the marking of section c in both the cbe and paper versions of providers... · the marking of...

TRANSCRIPT

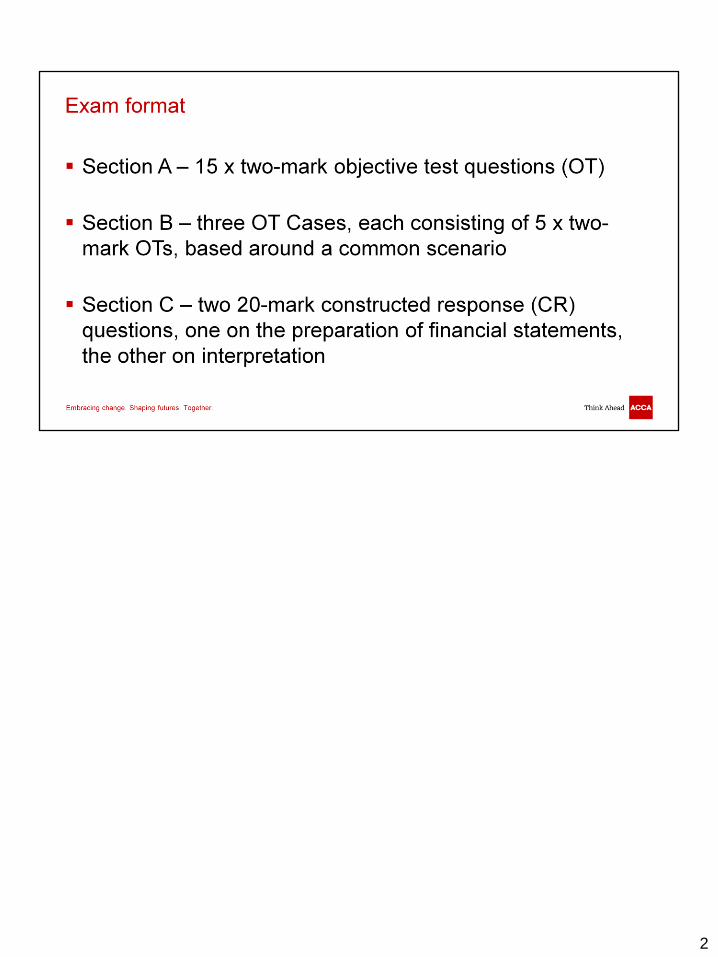

1

2

The marking of section C in both the CBE and paper versions of

the exam use marking processes that has been in place for many

years. The F7 team has a wealth of experience, many of whom

are long-term members.

3

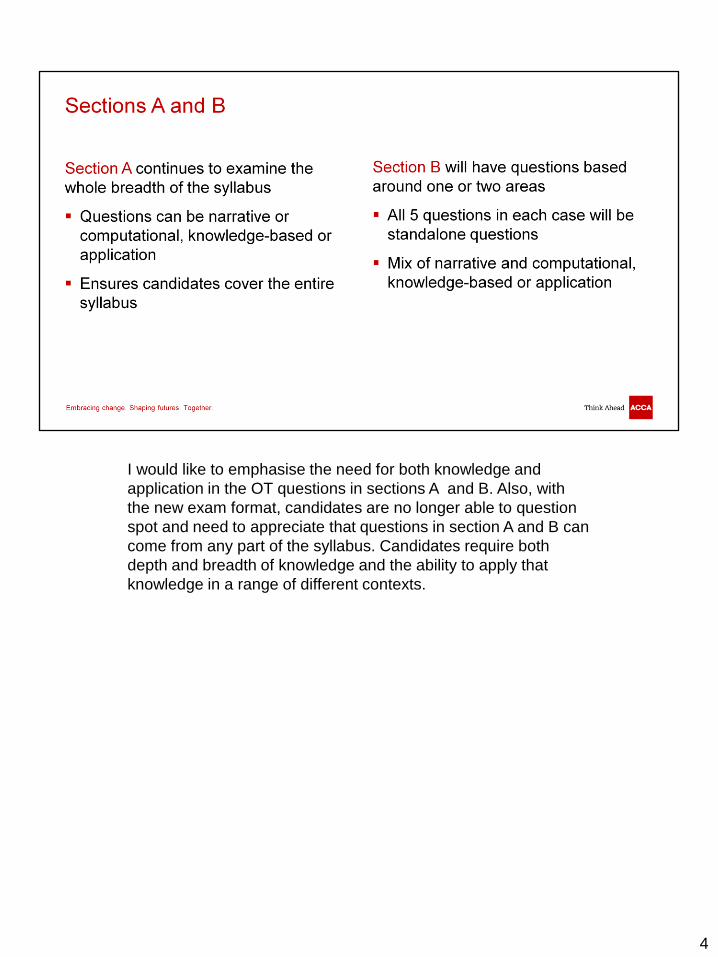

I would like to emphasise the need for both knowledge and

application in the OT questions in sections A and B. Also, with

the new exam format, candidates are no longer able to question

spot and need to appreciate that questions in section A and B can

come from any part of the syllabus. Candidates require both

depth and breadth of knowledge and the ability to apply that

knowledge in a range of different contexts.

