the mos memory market - smithsonian institution

TRANSCRIPT

OVERVIEW

Memory 1997 provides detailed coverage of the recents trends associated with DRAM, SRAM,EPROM, and flash memory IC devices. Market direction and technology inclinations for eachproduct segment are covered in separate sections. Details of the ROM and EEPROM markets arereferenced in this section.

The memory market is often looked upon to introduce new and innovative devices. Demandsfrom customers for more sophisticated and technically advanced systems necessitate that new ICproducts enter the market. When new products are introduced to the marketplace, existing ICcomponents are pushed further along the product lifecycle. Figure 1-1 provides ICE’s view ofwhere several memory ICs will be located in the 1997 product lifecycle.

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-1

1 THE MOS MEMORY MARKET

PRODUCT GROWTHINTRODUCTION MATURITY SATURATION DECLINE (OBSOLETE)

64K DRAM

RAMs HIGH SPEED CMOS/BiCMOS

SA

LE

S

32K EPROM

16K EPROMROMs

8M Flash32M Flash4M Flash 256K Flash

512K Flash

1M DRAM256K DRAM

256K SRAM 64K SRAM

16K SRAM

4K ECL SRAM

16K ECL SRAM

4M DRAM

1M SRAM

64K SRAM 16K SRAM1M SRAM

64K ECL SRAM

256K SRAM

1M ROM256K ROM

64K ROM4M ROM

64K PROM 32K PROM 16K PROM

1M EPROM 256K EPROM 64K EPROM

64K EEPROM256K EEPROM 16K EEPROM

128K PROM

128K EPROM512K EPROM

4K EEPROM32K EEPROM

16M ROM

4M EPROM

8M ROM

16M DRAM

4M SRAM

1M EEPROM

32M ROM

64M ROM

16M EPROM

4M EEPROM

64M DRAM

20175BSource: ICE, "Memory 1997"

1M Flash2M Flash

16M Flash64M Flash

Figure 1-1. Memory Product Lifecycle (1997)

