the methanol report - chemical intelligence · the methanol report december 13, 2015 price...

TRANSCRIPT

© Chemical Intelligence

www.chemicallintelligence.com

1

The Methanol Report

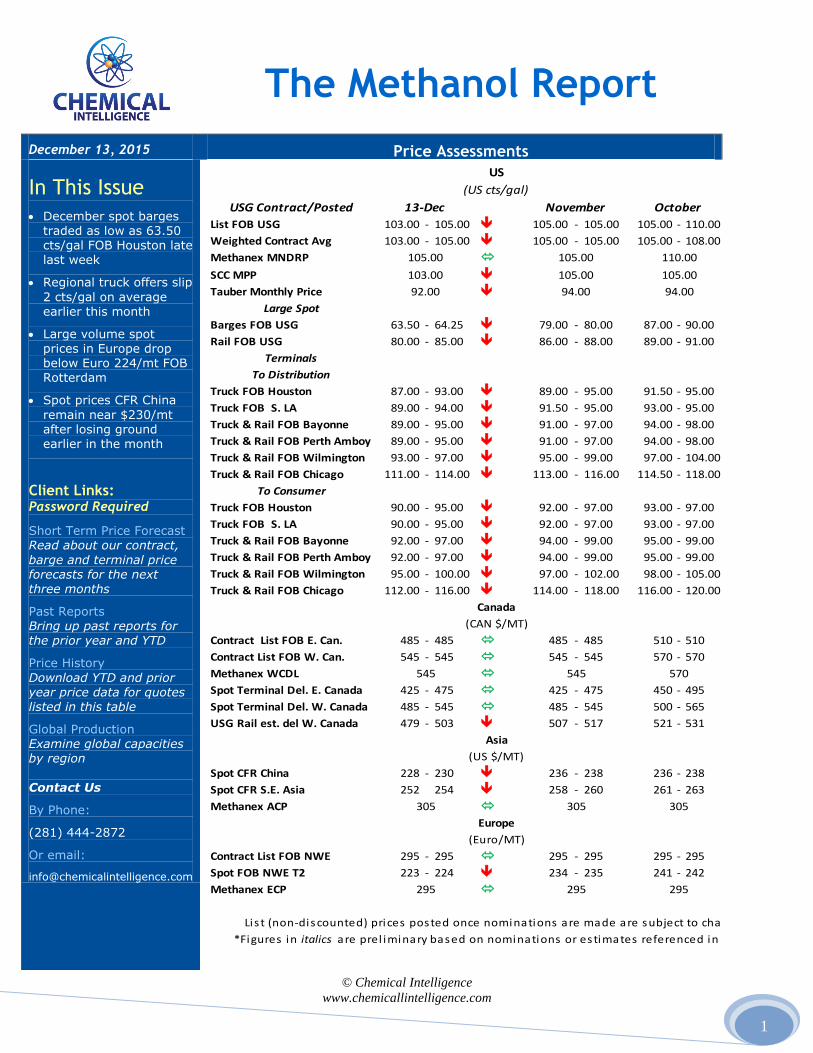

December 13, 2015 Price Assessments

In This Issue

December spot barges traded as low as 63.50 cts/gal FOB Houston late last week

Regional truck offers slip

2 cts/gal on average earlier this month

Large volume spot prices in Europe drop below Euro 224/mt FOB Rotterdam

Spot prices CFR China

remain near $230/mt after losing ground earlier in the month

Client Links: Password Required

Short Term Price Forecast Read about our contract,

barge and terminal price forecasts for the next three months

Past Reports Bring up past reports for the prior year and YTD

Price History

Download YTD and prior year price data for quotes listed in this table

Global Production Examine global capacities by region

Contact Us

By Phone:

(281) 444-2872

Or email:

USG Contract/Posted Q3AVG

List FOB USG 103.00 - 105.00 105.00 - 105.00 105.00 - 110.00 121.17

Weighted Contract Avg 103.00 - 105.00 105.00 - 105.00 105.00 - 108.00 120.67

Methanex MNDRP 122.67

SCC MPP 119.67

Tauber Monthly Price 108.00

Large Spot

Barges FOB USG 63.50 - 64.25 79.00 - 80.00 87.00 - 90.00 89.96

Rail FOB USG 80.00 - 85.00 86.00 - 88.00 89.00 - 91.00 97.83

Terminals

To Distribution

Truck FOB Houston 87.00 - 93.00 89.00 - 95.00 91.50 - 95.00 107.00

Truck FOB S. LA 89.00 - 94.00 91.50 - 95.00 93.00 - 95.00 107.25

Truck & Rail FOB Bayonne 89.00 - 95.00 91.00 - 97.00 94.00 - 98.00 110.50

Truck & Rail FOB Perth Amboy 89.00 - 95.00 91.00 - 97.00 94.00 - 98.00 110.50

Truck & Rail FOB Wilmington 93.00 - 97.00 95.00 - 99.00 97.00 - 104.00 112.83

Truck & Rail FOB Chicago 111.00 - 114.00 113.00 - 116.00 114.50 - 118.00 130.25

To Consumer

Truck FOB Houston 90.00 - 95.00 92.00 - 97.00 93.00 - 97.00 108.67

Truck FOB S. LA 90.00 - 95.00 92.00 - 97.00 93.00 - 97.00 108.83

Truck & Rail FOB Bayonne 92.00 - 97.00 94.00 - 99.00 95.00 - 99.00 112.67

Truck & Rail FOB Perth Amboy 92.00 - 97.00 94.00 - 99.00 95.00 - 99.00 112.67

Truck & Rail FOB Wilmington 95.00 - 100.00 97.00 - 102.00 98.00 - 105.00 107.67

Truck & Rail FOB Chicago 112.00 - 116.00 114.00 - 118.00 116.00 - 120.00 125.33

Contract List FOB E. Can. 485 - 485 485 - 485 510 - 510 552

Contract List FOB W. Can. 545 - 545 545 - 545 570 - 570 612

Methanex WCDL 612

Spot Terminal Del. E. Canada 425 - 475 425 - 475 450 - 495 515

Spot Terminal Del. W. Canada 485 - 545 485 - 545 500 - 565 573

USG Rail est. del W. Canada 479 - 503 507 - 517 521 - 531 522

Spot CFR China 228 - 230 236 - 238 236 - 238 255

Spot CFR S.E. Asia 252 254 258 - 260 261 - 263 285

Methanex ACP 350

Contract List FOB NWE 295 - 295 295 - 295 295 - 295 359

Spot FOB NWE T2 223 - 224 234 - 235 241 - 242 263

Methanex ECP 365

US

Asia

(US $/MT)

Canada

(CAN $/MT)

13-Dec November October

Lis t (non-discounted) prices posted once nominations are made are subject to change.

*Figures in italics are prel iminary based on nominations or estimates referenced in report

Europe

(Euro/MT)

305 305

295 295 295

305

545 545 570

92.00 94.00 94.00

(US cts/gal)

105.00

103.00

105.00

105.00

110.00

105.00

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

2

U.S. Market Summary

Bearish sentiments prevailed last week as

historically low crude prices and increasing

availability sent spot barge prices in the USG

dramatically lower. Although contract postings this

month reflected only a minor change on average,

recent spot prices led to somewhat premature

conjecture about the possibility of sizeable

concessions next month. By the end of last week

spot barge prices had dropped almost 40% below the

current posted contract average. Given that the

historical differential rarely remains much above

20% some observers believe adjustments of more

than 20 cts/gal would be needed if the current

disparity remains in place through the end of the

month. Others caution that several influential

importers maintain the ability to soak up excess spot

material and possibly initiate a near term recovery

before the holidays which could provide a basis for

more moderate concessions in January. This month

Methanex carried forward its US methanol posted price of $1.05/gal after implementing a 5 cts/gal decrease in November while

Southern Chemical Corporation (SCC) lowered its regional posted price 2 cts/gal to $1.03/gal on December 1st after rolling over

last month. Other major suppliers as well as many distributors reported carrying over existing prices this month after doing the

same last month, although a few issued notices of decreases that in several instances took the form of a 2 cts/gal drop. For a

complete list of contract adjustments and related benchmarks (national and regional) current subscribers can click here to access

the client website with your user name and password.

Regional availability continues to improve with the successful startup of new plants in the US Gulf in the last few weeks, although

supply from offshore producers remains impacted by ongoing feedstock constraints. Imports for October dropped 50% as

compared to last year. New supply in the form of the 1.3 mln mt/yr Fairway Methanol JV plant in Clear Lake, Texas started up in

October and reportedly reached full rates last month. A second relocated 1 mln mt/yr Methanex unit is still expected up in

Geismar, Louisiana by the end of the year. Once the new Methanex plant is operational US capacity will reach 5.75 mln mt/yr. As

previously noted in Chile Methanex reportedly started one unit back up on September 25th

after the state oil and gas company

agreed to supply the plant feedstock until at least April of next year allowing it to run at about 40% of capacity. In Trinidad

suppliers report production is still “normal” with gas supply related cuts moving forward expected to remain between 5% and

10%. Production in Venezuela was impacted by reported feedstock constraints that some observers claim remain a source of

concern, although the sellers affected in October appear better supplied at this time. With spot prices in the US seemingly elevated

in prior months there were also reports of imports moving this way during October and early November, although interest quickly

thinned in the following weeks.

Spot prices dropped precipitously last week as sellers attempted to unload volume or in some cases take short positions in

anticipation of a dramatic increase in domestic incremental availability in the coming weeks. Demand among large end users is

still impacted by slow economic conditions within the US and stocks among many buyers remain elevated. At the same time

production costs are low and crude prices remain depressed impacting MTO economics in Asia. To see the last price forecast

please log into the client website at http://www.chemicalintelligence.com.