4

In contrast to past exams, it is now unlikely that candidates will be

asked to produce a full set of financial statements for a single

entity i.e. a statement of profit or loss and a statement of changes

in equity and a statement of financial position. However,

candidates may now be expected to prepare a selection of these

financial statements; for example, to adjust a draft profit figure

and prepare a statement of financial position or prepare a

statement of profit or loss and a statement of changes in equity.

The same is true of questions that test the preparation of

consolidated financial statements, although it is possible that a

detailed statement of profit or loss might be required alongside a

summarised statement of financial position (or vice versa).

5

Candidates should be aware that very few marks will be awarded

for comments made about the increase/decrease of a ratio and

whether that is good/bad. Rather, marks are allocated where

candidates are able to explain why these increases/decreases

have occurred and the implications that these changes might

have for the company.

The analysis of consolidated financial statements is still fairly new

in this syllabus so students need to be aware of the importance of

discussing group issues here. For example, where there has

been an acquisition/disposal of a subsidiary, how this impacts on

the comparability of these financial statements. Candidates

should also expect to calculate some group numbers; for instance

goodwill, gain/loss on the disposal of a subsidiary, non-controlling

interests; retained earnings etc.

6

7

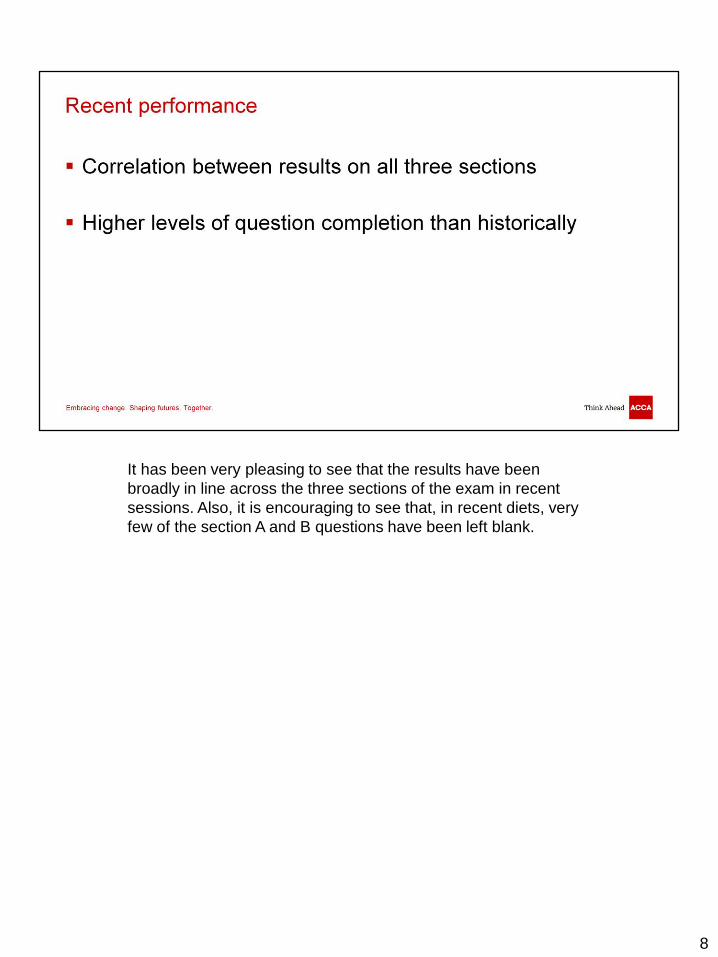

It has been very pleasing to see that the results have been

broadly in line across the three sections of the exam in recent

sessions. Also, it is encouraging to see that, in recent diets, very

few of the section A and B questions have been left blank.

8

Here are some other common problem candidates have in the

exam.

Encourage your students to take time and not rush through the

OT questions in sections A and B. These questions may contain

very plausible distracters, so they must always read the questions

very carefully.

In accounts preparation questions, requirements that ask for

adjustments, rather than a full set of financial statements, seem

to cause more difficulty. Make sure that your students practice a

wide range of styles of questions.

In the preparation of consolidated financial statements, we see

some fundamental errors, such as time apportioning in the

statement of financial position when there is a mid-year

acquisition.

9

Too many candidates produce the kind of statements that will

score very few marks, simply stating which items have increased

or decreased without any attempt to explain this in the context of

the information provided in the question. The application of

knowledge to the scenario is key.

Where ratios are calculated, credit can be given if candidates

have worked out a different one to that given in the suggested

solution, providing the marker can see workings and that the ratio

is valid.

10

Too many students answer this without considering the group

element.

Candidates knowledge of group accounting will be tested in these

questions – all of the same aspects that they will have learned in

the context of preparation of consolidated financial statements

can appear here and markers want to see answers that

demonstrate an understanding of how these affect the group in

the question.

11

12

From September 2017, the new standard on leases will be

examinable. All of the Approved Content Providers texts have

been reviewed for these changes, and it’s essential that tutors

understand the new standard before classes begin for

Septembe17.

13

14