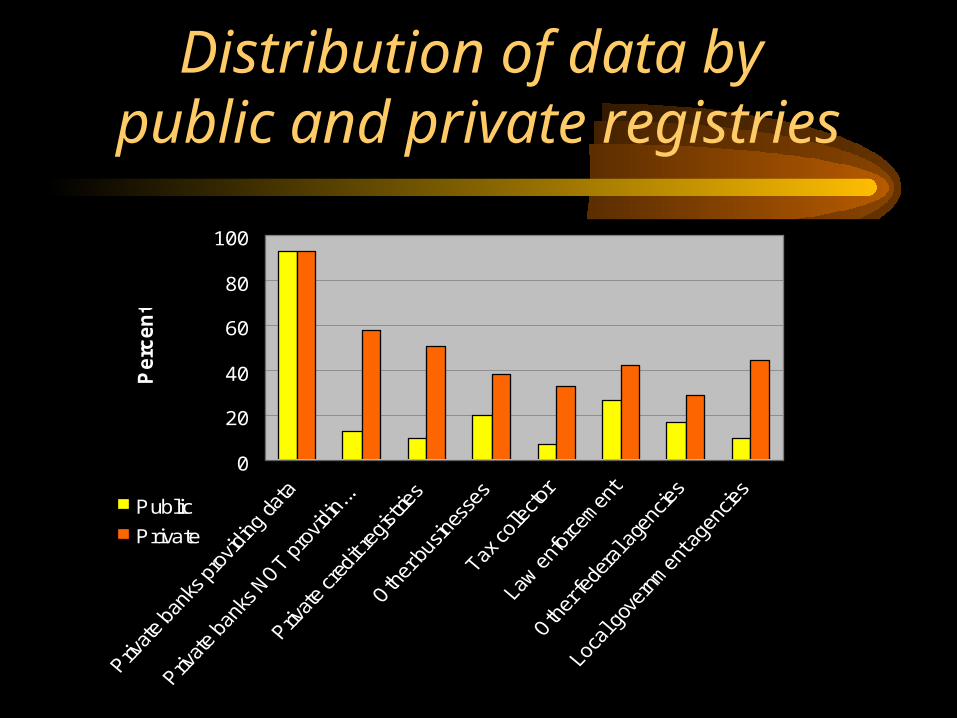

Distribution of data by public and private registries

0

20

40

60

80

100

Pe

rce

nt

Public

Private

Consumer Attention:Comparing Private and Public Registries

05

101520253035

Access toown data

ConsumerRelations

Department

Complaintstaken by

phone

Protocol fortaking

complaints

Comment onrecord

Surv

ey R

espo

nses

Private

Public

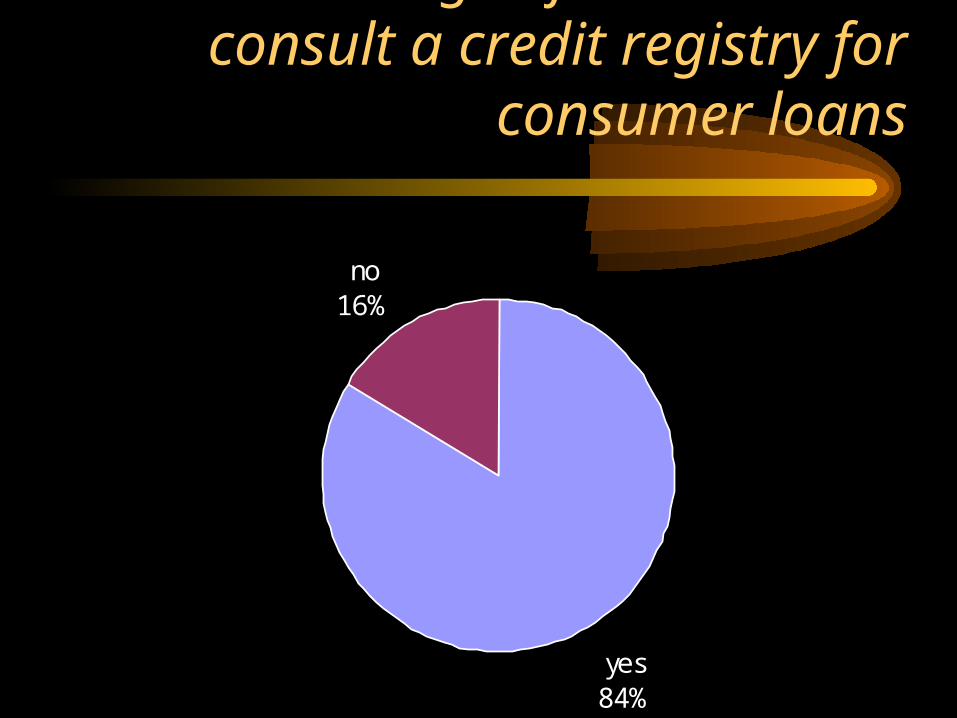

Percentage of Banks which consult a credit registry for consumer loans

yes84%

no16%

Percentage of Banks which consult a credit registry for small business loans

yes93%

no7%

Importance of Registry information relative to other sources of creditworthiness

0

5

10

15

20

25

30

35

Collateral Financial Standing ofthe Borrower

Borrower's Historywith the bank

num

ber

of fi

rms

Information from a credit registry is more important

Information from a credit registry is less important

Emerging elements of “good practice” Legal and regulatory framework

• Legal framework should encourage information sharing among lenders– review bank secrecy laws which can constrict

information flows

• Consideration of privacy issues important– broad privacy laws may unduly limit credit reporting

• Regulatory framework with enforcement– consumers have ability to bring complaints outside

judicial system

• Competition policy aspects of credit info.

Emerging elements of “good practice” Data collected and maintained

• Open system, not closed network– ownership by a limited group of lenders, bank

association, will discourage a broader database

• Collect both positive & negative information• Maintain data for a reasonable time frame - 5

years minimum– do not delete data on non-payments when debt repaid

Emerging elements of “good practice” Data collected and maintained

• Data should be inaccessible after a certain amount of time – time limits may vary by size of loan, type of inquiry

• Credit reports should not include highly sensitive information such as sexual orientation, political or religious affiliation, etc.

• Other identifying information, such as gender, should be evaluated more carefully

Emerging elements of “good practice” Data distributed

• Integrity and transparency are paramount– special standing of any group, including owners or

government, will discourage participation

• Open system preferable, reciprocity not necessary• Access to detailed information preferable

– loans described individually, not aggregates– institutions providing credit identified

• Restrictions to prevent “cherry-picking”• Distribution reflects privacy considerations

Emerging elements of “good practice” Credit reporting and bank supervision

• Supervisors include financial institution’s use of credit information as part of inspections

• Require publicly (government) owned financial institutions to provide data to legitimate credit reporting firms, associations

• Encourage all financial institutions to participate in credit reporting

Emerging elements of “good practice” Public Credit Registry (PCR)

• Clear objectives for PCR– consult with financial institutions, private credit

reporting firms

• Complement, not compete, with private firms

• Focus on larger loan sizes

• Provide customer service if data is distributed to financial system

Emerging elements of “good practice” Consumer Attention

• Borrowers should have access to their own data

• Consumer-friendly procedures in place to challenge erroneous information in reasonable time frame

• Record who has accessed data as part of report

• Clearly established privacy policy