250

300

350

400

450

500

0

100

200

300

400

500

600

700

Eu

ro

/MT

US

$/M

T

Contract/Benchmark Prices

US Prod Cost est US

China NWE

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

3

U.S. Large Volume Spot Market

Domestic barge assessments eroded quickly last week

amid ongoing concerns about excess availability,

although many traders claimed there were few

confirmed deals done. On Monday traders reported bids

near 74.25/gal with offers at or above 74.75/gal FOB

Houston or St. Rose. On Tuesday there were reports of

offers just above the 70 cts/gal mark with bids perhaps

close to 70 cts/gal. Early in the day one source reported

bids near 70.75/gal and offers at or above 71 cts/gal. By

Wednesday price ideas continued to erode with one

confirmed offer for December reported at 68 cts/gal

early in the day and no corresponding bids. By the end

of the week traders reported deals at progressively lower

prices. December barges were reportedly done at 65

cts/gal, 64.50 cts/gal and 63.50 cts/gal FOB Houston by

Friday. At the end of the day one trader assessed bids

near 63.50/gal and offers at or above 64 cts/gal FOB.

U.S. Terminal Markets

Many small volume spot markets are on the cusp of

correcting according to some regional sellers, although

activity on the whole is still somewhat thin and many

buyers have not actively sought price breaks in order to

drive new sales. This month offers adjusted down 2 cts/gal

on average according to distributors after most suppliers

carried over offers in November. Methanex and those

supplied by the company held small volume prices steady

while a number of other sellers across the country were

reported issuing concessions of as much as 2 cts/gal in

most instances. Downstream demand among seasonal end

users in the gas patch as well as windshield wash

manufacturers is still trailing forecasts with weather across

much of the US still well relatively mild. Inventories

among some service companies are reportedly high and

some are buying on a just in time basis. Slow conditions

and the prospect for increased supply is leading to

increased competition in some markets, although prices

have come under less pressure than many anticipated as liquidity in some cases is constrained due to the lack of spot interest

among consumers. Last month Methanex moved its posted price down 5 cts/gal but small volume spot marketers limited

November decreases to 2 cts/gal or in some cases rollovers.

Truck and railcar prices adjusted marginally lower this month, although many expect further softening in the weeks ahead.

Regional truck and railcar prices in the US Gulf adjusted down as much as 2 cts/gal on average this month according to

distributors and resellers, although with spot based replacement costs lower and competition among suppliers heating up additional

downward consolidation is possible. Several sellers adjusted established posted prices down this month including Tauber which

moved 2 cts/gal lower to 92 cts/gal on December 1st after rolling over last month. Mainstream offers to local distributors

reportedly drifted to 92 cts/al with support attributed to several active sellers near 91 cts/gal, although a few confirmed having to

meet competition nearer the 90 cts/gal mark last week. One active competitive seller is reported moving trucks to distributors as of

last week FOB Houston just under 90 cts/gal and offering FOB East Texas at or below 87 cts/gal. Spot railcar prices to active

distributors were reported near 80 cts/gal FOB Houston roughly a week ago, although with barge prices sharply lower some

contend new deals could occur well below 80 cts/gal. Seasonal demand in the Midwest tapered through last week as mild weather

prompted little restocking among wash manufacturers, many of whom report inventory levels remain high. Initially one local

marketer confirmed lowering offers by a penny, although another local seller later confirmed moving down 2 cts/gal and further

downward consolidation was expected. At the low end of the selling range trucks offers to distributors were reported between

