the microbanking bulletin spring 2009

DESCRIPTION

MIX is a non-profit company thatworks to support the growth and development of ahealthy microfinance sector. MIX is supported by theConsultative Group to Assist the Poor (CGAP), CitigroupFoundation, Deutsche Bank Americas Foundation,Omidyar Network, Open Society Institute, and others.To learn more about MIX, please visit the website atwww.themix.org.TRANSCRIPT

The

MicroBanking

BulleTin

Issue No. 18Spring 2009

A publicAtion DeDicAteD to the performAnce of orgAnizAtionS thAt proviDe bAnking ServiceS for the poor

Copyright (c) 2009

Microfinance Information Exchange, Inc.

The MicroBanking Bulletin is published twice annually by Microfinance Information Exchange, Inc.

ISSN 1934-3884. Copyright 2009. All rights reserved. The data in this volume have been carefully compiled and are believed to be accurate. Such accuracy is not however guaranteed. Feature articles in MBB are the property of the authors and permission to reprint or reproduce these should be sought from the authors directly. The publisher regrets it cannot enter into correspondence on this matter. Otherwise, no portion of this publication may be reproduced in any format or by any means including electronically or mechanically, by photocopying, recording or by any information storage or retrieval system, or by any form or manner whatsoever, without prior written consent of the publisher of the publication.

Prepared by: Job Continent Inc. www.jobcontinent.com

We would like to thank the following institutions for their participation in this issue: REGION COUNTRY # MFIS NaME OF PaRTICIPaNT

africa Benin 2 PADME, Vital Finance(69 MFIs) Burkina Faso 1 RCPB Cameroon 3 CamCCUL, CCA, CDS Congo 1 CAPPED Congo, Democractic Republic of 1 FINCA-DRC Ethiopia 12 ACSI, AVFS, BG, DECSI, Eshet, Gasha, Metemamen, OMO, PEACE, SFPI, Wasasa, Wisdom Ghana 13 APED, Bessfa RB, CFF, FASL, Kakum RB, Maata-N-Tudu, Naara RB, OISL, ProCredit-GHA, SAT, Sonzelle RB, Toende RB, Upper Manya RB Kenya 6 Equity Bank, KADET, K-Rep, KWFT, MDSL, SMEP Malawi 1 FINCA-MWI Mali 4 Jemeni, Kafo Jiginew, Kondo Jigima, Nyèsigiso Mozambique 5 BOM, FCC, FDM, NovoBanco-MOZ, Tchuma Nigeria 2 LAPO, SEAP Rwanda 1 UOMB Senegal 2 ACEP Senegal, CMS South Africa 2 Capitec Bank, SEF-ZAF Swaziland 1 FINCORP Tanzania 4 Akiba, FINCA-TZA, PRIDE-TZA, SEDA Togo 2 FUCEC Togo, WAGES Uganda 5 Centenary Bank, Faulu-UGA, FINCA-UGA, MED-Net, UML Zambia 1 FINCA-ZMB

asia Afghanistan 5 ARMP, BRAC-AFG, FINCA-AFG, FMFB-AFG, Parwaz(117 MFIs) Bangladesh 7 ASA, BRAC, BURO Bangladesh, Grameen Bank, IDF, JCF, TMSS Cambodia 9 ACLEDA, AMK, AMRET, CREDIT, HKL, PRASAC, Sathapana Limited, TPC, VFC China 1 CZWSDA India 32 ABCRDM, AML, AMMACTS, Bandhan, BASIX, BFL, BISWA, BSS, Cashpor MC, CReSA, ESAF, GK, GU, GV, KAS, KBSLAB, KRUSHI, Mahasemam-

SMILE, MFI, RASS, RGVN, Saadhana, Sanghamithra, Sarvodaya Nano Finance, SHARE, SKDRDP, SKS, SMSS, Spandana, SWAWS, Ujjivan, VFS Indonesia 12 LPD Ambengan, LPD Bayung Gede, LPD Bedha, LPD Buahan, LPD Celuk, LPD Ketewel, LPD Kukuh, LPD Kuta, LPD Pecatu, LPD Sibetan,

LPD Ubung, MBK Ventura Nepal 4 DD Bank, MGBB, Nirdhan, PGBB Pakistan 6 DAMEN, FMFB-Pakistan, Kashf, Khushhali Bank, NMFB, Rozgar Philippines 37 1st Valley Bank, ABS-CBN, ASHI, Banco Santiago de Libon, Bangko Kabayan, Bangko Mabuhay, BCB, Cantilan Bank, CARD Bank, CARD

NGO, CBMO, CEVI, CMEDFI, ECLOF-PHL, FCBFI, FICO, Green Bank, Kasagana-Ka, Kazama Grameen, KMBI, Mallig Plains RB, MEDF, New RB of Victorias, NWTF, OMB, PALFSI, RB Digos, RB Lebak, RB Mabitac, RB Oroquieta, RB Solano, RB Sto. Tomas, RB Talisayan, TSKI, TSPI, Valiant RB, VEF

Samoa 1 SPBD Sri Lanka 1 SEEDS Thailand 1 SED Vietnam 1 CEP

ECa Albania 3 BESA, Opportunity Albania, ProCredit Bank-ALB(98 MFIs) Armenia 8 ACBA, AREGAK, ECLOF-ARM, FINCA-ARM, Horizon, INECO, KAMURJ, SEF-ARM Azerbaijan 9 AccessBank, Azercredit, Azeri Star, CredAgro NBCO, FINCA-AZE, FinDev, MikroMaliyye Credit, Normicro, Viator Bosnia and Herzegovina 13 EKI, LIDER, LOK Microcredit Foundation, MI-BOSPO, MIKRA, Mikro ALDI, MIKROFIN, Partner, PRIZMA, ProCredit Bank-BIH, SINERGIJA,

Sunrise, Women for Women Bulgaria 4 Mikrofond, Nachala, ProCredit Bank-BGR, USTOI Croatia 2 DEMOS SLC, NOA Georgia 7 CREDO, Crystal, FINCA-GEO, ImerCredit, JSC Bank Constanta, Lazika Capital, ProCredit Bank-GEO Kazakhstan 2 Bereke, KMF Kosovo 7 AFK, BZMF, FINCA-KOS, KEP, KosInvest, KRK Ltd, ProCredit Bank-KOS Kyrgyzstan 4 Aiyl Bank, Bai Tushum, FMCC, Kompanion Macedonia, Former Yugoslav Republic of 4 FULM, Horizonti, Moznosti, ProCredit Bank-MKD Moldova 2 Microinvest, ProCredit-MDA Mongolia 3 Khan Bank, TFS, XacBank Montenegro 2 AgroInvest, OBM Poland 1 Fundusz Mikro Romania 3 CAPA, OMRO, ProCredit Bank-ROM Russia 11 Alternativa, CEF, FFECC, FORUS, Intellekt, KMB, Rost, SBS, Sodeistviye (Pyatigorsk), Sodeystviye, VRFSBS Serbia 3 MDF, OBS, ProCredit Bank Serbia Tajikistan 8 Agroinvestbank, Bank Eskhata, FINCA-TJK, FMFB TJK, Imkoniyat, IMON, MLF HUMO, MLF MicroInvest Ukraine 2 HOPE, ProCredit Bank-UKR

LaC Argentina 2 FIE Gran Poder, Grameen Mendoza(179 MFIs) Bolivia 17 AgroCapital, BancoSol, Coop Fátima, CRECER, Diaconia, EcoFuturo FFP, Emprender, FADES, Fassil FFP, FIE FFP, FONCRESOL, Fortaleza

FFP, FUNBODEM, IMPRO, ProCredit-BOL, PRODEM FFP, ProMujer-BOL Brazil 5 Banco da Familia, CEADe, CEAPE Maranhão, CrediAmigo, ICC BluSol Chile 3 BancoEstado, BanDesarrollo Microempresas, Credicoop Colombia 14 Actuar Caldas, Actuar Tolima, BCSC, CMM Bogotá, CMM Medellín, Contactar, FinAmérica, FMM Bucaramanga, FMM Popayán, FMSD,

Interactuar, Microempresas de Antioquia, OLC, WWB Cali Costa Rica 7 ACORDE, ADRI, CREDIMUJER, FIDERPAC, FOMIC, Fundación Mujer, FUNDECOCA Dominican Republic 3 ADOPEM, Banco ADEMI, Fundación San Miguel Ecuador 20 Banco Solidario, CEPESIU, COAC Acción Rural, COAC Jardín Azuayo, COAC MCCH, COAC Mushuc Runa, COAC Sac Aiet, COAC San

