the new planning paradigm: 1. introduction

TRANSCRIPT

1.

1. Introduction The high transfer tax exemptions adopted in the American Taxpayer’s Relief Act of 2012 (“ATRA”) and the significant income tax increases enacted in 2013 combine to drastically alter the dynamics in planning for our clients. The new laws have created a radically different landscape where many of our traditional solutions are no longer appropriate. In response to this new planning paradigm, Advanced Markets has created a new five issue series titled “ The New Planning Paradigm” which addresses the issues, concerns and opportunities in this new world. This issue examines investment, income, and insurance strategies that involve charities, charitable trusts, and private foundations. 2. Charitable Remainder Trust Although the IRC generally prevents gifts of partial interests, certain gifts and bequests to an irrevocable trust may be used to provide an interest in trust property to both a charitable and a non-charitable beneficiary. The charitable remainder trust (CRT) provides income to a non-charitable beneficiary for a term (or lifetime) and then passes the remainder interest to charity.1 The charitable lead trust (CLT) acts similarly, but in the opposite order; a charity receives income for a term and a non-charitable beneficiary receives the remainder. _______________________________

The New Planning Paradigm: Part 4 Charitable Giving Strategies _______________________________ Inside This Issue:

1. Introduction

2. Charitable Remainder Trust

3. Charitable Lead Trust

4. Charitable Gift Annuity

5. Wealth Replacement Trust

6. Charity-Owned Assets

7. Use of Life Insurance in a Private

Foundation

8. Conclusion

______________________________

1 The IRS provides sample documents for several forms of CRATs (see Rev. Proc. 2003-53, 2003-2 CB 230 through 2003-60, 2003-2 CB 274) and CRUTs (see Rev. Proc. 2005-52, 2005-34 IRB 326 through Rev. Proc. 2005-59, 2005-34 IRB 412).

Legal & Tax Trends is provided to you by a coordinated effort among the Advanced Markets Consultants.

Page 1 of 21

Charitable remainder trusts come in two basic types, the annuity trust (CRAT) and the unitrust (CRUT).2 A CRAT is a trust in which a fixed sum of not less than 5% (and no more than 50%) of the initial principal placed in the trust is paid at least annually to the non-charitable income beneficiary. A CRUT generally distributes a fixed percentage (but not less than 5% or more than 50% of the FMV of its assets) of the prior year ending value of the trust property to a non-charitable income beneficiary.3 Although each trust may have different payout terms, all CRTs must be structured so that there is an actuarial expectation that at least 10% of the trust’s initial value will pass to charity at the end of the term.4 A number of advantages have helped the CRT become a popular giving vehicle. Upon creation of the trust during life, the donor receives a current income and gift tax deduction based on the value of the future interest expected to pass to the charity.5 The trust is a tax-exempt entity, and may sell assets without paying income tax. Funding a CRT will reduce the donor’s estate tax, since assets are removed from the estate (in the case of a lifetime CRT) or create an estate tax deduction (in the case of a testamentary CRT) for the value expected to pass to charity.6 A CRT has two primary disadvantages. First, the trust is irrevocable. While a donor may carefully choose the most appropriate payout for his or her situation, the choice of formula or trust type may not be changed once the trust is created. Second, the trust, while not taxed itself, will pass income out to the beneficiary under an unfavorable scheme: ordinary income first, then capital gains, then non-taxable earnings and finally return of basis.7

A common form of the CRT involves the donation of low income-producing capital-gain property to a CRUT in which the donor retains an income interest. A CRT may sell and reinvest the gross proceeds for a desired income amount where the donor would otherwise only be able to reinvest the net after tax amount.8 Capital assets, e.g., stocks, bonds, etc., may be more attractive than ordinary income assets, e.g., life insurance, because the charitable deduction calculation for donations of a capital asset is based on the property’s fair market value, not the

2 See IRC §664 for CRTs, generally. 3 A donor may create a version of a CRUT known as a NICRUT from which the lifetime beneficiary will receive the lesser of trust income or the unitrust amount. Another form is the NIMCRUT, which acts as a NICRUT but allows for the trustee to “make-up” any prior distribution shortfalls during later years when income exceeds the unitrust amount. NICRUTs and NIMCRUTS may also switch or “flip” to become traditional CRUTs upon a triggering event. 4 Treasury Regulations provide that the donor must use the published 7520 rate in the calculations used to determine the relative value of the income and remainder interests for both CRTs and CLTs. 5 Since the value passing to charity will depend on investment performance, the actual amount passing to charity will not be known until the trust terminates and distributes the remaining assets. The apportionment of value between income beneficiary and charitable beneficiary is based on assumed rates of return (which use the 7520 rate for the month in question). 6 Many donors find that the costs of establishing and administering a charitable trust will not be justified for a gift of less than $100,000. 7 See IRC §664(b) for the tier system ordering rules. 8 The IRS will apply the step transaction doctrine to invalidate a donation to a CRT where there is an implied agreement or understanding that the CRT will sell the contributed property. In cases where, for example, a donor has negotiated a sale with buyer but decides to first give the property to a CRT, the IRS will treat the events as a sale by the donor and then a contribution of the proceeds. As a result, where evidence of a pre-arranged sale exists, prospective donors should be made aware of the risk that all the gain will still be charged to the donor in the year of the sale.

Page 2 of 21

basis. A unitrust allows the donor to participate in the future growth of the trust where an annuity trust would limit the donor’s interest to the same fixed dollar amount each year. The donor may receive increased income if the trust invests in assets that earn a higher rate of return than the asset. The trust also has more to invest since it does not pay capital gains tax on the sale of the asset.

