the macroeconomics of credit market imperfections (part i ... · preferences, technology, and...

TRANSCRIPT

The Macroeconomics of Credit MarketImperfections (Part I): Static Models

Jin Cao1

1Munich Graduate School of Economics, LMU Munich

Reading Group: Topics of Macroeconomics (SS08)

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

Problem: Introducing financial sector in macro

I It is extremely desired to introduce financial sector in macro:I Financial sector is gaining importance in economy, one of main

resources of funding;I Micro foundation for better understanding of macro, e.g.

economic growth, monetary policy, financial globalization, etc.

I However, it’s not straight forward to do so:I Financial sector is too complicated, reality versus tractability;I Severe technical problems, especially in dynamic macro

I Heterogeneity: challenging representative agent modelling;I Discontinuity and non-monotonicity: challenging dynamic

optimization.

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

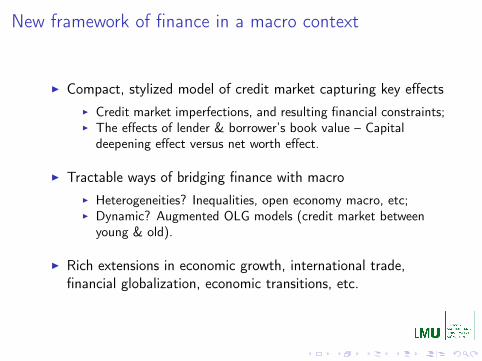

New framework of finance in a macro context

I Compact, stylized model of credit market capturing key effectsI Credit market imperfections, and resulting financial constraints;I The effects of lender & borrower’s book value – Capital

deepening effect versus net worth effect.

I Tractable ways of bridging finance with macroI Heterogeneities? Inequalities, open economy macro, etc;I Dynamic? Augmented OLG models (credit market between

young & old).

I Rich extensions in economic growth, international trade,financial globalization, economic transitions, etc.

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

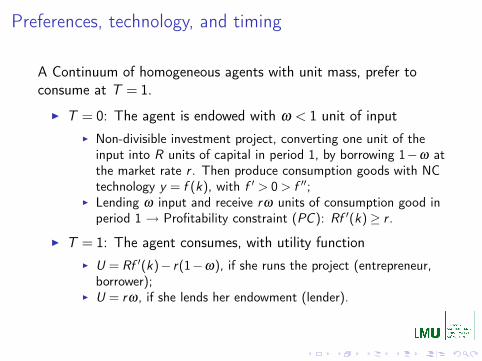

Preferences, technology, and timing

A Continuum of homogeneous agents with unit mass, prefer toconsume at T = 1.

I T = 0: The agent is endowed with ω < 1 unit of inputI Non-divisible investment project, converting one unit of the

input into R units of capital in period 1, by borrowing 1−ω atthe market rate r . Then produce consumption goods with NCtechnology y = f (k), with f ′ > 0 > f ′′;

I Lending ω input and receive rω units of consumption good inperiod 1 → Profitability constraint (PC ): Rf ′(k)≥ r .

I T = 1: The agent consumes, with utility functionI U = Rf ′(k)− r(1−ω), if she runs the project (entrepreneur,

borrower);I U = rω, if she lends her endowment (lender).

Credit market imperfection: borrowing constraint

I ω : Entrepreneur’s net worth, firm’s balance sheet, theborrower’s creditworthiness...

I The agent can borrow and invest only if borrowing constraint(BC ) satisfied: λRf ′(k)≥ r(1−ω). Measure of agencyproblem: λ < 1

I Reasons:I Strategic default, renegotiation, and inalienable human capital

(Hart & Moore, 1994);I Moral hazard (hidden action), etc.

I Interpretations:I Institutional quality;I The state of financial development, etc.

Example: Motivating λ by incomplete contract

I In T = 0 a borrower needs to borrow 1−ω to kick off herproject, promising the lender a rate weakly higher than marketrate r . And the project is used as collateral;

I Inalienable human capital: The project yields Rf ′(k) in T = 1if run by the borrower, but λRf ′(k) (λ < 1) if run by anybodyelse;

I Then in T = 1 the borrower may want to renegotiate andbargain down r – A credible threat;

I Therefore in the first place, the lender would never lend morethan the value of collateral – borrowing constraint (BC )λRf ′(k)≥ r(1−ω).