José, CODESARROLLO, Credi Fé, D-Miro, FED, FINCA-ECU, FODEMI, Fundación Alternativa, Fundación Espoir, FUNDAMIC, INSOTEC, ProCredit-ECU, UCADE Ambato

El Salvador 10 ACCOVI, AMC de R.L., Apoyo Integral, ASEI, ENLACE, Fundación CAMPO, FUNSALDE, Genesiss, ProCredit-SLV, Sociedad Cooperativa PADECOMSM

Guatemala 15 AGUDESA, ASDIR, Asociación Raíz, AYNLA, CDRO, CRYSOL, FAFIDESS, FAPE, FINCA-GTM, FONDESOL, Friendship Bridge, Fundación MICROS, FUNDEA, FUNDESPE, Génesis Empresarial

Haiti 4 ACME, Fonkoze, MCN, SOGESOL Honduras 10 ADICH, BanCovelo, FAMA OPDF, FINCA-HND, FINSOL, FUNDAHMICRO, FUNED, Hermandad de Honduras OPDF, ODEF Financiera S.A.,

World Relief-HND Mexico 7 ADMIC, ASP Financiera, Caja Popular Mexicana, CompartamosBanco, FINCA-MEX, FinComún, ProMujer-MEX Nicaragua 16 ACODEP, ADIM, BANEX (ex FINDESA), CEPRODEL, FDL, Financiera Fama, FINCA-NIC, FODEM, Fundación León 2000, Fundación

Nieborowski, FUNDENUSE, FUNDESER, PRESTANIC, ProCredit-NIC, PRODESA, ProMujer-NIC Panama 2 Microserfin, ProCaja Paraguay 6 Coop Universitaria, FIELCO, Financiera Familiar, Fundación Paraguaya, Interfisa, Visión Banco Peru 37 ADRA-PER, AMA, Asociación Arariwa, Caja Nor Perú, Caritas, CMAC Arequipa, CMAC Cusco, CMAC Del Santa, CMAC Huancayo, CMAC

Ica, CMAC Maynas, CMAC Paita, CMAC Sullana, CMAC Tacna, CMAC Trujillo, COOPAC San Martín, COOPAC Santo Cristo, CRAC Los Andes, Crediscotia, EDAPROSPO, EDPYME Alternativa, EDPYME Confianza, EDPYME Crear Arequipa, EDPYME Crear Tacna, EDPYME Efectiva, EDPYME Nueva Visión, EDPYME Proempresa, Financiera Edyficar, FINCA-PER, FONDESURCO, FOVIDA, IDESI Lambayeque, Manuela Ramos, MiBanco, MIDE, PRISMA, ProMujer-PER

Venezuela 1 BanGente

MENa Egypt 6 ABA, Al Tadamun, CEOSS, DBACD, Lead Foundation, SBACD(24 MFIs) Jordan 4 AMC, MEMCO, MFW, Tamweelcom Lebanon 2 Al Majmoua, Ameen Morocco 7 Al Amana, Al Karama, AMSSF/MC, FBPMC, FONDEP, INMAA, Zakoura Palestine 2 FATEN, UNRWA Tunisia 1 Enda Yemen 2 Azal, NMF

Abbreviations: ECA = Eastern Europe & Central Asia; LAC = Latin America & the Caribbean; MENA = Middle East & North Africa.

The MicroBanking Bulletin is one of the principal publications of MIX (Microfinance Information Exchange, Inc.). MIX is a non-profit company that works to support the growth and development of a healthy microfinance sector. MIX is supported by the Consultative Group to Assist the Poor (CGAP), Citigroup Foundation, Deutsche Bank Americas Foundation, Omidyar Network, Open Society Institute, and others. To learn more about MIX, please visit the website at www.themix.org.

PurposeBy collecting financial and portfolio data provided voluntarily by leading microfinance institutions (MFIs), organizing the database by peer groups, and reporting this information, MIX is building infrastructure that is critical to the development of the microfinance sector. The primary purpose of this database is to help MFI managers and board members understand their performance in comparison to other MFIs. Secondary objectives include establishing industry performance standards, enhancing the transparency of financial reporting, and improving the performance of microfinance institutions.

Benchmarking ServicesTo achieve these objectives, MIX provides the following benchmarking services: 1) the Bulletin’s Tables; 2) customized financial performance reports; and 3) network services.

MFIs participate in the MicroBanking Bulletin benchmarks database on a quid pro quo basis. They provide MIX with information about their financial and portfolio performance, as well as details regarding accounting practices, subsidies, and the structure of their liabilities. Participating MFIs must submit substantiating documentation, such as audited financial statements, annual reports, ratings, institutional appraisals, and other materials that help us understand their operations. With this information, we apply adjustments for inflation, subsidies and loan loss provisioning in order to create comparable results. Data are presented in the Bulletin anonymously within peer groups. While MIX performs extensive checks on the consistency of data reported, we do not independently verify the information.

In return, participating institutions receive a comparative performance report (CPR). These individualized

benchmark reports, which are an important output of the benchmarks database, explain the adjustments we made to the data, and compare the institution’s performance to that of peer institutions. MFI managers and board members use these tools to understand their institution’s performance in a comparative context.

The third core service is to work with networks of microfinance institutions (i.e., affiliate, national, regional), central banks, and researchers in general to enhance their ability to collect and manage performance indicators. MIX provides this service in a variety of ways, including 1) training these organizations to collect, adjust and report data on retail MFIs at the local level and use MIX’s performance monitoring and benchmarking software, 2) collecting data on behalf of a network, and 3) providing customized data analysis to compare member institutions to peer groups. This service to networks, regulatory agencies, and researchers allows MIX to reach a wider range of MFIs in order to improve their financial reporting.

New ParticipantsInstitutions that wish to participate in the Bulletin database should contact: [email protected], Tel +1 202 659 9094, Fax +1 202 659 9095. Currently, the only criterion for participation is the ability to fulfill fairly onerous reporting requirements. MIX reserves the right to establish minimum performance criteria for participation in the Bulletin database.

SubmissionsThe Bulletin welcomes submissions of articles and commentaries, particularly regarding analytical work on the financial performance of microfinance institutions. Submissions may include reviews or summaries of more extensive work published elsewhere. Articles should not exceed 2,500 words. To submit an article, please contact Elizabeth Downs, Managing Editor, at [email protected].

Disclaimer Neither MIX, MBB’s Editorial Board nor do MIX’s funders accept responsibility for the validity of the information presented or consequences resulting from its use by third parties.

The MicroBanking Bulletin (MBB)

The MicroBanking Bulletin

issue no. 18

spring 2009

Dedicated to the performance of organizations that provide banking services for the poor.

ediTorial sTaff

Publisher:

Peter Wall, Executive Director, MIX

Managing Editor:

Elizabeth Downs, Director of Marketing and Communications, MIX

ediTorial Board

Craig F. Churchill International Labour Organization

Asad Mahmood Deutsche Bank

J.D. Von Pischke Frontier Finance International

Elisabeth Rhyne ACCION International

Gabriel Solorzano BANEX

Chairman Emeritus:

Robert Peck Christen

The MicroBanking Bulletin is a publication of MIX (Microfinance Information Exchange, Inc.) To learn more about MIX, please visit the MIX website at www.themix.org

TaBle of conTenTs

From the Publisher ..............................................................................................................................................vii

feaTure arTicles

The Impact of Inflation on Microfinance Clients and its Implications for Microfinance Practitioners ............................................................................................................................................................ 1

S. Akbar Zaidi, Maheen Saleem Farooqi and Aleena Naseem, for the Pakistan Microfinance Network

Elevated Food Prices — Impact on Microfinance Clients ....................................................................... 6 Zaved Ahmed and Camilla Nestor, Grameen Foundation

Microfinance: Where Do We Stand Today? .................................................................................................. 9 By Ajit Jain and Caroline Norton, Deutsche Bank

The Impact of the Financial Crisis on Microfinance Institutions — Results froma CGAP Survey ......................................................................................................................................................13 Xavier Reille and Christoph Kneiding, CGAP

BulleTin highlighTs

Breaking It Down: Subsidy Dependence Index vs. Financial Self-Sufficiency ................................16 Scott Gaul, Product Development Manager, MIX

MFI Trend Lines Analysis ...................................................................................................................................20 Blaine Stephens, COO, MIX

BulleTin TaBles

Introduction to the Peer Groups and Tables .............................................................................................27

Trend Lines 2005 – 2007 MFI Benchmarks .................................................................................................29

Institutional Characteristics ................................................................................................................29

Financing Structure ...............................................................................................................................30

Outreach Indicators ...............................................................................................................................31

Macroeconomic Indicators .................................................................................................................34

Overall Financial Performance ...........................................................................................................35

Revenues ...................................................................................................................................................37

Expenses ....................................................................................................................................................37

Efficiency ...................................................................................................................................................38

Productivity ..............................................................................................................................................39

Risk and Liquidity ...................................................................................................................................40

Index of Terms and Definitions .......................................................................................................................41

Index of Indicators and Definitions ...............................................................................................................43

Guide to Peer Groups — Trend Lines 2005 – 2007 MFI Benchmarks ...............................................45

appendices

Appendix I : Notes to Adjustments and Statistical Issues .......................................................................74

Appendix II : Participating MFIs Trend Lines 2005 – 2007 Benchmarks .............................................77

vii

T his issue of the MicroBanking Bulletin focuses on the impacts of the current global economic crises on microfinance. Yes, I do mean “crises”

in the plural, because there are at least two global crises underway. While much of the world’s attention naturally focuses on the epicenters of the global financial crisis, whose ‘tsunami effects’ of toxic asset dumping and deflation are spilling over far and wide, one shouldn’t forget that an inflation crisis affecting the food prices began much earlier and continues to grow. The UN’s Food and Agricultural Organization recently reported an increase of 150 million chronically hungry people in developing economies in 2008 – 2009, with prospects of worse to come.

