the lessons of hurricane andrew: is florida really ready? economic incentives for building safer...

TRANSCRIPT

The Lessons of Hurricane Andrew: Is Florida Really Ready?

Economic Incentives for Building Safer CommunitiesWharton Risk Management and Decision Processes Center Roundtable

Institute for Building and Home Safety

The Wharton SchoolJune 11, 2002

Robert P. Hartwig, Ph.D., Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

Hurricane Andrew: A Summary of the Devastation

• Andrew struck S. FL on August 24, 1992 with sustained winds of 140 mph, gusts to 175 mph

• $15.5B insured losses ($20B in 2001 $)• $26 billion economic losses ($34B 2001 $)• 23 direct deaths• 700,000 homeowners claims• 28,066 home destroyed• 107,380 homes damaged• 82,000 businesses destroyed/damaged• 7,800 businesses closed as of Sept. 1992• 86,000 out of work as of Sept. 1992

World’s Largest Catastrophes(by insured loss)

$38.2

$20.1$16.8

$7.3 $6.3 $6.2 $6.0 $4.7 $4.3 $4.3

$0

$5

$10

$15

$20

$25

$30

$35

$40

Terro

rist A

ttack

s ('01

)*

Hurr. A

ndrew ('

92)

North

ridge

Eq.

('94

)

Typh. M

ireill

e

WS D

aria

WS L

othar

Hurr. H

ugo ('

95)

Misc

Sto

rms/F

lood

s

WS V

ivian

Typh B

art

$ Billions, in 2001 Dollars

*III Estimate; Includes life, liability, availtion and workers compensation losses.Source: Insurance Information Institute, Swiss Re;Note: WS = Winter Storm

United States: Disasters Waiting to Happen

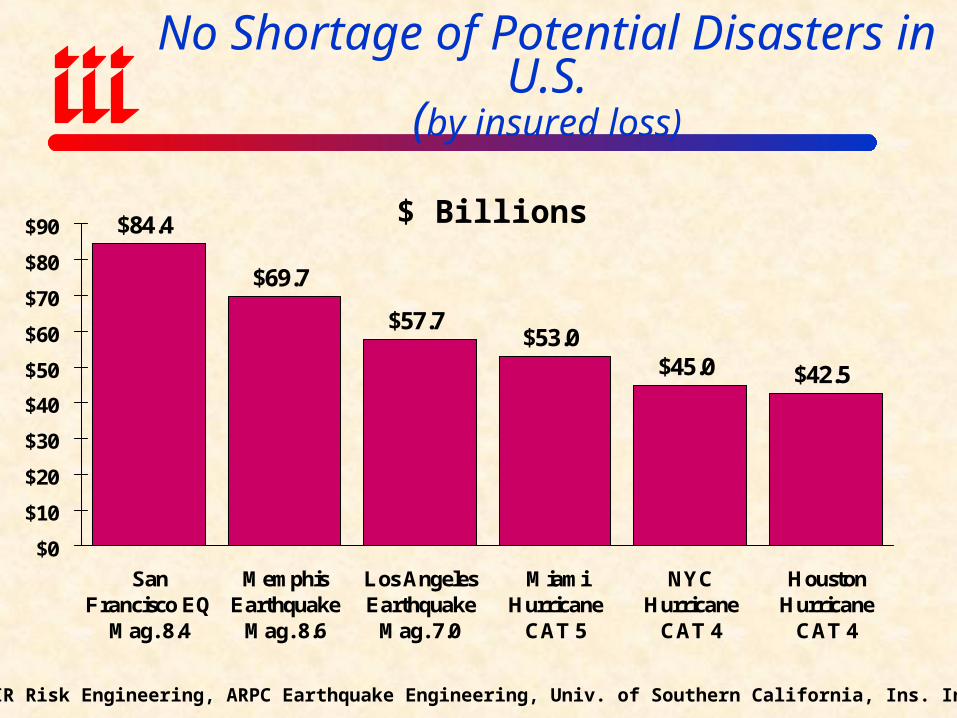

No Shortage of Potential Disasters in U.S.(by insured loss)