50

70

90

110

130

150

170

190

210

US

cts

/ga

l

U.S. Spot and Terminal Dist. Prices

Barge FOB USG FOB Houston

FOB Bayonne FOB Perth Amboy

FOB Chicago

0%

10%

20%

30%

40%

50%

60%

70%

US

ct

s/g

al

Methanol USG Spot Diff. to Contract

Benchmark

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

4

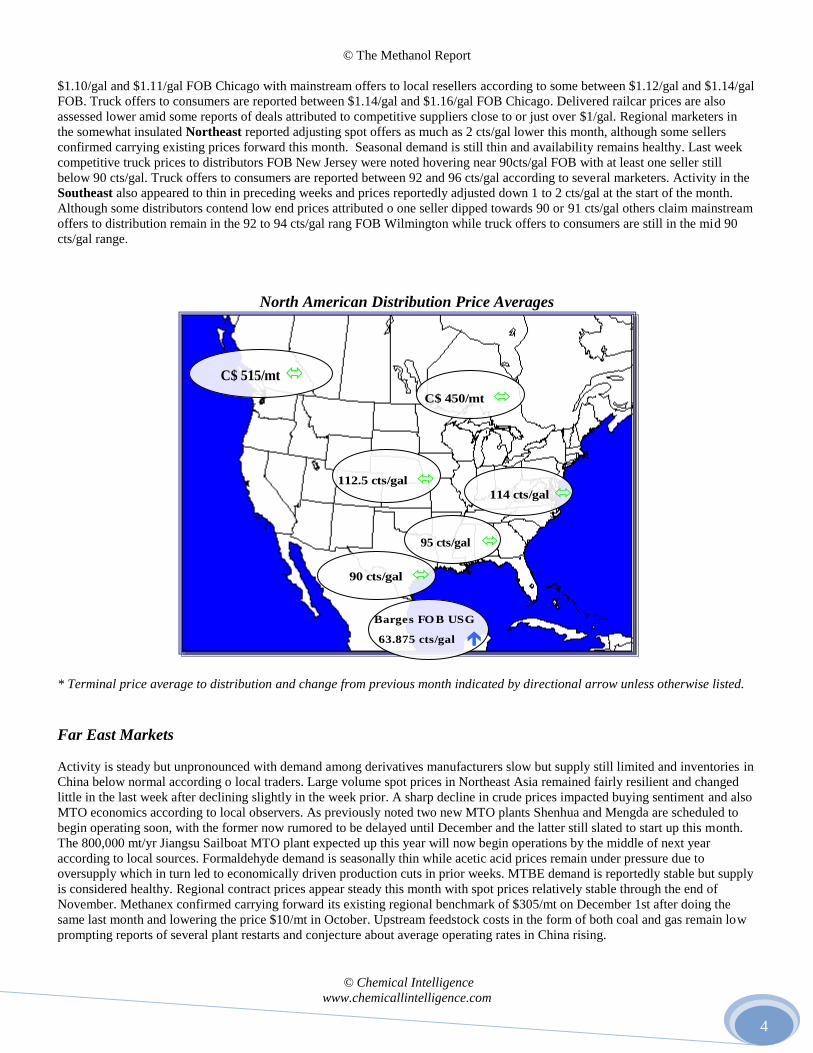

$1.10/gal and $1.11/gal FOB Chicago with mainstream offers to local resellers according to some between $1.12/gal and $1.14/gal

FOB. Truck offers to consumers are reported between $1.14/gal and $1.16/gal FOB Chicago. Delivered railcar prices are also

assessed lower amid some reports of deals attributed to competitive suppliers close to or just over $1/gal. Regional marketers in

the somewhat insulated Northeast reported adjusting spot offers as much as 2 cts/gal lower this month, although some sellers

confirmed carrying existing prices forward this month. Seasonal demand is still thin and availability remains healthy. Last week

competitive truck prices to distributors FOB New Jersey were noted hovering near 90cts/gal FOB with at least one seller still

below 90 cts/gal. Truck offers to consumers are reported between 92 and 96 cts/gal according to several marketers. Activity in the

Southeast also appeared to thin in preceding weeks and prices reportedly adjusted down 1 to 2 cts/gal at the start of the month.

Although some distributors contend low end prices attributed o one seller dipped towards 90 or 91 cts/gal others claim mainstream

offers to distribution remain in the 92 to 94 cts/gal rang FOB Wilmington while truck offers to consumers are still in the mid 90

cts/gal range.

North American Distribution Price Averages

* Terminal price average to distribution and change from previous month indicated by directional arrow unless otherwise listed.

Far East Markets

Activity is steady but unpronounced with demand among derivatives manufacturers slow but supply still limited and inventories in

China below normal according o local traders. Large volume spot prices in Northeast Asia remained fairly resilient and changed

little in the last week after declining slightly in the week prior. A sharp decline in crude prices impacted buying sentiment and also

MTO economics according to local observers. As previously noted two new MTO plants Shenhua and Mengda are scheduled to

begin operating soon, with the former now rumored to be delayed until December and the latter still slated to start up this month.

The 800,000 mt/yr Jiangsu Sailboat MTO plant expected up this year will now begin operations by the middle of next year

according to local sources. Formaldehyde demand is seasonally thin while acetic acid prices remain under pressure due to

oversupply which in turn led to economically driven production cuts in prior weeks. MTBE demand is reportedly stable but supply

is considered healthy. Regional contract prices appear steady this month with spot prices relatively stable through the end of

November. Methanex confirmed carrying forward its existing regional benchmark of $305/mt on December 1st after doing the

same last month and lowering the price $10/mt in October. Upstream feedstock costs in the form of both coal and gas remain low

prompting reports of several plant restarts and conjecture about average operating rates in China rising.

114 cts/gal

95 cts/gal

90 cts/gal

Barges FOB USG

63.875 cts/gal

C$ 515/mt

C$ 450/mt

112.5 cts/gal

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

5

Regional availability is healthy despite low inventory levels in some shore tank locations. In Saudi Arabia Sipchem was expected

to bring down its 1 mln mt/yr IMC plant in Jubail earlier last month for a 45 day turnaround and equipment upgrade that could last

until mid December. In Brunei the planned restart of the 850,000 mt/yr BMC plant that reportedly went down on October 18th

was

reportedly delayed. In Iran one 1.65 mln mt/yr Zagros plant is expected down in December for a 45 day turnaround. In Malaysia