So, in many developing countries, the poor increasingly face the worst of all possible worlds – inflation which pushes prices of food and shelter beyond their already thin means and which destroys any savings they may have accumulated, and credit squeezes (if they had any access to credit at all previously), as financial liquidity dries up throughout financial systems. To these woes are added the decline in remittances to families in developing economies as jobs dry up in developed economies, and price increases associated with currency depreciations.

To return to the earthquake and tsunami analogies, microfinance operations will be affected differently in different countries depending on their distance from the epicenters, to their prior exposures/dependence to foreign funding, and on whether they have ‘safe harbors’ or not. Research on microfinance institutions’ (MFIs) resilience to past macroeconomic crises, including work by MIX, has shown MFIs to have been fairly robust. But the extent of globalization of economies in general and domestic and cross-border commercial funding of microfinance has grown

dramatically since the last major test (Asia Crisis, 1997-2000). MFIs’ relationships to the crises’ epicenters have greatly intensified. Also, domestic savings’ funding of microfinance grew greatly in the period, and it remains to be seen how the poor’s savings patterns will react in an extended deep crisis.

The microfinance industry has been alert to the problems, and active in trying to get its hands around the extent and direction in a fast-changing environment. Publicly available reports on this include surveys recently released by Intellecap and the rating service MicroRate (focusing on Latin America). Both are highly recommended reading, as their findings illustrate a wide range of reactions and perceptions among MFIs and investors. As the MicroRate report notes, those shifted over a matter of weeks from the time MicroRate first began their research until they had completed it, as the tsunami began to show up.

The articles and analyses in this issue of MBB bring together some of the first broader global overviews of the impact of the crises, and how MFIs are coping. While we at MIX recognize that the situations are evolving quickly and that this issue of MBB will very likely not be the last to have a focus on microfinance and the global tsunami, we hope it sets a benchmark of how things looked, close to the start.

As I step down as executive director of MIX at the end of June, this is my last letter as publisher of MBB. It has been a privilege to be associated with MBB, and a pleasure to work with the Editorial Board and its editors. I look forward eagerly to reading future issues of MBB as another of its thousands of readers.

- Peter Wall, Publisher, MicroBanking Bulletin

From the Publisher Microfinance in the Global Tsunami — Will It Stay Afloat?

1 “Microfinance and the Global Recession”, Microfinance Insights, Mar/April 20092 “Cautious Resilience: The Impact of the Global Financial Crisis on Latin American and Caribbean Microfinance Institutions”, MFI Insights, March 2009, MicroRate, Inc.

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

1Microfinance Information Exchange, Inc

FEATURE ARTICLEs

The Impact of Inflation on Microfinance Clients and its Implications for Microfinance

A study undertaken by S Akbar Zaidi, Maheen Saleem Farooqi and Aleena Naseem, for the Pakistan Microfinance Network

MICROBANKING BULLETIN, IssUE 18, sPRING 2009

Introduction

As the inflation rate in Pakistan crosses 25 percent per annum — the highest in almost three decades — there is justifiable concern

that the Pakistani citizen, particularly the poor, will suffer the most and will bear the severest brunt of this economic crisis. Moreover, along with rising prices, indications suggest that Pakistan’s economy is also facing serious constraints and the high growth rates between 2002 – 2007 may have slowed down considerably, affecting economic opportunities for all, but particularly for the poor. Pakistan Microfinance Network in Islamabad has commissioned this study in order to understand and document the impact of a slowing economy and in particular, of rising inflation on microfinance clients.

This short report highlights findings based on discussions with 245 microfinance clients, both men and women, from very wide and diverse backgrounds, and with the staff of microfinance providers (such as loan or credit officers) who interact with these clients at the local, first contact, level and are far more aware about the conditions of their clients than are middle and senior management officers. It is important to state at the outset that this study is not an overview or assessment of the microfinance sector, of microfinance clients, or of microfinance institutions or providers. It has considerably limited ambitions and objectives and simply aims to understand and document the impact of inflation on microfinance clients and, to a limited extent, for microfinance practitioners.

Inflation and its ConsequencesInflation is the phenomenon where prices rise. Hence, inflation is not at all an uncommon feature of any economy. In fact, low or manageable levels of inflation — depending on the nature of the economy — are highly beneficial to suppliers and producers and act as an incentive to produce.

Inflation affects different segments of the population very differently, a fact often forgotten by most people and often exaggerated or misrepresented in the media. In general, inflation affects the rich far less than the poor, where the rich hold greater assets and have higher incomes which let them adjust to rising prices. Salaried individuals tend to be affected a great deal by inflation as their salaries tend to be ‘sticky’ and often do not rise in proportion to inflation or at the same speed. In contrast to salaried individuals, inflation affects many categories of producers in a neutral manner or can benefit them. For example, to maintain their profit margins, many producers pass on all price increases as they take place. Based on the elasticity of demand for their product or service this may result in higher or lower profits, or no change. Inflation, in ‘traditional’ or agricultural societies, is considered to be an urban phenomenon far more than it is a rural one based on assumptions such as rural populations produce a great deal of what they consume, and that they have less access to ‘modern’ facilities, commodities and goods (such as consumer items and utilities), the price for which often rise fastest. Similarly, there is also a marked difference on savers and borrowers, which has implications for this study and on microfinance clients more generally. Savers suffer as the purchasing power of their monetary assets dwindle in value, whereas those who have borrowed benefit as inflation rises, since the real value of their debt is reduced.

Just as we assume that many citizens will suffer the consequences of inflation, we should also be open to the possibility that some sections of the population will benefit from rising prices. This study tries to highlight where and how both trends persist amongst microfinance clients.

2

MICROBANKING BULLETIN, IssUE 18, sRING 2009FEATURE ARTICLEs

Microfinance Information Exchange, Inc

The Pakistan Context: Inflation, the Economy and Microfinance

Before we turn to describe how this study was conducted, it is important to highlight some of the issues which relate to Pakistan’s inflation rate, its economy, and the microfinance sector.

Like much of South Asia, inflation has seldom been a serious problem in Pakistan, and the inflation rate has been, for the most part, in single digits. However, for about a year, but perhaps more markedly since early 2008, the inflation rate in Pakistan has become the highest in over three decades, and has shot up dramatically from the annual 9 percent in fiscal year 2007 – 2008, to between 23 – 28 percent on an annualised basis today, with food and fuel prices driving the price spiral.

While inflation has been perhaps the most visible of Pakistan’s economic problems in the last few months, economic slowdown, as illustrated by falling levels of investment and slowing economic growth, have been equally troubling. The high growth period of 2002 – 2007, in which growth averaged over 6 percent of GDP per annum, has been replaced with a forecast for financial year 2008 – 2009, which could be nearer 4 percent of GDP growth. Similarly, there are predictions that a slowing economy and high inflation may raise the unemployment level in Pakistan. Most economists agree that economic activity, at least for the next year or so, will be well below the level of the last five years, affecting profitability, investment, employment and the poverty level. There are concerns that the dual problem of rising inflation and a slowing economy will push more people below the poverty line.

There are reported to be 1.8 million microfinance clients in Pakistan, which represent different arrangements of loans — group, individual, etc. Of these, a great majority are rural clients, which has important implications for how inflation has an impact on them. Almost half of microfinance clients are women. Often, the average profile of a microfinance client in Pakistan is that she is either a rural entrepreneur, involved in livestock development or passes on her loan to a male member of her family. Also, importantly, it seems that a very large majority of microfinance clients are repeat clients and once they begin to use microfinance services, the majority of clients stay loyal to the microfinance provider. These characteristics of microfinance clients will help determine how inflation affects them.