$84.4

$69.7

$57.7$53.0

$45.0 $42.5

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

SanFrancisco EQ

Mag. 8.4

MemphisEarthquake

Mag. 8.6

Los AngelesEarthquake

Mag. 7.0

MiamiHurricane

CAT 5

NYCHurricane

CAT 4

HoustonHurricane

CAT 4

$ Billions

Source: AIR Risk Engineering, ARPC Earthquake Engineering, Univ. of Southern California, Ins. Info Inst.

Probable Costs of FutureU.S. Natural Disasters

Source: AIR Risk Engineering, ARPC Earthquake Engineering, University of Southern California

$57.7 BILLION7.0 EARTHQUAKE

LOS ANGELES

$84.4 BILLION8.2 EARTHQUAKE

SAN FRANCISCO

HONOLULU

$30 BILLIONCLASS 4 HURRICANE

$25.6 BILLIONCLASS 5 HURRICANE

NEW ORLEANS

GALVESTON

$42.5 BILLIONCLASS 5 HURRICANE

MIAMI

$53 BILLIONCLASS 5 HURRICANE

$33.5 BILLIONCLASS 5 HURRICANE

HAMPTON

$52 BILLIONCLASS 4 HURRICANE

ASBURY PARK

$45 BILLIONCLASS 4 HURRICANE

NEW YORK

MEMPHIS

$69.7 BILLION8.6 EARTHQUAKE

$33.3 BILLION7.5 EARTHQUAKE

SEATTLE

10 Costliest Disasters in U.S. History(by insured loss)

$20.3 $19.6

$14.9

$5.9$3.2 $2.9 $2.5 $2.4 $2.1 $2.0

$0

$5

$10

$15

$20

$25

Ter

rori

stA

ttac

k: S

ept.

2001

Hur

rica

neA

ndre

w:

Aug

ust

1992

Nor

thri

dge

Ear

thqu

ake:

Jan.

199

4

Hur

rica

neH

ugo:

Sep

t.19

89

Hur

rica

neG

eorg

es:

Sept

.19

98

Hur

rica

neB

etsy

: Se

pt.

1965

TS

Alli

son:

Jul

y20

01

Hur

rica

ne O

pal:

Oct

ober

199

5

Hur

rica

neF

loyd

: Se

pt.

1999

Hur

rica

ne I

niki

:Se

pt. 1

992

$ Billions

Source:Insurance Services Office, Insurance Information Institute.

U.S. InsuredCatastrophe Losses

$7.5

$2.7$4.7

$22.9

$5.5

$16.9

$8.3 $7.3

$2.6

$10.1$8.3

$4.3

$28.1

$1.30

5

10

15

20

25

30

89 90 91 92 93 94 95 96 97 98 99 00 01* 02**

*Includes $20.3B for 9/11 losses estimated by ISO/PCS as of 6/18/02. Includes only business and personal property claims, business interruption and auto claims.**Through April 2002.Source: Property Claims Service, Insurance Information Institute

$ BillionsCAT Losses for 2001 Set a Record

•20 events (lowest since 1969)•1.5 million claims

•9/11: $20.3B = 51,000 claims

How Exposed is Florida Today?