Petronas is reported running its 1.7 mln mt/yr Unit 2 in Labuan at a reduced rate after restarting in October following an extended

turnaround that began in August

Large volume spot prices remained relatively stable through most of last week after drifting lower in the prior week, although

higher prices in other major centers of trade continued to attract more volume away from the region (a dynamic that is starting to

change). On Monday traders reported large spot volumes offered CFR China near $229/mt while prices CFR SE Asia remained

assessed at $252/mt. At the end of the week large volume spot assessments were relatively unchanged with imports CFR CMP

reportedly bid near $228/mt and offered closer to $230/mt while spot CFR SE Asia was reported bid near $252/mt and offered

nearer $254/mt. Late last month prices CFR China were noted near $237/mt with prices CFR SE Asia closer to $259/mt. Steady to

slow demand and adequate supply contributed to balanced markets in Chinese domestic markets. Trading activity appeared light

in most regions. Competitive offers in Eastern provinces were reported as relatively flat in the low CNY 1,800/mt range with

January assessments reported nearly CNY 100/mt lower around CNY 1,725/mt. In the South competitive offers appeared mostly

lat with locals noting offers near or just under CNY 1,880/mt. In the North offers continue to span a wide range between CNY

1,680 and CNY 1,730/mt ex-Hebei.

European Market

Regional demand among large end users is seasonally thin and prices among some derivative producers reportedly eased in the last

two weeks. A sharp drop in crude values along with a minor uptick in the value of the Euro also helped propel spot methanol

assessments lower. Availability is healthy with inland logistics improved after water levels in the Rhine and other tributaries rose.

As previously noted production in Tomsk is still possibly curtailed somewhat but the 1 mln mt/yr Metafrax plant was expected up

in October following a turnaround. The 200,000 mt/yr Kikinda plant in Serbia was also expected to start up by the beginning of

November. The 720,000 mt/yr AzMeCo plant is reportedly operating at roughly half of nameplate with no plans to raise

production after the company suspended gas purchases from Gazprom in Russia. In Egypt the E-Methanex unit in Damietta is

reported idle subject to further gas curtailments. Contract prices could adjust lower in Q1, although conjecture about the magnitude

is still premature.

Large volume spot prices moved progressively lower through last week amid concerns about oversupply, both globally and within

Europe. On Monday traders reported relatively slow conditions with bids and offers on either side of Euro 228.50 /mt FOB

Rotterdam T2. By midweek traders reported both bids and offers trending lower with both near or below the Euro 225/mt mark.

Late in the week spot was reported lower near Euro 223.50/mt (two weeks prior spot was noted closer to Euro 235/mt).

Canadian Market

Mild weather across the East and West continues to impact demand among seasonal end users, although a steady decline in the

value of the Canadian dollar helped to offset lower methanol costs in recent months. The value of the Canadian dollar as

compared to the US dollar dropped over 15% during the course of the year and in the last month the value of the Canadian dollar

dropped another 3%. With demand sluggish regional availability is healthy with no reports of logistical issues noted as of last

week. Wash sales are slow with many blenders reporting inventories high pending the first wave of winter weather. Demand into

the gas patch is also thin with some service companies claiming business in the West is down 20% or more as compared to last

year. The prospect of price corrections in the near term is also impacting demand among consumers. This month contract and spot

prices were largely unchanged according to distributors as many claim most sellers were reluctant to pass on minor concessions

once a major supplier announced a rollover. Others suggest easing is inevitable with spot based replacement costs in the US

dramatically lower. This month prices reportedly settled down as much as CAN $25/mt in line with producer announcements after

rolling over last month. In September US benchmarks dipped US 15 cts/gal (CAN $65/mt) to US 18 cts/gal (CAN $78/mt) and

spot in many markets appeared to drop US 15 cts/gal (CAN $65/mt) to 17 cts/gal (CAN $73.50/mt), but producer led decreases in

Canada reportedly averaged CAN $50/mt

Activity in the West is flat or only slightly improved according to several distributors contacted late last week, although sales on

the whole continue to trail forecasts and mild temperatures are expected to remain in place through the remainder of the month.

Demand among service companies in the gas patch is still thin amid ongoing reports of cost cutting measures. Availability is

healthy with no reports of any logistical issues or delays and supply augmented by intermittent railcar imports. This month

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

6

Methanex carried forward its Western Canadian Distributor List (WCDL) price of CAN $545/mt following a CAN $25/mt drop

last month and a rollover in October. Other suppliers were reportedly also rolling over this month, although in some cases their

costs were expected to move down. Although prices remain relatively steady at this time and many distributors and resellers are

holding what would now be considered high cost inventory, USG based replacement costs eroded significantly last week which

will likely impact local offers in the near future. At this time small volume spot prices at the low end of the range to distributors

remain stable on either side of CAN $500/mt FOB Edmonton. Small volume offers to service companies and end users are

reported in a wider range between CAN $535/mt and CAN $550/mt FOB Edmonton.

Similarly, overall activity in the East is also subdued in a large part due to the relatively mild weather of late in the region, and

prices remained largely unchanged through last week. Seasonal wash manufacturers confirm sales are lagging expectations with

resellers and retailers holding high inventories. Some buyers continue to take just in time quantities, although most are reluctant to

accumulate much given the likelihood for further easing. This month Methanex carried forward existing prices and other sellers

reportedly did the same despite receiving minor supplier led concessions, although many buyers expect prices to ease in the near

future. At this time spot trucks delivered Quebec are assessed stable in the low to mid $400/mt range amid some rumors of volume

moving below CAN $400/mt. Small volume spot delivered lower Ontario is also reported steady between CAN $470/mt and CAN

$500/mt.