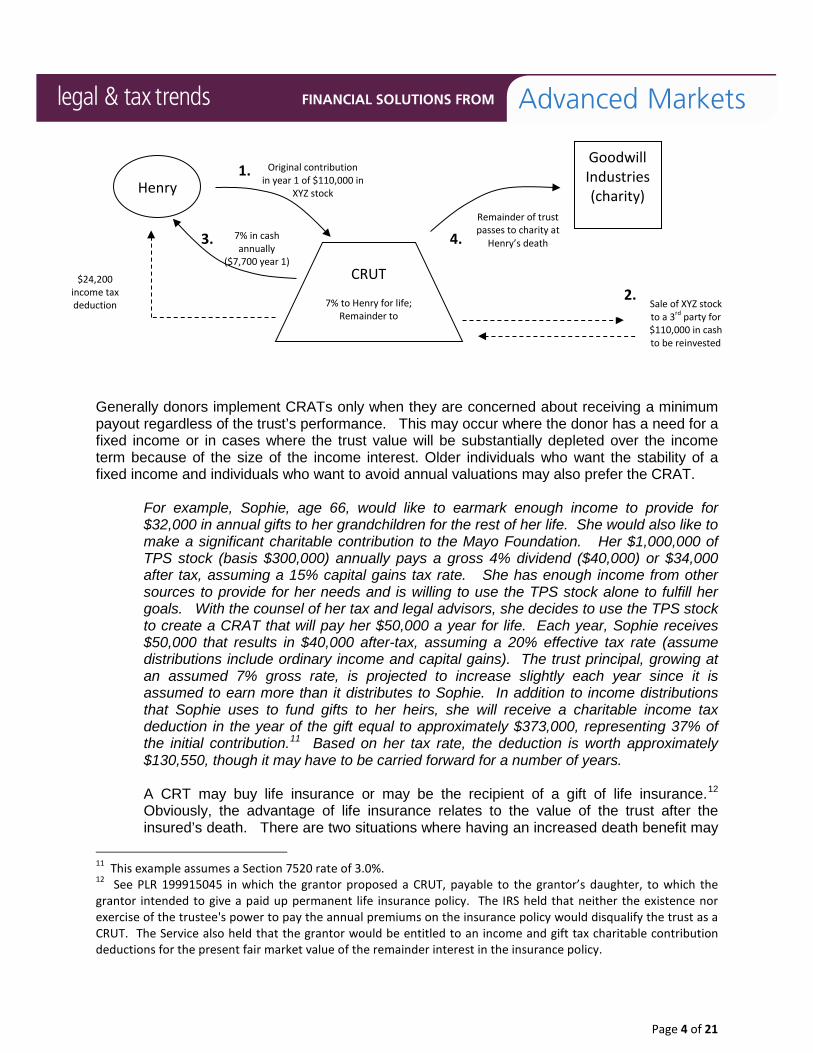

For example, consider a client, Henry, who is 55 years old and has a gross estate of $6,600,000. He is considering leaving a bequest to Goodwill Industries Int’l. Assume he owns highly appreciated XYZ stock, which cost $10,000. It is now worth $110,000 and pays a 3% dividend ($3,300 per year). If Henry sold the asset himself, he would recognize the capital gain of $100,000. Assuming a 15% federal capital gains tax bracket (state and local taxes would be additional) the tax would be $15,000, leaving only $95,000 to reinvest. If reinvestment of the $95,000 earns 7% gross taxable income annually ($6,650) he would have $4,655 of net income available (assuming a 30% ordinary income tax rate). At Henry’s death, $95,000 will be available to fulfill his charitable bequest. Now consider the results if Henry creates a lifetime CRUT that pays him 7% of the trust value each year for life. Assume Henry contributes the $110,000 of XYZ stock to the CRUT. The trustee, concerned about lack of diversification in the trust portfolio, sells the XYZ stock and reinvests in a blended portfolio that earns 7% gross annually.9 The trust does not pay tax on the sale or on the income earned. Each year the CRUT distributes 7% of its assets ($7,700 in year 1) to Henry. The distribution is taxable to him under the tier system as a combination of ordinary income and capital gains (assume an effective rate of 25%) leaving him $5,775 of net income. At Henry’s death the remaining assets in the trust, $110,000, will be available to fulfill his charitable bequest. In addition to the income distributions, Henry will receive a charitable income tax deduction in the year the gift is made, equal to approximately 22% of the $110,000 donation, or $24,200.10 Assuming a 30% tax rate and that Henry’s AGI will enable him to use the full deduction, the deduction will generate tax savings of $7,260.

9 Both examples assume that the income distributions exactly match the amount earned on the principal. As a result, the principal is preserved for the charity. In reality, the earnings would vary from year to year. The timing of distributions affects the calculations as well. Here, the example assumes distributions are made on the last day of the year. 10 This example assumes a Section 7520 rate of 2.4%.

Page 3 of 21

Generally donors implement CRATs only when they are concerned about receiving a minimum payout regardless of the trust’s performance. This may occur where the donor has a need for a fixed income or in cases where the trust value will be substantially depleted over the income term because of the size of the income interest. Older individuals who want the stability of a fixed income and individuals who want to avoid annual valuations may also prefer the CRAT.

For example, Sophie, age 66, would like to earmark enough income to provide for $32,000 in annual gifts to her grandchildren for the rest of her life. She would also like to make a significant charitable contribution to the Mayo Foundation. Her $1,000,000 of TPS stock (basis $300,000) annually pays a gross 4% dividend ($40,000) or $34,000 after tax, assuming a 15% capital gains tax rate. She has enough income from other sources to provide for her needs and is willing to use the TPS stock alone to fulfill her goals. With the counsel of her tax and legal advisors, she decides to use the TPS stock to create a CRAT that will pay her $50,000 a year for life. Each year, Sophie receives $50,000 that results in $40,000 after-tax, assuming a 20% effective tax rate (assume distributions include ordinary income and capital gains). The trust principal, growing at an assumed 7% gross rate, is projected to increase slightly each year since it is assumed to earn more than it distributes to Sophie. In addition to income distributions that Sophie uses to fund gifts to her heirs, she will receive a charitable income tax deduction in the year of the gift equal to approximately $373,000, representing 37% of the initial contribution.11 Based on her tax rate, the deduction is worth approximately $130,550, though it may have to be carried forward for a number of years. A CRT may buy life insurance or may be the recipient of a gift of life insurance.12 Obviously, the advantage of life insurance relates to the value of the trust after the insured’s death. There are two situations where having an increased death benefit may

11 This example assumes a Section 7520 rate of 3.0%. 12 See PLR 199915045 in which the grantor proposed a CRUT, payable to the grantor’s daughter, to which the grantor intended to give a paid up permanent life insurance policy. The IRS held that neither the existence nor exercise of the trustee's power to pay the annual premiums on the insurance policy would disqualify the trust as a CRUT. The Service also held that the grantor would be entitled to an income and gift tax charitable contribution deductions for the present fair market value of the remainder interest in the insurance policy.

4. 3.

1.

Henry

CRUT

7% to Henry for life; Remainder to

Goodwill Industries (charity)

7% in cash annually

($7,700 year 1)

Original contribution in year 1 of $110,000 in

XYZ stock

$24,200 income tax deduction

Remainder of trust passes to charity at

Henry’s death

Sale of XYZ stock to a 3rd party for $110,000 in cash to be reinvested

2.

Page 4 of 21

be useful. First, where a charity will receive the trust value after the life of the insured-grantor, an insurance policy will provide an immediate increase in the value of the assets passing to the charity. Thus, while distributions to the grantor will be fixed (for a CRAT) or based upon trust values (for a CRUT), the death benefit will enable a significantly larger amount to pass to the charity.13 Second, where a non-charitable beneficiary will take over lifetime payments after the grantor’s death, the presence of a life insurance policy on the grantor will create a larger asset base from which the survivor may take income. Best used in the context of a CRUT, this second situation may work as follows:

Chandra creates a CRUT in which she will retain a 6% unitrust interest for her life. After her death, her husband, Ganesh, if living, will receive the 6% payments for his life. Chandra gives cash and appreciated stock to the CRUT, as well as a life insurance policy on her life with a fair market value of $50,000 and a death benefit of $200,000. At Chandra’s death, the CRUT’s value increases by $150,000 enabling a larger unitrust interest to be paid to Ganesh for his life.

