the manitowoc company, inc.s21.q4cdn.com/264200883/files/doc_presentations/2016/nov/... ·...

TRANSCRIPT

The Manitowoc Company, Inc.

INVESTOR DAY

NOVEMBER 10, 2016

2INVESTOR DAY

NOVEMBER 10, 2016

Safe Harbor Statement

Any statements contained in this presentation that are not historical facts are “forward-looking statements.” These statements are based on the current expectations of the management of the company, only speak as of the date on which they are made, and are subject to uncertainty and changes in circumstances.

We undertake no obligation to update or revise forward-looking statements, whether as a result of new information, future events, or otherwise. Forward-looking statements include, without limitation, statements typically containing words such as “intends,” “expects,” “anticipates,” “targets,” “estimates,” and words of similar import. By their nature, forward-looking statements are not guarantees of future performance or results and involve risks and uncertainties because they relate to events and depend on circumstances that will occur in the future.

There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by such forward-looking statements. These factors include, but are not limited to, those relating to revenue growth of the company, future market strength of the company’s business segments and products, market acceptance of existing products and new product introductions and technology, economic conditions, successful acquisitions, manufacturing and facility utilization efficiencies, risks relating to actions of activist shareholders, and other factors listed in the company’s preliminary offering circular with respect to the notes, dated May 5, 2016. Any “forward-looking statements” in this presentation are intended to qualify for the safe harbor from liability under the Private Securities Litigation Reform Act of 1995.

3INVESTOR DAY

NOVEMBER 10, 2016

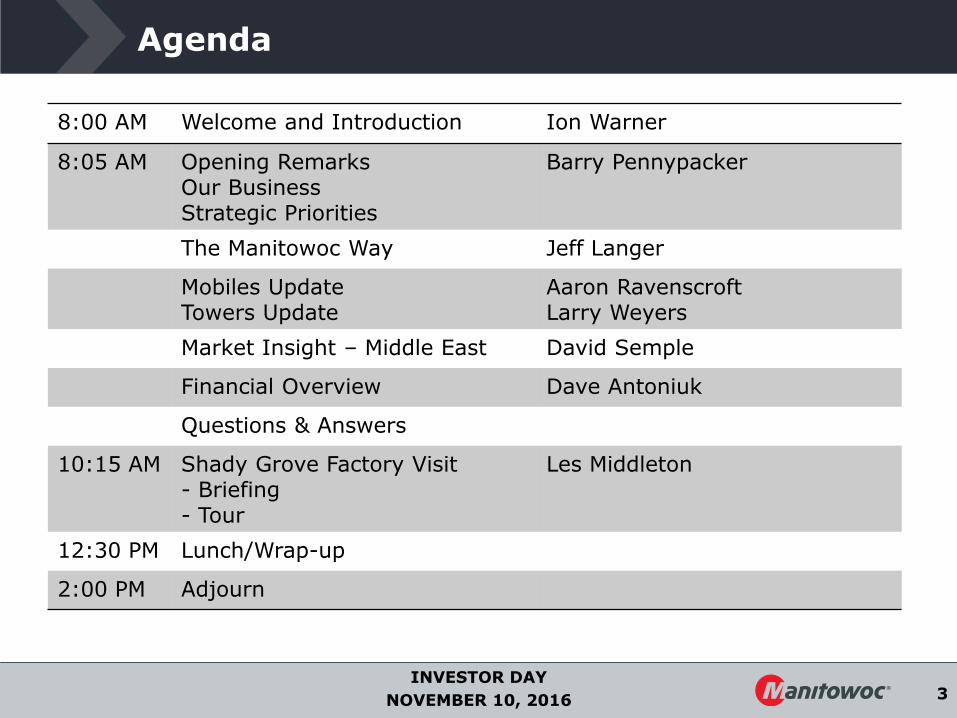

Agenda

8:00 AM Welcome and Introduction Ion Warner

8:05 AM Opening RemarksOur BusinessStrategic Priorities

Barry Pennypacker

The Manitowoc Way Jeff Langer

Mobiles UpdateTowers Update

Aaron RavenscroftLarry Weyers

Market Insight – Middle East David Semple

Financial Overview Dave Antoniuk

Questions & Answers

10:15 AM Shady Grove Factory Visit- Briefing- Tour

Les Middleton

12:30 PM Lunch/Wrap-up

2:00 PM Adjourn

4INVESTOR DAY

NOVEMBER 10, 2016

President & Chief Executive OfficerBarry Pennypacker

5INVESTOR DAY

NOVEMBER 10, 2016

Investment Highlights

Leading Global Crane Manufacturer with industry-leading innovations

Well-positioned to capitalize on opportunities when market improves

Unique aftermarket support drives recurring revenue

Geographically diverse customer and end market base

Executing on strategic priorities to improve margins, earnings, and cash flow

New, Operationally-Focused Team Driving Results

Early stages of transformation to a high quality, higher margin crane company compared to peers

6INVESTOR DAY

NOVEMBER 10, 2016

MTW Summary

• Global leader in lifting equipment

• Serve wide range of end markets

• Broadest product and service offering

• Innovation leader

• Global channel and reach

• Aftermarket solutions

• Financing solutions

Leading crane manufacturer

7INVESTOR DAY

NOVEMBER 10, 2016

Leading Global Crane Company with Well-Known Brands

Government Municipal

All Terrain

Rough Terrain

Truck Mounted

Industrial

Telecrawler

Self Erecting Tower

Top Slewing Tower

Lattice Boom Crawler

Boom Truck

Top Slewing Tower

8INVESTOR DAY

NOVEMBER 10, 2016

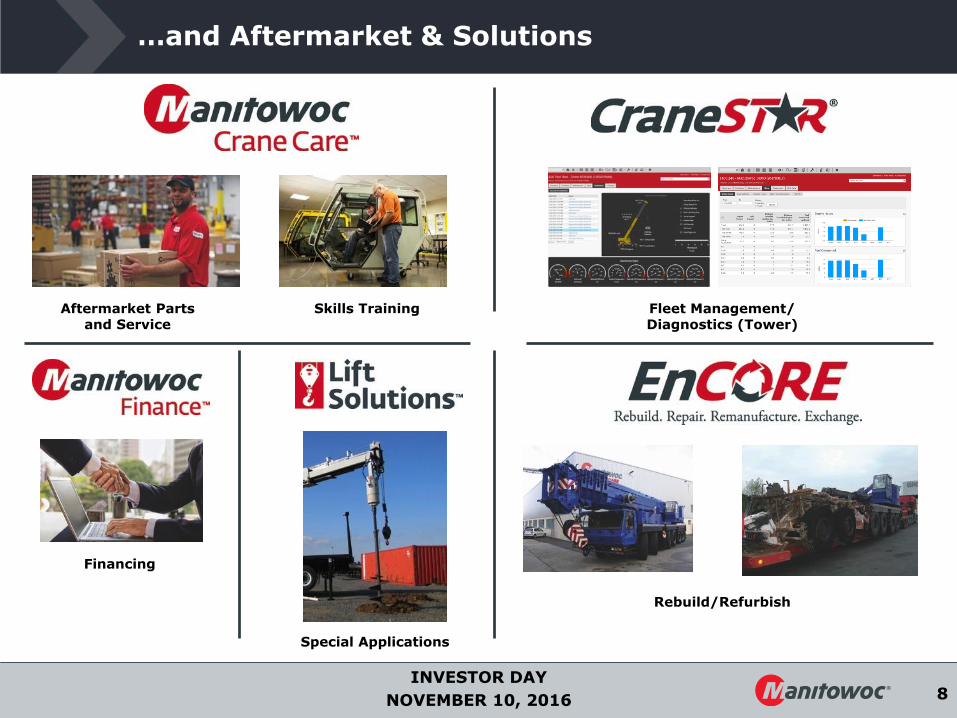

…and Aftermarket & Solutions

Aftermarket Parts and Service

Skills Training

Financing

Rebuild/Refurbish

Special Applications

Fleet Management/Diagnostics (Tower)

9INVESTOR DAY

NOVEMBER 10, 2016

Diversified End Markets and Global

Geographic Exposure

End Markets 1

Americas52%

APAC12%

EMEA36%

1 Includes new equipment sales only.

Growth DriversIndustrial /

Petrochemical35%

Power / Utilities18%

Commercial25%

Residential5%

Infrastructure17%

• Leading brands and products

• Strong distribution channels globally

• Products for wide range of end markets

• Large installed base

• Aftermarket opportunities

• Need for increased lifting capacity and performance

• Energy sector recovery

• Alternative energy sources – e.g., Wind

• Infrastructure investment

10INVESTOR DAY

NOVEMBER 10, 2016

Situational Analysis -- Mobiles

• Uncertainty on industry trough

• Depressed energy markets

• Infrastructure investments

• Lower resale values

• Lower rental rates

• Lower utilization rates

Summary

Persistently weak market conditions; Looking for signs of stabilization

11INVESTOR DAY

NOVEMBER 10, 2016

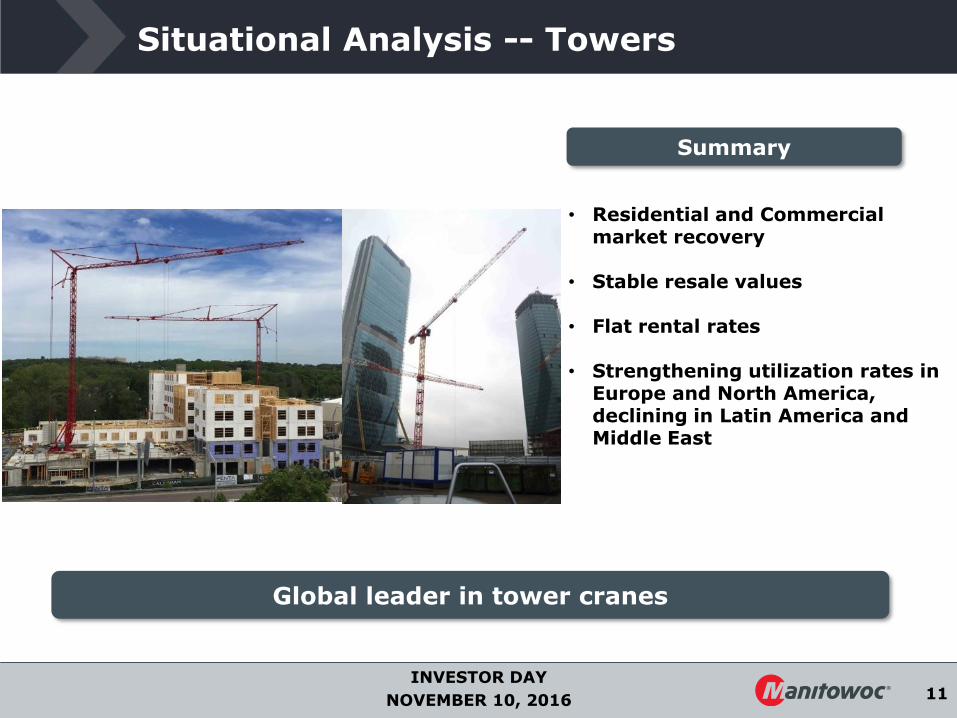

Situational Analysis -- Towers

Summary

Global leader in tower cranes

• Residential and Commercial market recovery

• Stable resale values

• Flat rental rates

• Strengthening utilization rates in Europe and North America, declining in Latin America and Middle East