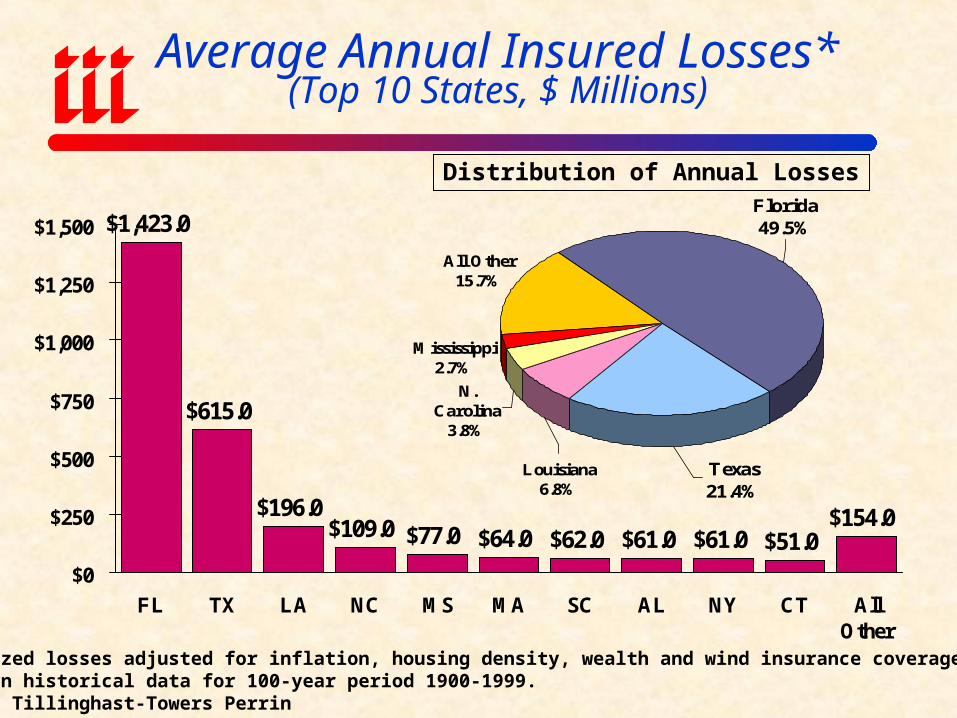

Average Annual Insured Losses*(Top 10 States, $ Millions)

$1,423.0

$615.0

$196.0$109.0 $77.0 $64.0 $62.0 $61.0 $61.0 $51.0

$154.0

$0

$250

$500

$750

$1,000

$1,250

$1,500

FL TX LA NC MS MA SC AL NY CT AllOther

*Normalized losses adjusted for inflation, housing density, wealth and wind insurance coverage, based on historical data for 100-year period 1900-1999.Source: Tillinghast-Towers Perrin

Louisiana6.8%

N. Carolina

3.8%

Mississippi2.7%

All Other15.7%

Texas 21.4%

Florida49.5%

Distribution of Annual Losses

Hurricanes Making Landfall During the 20th Century

*Normalized to adjusted for inflation, housing density, wealth and wind insurance coverage.Source: Tillinghast-Towers Perrin

Frequency

CAT 3 =47 Storms

29%

CAT 4 =15 Storms

9%

CAT 5 =2 Storms

1%

CAT 2 = 38 Storms

23%

CAT 1 = 62 Storms

38%

Cost*

CAT 3 =$943Mill

32.5%

CAT 4 =$1,579Mil

55.0%

CAT 5 =$41 Mil

1.4%

CAT 2 = $243Mil

8.3%

CAT 1 =$76 Mil2.6%

Estimated New Construction in Miami-Dade County, 1992-2001

$3,095.3

$12,981.8

$3,069.7

$305.5

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

South Miami-Dade All Miami-Dade

($ M

illi

ons)

New Residential Exposure New Commercial Exposure

$3.4 Billion

$16.1 Billion

Source: Best’s Review, June 2002 (International Hurricane Center, Florida International University), Ins. Info. Institute

Huge build-up in exposure in Florida

since 1992

•81% residential

•19% commercial

Estimated New ConstructionMiami-Dade County, Florida

Source: Best’s Review, June 2002 (International Hurricane Center, Florida International University)

South Miami-Dade was designated the county’s high-impact zone following Hurricane Andrew. Estimates include construction from 1992 through 2001

