the new f&he sorp and colleges - aoc

TRANSCRIPT

The New F&HE SORP and colleges 23 May 2014

Introduction and Background

1 In 2015, colleges will be adopting international accounting standards when

presenting their accounts. They will be doing this at the same time as

universities, charities and smaller companies, all of whom will be revising their

accounts in line with new Financial Reporting Standards (FRS 100, 101 and

102). The university and college sector in the UK has developed a new Further

and Higher Education Statement of Recommended Practice (F&HE SORP)

which makes these standards meaningful for education organisation. The new

F&HE SORP is effective from the 2015/16 financial year. College 2015/16

accounts will include comparative data for 2014/15 so it is necessary to start

work now.

2 The College Finance Directors’ Group (CFDG) and Association of Colleges (AoC)

would like all colleges to be sufficiently prepared for implementation of the

revised F&HE SORP. Although full implementation will not start until 1 August

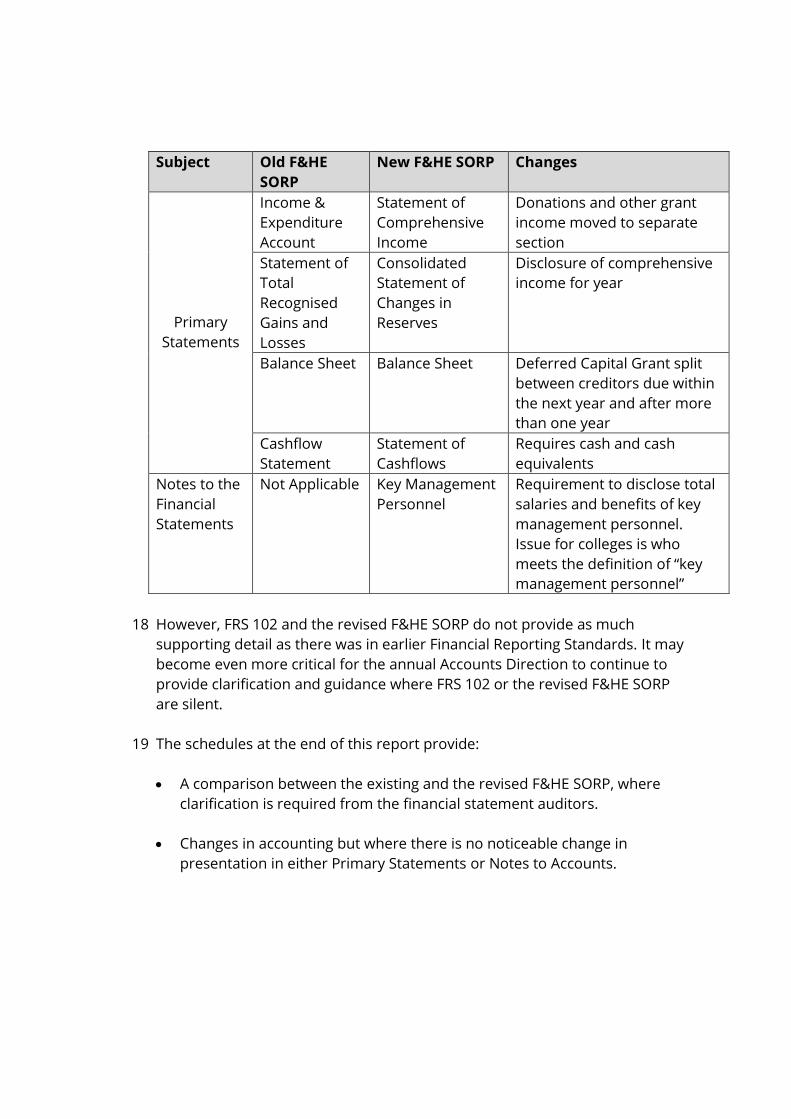

2015, being prepared is important and that colleges will need to commence

gathering the necessary information for the 2014-15 comparatives from 1

August 2014.

3 In order to prepare the sector for the change, Darwen Financial Management

Limited (DFM) was appointed to consider the implications. A working group of

college representatives was created to support DFM in this task (see Annex 1).

4 The initial view of this group is that many of the changes resulting from the

revised F&HE SORP may not be significant for some colleges but that time is

needed to fully evaluate them and to consult with the key audit firms and

other interested parties active in the further education sector.

5 The report provides:

An overview of the change.