Using life insurance in a CRT, however, is not without its issues. Most forms of CRT require a payment to the grantor regardless of the investment performance of the trust. Thus, a trust holding life insurance may have to either surrender the policy or give the grantor a partial ownership of the policy in satisfaction of that year’s payout obligation.14 The exception to this rule is the net-income charitable remainder unitrust (NICRUT).15 Its terms provide that the trustee need not meet the designated payout for a year in which the trust’s income is insufficient. Instead the NICRUT need only pay the grantor the net income from the trust. Of course, in years with no income the grantor will be receiving less than his or her designated share. A CRT trustee might not want to own life insurance from an investment perspective. Trustees have a fiduciary duty to manage the trust’s assets for the benefit of both the income beneficiary and the remainderman. Consider the case where the trust’s life insurance policy will lapse without the payment of future premiums: the lifetime beneficiary’s interest could be hurt by the payment of premiums on a policy that will not benefit him, while the remainder beneficiary will be disadvantaged if the policy lapses.16 Trustees need to carefully evaluate the place that the insurance has in the trust’s overall investment approach, balancing both party’s needs. Donors may not want to make a gift of a policy to a CRT when they learn that the tax deduction for ordinary income property, such as life insurance, is limited to its basis. As indicated earlier,

13 For example, the CRUT may require a 6% annual distribution to the grantor, based on the fair market value of the policy and other trust assets. However, the value passing to charity will be based on the face amount of death benefit and other trust assets. Since the death benefit will be higher than the lifetime fair market value, the charity will get some value from which the unitrust interest was never paid (i.e., on the death benefit in excess of the policy fair market value). 14 A similar problem occurs where the trust holds illiquid property which is not income producing, such as undeveloped real estate. 15 See IRC §664(d)(3). 16 Clients should evaluate the needs of the income beneficiary before establishing and funding the trust. A CRAT, for example, may be appropriate where the trust will own life insurance since the policy value will not affect the lifetime beneficiary’s payout amount.

Page 5 of 21

most grantors fund CRTs with appreciated capital property since its deduction base is the fair market value of the property, not its cost basis. Keep in mind that the existence of a policy loan will further reduce the value for deduction purposes. Remember that a gift of debt-encumbered property, such as a life insurance policy with a policy loan, may result in an act of self-dealing, since the transaction – though structured as a gift – must be treated as a part-sale. The trustee and the donor are disqualified persons who may not enter into such transactions. Even where the donor remains liable for the loan, an act of self-dealing may occur. Further, when a CRT owns a policy with a loan, any income earned by the trust might be considered debt-financed income, resulting in the taxation of trust income.17 As a result of these considerations, advisors should only recommend placing life insurance in a CRT after carefully analyzing all of the economic and fiduciary issues.

Although a CRT may buy a deferred annuity contract, the practice is uncommon because the income tax deferral of the annuity is already available by virtue of the charitable trust’s tax-exempt status.18 The IRS ruled in PLR 9009047 that although a CRT’s ownership of a deferred annuity would not jeopardize the trust’s status as a CRT, the annuity itself would lose its tax-exempt status since the trust owner was not a natural person. Of course, since the trust does not pay income tax, the concern is not as great as it would be for other non-natural person annuity owners. The trustee of a net-income make-up charitable remainder unitrust (NIMCRUT) may find the use of a deferred annuity appropriate since it can provide flexibility in distributions – i.e., the annuity’s distribution options can mirror the NIMCRUT trustee’s desire to delay distributions until a future date.19 The appropriateness of using an annuity in a CRT will depend, in part, on how the contract complements the trust’s other assets (if any), keeping in mind the fiduciary’s prudent investor duty. In this respect, for example, the trustee might weigh the guarantees available in commercial annuities against the surrender fees and other costs of the annuity. The trustee might also consider how the ordinary income realized (but not recognized by the CRT) will affect the net after-tax distribution available to the beneficiaries. That is, although the CRT will not pay tax on the annuity gains, the tier-taxation rules applicable to CRT distributions cause the income beneficiary to bear the tax as distributions are made.

17 See IRC §514(c)(2). A policy with a loan may cause acquisition indebtedness even where the donor agrees to continue paying the loan. 18 The IRS ruled in TAM 9825001 that a CRUT’s purchase of a deferred annuity in which the trust’s beneficiaries were named the annuitants did not disqualify the trust or create an act of self-dealing. TAM 9825001 (6/18/1998). The trust in the TAM was a NICRUT. It bought single life deferred annuities on the grantor and his wife, naming itself owner and beneficiary. The IRS simply stated that the purchase did not disqualify the trust. The finding related to self-dealing was more roundabout, but in part hinged on the fact that the annuitant and CRT beneficiary did not exert any undue influence or control over the trustee. Although the trust’s purchase of the annuity helped accomplish the beneficiary’s retirement goals, the IRS found that “…the Trustee merely took into consideration the particular financial needs of [the beneficiary] before reinvesting [in an annuity] the proceeds from the sale of the trust assets.” 19 Although the annuity gains create income for the trust each year – albeit income that is not taxed – for income tax purposes, the gains do not automatically create income for trust accounting purposes under state law. As a result, the trustee of a NICRUT or NIMCRUT may continue to accumulate gains instead of distributing them.

Page 6 of 21

Clients who may consider the use of a deferred annuity contract in conjunction with a CRT should be aware that a gift of a deferred annuity contract issued after April 22, 1987 is an income tax recognition event. The donor is treated as having received the cash surrender value in the contract, and will be taxed on that amount, less his or her basis.20 In the charitable context this treatment may be partially or fully offset, since although the gain must be recognized the donor does not have to reduce the value of the contract when calculating the charitable deduction.21 CRT as alternative to Stretch IRA Charitable remainder trusts can be used as an alternative to the common practice of stretching inherited IRA distributions over a beneficiary’s life expectancy under the Code’s required minimum distribution (RMD) rules. A CRT is named as the beneficiary of the IRA. The CRT trustee takes the required RMDs from the IRA, but only distributes a portion of the RMD to the non-charitable income beneficiary. Where the surviving spouse is relatively older, this design will result in a longer, more even income distribution profile than would occur if the beneficiary received distributions directly from the IRA account. The CRT design also allows for the decedent to limit the payout to the surviving spouse in a way not possible if either the spouse or a QTIP trust for the spouse’s benefit were named beneficiary. This may be attractive in situations where the decedent would like to ensure that some portion of the account be preserved for children (e.g., as in a second marriage with children from first marriage).

Mavis owns a $300,000 IRA. She is married to Rich, age 72, and has a child Sarah, age 42, from a prior marriage. Mavis would like the IRA to benefit Rich for his life and then benefit Sarah. She considers three options for her beneficiary designation. Assume that Mavis does not have an estate tax concern. [1] Rich named directly. This option will provide a good result from an RMD perspective, since Rich will be able to execute a spousal rollover. This will allow for the use of the Uniform Life Table to determine his RMDs. For example, if he is age 75 at the time of Mavis’ death, and 76 in his first distribution year, he must distribute about 4.5% (based on 22.0 life expectancy divisor) of the account. This percentage will increase as he ages, but will ensure that some amount will pass at his death, since the percentage is recalculated annually based on his actual age each year. This plan may not appeal to Mavis, however, since Rich will be able to name a new beneficiary, and may exclude Sarah from future distributions. [2] Conduit testamentary trust for Rich and then Sarah. The trustee will take RMDs from the IRA as required. From the trust Rich will receive a specified percentage or amount as Mavis has determined; the balance will be accumulated for Sarah. This plan satisfies Mavis’ concern about preserving some of the account, but results in faster distributions from the IRA than under the prior option. Since it is an inherited IRA, the oldest beneficiary (Rich) will be the measuring life for distribution calculations. If Rich is 76 in the first distribution year, the trust must take out 7.8% of the account (based on 12.7 life expectancy divisor), and an increasing percentage each year until the account

20 See IRC §72(e)(4)(C). 21 See Treas. Reg. §1.170A-4(a)

Page 7 of 21

is liquidated in the 13th year.22 Under this plan the IRA’s advantage of deferred tax on growth will not last as long as in the first option. Further, the trust (a non-grantor trust) will be taxed at trust rates on any income not distributed to Rich. [3] Testamentary CRUT for Rich then Sarah. A CRUT created under Mavis’ revocable trust will liquidate the account in the year of Mavis’ death. It will make distributions of 5% of trust value to Rich for his life, then to Sarah for her life.23 The remaining assets will pass to a local church (designated by Mavis) at Sarah’s death. Although the IRA is liquidated in the year of Mavis’ death, the CRUT will not pay tax on the IRA distribution. In effect, the tax deferral benefit will continue to the extent that assets remain in the trust.24 This alternative will entail a loss of the asset to the family at Sarah’s death, however, since the trust remainder must go to the Church.

