the merchants trust plc - theaic.co.uk · 16 2 -p-it \ st the merchants trust ... term pricing...

TRANSCRIPT

The Merchants

Trust PLC

13 October 2016

A challenging time for income

investors

AIC Adviser Seminar, Harrogate

Simon Gergel

For professional investors only

2 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Past performance is not a reliable indicator of future results.

Source: Thomson Reuters Datastream, as at 31 August 2016.

Some perspective:

A challenging time for income investors

British American Tobacco vs FTSE 100 rebased

2000 2002 2004 2006 2008 2010 2012 2014 2016 50 60 70 80 90 100

200

300

400

500

600 700 800 900 1000

50 60 70 80 90

100

200

300

400

500

600 700 800 900

1000

Rebase BRITISH AMERICAN TOBACCO to 100 Rebase FTSE 100 to 100

BATS has been one of the best performing stocks this

century

It has outperformed the FTSE 100 index 10-fold

British American Tobacco Dividend Yield vs FTSE 100 Yield

However, the dividend yield started 4-5 x higher than FTSE

100

BATS now yields less than the market

2000 2002 2004 2006 2008 2010 2012 2014 2016

2

3

4

5

6

7

8

9

10

2

3

4

5

6

7

8

9

10

BRITISH AMERICAN TOBACCO - DY FTSE 100 - DY

3 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Past performance is not a reliable indicator of future results.

Source: Thomson Reuters Datastream, as at 31 August 2016.

Some perspective (cont’d):

A challenging time for income investors

Yield divergence within UK market

A similar situation is seen at other traditional

income stocks; e.g. Unilever

Many traditional income stocks are unlikely to

provide high future returns

However, there are still high yield

opportunities; e.g. Shell, GSK

Investors need to be selective

2011 2012 2013 2014 2015 2016

3

4

5

6

7

8

9

3

4

5

6

7

8

9

BRITISH AMERICAN TOBACCO - DY ROYAL DUTCH SHELL B - DY

FTSE 100 - DY GLAXOSMITHKLINE - DY UNILEVER (UK) - DY

4 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Dividend yield 5.6%*, one of the highest in its sector

34 years of dividend growth, strong reserves position

Actively managed, high conviction portfolio, delivering strong performance

Geared exposure to UK equity market, NAV will benefit from “pull to par”

Low management fee: 0.35%

Past performance is not a reliable indicator of future results.

*Source: AllianzGI, as at 22 September 2016.

The Merchants Trust

Objective: “To provide an above

average level of income and

income growth, together with

long term growth of capital,

through a policy of investing

mainly in higher yielding UK

FTSE 100 Companies.”

5 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

* As at 30 June 2016. Source: Allianz Global Investors. Any differences in totals are due to rounding. ** Includes money market. *** Managed in respective region.

Assets under management: EUR 469 billion*

AllianzGI – Substantial resources and broad expertise

Leveraging the expertise and insights gained through our significant presence in institutional and

retail markets

AuM by asset class AuM by region*** AuM by retail / institutional business

Europe

EUR 363 bn

(77%)

US

EUR 76 bn

(16%)

Asia Pacific

EUR 29 bn

(6%) Equity

EUR 135 bn

(29%)

Fixed Income**

EUR 204 bn

(44%)

Multi Asset

EUR 116 bn

(25%)

Alternatives

EUR 14 bn (3%) Retail

EUR 144 bn

(31%)

Institutional

EUR 325 bn

(69%)