Methodology

This study to assess and observe — but not to measure — the impact of inflation on microfinance clients, is built around the Focus Group Discussion (FGD) approach. Despite its many limitations, this approach allows us to draw broad conclusions about the impact of inflation on microfinance clients.

A selection was made of different sorts of microfinance providers. In all, nine institutions were selected in three provinces and 12 FGDs were held. In total, 245 clients were present at the FGD of which 189 (77 percent) were women.

The FGDs were used to understand how inflation had an impact on borrowers and how they were coping under inflationary pressures. Questions were asked to find out if clients were having problems repaying their monthly instalments, whether their economic activity had fallen, and how this affected their household consumption. Information was acquired to see if household consumption patterns had changed in the last year or so as prices had risen. There was also discussion on how clients were prioritizing loan instalments in relation to other household expenses in this inflationary environment compared to the past. The issue of inflation was not initiated as it was thought it would be better for clients to volunteer information and opinions about their concerns themselves and to prioritise their own issues, of which inflation ought to have been one. If it was not raised by the discussion participants, specific questions on inflation were put to them.

Discussions were held with loan officers and MFP management to assess whether they saw any changes in borrowers’ behaviour and their demand for loans and repayments.

Findings from Focus Group DiscussionsThe results from the discussion with microfinance clients regarding the impact of inflation on their incomes, assets and repayment capabilities, come as a complete surprise. Our assumption was, as it is of most people, that the high inflation rate in Pakistan has been a disaster for most Pakistanis. However, a predominant majority of clients who spoke, irrespective of gender, location, type of activity, amount and purpose of loan, or by any other criteria, was that inflation was ‘not a problem’. While almost every single participant in the 12 FGDs felt that the loans were in general

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

3Microfinance Information Exchange, Inc

highly beneficial to them and to their economic activities, except for a very small minority, most felt that inflation was not resulting in them having a significantly negative impact on their businesses or lives. In fact, there were a large number of clients who felt that inflation was a positive aspect and that they were capturing higher profits on account of the price rises. Overall, one can safely conclude that on the basis of the FGDs, it was clear that a huge majority felt that inflation had a neutral influence on them, while a substantial proportion of the clients felt that inflation was substantially beneficial.

The explanations of these unexpected findings were given by the clients themselves. Many felt that in their line of business, it was easy to pass-on costs which were imposed on them and were able to argue how the loan had made it easier for them to deal with inflation. Moreover, there were certain clients who confessed that they were passing-on larger amounts of the rise in their costs and were also ‘causing’ inflation. It has to be remembered, that all these clients had been given loans in the past and were now repaying the instalments. Hence, inflation for them was a relatively more recent phenomenon and took place largely after they had made use of their loan. Many urban clients, such as those who had shops or small outlets, all felt that a lump sum loan allows them to buy goods in bulk and stock-up. All those clients who had taken a loan to buy stocks in the past had done so and were now able not just to pass-on prices, but also to increase the prices of goods that were cheaper earlier.

For the most part, in urban areas, with the exception of men in Orangi (more below) most clients, such as women who ran beauty parlours in neighbourhoods or women who were in the small business of making jewellery or clothes, all claimed to pass-on at least the full impact of inflation, and hence neutralise the impact of inflation on them. On being asked if their clientele had declined or their profits denuded on account of higher prices for the goods and services they provided, most said that they had not.

There was also a general understanding about the inflation phenomenon in Pakistan by almost all clients. A repeated answer to how these clients, all across Pakistan, had become immune to inflation and neutralised its impact was that they were all using their loans for productive purposes rather than for consumption needs, and hence would be able to recoup their investment. Most clients even realised that the instalments they were paying back every month were declining in real value due to inflation.

Not a single client complained that they were unable to repay their instalments.

Moreover, two further explanations were given as to how in times of high inflation — and every single client was cognisant of the fact that these were such times — managed to make profits, were as follows. Firstly, clients stated repeatedly that they were working much harder than they had in the past. The second explanation of how they were dealing with inflation was that they would include more members from their household in their economic activity if they could. In general, many clients said that there were also more earners in their family and this was helping them through these times. Additionally, most clients stated that they were no longer able to maintain any savings.

Without doubt, the greatest beneficiaries of inflation were agricultural producers and rural dwellers, the latter representing the majority of clients in the microfinance sector in Pakistan. Those who grew some agricultural crop were benefiting from the higher crop prices and said that they had made many times the income they anticipated. As microfinance clients they stated that the lump sum loan amount had allowed them to purchase inputs for their land in bulk some months ago, and hence cheaply, and now they were enjoying the double benefits of higher support prices for key food crops and for cotton. It seems that many farmers would have benefited from the higher output prices of agricultural products, but the advantage of microfinance clients would be that they could use the loan to purchase inputs in bulk and more cheaply. While many farmers borrowed from numerous sources, it seems that those who borrowed from non-traditional, formal systems claimed that they were better off.

Another category in the rural and peri-urban sectors who said that they benefited markedly by the price rise were those who had taken loans for livestock, and particularly for buffaloes and milk production. At every FGD, clients claimed that the increase in the purchase price of raw milk had caused their incomes to grow very substantially. Similarly, flower producers in Pattoki also stated that while their input prices had risen slightly, the price they received for flowers in large urban centres like Islamabad and Lahore was considerably higher.

There were a very small minority who stated that inflation had made them worse off. Of these individuals, perhaps three or four had mentioned that they may have had to sell a household asset — like a mobile phone — because they could not afford it and

4

MICROBANKING BULLETIN, IssUE 18, sRING 2009FEATURE ARTICLEs

Microfinance Information Exchange, Inc

because they needed the money. There was just one single case of a woman who had said that she had to switch her child from a private school to a public school. But these examples were almost non-existent. However, all the seven clients of the Orangi Charitable Trust in Karachi stated that they were having great difficulty coping with repayments, not so much due to inflation, but because of economic slowdown. These clients were all involved in the loom/textile sector, a sector which has suffered a great deal in recent years, and it was clear that they were struggling. For the most part, inflation, per se, was not seen as the main culprit.

Discussions with loan and credit officers about whether it had become particularly difficult for clients to make the instalment repayments, suggested that there had been some change, but not a great deal. In the case of Karachi, it was clear that loan officers for the Orangi Charitable Trust had to make extra visits and accommodate clients. Officers in other microfinance institutions did not state that the default rate had risen and few stated that they had significant problems.

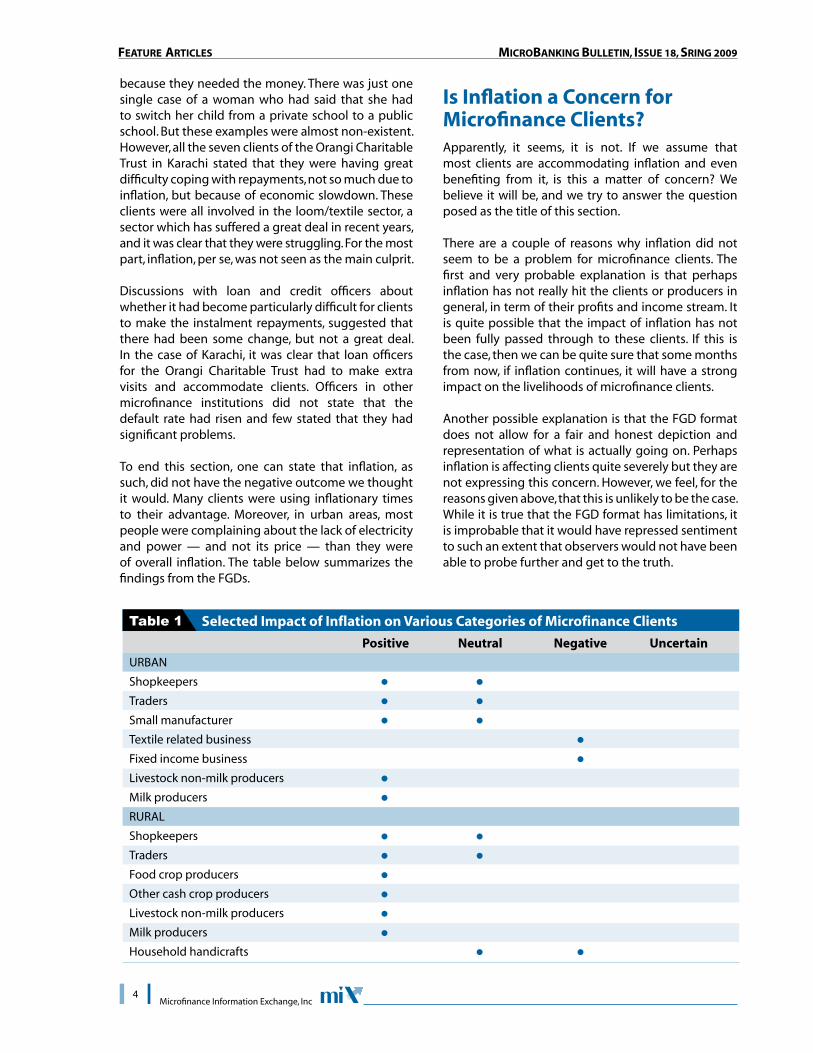

To end this section, one can state that inflation, as such, did not have the negative outcome we thought it would. Many clients were using inflationary times to their advantage. Moreover, in urban areas, most people were complaining about the lack of electricity and power — and not its price — than they were of overall inflation. The table below summarizes the findings from the FGDs.