South Miami Dade

New Residential Exposure (Construction) $3,095,273,681

New Commercial Exposure (Construction) $305,492,393

All Miami-Dade

New Residential Exposure(Construction) $12,981,843,085

New Commercial Exposure(Construction) $3,069,654,106

Insured Losses in Florida ifHurricane Andrew Hit Today

Source: Best’s Review, June 2002 (EQECAT)

$20.3

$36.2

$46.7 $48.2 $46.3$43.5

$0$5

$10$15$20$25$30$35$40$45$50

Andrew'sOriginal

Path

Moved 0.1degreeNorth

Moved 0.2degreesNorth

Moved 0.3degreesNorth

Moved 0.4degreesNorth

Moved 0.5degreesNorth

Insu

red

loss

es, $

Bil

lion

s

•Each 0.1 degree equals about 7 miles

•A path of 0.3 degrees north of Andrew’s original location would create a direct hit on Miami

•Estimates are losses in today’s dollars after application of deductibles.

2000 Capacity of Florida Property Insurance Market

$11 Billion Capacity

$7.36B Bonding Capacity (Includes Loss Adj. Expenses)

$3.64B Cash*

$3.212B Industry Agg. Retention

$1.8

96B

Ind

.

Co-

paym

ents

$16.

1B O

vera

ll I

ndus

try

Los

s

*Projected for year-end 2000

Source: Florida Hurricane Catastrophe Fund

-$2.2-$2.8

-$4.0

-$2.9

-$5.4

-$0.3

-$2.6 -$2.4

-$3.6

-$8.9

-$6.5

-$11.5($12)

($10)

($8)

($6)

($4)

($2)

$01

99

1

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

E

20

02

F

Insurers Not Anxious to Assume Wind Risk in FL: U.S. UW Loss in HO Insurance, 1991-2002F

Source: A.M. Best, Insurance Information Institute

$ B

illi

ons

Underwriting losses in US homeowners insurance from 2000 to 2002 alone are

estimated at $19.0 billion, 14.5% above the $16.6 billion in 9/11 property losses.