Aggregate capital formation in equilibrium

I Both BC : λRf ′(k)≥ r(1−ω) and PC : Rf ′(k)≥ r satisfied,

Rf ′(k) = max{

1,1−ω

λ

}r

I If λ +ω < 1, then BC is tighter than PC , Rf ′(k) = 1−ω

λr > r

I Too little investment;I Credit market imperfection → Net worth effect, i.e.

ω ↑→ f ′(k) ↓→ k ↑.

I If λ +ω > 1, then PC is tighter than BC , Rf ′(k) = r > 1−ω

λr

I Optimal investment;I No net worth effect.

Appealing features in equilibrium

I Endogenized entrepreneurs / lendersI If λ +ω > 1, Rf ′(k) = r , indifferent between being

entrepreneurs and lenders;I If λ +ω < 1, Rf ′(k) > r , agents prefer being entrepreneurs.

However, BC makes it a mixed strategy equilibrium.

I The role of indivisibility of investmentI If, instead, we start from heterogeneous agents, i.e. assume

entrepreneurs / lenders, then usually difficult to find equilibria;I However, ex ante homogenous agent plus indivisibility →

endogenized heterogeneity ex post!I Easier to introduce heterogeneities in other dimemsions, e.g.

heterogeneities in endowment ω or / and profitability R.

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

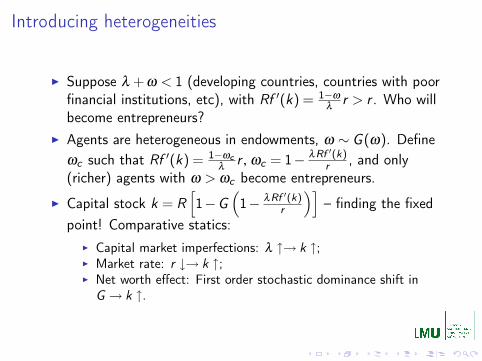

Introducing heterogeneities

I Suppose λ +ω < 1 (developing countries, countries with poorfinancial institutions, etc), with Rf ′(k) = 1−ω

λr > r . Who will

become entrepreneurs?I Agents are heterogeneous in endowments, ω ∼ G (ω). Define

ωc such that Rf ′(k) = 1−ωcλ

r , ωc = 1− λRf ′(k)r , and only

(richer) agents with ω > ωc become entrepreneurs.

I Capital stock k = R[1−G

(1− λRf ′(k)

r

)]– finding the fixed

point! Comparative statics:I Capital market imperfections: λ ↑→ k ↑;I Market rate: r ↓→ k ↑;I Net worth effect: First order stochastic dominance shift in

G → k ↑.

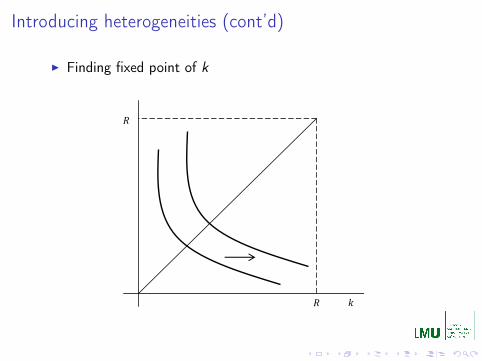

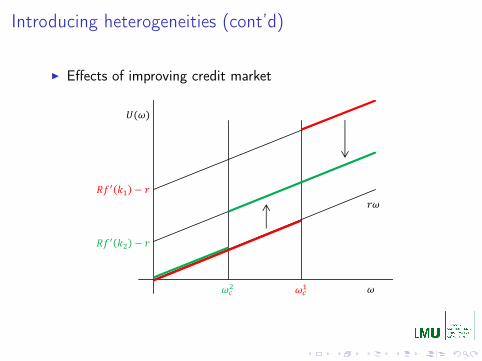

Introducing heterogeneities (cont’d)