Is Inflation a Concern for Microfinance Clients?Apparently, it seems, it is not. If we assume that most clients are accommodating inflation and even benefiting from it, is this a matter of concern? We believe it will be, and we try to answer the question posed as the title of this section.

There are a couple of reasons why inflation did not seem to be a problem for microfinance clients. The first and very probable explanation is that perhaps inflation has not really hit the clients or producers in general, in term of their profits and income stream. It is quite possible that the impact of inflation has not been fully passed through to these clients. If this is the case, then we can be quite sure that some months from now, if inflation continues, it will have a strong impact on the livelihoods of microfinance clients.

Another possible explanation is that the FGD format does not allow for a fair and honest depiction and representation of what is actually going on. Perhaps inflation is affecting clients quite severely but they are not expressing this concern. However, we feel, for the reasons given above, that this is unlikely to be the case. While it is true that the FGD format has limitations, it is improbable that it would have repressed sentiment to such an extent that observers would not have been able to probe further and get to the truth.

Table 1Positive Neutral Negative Uncertain

Selected Impact of Inflation on Various Categories of Microfinance Clients

URBAN

Shopkeepers

Traders

Small manufacturer

Textile related business

Fixed income business

Livestock non-milk producers

Milk producers

RURAL

Shopkeepers

Traders

Food crop producers

Other cash crop producers

Livestock non-milk producers

Milk producers

Household handicrafts

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

5Microfinance Information Exchange, Inc

What also emerged from the FGD was that most clients, realising that we are living in inflationary times, felt that the loan amounts made available were insignificant and were interested in inflation-indexed loans. However, many did also state that the instalment amounts should not be raised too significantly as this would make repayments difficult. For microfinance providers/institutions rather than clients, the concerns that will emerge in the future relate to delinquency, delayed payments and default. At the moment, it does not seem like these issues are threatening the functioning of institutions, but it is possible that they might put a strain on the profitability of some institutions. Also, it is very clear that if inflation stays at 20 – 25 percent, most microfinance providers will have to raise their credit levels to match the real value of the loans. Whether microfinance providers can do that will depend on their overall financial strength, access to funds and ability to respond innovatively.

ConclusionsIf inflation has not had a damaging effect on microfinance clients in the first nine months of 2008 when inflation has touched 25 percent, as a very high majority of clients claim, it is very likely that it will have an effect some months from now if inflation continues to persist. However, if as expected, inflation begins to

fall and becomes more manageable, it seems that the concern for the impact of high inflation will no longer exist and that we will return to the situation of a few years ago. This short, illustrative study suggests that most clients have been able to deal with inflation and many, particularly those producing food crops and agricultural commodities, have actually profited a great deal from it. These conclusions come as a surprise, for conventional wisdom would have suggested that all citizens suffer the impact of inflation.

What emerges from this survey also, is the clear fact that loans have helped clients, largely because they have been able to buy cheap, or in bulk, and have been able to sell at the increased market price. Clearly, those who have access to credit are at an advantage compared to those who do not have access to credit at cheap rates. This has been the general principle of microfinance and it seems to have particular significance in the times of high inflation.

If inflation rates persist, some rethinking on the behalf of microfinance providers may be necessary. They might have to raise their credit ceilings keeping in mind the real value of the loan, and may be required to increase the loan instalment process by some months to ease the likely pressure on clients.

6Microfinance Information Exchange, Inc

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

FEATURE ARTICLEs

Elevated Food Prices — Impact on Microfinance Clients

By Zaved Ahmed and Camilla Nestor, Grameen Foundation

MICROBANKING BULLETIN, IssUE 18, sPRING 2009

Approximately 1 billion people — or nearly one-sixth of the world’s population — subsist on less than USD 1 per day. Of this population,

162 million survive on less than USD 0.50 per day. According to the International Food Policy Research Institute, increasing food prices have the greatest effect on poor and food-insecure populations, who spend between 70 and 85 percent of their household income on food. This issue is especially acute for the poorest people within developing countries — the very clients that many microfinance institutions (MFIs) serve. This article will provide a general overview of the evolving global situation surrounding inflation linked to increasing food commodity prices and its impact on microfinance institutions supported by Grameen Foundation and their clients.

During mid–2008, rising food prices, particularly for staples like rice, soybeans and wheat, raised significant concern in the microfinance community given the disproportionate impact of such high prices on microfinance clientele and the potential effects on the clients’ long-term health and food security, as well as on the MFIs. While global attention has largely turned away from this issue to focus on the global financial meltdown, the reality is that food prices in developing countries remain elevated — in many cases above international market prices — and continue to negatively impact microfinance clients.

Although global food prices have come down from the mid – 2008 highs, data from the United Nations Food and Agriculture Organization (FAO) indicate that this has not trickled down to the retail level. For example, the price of rice — the principal source of food for much of the developing world — remains significantly higher in most developing countries than it was in December 2006. To demonstrate this, Grameen Foundation looked at retail prices of rice in 10 countries during the period 2007 to 2008. In our calculations, we took quarterly data listed on the FAO website and indexed it against Q1 2007 prices. Table 1 highlights this.

Even as the price of rice fell from the mid–2008 highs, on average, the price of rice in these countries increased 50 percent between late 2006 and 2008. This has forced families who previously spent up to 85 percent of their income on food to either eat less or consider ways to increase their income. Conversely, some microfinance clients are fortunate enough that family members are paid in food grains. Anup Kumar Singh, Managing Director of Sonata in India observed the role the informal ‘barter system’ has played to balance the increased cost of food: “As wages, most of the agricultural laborers are not receiving cash, but they receive 5 kg grains…per day. During the harvesting season they try to earn as much as they can… to meet their other daily expenses. They [make] purchases against the exchange of stored grains.”

1Q 07

2Q 07

3Q 07

4Q 07

1Q 08

2Q 08

3Q 08

4Q 08

100.00

99.30

105.96

112.63

116.14

135.44

142.81

142.46

100.00

100.05

110.48

144.06

160.85

160.70

150.38

124.26

100.00

96.32

96.32

102.45

107.36

142.33

137.42

126.99

100.00

100.00

110.25

112.70

153.69

148.77

N/A

N/A

100.00

100.00

100.00

113.33

120.00

133.33

146.67

146.67

100.00

100.78

101.71

120.34

123.38

143.65

148.64

156.04

100.00

122.36

122.36

130.80

174.26

200.00

200.00

199.83

100.00

102.37

106.48

106.39

136.01

162.07

N/A

N/A

100.00

92.40

99.20

107.60

120.00

186.80

184.00

180.00

100.00

98.02

99.82

112.16

124.92

184.64

163.11

151.04

Bangladesh Brazil Egypt India Mozambique Pakistan Peru Philippines Senegal Vietnam

Table 1 Index of Retail Prices of Rice by Quarter

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

7Microfinance Information Exchange, Inc

There are several reasons for the disconnect between international market prices and retail prices in developing countries. As reported by the Financial Times: “Food aid officials attribute the disconnect between local and international food prices to time lags, poor harvests in developing countries and…lack of trade finance.”1 We researched the possibility that excess profiteering by wholesalers was another cause of the disconnect, but this did not bear out in the analysis.2

High food prices are likely to persist in the medium term. While forecasts in the current environment are subject to considerable uncertainty, the World Bank expects food prices will remain high in 2009 and 2010.

Table 2 shows that prices are likely to remain well above 2004 levels through 2015 for most food crops. These forecasts are broadly consistent with those of other agencies such as United States Department of Agriculture and the FAO. While world grain production is forecast to grow, increased utilization is expected to lead to a decline in stocks in the 2008/2009 crop year. The FAO predicts that total grain end stocks will reach a 25 – year low by the end of crop year 2008/2009.

