the north american automobile industrythe north american automobile industry ! kimhill...

TRANSCRIPT

The North American Automobile Industry

Kim Hill

Director, Sustainability and Economic Development Strategies Center for Automo;ve Research

Ann Arbor, Michigan

FTA Revenue Es;ma;ng Conference Hilton Springfield, Springfield, IL

October 7, 2013

The Center for Automotive Research conducts leading-edge research that impacts the future of the global automotive industry.

• Automo;ve industry contract research and service organiza;on

• CAR is a standalone Non-‐Profit 501(c)3 since 2003 • Based in Ann Arbor, MI – 30+ Employees • CAR forecasts industry trends, advises on public

policy, and sponsors mul;-‐stakeholder communica;on forums

CAR Research

CAR Research and Analysis includes industry impact, economics and forecas;ng:

• Manufacturing, Engineering and Technology

• Transporta;on Systems Analysis

• Industry & Labor Analysis Group

• Sustainability & Economic Development Strategies

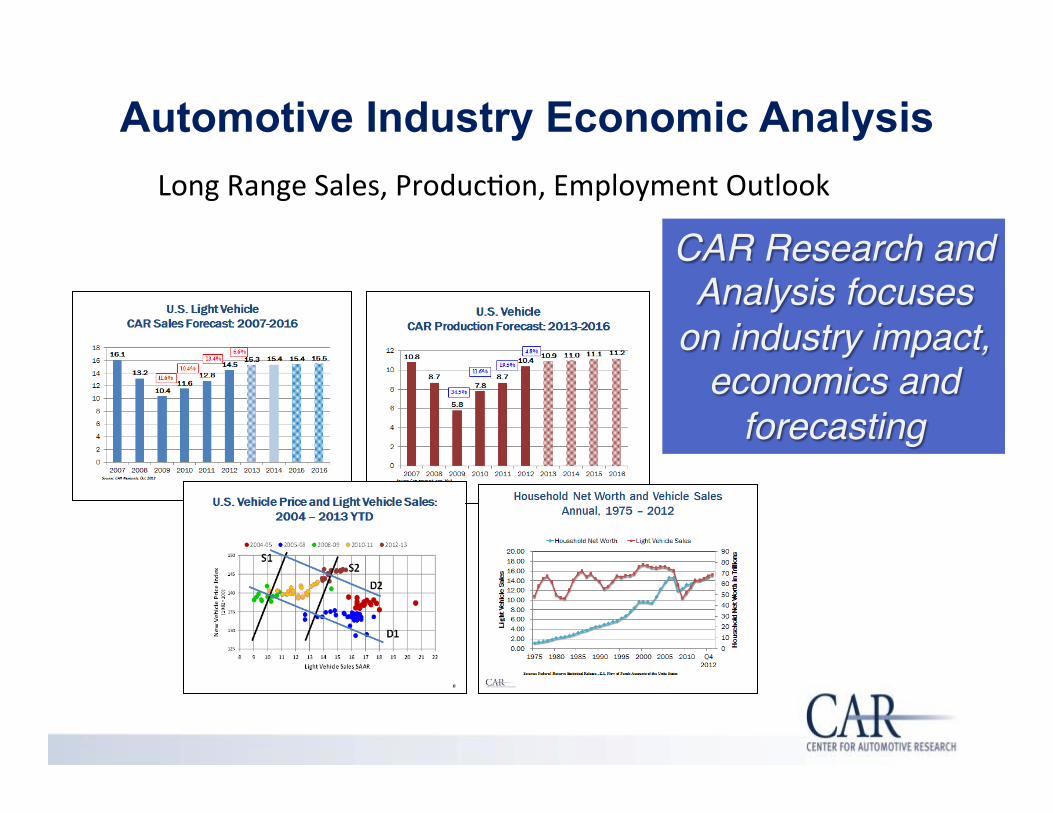

Automotive Industry Economic Analysis Long Range Sales, Produc;on, Employment Outlook

CAR Research and Analysis focuses

on industry impact, economics and

forecasting!