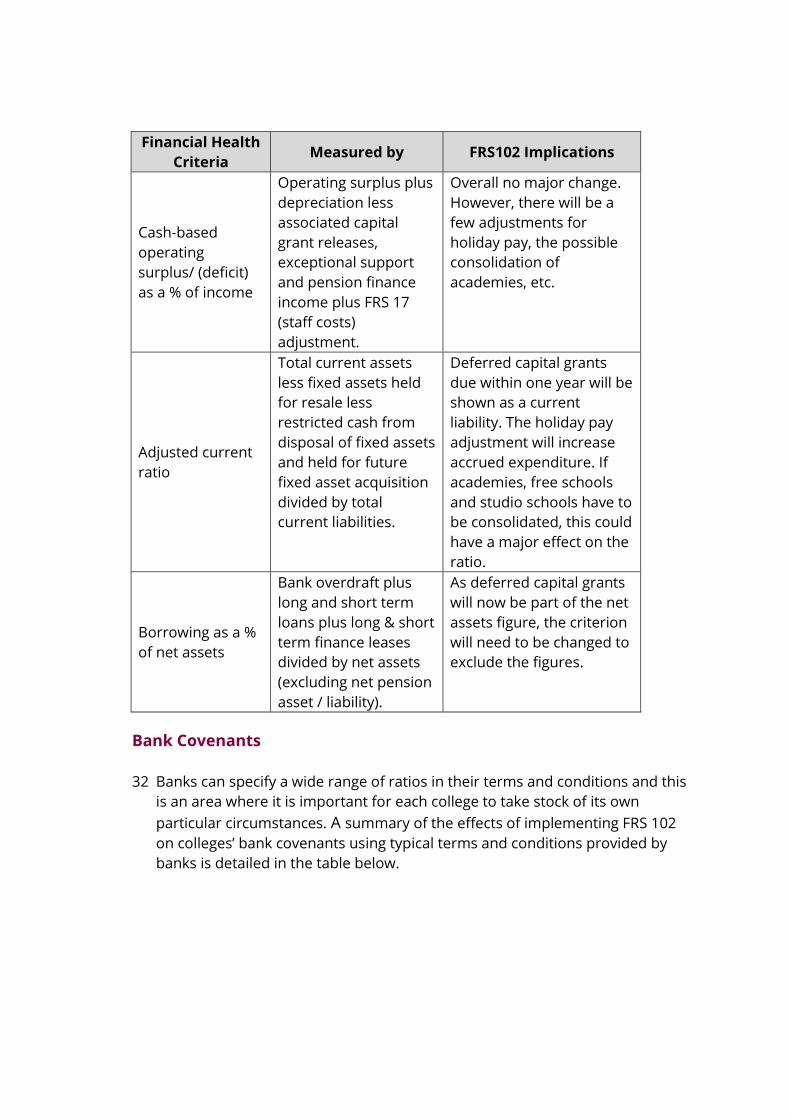

An assessment of the impact of the change on the annual Accounts

Direction and related guidance.

The impact of Financial Health Automatic Score Calculations.

The impact on bank covenants.

Actions the funding bodies and colleges need to take from now to

implementation of the revised F&HE SORP.

This change is important

6 The change is important because it also means colleges moving from

Generally Accepted Accounting Practice in the United Kingdom (UK GAAP) to

international accounting standards. For colleges, all the applicable

international standards are consolidated within the new concise Financial

Reporting Standard (FRS) 102 The Financial Reporting Standard Applicable in the

UK and Republic of Ireland. For many finance directors and managers, this will

mean a change away from the framework of accounting standards that may

have underpinned their initial professional training.

7 It has taken two years to develop the new F&HE SORP and this has been a

process which has involved college finance directors and AoC. The college

sector responded robustly to the draft F&HE SORP proposals issued for

consultation in July 2013. Changes were approved by the F&HE SORP Board in

December 2013 and the Financial Reporting Council approved the whole

document in March 2014.

The working group

8 It is only possible to understanding the impact of the new F&HE SORP by

looking at existing college data. The working group therefore agreed to collect

more information from colleges’ 2012/13 financial statements so that the

effects of could be modeled. The request was made via the Finance Directors’

JISC mailbase and by AoC. By 24 April 2014, 51 responses from colleges had

been received.

9 In April 2014, the Skills Funding Agency published College Accounts 2012/13.

This is a consolidation of all colleges’ 2012/13 finance records. The extra data

supplied by the respondent colleges has been added to the information

provided in the College Accounts 2012/13 publication. Accordingly, three new

tabs have been added to the data:

Comprehensive Income Statement (previously called the I&E account).

Balance Sheet.

Financial ratios.

10 The new tabs display, for each college, the existing Income and Expenditure

Account, Balance Sheet and Financial Ratios (from the 2012/13 accounts) and

set out the likely effects of the new F&HE SORP on these figures. In order to

ensure that colleges could quickly provide the extra information, only four

areas were chosen:

Deferred capital grant.

Holiday pay.

Academies, free schools, studio schools accounts for 2012/13 (where

not already consolidated).

Pooled pension schemes where the college has agreed a deficit

recovery programme.

11 On closer analysis of the 51 returns from colleges, the group decided to

restrict modelling the effects of the revised F&HE SORP for deferred capital

grant and holiday pay. The issues related to academy consolidation are critical

for some colleges but will need to be addressed on a case-by-case basis.

12 The model can be downloaded from AoC’s website at

http://www.aoc.co.uk/funding-and-corporate-services/funding-and-

finance/accounting

13 To operate the model, users will need to choose their college short code at cell

D4 of the Comprehensive Income Statement.

14 Where a college has supplied the data, the key changes will be evident at:

The Total Net Assets/(Liabilities) line of the Balance Sheet.

Columns E and F of the Comprehensive Income Statement.

15 If a college has not provided any of the extra information requested, they can

still see the effect of implementing the new F&HE SORP. However, there will

not be any breakdown of, say, the deferred capital grant. For these colleges, in

order to ensure everything balances, the deferred capital balance has been

released fully to the Comprehensive Income Statement. To complete this in

line with actual data, non-respondent colleges will need to know and fill in the

split between what is due to be released within 12 months and after 12

months.

The key changes

16 The F&HE SORP is being revised because of the mandatory implementation of

FRS 102. FRS 102 brings about the long anticipated convergence with

international accounting standards. FRS 102 replaces all previously issued

extant Statements of Standard Accounting Practice, and Financial Reporting

Standards up to and including FRS 30 Heritage Assets.