12INVESTOR DAY

NOVEMBER 10, 2016

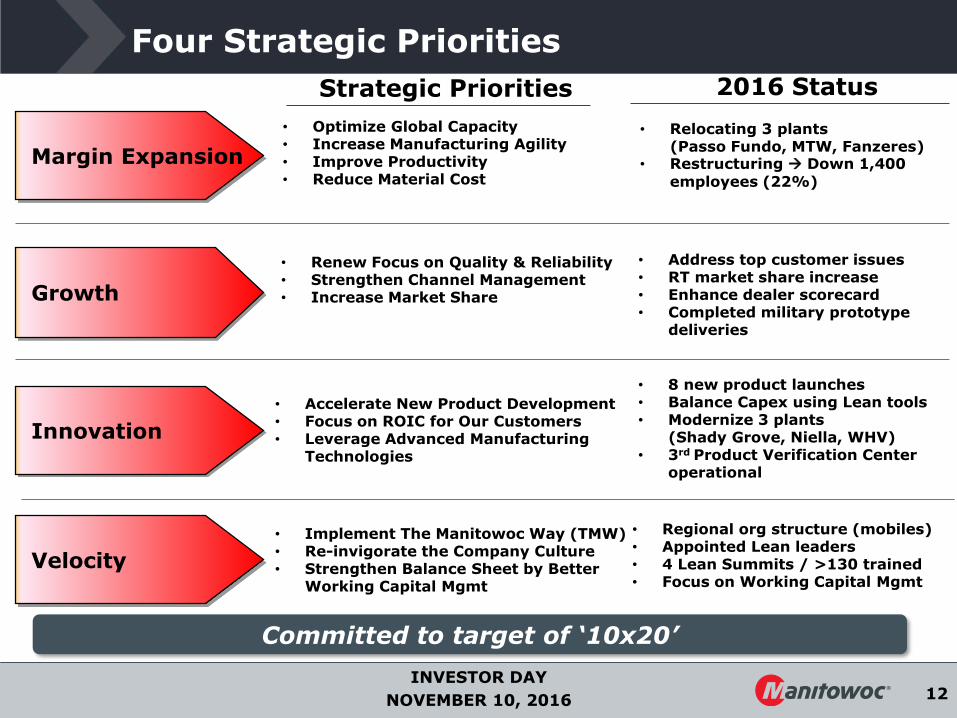

Four Strategic Priorities

• Renew Focus on Quality & Reliability• Strengthen Channel Management• Increase Market Share

• Optimize Global Capacity • Increase Manufacturing Agility• Improve Productivity• Reduce Material Cost

• Accelerate New Product Development• Focus on ROIC for Our Customers• Leverage Advanced Manufacturing

Technologies

Margin Expansion

Growth

Innovation

Velocity

• Implement The Manitowoc Way (TMW)• Re-invigorate the Company Culture• Strengthen Balance Sheet by Better

Working Capital Mgmt

Strategic Priorities 2016 Status

• Address top customer issues• RT market share increase• Enhance dealer scorecard• Completed military prototype

deliveries

• Relocating 3 plants (Passo Fundo, MTW, Fanzeres)

• Restructuring Down 1,400

employees (22%)

• 8 new product launches• Balance Capex using Lean tools• Modernize 3 plants

(Shady Grove, Niella, WHV)• 3rd Product Verification Center

operational

• Regional org structure (mobiles)• Appointed Lean leaders• 4 Lean Summits / >130 trained• Focus on Working Capital Mgmt

Committed to target of ‘10x20’

13INVESTOR DAY

NOVEMBER 10, 2016

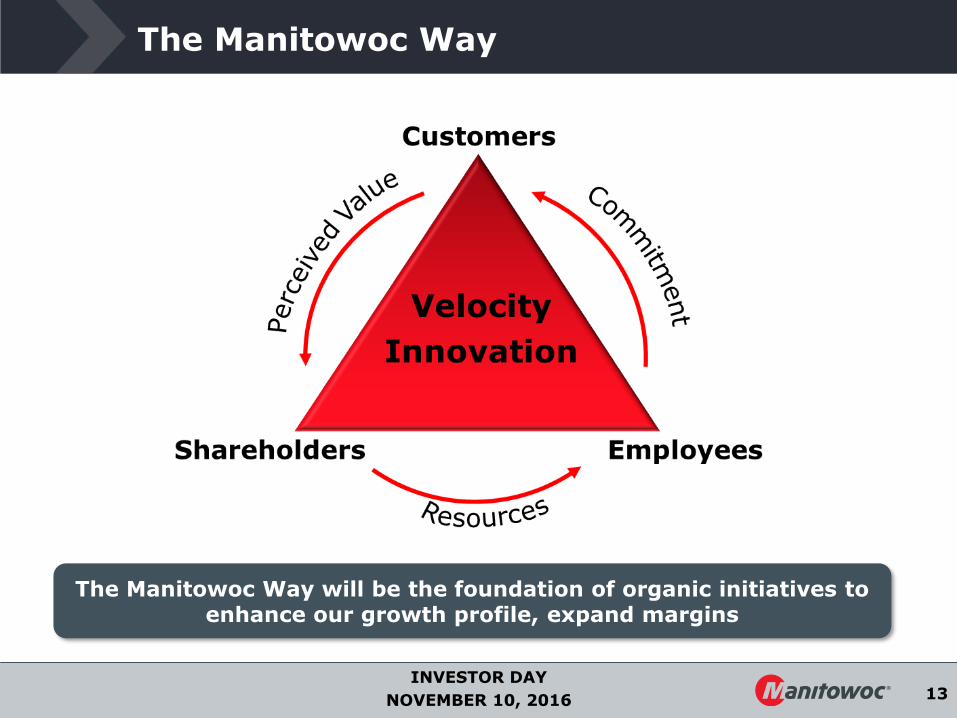

The Manitowoc Way

The Manitowoc Way will be the foundation of organic initiatives to enhance our growth profile, expand margins

14INVESTOR DAY

NOVEMBER 10, 2016

Vice President, The Manitowoc WayJeff Langer

15INVESTOR DAY

NOVEMBER 10, 2016

The Manitowoc Way – Strategy Lean

Corporate StrategicObjectives (CSO)

Strategic Plan(STRAP)

Identify CriticalValue Streams

Value Stream Mapping (VSM)

Current StateFuture StateAction Plan

KaizenSchedule

• Tracked by Priority Deployment(PD)

• Material & Info Flow

• Value Add vs Non-Value Add (VA/NVA) Ratio

• What is critical to the Customer

• Identify Opportunities

• Prioritize Based on Results

STRATEGIC CONTINUOUS IMPROVEMENT

16INVESTOR DAY

NOVEMBER 10, 2016

The Manitowoc Way – 2016 Implementation Plan

• Each Facility will appoint a dedicated Manitowoc Way champion

• Executive Staff members will participate in two Major Kaizen activities per year

• Develop The Manitowoc Way portal site

Publish the Kaizen schedules for each facility Training document library Templates/Forms Contact lists Lessons Learned

17INVESTOR DAY

NOVEMBER 10, 2016

The Manitowoc Way In Action – Site Leaders

The Towers Team

Dave SawyerMobile – SG, USA

Matthias DreierMobile – WHV, Germany

An experienced team with over 75 years of service

Lionel Vroman – Charlieu, Manuel Castro –Baltar, Bertrand Depale – Moulins, Diego Marabotto – Niella, Chunyu Ma - APAC

18INVESTOR DAY

NOVEMBER 10, 2016

The Manitowoc Way In Action – Training Summits

Niella, Italy September 14-1644 Participants

Wilhelmshaven, Germany September 19-2133 Participants

* Not Pictured: Shady Grove, PA August 16-18

25 Participants

Shady Grove, PA June 7-929 Participants

19INVESTOR DAY

NOVEMBER 10, 2016

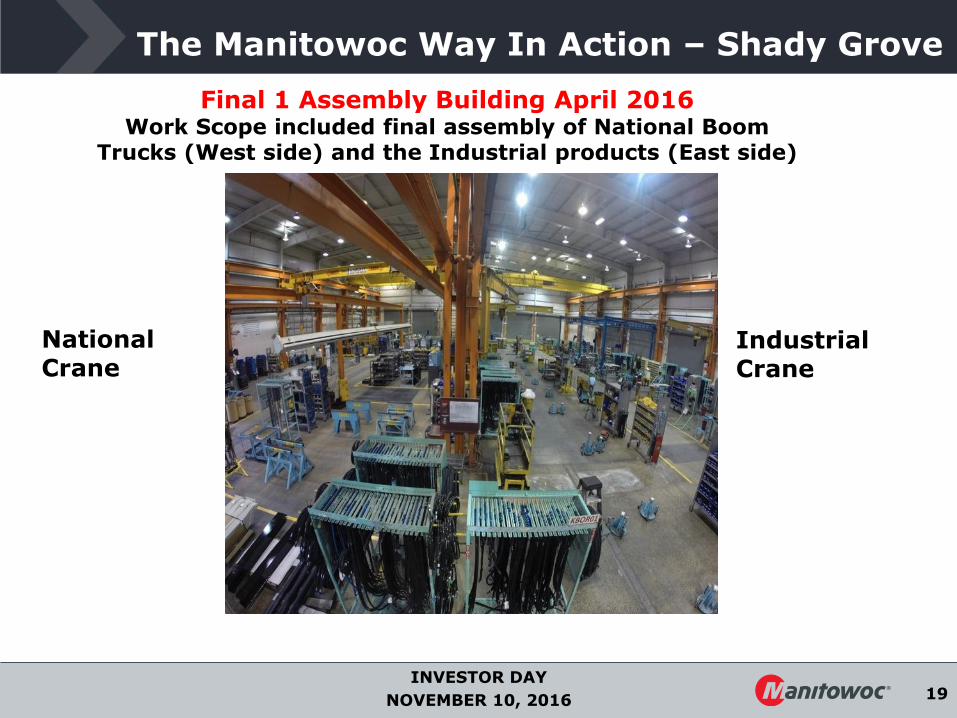

The Manitowoc Way In Action – Shady Grove

Final 1 Assembly Building April 2016Work Scope included final assembly of National Boom

