the liquidity risk premium - ph&nthe liquidity risk premium: a free lunch for institutional...

TRANSCRIPT

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

What is Liquidity? Thinking of Portfolio Liquidity as an Asset

Individual Security

Liquidity:

The ability to transact

in a security at a given

point in time,

without affecting price

Opportunity:

The additional compensation for holding an

investment comprised of less-liquid securities.

Portfolio Liquidity:

The ability to

sufficiently fund cash

requirements

Investors can benefit from the Liquidity Risk

Premium inherent in less liquid investments

1

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

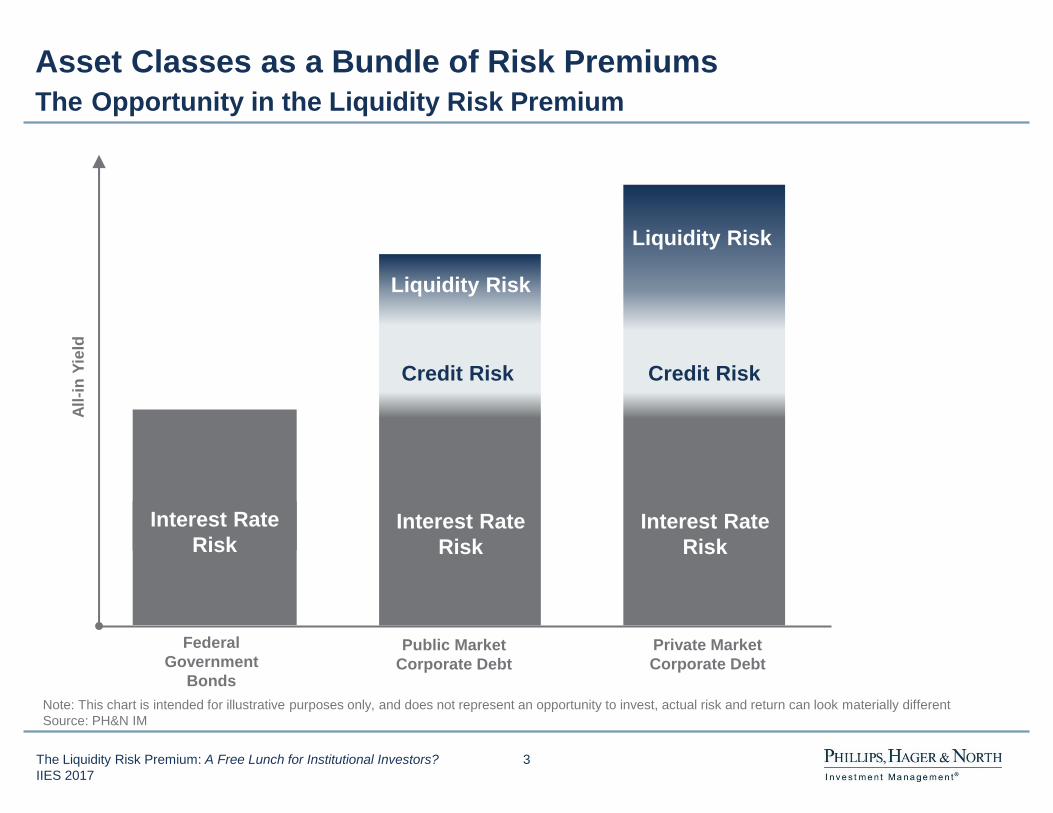

Asset classes are combinations of different risk

premiums, for example:

Economic growth risk

Interest rate risk

Inflation risk

Credit risk

Political risk

Liquidity risk

Risk Premium Investing

A risk premium is an expected excess return for bearing a risk

2

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Asset Classes as a Bundle of Risk Premiums

The Opportunity in the Liquidity Risk Premium

Interest Rate

Risk

Federal

Government

Bonds

Private Market

Corporate Debt

Interest Rate

Risk

Credit Risk

Liquidity Risk

All

-in

Yie

ld

Public Market

Corporate Debt

Interest Rate

Risk

Credit Risk

Liquidity Risk

Note: This chart is intended for illustrative purposes only, and does not represent an opportunity to invest, actual risk and return can look materially different