17 FRS 102 would appear to be broadly similar in many aspects with current UK

GAAP. The key differences to the primary statements are summarised in the

table below:

Subject Old F&HE

SORP

New F&HE SORP Changes

Primary

Statements

Income &

Expenditure

Account

Statement of

Comprehensive

Income

Donations and other grant

income moved to separate

section

Statement of

Total

Recognised

Gains and

Losses

Consolidated

Statement of

Changes in

Reserves

Disclosure of comprehensive

income for year

Balance Sheet Balance Sheet Deferred Capital Grant split

between creditors due within

the next year and after more

than one year

Cashflow

Statement

Statement of

Cashflows

Requires cash and cash

equivalents

Notes to the

Financial

Statements

Not Applicable Key Management

Personnel

Requirement to disclose total

salaries and benefits of key

management personnel.

Issue for colleges is who

meets the definition of “key

management personnel”

18 However, FRS 102 and the revised F&HE SORP do not provide as much

supporting detail as there was in earlier Financial Reporting Standards. It may

become even more critical for the annual Accounts Direction to continue to

provide clarification and guidance where FRS 102 or the revised F&HE SORP

are silent.

19 The schedules at the end of this report provide:

A comparison between the existing and the revised F&HE SORP, where

clarification is required from the financial statement auditors.

Changes in accounting but where there is no noticeable change in

presentation in either Primary Statements or Notes to Accounts.

Specific guidance in the Accounts Direction Handbook

20 The funding bodies publish an annual Accounts Direction to colleges in the

form of the Accounts Direction Handbook. The handbook has been a “one-

stop shop” which relates solely to further education colleges and sixth form

colleges and which helps finance directors deal with specific issues, for

example Train to Gain accounting or land and buildings owned by a third party

(for example a trust or church).

21 All references to existing UK GAAP and the old F&HE SORP in the current

handbook will need to be checked against the relevant paragraph of FRS 102

and/or the revised F&HE SORP.

22 Consultation should take place with colleges regarding the applicability of

certain sections of Chapter 6 ‘Detailed Guidance on Specific Topics’. For example,

the chapter provides several pages on discontinued activities, but these are

rare. Is this guidance still required? It would be sensible to create a working

group to review the handbook to ensure only relevant and up to date

information is published.

23 Chapter 5 of the handbook covers guidance on the preparation of the annual

report and notes to the financial statements. This chapter will need to be

revised to reflect the new layout of the primary statements and the extra

disclosures notes, such as the requirement to disclose total salaries and

benefits of key management personnel.

24 The Enhanced Pension spreadsheet will need to be checked to ensure that its

methodology is still applicable under FRS 102.

Financial Planning

25 Apart from detailing any necessary changes to the automatic financial health

calculation, the detailed guidance notes of the Financial Planning Publication

issued by the funding bodies does not need to be changed to reflect the

revised F&HE SORP.

26 The financial planning template will need to be up-dated to reflect:

Changes to the primary statements.

Changes to the automatic financial health score (see below).

A need to update the help facility in some cells (shown by a red cap in the

right hand side of a cell).

Transitional arrangements. For example, should the figures for the 2014/15

forecast outturn reflect the old or revised F&HE SORP; how will prior year

adjustments be shown?

Deferred capital grants in schedule 2e being moved to the creditors’

schedule 2d.

Finance Record

27 Although the Finance Record for 2014/15 should reflect the old F&HE SORP,

additional schedules will need to be added to the spreadsheet for the revised

F&HE SORP. This will enable both the funding bodies and the college to see the

impact of the revised F&HE SORP. It would be sensible for funding bodies

request the financial statements auditors to review these figures when

auditing the 2014/15 accounts. This will provide the college with certainty that

their auditors are content with the opening balance figures at 1 August 2015.

College Accounts Publication

28 The College Accounts publication is issued annually by the funding bodies to

provide a snapshot of the health of the FE sector as at 31 July. It is produced

through collating all colleges’ finance records into one return. Various

stakeholders, ranging from banks, trade unions, newspapers, competitors and

the public use it. It will be necessary to explain the figures because the

changes resulting from the new capital grant accounting may be large. If a

particular college had net assets of £45m using the old F&HE SORP, and now

has net liabilities of £5m using the revised F&HE SORP, clarification is required.

Funding agencies will need to provide clarification when the spreadsheet is

published.

Financial Health Automatic Score Calculations

29 The funding bodies’ approach to grading the financial health of colleges is

incorporated into the college financial returns. It results in one of four

assessment grades: outstanding, good, satisfactory or inadequate.

30 In calculating the automatic financial health score, the following criteria are

used:

Cash-based operating surplus/ (deficit) as a % of income.

Adjusted current ratio.

Borrowing as a % of net assets.

31 The effect of the revised F&HE SORP on the above three criteria is overleaf:

Financial Health

Criteria Measured by FRS102 Implications

Cash-based

operating

surplus/ (deficit)

as a % of income

Operating surplus plus

depreciation less

associated capital

grant releases,

exceptional support

and pension finance

income plus FRS 17

(staff costs)

adjustment.

Overall no major change.

However, there will be a

few adjustments for

holiday pay, the possible

consolidation of

academies, etc.

Adjusted current

ratio

Total current assets

less fixed assets held

for resale less

restricted cash from

disposal of fixed assets

and held for future

fixed asset acquisition

divided by total

current liabilities.

Deferred capital grants

due within one year will be

shown as a current

liability. The holiday pay

adjustment will increase

accrued expenditure. If

academies, free schools

and studio schools have to

be consolidated, this could

have a major effect on the

ratio.

Borrowing as a %

of net assets

Bank overdraft plus

long and short term

loans plus long & short

term finance leases

divided by net assets

(excluding net pension

asset / liability).

As deferred capital grants

will now be part of the net

assets figure, the criterion

will need to be changed to

exclude the figures.