Trucks (West side) and the Industrial products (East side)

National Crane

Industrial Crane

20INVESTOR DAY

NOVEMBER 10, 2016

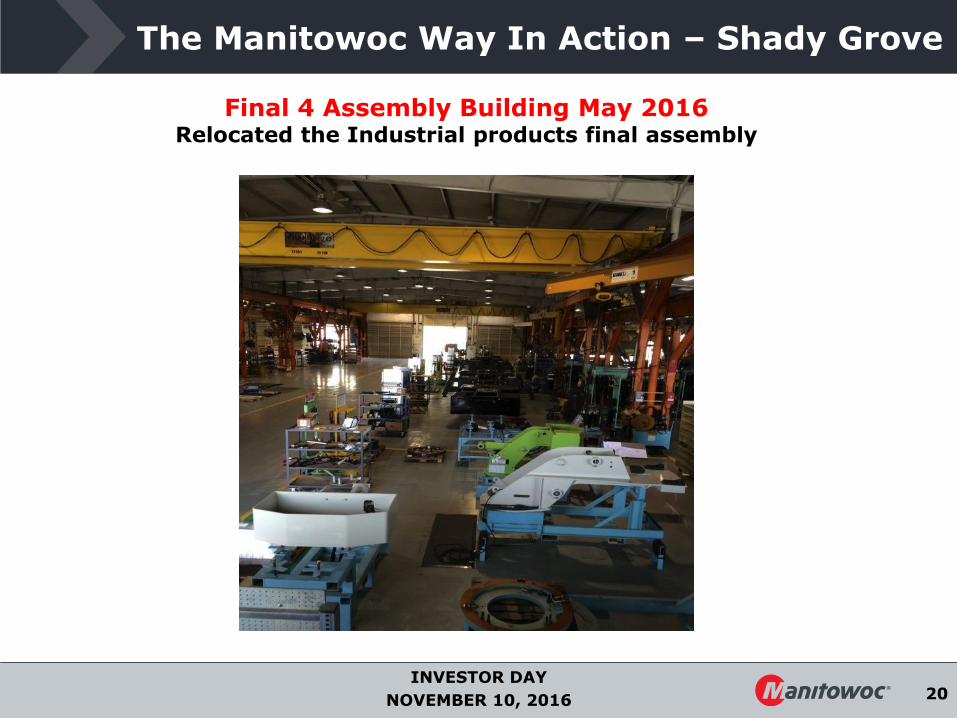

The Manitowoc Way In Action – Shady Grove

Final 4 Assembly Building May 2016Relocated the Industrial products final assembly

21INVESTOR DAY

NOVEMBER 10, 2016

The Manitowoc Way In Action – Shady Grove

Final 2 Assembly Building April 2016TM final assembly with 8 work Stations

Final 1 Assembly Building May 2016Consolidated the TM final assembly from 8 to 4 work stations and relocated it from F2 to F1

Assembly line moves freed up approximately 24,000 sq ft

22INVESTOR DAY

NOVEMBER 10, 2016

The Manitowoc Way In Action – Wilhelmshaven, Germany

Hall 9, Paint shop improvements

Before After

Hall 13, Boom Assembly

23INVESTOR DAY

NOVEMBER 10, 2016

Executive Vice President, MobilesAaron Ravenscroft

24INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Overview

Carrydeck

All-Terrain

Boom Truck

Rough-Terrain

Crawler

Truck-Mounted

25INVESTOR DAY

NOVEMBER 10, 2016

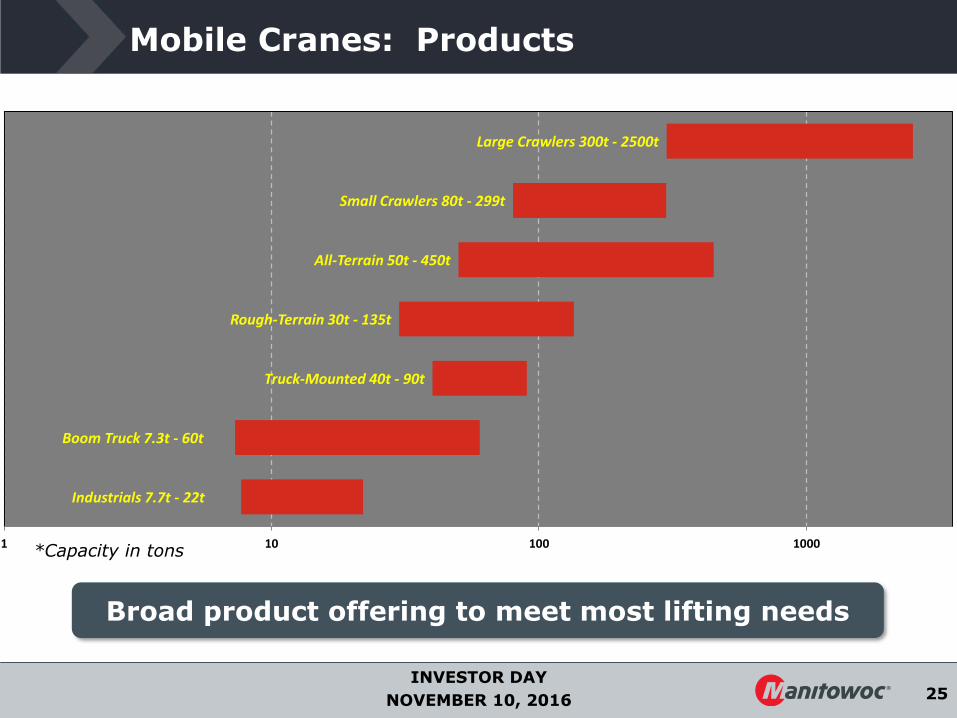

Mobile Cranes: Products

*Capacity in tons

Broad product offering to meet most lifting needs

Industrials 7.7t - 22t

Boom Truck 7.3t - 60t

Truck-Mounted 40t - 90t

Rough-Terrain 30t - 135t

All-Terrain 50t - 450t

Small Crawlers 80t - 299t

Large Crawlers 300t - 2500t

1 10 100 1000

26INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Lift Solutions

Boom Dollies

Hitches

Track Units

Ringers

External generators

Personnel baskets

Boom extensions, attachments, & inserts

Barge Applications

27INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Manufacturing

• Founded 1947

• 300+ acres

• 1.3 million square feet

• Manufacture rough-terrain,truck-mounted, boom trucks, industrials, and crawler cranes

• Capability: R&D, welding, machining, assembly, testing

• Founded 1946

• 50+ acres

• 410,000 square feet

• Manufacture all-terrain cranes

• Capability: R&D, welding, assembly, testing

Shady Grove, Pennsylvania Wilhelmshaven, Germany

28INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Market

North America• Weak demand, lower

rental rates, lower utilization rates

APAC• India: fragile demand• SE Asia: slowing down• ANZ: Modest signs of

improvement

Europe • Germany & France stable• UK stable• Southern EU: slight

recovery

Middle East• KSA: liquidity crisis/

Other conflicts • Region: Geopolitical

instability

Africa• Flat to declining demand

LATAM• Depression-like market

29INVESTOR DAY

NOVEMBER 10, 2016

Mobile Strategy

Strategic Priorities

1. Margin Expansion

2. Growth

3. Innovation

4. Velocity

• Optimize Manufacturing footprint• Increase Manufacturing Agility• Reduce Material cost

• Sales Channel Expansion• Aftermarket growth and expansion• Increase Market share via new products

• IPD• Implement the Manitowoc Way• Safety < 1 RIR

• Accelerate New Product Development• Focus on ROIC for our Customers• Leverage advanced manufacturing technologies

30INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Margin Expansion

• Intent to relocate from Manitowoc, WI to Shady Grove, PA

• Completion: year end 2016

• Cross-functional task force in place to implement plan

Crawler plant relocation

• Annualized pre-tax cost savings: $25-30M

• Cash outflows: $35-50M• Non-cash charges:

Approx. $95-100M

31INVESTOR DAY

NOVEMBER 10, 2016

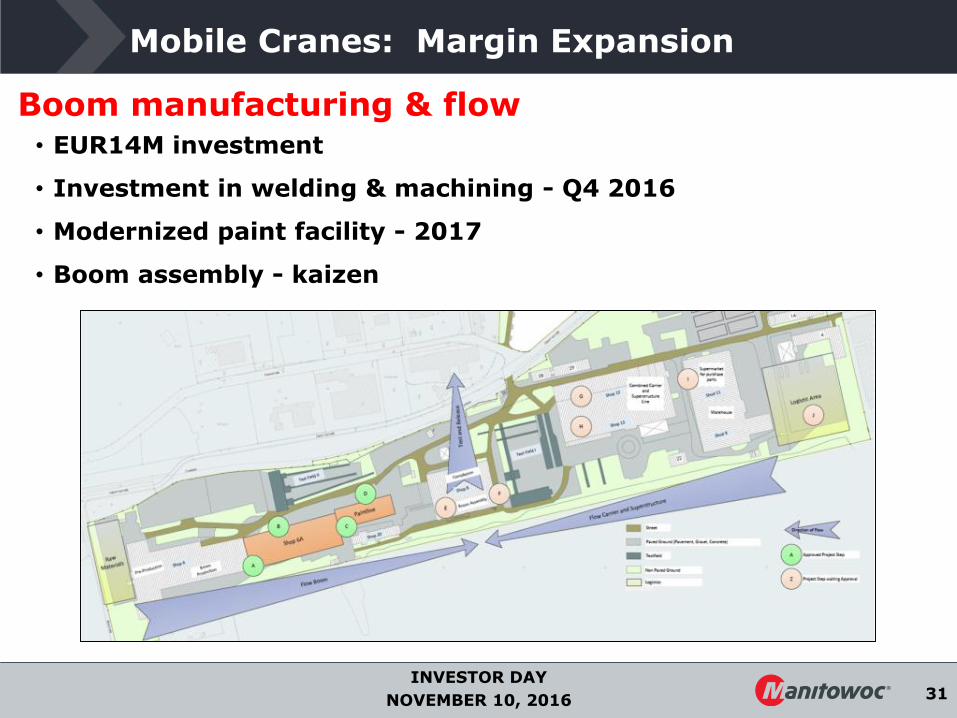

Mobile Cranes: Margin Expansion

• EUR14M investment

• Investment in welding & machining - Q4 2016

• Modernized paint facility - 2017

• Boom assembly - kaizen

Boom manufacturing & flow

32INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Growth

GMK4060HC

• $192M/5 years; total $270M with 2-year option exercised

• 3 Prototypes completed in Q3 2016

• Government testing starts Nov. 2016

• First production shipments Q4 2017

• Yearly production of 20 units starting 2018

• Long-term aftermarket parts revenue

AT422T Service Life Extension Program (SLEP)