Derivative Markets

Downstream demand among large end users remains

tepid with no marked improvement noted among

several buyers last week. In some cases the strength

of the US dollar has reportedly impacted exports

among some derivative producers. Construction and

housing markets within the US remain seasonally

slow and wood products manufacturers reported

structural panel prices under pressure once again last

week as some sellers attempted to move existing

inventory. Seasonal wash blenders report slower

than anticipated conditions across the country as

mild weather continues to impact sales among

jobbers and retailers.

Natural Gas

Mild temperatures across key consuming areas of the US continues to

impact consumption and send gas prices lower while high global

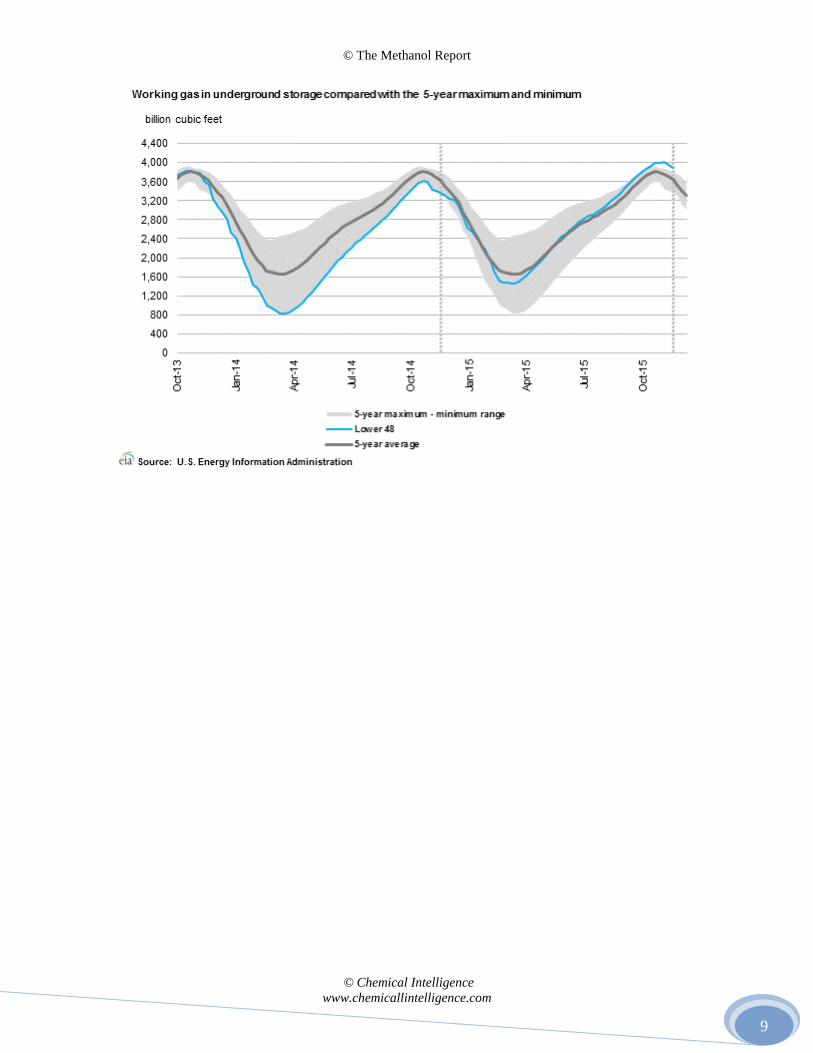

inventories put pressure on crude values once again last week. The EIA

reported U.S. natural gas inventories posted their first decline of the

winter heating season in late November, but natural gas inventories at

the end of December are expected to be the third highest ever for the

month.” Baker Hughes reported US gas rigs down 7 at 185, off 161 rigs

compared to last year. Operating oil rigs slipped

21 to 524, down 1022 from a year prior. In

Canada gas rigs rose by 1 to 101, still down 115

compared to a year prior, while oil rigs dropped

by 4 to 73, down by 142 compared to a year prior.

Oil and gas rigs operating in the US are at their

lowest combined level since 1999.