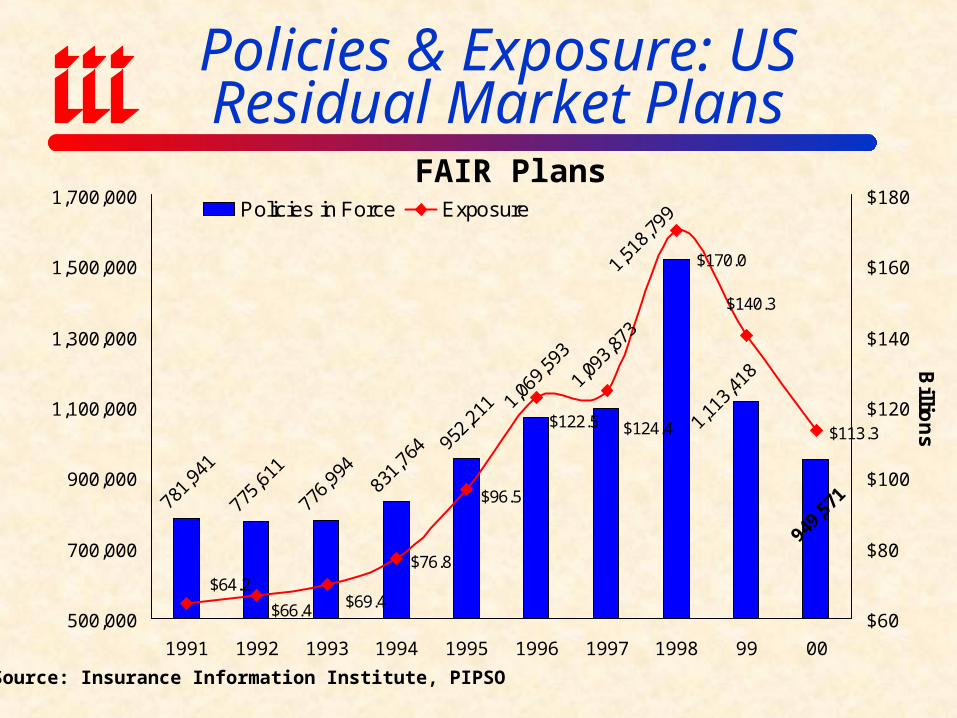

Policies & Exposure: US Residual Market Plans

781,

941

775,

611

776,

994

831,

764 95

2,21

1 1,06

9,59

3

949,

571

1,11

3,41

81,09

3,87

3

1,51

8,79

9

$113.3

$140.3

$170.0

$124.4$122.5

$96.5

$76.8

$69.4$66.4

$64.2

500,000

700,000

900,000

1,100,000

1,300,000

1,500,000

1,700,000

1991 1992 1993 1994 1995 1996 1997 1998 99 00

$60

$80

$100

$120

$140

$160

$180

Billio

ns

Policies in Force Exposure

Source: Insurance Information Institute, PIPSO

FAIR Plans

Policies in Force: Florida P/C JUA

270,910

675,497

849,271

705,988

487,590

256,753

107,62867,901

102,792116,027

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

Dec-93 Dec-94 Dec-95 Dec-96 Dec-97 Dec-98 Dec-99 Dec-00 Dec-01 Feb-02

Source: Insurance Information Institute, PIPSO

JUA is showing signs of growth

Florida’s Windstorm Underwriting Association

505,

076

457,

818

502,

369

442,

146

319,

843

240,

824

192,

842

135,

724

61,0

74

57,3

05$92.6$86.4

$7.0 $7.5

$15.3

$27.0

$36.3

$49.5

$75.4

$91.1

50,000

150,000

250,000

350,000

450,000

550,000

650,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Billio

ns

Policies in Force Exposure

Source: Insurance Information Institute, PIPSO

Southeast States HomeownersInsurance Premiums vs. US

$861

$657$594

$505 $487$457 $448

$266

$0

$200

$400

$600

$800

$1,000

TX FL MS SC US AL GA WI

Source: Insurance Information Institute from NAIC Data, 1999.

Highest in USLowest in US

5% Business Closure Scenario

Figure 3A: 5% Hurricane Closure Scenario Number of Business Closures

Source: Insurance Information Institute from US Census of Manufactures data.

2,459

1,5321,272

921

401127

0

500

1,000

1,500

2,000

2,500

Dade

Browar

d

Palm B

ch

H'b

orou

gh Lee

Mon

roe

Estimated number of business establishments that would be closed assuming a 5% closure rate.