6 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Investment philosophy

Understand Act

A high conviction portfolio to deliver long-term

outperformance The stock market is not efficient

Fundamental research, conducted and disseminated

globally provides an information advantage

Companies and industries are complex and

dynamic

Focus on underlying cash-flow for a true picture of

performance and potential dividend payments

Companies portray misleading and flattering

view of reality

Maintain long-term focus to take advantage of short

term pricing anomalies

Investors and markets are increasingly short-

term

Active portfolio management with strong valuation

emphasis in Buy and Sell discipline

Share price returns are related to the purchase

price

7 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

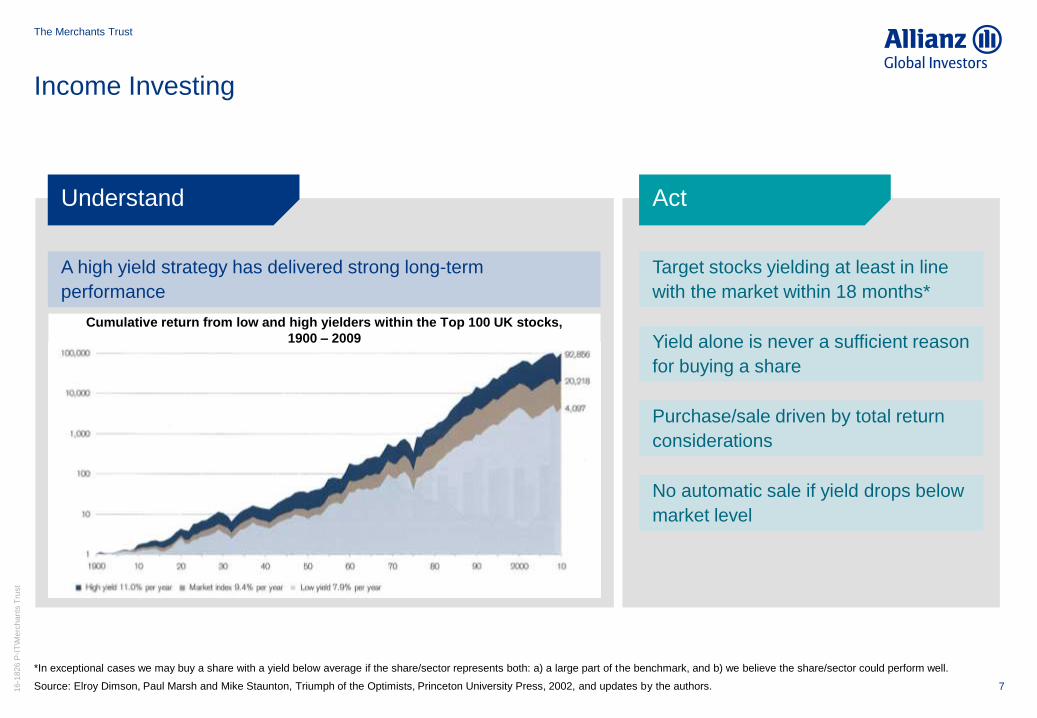

Income Investing

*In exceptional cases we may buy a share with a yield below average if the share/sector represents both: a) a large part of the benchmark, and b) we believe the share/sector could perform well.

Source: Elroy Dimson, Paul Marsh and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and updates by the authors.