Bank Covenants

32 Banks can specify a wide range of ratios in their terms and conditions and this

is an area where it is important for each college to take stock of its own

particular circumstances. A summary of the effects of implementing FRS 102

on colleges’ bank covenants using typical terms and conditions provided by

banks is detailed in the table below.

Bank Covenant

FRS102 Implications Outstanding Issues

Total external debt shall

not exceed XX% for

DD/MM/201Y of total

reserves (excluding

exceptional items).

Please refer to the

revenue reserves

comment below.

Treatment of inherited

revaluation reserves and their

possible release to the Income

and Expenditure Account

reserve.

Total borrowing costs

not to exceed A% of

total consolidated

income (incl. grant

income) (Interest Paid

+Capital Repayments

divided by Total

Income).

Total consolidated

income subject to annual

fluctuations due to

releases of non

Government Deferred

Capital Grants.

The possible consolidation of

academies, free schools and

studio schools into colleges'

accounts, will inflate income.

Clarification is sought from

banks whether they will

continue to exclude from their

calculations academies, free

schools and studio schools

because these organisations

cannot borrow without the

permission of the Secretary of

State for Education.

Borrowing could increase

due to the removal of the

90% rule for assessing

whether a transaction

should be treated as a

finance lease.

Revenue reserves shall

not be less than XX% of

the total consolidated

income for

DD/MM/201Y

Revenue reserves could

change due to a greater

emphasis on component

accounting (leading to

higher depreciation);

holiday pay accruals;

treatment of non

Government deferred

capital grants.

Treatment of inherited

revaluation reserves and their

possible release to the Income

and Expenditure Account

reserve.

As per comment above

regarding total borrowing costs

not exceeding A% of total

consolidated income.

Historical Cost Deficits

permitted in 2 out of

any 3 years

Historical cost

surplus/(deficit) figure

does not appear in

Statement of

Comprehensive Income.

Clarification is sought from the

banks whether they will

continue to ask colleges for the

historical cost figure or will

request an equivalent

figure.Clarification is also

sought on their reaction to the

impact of a release of a non-

government grant in a single

year in accordance with FRS102.

Historical Cost Deficit

shall not be above

£500k in any one year.

Historical cost

surplus/(deficit) figure

does not appear in

Statement of

Comprehensive Income.

Action from now to implementation of the revised F&HE SORP Funding agencies

33 The two funding agencies will issue clear and timely guidance on the

implementation of the revised F&HE SORP before the 2015/16 financial

statements need to be prepared. As colleges will need to prepare 2014/15

comparatives in the 2015/16 financial statements, it is essential that the

funding agencies provide this guidance by March 2015 at the latest.

34 The financial plan template completed by colleges between May and July 2015

will include a forecast outturn for 2014/15 based upon the old F&HE SORP and

figures after 1 August 2015 based upon the revised F&HE SORP. A decision will

need to be made on whether this is acceptable or should be changed to use

the same basis, such as the revised F&HE SORP.

35 The finance record for 2014/15 will be the last year for colleges using the old

F&HE SORP. Additional schedules should be added to the spreadsheet so that

the figures are also displayed using the revised F&HE SORP. This will have the

advantage for the college, in that they would have already calculated the

2014/15 comparator figures for the following year’s financial statements.

36 While the 2013/14 finance record has been published without any additional

schedules, the funding bodies may consider publishing an amended version in

late summer, after clarification has been sought from the audit firms on the

issues detailed below. As such, it would provide colleges with opening

balances for 1 August 2014 and institutions could at least give an indication of

the impact in their own discussions with banks, etc.

Colleges

37 Colleges need to model the effect of the revised F&HE SORP on their accounts.

Although a template has been provided with this report, each college will have

unique characteristics, which may not be reflected in the template.

38 If the college has borrowing, then it needs to discuss with its lender the

implications of the implementation of the revised F&HE SORP on its existing

covenants.

39 Colleges need to inform senior management and the Board of the implications

of the revised F&HE SORP.

40 There could be a training need for both governors and staff.

Acknowledgements

41 AoC and CFDG would like to thank Darwen Financial Management Limited for

preparing this report, the college Finance Directors who volunteered to be

members of the steering group, and BUFDG for allowing extracts of the Pilot

Conversion Summary Report to be used.