$3,828

$2,637

$1,523

$1,962

$500$137

$0$500

$1,000$1,500$2,000$2,500$3,000$3,500$4,000

Mil

lio

ns

Figure 3B: 5% Hurricane Closure Scenario Sales Lost

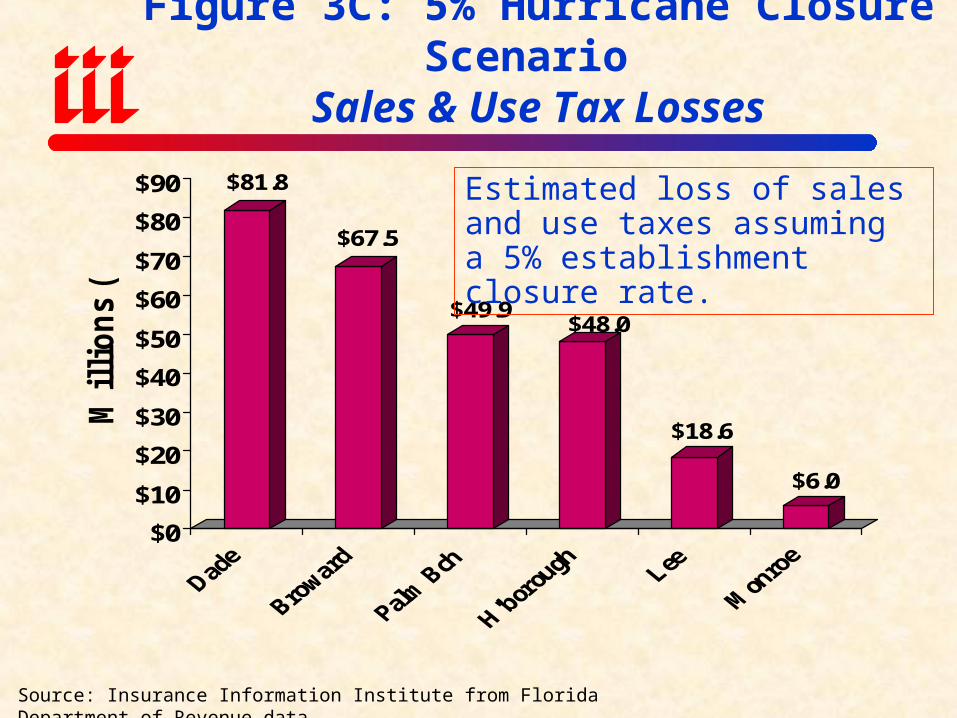

Source: Insurance Information Institute from Florida Department of Revenue data.

Estimated sales losses assuming a 5% establishment closure rate.

$81.8

$67.5

$49.9$48.0

$18.6

$6.0

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

Mil

lio

ns

($)

Estimated loss of sales and use taxes assuming a 5% establishment closure rate.

Figure 3C: 5% Hurricane Closure Scenario

Sales & Use Tax Losses

Source: Insurance Information Institute from Florida Department of Revenue data.

$798

$579

$432 $427

$113$23

$0$100$200$300$400$500$600$700$800

Mil

lion

s

Source: Insurance Information Institute from Florida Department of Revenue data.

Estimated payroll losses assuming a 5% establishment closure rate.

Figure 3D: 5% Hurricane Closure Scenario

Payroll Losses

30,036

22,039

15,64016,756

5,1511,184

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Source: Insurance Information Institute from US Census of Manufactures data.

Estimated job losses assuming a 5% establishment closure rate.

Figure 3E: 5% Hurricane Closure Scenario

Job Losses

$4,708

$3,283

$2,004

$2,437

$631$165

$0

$1,000

$2,000

$3,000

$4,000

$5,000

Mil

lion

s ($

)

Dade

Browar

d

Palm B

ch

H'bor

ough Lee

Mon

roe

Source: Insurance Information Institute from US Census of Manufactures and Florida Department of Revenue data.

Figure 3F: 5% Hurricane Closure Scenario Total Losses

Estimated total lost revenue, sales & use tax and payroll assuming a 5% establishment closure rate.

10% Business Closure Scenario(approximates Hurricane

Andrew experience in 1992)

Figure 4A: 10% Hurricane Closure Scenario Number of Business Closures

Source: Insurance Information Institute from US Census of Manufactures data.

4,918

3,0632,543

1,842

802254

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

Dade

Browar

d

Palm B

ch

H'b

orou

gh Lee

Mon

roe

Estimated number of business establishments that would be closed assuming a 10% closure rate.

$7,657

$5,273

$3,045

$3,925

$999$274

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000

Mil

lio

ns

Figure 4B: 10% Hurricane Closure Scenario Sales Lost

Source: Insurance Information Institute from Florida Department of Revenue data.

Estimated sales losses assuming a 10% establishment closure rate.

$163.7

$135.0

$99.9$95.9

$37.3

$11.9

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

Mil

lio

ns

($)

Estimated loss of sales and use taxes assuming a 10% establishment closure rate.