• Pilot Build of 4 Cranes Complete

• Production area ready Q3 2017

• Shipments start Q4 2017

• Estimate 60 Units Delivered Annually

• $75-100M potential

Military

Unique Defense Opportunity

33INVESTOR DAY

NOVEMBER 10, 2016

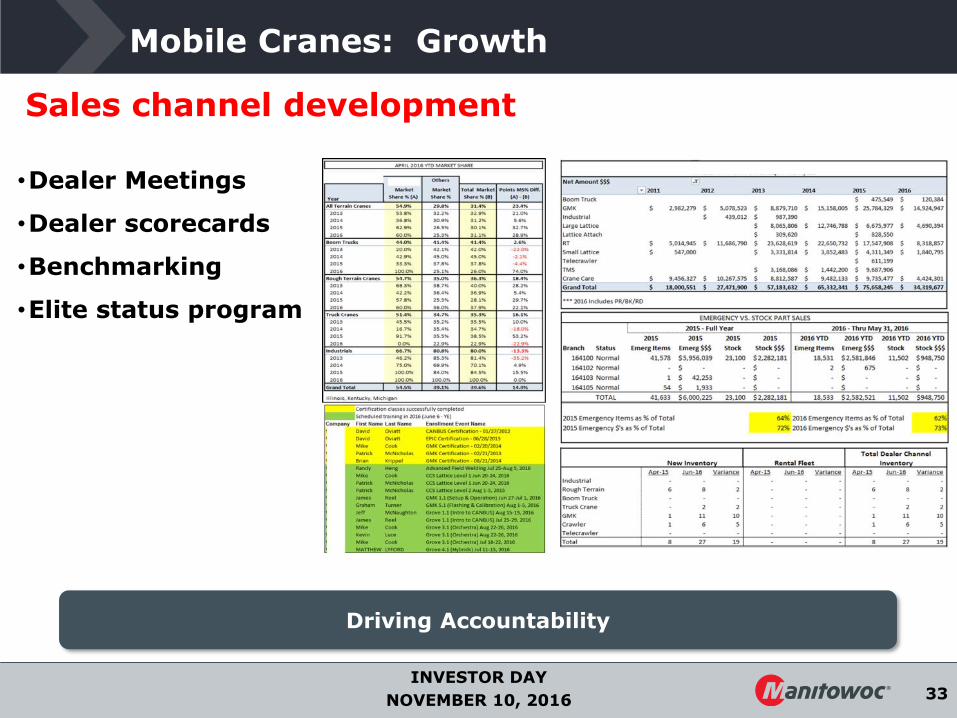

Mobile Cranes: Growth

Driving Accountability

•Dealer Meetings

•Dealer scorecards

•Benchmarking

•Elite status program

Sales channel development

34INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Innovation

New Products Drive Market Share Growth

GMK4100L-1

GMK5150/5150L

GMK5250L

New Product Initiatives• “Taxi” strategy

• Class-leading load charts

• Crane Control System (CCS)

• MEGATRAK suspension system

• Better maneuverability and fuel economy with VIAB turbo clutch and integrated retarder

• Meets global roading needs

35INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Innovation

New Products Drive Market Share Growth

New Product Initiatives

• Global product strategy

• Greater capacity than competitors – up to 27%

• Full-power booms & best-in-class line pulls

• Crane Control System (CCS)

• Broad jib options; new stowage systems

GRT880

GRT8100

“New” Models

36INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Velocity

The Team is Accountable & Responsible

IPD process – New mobile crane

• Designated team of 10

• Streamlined IPD process

• VOC – 3 crane operators involved in process

• Goal: class-leading capacity, boom, and load charts

• Launch: ConExpo 2017

37INVESTOR DAY

NOVEMBER 10, 2016

Mobile Cranes: Velocity

• Dedicated Manitowoc Way leaders appointed at each facility

• Executive Staff members will participate in two Major Kaizen activities per year

• The Manitowoc Way portal site

The Manitowoc Way

The Team is Accountable & Responsible

38INVESTOR DAY

NOVEMBER 10, 2016

Executive Vice President, TowersLarry Weyers

39INVESTOR DAY

NOVEMBER 10, 2016

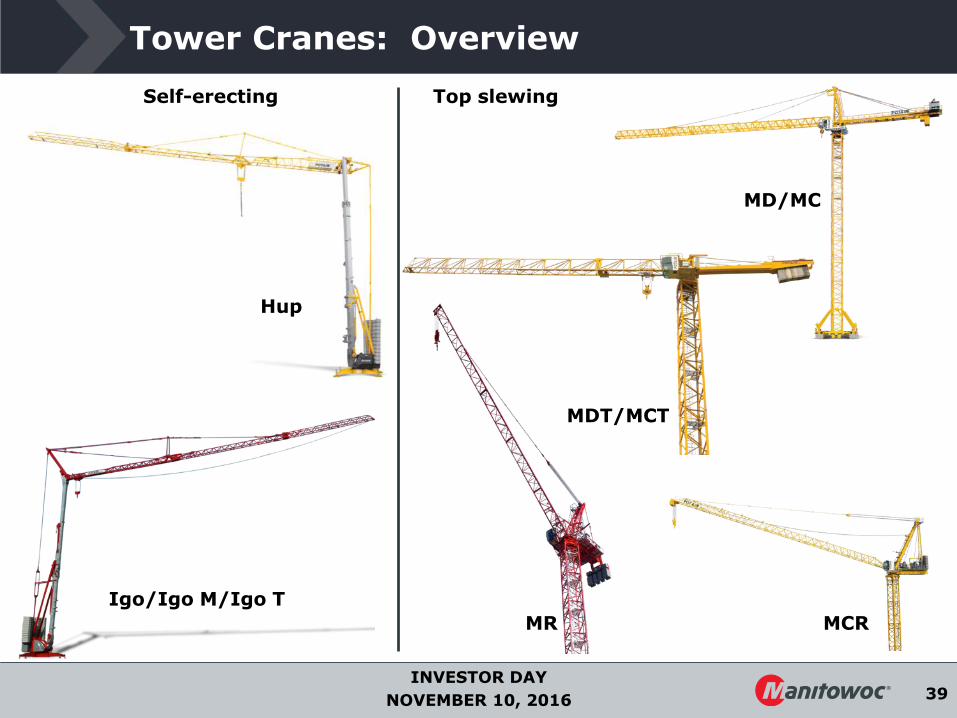

Tower Cranes: Overview

Igo/Igo M/Igo T

Hup

MD/MC

MDT/MCT

MCRMR

Self-erecting Top slewing

40INVESTOR DAY

NOVEMBER 10, 2016

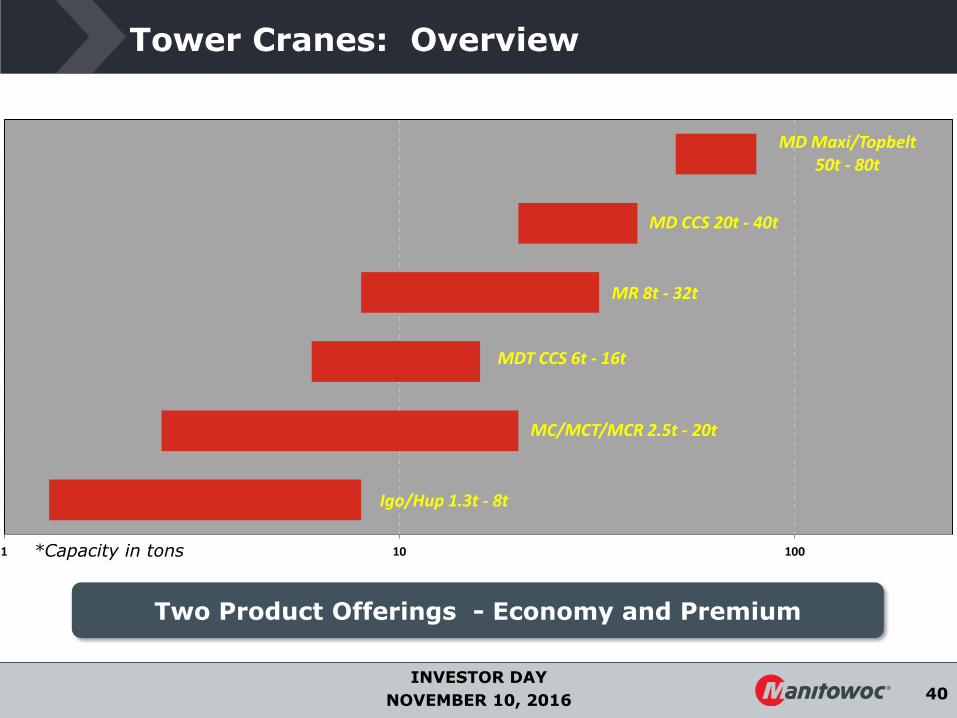

Tower Cranes: Overview

*Capacity in tons

Two Product Offerings - Economy and Premium

Igo/Hup 1.3t - 8t

MC/MCT/MCR 2.5t - 20t

MDT CCS 6t - 16t

MR 8t - 32t

MD CCS 20t - 40t

MD Maxi/Topbelt50t - 80t

1 10 100

41INVESTOR DAY

NOVEMBER 10, 2016

…with Special Applications

Broad product offering for a variety of applications

Internal climbing Anchorages

Dam and bridge construction

42INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Manufacturing

Charlieu, France• 323,000 square feet• Large self erecting cranes • Hoist and mechanism feeder plant• EnCORE rebuild business