Note that this IRA to CRT technique is only possible where the CRT beneficiaries are old enough that the trust meets the IRS requirements for a minimum 10% amount that is expected to pass to the charitable remainder beneficiary. In practical terms, this means that one beneficiary must be at least age 70, and the other at least 40 for the CRT to pass the charitable threshold. If the IRA stretch provisions are ever repealed, (e.g., if the law changes to require five-year payouts of inherited IRAs) then many taxpayers will become interested in the designation of charities and CRTs as beneficiaries of IRA and qualified plan accounts. 3. Charitable Lead Trust Like the CRT, the Charitable Lead Trust (or CLT) is an irrevocable trust to which the donor makes gifts that will benefit both a term (or life) beneficiary and a remainder beneficiary. However, in a charitable lead trust the charity is the term beneficiary and the donor’s heirs are the remainder beneficiaries. As with CRTs, CLTs may be established during life (with gift tax implications) or at death (with estate tax implications), and may be formed with an annuity or unitrust payout formula. The charitable lead trust offers unique estate planning advantages. Since the assets will ultimately pass to a non-charitable beneficiary (e.g., the donor’s heirs), the CLT can facilitate a charitable gift without depriving family members of the ultimate ownership of the donor's accumulated wealth. Thus, although the heirs will have to wait until after the charitable lead term to receive the trust assets, some portion of those assets will be returned to the family. In a sense, the charity will merely receive the use of the trust assets for a period of time, while the heirs will hopefully receive the principal and any growth beyond the charitable distribution amount.

22 Even if Sarah survives Rich, she will be locked into the distribution formula under which the trust was taking distributions while he was alive. This means that the trust must liquidate the IRA by the end of the 13th distribution year. 23 Assuming a 2.4% 7520 rate, if Rich is 75 and Sarah 45 when the CRUT comes into being, its payout rate could be as high as 7.6%. 24 The first $300,000 in trust distributions will be taxed as ordinary income. Distributions will thereafter be taxed under the tiered system and will depend on how the trust’s assets have been invested.

Page 8 of 21

The principal tax advantages to the donor may be found in the reduced value for transfer tax purposes of the heirs’ interest and the increased charitable gift or estate tax deduction available for the value of the charitable beneficiary’s interest. Only the present value of the interest passing to the non-charitable beneficiaries will be a taxable gift in the year the donor creates the trust. In some cases, the value of the charitable interest (and corresponding transfer tax deduction) will significantly reduce the gift or estate tax value of the amount of the non-charitable interest, even to zero value.25 As a result, the most frequent use of CLTs occurs in very large estates where the estate tax exemption amount will not significantly shelter the client’s gross estate and where the non-charitable beneficiary can afford to wait for his or her interest.26 For example, Joe dies in 2006 with a $15m estate. Included in his estate is $3m in commercial real estate. Joe’s revocable trust provides that at his death the real estate be placed in a CLT benefiting the Humane Society of Cleveland (HSC) for 15 years. The trust will pay HSC $150,000 a year for the 15-year term, after which time the assets will pass to a trust benefiting his heirs. If the trust property earns (and/or grows) at 9%, his heirs can expect to receive just over $6.5m. For estate tax purposes, using an assumed Section 7520 rate of 1.2%, Joe’s executor may deduct the value of HSC’s annuity interest ($2,047,935). As with the CRT, the charitable lead trust is one of the more sophisticated methods of charitable giving. Clients must work with an attorney when establishing a CLT as part of their estate plan. In particular, clients should be aware of the income tax consequences of lead trusts. A lifetime CLT presents the grantor/donor with a choice as to how to be taxed for income tax purposes. In order to receive an up-front income tax deduction for the actuarial value passing to charity, the trust must be taxed as a grantor trust, meaning that future gains and income earned by the trust will be taxed to the grantor even though the money will stay in the trust or be distributed to charity.27 Many grantors instead forgo the deduction and establish CLTs that are taxed as

25 The interest passing to the non-charitable beneficiary will not qualify for the IRC §2503(b) gift tax annual exclusion since the benefit is not a present interest. 26 Famously, the estate plan of Jacqueline Kennedy Onassis proposed use of a CLT to help reduce the value of her taxable estate. 27 IRC §170(f)(2)(B) provides in part for a recapture of the deduction in the year in which the CLT loses grantor trust status: “If the donor ceases to be treated as the owner of such an interest for purposes of applying section

Remainder after 15 years; estimated to be about $6.5m

if the trust earns 9% (net) per year

$150k annually for 15 years

Estate tax deduction of $2,047,935

CLT $150k to HSC for 15 years;

Remainder to Trust for Joe’s heirs

Joe’s Revocable

Trust

Contribution of $3m of real estate to CLT

Humane Society (charity)

Trust for Joe’s heirs

1. 2.

3.

Page 9 of 21

stand-alone entities for income tax purposes. In this stand-alone form the grantor is not taxed on trust income. The trust reports income under the trust income tax system, receiving a tax deduction for amounts distributed to charity each year. Lifetime CLTs should be compared to retaining the assets and making annual or systematic contributions to charity. The CLT allows for the possibility that the heirs will receive more than the amount reportable for gift tax purposes. That is, if the trust earns more than the assumed rate (i.e., the 7520 rate), the heirs will be better off. However, use of the CLT has administrative and legal costs, and requires the donor to irrevocably part with the asset. Further, the heirs will have to wait to receive any benefit. Testamentary CLTs should be compared to a direct bequest to heirs of a smaller amount than that set aside in the CLT. For example, instead of giving $1m to a CLT of which the heirs are expected to receive 10%, a testator could simply bequeath $100,000 to the heirs directly (and $900,000 to the charity). For estate tax purposes the CLT option and the direct bequest are the same. However, the CLT option has the potential to pass a greater value over time if the trust can earn more than the 7520 rate. Clients should evaluate the beneficiary’s immediate use of the money, the CLT’s costs, and the potential estate tax savings available through the CLT. 4. Charitable Gift Annuity A charitable gift annuity is an arrangement between a charity and a donor in which the donor transfers an asset to the charity in return for a stream of payments (i.e., the annuity) typically paid over the donor’s life. In effect, since the annuity payments must be actuarially less than the value of the property transferred, the transaction is part gift and part sale.28 A charitable gift annuity resembles a CRT in some respects: it represents an individual arrangement with the charity (unlike a pooled income fund, for example); it allows for a lifetime income stream; and it has a fractional charitable gift element (and a corresponding tax deduction). A deferred charitable gift annuity will result in payments that may be delayed until a future time, just as in certain CRUTs. Besides the difference in underlying legal form, the charitable gift annuity also differs from the CRT in that the transaction partially represents a sale on which the donor will recognize some gain if transferring appreciated property. A portion of each annuity payment received by the donor will be treated as capital gain. Lastly, where a CRT’s payment obligation is backed solely by trust assets, the charity’s obligation in a charitable gift annuity is backed by the assets of the charity. The benefits of a charitable gift annuity to the donor include receipt of a fixed income for his or her life or for the joint lives of the donor and another individual, freedom from management responsibility and federal estate tax savings (since the annuity terminates at the death of the annuitant). These benefits should be balanced against the fixed nature of the arrangement (i.e.,

671, at the time the donor ceases to be so treated, the donor shall for purposes of this chapter be considered as having received an amount of income equal to the amount of any deduction he received under this section for the contribution…” 28 Charitable gift annuities are specifically exempt from the debt-financed property and unrelated business income rules that would otherwise impair the ability of a charity to engage in this type of transaction. See e.g., PLRs 9743054 and 2000449033. The charitable annuity rate usually conforms to rate schedules published by the American Council on Gift Annuities (ACGA). The ACGA rates pay substantially less than a similarly funded commercial annuity, allowing for a built-in return for the charity. See www.acga-web.org.