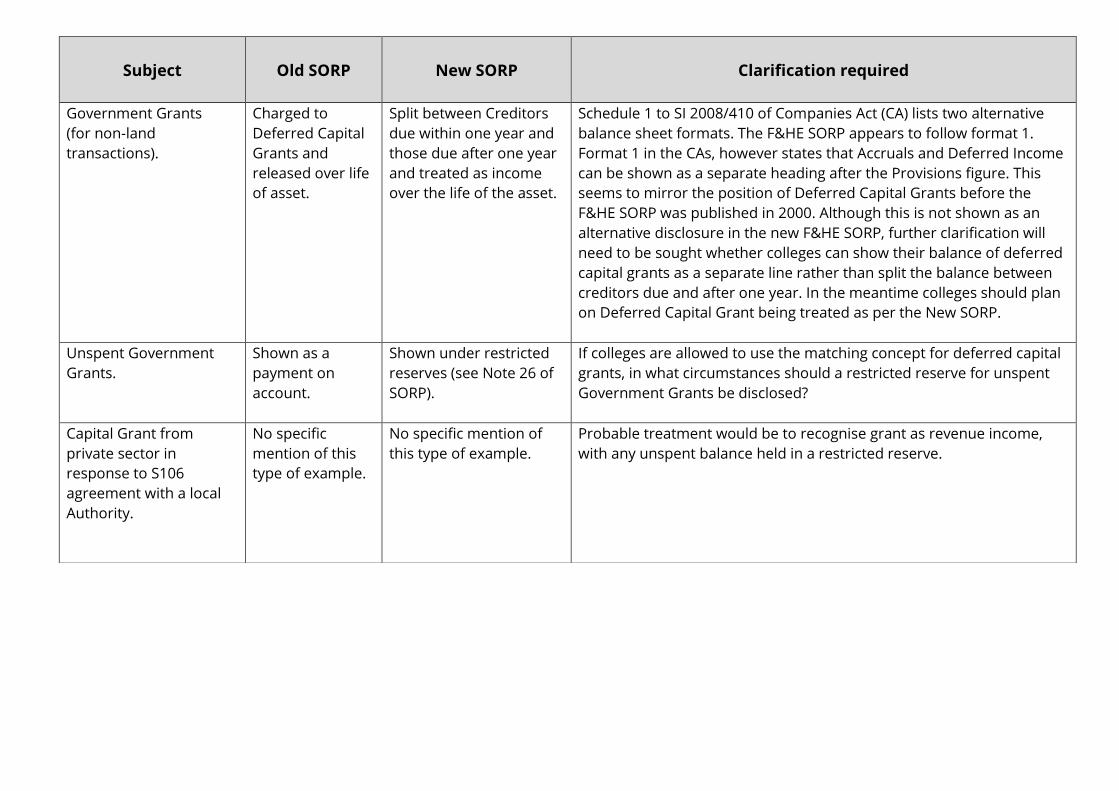

Subject

Old SORP New SORP Clarification required

Government Grants

(for non-land

transactions).

Charged to

Deferred Capital

Grants and

released over life

of asset.

Split between Creditors

due within one year and

those due after one year

and treated as income

over the life of the asset.

Schedule 1 to SI 2008/410 of Companies Act (CA) lists two alternative

balance sheet formats. The F&HE SORP appears to follow format 1.

Format 1 in the CAs, however states that Accruals and Deferred Income

can be shown as a separate heading after the Provisions figure. This

seems to mirror the position of Deferred Capital Grants before the

F&HE SORP was published in 2000. Although this is not shown as an

alternative disclosure in the new F&HE SORP, further clarification will

need to be sought whether colleges can show their balance of deferred

capital grants as a separate line rather than split the balance between

creditors due and after one year. In the meantime colleges should plan

on Deferred Capital Grant being treated as per the New SORP.

Unspent Government

Grants.

Shown as a

payment on

account.

Shown under restricted

reserves (see Note 26 of

SORP).

If colleges are allowed to use the matching concept for deferred capital

grants, in what circumstances should a restricted reserve for unspent

Government Grants be disclosed?

Capital Grant from

private sector in

response to S106

agreement with a local

Authority.

No specific

mention of this

type of example.

No specific mention of

this type of example.

Probable treatment would be to recognise grant as revenue income,

with any unspent balance held in a restricted reserve.

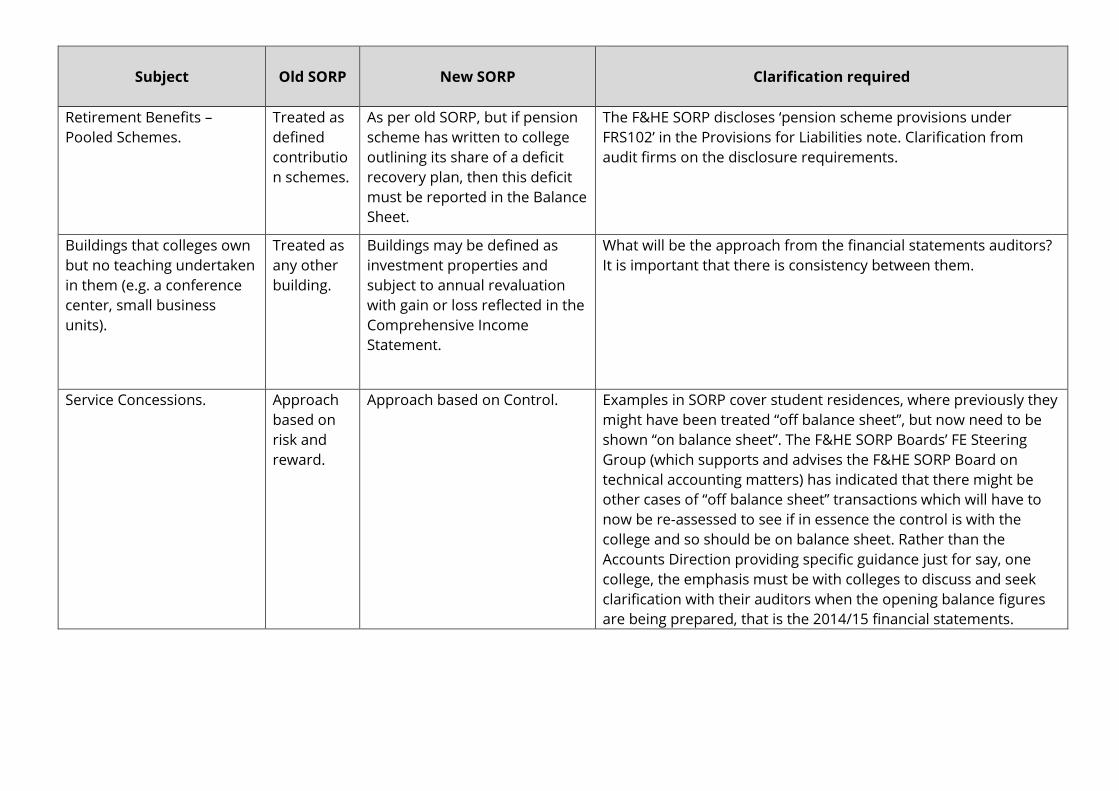

Subject Old SORP New SORP

Clarification required

Retirement Benefits –

Pooled Schemes.