Baltar, Portugal• 121,000 square feet• MDT City class tower cranes• EnCORE rebuild business• Used cranes

Moulins, France• 370,000 square feet• Large MD Top slewing cranes• Large MDT topless tower cranes• Large MR luffing towers

Niella Tanaro, Italy• 258,000 square feet• All small self erecting cranes

(HUP)

Zhangiagang, China• 547,000 square feet• MC , MCT and MCR economy line of top

slewing tower cranes• MD1100 & MD1600 specialized cranes

Pune, India• 169,000 square feet• MC range of economy cranes for

India Market

43INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Market

Americas• NA: modest increase,

higher utilization rates• Brazil: depressed• LATAM: impacted by

Brazil slowdown

APAC• China: depressed• S. Korea: high activity• Rest of Asia: growing

Europe• Germany, France: growing

and increasing market share with CCS intro

• Central Europe: slight growth• CIS: activity recovering but

financing remains difficult

Middle East• GCC: slowing down due

to lack of financing• Other: Declining demand

Africa• Declining demand in

some countries, mainly impacting Chinese manufacturers

44INVESTOR DAY

NOVEMBER 10, 2016

Tower Strategy

Strategic Priorities

1. Margin Expansion

2. Growth

3. Innovation

4. Velocity

• Optimize Manufacturing footprint• Increase Manufacturing Agility• Product line rationalization

• Increase Market share via new products• Aftermarket growth and expansion• Used and Crane Rental business• Sales Channel Expansion

• Accelerate New Product Development• Leverage advanced manufacturing

technologies

• IPD• Implement the Manitowoc Way• Safety < 1 RIR

45INVESTOR DAY

NOVEMBER 10, 2016

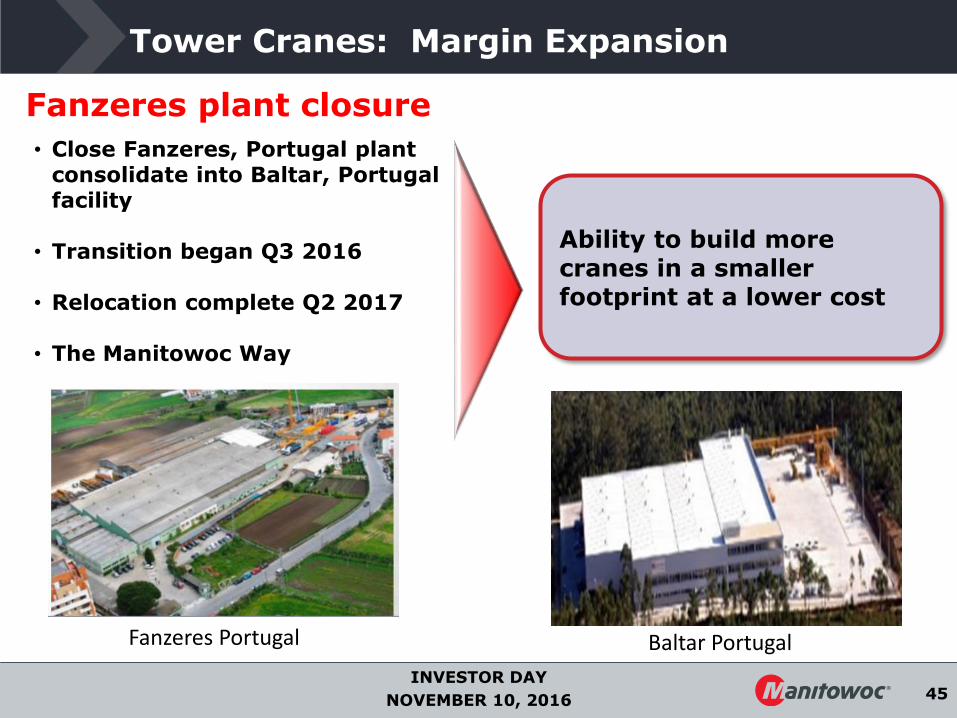

Tower Cranes: Margin Expansion

• Close Fanzeres, Portugal plant consolidate into Baltar, Portugal facility

• Transition began Q3 2016

• Relocation complete Q2 2017

• The Manitowoc Way

Fanzeres plant closure

Ability to build more cranes in a smaller footprint at a lower cost

Baltar PortugalFanzeres Portugal

46INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Margin Expansion

Igo26 Igo30 Igo32 Igo36

6 to 2 models

HUP 32-27Q3 2016 Shipments

Igo42 Igo50

HUP 40-30Q4 2016 Shipments

Product line consolidation drives margin improvement

47INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Margin Expansion

Niella Tanaro, Italy - Transformation Complete

• Optimized material flow - improved VA:NVA ratio

• Modernized paint line w/ auto load system

• Higher productivity with less manpower

• 80% of chassis welding by robot

• Improved Safety

Advanced manufacturing

48INVESTOR DAY

NOVEMBER 10, 2016

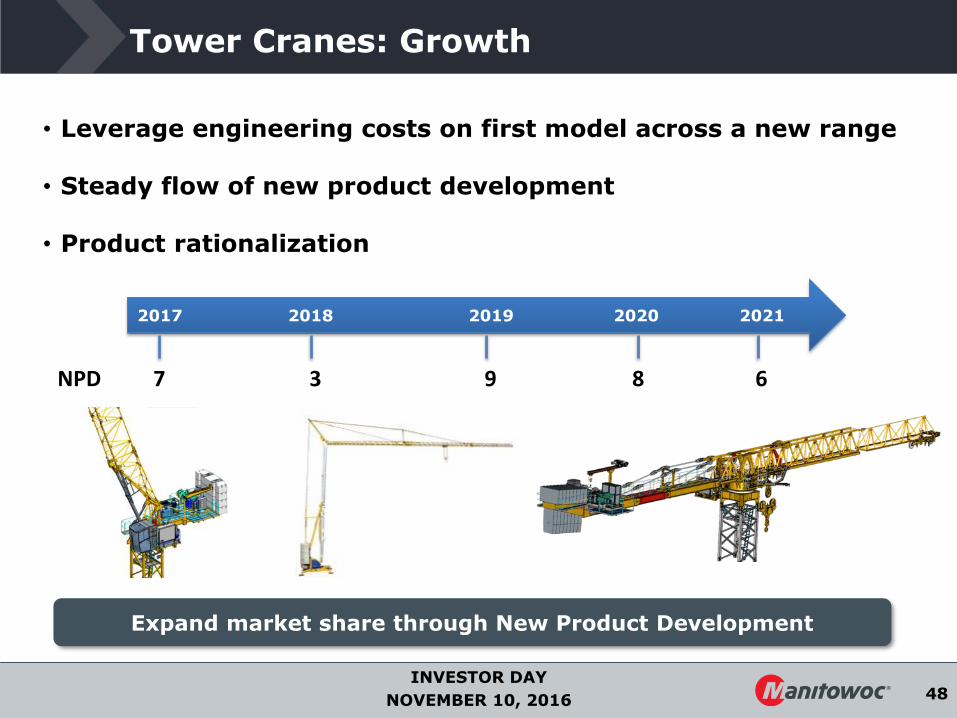

Tower Cranes: Growth

Expand market share through New Product Development

• Leverage engineering costs on first model across a new range

• Steady flow of new product development

• Product rationalization

2017 2018 2019 2020 2021

NPD 7 3 9 8 6

49INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Growth

Comprehensive service and support model and large install base

Aftermarket Growth• Complete value added support model

including crane erection, tie-off engineering, transport and anchorage design.

• Improvement of velocity and capability in service network via CraneStar DIAG and CCS. Diagnose the issue without sending a service technician

• Revenue opportunity from crane passenger lift requirement in Europe above 98 ftheight

• High fill rate driving increased parts sales and customer satisfaction

50INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Growth

Energize secondary market potential

• Reorganize resources to promote double digit growth

• Proactive purchasing

• Unique market positioning

Leverage EnCORE operations & partners

Optimize global sales network Strengthen warranty Tool to enter emerging markets

Used crane business

BEFORE

AFTER

51INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Innovation

Integrated Solution for Operator Lift Requirement

Cablift

• New regulations in France to require operator lift for all tower cranes erected above 98 ft high

• Patent pending integrated crane driver lift

• Replacing current access features (ladders and platforms)

• Used for Tower crane erection assistance and crane cabin access

• Internal vs external allowing higher erection heights

Innovative solution for both new and existing cranes

52INVESTOR DAY

NOVEMBER 10, 2016

Tower Cranes: Velocity

The Manitowoc Way – The foundation of our culture

Lean implementationLean implementation

• Dedicated Manitowoc Way leaders appointed at each facility

• Executive Staff members will participate in two Major Kaizen activities per year