Figure 4C: 10% Hurricane Closure Scenario

Sales & Use Tax Losses

Source: Insurance Information Institute from Florida Department of Revenue data.

$1,596

$1,157

$863 $853

$226$45

$0$200$400$600$800

$1,000$1,200$1,400$1,600

Mil

lion

s

Source: Insurance Information Institute from Florida Department of Revenue data.

Estimated payroll losses assuming a 10% establishment closure rate.

Figure 4D: 10% Hurricane Closure Scenario Payroll Losses

60,072

44,079

31,28033,512

10,3032,369

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Source: Insurance Information Institute from US Census of Manufactures data.

Estimated job losses assuming a 10% establishment closure rate.

Figure 4E: 10% Hurricane Closure Scenario Job Losses

$9,416

$6,566

$4,009

$4,874

$1,263$331

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000$9,000

$10,000

Mil

lion

s ($

)

Dade

Browar

d

Palm B

ch

H'bor

ough Lee

Mon

roe

Source: Insurance Information Institute from US Census of Manufactures and Florida Department of Revenue data.

Figure 4F: 10% Hurricane Closure Scenario Total Losses

Estimated total lost revenue, sales & use tax and payroll assuming a 10% establishment closure rate.

Has Florida Learned Anything over the Past Decade?

Education

Mitigating Catastrophe Risk

Financial Incentives

Mitigation

Regulation

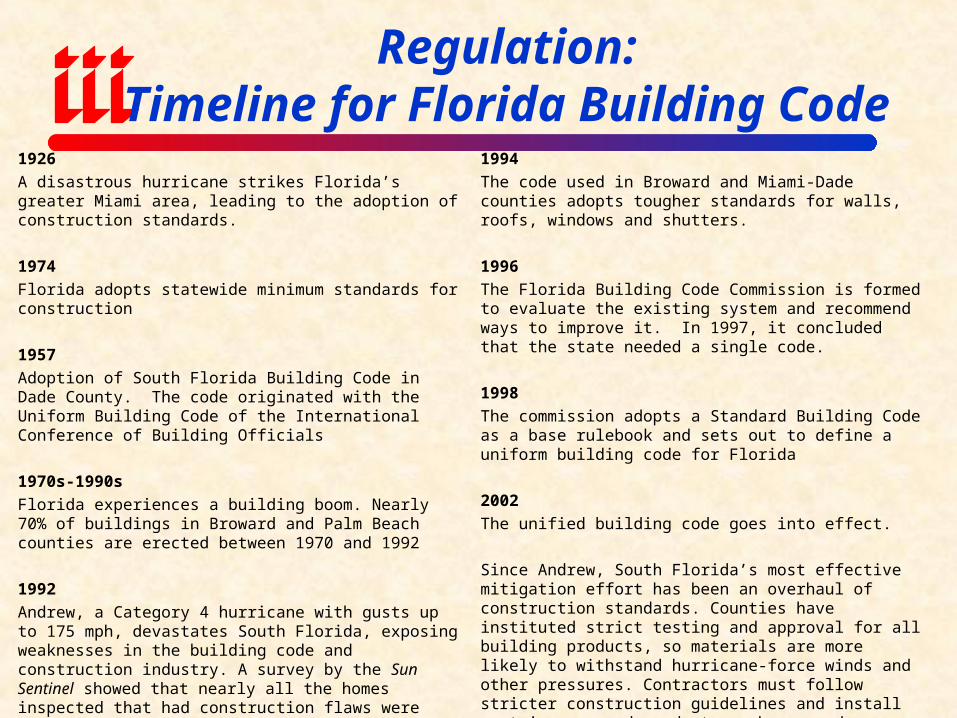

Regulation:Timeline for Florida Building Code

1926

A disastrous hurricane strikes Florida’s greater Miami area, leading to the adoption of construction standards.