Page 10 of 21

the inability to change the investment strategy or distribution amounts) and the risk that the charity becomes insolvent.

For example, Nigel and his wife, Rose, both age 60, would like to make a donation of their $1m vacation home to the John F. Kennedy Center for the Performing Arts, but would feel more comfortable retaining some income from the property than simply giving it away outright. Nigel donates the property to the Center in exchange for a charitable gift annuity for his and Rose’s joint lives. At the time of the gift, their basis in the property is $600,000. Based on their ages and the recommended ACGA annuity rate, the Center will pay them $54,000 annually for their joint and survivor lives. Their joint life expectancy is 29.6 years. Their charitable income tax deduction, based on the fair market value of the property less the value of the annuity, is $255,766. For the first 29 years, $28,856 of each $54,000 payment will be ordinary income. The remaining $25,144 will be split between capital gains and return of basis. Nigel must allocate his basis both to the charitable portion (approximately 25.57%) and the annuity portion (approximately 74.42%) of the transferred asset, meaning that he will recover only $446,540 of the basis (74.42% x $600,000) over his life expectancy (29.6). Thus, $15,085 of each payment will be return of basis while the remaining $10,059 (equal to $25,144 less basis return of $15,085) will be capital gains. After 29 years – i.e., if Nigel and/or his wife reach life expectancy – the entire $54,000 will thereafter be taxable as ordinary income.

As with other split-interest charitable giving techniques, a charitable gift annuity is appropriate where the donor would like to retain an income stream and benefit a charitable organization. Where an income stream is not needed, a direct gift may be preferable. 5. Wealth Replacement Trust Many prospective donors hesitate to implement a charitable technique because the assets given to charity will not pass to the donor’s heirs. In most cases the use of a charitable technique will not benefit the donor’s family more than a direct transfer to them, notwithstanding the significant estate or gift tax that may apply to such a transfer. For this reason, clients without strong charitable desires will not often implement a charitable technique. However, the use of life insurance along with a Wealth Replacement Trust (WRT) can help to mitigate this concern and help those with some charitable inclination to proceed, knowing that their heirs will receive other assets to replace those passing to charity. While the form may differ, in most cases the client creates the irrevocable WRT during life and funds it with annual exclusion or lifetime exemption gifts. The trustee uses the income and/or principal of the trust property to pay premiums on a life insurance policy on the grantor(s).29 The face amount of the insurance will depend on the premium available, the insured’s needs and insurability, but will generally attempt to equal the amount of assets in the insured’s estate that

29 The WRT is simply an irrevocable life insurance trust (ILIT) whose purpose relates primarily to wealth replacement instead of estate liquidity. In many cases it would be appropriate to refer to the ILIT as the WRT since the designations do not distinguish them by legal operation but by goal.

Page 11 of 21

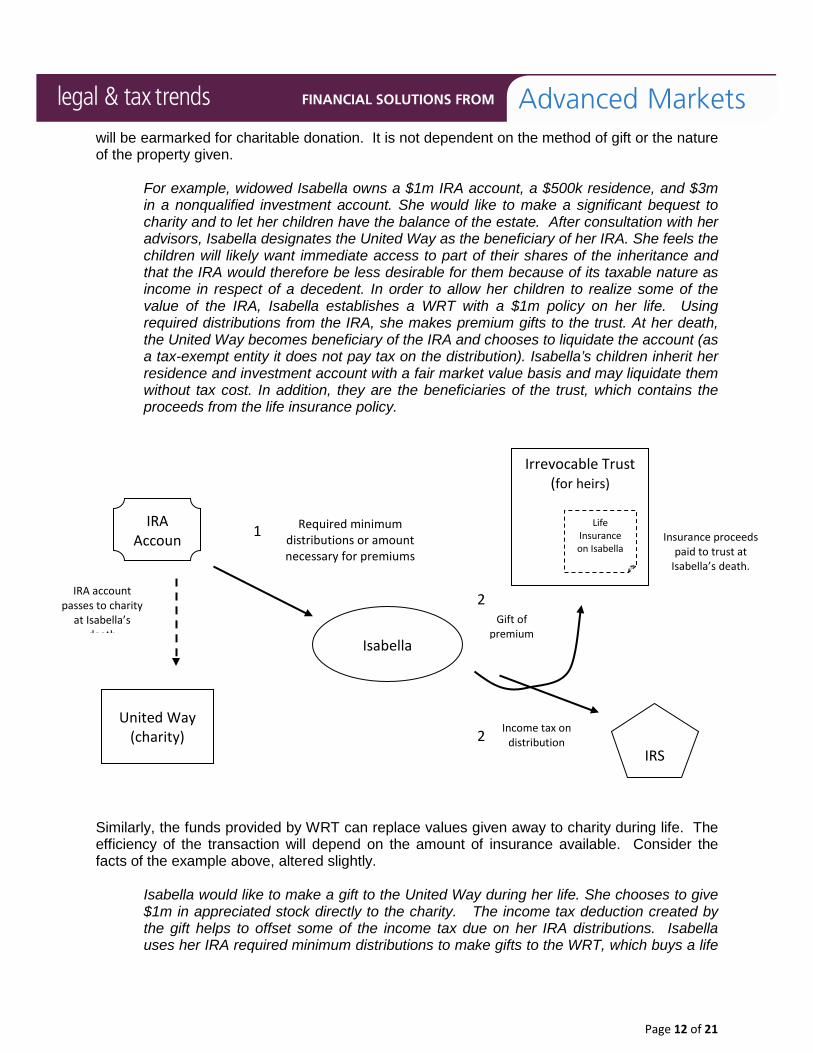

will be earmarked for charitable donation. It is not dependent on the method of gift or the nature of the property given.

For example, widowed Isabella owns a $1m IRA account, a $500k residence, and $3m in a nonqualified investment account. She would like to make a significant bequest to charity and to let her children have the balance of the estate. After consultation with her advisors, Isabella designates the United Way as the beneficiary of her IRA. She feels the children will likely want immediate access to part of their shares of the inheritance and that the IRA would therefore be less desirable for them because of its taxable nature as income in respect of a decedent. In order to allow her children to realize some of the value of the IRA, Isabella establishes a WRT with a $1m policy on her life. Using required distributions from the IRA, she makes premium gifts to the trust. At her death, the United Way becomes beneficiary of the IRA and chooses to liquidate the account (as a tax-exempt entity it does not pay tax on the distribution). Isabella’s children inherit her residence and investment account with a fair market value basis and may liquidate them without tax cost. In addition, they are the beneficiaries of the trust, which contains the proceeds from the life insurance policy.