• The Manitowoc Way portal site

53INVESTOR DAY

NOVEMBER 10, 2016

Vice President, Sales – Middle East and Asia PacificDavid Semple

54INVESTOR DAY

NOVEMBER 10, 2016

Middle East

55INVESTOR DAY

NOVEMBER 10, 2016

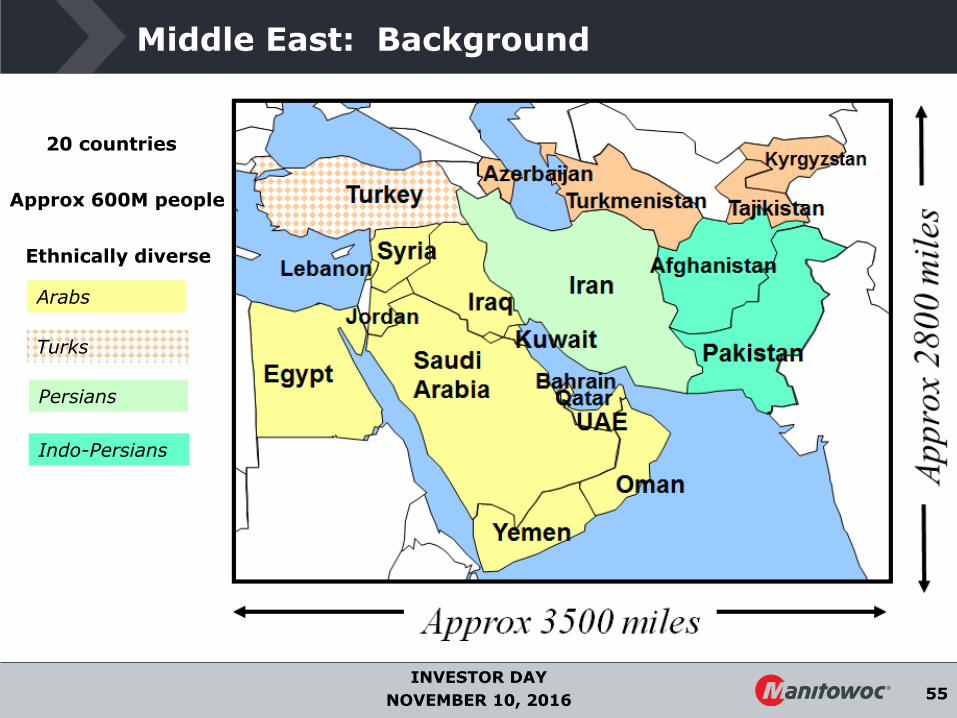

Middle East: Background

20 countries

Arabs

Turks

Persians

Indo-Persians

Ethnically diverse

Approx 600M people

56INVESTOR DAY

NOVEMBER 10, 2016

Middle East: Background

Cost to produce 1 barrel of oil

Source: UCube by Rystad Energy; Interactive published Nov. 23, 2015

$10 $20 $30 $40 $50

Extraction costs of oil from the Middle-East : 1/5 of the current oil price…

57INVESTOR DAY

NOVEMBER 10, 2016

Middle East: Background

0 50 100 150 200

SYRIA

BAHRAIN

YEMEN

PAKISTAN

TURKMENISTAN

AZERBAIJAN

EGYPT

OMAN

QATAR

KUWAIT

IRAQ

UAE

IRAN

SAUDI ARABIA

Billion USD

Yearly income potential from Oil & Gas(assuming $50/b for oil and $3/mBTU for gas)

income from Gas (Bn$/y)

income from Oil (Bn$/y)

* Saudi Arabia, UAE, Kuwait, Qatar, Iraq:

Total yearly O&G income~$450B

Less costs of extraction~$100B

Net ~$350B

*

*

*

*

*

Half of world’s oil reserves/one-third of world’s gas reserves

58INVESTOR DAY

NOVEMBER 10, 2016

2011 – 2012 – 2013 – 2014 – 2015 - 2016

Negative

Impact

on o

ur

busin

ess

Arab SpringEgypt, Bahrain, Yemen, Syria,

Peak impact late 2012

TurkeyGezi Park protestsSummer 2013

ISIS in parts of IraqSummer 2014

Saudi war in YemenQ1-2015

Dealing with « structural instability »

Saudi / Iran relationship ?

Middle East: Political Instability

59INVESTOR DAY

NOVEMBER 10, 2016

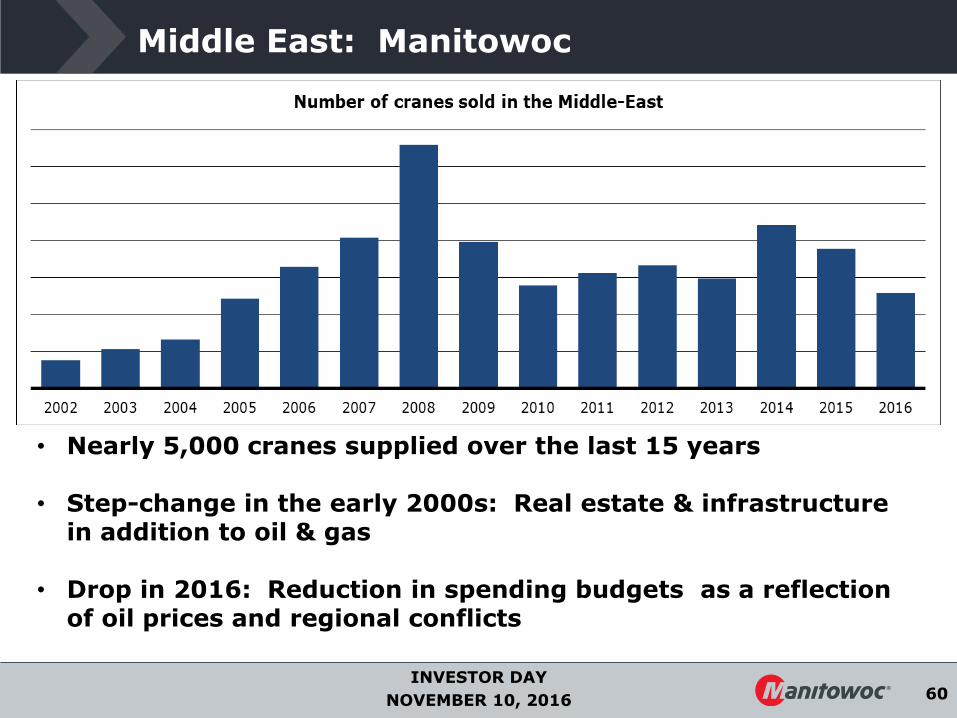

Middle East: Manitowoc

• Grove, Potain, & Manitowoc brands popular since the 1960s• 2007: Opened in Jebel Ali Free Zone, Dubai• 35 employees, ~ $200M of business in the region

60INVESTOR DAY

NOVEMBER 10, 2016

Middle East: Manitowoc

• Nearly 5,000 cranes supplied over the last 15 years

• Step-change in the early 2000s: Real estate & infrastructure in addition to oil & gas

• Drop in 2016: Reduction in spending budgets as a reflectionof oil prices and regional conflicts

61INVESTOR DAY

NOVEMBER 10, 2016

Middle East: Long-Term

62INVESTOR DAY

NOVEMBER 10, 2016

Middle East: Thank you !

63INVESTOR DAY

NOVEMBER 10, 2016

Senior Vice President & Chief Financial OfficerDave Antoniuk

64INVESTOR DAY

NOVEMBER 10, 2016

Finance Overview

New Operationally-Focused Leadership Team Driving Transformation

Ability to manage the cycle… contingency planning

Margin expansion commitment… “The Manitowoc Way”

Laser focus on cash… Disciplined working capital management

Role of Finance… Business partner, transparency, conservatism, balance sheet clean-up

Focused on Liquidity & Earnings Growth

65INVESTOR DAY

NOVEMBER 10, 2016

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1st

Qtr

-03

2n

d Q

tr-0

3

3rd

Qtr

-03

4th

Qtr

-03

1st

Qtr

-04

2n

d Q

tr-0

4

3rd

Qtr

-04

4th

Qtr

-04

1st

Qtr

-05

2n

d Q

tr-0

5

3rd

Qtr

-05

4th

Qtr

-05

1st

Qtr

-06

2n

d Q

tr-0

6

3rd

Qtr

-06

4th

Qtr

-06

1st

Qtr

-07

2n

d Q

tr-0

7

3rd

Qtr

-07

4th

Qtr

-07

1st

Qtr

-08

2n

d Q

tr-0

8

3rd

Qtr

-08

4th

Qtr

-08

1st

Qtr

-09

2n

d Q

tr-0

9

3rd

Qtr

-09

4th

Qtr

-09

1st

Qtr

-10

2n

d Q

tr-1

0

3rd

Qtr

-10

4th

Qtr

-10

1st

Qtr

-11

2n

d Q

tr-1

1

3rd

Qtr

-11

4th

Qtr

-11

1st

Qtr

-12

2n

d Q

tr-1

2

3rd

Qtr

-12

4th

Qtr

-12

1st

Qtr

-13

2n

d Q

tr-1

3

3rd

Qtr

-13

4th

Qtr

-13

1st

Qtr

-14

2n

d Q

tr-1

4

3rd

Qtr

-14

4th

Qtr

-14

1st

Qtr

-15

2n

d Q

tr-1

5

3rd

Qtr

-15

4th

Qtr

-15

1st

Qtr

-16

2n

d Q

tr-1

6

3rd

Qtr

-16

Orders Backlog

Cyclicality of The Business

Weathering the Downside of the Cycle

($ Millions)

66INVESTOR DAY

NOVEMBER 10, 2016

Reinvigorated Operational Focus

Prepared for Economic Volatility

Innovation

↓ 1,400 Employees,

22% reduction

Relocate3 plants

Hup 40-30, GMK5250L,

GMK4100L-1, GRT8100

$270M U.S. Army

Contract

Margin Expansion

Lean transformations

in U.S., Germany, Italy

Next generation crane; intro at ConExpo 2017

Velocity Growth

The Manitowoc Way

67INVESTOR DAY

NOVEMBER 10, 2016

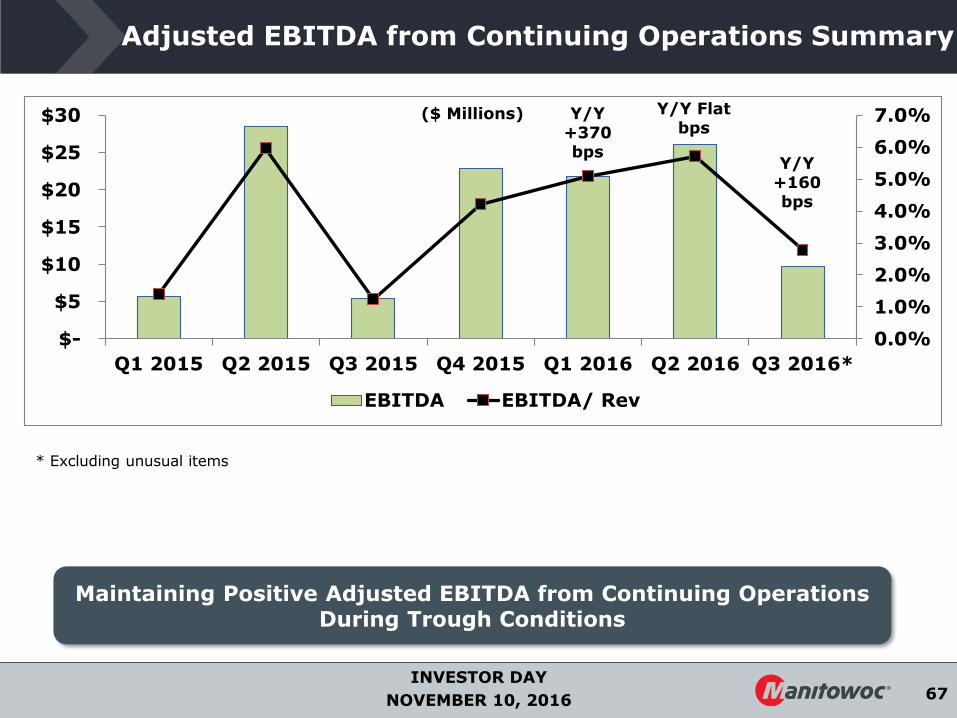

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

$-

$5

$10

$15

$20

$25

$30

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016*

EBITDA EBITDA/ Rev

Adjusted EBITDA from Continuing Operations Summary

Maintaining Positive Adjusted EBITDA from Continuing Operations During Trough Conditions