700

800

900

1000

1100

1200

1300

Sta

rts

Seasonally Adjusted Housing Starts

Total for lower 48 States 379

Change from prior week (1)

Compared with last year 18

Compared with 5 year average 32

US Gas Stocks as of 12/13/2015

Price Change Pct change from year ago

Henry Hub Spot $1.91 -9 -39.27%

NYMEX Jan16 $2.02 -5 -32.18%

NYMEX 12 Month Strip $2.32 -2 -24.57%

Aeco Spot $2.25 -5 -20.89%

Dawn $2.63 -12 -45.63%

Gas Prices

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

7

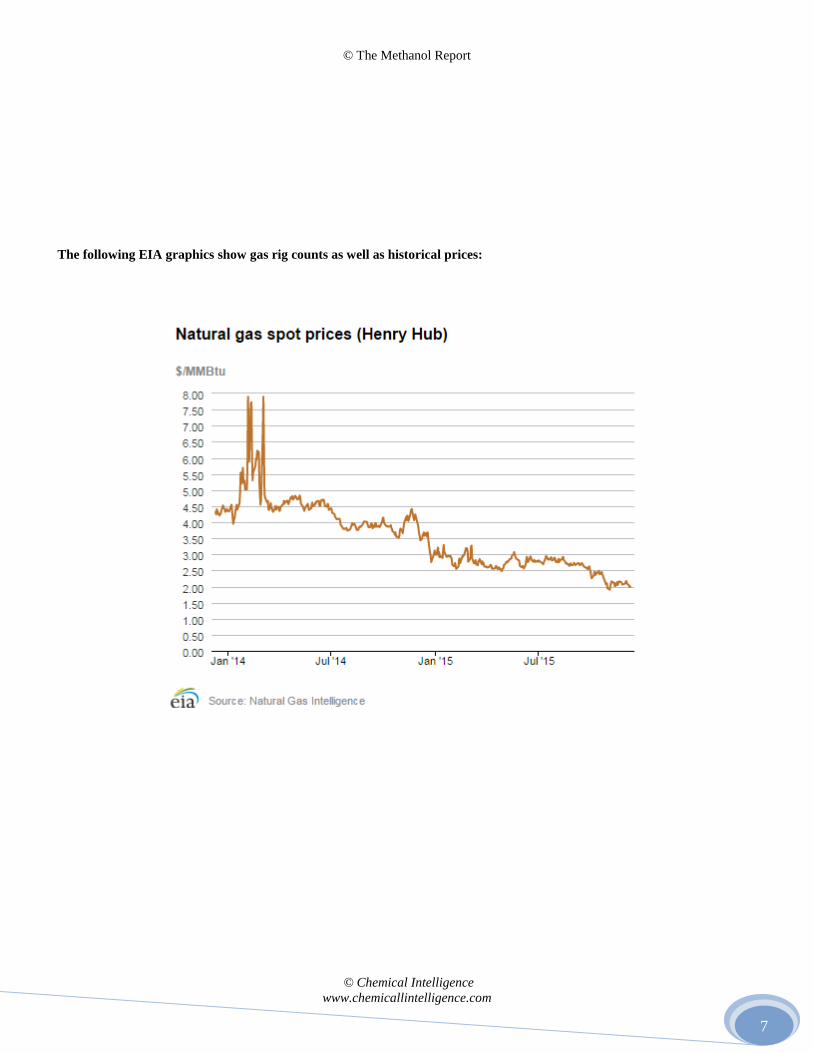

The following EIA graphics show gas rig counts as well as historical prices:

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

8

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

9

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

10

Planned & Unplanned Outages

Company Product Location Cap. (mt/yr) Dates Details

Ampco Methanol Eq. Guinea 1,000,000 Feb 2015 T/R set for Feb. 1st.

Atlas Methanol Pt. Lisas, Trinidad 1,650,000 Apr 2015 Gas cut to 30% 1 week

AzMeCo Methanol Karadag, Azerbaijan 720,000 Oct- 2015 RR

BMC Methanol Brunei 850,000 March 2015 TR 75 days

BP Methanol Gelsenkirchen, Ger. 100,000 Aug 31 2015 7 week T/R

E-Methanex Methanol Damietta, Egypt 1,300,000 Feb 2015-Nov S/D

Fanavaran Methanol Bandar Imam, Iran 1,000,000 Dec 17-Jan ‘14 S/D due to gas shortage

GPIC Methanol Sitra, Bahrain 430,000 Mar-Apr 2015 2 week T/R

GNFC Methanol Gujarat, India 290,000 April 2014 T/R

IMC Methanol Jubail, S. Arabia 1,000,000 Nov 2015 45day T/R

Jiutai Methanol Erdos, Mongolia 1,000,000 July 7-17 Maintenance

Kaltim Methanol Bontang, Indonesia 660,000 Oct 20-Dec 4 ‘15 T/R

Kharg Methanol Kharg Island, Iran 660,000 Nov 11-Dec 2 ‘14 T/R

LyondellBasell Methanol Channelview, TX 780,000 Q1 2015 T/R

M5000 Methanol Pt. Lisas, Trinidad 1,890,000 April 2015- Gas curtailments

Metafrax Methanol Gubakha, Russia 1,000,000 Sep-Oct 2015 T/R

Methanex Methanol Medicine Hat, AB 600,000 Dec -Jan 10 ‘14 Unplanned outage

Methanex Methanol Chile 1, Punta Arenas 1,000,000 Nov 2015- 40% OR

Metor I Methanol Jose, Venezuela 730,000 April 2015 Gas leak, disruptions

Millennium Methanol LaPorte, TX 600,000 Feb 2014 T/R

NOC Methanol Marsa El Brega,Libya 330,000 Ongoing RR since SU Mar 2013

OCI Methanol Beaumont, TX 912,500 Feb-Apr. 2015 Debottleneck

OMC Methanol Sohar, Oman 1,000,000 Jan –Mar 2015 Extended T/R.