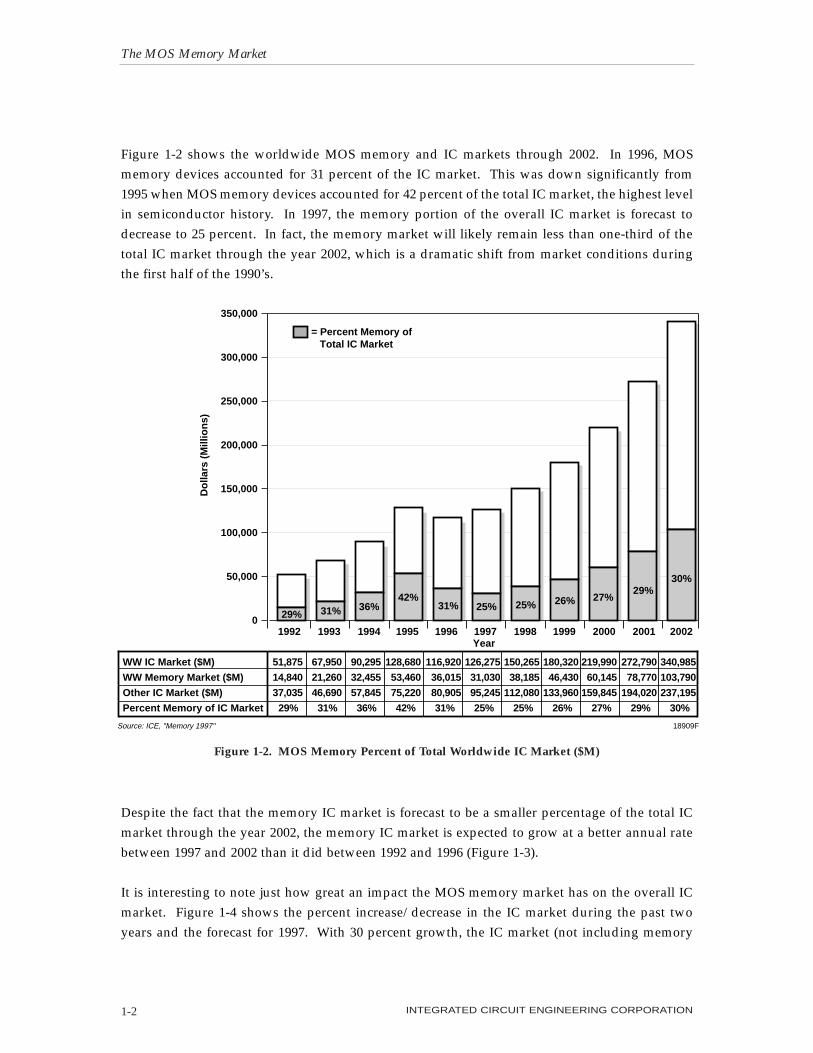

Figure 1-2 shows the worldwide MOS memory and IC markets through 2002. In 1996, MOSmemory devices accounted for 31 percent of the IC market. This was down significantly from1995 when MOS memory devices accounted for 42 percent of the total IC market, the highest levelin semiconductor history. In 1997, the memory portion of the overall IC market is forecast todecrease to 25 percent. In fact, the memory market will likely remain less than one-third of thetotal IC market through the year 2002, which is a dramatic shift from market conditions duringthe first half of the 1990’s.

Despite the fact that the memory IC market is forecast to be a smaller percentage of the total ICmarket through the year 2002, the memory IC market is expected to grow at a better annual ratebetween 1997 and 2002 than it did between 1992 and 1996 (Figure 1-3).

It is interesting to note just how great an impact the MOS memory market has on the overall ICmarket. Figure 1-4 shows the percent increase/decrease in the IC market during the past twoyears and the forecast for 1997. With 30 percent growth, the IC market (not including memory

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-2

18909F

Do

llars

(M

illio

ns)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

20022001200019991998199719961995199419931992

29% 31% 36%42%

31% 25% 25% 26% 27%29%

30%

= Percent Memory of Total IC Market

Year

Source: ICE, "Memory 1997"

WW IC Market ($M)

WW Memory Market ($M)

Other IC Market ($M)

Percent Memory of IC Market

51,875

14,840

37,035

67,950

21,260

46,690

90,295

32,455

57,845

128,680

53,460

75,220

116,920

36,015

80,905

126,275

31,030

95,245

150,265

38,185

112,080

180,320

46,430

133,960

219,990

60,145

159,845

272,790

78,770

194,020

340,985

103,790

237,195

29% 31% 36% 42% 31% 25% 25% 26% 27% 29% 30%

Figure 1-2. MOS Memory Percent of Total Worldwide IC Market ($M)

ICs) was extremely good in 1995 ($75.2 billion). However, when the MOS memory segment wasfactored in, the overall growth of the IC market increased 13 additional percentage points to 43percent, or $128.7 billion!

A similar impact was felt in 1996 when the total IC market was $116.9 billion. This represented adecrease of nine percent from the previous year. However, if the memory segment of this figureis excluded, the IC market actually witnessed eight percent growth in 1996.

Figure 1-5 provides a complete review of the MOS memory and IC markets for the years 1992-2002. Following three straight years of better than 40 percent growth (1993, 43%; 1994, 53%; 1995,65%), the 1996 MOS memory market experienced the “correction year” that was anticipated forsome time.

As will be discussed later, a great amount of new wafer fab capacity led to greatly reduced aver-age selling prices for memory products. This, in turn, led to the -33 percent reduction in the sizeof the 1996 MOS memory market. Excess wafer fab capacity is forecast to remain through 1997,which will likely keep the memory market surpressed.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-3

Do

llars

(M

illio

ns)

18903F

Year

Source: ICE, "Memory 1997"

MOS Memory Market ($M)

Percent Change

103,790

32

14,840

21

21,260

43

32,455

53

53,460

65

36,015

–33

31,030

–14

38,185

23

46,430

22

60,145

30

78,770

31

1992-1996 CAGR = 25%1997-2002 CAGR = 27%

0

20,000

40,000

60,000

80,000

100,000

120,000

20022001200019991998199719961995199419931992–40

–30

–20

–10

0

10

20

30

40

50

60

70

Per

cen

t C

han

ge

Worldwide MOS Memory Market ($M)Percent Change

Figure 1-3. 1992-2002 MOS Memory Market CAGR

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-4

–10

0

10

20

30

40

50

1996/19951997/1996

(FCST)1995/1994

Per

cen

t C

han

ge

Source: ICE, "Memory 1997" 22424

128,680

75,220

IC Market ($M)(Including Memory)

IC Market ($M)(Excluding Memory)

116,920

80,905

126,275

95,245

IC Market Growth (Including Memory)

IC Market Growth (Excluding Memory)

Year 1995 1996 1997

Figure 1-4. Effects of Memory Market on Total IC Market

WW IC Market ($M)

WW MOS Memory Market ($M)

WW Memory Percent Change

Percent Memory of Total IC

DRAM ($M)

SRAM ($M)

EPROM ($M)

Flash ($M)