Similarly, the funds provided by WRT can replace values given away to charity during life. The efficiency of the transaction will depend on the amount of insurance available. Consider the facts of the example above, altered slightly.

Isabella would like to make a gift to the United Way during her life. She chooses to give $1m in appreciated stock directly to the charity. The income tax deduction created by the gift helps to offset some of the income tax due on her IRA distributions. Isabella uses her IRA required minimum distributions to make gifts to the WRT, which buys a life

Required minimum distributions or amount necessary for premiums

IRA Accoun

Isabella

United Way (charity)

IRS

Irrevocable Trust (for heirs)

Life Insurance on Isabella

Income tax on distribution

Gift of premium

1

2 3

2

IRA account passes to charity

at Isabella’s death

Insurance proceeds paid to trust at

Isabella’s death.

Page 12 of 21

insurance policy on her life. At her death, her children receive distributions of cash from the WRT and choose to liquidate the residence. Under the stretch IRA principle, they keep the IRA balance intact, taking only required distributions and maximizing its tax-deferral capability.

The principle of replacement through use of lifetime income also applies to gifts made in the form of a CRT or charitable gift annuity. In each of these cases the donor will be receiving an income stream for a period of time. The goal of the WRT here will be to acquire a life insurance policy with a death benefit as near as possible to the amount transferred to the trust. The key to the success of this technique will be the amount and duration of after-tax income available from the trust relative to the premium required to replace the asset. Also important will be the tax leverage obtained from the deductible portion of the gift.

For example, Warren (65) and Anne (65) are considering a donation to charity of all or a part of $1m of appreciated real estate ($600k basis) through either a lifetime CRUT or a direct bequest. The property is assumed to appreciate at 8% per year (to $3m in 15 years and to $6.3m in 25 years at life expectancy) but produces no income. They expect to be in a 40% estate tax bracket after use of any exemptions or credits. Under the direct bequest scenario (assuming death in the 25th year) their estate will likely liquidate the property to accomplish the $1m bequest. After deducting the charitable bequest amount ($1m), the estate tax attributable to the $5.3 remaining sale proceeds will be about $2.1m, leaving a potential bequest to their children of approximately $3.2m. Under the alternative scenario, they will create a 15-year CRUT, retaining a 5% unitrust interest. Using a 7520 rate of 3.0%, the present value of the charitable remainder is about 47%, or $468,711. Projections indicate the trust will provide distributions each year beginning at $50,000 and increasing to $73,000 over the trust term. If the CRUT sells the property and if the CRUT is able to invest in assets producing income of 5% and growth of 3%, the CRUT is expected to have a remainder value of just over $1,500,000 in the final (15th) year. To provide for the children, Warren and Anne consider paying for a joint survivorship life insurance policy held by a WRT. For premium gifts, they will have available the after-tax CRUT distribution amount, but only for 15 years.30 At an assumed blended tax rate of 30% (ordinary and capital gain) they should have annual after-tax distributions between $35,000 (the 1st year) and $51,000 (the 15th year). They may also consider the savings garnered from the income tax deduction. If used equally over 5 years, and assuming a 40% income tax rate, the $468,711 charitable deduction would save them about $37,500 per year. In summary, for years 1-5, they should be able to support premiums ranging from $72,500 (net income of $35k and tax savings of $37,500) to $75,500. For the remaining 10 years, the net CRUT distributions will allow for premiums from $40,000 to $51,000.

30 These distributions will be taxable under the tier rules, which first send out ordinary income (if any), then capital gains, then tax-free income and finally return of basis. In this example, any ordinary income earned by the CRUT after reinvestment of the sale proceeds would be the first income distributed. If there were $50,000 of rental income the first year, for example, the entire $50,000 would be taxable to them at ordinary income rates. Should the trust’s annual distribution exceed the ordinary income amount, t clients would begin to receive a portion of the $400k of gain realized from the sale of the donated property.

Page 13 of 21

From the heirs’ perspective, for the CRUT/WRT plan to exceed the direct bequest scenario, the WRT must be able to buy a life insurance policy that will provide more than $3.2m of death benefit using only the aforementioned premium stream (approximately $880,000 aggregated). From the charity’s perspective, the CRUT scenario will be preferable since the charity will receive more money ($1.5 vs. $1m) and will likely receive it sooner (after 15 years instead of at life expectancy).

The clients will need to model both the CRT and the life insurance policy illustration to decide which scenario best accomplishes their goals. In doing so, they should offset the potential inheritance loss faced by the heirs under the CRUT alternative against both the potential increased income stream and the charity’s earlier acquisition of the donation.

The wealth replacement trust functions differently in the context of a charitable lead trust. The CLT will ultimately provide a benefit to the grantor’s heirs, so the WRT will be used to provide interim income to the client’s heirs between the time that the asset is contributed to the CLT and the termination of the charitable lead term.

For example, Berina’s advisors recommend that she establish a testamentary CLT to help reduce the impact of estate taxes at her death. She amends her revocable trust to provide for a contribution of $4m to a ten-year CLT that will pay to the charity America’s Second Harvest an annuity of $260,000 per year. At an assumed 7520 rate of 3.0%, Berina expects a charitable estate tax deduction of approximately $2,217,000 for the value of the charitable income portion of the contribution. In order to provide her heirs with access to some of the money that will pass to charity, she creates a lifetime WRT to hold a $1m death benefit life insurance policy on her life. The policy death proceeds will

Irrevocable Trust (for heirs)

Joint Life Policy on Warren &

Anne

United Way (charity)

Warren &

Anne

Heirs Heirs

Income tax deduction of $472,000, used over

5 years

Remainder of trust after 15 years.

Projected to be $1.5m

5% Annual distributions for 15 years

Gifts of net distribution

from CRUT & value of tax deduction

Policy death benefit to heirs after second death

1.

CRUT 5% distribution

for 15 years

1. 2.

3.

4.

Page 14 of 21

allow the trustee of the WRT to make distributions in the ten years following her death during which the heirs will not be able to access the CLT funds. At the end of ten years, assuming a CLT growth rate of 8%, Berina expects her heirs to receive approximately $4.8m.

A non-grantor irrevocable gift trust may also be used for charitable donors concerned about charitable income tax deduction limitations. In this scenario, a non-grantor irrevocable trust will divert some of its income to a charitable beneficiary. For example, a donor gives an income-producing asset to the trust, which will distribute income annually to a charitable organization. It compares favorably (with respect to Net Investment Income Tax (NIIT)) to making outright gifts of income from a personally owned asset, because of the manner in which the trust is allowed to take its income tax deductions. The Form 1041 Trust Income Tax Return places charitable deductions “above-the-line,” that is, not subject to AGI limitations. Compare this to reporting for income from a personal asset (including income by grantor trusts) where charitable gifts are reported on the 1040 Schedule A. Schedule A “below-the-line” deductions are subject to AGI percentage limits (50/30/20%) based on the type of property and the type of charitable donee. For some very high income taxpayers, the phase-out of itemized deductions may also impair the tax benefit of a personal charitable gift. A trust’s charitable deductions are not similarly reduced by any itemization phase-out. The primary drawback of this technique is the loss of direct ownership and control of the asset, although here the trustee may have the discretion to direct income to a non-charitable beneficiary. Donors should also consider the inefficiency from a gift tax perspective of using annual exclusion or exemption protection to gift assets that will in part go to charity. 6. Charity Owned Income-Producing Asset For clients concerned with the 3.8% NIIT but also interested in charitable giving, a gift of income-producing assets may be of interest. Here the donor makes a direct gift of income-producing property to a charitable entity (e.g., donor-advised fund) in lieu of annual gifts of the income produced by a personally owned asset. The shifting of income to the charity yields a tax advantage in that the charity will not be subject to NIIT, while the donor will be – even where the donor gives the investment income to a charity.