I Finding fixed point of k

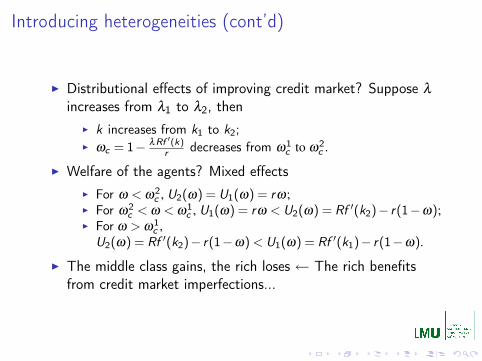

Introducing heterogeneities (cont’d)

I Distributional effects of improving credit market? Suppose λ

increases from λ1 to λ2, thenI k increases from k1 to k2;I ωc = 1− λRf ′(k)

r decreases from ω1c to ω2

c .

I Welfare of the agents? Mixed effectsI For ω < ω2

c , U2(ω) = U1(ω) = rω;I For ω2

c < ω < ω1c , U1(ω) = rω < U2(ω) = Rf ′(k2)− r(1−ω);

I For ω > ω1c ,

U2(ω) = Rf ′(k2)− r(1−ω) < U1(ω) = Rf ′(k1)− r(1−ω).

I The middle class gains, the rich loses ← The rich benefitsfrom credit market imperfections...

Introducing heterogeneities (cont’d)

I Effects of improving credit market

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

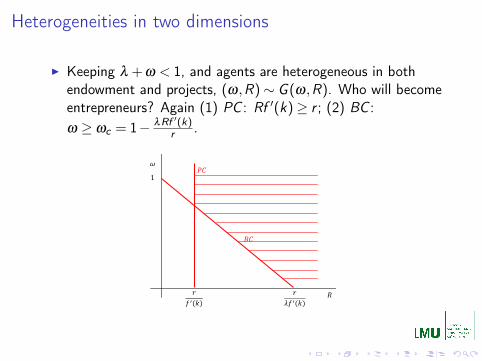

Heterogeneities in two dimensions

I Keeping λ +ω < 1, and agents are heterogeneous in bothendowment and projects, (ω,R)∼ G (ω,R). Who will becomeentrepreneurs? Again (1) PC : Rf ′(k)≥ r ; (2) BC :ω ≥ ωc = 1− λRf ′(k)

r .

1

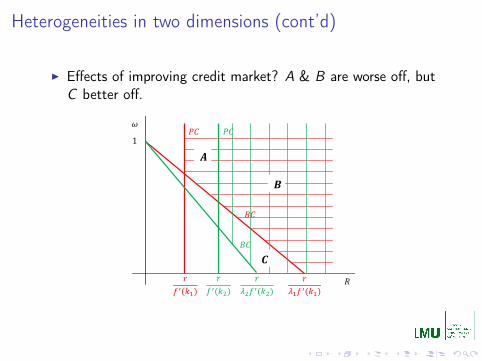

Heterogeneities in two dimensions (cont’d)

I Effects of improving credit market? A & B are worse off, butC better off.

1

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

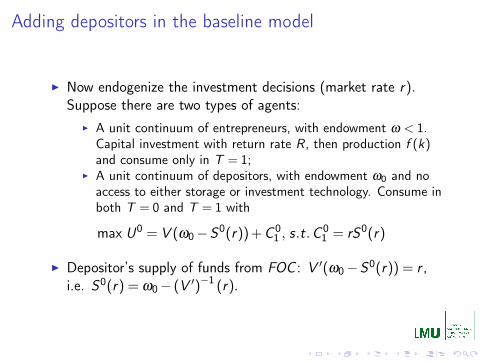

Adding depositors in the baseline model

I Now endogenize the investment decisions (market rate r).Suppose there are two types of agents:

I A unit continuum of entrepreneurs, with endowment ω < 1.Capital investment with return rate R, then production f (k)and consume only in T = 1;

I A unit continuum of depositors, with endowment ω0 and noaccess to either storage or investment technology. Consume inboth T = 0 and T = 1 with

max U0 = V (ω0−S0(r))+C 01 , s.t.C 0

1 = rS0(r)

I Depositor’s supply of funds from FOC : V ′(ω0−S0(r)) = r ,i.e. S0(r) = ω0− (V ′)−1 (r).