Understand Act

Target stocks yielding at least in line

with the market within 18 months*

A high yield strategy has delivered strong long-term

performance

Yield alone is never a sufficient reason

for buying a share

Purchase/sale driven by total return

considerations

No automatic sale if yield drops below

market level

Cumulative return from low and high yielders within the Top 100 UK stocks,

1900 – 2009

8 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

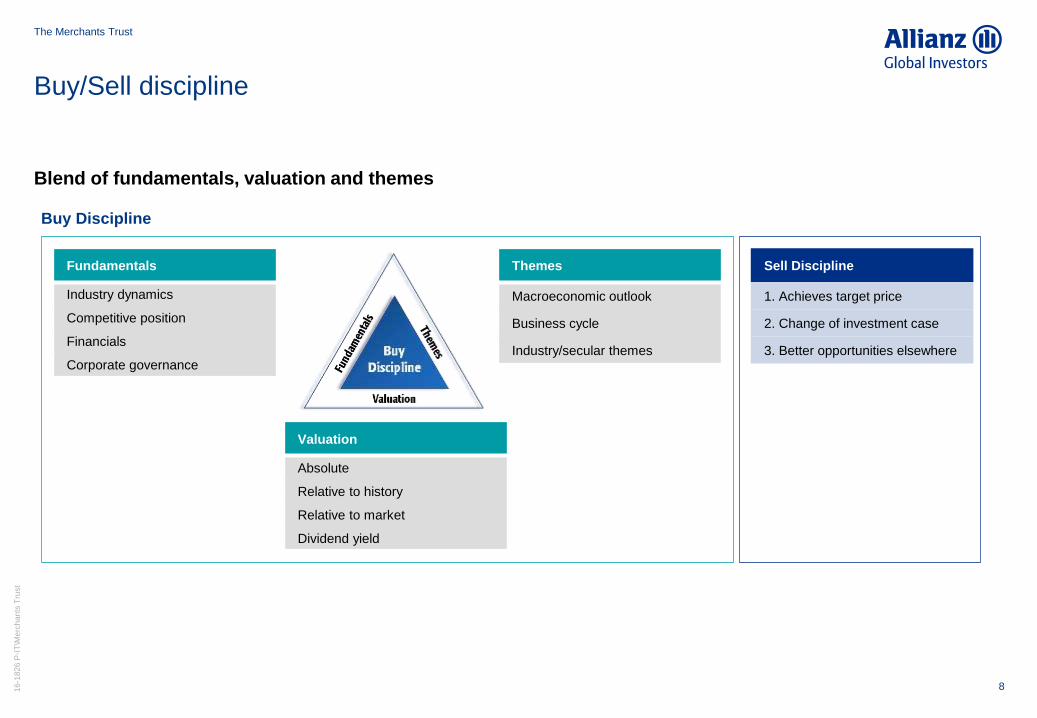

Buy/Sell discipline

Blend of fundamentals, valuation and themes

Fundamentals

Industry dynamics

Competitive position

Financials

Corporate governance

Buy Discipline

Themes

Macroeconomic outlook

Business cycle

Industry/secular themes

Valuation

Absolute

Relative to history

Relative to market

Dividend yield

Sell Discipline

1. Achieves target price

2. Change of investment case

3. Better opportunities elsewhere

9 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Source: Bloomberg, as at 26 September 2016.

Strong fundamentals, attractive valuation and supportive themes

Stock example – GlaxoSmithkline

Fundamentals

Global leader in consumer

health – Sensodyne, Panadol,

Voltaren etc.

Leading vaccine producer

Scale player in pharmaceuticals

Robust balance sheet,

improving cash flow

Intellectual property, brands,

technology and distribution

assets

Source: Thomson Reuters Datastream

Glaxo share price vs FSTE 100 over 1 year Themes

Restructuring: Improving mix of

business, margin potential

Favourable demographics –

ageing population

EM exposure – vaccines /

consumer health

Growth – Vaccines, consumer,

HIV

Risk: Advair generics – Offset by

new products

Valuation

Valuation reflects historic issues not future

prospects

Modestly priced compared to consumer staples

5% Yield

p/e 16x (2017)

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

2015 2016

100

110

120

130

100

110

120

130

GlaxoSmithKline (rebased)

FTSE 100 (rebased)

10 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Key features and objectives

Source: AllianzGI/JP Morgan Cazenove, as at 22 September 2016.

Objective: “To provide an above

average level of income and

income growth, together with

long term growth of capital,

through a policy of investing

mainly in higher yielding UK

FTSE 100 Companies.”

Total Assets £651m

Debt Long Term Debentures (Historic) £111m

Net Assets £540m

Gearing 17%

Debt – Average Duration 7 years

First Debenture Repayment Jan 2018

Structure:

Share Price 431p

Yield 5.6%

Market Cap £468m

NAV (Debt at market) 465p

(Discount)/Premium (Debt at market) (7.5%)

Valuation:

11 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

2.1 2.3 2.43.0

3.84.5

5.46.6

8.09.0

10.010.6 11.0

11.5

12.313.7

14.3

15.6

16.0

16.4 16.8

17.2

17.618.0

18.920.0

21.622.3

22.5 22.8 23.0 23.2

23.6

23.8

24.00.5

0p

2p

4p

6p

8p

10p

12p

14p

16p

18p

20p

22p

24p

26p

28p

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Net

Div

iden

d pe

r Sha

re

Past performance is not a reliable indicator of future results.

Source: AllianzGI, as at 22 September 2016.

34 years of rising dividends

1st objective: High income and dividend growth

5.6% yield, fully covered by earnings in FY 2016

Significant yield premium over sector and wider market

Reserves built up in good years to offset pressures in difficult years

Revenue reserves of 22.6p available = 94% of full year dividend

Special

Dividend

Reserve accumulation Reserve depletion

12 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

UK Equity Income Trusts

Source: JP Morgan Cazenove/FTSE as at 31 August 2016.

Dividend yields

Merchants has one of the highest yields in the sector

The yield is well above the FTSE 100 yield of 3.7%

10.3

5.7 5.4 4.6 4.4 4.2 4.0 4.0 3.9 3.8 3.7 3.7 3.7 3.6 3.6 3.6 3.4 3.4 3.3 3.2 3.1 3.1