* Excluding unusual items

($ Millions) Y/Y +370 bps

Y/Y +160 bps

Y/Y Flat bps

68INVESTOR DAY

NOVEMBER 10, 2016

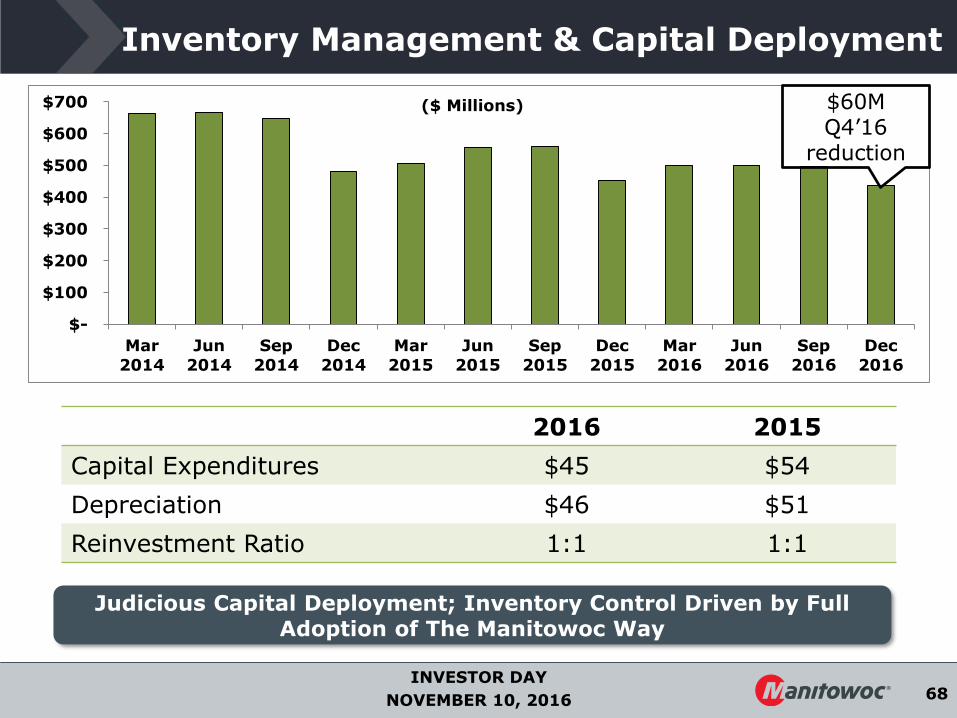

$-

$100

$200

$300

$400

$500

$600

$700

Mar

2014

Jun

2014

Sep

2014

Dec

2014

Mar

2015

Jun

2015

Sep

2015

Dec

2015

Mar

2016

Jun

2016

Sep

2016

Dec

2016

Inventory Management & Capital Deployment

Judicious Capital Deployment; Inventory Control Driven by Full Adoption of The Manitowoc Way

2016 2015

Capital Expenditures $45 $54

Depreciation $46 $51

Reinvestment Ratio 1:1 1:1

$60M Q4’16

reduction

($ Millions)

69INVESTOR DAY

NOVEMBER 10, 2016

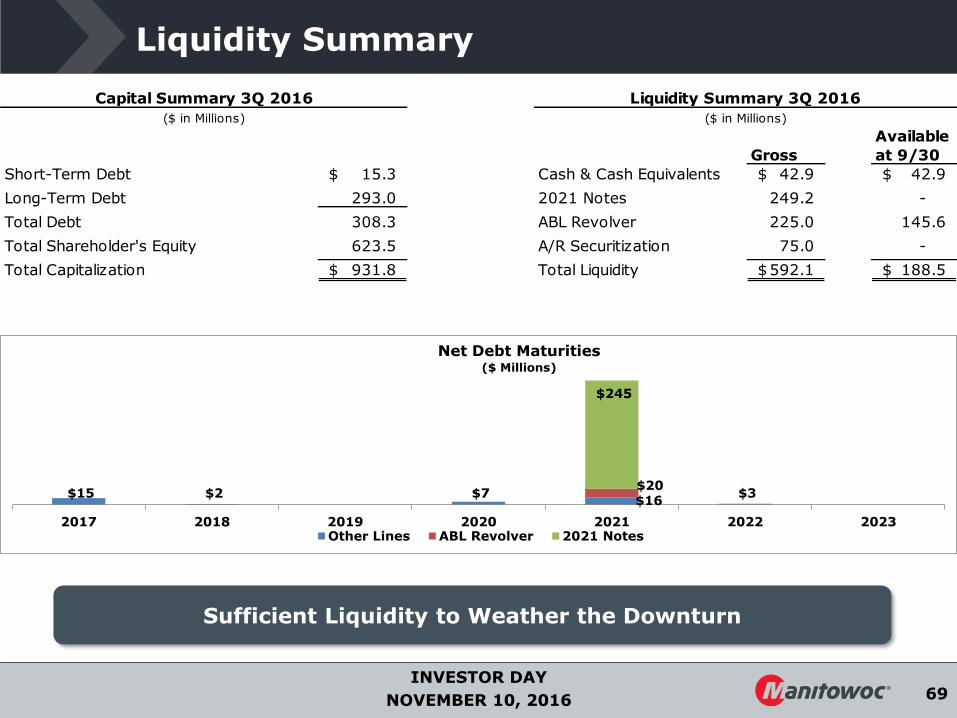

Liquidity Summary

Sufficient Liquidity to Weather the Downturn

$15 $2 $7 $16

$3 $20

$245

2017 2018 2019 2020 2021 2022 2023

Net Debt Maturities($ Millions)

Other Lines ABL Revolver 2021 Notes

Gross

Available

at 9/30

Short-Term Debt 15.3$ Cash & Cash Equivalents 42.9$ 42.9$

Long-Term Debt 293.0 2021 Notes 249.2 -

Total Debt 308.3 ABL Revolver 225.0 145.6

Total Shareholder's Equity 623.5 A/R Securitization 75.0 -

Total Capitalization 931.8$ Total Liquidity 592.1$ 188.5$

Capital Summary 3Q 2016

($ in Millions)

Liquidity Summary 3Q 2016

($ in Millions)

70INVESTOR DAY

NOVEMBER 10, 2016

Internal Long-Term Financial Goals

“10 x 20”

Financial Metrics 2015 2016 5-Year Target

Revenue $1.9B ~$1.6B $1.8- $2.0B

Adjusted Operating Margin 0.6% ~ (1)-(2) % 10%

Assumes Normalized Market Growth

Continued Margin Expansion… The Manitowoc Way

>100% Cash Conversion… Utilize Tax NOL’s

71INVESTOR DAY

NOVEMBER 10, 2016

Questions & Answers

72INVESTOR DAY

NOVEMBER 10, 2016

Senior Vice President, The AmericasLes Middleton

73INVESTOR DAY

NOVEMBER 10, 2016

• Safety is our #1 priority

• Please stay with your tour group at all times

• Please keep your safety glasses and hi-vis vests on at all times

• Stay within the designated aisle ways and with your designated tour guide

• Please do not handle parts

• If an alarm sounds, stay calm, and follow the instructions from your tour guide

• NO PHOTOS OR VIDEO PLEASE

Facility safety guidelines

74INVESTOR DAY

NOVEMBER 10, 2016

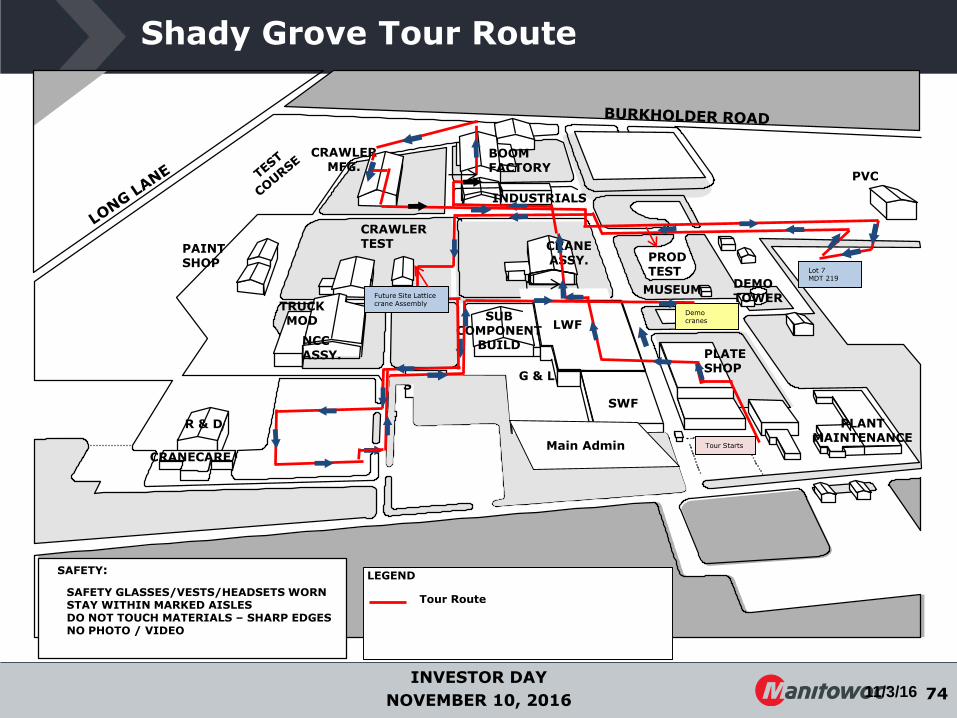

Shady Grove Tour Route

11/3/16

STORE

NCC ASSY.

CRANE ASSY.

BOOM FACTORY

PLATE SHOP

SWF

SUB COMPONENT

BUILD

LWF

MAIN OFFICE

PLANT MAINTENANCE

PAINT SHOP

MUSEUM

PROD TEST

PVC

DEMO TOWER

INDUSTRIALS

CRANECARE

CRAWLER MFG.