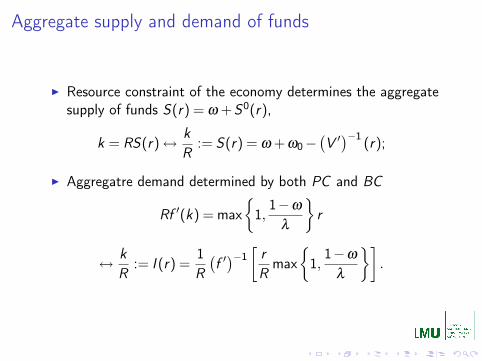

Aggregate supply and demand of funds

I Resource constraint of the economy determines the aggregatesupply of funds S(r) = ω +S0(r),

k = RS(r)↔ kR

:= S(r) = ω +ω0−(V ′

)−1(r);

I Aggregatre demand determined by both PC and BC

Rf ′(k) = max{

1,1−ω

λ

}r

↔ kR

:= I (r) =1R

(f ′

)−1[

rR

max{

1,1−ω

λ

}].

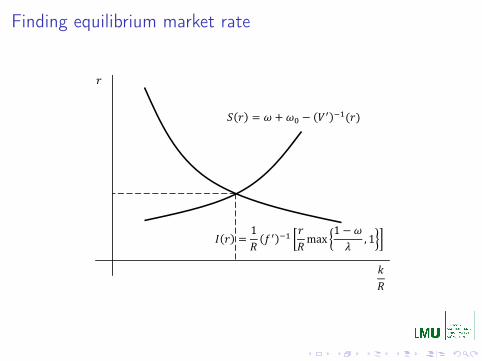

Finding equilibrium market rate

1

1max

1, 1

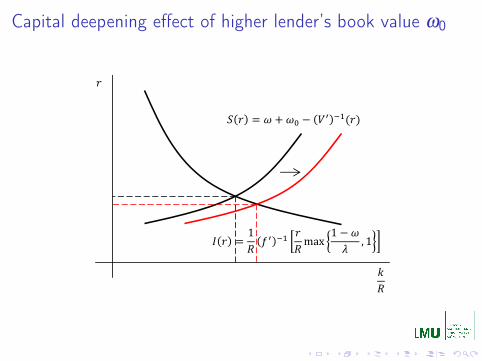

Capital deepening effect of higher lender’s book value ω0

1max

1, 1

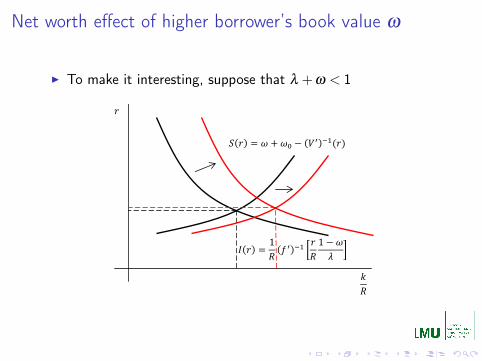

Net worth effect of higher borrower’s book value ω

I To make it interesting, suppose that λ +ω < 1

1max

1, 1

1 1

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

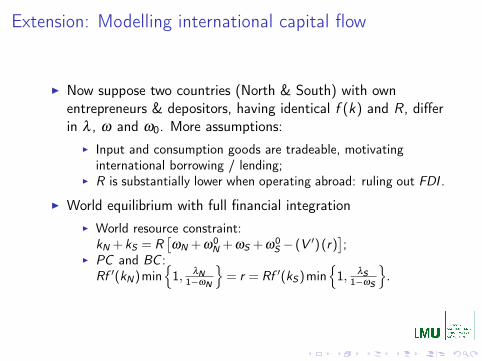

Extension: Modelling international capital flow

I Now suppose two countries (North & South) with ownentrepreneurs & depositors, having identical f (k) and R , differin λ , ω and ω0. More assumptions:

I Input and consumption goods are tradeable, motivatinginternational borrowing / lending;

I R is substantially lower when operating abroad: ruling out FDI .