Impact on Microfinance BorrowersChange in food consumption: During GF’s conversations with MFIs, they raised serious concerns about the quantity of food consumed by their borrowers. The increased costs of essentials are forcing them to eat less. Dr. Aris Alip, Managing Director of CARD in the Philippines brought this out: “The immediate impact on our clients was on food security. I heard stories of mothers cutting down on consumption of meat (from once a week to once

a month) or for worse-off clients, cooking rice into porridge so a kilo of rice would suffice for a day for a family of six.”

In the short-run, such frugal practices by microfinance clients may not have a significant impact, but if continued on a prolonged basis, can lead to permanent health damage to them and their families.

Depletion of savings with MFIs: In some of the countries where MFIs are allowed to accept savings, MFIs have started reporting a decrease in the voluntary savings rate. It is still too early to determine if this is a general trend or is restricted to specific regions or countries. However, some MFIs have noticed that mature clients are withdrawing their savings to finance their working capital needs, instead of taking a new loan. This has been reported by MFIs in Philippines and in Nigeria.

For MFIs that offer savings, this trend has naturally impacted savings as a funding source for the MFI. It has also reduced the cushion that clients might have to weather continued price increases.

Loan Funds Diverted for Consumption: In extreme cases, clients may be diverting loan funds to buy essentials to survive. MFIs have to maintain close contact with clients to identify those who are hit the hardest by inflationary pressures and take specific measures to align loan purpose with usage.

Higher Incidence of school Drop-outs: Some GF partner MFIs reported that their borrowers have stopped sending their children to school so that children can support the family’s income generating activities. This may have severe repercussions on borrowers’ struggle to break free from the cycle of

Table 22007 2008 2009 2010 2015

Index of Projected Real Food Crop Prices (2004 = 100)

Maize 139 175 165 155 148

Wheat 154 215 191 166 140

Rice 130 243 208 183 160

Soybeans 119 156 147 139 115

Soybean Oil 136 187 173 160 110

Sugar 133 157 167 176 182

SOURCE: The World Bank

1 ‘Poor still hit by high food prices, says UN’ Javier Blas, Financial Times, March 19, 2008.To test this hypothesis, GF did an analysis comparing retail and wholesale prices of rice in four countries; there was not a significant differential between the retail and wholesale prices, indicating that middlemen are not at fault for driving the prices up. Lack of reliable data prevented us from testing this with a larger sample size.

2

8

MICROBANKING BULLETIN, IssUE 18, sRING 2009FEATURE ARTICLEs

Microfinance Information Exchange, Inc

poverty. In Pakistan, one MFI informally reported that the drop-out level of clients’ children has almost doubled during this period.

Impact on Loan sizes: The impact on loan sizes is not consistent. In some countries, microfinance borrowers are requesting larger loans, driven in part by the increased cost of running their existing ventures. In other cases, the borrowers feel the need to establish new ventures to make ends meet, creating additional funding pressure for MFIs. For example, the average loan size for the three MFIs GF works with in Nigeria has increased by 45 percent during the last 12 months.

On the other hand, some MFIs are reporting decreased demand and in turn, decreasing average loan sizes. For example, in the Philippines, Dr. Alip of CARD said: ”What is striking is that our clients are themselves reducing their borrowing (eligible for Peso 5,000 but they will now borrow Peso 3,000) since they say that business is not good.” It seems that basic business practice of frugality during tough times may be lost on certain Wall Street executives, but not on poor borrowers in the Philippines.

Impact on the MFIThe impacts noted below are driven in part by inflation (fueled by food price increases) but are also attributable to the global financial meltdown. Given the interconnected nature of global financial and economic trends, it is not possible to cleanly separate the impact of one particular driver from the others; as such, GF has noted the general trends it is seeing among the MFIs it supports below.

Portfolio Quality: Although it was expected that rising food prices would impact clients’ ability to repay, based on the 4Q 2008 data, there is no rise yet in delinquencies among GF’s partners. Nevertheless, several MFI leaders have noted that they expect to

see an uptick in portfolio at risk (PAR) if food prices remain elevated.

Refinancing Risk: As has been reported elsewhere, refinancing risk is a major issue facing MFIs due to the twin pressures of contracting liquidity in local bank markets and among some of the microfinance investment vehicles, coupled with a reduction in risk appetite by lenders. The inability to refinance on attractive terms, or in some cases at all, will likely slow MFI growth significantly in 2009. Among the 20 MFIs in GF’s Growth Guarantees portfolio, average quarterly growth slowed to 11.2 percent in Q4 2008 from 25.0 percent in Q4 2007.

Increased Operating Expenses: The nature of the microfinance industry is such that wages and salaries are the single largest expense component for most MFIs. Inflation will naturally drive wages and salaries up. Hence, MFIs will either have to find a way to absorb most of this increase or face the unattractive option of raising interest rates to end borrowers.

The world in general has moved on from the food price issue and is focusing all of its resources on combating the financial sector meltdown. That coupled with the drop in international food prices from mid-2008 highs has led to a situation where the food price issue hardly registers on the radar screen now. As we have shown, however, local food prices are not tracking international prices, and it is clear that a prolonged period of continued elevated food prices will have a significant impact on microfinance clientele.

To date, clients have shown an amazing degree of resiliency and innovation in absorbing the increase in food prices. However, these clients’ coping remedies may have significant long term consequences on their families’ well being — the impact of which is still too early to measure.

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

9Microfinance Information Exchange, Inc

FEATURE ARTICLEs

Microfinance: Where do we stand Today?

By Ajit Jain and Caroline Norton, Deutsche Bank MICROBANKING BULLETIN, IssUE 18, sPRING 2009

Microfinance — Does Everything Correlate in Bad Times?

In the last ten years, conventional wisdom has held that microfinance as an asset class enjoys a striking lack of correlation with trends in the global

economy. The informality of most of the micro-businesses feeding into the microfinance industry was supposed to shield it to a certain degree from macroeconomic booms and busts. Challenging this assertion, however, is another tenet that emerged from the decade of Long Term Capital Management, which holds that in bad times, everything correlates. With waves of the international financial crisis rippling through the global economy, the current situation provides an opportune testing ground to determine which of these seemingly opposed conventional wisdoms holds water. While microfinance has certainly not proved to be immune from the travails of the traditional banking sector, it has not come close to suffering the same damage, suggesting that opportunities still exist in the microfinance sector for MFIs and for investors. Indeed, MFIs have shown remarkable resiliency and foresight as they respond

to the crisis by shoring up their core operations and returning with new purpose to their social missions.

The last decade has witnessed a remarkable rise for microfinance. International investors discovered the potential of microfinance in zeal in the second half of the 2000s, as structured products permitted microfinance investment vehicles (MIVs) to market funds to a wide range of investors, from the socially-oriented development agencies to pension funds with fiduciary roles. The first microfinance CDO was closed in 2004, and it was followed shortly afterward by a string of other structured funds, which offered private and institutional investors a new opportunity to acquire notes collateralized by loans to MFIs. These products allowed MFIs to access large new pools of funding to fuel remarkable expansion. The models of structured credit products in microfinance have stayed conservative, after an initial spurt in innovative risk distribution mechanisms. The first microfinance CDO was structured by Blue Orchard and had been offered with a 100 percent guarantee to the Senior note holders. This structure soon gave way to a partial guarantee structure with 40 percent subordination to the Senior note holders. The Global Commercial

Asset Growth Savings Growth Growth in External Credit

Growth in Total Capital Borrower Base Growth

150%

120%

90%

60%

30%

0%

Graph 1 Growth Patterns in Microfinance

Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

The microfinance industry witnessed rapid growth over the last few years and in the recent past, much of this growth was funded through savings deposits and increasinginterest of the mainstream finance industry in microfinance balance sheet components. This was complemented by the increasing appetite of MFIs for a more leveredcapital structure. However, the impact of macroeconomic crisis can be clearly seen in the lowered growth rates over 2008 - 2009.

10

MICROBANKING BULLETIN, IssUE 18, sRING 2009FEATURE ARTICLEs

Microfinance Information Exchange, Inc

Microfinance Consortium transaction structured by Deutsche Bank was one of the first of such kind. Most of the structures marketed since have been modeled with very similar risk classification mechanisms.

Risk of Mission DriftBooming local economies spurred the growth of savings deposits (among MFIs whose legal structures permitted savings mobilization), as more clients were able to afford to stash away some of their earnings for a rainy day. These two pools of funding continued to deepen up until 2008, providing the means for MFIs to grow their portfolios and client bases at a staggering pace, some by 50 to 100 percent year on year.