Treated as

defined

contributio

n schemes.

As per old SORP, but if pension

scheme has written to college

outlining its share of a deficit

recovery plan, then this deficit

must be reported in the Balance

Sheet.

The F&HE SORP discloses ‘pension scheme provisions under

FRS102’ in the Provisions for Liabilities note. Clarification from

audit firms on the disclosure requirements.

Buildings that colleges own

but no teaching undertaken

in them (e.g. a conference

center, small business

units).

Treated as

any other

building.

Buildings may be defined as

investment properties and

subject to annual revaluation

with gain or loss reflected in the

Comprehensive Income

Statement.

What will be the approach from the financial statements auditors?

It is important that there is consistency between them.

Service Concessions.

Approach

based on

risk and

reward.

Approach based on Control. Examples in SORP cover student residences, where previously they

might have been treated “off balance sheet”, but now need to be

shown “on balance sheet”. The F&HE SORP Boards’ FE Steering

Group (which supports and advises the F&HE SORP Board on

technical accounting matters) has indicated that there might be

other cases of “off balance sheet” transactions which will have to

now be re-assessed to see if in essence the control is with the

college and so should be on balance sheet. Rather than the

Accounts Direction providing specific guidance just for say, one

college, the emphasis must be with colleges to discuss and seek

clarification with their auditors when the opening balance figures

are being prepared, that is the 2014/15 financial statements.

Subject Old SORP

New SORP

Changes

Consolidation of

subsidiaries.

Question of

control and

risk and

reward.

Question of control. If academies have to be consolidated, clarification is required over

their financial year. FRS102 indicates that the consolidation of the

subsidiary can be based on financial statements made up to its last

reporting date, providing that the subsidiary’s accounting period

ends no more than three months before that of its parent. If not,

the subsidiary must prepare interim financial statements to

coincide with the end of the parent’s financial year. Academies

have a 31 August financial year end, which is 11 months before the

college year end date of 31 July. Interim financial statements may

be required.

Treatment of EFA income if

academies are

consolidated.

No

mention.

No mention. Academies must show any EFA/DfE income as ‘restricted income’ in

their accounts. Colleges will also receive funding from the EFA/DfE

via the SFA. If academies’ accounts are consolidated, how should

this income and associated expenditure be treated? If it is left as

restricted, then shouldn’t all Government funding be treated as

restricted as well?

Revaluation Reserves. Covered in

old SORP.

No change. BUFDG1 commissioned a consultant to oversee a number of

pilotsat universities to consider in the main university based

issues. In one of the conclusions2, the consultant indicates that on

transition all historic revaluation reserves will be released to

‘retained earnings’, which is taken to mean the Income and

Expenditure Account Reserve. However, there is no other

reference to this in either the F&HE SORP or FRS102. Therefore,

clarification is required to be sought from audit firms.

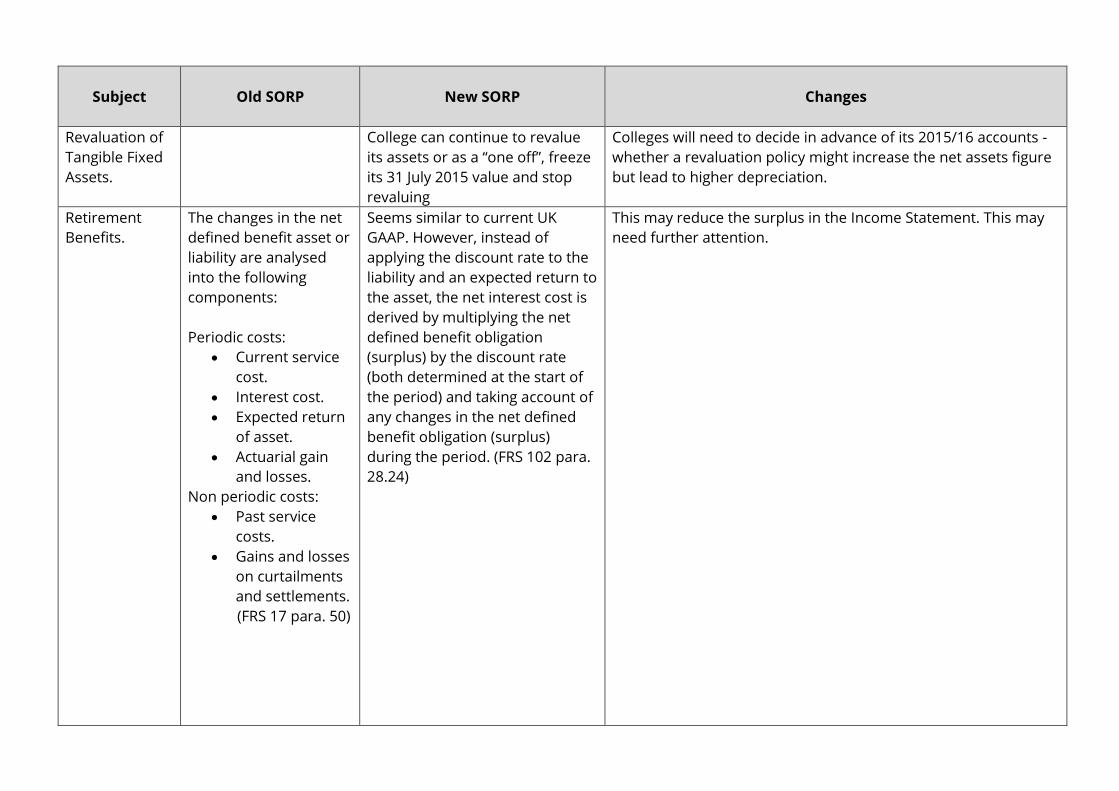

1British Universities Finance Directors Group 2 BUFDG “The Pilot Conversion Summary Report”, published October 2013, Page 28 Revaluation Reserves