Source: PH&N IM

3

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

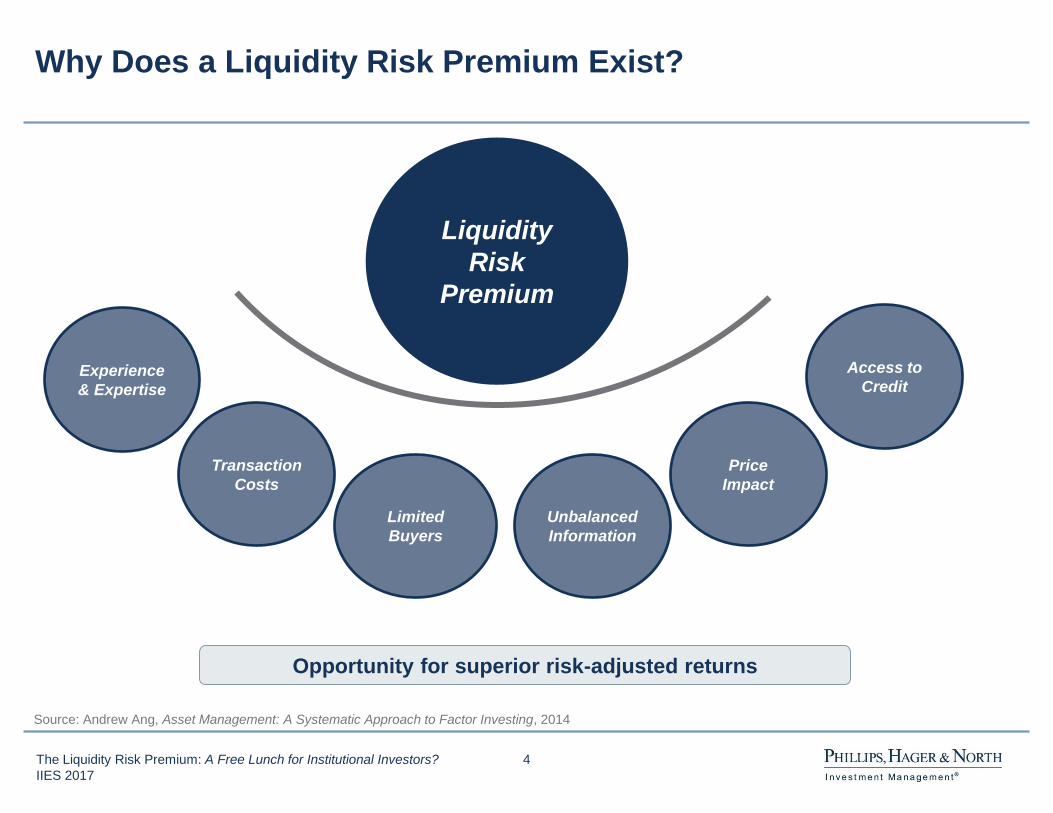

Why Does a Liquidity Risk Premium Exist?

Source: Andrew Ang, Asset Management: A Systematic Approach to Factor Investing, 2014

Liquidity

Risk

Premium

Unbalanced

Information

Opportunity for superior risk-adjusted returns

Price

Impact

Access to

Credit

Limited

Buyers

Transaction

Costs

Experience

& Expertise

4

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

A skilled manager must:

How Can You Benefit from It? Skilled Manager Needed for Navigation

Identify and

price risks

appropriately

Mitigate risks Exit

profitably

Create access

to unique

opportunities

5

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

The Benefits of Using a Fund Structural Liquidity of Vehicle and Underlying Securities