ROM ($M)

EEPROM ($M)

Other Memory ($M)

Total MOS Memory ($M)

128,680

53,460

65%

42%

40,835

6,075

1,385

1,860

1,965

885

455

53,460

116,920

36,015

–33%

31%

25,130

4,745

1,105

2,610

1,340

920

165

36,015

1995 1996

126,275

31,030

–14%

25%

21,485

3,500

815

3,000

1,100

975

155

31,030

1997

51,875

14,840

21%

29%

8,525

2,890

1,250

270

1,225

480

200

14,840

67,950

21,260

43%

31%

13,140

3,295

1,350

740

1,625

700

410

21,260

1992 1993

90,295

32,455

53%

36%

23,420

3,755

1,390

865

1,890

720

415

32,455

1994

150,265

38,185

23%

25%

27,750

3,955

695

3,585

970

1,090

140

38,185

180,320

46,430

22%

26%

34,605

4,510

580

4,530

870

1,210

125

46,430

272,790

78,770

31%

29%

61,890

6,015

420

8,175

680

1,490

100

78,770

1998 1999 2000

219,990

60,145

30%

27%

46,080

5,275

500

6,050

775

1,355

110

60,145

2001

340,985

103,790

32%

30%

82,870

6,915

375

11,280

610

1,650

90

103,790

2002

18914HSource: ICE, "Memory 1997"

Figure 1-5. MOS Memory Market Forecast

Despite a one or two-year period of“slower” market growth, ICE showsin Figure 1-6 that the 10-year aver-age annual growth rate of the MOSmemory market looks bright. OnlyROMs, EPROMs, and the “othermemory” (i.e., FIFOs, etc.) cate-gories are shown experiencingdeclining markets through the year2002.

In terms of dollar volume, DRAMsmake up the majority of MOSmemory sales and are forecast to bethe dominant memory product through the year 2002 (Figure 1-7). In fact, ICE forecasts that inthe year 2002, 80 percent of the MOS memory market will be attributed to DRAM sales as shownin Figure 1-8.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-5

DRAM

SRAM

EPROM

FLASH

ROM

EEPROM

Other Memory

Total Memory

26%

9%

–11%

45%

–7%

13%

–8%

21%

22425Source: ICE, "Memory 1997"

Figure 1-6. Ten Year Average Annual Growth Rates (1992-2002)

0

20,000

40,000

60,000

80,000

100,000

120,000

20022001200019991998199719961995199419931992Year

Do

llars

(M

illio

ns)

18902ESource: ICE, "Memory 1997"

DRAM ($M)

SRAM ($M)

EPROM ($M)

Flash ($M)

8,525

2,890

1,250

270

13,140

3,295

1,350

740

23,420

3,755

1,390

865

40,835

6,075

1,385

1,860

25,130

4,745

1,105

2,610

21,485

3,500

815

3,000

27,750

3,955

695

3,585

34,605

4,510

580

4,530

46,080

5,275

500

6,050

61,890

6,015

420

8,175

82,870

6,915

375

11,280

Figure 1-7. Dollar Volume of MOS Memory Product Segments

Flash memory sales accounted for three percent of the MOS memory market in 1995 and sevenpercent in 1996. Beginning in 1997 and lasting through at least the year 2002, the flash memorymarket is forecast to represent a double-digit percentage of the total MOS memory market.Meanwhile, as a percent of the total memory market, the SRAM, ROM, EPROM, and EEPROMmarkets will remain flat or decline over the next five years.

MOS memory unit shipments are also dominated by DRAMs as displayed in Figure 1-9. Notehow DRAM unit shipments continued upward even though this particular market tumbledalmost 40 percent in 1996.

Although DRAM unit demand remained strong, not all categories experienced an uptick in ship-ments in 1996. SRAMs, EPROMs, and ROMs each suffered through a decline in shipments in1996. All three categories are forecast to experience additional shipment declines in 1997. Figure1-10 provides an overview of the complete unit shipment forecast for MOS memory devices.Additional unit shipment detail is found in each product section.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-6

DRAMSRAM

ROMEPROM

EEPROMFLASHOTHERTOTAL:

–––––––

70%13%

4%3%3%7%

<1%$36.0B

DRAMSRAM

ROMEPROM

EEPROMFLASHOTHERTOTAL:

–––––––

69%11%

4%3%3%

10%<1%

$31.0 B

DRAMSRAM

ROMEPROM

EEPROMFLASHOTHERTOTAL:

–––––––

75%10%

2%1%2%

10%<1%

$46.4B

DRAMSRAM

ROMEPROM

EEPROMFLASHOTHERTOTAL:

–––––––

73%10%

2%2%3%

10%<1%

$38.2B

1999

1998

17213L

1997

1996

DRAMSRAM

ROMEPROM

EEPROMFLASHOTHERTOTAL:

–––––––

77%9%1%1%2%

10%<1%

$60.1B

2000

DRAMSRAM

ROMEPROM

EEPROMFLASHOTHERTOTAL:

–––––––

79%8%1%

<1%2%

10%<1%

$78.8B

2001 DRAMSRAM

ROMEPROM

EEPROMFLASHOTHERTOTAL:

–––––––

80%7%1%

<1%1%

11%<1%

$103.8B

2002

Source: ICE, "Memory 1997"

Figure 1-8. MOS Memory Product Marketshare

A brief review of regional MOS memory consumption is shown in Figure 1-11. Driven by sales ofnew computers and upgrades to existing computer systems, the North America region led theworld in the consumption of memory ICs in 1995 and in 1996. Furthermore, it is forecast to remainthe leading consuming region in 1997.

The ROW region (Korea, Taiwan, et al), increased its share of memory IC consumption during thepast few years. For many years, the ROW was primarily a consumer of memory ICs that wereinstalled in various electronic systems then shipped abroad. More recently, however, the ROW’sconsumption of memory ICs has been to meet the growing domestic demand created by a matur-ing market-driven economy. Strong local economies in this region (along with greater disposableincome) will only lead to further consumption of MOS memory devices in the ROW region in thecoming years.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-7

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

������������������������������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

199719961995199419931992

���������

��������

Year

Un

its

(Mill

ion

s)

22426Source: ICE, "Memory 1997"

DRAM (M)

SRAM (M)

EPROM (M)

Flash (M)

ROM (M)

EEPROM (M)

Other Memory

Total Memory Units (M)

1,482

888

443

26

363

329

175

3,706

1,499

901

425

73

411

500

251

4,060

1,920

770

433

112

418

700

585

4,938

2,477

1,095

498

235

421

766

600

6,092

2,762

964

370

359

345

1,106

300

6,206

3,064

880

330

554

305

1,300

310

6,743

Figure 1-9. MOS Memory Unit Shipments by Product

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-8

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1997199619951994199319920

5

10

15

20

25

Un

its

(Mill

ion

s)

Per

cen

t C

han

ge

Source: ICE, "Memory 1997" 22427

3,706

17

Total Memory Units (M)

Percent Change

4,060

10

4,938

22

6,092

23

6,206

2

6,743

9

Total Memory Units (M)

Percent Change

Figure 1-10. Total MOS Memory Unit Shipments

North America37%

Japan23%

Europe18%

ROW22%

18912J

North America38%

Japan19%

Europe18%

ROW25%

1995$53.5B

1997 (FCST)$31.0B

North America38%

Japan20%

Europe19%

ROW23%

1996$36.0B

Source: ICE, "Memory 1997"

Figure 1-11. MOS Memory Consumption by Region

Figure 1-12 leaves no doubt that the Japanese companies remain the largest producer of MOSmemory devices, although the ROW region remains a keen competitor. With numerous huge, newDRAM fabs slated to come on line in 1997 and 1998, Korea, Taiwan, and other countries in theROW region will likely make further in-roads into Japan’s dominance of memory IC production.

Regional production for each MOS memory segment is shown for 1996 in Figure 1-13. In 1996,Japanese firms supplied the biggest portion of DRAMs, SRAMs (the two largest memory mar-kets), and ROMs. However, as shown in Figure 1-14, ROW firms continued to gain additionalmarketshare in each of the product segments (DRAM and SRAM) where Japan dominated.

North American companies maintained their recent 10-15 percent marketshare in the DRAM seg-ment, while dominating the EPROM, EEPROM, and fast-growing flash memory markets. SGS-Thomson, the world’s leading EPROM manufacturer, was the source of Europe’s strong showingin the EPROM market and was also a contributor to the flash memory market.