I World equilibrium with full financial integrationI World resource constraint:

kN +kS = R[ωN +ω0

N +ωS +ω0S − (V ′)(r)

];

I PC and BC :Rf ′(kN)min

{1, λN

1−ωN

}= r = Rf ′(kS)min

{1, λS

1−ωS

}.

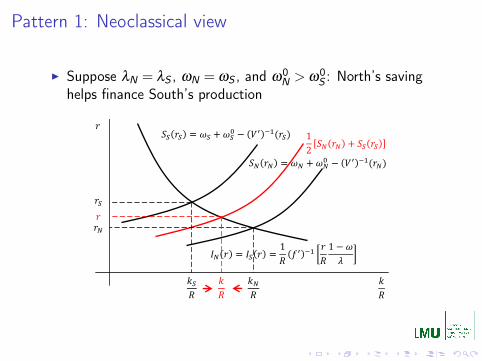

Pattern 1: Neoclassical view

I Suppose λN = λS , ωN = ωS , and ω0N > ω0

S : North’s savinghelps finance South’s production

1 1

12

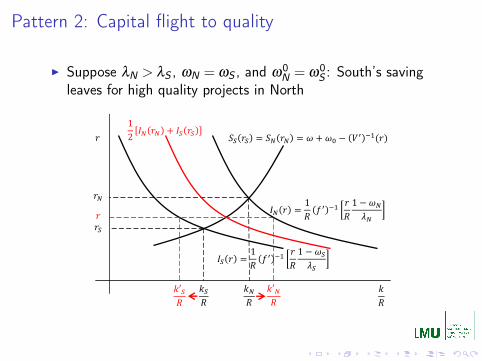

Pattern 2: Capital flight to quality

I Suppose λN > λS , ωN = ωS , and ω0N = ω0

S : South’s savingleaves for high quality projects in North

1 1

12

1 1

12

1 1

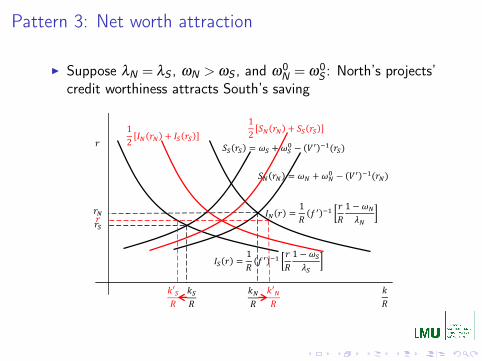

Pattern 3: Net worth attraction

I Suppose λN = λS , ωN > ωS , and ω0N = ω0

S : North’s projects’credit worthiness attracts South’s saving

1 1

12

1 1

12

Outline

MotivationBridging finance towards macroWhat’s new

Static Partial Equilibrium ModelsHomogeneous agentsHeterogeneous agentsMore complicated cases

Static General Equilibrium ModelsA model with depositorsAn open economy extensionAn international trade extension

Extension: Modelling international trade

I Consider two countries (North & South) involved in tradingconsumption goods: A continuum of tradeable consumptiongoods indexed by z ∈ [0,1];

I In each country, unit mass homogeneous agents each endowed

with ω < 1 labor, utility from consumption: U =(∫ 1

0 zεdz) 1

ε

;

I z are produced in the projects run by some of the agents(entrepreneurs)

I Each agent runs at most one project;I Each project in sector z converts unit labor into R units z .

I Threshold value: An entrepreneur has to hire 1−ω labor atmarket wage rate w from the workers. No flow of labor.