Patiently

deploy

capital

Fund

withdrawals

Create

internal

liquidity

Investment Vehicle Underlying securities

• Pooled fund structure

• Capital call/distribution

framework

• Allocation to cash &

equivalents

• Amortization

• Mixture of fixed and

floating rate securities

• Maturity profile

6

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Less-Liquid Fixed Income Investments Spectrum of Liquidity and Credit Risk

Note: This chart is intended for illustrative purposes only, and does not represent an opportunity to invest, actual risk and return can look materially different

Source: PH&N IM

Less

Liquid

Credit Risk

Federal

Agency

Provincial

Public IG

Fixed Income

High Yield

Private Placement

Corporate Debt

Conventional

Mortgages

Direct

Lending

Private Fixed Income

Public Fixed Income

More

Liquid

High Yield

Mortgages

7

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

De

c-0

1

De

c-0

2

De

c-0

3

De

c-0

4

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

De

c-1

6

Yie

ld S

pre

ad

vs.

Sim

ilar

Te

rm C

an

ad

as (

%)

The Liquidity Risk Premium in Mortgages

Mortgage and Bond Yield Spreads

Versus Similar-Term Canadas

*Spread on mortgages in PH&N Mortgage Pension Trust

** FTSE TMX Canada Short Term Corporate Bond Index

Source: FTSE TMX Global Debt Capital Markets Inc.

Conventional Mortgage

Spread*

“A” Rated

Corporate Bond Spread**

Key Features:

Investment backed by physical asset

Additional yield spread vs.

comparable credit risk investments

Diverse opportunity set

Stable source of high quality income

Portfolio diversification benefits

50 – 100 bps

50 – 100 bps

8

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

The Liquidity Risk Premium in Mortgages Range of Strategies

Universe Bond

Strategies

Conventional

Mortgage

Strategy

High Yield

Mortgage

Strategy

Interest Rate Risk Highest Medium Lowest

Credit Risk Medium Medium Highest

Yield Lowest Medium Highest

Liquidity Risk Lowest Medium Highest

9

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

IG Public Market

50 - 60

+106

Private Placement Corporate Debt What is It?

Liquidity Risk Premium

IG Private Placements

Rated Unrated

Lower Higher

Utility

Company Bridge (P3)

Power

Generation

Private Placement Corporate Debt: A highly customized form of debt financing.

10

+180

+35-45

3

+3952

+150-200

1 Current trading levels, February 2017

2 Floating rate spread

Source: PH&N IM

Buyers

Spread (bps)1

LRP (bps)1

Index Eligibility

10

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Private Placement vs. Public Market Issue Comparable Credit Risk with Liquidity Premium

Key Features of Private Placements

Incremental yield spread

Stronger credit protection

Customized deal terms

Structural liquidity

Diverse opportunity set

Stronger protection against economic loss1

Fewer participants, access to unique opportunities

Source: BMO Capital Markets, PCBond, BondLab. For illustrative purposes only.

*Spread levels shown are indicative of where issuers could issue in the Canadian Market versus the 30-year Government of Canada benchmark bond as of September 1, 2016 1 Moody’s Infrastructure Default and Recovery Rates, 1983-2015, 2003-12 Cred Loss Experience Study: Private Placement Bonds, 2016 Society of Actuaries

Yie

ld S

pre

ad

vs

. C

an

ad

as

(%

)

Incremental

Spread

+68 bps

Yield Spread

Recent 30-Year

Utility Sector Unrated IG Private Placement*

Public Issue Private Issue

11

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

What is Direct Lending? Lending Source as an Alternative to Banking System

Unique financing requirements,

limited sources of capital

Regulatory and balance sheet

constraints of traditional lenders

Supply side factors Demand side factors

Potential for attractive

risk-adjusted returns

Increasing demand for credit

Private debt recognized as a

genuine financing solution

Private companies with limited access to public markets

Event-driven situations in small- to medium-sized enterprises

Typically first or second in capital structure

The Opportunity

Direct Lending: A loan from a non-bank lender made directly to a company

12

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Structural Considerations

Capital call and distribution framework

Capital commitment and lock-up period

Investment period

Management fee + carried interest

Source: BlueBay internal estimates. For illustrative purposes only.