Listed in Figure 1-15 are marketshare figures for the top five worldwide MOS memory suppliersin 1995 and 1996. Together, the five firms accounted for approximately half of all MOS memorysales during the past two years.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-9

20173E

North AmericanCompanies

22%

North AmericanCompanies

21%

EuropeanCompanies

5%

EuropeanCompanies

4%

JapaneseCompanies

46%

JapaneseCompanies

45%

ROWCompanies

29%

ROWCompanies

28%

1996$36.0B

1995$53.5B

Source: ICE, "Memory 1997"

North AmericanCompanies

21%

EuropeanCompanies

5%

JapaneseCompanies

44%ROWCompanies

30%

1997 (FCST)$31.0B

Figure 1-12. MOS Memory Production

Samsung continued to set the pace as the leading supplier of MOS memory devices in 1996. Infact, it increased its marketshare in 1996. NEC, Toshiba, and Hitachi, three leading Japanese ICsuppliers, maintained their leading positions. New to the top memory IC supplier list in 1996 wasKorea’s Hyundai. Its 1996 memory sales were solely from DRAM devices.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-10

0

20

40

60

80

100

������������������������������������������������������������

����������������������������������������

������������������������������������

����������������

���� ����

4%

12%

35%

22%

3%

47%

28%

49%

2% 1%

78%

8%

58%52%

19%

33%

7%

38%

1%3%

EEPROM$785M

ROM$1,340M

SRAM$4,745M

EPROM$1,105M

DRAM$25,130M

������������������������

North AmericanCompanies

EuropeanCompanies

JapaneseCompanies

ROWCompanies

14516R

Per

cen

tag

e

87%

3%

9%

1%

Flash$2,610M

Source: ICE, "Memory 1997"

Figure 1-13. 1996 MOS Memory Production by Product Segment ($M)

0

20

40

60

80

100

1996199519941993

62%

25%

54%

28%

49%

33% 35%

49%

Per

cen

t

DRAM

0

20

40

60

80

100

1996199519941993

67%62%

6%10%

20% 22%

47%47%

Per

cen

t

SRAM

JAPAN

ROW =

=

Source: ICE, "Memory 1997" 21185B

Figure 1-14. ROW (Korea) Muscles Production from Japan

In Figure 1-16, ICE shows the memory IC usage by system type. Over the course of five years,end-use applications for memory devices changed very little while the market tripled in size.

THE ROM MARKET

Read-only memories (ROMs) represent the least expensive type of semiconductor memory. Theyare used primarily for storing data in electronic equipment such as laser printer fonts, dictionarydata in word processors, and sound-source data in electronic musical instruments. ROMs arealso used extensively in video game software. The ROM market grew well through the first halfof the 1990’s, coinciding closely with a jump in PC sales and other consumer-oriented electronicsystems (Figure 1-17).

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-11

Rank

1

2

3

4

5

Other

Total

Samsung

NEC

Hitachi

Toshiba

Hyundai

5,428

4,180

3,360

2,885

2,300

17,862

36,015

15

12

9

8

6

49

100

1996

Company Sales($M)

Marketshare(%)

—

—

Samsung

NEC

Hitachi

Toshiba

TI

7,545

5,630

5,028

4,535

3,555

27,172

53,465

14

11

9

8

7

50

100

1995

Company Sales($M)

Marketshare(%)

—

—

14495RSource: ICE, "Memory 1997"

Figure 1-15. Total MOS Memory Market Leaders

1991$12.3B

1996$36.0B

Computer68%

Communications10%

Consumer10%

Industrial8% Auto 2% Auto 2%

Military 1% Military 1%Industrial7%

Communications8%

Consumer13%

Computer70%

Source: WSTS/ICE, "Memory 1997" 21759A

Figure 1-16. Memory IC Usage by System Type

However, as shown in Figure 1-18, the ROM market declined significantly (-32 percent) in 1996.Among the reasons for the 32 percent decline in 1996 were the weak Japanese yen measuredagainst the dollar (109 yen to the dollar in 1996 versus 94 yen to the dollar in 1995). Since the ROMmarket is largely dominated by Japanese manufacturers and end users, it is closely tied to fluctu-ations in the yen.

Another factor contributing to the ROM market decline is the fact that one of the biggest end usersof these devices—video games—is moving toward CD-ROM-based machines. Additionally, othermemory products that afford greater functionality have become relatively cost competitive withROMs. As shown, ICE believes that the ROM market will continue to decline through the year2002.

Following several years of unit growth, ROM shipments also declined sharply (-18 percent) in1996 as shown in Figure 1-19. ICE anticipates this downward trend of ROM unit shipments tocontinue during the next five years as well.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-12

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1996199519941993199219910.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Mill

ion

s o

f D

olla

rs a

nd

Un

its

AS

P (

$)

Source: WSTS/ICE, "Memory 1997" 20607B

1,025

330

3.11

Market ($M)

Units (M)

ASP ($)

1,225

363

3.37

1,625

411

3.96

1,890

418

4.53

1,965

421

4.67

1,340

345

3.88

Market

Units

ASP

Figure 1-17. ROM Market History

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-13

Do

llars

(M

illio

ns)