1.9

0

2

4

6

8

10

12

Bri

tish &

Am

eri

ca

n

Me

rcha

nts

Tru

st

Sh

ire

s In

co

me

Dun

ed

in I

nco

me

Gro

wth

Mu

rra

y I

nco

me

Tru

st

Va

lue

& In

com

e

Schro

der

Inco

me

Gro

wth

Che

lvert

on

Sm

all

Co

mp

anie

sD

ivid

en

d

City o

f L

on

do

n

JP

Mo

rga

n E

lect M

an

ag

ed

Inc

F&

C C

apita

l &

In

co

me

JP

Mo

rga

n C

laverh

ouse

Sta

nd

ard

Life

Eq

uity I

nco

me

Inve

sco I

nco

me G

row

th

UK

Eq

uity In

co

me W

ghtd

Avg

Te

mp

le B

ar

Ed

inb

urg

h I

nve

stm

en

t

Pe

rpe

tual In

co

me

& G

row

th

Low

lan

d

Bla

ckR

ock I

nco

me

and

Gro

wth

Tro

y I

nco

me

& G

row

th

Div

ers

e I

nco

me

Tru

st

Fin

sbu

ry G

row

th &

Inco

me

Div

ide

nd

Yie

ld %

13 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Past performance is not a reliable indicator of future results.

Source: AllianzGI/Merchants Trust, as at 31 January 2016.

The Merchants Trust

Disciplined process to pick high yielding cheap stocks

High conviction, actively managed portfolio

Good long term performance, challenging year

Total Return

Periods to 31 January 2016 %

1 Year 3 Years p.a. 5 Years p.a. 10 Years p.a. Financial Year

to 31 August

Merchants’ Portfolio (excludes gearing) -3.8 5.5 7.5 5.5 10.5

FTSE 100 Index -6.5 2.6 4.5 4.3 15.0

Difference +2.8 +2.9 +3.0 +1.2 -4.2

14 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Total Return: NAV Performance

Past performance is not a reliable indicator of future results.

Source: Thomson Reuters Datastream, Total return portfolio performance 31/01/16-31/08/16 = +10.52% v +14.98% (FTSE 100 TR) .

Gearing amplifies performance of NAV level

Falling bond yields, rising values, have held back NAV

Pull to par will reduce debt value in future

Merchants Trust NAV vs FTSE 100: 5 years to August 2016

2011 2012 2013 2014 2015 2016

80

100

120

140

160

180

80

100

120

140

160

180

MERCHANTS TRUST - NAV (Debt at Fair Value) Total Return FTSE 100 Total Return

15 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Active portfolio management

Active stock selection, driven by opportunities

6 additions, 7 disposals within 43 stock portfolio

Purchases focused on:

- Undervalued growth

- Cyclical recovery

- New IPO’s – Strong business franchises, attractive

valuations

Sales driven by:

- Full valuation/bond proxies

- Change of view, deteriorating trading

Financial year to 31 January 2016

New Additions Disposals

Lloyds Unilever

Barclays Hammerson

Prudential Cineworld

Antofagasta Premier Farnell

Equiniti Amec Foster Wheeler

Hostelworld Britvic

Smiths

Current Financial year

New Additions Disposals

Senior Segro

Sirius Real Estate Barclays

16 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Growth will be restrained by high debt burden, financial repression

Corporates generally in good shape, balance sheets repaired

Large companies geographically diversified

Yield to remain an important factor

Best value in Mega Caps and recovery situations

Safe defensive stocks and bond proxies expensive

Economic and market outlook – Long term themes

17 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Key portfolio themes

This is no recommendation or solicitation to buy or sell any particular security. A stock mentioned as example above will not necessarily be comprised in the portfolio by the time this document

is disclosed or at any other subsequent date.

Investment Themes

Inflation “tail risk”: Real assets, inflation-linked revenues attractive

Earnings growth is hard to achieve: Favour growth stocks on

reasonable valuations Turnaround situations

Exposure to emerging market consumer spending growth Financials: exposure to rising interest rates/volatility

Large core holdings in well financed global, “mega” caps with strong

franchises and good yields

Cyclical Recovery situations: Industries recovering, companies on

modest valuations

GlaxoSmithKline Shell | BP HSBC

Ashmore Inmarsat

GlaxoSmithKline UBM Mothercare

Mothercare Marks & Spencer First Ladbrokes

Greene King Pennon Sainsburys

Balfour Beatty SThree Carnival Hansteen

Hostelworld

ICAP | IG Group HSBC/Lloyds Equiniti Prudential

18 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Different to other UK equity income funds

This is no recommendation or solicitation to buy or sell any particular security.

Source: AllianzGI, as at 31 August 2016.