Subject Old SORP

New SORP

Changes

Revaluation of

Tangible Fixed

Assets.

College can continue to revalue

its assets or as a “one off”, freeze

its 31 July 2015 value and stop

revaluing

Colleges will need to decide in advance of its 2015/16 accounts -

whether a revaluation policy might increase the net assets figure

but lead to higher depreciation.

Retirement

Benefits.

The changes in the net

defined benefit asset or

liability are analysed

into the following

components:

Periodic costs:

Current service

cost.

Interest cost.

Expected return

of asset.

Actuarial gain

and losses.

Non periodic costs:

Past service

costs.

Gains and losses

on curtailments

and settlements.

(FRS 17 para. 50)

Seems similar to current UK

GAAP. However, instead of

applying the discount rate to the

liability and an expected return to

the asset, the net interest cost is

derived by multiplying the net

defined benefit obligation

(surplus) by the discount rate

(both determined at the start of

the period) and taking account of

any changes in the net defined

benefit obligation (surplus)

during the period. (FRS 102 para.

28.24)

This may reduce the surplus in the Income Statement. This may

need further attention.

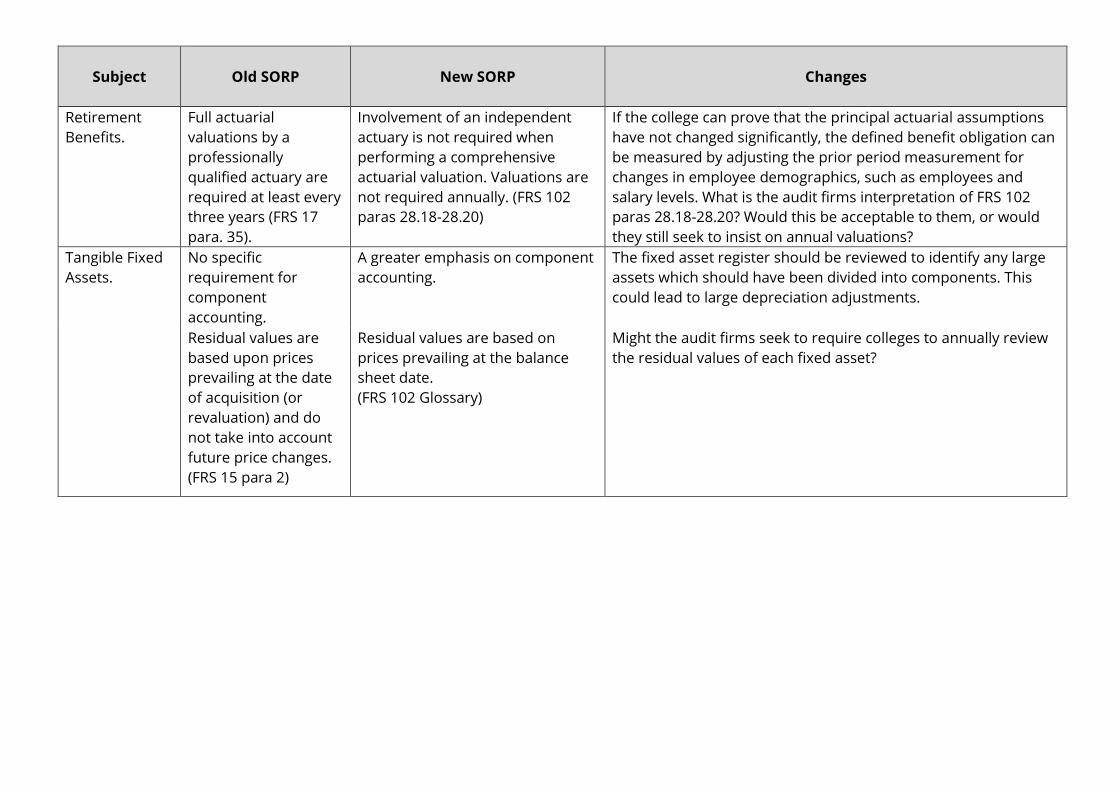

Subject

Old SORP

New SORP Changes

Retirement

Benefits.

Full actuarial

valuations by a

professionally

qualified actuary are

required at least every

three years (FRS 17

para. 35).

Involvement of an independent

actuary is not required when

performing a comprehensive

actuarial valuation. Valuations are

not required annually. (FRS 102

paras 28.18-28.20)

If the college can prove that the principal actuarial assumptions

have not changed significantly, the defined benefit obligation can

be measured by adjusting the prior period measurement for

changes in employee demographics, such as employees and

salary levels. What is the audit firms interpretation of FRS 102

paras 28.18-28.20? Would this be acceptable to them, or would

they still seek to insist on annual valuations?

Tangible Fixed

Assets.

No specific

requirement for

component

accounting.

A greater emphasis on component

accounting.