+200-275bps

Spread

(illiquidity)

Private Market Lending Capturing Illiquidity Premium Through Bespoke Private Loans

Just ML HY MT2 (yield

as liquid comparable) vs.

DL (make DL blurred of

~200-275bps)

Net

Ex

pec

ted

IR

R (

%)

Incremental

Spread

+100 – 300bps

High Yield Direct Lending

(Senior)

Investment Strategy

Target superior returns to equivalent public debt

securities, through liquidity and credit premiums

Senior secured loans and subordinated debt (short

term, floating rate)

Capital protection, contractual returns, current income

13

Bringing it All Together

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Improving the Risk-Reward Profile Adding Less-Liquid Fixed Income Investments

Modeled Expectations1

10-yr Annualized Return 2.6%

Annual Downside Risk2 -7.7%

Annual Volatility 4.0%

Sharpe Ratio 0.23

Modeled Expectations1

10-yr Annualized Return 3.4%

Annual Downside Risk2 -6.5%

Annual Volatility 3.6%

Sharpe Ratio 0.46

Baseline Enhanced

1 Refer to appendix for modelling assumptions and disclosures. Hypothetical performance analyses are for illustrative purposes only and there is no guarantee that hypothetical returns or

projections will be realized. 2 CVaR95 which represents the expected loss during the worst 5% of return outcomes.

Universe Bonds 70%

Mortgages 10%

Direct Lending

10%

Private Corporate

Debt 10%

Universe Bonds 70%

Corporate Bonds 30%

15

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Less-Liquid Investment Considerations

Policy Considerations

Trustee/Committee Education

Ability to Bear Illiquidity?

What is Your Objective?

Reporting and Performance Analysis

Modelling Challenges

Portfolio Management

Considerations

Governance

Manager Due Diligence Investment Strategy and Process

Risk Management and Infrastructure

Fund Structure and Fees

16

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

The Liquidity Risk Premium A Free Lunch for Institutional Investors?

Conditions for success:

Long-horizon investor

Predictable liquidity needs

Stable pension fund governance

Appropriate investment expertise

Skilled investment managers

17

Appendix

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Assumptions and Disclosures Capital Market Assumptions

Assumptions represent the views of PH&N for the purposes of illustrating and understanding the potential risk-reward trade-off of different portfolio decisions. Investors should be aware of the

limitations using forward-looking assumptions in that there is absolutely no guarantee that future performance will occur according to any ex-ante expectation.

Asset Classes Representative Data Series

Expected

10-yr

Annualized

Return

Expected

Annual

Volatility

Expected

Annual

Downside

Risk

Universe Bonds FTSE TMX Canada Universe Bond Index 2.4% 4.2% -7.7%

Long Term Government Bonds FTSE TMX Canada Long Term Government Bond Index 2.7% 7.6% -14.1%

Long Term Corporate Bonds FTSE TMX Canada Long Term Corporate Bond Index 3.9% 7.4% -17.1%

20+ Strip Bonds FTSE TMX Canada 20+ Strip Bond Index 3.4% 14.8% -28.9%

Corporate Bonds FTSE TMX Canada All Corporate Bond Index 3.1% 3.8% -7.8%

Mortgages PH&N Mortgage Pension Trust 3.6% 2.4% -1.3%

Long Mortgages PH&N Long Mortgage Pension Trust 3.5% 6.9% -10.5%

Private Corporate Debt Constructed from FTSE TMX Canada corporate indices 3.7% 4.1% -8.6%

Direct Lending Credit Suisse Leveraged Loan Index (USD) 9.0% 8.6% -17.8%

Canadian Equities S&P/TSX Composite Index 6.8% 17.1% -29.9%

Global Equities MSCI World Index (CAD) 7.3% 14.9% -28.0%

Liability

Illustrative cash flows discounted using a proxy of the CIA's

prescribed methodology for commuted value (Government of

Canada spot curve + 90 bps) and annuity purchase liabilities

(provincial spot curve) resulting in an overall solvency

duration of 14.5 years

2.9% 7.9% -13.9%

19

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Assumptions and Disclosures Capital Market Assumptions

Assumptions represent the views of PH&N for the purposes of illustrating and understanding the potential risk-reward trade-off of different portfolio decisions. Investors should be aware of the

limitations using forward-looking assumptions in that there is absolutely no guarantee that future performance will occur according to any ex-ante expectation.