Strong valuation discipline

Opportunities in recovery situations:

- Financial services

- Construction and materials

- Travel and leisure

Limited exposure to expensive defensives

Sector View

Stock Views

Underweight

Tobacco

Household Goods

Pharmaceuticals

Beverages

Personal Goods

Pharmaceuticals

Overweight

Financial Services

Construction & Materials

Gas, Water & Multi Utilities

Travel & Leisure

Aerospace & Defence

Underweight

British American Tobacco

Astra Zeneca

Vodafone

Reckitt Benckiser

Unilever

Overweight

UBM

Inmarsat

Centrica

Tate & Lyle

GlaxoSmithKline

Merchants Trust

2.8

3.2

3.4

5.0

5.2

-2.8

-3.5

-3.6

-3.7

-6.5

-8.0 -4.0 0.0 4.0 8.0

2.5

3.0

3.0

3.1

4.5

-2.4

-2.6

-3.5

-3.5

-4.3

-8.0 -4.0 0.0 4.0 8.0

Merchants Trust

% position relative to FTSE 100 Index

19 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Good performance track record

Active, value driven, stock selection approach

34 years of dividend growth

High yield supported by significant reserves

Merchants is well positioned for the future

Low management fee

Why The Merchants Trust

For further information:

www.merchantstrust.co.uk

Blog: www.unconstrainedthinking.com

MELISSA GALLAGHER: 020 3246 7539

SIMON GERGEL: 020 3246 7431

20 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

A Appendices

21 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

UK Equity investment team

Source: AllianzGI. As at 31 March 2016. GrassrootsSM Research is a division within the Allianz Global Investors group of companies that commissions investigative research for

asset-management professionals. Research data used to generate GrassrootsSM Research reports are received from reporters and field force investigators who work as independent, third

party research providers, supplying research that is paid for by commissions generated by trades executed on behalf of clients.

25-35 stock portfolio

Simon Gergel

CIO UK Equities Income

28 years experience

Matthew Tillett

Unconstrained/Income

10 years experience

Andrew Neville

Mid Cap

19 years experience

Matthew Hall

Mid Cap

7 years experience

European Research Platform Analysts

Healthcare 3

Financials 4

Telecom/Media 2

Industrials & Services 5

Materials 7

Technology 2

Consumer 4

ESG Research 6

GrassrootsSM Research 2

Portfolio Management Team

Europe Equity 41

Macro Research

Global Policy Council 16

GrassrootsSM Research

Help identify key stock

drivers

In-house staff of 10

62 reporters

Over 300+ field force

investigators

Conduct over 400

company/industry studies

per year

50,000 industry contacts

22 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Dividend sustainability: Yield profile of UK Equity portfolio

1 As at 22 August 2016, historic yields.

Source: Allianz Global Investors.

Portfolio diversified across yield spectrum

Two thirds of portfolio has historic yields <5%

19% of portfolio yields <3% - should contribute more income in future

Sample

Companies

First Group

Balfour Beatty

Ladbrokes

Antofagasta

Carnival

Prudential

UBM

Greene King

Glaxo

Kier

M&S

Centrica

Legal &

General

Man

Shell

HSBC

Po

rtfo

lio

Weig

ht

(%)

1.5%

5.5%

12.2% 14.5%

28.0%

16.0%

2.9%

19.1%

0%

5%

10%

15%

20%

25%

30%

35%

0 <2% 2.0% to 3.0% 3.0% to 4.0% 4.0% to 5.0% 5.0% to 6.0% 6.0% to 7.0% 7.0% to 8.0%

Yield Bucket

23 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Debt structure

Source: AllianzGI, as at 31 January 2016.

Long dated debt permits long term investment horizon

Gearing amplifies portfolio returns, partially offset by low beta

As debt approaches maturity the debt value will approach par

Debt Average

Coupon

Rate

Maturity

Date

Amount

Repayable

on

Maturity

£m

Clean Market

Value Average “pull to par” p.a.