Married couple Maxim and Tatiana own $100,000 of Sochi Corp. stock, which produces $5,000 of qualified dividend income each year. Apart from this income they have AGI of $300,000. In 2015, they give the $5,000 to the local Russian Orthodox Church (a 501(c)(3) organization). On their Form 1040 for 2015, they will report the $5,000 of income and claim an itemized deduction of $5,000. Although the deduction will offset the income, the $5,000 this technique will still create NIIT for the couple since their AGI is over the $250,000 threshold. In this example, their NIIT from the Sochi stock is $190.

The small tax advantage (avoiding a 3.8% tax) may not itself be enough to tip the scales in favor of this irrevocable gift for all donors, but when coupled with a present charitable deduction of the property’s fair market value, will be attractive to some wealthy donors who intend to make systematic charitable gifts over an extended period of time.

Page 15 of 21

7. Use of Life Insurance in a Private Foundation The use of life insurance in a private foundation most often arises (i) as part of a compensation program for an executive or director, (ii) as part of the foundation’s investment strategy (whether because of a donor’s gift of a policy or an investment by the foundation), or (iii) for key person coverage on a particularly important officer or director. These applications can represent valid reasons for owning the policy, but not without careful examination. Life Insurance as Compensation Compensatory life insurance arrangements for executives of non-profit organizations usually entail either the financing of a nonqualified retirement benefit or the providing of life insurance protection under a split dollar agreement. The nonqualified benefit may be accomplished through a §457(f) plan. While the nonqualified retirement plan represents only an unfunded promise to pay the participant an amount at retirement, a foundation may choose to informally finance the benefit – accumulate assets for the future payment to be made – using a cash value life insurance policy. As with other investments made by the foundation, the foundation’s investment manager must evaluate the use of the policy for this purpose in the context of the foundation’s overall investment strategy.31 A compensatory split dollar arrangement differs from the prohibited (donative) split dollar arrangements discussed earlier. Here, the foundation may agree to provide as part of a director’s or officer’s compensation an insured benefit payable to the insured’s designated beneficiary. Under the split dollar arrangement, the foundation owns and pays the premium on a life insurance policy on the insured. The insured may name the beneficiary of a portion of the policy death benefit. The foundation will receive the balance. Under split dollar rules, the insured must treat the life insurance protection – the so-called economic benefit – as compensation and include the value of the coverage in his or her income.32 If he or she should die while the arrangement is in effect, and assuming that the economic benefit has been properly reported, his or her beneficiary will receive the designated portion of the proceeds income tax-free33. The compensatory element of this life insurance plan distinguishes it from the prohibited charitable split dollar arrangements. That is, the foundation is not engaged in a speculative renting out its tax-exempt status, but is receiving the services of the insured participant. Of course, the compensation must still be reasonable. The prohibition from self-dealing includes expenditures from foundation assets to provide personal protection to its directors, officers, or other disqualified persons unless the protection afforded is treated as compensation and is reasonable, keeping in mind the fiduciary’s duties and other forms of compensation provided.34

31 A complete analysis of the investment standards to be used is beyond the scope of the document. However, the fiduciary duty to protect the assets of the foundation includes the responsibility to pursue investment options through a reasonable and defensible plan. See e.g. §227 of Restatement of the Law Third: Trusts, Prudent Investor Rule (1992): “The trustee is under a duty to the beneficiaries to invest and manage the funds of the trust as a prudent investor would, in light of the purposes, terms, distribution requirements, and other circumstances of the trust.” 32 The IRS Table 2001 rates, or if available a carrier’s one year term rates, are used to compute the cost of coverage to be included in income. 33 Also, see IRC §101(j) for notice and consent requirements which must be met. 34 See Jerry J.MCCoy and Kathryn W. Miree, Family Foundation Handbook (2001).

Page 16 of 21

Life Insurance as an Investment Donors often give unmatured life insurance policies to foundations with the intent that the policy proceeds will help further the foundation’s particular charitable mission. As discussed earlier, such gifts may fit into the foundation’s investment plan and provide an opportunity for a gift or bequest substantially larger than the corresponding premiums alone. However, as with other investments made by the foundation, the foundation’s investment manager may not presume that the policy represents the best use of foundation assets.35 He or she should continually monitor the policy in light of the foundation’s investment objectives. Another consideration affecting the gift or purchase of life insurance by a foundation is whether the life insurance jeopardizes the carrying out of the charitable purposes of the private foundation. In Revenue Ruling 80-133, the IRS ruled that acceptance of a gift of a whole life policy with an outstanding loan represented a jeopardizing investment subject to an excise tax.36 The IRS found that despite a ten-year life expectancy for the insured, that the premiums and interest to be paid on the loan would exceed any benefit beginning in the eighth year. In comparison, in PLR 200232036, the IRS ruled that a private foundation would not be entering into a jeopardy investment if it owned, controlled and continued to pay premiums on an unencumbered life insurance policy insuring the life of its donor.37 As a condition of accepting and continuing the policy the foundation stipulated that the insured donor would make annual contributions sufficient to pay the required premiums. Another problem related to policy loans involves unrelated business taxable income (UBTI). Under IRC §511-514, non-profit entities, including foundations and qualified pension trusts, are subject to a tax on investment income derived from borrowed funds.38 While this rule most obviously targets direct loans from banks and individuals, it also applies to proceeds from policy loans. If a foundation takes out a policy loan, any proceeds not used to directly further the exempt purpose of the foundation but instead invested, will create a tax liability on the income earned. Given that a foundation will not be taxed on a similar investment if made with foundation assets (not loan proceeds), fiduciaries risk an obvious violation of its fiduciary duty to invest prudently.

35 This duty exists even where the donor has made clear that future gifts (equal to the policy’s premium due) may not be forthcoming if the foundation chooses to surrender the insurance policy. The prudent investor standards applicable to foundation management supersede any understanding communicated by the donor. 36 Rev. Rul. 80-133, 1980-1 CB 258. “Section 53.4944-1(a)(2)(i) of the Foundation Excise Tax Regulations provides that an investment shall be considered to jeopardize the carrying out of the exempt purposes of a private foundation if it is determined that the foundation managers, in making such investment, have failed to exercise ordinary business care and prudence, under the facts and circumstances prevailing at the time of making the investment, in providing for the long-term and short-term financial needs of the foundation to carry out its exempt purposes. In the exercise of the requisite standard of care and prudence the foundation managers may take into account the expected return on an investment and the need for diversification within the investment portfolio. The determination whether the investment of a particular amount jeopardizes the carrying out of the exempt purposes of a foundation shall be made on an investment by investment basis, in each case taking into account the foundation's portfolio as a whole.” 37 PLR 200232036 (May 17, 2002). This ruling involved the transfer of a convertible term policy against which a policy loan could not be made. Any loans made after conversion could only be made to the foundation. 38 The tax applies at the corporate tax rates under IRC §11.