Year

20348FSource: WSTS/ICE, "Memory 1997"

0

500

1,000

1,500

2,000

20022001200019991998199719961995199419931992

ROM Market ($M)

Percent Change

1,225

20

1,625

33

1,890

16

1,965

4

1,340

–32

1,100

–18

970

–12

870

–10

775

–11

610

–10

680

–12

–35

–30

–25

–20

–15

–10

–5

0

5

10

15

20

25

30

35

Per

cen

t C

han

ge

Figure 1-18. The ROM Market

Un

its

(Mill

ion

s)

Year

20608ASource: WSTS/ICE, "Memory 1997"

Total Units (M)

Percent Change

330

–8

363

10

411

13

418

2

421

1

305

–12

345

–18

0

50

100

150

200

250

300

350

400

450

1997199619951994199319921991

–20

–15

–10

-5

0

5

10

15

Per

cen

t C

han

ge

Figure 1-19. ROM Unit Shipments

Of the ROM units that continue to ship, more and more are high-density devices. Figure 1-20shows the trend toward high-density ROM devices. Most manufacturers kept their ROM pro-duction at the 4Mbit level. However, companies such as Sharp, NEC, and Macronix developedmask ROMs at and above the 32Mbit density.

Through the first half of the decade, the average selling price (ASP) for ROM devices increasedmostly due to the transition to higher density devices (Figure 1-21). Although the ROM ASPdeclined in 1996, a smaller ROM market moving toward higher densities may force ASPs to trendupward in the second half of the decade.

ROM consumption by geographic region is shown in Figure 1-22. Despite marketshare gainsmade by vendors in the ROW region, Japanese IC makers continued to hold a tight grip as theleading suppliers of ROM ICs (Figure 1-23). Together, Sharp and NEC held about half of the ROMmarket in 1995 and 1996. A few notes of activity from selected ROM suppliers are shown below.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-14

���������

������

0

50

100

150

200

250

300

350

400

450

�������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

199619951994199319921991

Un

its

(Mill

ion

s)

Source: WSTS/ICE, "Memory 1997" 20609A

200

130*

—

—

330

* Includes ≥4M densities.

≤2M

4M

8M

≥8M

159

204*

—

—

363

114

297*

—

—

411

100

130

73

115

418

86

124

83

128

421

61

91

84

109

345

Year

Total Units (M)

Figure 1-20. ROM Unit Shipments by Density

Sharp

Sharp remained the leading ROM supplier in 1996 and continued to bolster its portfolio of 3V,high-denisty ROMs. Additionally, it concluded that there was demand for 64Mbit ROM devicesand began mass producing these in 3Q96 using its 0.4µm process technology.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-15

AS

P (

$)

Year

20610ASource: WSTS/ICE, "Memory 1997"

Total ASP ($)

Percent Change

3.11

12

3.37

8

3.96

18

4.53

14

4.67

3

3.88

–17

3.61

–7

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

1997199619951994199319921991–20

–15

–10

–5

0

5

10

15

20

Per

cen

t C

han

ge

Figure 1-21. ROM ASPs

16790M

Japan61%

Europe3%

ROW19%

NorthAmerica

17%

Japan57%

Europe3%

ROW22%

NorthAmerica

18%

1995$1,965M

1996$1,340M

Source: WSTS/ICE, "Memory 1997"

Figure 1-22. ROM Market by Region

Sharp targeted the 32-bit embedded applications market when it introduced two ROMs (1Mbit x32 and 2Mbit x 16) in late 1996. Designed especially for 32-bit embedded systems, Sharp expectsits new 3V devices to be a popular choice in applications such as font storage in laser and ink-jetprinters where cost is critical and performance demands are high. Sharp believes its new deviceswill help reduce overall parts count, eliminate some system overhead, and improve overall systemperformance.

NEC

In 4Q96, NEC began taking orders for high-speed 32Mbit mask ROMs that operate at 3V.Targeting office and game machine program and fixed-data storage applications, the devices wereinitially priced at $27.50. Initial shipments were to begin at the rate of 350,000 units per month.

Macronix

Based on its proprietary Flat ROM cell technology, Macronix developed and now offers a ROMfamily ranging from 4Mbits to 16Mbits. The devices are manufactured using a 0.8µm processtechnology. The company is eager to move to the 32Mbit density for its ROM products. At thislevel, the devices will be manufactured using 0.6µm design rules.