Correlation

Lon

g T

erm

Go

ve

rnm

ent B

ond

s

Lon

g T

erm

Co

rpo

rate

Bo

nd

s

20+

Str

ip B

ond

s

Co

rpo

rate

Bo

nd

s

Un

ive

rse

Bo

nd

s

Mo

rtg

ag

es

Lon

g M

ort

ga

ge

s

Dire

ct L

en

din

g

Canadia

n E

quitie

s

Glo

ba

l E

qu

itie

s

So

lve

ncy A

nnu

ity P

urc

ha

se

Lia

bili

ty

So

lve

ncy C

om

mu

ted

Va

lue L

iabili

ty

Priva

te C

orp

ora

te D

ebt

Long Term Government Bonds 1

Long Term Corporate Bonds 0.8 1

20+ Strip Bonds 1.0 0.8 1

Corporate Bonds 0.8 0.9 0.8 1

Universe Bonds 1.0 0.8 0.9 0.9 1

Mortgages 0.8 0.6 0.7 0.7 0.9 1

Long Mortgages 0.8 0.7 0.8 0.7 0.8 0.8 1

Direct Lending -0.1 0.3 0.0 0.3 -0.1 -0.2 -0.3 1

Canadian Equities 0.0 0.2 0.0 0.1 -0.1 -0.2 -0.1 0.4 1

Global Equities 0.1 0.2 0.1 0.1 0.0 0.0 0.0 0.3 0.6 1

Solvency Annuity Purchase Liability 1.0 0.8 1.0 0.8 1.0 0.8 0.8 0.0 0.0 0.1 1

Solvency Commuted Value Liability 1.0 0.7 0.9 0.7 0.9 0.8 0.9 -0.2 -0.2 0.0 0.9 1

Private Corporate Debt 0.8 0.8 0.8 0.9 0.9 0.8 0.7 0.1 -0.2 -0.1 0.9 0.8 1

20

The Liquidity Risk Premium: A Free Lunch for Institutional Investors?

IIES 2017

Disclaimer

This presentation is intended for institutional investors only.

This document has been provided by Phillips, Hager & North Investment Management (PH&N IM) for information purposes only and may not be reproduced, distributed or published without the

written consent of PH&N IM. It is not intended to provide professional advice and should not be relied upon in that regard.

PH&N IM takes reasonable steps to provide up-to-date, accurate and reliable information, and believes the information to be so when printed. Information obtained from third parties is believed to be

reliable, but no representation or warranty, express or implied, is made by PH&N IM, its affiliates or any other person as to its accuracy, completeness or correctness. We assume no responsibility for

any errors or omissions. The views and opinions expressed herein are those of PH&N IM as of the publication date and are subject to change without notice. This information is not intended to be

an offer or solicitation to buy or sell securities or to participate in or subscribe for any service. No securities are being offered, except pursuant and subject to the respective offering documents and

subscription materials, which shall be provided to qualified investors. This document is for general information only and is not, nor does it purport to be, a complete description of an investment in any

RBC, PH&N or BlueBay funds. If there is an inconsistency between this document and the respective offering documents, the provisions of the respective offering documents shall prevail.