SAFETY GLASSES/VESTS/HEADSETS WORNSTAY WITHIN MARKED AISLESDO NOT TOUCH MATERIALS – SHARP EDGESNO PHOTO / VIDEO

TRUCK MOD

SAFETY:

G & L

Demo cranes

LEGEND

R & D

Lot 7MDT 219

Main Admin

Tour Route

Future Site Lattice crane Assembly

CRAWLER TEST

Tour Starts

INVESTOR DAY

NOVEMBER 10, 2016

Appendix: Additional Materials and Financials

76INVESTOR DAY

NOVEMBER 10, 2016

Manitowoc: Large Installed Base

~55,000 7-9 years

~50,0003 Self-Erecting: 6-8 yearsTop-Slewing: 10-12 years

~9,000 9-12 years

~27,000 7-9 years

Mobile Telescopic Cranes

Tower Cranes

Lattice-Boom Cranes

Boom Trucks

Leading Brands Active Installed Base1Category

Extensive installed base across diverse geographies provides recurring service and replacement parts revenue opportunities

1 Reflects management approximation of the active installed base based on internally available data.2 Reflects management approximation of the average fleet replacement based on available data and feedback from the customers.3 Includes top-slewing and self-erecting tower cranes.

Average Fleet Replacement2

Total: ~140,000

77INVESTOR DAY

NOVEMBER 10, 2016

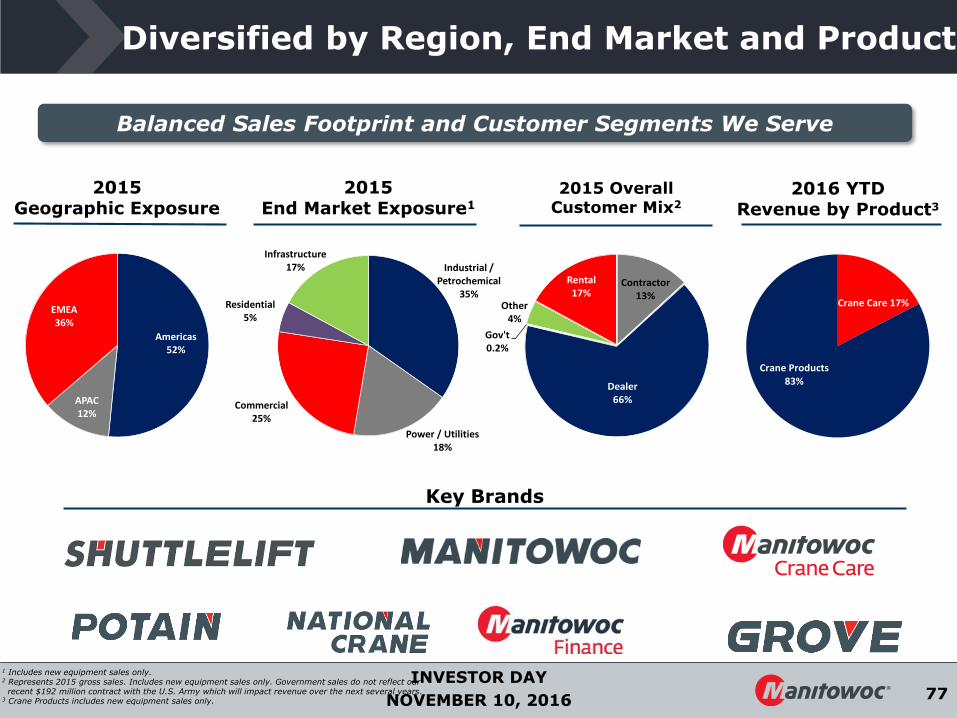

Diversified by Region, End Market and Product

Key Brands

2015Geographic Exposure

2015End Market Exposure1

2016 YTDRevenue by Product3

Americas52%

APAC12%

EMEA36%

1 Includes new equipment sales only.2 Represents 2015 gross sales. Includes new equipment sales only. Government sales do not reflect our recent $192 million contract with the U.S. Army which will impact revenue over the next several years.

3 Crane Products includes new equipment sales only.

Balanced Sales Footprint and Customer Segments We Serve

2015 Overall Customer Mix2

Industrial / Petrochemical

35%

Power / Utilities18%

Commercial25%

Residential5%

Infrastructure17%

Contractor13%

Dealer66%

Gov't0.2%

Other4%

Rental17%

Crane Care 17%

Crane Products 83%

78INVESTOR DAY

NOVEMBER 10, 2016

Q3 2016 Q3 2015 YoY ∆ Q2 2016 QoQ ∆

Orders 309.9$ 338.2$ (8.4)% 348.9$ (11.2)%

Net sales 349.8$ 438.2$ (20.2)% 457.7$ (23.6)%

Operating (loss) income (133.5)$ (8.2)$ n/m 4.8$ n/m

Non-GAAP adjusted operating (loss) income (31.5)$ (7.7)$ n/m 14.8$ n/m

Net (loss) income (140.0)$ 4.8$ n/m (4.9)$ n/m

Non-GAAP adjusted net (loss) income from

continuing operations (38.1)$ (29.8)$ (27.9)% 5.0$

n/m

Net cash used for operating activities of

continuing operations

(1.4)$ (37.2)$ n/m (14.6)$ n/m

Capital expenditures 10.1$ 9.4$ 7.4 % 13.8$ (26.8)%

Backlog 353.6$ 631.0$ (44.0)% 393.5$ (10.1)%

Book-to-bill 0.89 0.77 14.8 % 0.76 16.2 %

n/m- Not meaningful

Financial & Other Key Metrics

1 Excludes amortization and restructuring expense.

79INVESTOR DAY

NOVEMBER 10, 2016

GAAP Reconciliation Summary

80INVESTOR DAY

NOVEMBER 10, 2016

Historical Revenue and EBITDA

(US$ in millions)

Revenue EBITDA & Margin

Cranes generates significant revenue and EBITDA during cyclical upturns

During industry downturns, predictable replacement demand and differentiated product offerings support demand

Restructuring initiatives in progress

$1,708

$2,135

$2,427 $2,506

$2,305

$1,862

2010 2011 2012 2013 2014 2015

Revenue

$149

$172

$214

$266

$210

$110

8.7% 8.1%8.8%

10.6%9.1%

5.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$-

$50

$100

$150

$200

$250

$300

2010 2011 2012 2013 2014 2015

EBITDA % Margin

Note: Revenue and EBITDA from 2010 – 2015 represent historical Cranes segment results. EBITDA is calculated as Operating Earnings from Continuing Operations plus Depreciation and excludes corporate allocations.

81INVESTOR DAY

NOVEMBER 10, 2016

Historical Capital Needs & Cash Flow

(US$ in millions)

Capex & % of Sales

Note: Capex and Unlevered Free Cash Flow represent historical Cranes segment results. EBITDA calculated as Operating Earnings from Continuing Operations plus Depreciation and excludes corporate allocations. 1 Free Cash Flow defined as EBITDA less Capex.

Free Cash Flow1 & % Conversion

Moderate capital intensity and working capital requirements allow earnings to largely flow to cash flow

Working capital needs decrease when revenue declines, providing a strong cash flow offset during industry downturns

Free cash flow¹ generation through the cycle

$21

$52 $53

$69

$57 $52

1.2%2.4% 2.2% 2.8% 2.5% 2.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

$-

$20

$40

$60

$80

$100

$120

$140

2010 2011 2012 2013 2014 2015

Capex % of Sales

$129 $120

$161 $196

$152

$58 86.2%69.7% 75.4% 73.9% 72.7%

52.9%0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014 2015

FCF % Conversion

82INVESTOR DAY

NOVEMBER 10, 2016

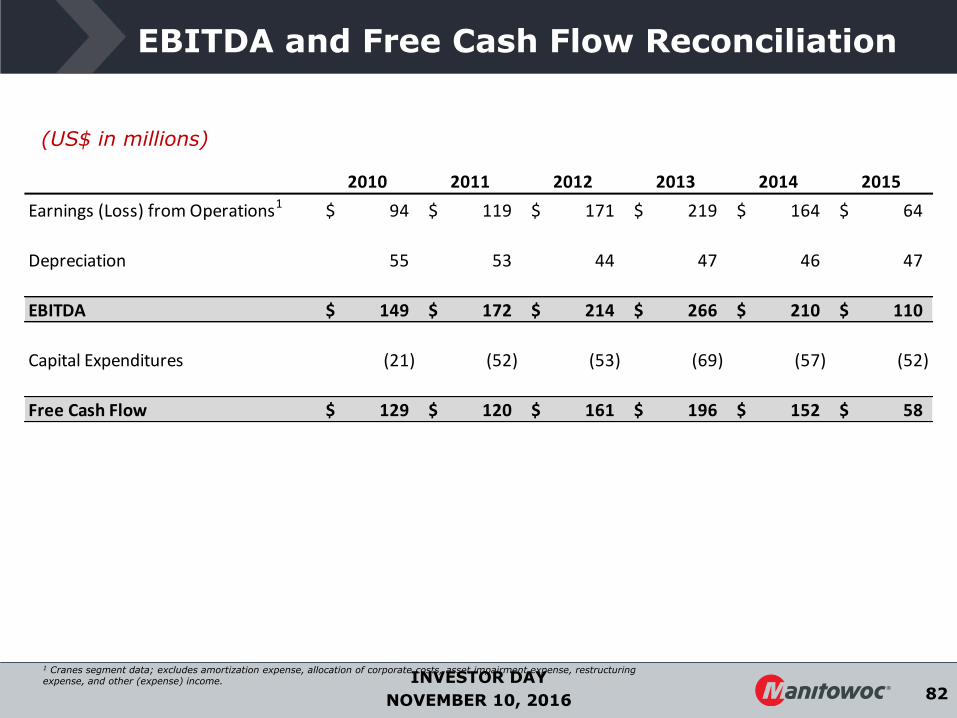

EBITDA and Free Cash Flow Reconciliation

(US$ in millions)

2010 2011 2012 2013 2014 2015

Earnings (Loss) from Operations1 94$ 119$ 171$ 219$ 164$ 64$

Depreciation 55 53 44 47 46 47

EBITDA 149$ 172$ 214$ 266$ 210$ 110$

Capital Expenditures (21) (52) (53) (69) (57) (52)

Free Cash Flow 129$ 120$ 161$ 196$ 152$ 58$

1 Cranes segment data; excludes amortization expense, allocation of corporate costs, asset impairment expense, restructuring expense, and other (expense) income.

83INVESTOR DAY

NOVEMBER 10, 2016