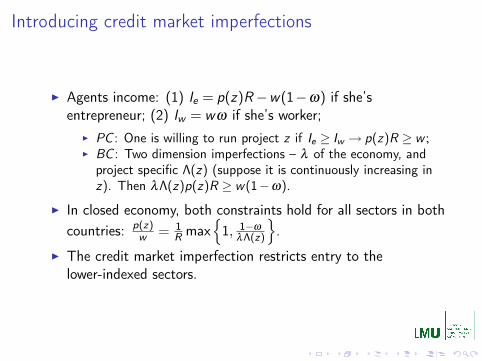

Introducing credit market imperfections

I Agents income: (1) Ie = p(z)R−w(1−ω) if she’sentrepreneur; (2) Iw = wω if she’s worker;

I PC : One is willing to run project z if Ie ≥ Iw → p(z)R ≥ w ;I BC : Two dimension imperfections – λ of the economy, and

project specific Λ(z) (suppose it is continuously increasing inz). Then λΛ(z)p(z)R ≥ w(1−ω).

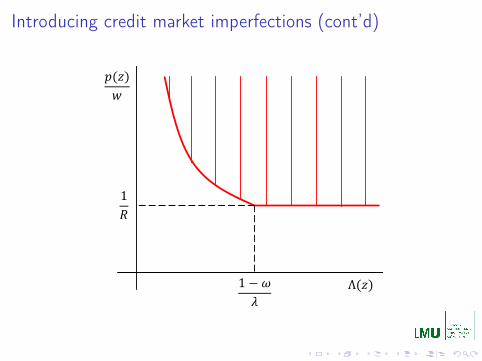

I In closed economy, both constraints hold for all sectors in bothcountries: p(z)

w = 1R max

{1, 1−ω

λΛ(z)

}.

I The credit market imperfection restricts entry to thelower-indexed sectors.

Introducing credit market imperfections (cont’d)

1 1

12

1 1

12

1

1

Λ

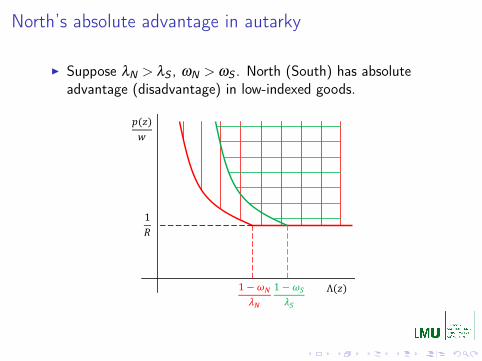

North’s absolute advantage in autarky

I Suppose λN > λS , ωN > ωS . North (South) has absoluteadvantage (disadvantage) in low-indexed goods.

1

1

Λ1

Comparative advantage in international trade

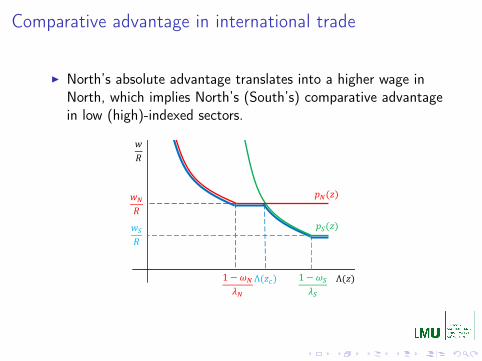

I North’s absolute advantage translates into a higher wage inNorth, which implies North’s (South’s) comparative advantagein low (high)-indexed sectors.

1

1

Λ1

1

Λ1Λ

Summary

I What have we done so far? Static modelsI Modelling credit market imperfections. Key factors: λ –

measure of imperfection; ω – net worth;I Market economy fails to allocate the credit to its most

productive use;I Net worth / balance sheet conditions play crucial roles in

allocating the credit.

I Partial equilibrium models with homo- / heterogeneous agents;I General equilibrium models with open economy extensions.

I To be discussed next time: Dynamic modelsI Models with homo. agents: Persistence, volatility, and growth;I Models with hetero. agents: (Open economy) extensions.

For Further Reading... I

Hart, O. and J. MooreA theory of debt based on the inalienability of human capital.Quarterly Journal of Economics, 109, 841–879, 1994.

Matsuyama, K.Aggregate implications of credit market imperfections.in D. Acemoglu, K. Rogoff, and M. Woodford. (eds.)NBER Macroeconomics Annual 2007.Cambridge: MIT Press, 2008.

Agion, P. and A. BenerjeeVolatility and Growth (Clarendon Lectures in Economics)New York: Oxford University Press, 2005.