These materials contain statements that are not purely historical in nature, but are “forward-looking statements.” These include, among other things, projections, hypothetical performance analyses,

hypothetical analyses of income, yield or return, future performance targets, sample or pro forma portfolio structures or portfolio composition, scenario analyses, specific investment strategies and

proposed or pro forma levels of diversification or sector investment. These forward-looking statements are based upon certain assumptions and involve significant elements of subjective judgment

and analysis. No representation is made that any returns indicated will be achieved or that all assumptions have been considered or stated. Actual events are difficult to predict and are beyond our

control. Hence, actual events may differ materially from those assumed. All forward-looking statements included are based on information available on the date hereof and we do not assume any duty

to update any forward-looking statement. Some important factors which could cause actual results to differ materially from those in any forward-looking statements include, without limitation, changes

in general economic, market, legal and financial conditions. Accordingly, there can be no assurance that hypothetical returns or projections can be realized, that forward-looking statements will

materialize or that actual returns or results will not be materially different than those presented.

Commissions, trailing commissions, management fees and expenses all may be associated with the funds mentioned in this presentation. Please read the offering materials for a particular fund

before investing. The performance data provided are historical returns, they are not intended to reflect future values of any of the funds or returns on investment in these funds mentioned in this

presentation. Further, the performance data provided assumes reinvestment of distributions only and does not take into account sales, redemption, distribution or optional charges or income taxes

payable by any unitholder that would have reduced returns. The unit values of non-money market funds change frequently. For money market funds, there can be no assurances that the fund will be

able to maintain its net asset value per unit at a constant amount or that the full amount of your investment in the fund will be returned to you. Mutual fund securities are not guaranteed by the

Canada Deposit Insurance Corporation or by any other government deposit insurer. Past performance may not be repeated.

The amount of risk associated with any particular investment depends largely on the investor’s own circumstances. Investors should consult their professional advisors/consultants regarding the

suitability of the investment solutions mentioned in this presentation.

This document may contain forward-looking statements about general economic factors which are not guarantees of future performance. Forward-looking statements involve inherent risk and

uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. We caution you not to place undue reliance on these statements as a

number of important factors could cause actual events or results to differ materially from those expressed or implied in any forward-looking statement. All opinions in forward-looking statements are

subject to change without notice and are provided in good faith but without legal responsibility.

PH&N IM is a division of RBC Global Asset Management Inc. (RBC GAM Inc.). RBC GAM Inc. is the manager and principal portfolio adviser of the Phillips, Hager & North (PH&N) investment funds.

RBC GAM Inc. is registered with the various securities commissions of Canada as a portfolio manager, which permits it to provide discretionary investment management services to its clients, and as

an exempt market dealer which permits it to act as a dealer for prospectus exempt trades in certain circumstances. RBC GAM Inc. is also registered as an Investment Fund Manager in Ontario,

British Columbia, Quebec and Newfoundland and Labrador and as a Commodity Trading Manager in Ontario.

Each of RBC GAM Inc. and BlueBay Asset Management LLP (BlueBay) is a wholly-owned subsidiary of Royal Bank of Canada, and an affiliated company and may be considered as related issuers

and/or connected issuers under applicable securities legislation.

®/™ Trademark(s) of Royal Bank of Canada. Used under licence. IC1702123

© RBC Global Asset Management Inc., 2017.

NOTE: [*Updated January 6, 2017]

This disclosure is for institutional presentations

about PH&N investment funds that include

performance data. Please adjust the disclosure

accordingly if not including performance, or if

the topics covered in the presentation include,

for example, BlueBay capabilities, Alternative

asset capabilities, QUANT Funds

“performance”. Approval for institutional

marketing materials and information about

compliance with legal, regulatory, corporate or

brand standards may be sought from

21

V A N C O U V E R Waterfront Centre, 20th Floor

200 Burrard Street

Vancouver, British Columbia

V6C 3N5 Canada

T 604-408-6000

T O R O N T O 22nd Floor

155 Wellington St. West

Toronto, Ontario

M5V 3K7 Canada

T 416-974-2710

M O N T R É A L 6th Floor, North Wing

1 Place Ville Marie

Montréal, Québec

H3B 1Z5 Canada

T 514-876-1256