Petronas Methanol Labuan, Malaysia 1,700,000 Aug-Sep 2015 45 Day T/R

Petronas Methanol Labuan, Malaysia 660,000 Aug-Oct 2014 TR 60 days

Qafac Methanol Qatar 990,000 Mar 2014 Planned T/R

Salalah Methanol Salalah, Oman 1,000,000 Jan 2015 T/R

Supermetanol Methanol Jose, Venezuela 730,000 April 2015 Reported disruptions

Tchekinoazot Methanol Russia 450,000 April 24-May 24 T/R

Zagros 1 Methanol Assaluyeh, Iran 1,650,000 Mar -May 2015 Outage

Zagros 2 Methanol Assaluyeh, Iran 1,650,000 Nov 2015 T/R

© The Methanol Report

© Chemical Intelligence

www.chemicallintelligence.com

11

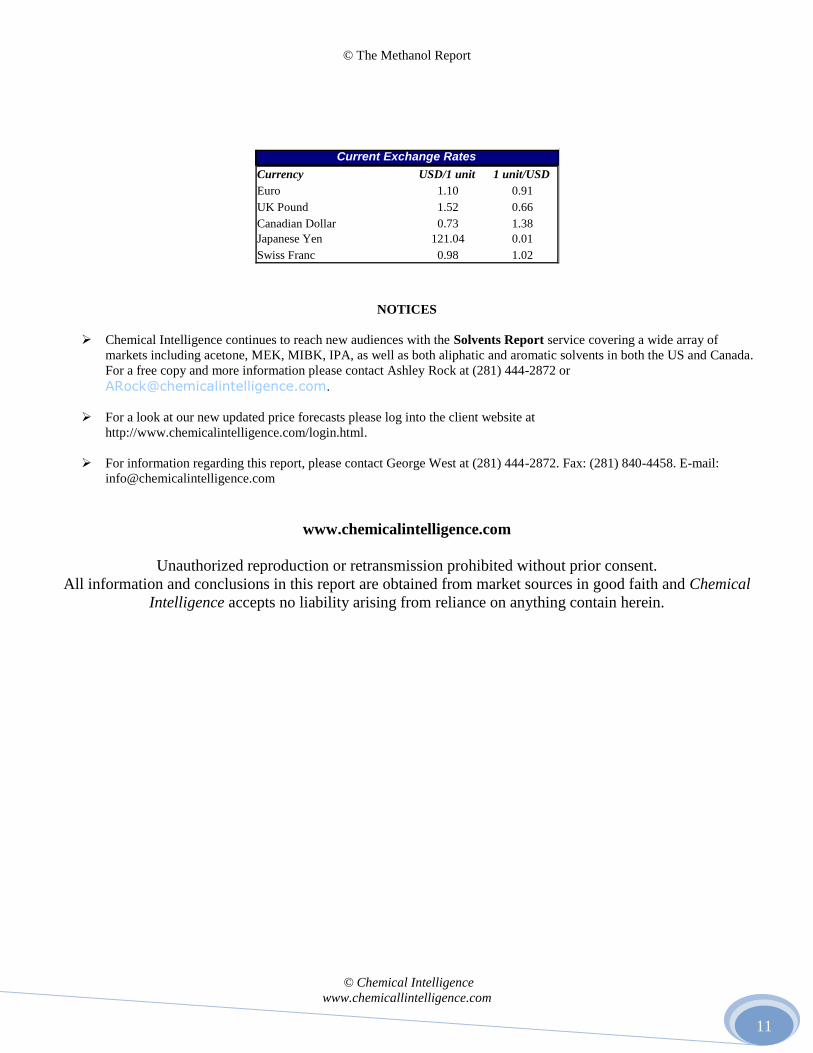

Currency USD/1 unit 1 unit/USD

Euro 1.10 0.91

UK Pound 1.52 0.66

Canadian Dollar 0.73 1.38

Japanese Yen 121.04 0.01

Swiss Franc 0.98 1.02

Current Exchange Rates

NOTICES

Chemical Intelligence continues to reach new audiences with the Solvents Report service covering a wide array of

markets including acetone, MEK, MIBK, IPA, as well as both aliphatic and aromatic solvents in both the US and Canada.

For a free copy and more information please contact Ashley Rock at (281) 444-2872 or

For a look at our new updated price forecasts please log into the client website at

http://www.chemicalintelligence.com/login.html.

For information regarding this report, please contact George West at (281) 444-2872. Fax: (281) 840-4458. E-mail:

www.chemicalintelligence.com

Unauthorized reproduction or retransmission prohibited without prior consent.

All information and conclusions in this report are obtained from market sources in good faith and Chemical

Intelligence accepts no liability arising from reliance on anything contain herein.