The fixed asset register should be reviewed to identify any large

assets which should have been divided into components. This

could lead to large depreciation adjustments.

Residual values are

based upon prices

prevailing at the date

of acquisition (or

revaluation) and do

not take into account

future price changes.

(FRS 15 para 2)

Residual values are based on

prices prevailing at the balance

sheet date.

(FRS 102 Glossary)

Might the audit firms seek to require colleges to annually review

the residual values of each fixed asset?

Subject

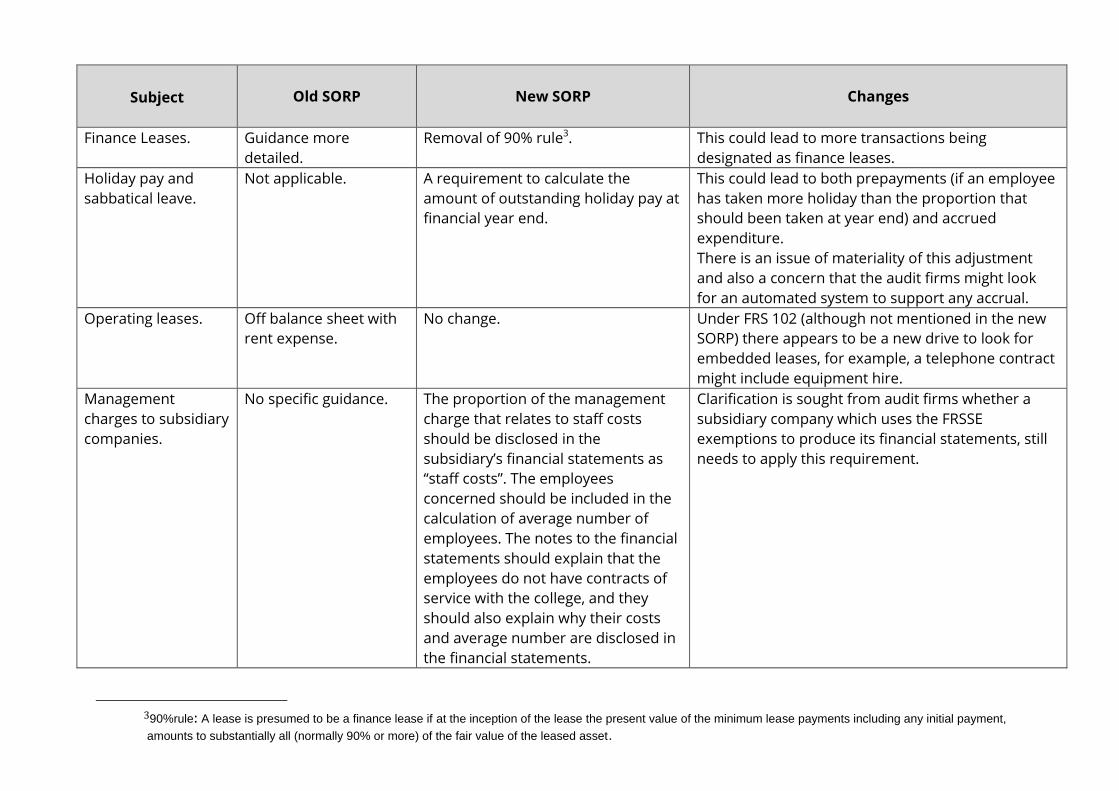

Old SORP New SORP Changes

Finance Leases. Guidance more

detailed.

Removal of 90% rule3. This could lead to more transactions being

designated as finance leases.

Holiday pay and

sabbatical leave.

Not applicable. A requirement to calculate the

amount of outstanding holiday pay at

financial year end.

This could lead to both prepayments (if an employee

has taken more holiday than the proportion that

should been taken at year end) and accrued

expenditure.

There is an issue of materiality of this adjustment

and also a concern that the audit firms might look

for an automated system to support any accrual.

Operating leases. Off balance sheet with

rent expense.

No change. Under FRS 102 (although not mentioned in the new

SORP) there appears to be a new drive to look for

embedded leases, for example, a telephone contract

might include equipment hire.

Management

charges to subsidiary

companies.

No specific guidance. The proportion of the management

charge that relates to staff costs

should be disclosed in the

subsidiary’s financial statements as

“staff costs”. The employees

concerned should be included in the

calculation of average number of

employees. The notes to the financial

statements should explain that the

employees do not have contracts of

service with the college, and they

should also explain why their costs

and average number are disclosed in

the financial statements.

Clarification is sought from audit firms whether a

subsidiary company which uses the FRSSE

exemptions to produce its financial statements, still

needs to apply this requirement.

390%rule: A lease is presumed to be a finance lease if at the inception of the lease the present value of the minimum lease payments including any initial payment,

amounts to substantially all (normally 90% or more) of the fair value of the leased asset.

Appendix

Members of the Steering Group

Name Organisation

Alan Searle Skills Funding Agency

Brian Godbold Godbold Consultancy

Brian Page Epping Forest College

Chris Knight North Warwickshire and Hinckley College

David McIntyre City Liverpool College

Evelyn Dixon Highbury College

Jennifer Eastham Myerscough College

John Foster Wakefield College

Kevin Hodge City of Islington College

Marc Webb Richard Huish College

Margaret Playle Bridgwater College

Mark Albrighton West Nottinghamshire College

Mike Hobbs Education Funding Agency

Peter Darwen Darwen Financial Management Limited

Rav Garcha Walsall Adult Community College

Sarah Horan Loreto College

Tracy Waite Leeds City College