American Microsystems Inc. (AMI)

Although not a leading ROM supplier, AMI unveiled two high-speed (45ns and 70ns) 1Mbitdevices targeted for disk drive applications. Initial versions operated at 5V, but the companyplans to introduce parts based on 3.3V technology in 1997.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-16

14496T

RankCompany Sales

($M)Marketshare

(%)

1

2

3

4

5

Other

Total

Sharp

NEC

Macronix

Toshiba

Hitachi

375

280

204

170

160

151

1,340

28

21

15

13

12

11

100

Sharp

NEC

Samsung

Toshiba

Hitachi

500

400

230

255

245

335

1,965

25

20

12

13

13

17

100

19961995

Company Sales($M)

Marketshare(%)

—

—

—

—

Source: ICE, "Memory 1997"

Figure 1-23. ROM Market Leaders

Siemens

An interesting ROM development targeting the multimedia market is the Record-On-Silicon(ROS) device from Siemens. With a 50-percent reduction in die area compared with conventionalROM, the company claims the ROS could halve the cost of conventional ROM and push into mar-kets for non-semiconductor storage, such as compact disks and photographic film. A 64Mbit ver-sion of the device is planned for introduction in 1997.

Fujitsu

In recent years, a few ROM suppliers announced intentions to withdraw from the mask ROMbusiness. Fujitsu, for example, cancelled development efforts of its 32Mbit and other next-gener-ation ROM devices and stopped producing and shipping its line of 16Mbit-and-smaller productsin 1996.

THE EEPROM MARKET

EEPROMs (electrically erasable programmable read only memories) offer users excellent capabil-ities and performance. Two key advantages of using EEPROMs include in-system reprogramma-bility and small, bit by bit erasure capability.

The EEPROM market forecast through the year 2002 is shown in Figure 1-24. In 1996, theEEPROM market was up four percent after posting two years of 20-plus percent growth. ICE fore-casts that through the year 2002, the EEPROM market will average 11 percent growth per year.

EEPROM consumption by region is shown in Figure 1-25. Due in part to military use, NorthAmerica was the largest regional market for EEPROMs in 1996.

EEPROMs are available in either a serial or parallel version. Parallel devices are generallyfaster, offer high endurance and reliability, but also cost more than their serial counterparts.Parallel EEPROMs are found mostly in the military market. Serial EEPROMs, though gener-ally less dense and slower than parallel devices, are much cheaper and used in more of the“commodity” applications.

ICE estimates that serial EEPROMs accounted for 92 percent of the $885 million EEPROM marketin 1996 (Figure 1-26). With few exceptions, the largest serial EEPROM density shipping in volumewas the 64Kbit device. Companies such as Atmel, Xicor, and SGS-Thomson supplied the largemajority of these devices.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-17

Until late in 1996, designers who needed more than 64Kbit of EEPROM had to use two or moresmaller serial EEPROMs connected in parallel. However, in 4Q96, SGS-Thomson pushed serialdensities to a new level with the introduction of its 128Kbit and 256Kbit devices.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-18

Do

llars

(M

illio

ns)

20347ESource: ICE, "Memory 1997"

EEPROM Market ($M)

Percent Change

480

19

700

43

885

23

920

4

975

6

1,090

12

1,210

11

1,490

10

1,650

11

720

20

1,355

12

Year

Per

cen

t C

han

ge

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

20022001200019991998199719961995199419931992–10

–5

0

5

10

15

20

25

30

35

40

45

Figure 1-24. EEPROM Market Growth

16792KSource: WSTS/ICE, "Memory 1997"

1996 $920M Europe

37%

ROW8%

North America

40%

Japan15%

Figure 1-25. 1996 EEPROM Market

The largest parallel EEPROMs built in volume during 1996 were 1Mbit devices. They were usedextensively, although not exclusively, in military applications. Parallel EEPROMs are of particularinterest in the military because they offer more flexibility than other kinds of solid-state memory.

Parallel EEPROMs can be found in military applications such as flight controllers, vehicle controlsystems, field communications equipment, secure radios, command and control systems, radar,and guidance subsystems. The lightness, ruggedness, and fast performance of parallel EEPROMsmake them well suited for harsh environments.

Consumer-oriented applications rep-resented the largest end-use of serialEEPROMs in 1996 (Figure 1-27). Ledby low-voltage parts, EEPROM sup-pliers in 1996 found a healthy andvibrant business in rapidly growingportable consumer and industrialapplications.

Small density serial EEPROMs wereused extensively in portable, bat-tery-powered devices includingpagers, modems, and cellular and cordless phones. They have also showed up in parameter andconfiguration setups in disk drives, printers, and industrial data-acquisition applications. In auto-motive applications, EEPROMs are used in air bags, antilock braking systems, and car radios.