1974

Florida adopts statewide minimum standards for construction

1957

Adoption of South Florida Building Code in Dade County. The code originated with the Uniform Building Code of the International Conference of Building Officials

1970s-1990s

Florida experiences a building boom. Nearly 70% of buildings in Broward and Palm Beach counties are erected between 1970 and 1992

1992

Andrew, a Category 4 hurricane with gusts up to 175 mph, devastates South Florida, exposing weaknesses in the building code and construction industry. A survey by the Sun Sentinel showed that nearly all the homes inspected that had construction flaws were built between 1975 and 1992, during the peak of South Florida’s residential growth. A survey conducted to identify code violations and construction deficiencies concluded that the majority of failures were attributed to noncompliance with the prescriptive requirements of the area building code

1994

The code used in Broward and Miami-Dade counties adopts tougher standards for walls, roofs, windows and shutters.

1996

The Florida Building Code Commission is formed to evaluate the existing system and recommend ways to improve it. In 1997, it concluded that the state needed a single code.

1998

The commission adopts a Standard Building Code as a base rulebook and sets out to define a uniform building code for Florida

2002

The unified building code goes into effect.

Since Andrew, South Florida’s most effective mitigation effort has been an overhaul of construction standards. Counties have instituted strict testing and approval for all building products, so materials are more likely to withstand hurricane-force winds and other pressures. Contractors must follow stricter construction guidelines and install certain approved products on homes and businesses. Hurricane shutters must pass stringent impact and wind tests.

Source: Best’s Review, June 2002 (Risk Management Solutions)

What Insurers are Doing: Education

• Most insurers have catastrophe safety information on their web sites:

• Similar information available through trade associations:Insurance Information Institute: www.iii.orgInstitute for Building and Home Safety:

www.ibhs.org

What Insurers are Doing: Education (continued)

Mitigation of Property DamageSecondary issue in earthquakes (though not mutually

exclusive from preservation of life)Excellent information available from IBHS

Buying appropriate catastrophe coverage III good source of informationBanks/agents sometimes weak link in chainLessons from Floyd: Flood insurance, windstorm

deductibles

What Insurers are Doing: Education•Also from IBHS “Open for Business: Disaster Recovery Guide for Small Business”

•III Brochures/web: “Am I Covered: Common Questions Asked by Homeowners about Insurance”

“Settling Insurance Claims after a Disaster”

“Insuring Your Business Against a Catastrophe”

Available free from IBHS at www.ibhs.org

What Insurers are Doing: Mitigation

• Sponsor research (and education) through IBHS and other organizations

• Support state and local efforts to strengthen building codes (ISO BCEGS Program):Building Code Effectiveness Grading Schedule

Financial Incentives

• Discounts

• Mandatory 2% wind deductibles

• Higher premiums

• Excluding wind

• Refusal to write beachfront properties

Running Against the Wind?Is Florida in Denial

• Serious Obstacles to Reducing CAT Losses in FLUnwillingness to significantly alter land use policiesNo risk-based lending practicesPolitical/lobbying efforts by developers, real estate interests defeat

restrictionsHomeowners oppose added cost to dwellingsSubsidies (e.g., flood insurance, rate suppression)Continued strong demographics

# housing units rising by 4%+ in FL, 2% nationally 17% increase in number of commercial/residential units, & 50% increase in replacement value of properties 1992-2002

• FEMA—Will emphasis shift to “Homeland Security?” FEMA was an “independent” agency with 5,100 employees Added layers of bureaucracy? Reduced effectiveness? Loss of focus?

Mitigation: Much, Much More Needed

• Mitigation is an Effective Tool, But Impact so Far Limited—Much more to be done!Only 15-20% of S. FL building stock

constructed since 1994Loss reduction of post 1994-buildings only

about 10%Even if replaced entire stock, impact would be

modest

Insurance Information Institute On-Line

If you would like a copy of this presentation, please give me your business card with e-mail address