Page 17 of 21

As mentioned earlier, the transfer of a policy with a loan by a disqualified person may be an act of self-dealing.39 A foundation should not accept a gift of policy with a loan from a disqualified person. Key Person Life Insurance Just as for-profit enterprises purchase key person life insurance policies to insure against the loss of an employee critical to the ongoing success of the business, so too may a private foundation choose to buy a key person policy to protect against the premature death of a director, manager, or employee whose loss would significantly impair the foundation’s capability. Insurance, for example, may provide the funds to allow the foundation to recruit and hire a new planned giving officer, lessening the loss the foundation might otherwise suffer if a suitable candidate could not be found quickly. Where a state’s insurable interest laws allow, a foundation may also insure a donor or donor/employee whose regular contributions had become an anticipated revenue source. Proceeds from a life insurance policy could be used to offset the missing gifts. CHOLI In response to the popularity of premium financing arrangements and a purported opportunity for a no-cost charitable contribution on behalf of the insured, a number of arrangements involving the temporary use of a charity’s insurable interest have surfaced. Although it comes in various forms, charitable owned life insurance (CHOLI) generally calls for an agreement between a charity, the insured and group of investors to buy a life insurance policy.40 In one form, the charity establishes a trust to which the investors contribute, or the investors establish a limited partnership with the charity as a residual beneficiary. The trust or partnership often acquires a life insurance policy on the insured. The funds contributed by the investors (or an immediate annuity bought with such funds) pay for the policy’s premiums and provide for a return to the investors. At the death of the insured “donor,” the trust or partnership receives the proceeds. The investors are repaid their investment; any funds remaining pass to the charity. In this form the insured is considered a “donor” insofar as his or her gift of insurability may ultimately benefit the charity. Another form has the investors lending money to an insured to buy life insurance on his or her life. The donor assigns a portion of the death benefit to the investor group and names the remainder to a charity. Under the lending agreement, after a two-year period, the insured can repay the loan, or can give the investors the policy in satisfaction of the loan. Insured “donors” may be offered, in effect, the ability to provide a death benefit to the charity at no up-front cost to them. A typical example would require the repayment to include accrued interest at a rate significantly higher than the corresponding applicable federal rate.41 As a result, few insureds

39 See Rev. Rul. 80-132. 40 Please note that CHOLI should not be confused with the outright ownership of a life insurance policy by a charity, a valid technique that is not tainted by the prospect of a non-charitable benefit. 41 Arrangements without a charitable component have been called alternatively Stranger Owned Life Insurance (SOLI), Investor Owned Life Insurance (IOLI), or nonrecourse premium financing. MetLife opposes the use of all such methods to acquire life insurance, as does at least one state insurance department. See also New York Insurance Department Letter Opinion (December 19, 2005), in which the Department concluded, in part, “…that the transaction presented involves the procurement of insurance solely as a speculative investment for the

Page 18 of 21

choose to repay the loan. In most cases after year two when an insured assigns full ownership to the investors, there is little, if any, benefit available to the charity. As with charitable split dollar, the CHOLI arrangement provides for a benefit to inure to a non-charitable person or entity while using the charity’s tax-exempt status to facilitate the transaction. The structures may differ amongst CHOLI proposals, but similar flaws underlie each: a group of investors pool their funds and gamble on and invest in the life of a stranger. A charity may get a portion of the death proceeds, but the investors get the bulk. From the insured’s point of view, the arrangement will only live up to its billing as “free” life insurance if the policy values exceed the principal and interest of the loan by the end of the second year – an unlikely scenario given the built-in policy mortality costs and the high rates of interest imposed under the loan agreement. MetLife does not support any of these arrangements and has been active in opposing changes to state insurable interest laws that would grant an insurable interest to unrelated third parties.42 These CHOLI arrangements essentially turn life insurance policies into an investment or a commodity, a purpose to which their tax-favored treatment was not intended. This manipulation of the insurable interest laws risks a loss of the special tax treatment that life insurance products have been afforded based on a much different public policy benefit. Further, misapplication of the life settlement guidelines, while obviously beneficial to the program’s investors, may result in Congressional action to prevent all such settlements, which in the long run hurt the ability of legitimate settlors to access death benefit values. In addition, some arrangements imply the use of underwriting arbitrage between the annuity provider and the life provider to get favorable rates from competing insurers. As an industry, such a practice would have a substantial negative impact on the underwriting risk assumptions necessary to conduct business. Finally, because all outstanding coverage is taken into account, a donor’s “gift” of his or her insurability can have a negative effect upon his or her ability to acquire future coverage for the funding of other needs.43 As a matter of policy, MetLife does not support any form of Investor Owned Life Insurance including “nonrecourse premium financing” in the non-charitable context where the parties intend to eventually transfer the policy to an investor. Even where a particular state’s insurable interest laws may otherwise permit a charity to buy insurance, if the facts developed in conjunction with a submitted application indicate that the policy applied for is to be used in an investor owned charitable giving scheme, the policy will not be issued.

ultimate benefit of a disinterested third party. Such activity … is contrary to long established public policy against ‘gaming’ through life insurance purchases.” 42 In response to these perceived abusive CHOLI arrangements, federal legislation has been proposed to curtail their use. In 2005 a proposed bill (S. 993), sponsored by Senators Grassley and Baucus, would have imposed a very substantial penalty on CHOLI investors in the form of an excise tax equal to the premium costs of acquiring life insurance policies under certain of these arrangements. Bush Administration budget proposals would have eliminated SOLI through the creation of an excise tax on the policy death benefit if the charity owned the insurance contract and then sold it to a private individual or another entity. 43 The June15, 2004, Volume 2, NO.11 edition of NAIFA’s “Frontline,” included the following statement on different forms of investor-driven life insurance arrangements. “NAIFA and AALU strongly oppose these efforts to erode the integrity of long-standing insurable interest principles, which were designed to ensure that life insurance is used by those with a relationship to the insured for the benefit of families, businesses, employees and charities.” These industry groups continue to oppose such transactions.

Page 19 of 21

8. Conclusion Life insurance can play an important role in the accomplishment of charitable goals, whether those goals anticipate lifetime giving or making charitable bequests and whether or not the donor is sensitive to the tax benefits charitable giving may afford. Clients, working with their tax and legal advisors, should take the time to carefully consider the consequences of each technique to ensure that the life insurance meets the client’s goals.

Page 20 of 21

Legal & Tax Trends is provided to you by a coordinated effort among the Advanced Markets consultants. The following individuals from the Advanced Markets Organization contribute to this publication: Thomas Barrett, Michele B. Collins, Kenneth Cymbal, John Donlon, Lori Epstein, Jeffrey Hollander, Jeffrey Jenei, and Barry Rabinovich. All comments or suggestions should be directed to Tom Barrett or John Donlon at [email protected]. The information contained in this document is not intended to (and cannot) be used by anyone to avoid IRS penalties. This document supports the promotion and marketing of insurance or other financial products and services. Clients should seek advice based on their particular circumstances from an independent tax advisor since any discussion of taxes is for general informational purposes only and does not purport to be complete or cover every situation. MetLife, its agents, and representatives may not give legal, tax or accounting advice and this document should not be construed as such. Clients should confer with their qualified legal, tax and accounting advisors as appropriate.

Metropolitan Life Insurance Company 200 Park Avenue

New York, NY 10166

L0715431348[exp0916][All States][DC]

Page 21 of 21