Newer EEPROM applications include satellite communication boxes and monitors and sense-detect functions in memory modules. Suppliers are also excited about the potential of EEPROMsin the smart-card market.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-19

1996$920M

Serial EEPROM92% Parallel EEPROM

8%

20413CSource: ICE, "Memory 1997"

Figure 1-26. 1996 EEPROM Market by Type

Consumer36%

Telecom20%

Industrial15%

Office 7%

Automotive8%

Military/Aerospace7%

Computer-Related7%

Units

19520DSource: ICE, "Memory 1997"

Figure 1-27. Serial EEPROM Applications

Most leading manufacturers have begun to offer their devices in low-voltage versions. SGS-Thomson’s Eagle Range serial EEPROM family, for example, supports operation as low as 1.8Vand its next generation will support 1V operation. In 3Q96, Atmel introduced the first 3V 1Mbitparallel EEPROM.

Innovative features have been added to EEPROMs by many manufacturers. In 1996, Xicor intro-duced Block Lock protection on two of its EEPROMs. By allowing a user to partition its devicewith 25, 50, or 100 percent write protection, Block Lock allows the combination of alterable datawith secured data.

Several vendors agree that EEPROM technology is facing increased competition from flashmemory. However, flash memory remains a mass-storage technology and is virtually unavailable(and not as cost effective) in densities under 1Mbit. EEPROMs, on the other hand, are mainly usedfor storing small amounts of data that are frequently changed.

Leading EEPROM suppliers are shown in Figure 1-28. Atmel, SGS-Thomson, and Xicor contin-ued to make strides in the market. For these and other companies that manufacture them, theEEPROM business should remain reasonably healthy and stable through 2002.

SGS-Thomson

To meet a growing need, SGS-Thomson developed its “Super Flash” device, a part that combinesnon-volatile flash technology and full-featured EEPROM functionality. A key benefit of a com-bined EEPROM/flash chip, compared with the common technique of simulating EEPROM inflash memory, is that the host controller can read the flash memory while an EEPROM write cycleis in progress. SGS-Thomson plans to introduce the part in 1997.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-20

14498R

RankCompany Sales

($M)Marketshare

(%)

1

2

3

4

5

6

SGS-Thomson

Atmel

Xicor

Microchip

National

Siemens

280

180

115

109

70

66

100

920

30

20

12

12

8

7

11

100

167

154

100

85

64

53

262

885

19

17

11

10

7

6

30

100

1996

Company Sales($M)

Marketshare(%)

SGS-Thomson

Atmel

Xicor

Microchip

National

Siemens

Other

Total

—

—

Source: ICE, "Memory 1997"

1995

Figure 1-28. EEPROM Market Leaders

Atmel

Atmel unveiled its line of in-system programmable (ISP) EEPROM-based serial memories thatprovide an alternative approach to programming 3.3V SRAM-based field programmable gatearrays. The devices are designed to compete against and replace existing one-time-programma-ble (OTP) EPROM solutions that must be physically removed in order to reprogram FPGA con-figuration code. Atmel believes its ISP EEPROM will save time and afford greater flexibility in thepre-production stage of the FPGA product life when code is still evolving.

Xicor

Xicor introduced its family (4Kbit, 8Kbit, and 64Kbit) of serial peripheral interface (SPI) EEPROMsthat features 5MHz speed (Figure 1-29). The chips are targeted for use in mobile wireless systemsand also include the company’s Block Lock and partitioned memory architecture. It is specifiedto operate from a battery power source over the range of 2.5V to 5.5V.

The company also announced that Yamaha (Japan) signed on to manufacture its EEPROMsunder the Xicor brand name and that both companies would cooperate in process technologydevelopment.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION 1-21

Xicor SPI 5MHzSPI 2MHzMicroWire 1MHzI2C 0.1MHzSource: Xicor/ICE, "Memory 1997" 22428

Figure 1-29. Xicor Speeds SPI EEPROMs

Hitachi

Hitachi introduced 64Kbit and 256Kbit EEPROMs that can operate from voltages as low as 2.2V.The low voltage will help designers implement systems that can use unregulated portable powersupplies and will provide a power savings of about 20 percent compared to devices that operateat 2.7V. Samples of the 64Kbit devices were delivered in April 1997 (volume 3Q97), while the256Kbit part was slated for volume production in 2Q97. Pricing in volume quantities was set at$5.00 for the 64Kbit device and $10.00 for the 256Kbit product.

The MOS Memory Market

INTEGRATED CIRCUIT ENGINEERING CORPORATION1-22