Although such growth meant that more poor clients were able to access financial services, not all side effects of the MFIs’ rapid growth were so positive. As the sector has embraced commercialization, some MFIs seeking to take advantage of the commercial funds that were suddenly so readily available moved away from their traditional areas of strength, such as micro group lending, into less familiar products such as SME lending, in an effort to attract more clients and cover rising financial costs and operational costs associated with expansion. With this move into new businesses came an element of mission drift for some institutions.

A recent Women’s World Banking study discovered that as MFIs transformed from NGOs into commercial entities, their average loan sizes began to grow, and the number of women served began to decline, despite the missions of many MFIs in the sample to serve the poor and in particular, women. Even more disturbingly, in some markets, as MFIs have grown, they have encroached upon their peers’ areas of operation, generating fierce competition and leading to over-indebtedness of the very borrowers that the institutions originally sought to aid.

Investor AppetiteWhen the financial crisis struck in its full strength in 2008, blowing out credit default spreads to levels not seen in decades, it hit the microfinance investment industry along with the traditional banking sector. Liquidity dried up almost overnight, with planned microfinance funds being pulled late in the marketing process. Deutsche Bank had been in the process of structuring a USD 350 million global microfinance fund during Q3-2008 and was forced to shelve the marketing plans following a precipitous widening of credit spreads and a near shut-down of structured credit products market.

Finding themselves with fewer funds available to put to work in alternative investments, such as microfinance, investors are now tuning in more closely to the risks involved in microfinance investments. Their questions are centering on topics such as portfolio quality, liquidity risk, open FX risk and internal controls. In addition, investors are seeking to

8%

6%

4%

2%

0%

75%

60%

45%

30%

15%

0%Q2 07 Q3 07 Q4 07 Q2 08Q1 08 Q3 08 Q4 08 Q1 09

Graph 2Concentration Risk inMicrofinance Portfolio

Top 10 Loan Concentration Single Group Exposure

Related Party Lending Ratio

% of Women Borrowers % Rural

The rapid growth of the industry also witnessed a spike in concentrated exposures to specifically profitable loan groups and the larger borrowers. This trend however has been on the decline for the last three quarters, possibly due to a conservative approach taken by most MFIs as a response to the global macroeconomic crisis.

7%

6%

5%

4%

3%

2%

1%

0%99 00 01 02 03 0604 05 07 08 09

Graph 3 Key Rates in the G3 Countries

Fed Funds ECB refi BoJ

Various central banks across the world have acted in close coordination to bring down the overall cost of borrowing. In microfinance, the cost of borrowing has typically been significantly below commercial funding levels.

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

11Microfinance Information Exchange, Inc

be as catalytic as possible with their limited funding, carefully selecting targeted countries and MFI profiles. Commitment to a double bottom line objective has reemerged as a concern for investors, perhaps an acknowledgement of the unscrupulous lending practices in the developed world that contributed to the financial crisis.

As investors take a closer look at these elements of MFIs’ operations and finances, the picture that emerges is not as discouraging as the global economic malaise would suggest. While portfolio quality has generally deteriorated across regions, MFIs are demonstrating an ability to return to their operational strengths, even in countries that have been hit hardest by the crisis.

Responding to the Crisis: Conservative MeasuresAcross Deutsche Bank’s portfolio, in a trend mirrored by the portfolios of other microfinance fund managers, Portfolio at Risk > 30 days has risen from an excellent 1.8 percent to a less spectacular, but hardly alarming 3.8 percent. In some cases, while MFIs were growing rapidly, rising loan portfolio values and client counts masked problems in the portfolio. Now that the funding that was feeding this growth has lessened, these problems are beginning to emerge. In other cases, MFI clients are feeling the squeeze of the economic circumstances, as demand for their goods has fallen off, and they are less able to repay their loans. MFIs seem to be reacting to these problems by tightening their credit standards and by lowering the size of the loans that they offer.

These prudent measures have caused a decline in the average gross loan portfolio for the first time in many periods, as MFIs respond to falling portfolio quality and uncertain future funding by tightening lending standards, shrinking disbursed loan sizes, and holding more cash on hand. Interestingly, however, the average number of active clients has continued to grow, albeit more slowly than before, signaling that MFIs on the whole have not been dramatically wounded by the recent external shocks.

Rather, they seem to be returning to the basics of microfinance: small loan sizes for short terms provided in the form of standard products.

Profitability has been leaner since the crisis struck, though on average it is still positive. As the US dollar has recently appreciated versus many world currencies, MFIs that borrowed heavily in hard currency in the last few years without hedging that exposure are experiencing losses related to foreign currency mismatches. In response, MFIs are demanding more loans in local currency and are working to eliminate these mismatches by all means at their disposal. In addition, MFIs are allocating more expenses toward provisioning to ensure that they have adequately reserved for delinquencies.

4%

3%

2%

1%

0%

1500%

1200%

900%

600%

300%

0%Q2 07 Q3 07 Q4 07 Q2 08Q1 08 Q3 08 Q4 08 Q1 09

Graph 4 Asset Quality

PAR > 30 LLR Coverage PAR > 30

PAR > 90 LLR Coverage PAR > 90

PAR 1 - 30 Net Charge-offs/Loan Loss Exp

The portfolio delinquencies, as measured by PAR > 30 days and PAR > 90 days have been on the rise over the last two years.

Key PerformanceImpacting TrendsGraph 5

12%

11%

10%

9%

8%

7%

6%

5%

4%

3%

2%1 8765432

Financial Costs Provision Exp/Ave. GLP ROA

Rising Financial costs and loan loss provision expenses have impacted the overall profitability of microfinance institutions.

12

MICROBANKING BULLETIN, IssUE 18, sRING 2009FEATURE ARTICLEs

Microfinance Information Exchange, Inc

ConclusionCertainly MFIs face challenges as slowing growth and funding opportunities force them to refine their risk management systems, to tackle rising delinquencies, and to actively manage their liquidity, for the first time for many MFIs. However, we prefer to view the current situation in the microfinance market as an opportunity for the best run MFIs to distinguish themselves, for social investors to prove their commitment to the field, and for the industry to return to its original social mission, with renewed attention to initiatives such as the Client Protection Principles.

To look back to the two original conventional wisdoms that we began with, perhaps instead of debunking one or both, we could add a truism of our own: microfinance may not have completely decoupled from the global economy, but its resilience in challenging times should be the envy of banks across Wall Street.

Note: All charts in this document have been drawn based on data from the portfolios managed by the Global Social Investments Group at Deutsche Bank.

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

13Microfinance Information Exchange, Inc

FEATURE ARTICLEs

The Impact of the Financial Crisis on Microfinance Institutions

Results from CGAP’s March 2009 Opinion survey

Xavier Reille and Christoph Kneiding1, CGAPMICROBANKING BULLETIN, IssUE 18, sPRING 2009

Introduction

The global crisis is spreading quickly in emerging markets but little is known about its impact on the microfinance sector: Which regions are most

affected and why? Are microfinance institutions (MFIs) resilient to this unprecedented economic downturn? What is the effect of the crisis on MFI business models? And how do MFIs foresee their liquidity situation in the near future?

CGAP conducted an online survey with MFIs in March 2009 to answer some of these questions and to monitor the impact of the crisis. The survey was widely disseminated to MFIs with support from MIX and the Microcredit Summit Campaign, as well as from several large MFI networks2. Over 400 completed responses3 were sent back from MFI managers, which reflected a good distribution among regions4 and institutional sizes.5

ECA: 44

EAP: 26SA: 59

MENA: 29

SSA: 115

LAC: 114

1 With research assistance from Meritxell Martinez, CGAP.ACCION, Grameen, FINCA, Freedom from Hunger, MFN, Opportunity, Women’s World Banking, and Sanabel. Respondents were asked to indicate the asset size of their institutions, for which the following brackets were provided: Tier 1 (assets above $50m), Tier 2 (assets between $3 – 50m), and Tier 3 (assets below $3m). Around 76 percent of MFIs in our sample are in Tier 2 or 3 and 24% tier one. Credit unions and cooperatives represent only 14.5% of the sample. EAP East Asia and Pacific, ECA Europe and Central Asia, LAC Latin America and Caribbean, MENA Middle East and North Africa, SA South Asia and SSA sub-Saharan Africa. This article presents the high level findings of the survey with a focus on MFI impact. CGAP will produce another report to be posted on www.cgap.org with the full results.