31/01/16

£m £m

% NAV

(market) Years

First Debenture Finance 11.125% 2018 34.0 39.2 2.6 0.5 2.0

Fin Trust 9.25% 2023 42.0 57.0 2.1 0.4 7.2

Secured Bonds 5.875% 2029 30.0 35.4 0.4 0.1 13.8

4% Perpetual Debenture Stock 4.0% N/A 1.4 1.0 - - -

3.65% Cumulative Preference Shares 3.65% N/A 1.2 0.9 - - -

Total 108.6 133.8 5.1 1.0 N/A

24 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Income investing in the UK

We believe that:

The UK has a large variety of high yielding companies

A culture that encourages consistent dividend payments

A strong legal and corporate governance framework

The takeover panel – ensures “fair play”

The UK is one of the best places for income investors % Market Cap with Yield >4% by MSCI Region

80

70

60

50

40

30

20

10

0

% o

f m

ark

et

ca

p w

ith

DY

= X

%

Dec 0

4

Ju

n 0

5

Dec 0

5

Ju

n 0

6

Dec 0

6

Ju

n 0

7

Dec 0

7

Ju

n 0

8

Dec 0

8

Ju

n 0

9

Dec 0

9

Ju

n 1

0

Dec 1

0

Ju

n 1

1

Dec 1

1

Ju

n 1

2

Dec 1

2

Ju

n 1

3

UK Japan US Asia ex Japan Europe ex UK

Performance across the yield spectrum (UK) Performance of UK Dividend stocks (Quintiles Q1 – Q5)

Source: SG Cross Assrt Research, MSCI, as at 1 November 2014.

0

50

100

150

200

250

300

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Quintile 4 Quintile 1 Quintile 2 Quintile 3 Quintile 5

Source: HSBC, December 1994 - September 2014. Past performance is not a reliable indicator of

future results.

Performance and yield are related

Highest yielders have been best performers

Despite including the tech bubble

TMT Bubble

Perf

orm

an

ce %

Years

25 16

-18

26

P-I

T\M

erc

ha

nts

Tru

st

The Merchants Trust

Disclaimer

This is no recommendation or solicitation to buy or sell any particular security. Any security mentioned above will not necessarily be comprised in the portfolio by the time this

document is disclosed or at any other subsequent date.

Investing involves risk. The value of an investment and the income from it may fall as well as rise and investors may not get back the full amount invested. The views and opinions

expressed herein, which are subject to change without notice, are those of the issuer and/or its affiliated companies at the time of publication. The data used is derived from various

sources, and assumed to be correct and reliable, but it has not been independently verified; its accuracy or completeness is not guaranteed and no liability is assumed for any direct or

consequential losses arising from its use, unless caused by gross negligence or wilful misconduct. The conditions of any underlying offer or contract that may have been, or will be,

made or concluded, shall prevail.

Investment trusts are quoted companies listed on the London Stock Exchange. Their share prices are determined by factors including the balance of supply and demand in the

market, which means that the shares may trade below (at a discount to) or above (at a premium to) the underlying net asset value.

A trust’s Net Asset Value (NAV) is calculated as available shareholders’ funds divided by the number of shares in issue, with shareholders’ funds taken to be the net value of all the

company’s assets after deducting liabilities. In line with current industry best practice NAVs are now shown that take into account the ‘fair value’ of debt. This means NAVs are

calculated after allowing for the valuation of debt at fair value or current market price, rather than at final repayment value. NAVs with debt at market value provide a more realistic

impact of the cost of debt, and thus a more realistic discount. It is the capital NAV that is shown, which excludes any income.

Past performance is not a reliable indicator of future returns. You should not make any assumptions on the future on the basis of performance information. The value of an investment

and the income from it can fall as well as rise as a result of market fluctuations and you may not get back the amount originally invested. This investment trust charges 65% of its

annual management fee to the capital account and 35% to revenue. This could lead to a higher level of income but capital growth will be constrained as a result.

Merchants seeks to enhance returns for its shareholders through gearing in the form of long-term debentures. Gearing can boost the Trust’s returns when investments perform well,

though losses can be magnified when investments lose value. You should be aware that this Trust may be subject to sudden and large falls in value and you could suffer substantial

capital loss. Derivatives are used to manage the trust efficiently. Covered call options are written to supplement the income generation of the portfolio. This may lead to an opportunity

cost if options are exercised.

All data source Allianz Global Investors as at 31 August 2016 unless otherwise stated. This is a marketing communication issued by Allianz Global Investors GmbH, an investment

company with limited liability, incorporated in Germany, with its registered office at Bockenheimer Landstrasse 42-44, D-60323 Frankfurt/M, registered with the local court Frankfurt/M

under HRB 9340, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht (www.bafin.de). Allianz Global Investors GmbH has established a branch in the United Kingdom,

Allianz Global Investors GmbH, UK branch, 199 Bishopsgate, London EC2M 3TY, which is subject to limited regulation by the Financial Conduct Authority (www.fca.org.uk). Details

about the extent of our regulation by the Financial Conduct Authority are available from us on request.

Web site: www.merchantstrust.co.uk