2

3

4

5

14

MICROBANKING BULLETIN, IssUE 18, sRING 2009FEATURE ARTICLEs

Microfinance Information Exchange, Inc

Dramatic slowdown in Portfolio Growth

Microfinance has enjoyed a decade of exceptional growth. In 2007 alone the overall loan portfolio of MFIs reporting to MIX Market increased by 47 percent. However, the survey results show that this period of rapid growth has ended. Sixty-five percent of MFI respondents reported that their gross loan portfolios remained stable or decreased over the last six months. This trend was consistent across all regions, but not across institutional types: MFIs that mobilize savings (banks and credit unions) experienced significantly less reductions in their portfolio than those that depend solely on credit as a source of funding. This underlines the importance of alternative funding sources in an economic situation like this. Overall, the credit crunch and the economic recession are clearly forcing most MFIs to slow down the growth of their microcredit portfolios.

Portfolio Quality Down GloballyThe lending business contraction is occurring alongside a deterioration in the quality of MFIs’ loan portfolios, a trend that according to MIX numbers had already started in 2007. Sixty-nine percent of MFI respondents reported an increase in Portfolio at Risk (PAR). Non-performing loans increased for all sizes of MFIs with no significant variations among MFI tiers. The broad increase in non-performing loans as a percentage of gross loan portfolio reflects clients’ economic hardship. The indicator is also pushed upwards due to decreasing loan portfolios. The region hit hardest by this decrease in portfolio quality is ECA, where 97 percent of institutions report a stagnating or increasing PAR. Of all regions, EAP and MENA have been most resilient so far, but even there the majority of MFIs report deteriorations in their PAR.

In search of LiquidityThe liquidity constraints highlighted during CGAP’s virtual conference in December 2008 are still present, but less dramatic than the drop in portfolio growth and the broad increase in non-performing loans. Overall, 52 percent of the MFI respondents reported liquidity constraints over the past six months. As could be expected given their asset size, smaller MFIs are more affected, with 64 percent of small (tier 3) MFIs reporting funding problems versus only 35 percent for large (tier 1) MFIs. Small and medium MFIs appear to be struggling more with liquidity issues: 74 percent of small (tier 3) MFI managers expect their liquidity situation to worsen in the next 6 months. Regionally, the most pressing needs for capital are in sub-Saharan Africa and in South Asia (with 68 percent and 57 percent respondents reporting liquidity problems, respectively).

A majority of savings-based MFIs (56 percent) does not face liquidity constraints. However, these institutions are far from being immune to the effects of the crisis and reported higher levels of PAR increases versus non-deposit based MFIs (76 percent of the savings-based MFIs had an increase in PAR versus 66 percent for non-deposit based MFIs).

No significant Business Adjustments YetWhat has been the MFIs’ response to the crisis so far? One could assume that increasing costs of funds (in most markets estimated around 200 to 400 basis points) could force MFIs to raise their interest rates.

% o

f res

po

nd

ents

80

60

40

20

0

Tier 1 Tier 2 Tier 3

Portfolio Same or Down Last 6 Months, by Size of MFI.Figure 1

mean of liquidity now mean of liquidity later

% o

f res

po

nd

ents

80

60

40

20

0

Tier 1 Tier 2 Tier 3

Figure 2Liquidity Constraints Now andin the Next 6 - 12 Months, bySize of MFI.

MICROBANKING BULLETIN, IssUE 18, sPRING 2009 FEATURE ARTICLEs

15Microfinance Information Exchange, Inc

But most MFIs (61 percent) reported no changes in their lending rates to clients. Such measures would indeed be difficult to implement and very unpopular in times of crisis. The survey also found that 23 percent of respondent MFIs have been downsizing their staff to trim costs. This marks a clear reversal of the expansionary trend in staff levels over the past years.

Conclusion and Outlook Although opinion surveys are limited in their explanatory power and potentially biased, the CGAP study provides an insightful picture of MFI managerial views on the impact of the global crisis on microfinance as of March 2009. While in 2008, CGAP’s

“Banana Skins” survey among MFI managers ranked a lack of funding sources last in terms of potential risks for the industry, this perception has radically changed over the past months. Liquidity issues and credit risk are clearly the biggest managerial concerns, and one can expect the situation to worsen as the full effects of the crisis unfold in emerging markets in the coming months. Amid the gloom, MFI managers appear surprisingly optimistic: three-quarters of respondents believe that their performance will remain stable or improve over the next six months. While this may be wishful thinking for some MFIs, it could also indicate that MFI managers are undertaking measures to confront the crisis and prevent further deterioration.

16

MICROBANKING BULLETIN, IssUE 18, spRING 2009BREAKING IT DOWN

Microfinance Information Exchange, Inc

BREAKING IT DOWN...sDI vs. Fss

Scott Gaul, Product Development Manager, MIX

MICROBANKING BULLETIN, IssUE 18, spRING 2009

IntroductionMicrofinance practitioners have often sought a single, easy-to-understand indicator for evaluating the performance of microfinance institutions (MFIs). To date, the most commonly used indicator has been financial self-sufficiency (FSS). However, FSS is an incomplete model of an institution’s performance, as is any single number. The subsidy-dependence index (SDI) has been suggested as an alternative measure that more accurately reflects an MFI’s reliance on subsidies relative to its peers. In this article, we investigate some of the similarities and differences between FSS and SDI and compare both indicators on MBB data from 2003 – 2007.

What is sDI?The SDI model has been proposed and fleshed out by Yaron and others in a series of papers.1 The SDI is ‘designed to measure the self-sustainability level of the MFI with a single number.’ To measure this, SDI enumerates a range of subsidies potentially received by an MFI (on an annual basis) and compares the total subsidy to the income received by the MFI on its loan portfolio. The comparison of total subsidy and income from loans (in the form of the SDI) yields two results:

[A]n indication of the percentage by which the average yield obtained on the MFI’s LP [loan portfolio] would have to increase in order to make it subsidy independent. It also indicates the cost to society of subsidizing the MFI, relative to the interest plus fees paid by the target clientele to the MFI.2

We will cover the formulas for SDI and FSS in more detail below.

Models vs. parametersBefore stepping into a comparison of FSS and SDI, it is important to keep in mind the distinction between model and parameters. FSS and SDI both incorporate parameters or external factors — such as the inflation rate — to adjust MFI performance numbers for context. If we were to calculate SDI and FSS using different rates for adjustments, it would not be a reasonable comparison since we would simultaneously have to account for differences in the models and in the rates chosen. Consequently, we will first look at the models, assuming they have the same parameters. Then, we can look at the impact of different parameters on both models.

Comparing DefinitionsIn this section, we break down the formulas for FSS and SDI to try to understand each model in terms of the other.3 The formula for FSS can be stated simply as:

However, MBB policy makes only small adjustments to revenue, so the adjustments primarily affect the denominator of this indicator. If we separate the adjustments from the unadjusted expenses, we have the following approximation:

A similarly schematic definition of SDI is:

FSS = (Adjusted Revenue / Adjusted Expense) (1)

1 Primary resources on SDI used for this note are the following: Schreiner, M. and Yaron, J. (2001), Development Finance Institutions. Measuring their Subsidy, Washington, DC: World Bank. Yaron, J. and R. Manos, (2007), Is the microfinance industry misleading the public regarding its subsidy dependence?, Savings and Development, 2. Yaron and Manos, 2007, 13. For a more detailed version of the following, please see forthcoming MIX paper on SDI and FSS.

2

3

FSS = Revenue/(Adjustments + Expenses) (2)

SDI = Subsidy/Loan Revenue (3)

MICROBANKING BULLETIN, IssUE 18, spRING 2009 BREAKING IT DOWN

17Microfinance Information Exchange, Inc

Where the level of subsidy is equal to:

Separating the Net Income term into its components, and dividing by loan revenue yields:

If we assume that total Revenue for an MFI is ‘close’ to Loan Revenue4, then this can be rewritten as:

And this reduces finally to:

While this approximation oversimplifies both models, it preserves the main insights. The approximation also holds up when we apply this to actual MFI data. The formula (9) from above has a 96 percent correlation with the full SDI, when we calculate both formulas on the MBB sample from 2003 – 2007.

From the breakdown of the formulas, we can already learn some things about the relationship between FSS and SDI:

. FSS and SDI are closely related — we can approximate either one well in terms of the other.

. FSS and SDI are inversely related; as FSS goes up, SDI goes down.

. SDI is centered around 0, while FSS is centered around 1 (Institutions with FSS > 1 are ‘financially self-sufficient’; institutions with SDI < 0 are ‘subsidy independent’.)

. SDI differs from FSS through the inclusion of donations inflows.

. FSS differs from SDI through the inclusion of non-loan revenues.