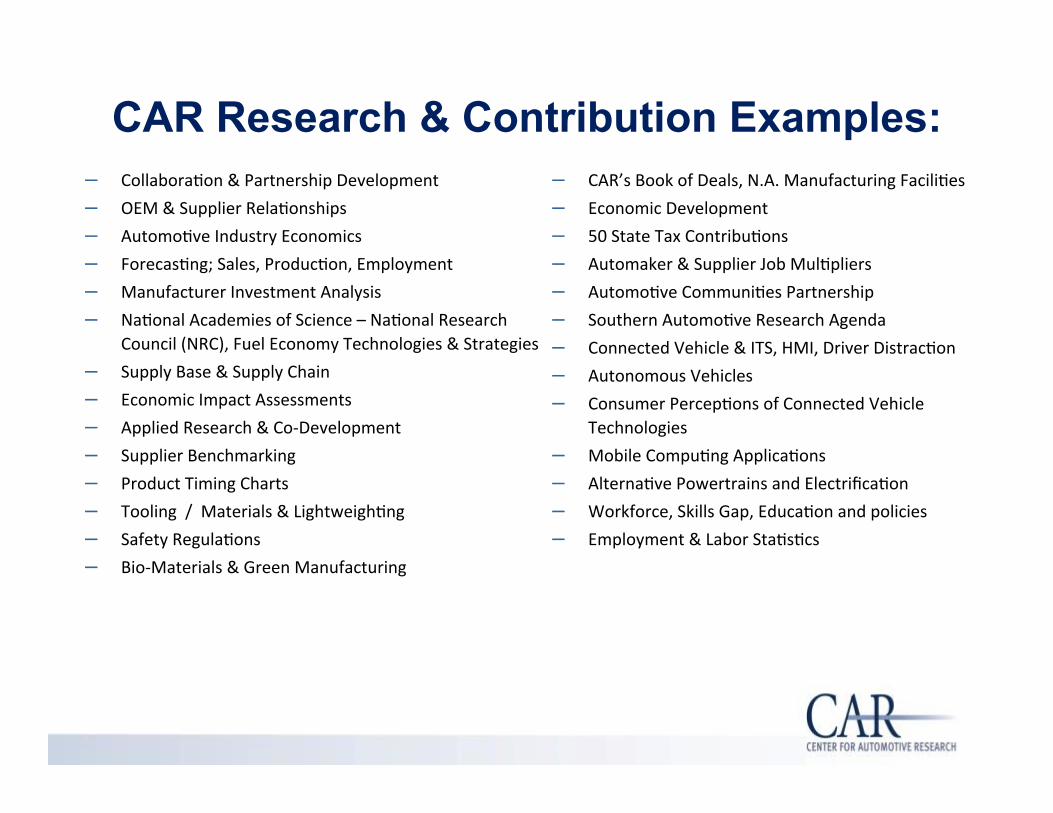

CAR Research & Contribution Examples: – Collabora;on & Partnership Development – OEM & Supplier Rela;onships – Automo;ve Industry Economics – Forecas;ng; Sales, Produc;on, Employment – Manufacturer Investment Analysis – Na;onal Academies of Science – Na;onal Research

Council (NRC), Fuel Economy Technologies & Strategies – Supply Base & Supply Chain – Economic Impact Assessments – Applied Research & Co-‐Development – Supplier Benchmarking – Product Timing Charts – Tooling / Materials & Lightweigh;ng – Safety Regula;ons – Bio-‐Materials & Green Manufacturing

– CAR’s Book of Deals, N.A. Manufacturing Facili;es – Economic Development – 50 State Tax Contribu;ons – Automaker & Supplier Job Mul;pliers – Automo;ve Communi;es Partnership – Southern Automo;ve Research Agenda – Connected Vehicle & ITS, HMI, Driver Distrac;on – Autonomous Vehicles – Consumer Percep;ons of Connected Vehicle

Technologies – Mobile Compu;ng Applica;ons – Alterna;ve Powertrains and Electrifica;on – Workforce, Skills Gap, Educa;on and policies – Employment & Labor Sta;s;cs

The Automotive Communities Partnership

• Widespread par;cipa;on from Ontario to Illinois, with diversity of par;cipants • 35 regional ED organiza;ons—

represen;ng 50 coun;es • 7 u;lity companies, 5 automobile

companies (DCX, Honda, GM, Ford, Toyota), numerous suppliers (ArvinMeritor, Dana, Denso, JCI, etc.)

• Specialized analyses • Objec;ve advice

• Best prac;ces • Forum for topical issues and ac;ons • Providing communi;es with much needed industry informa;on

• Collabora;ng on a common mission

Companies and communi;es working on enhancing the automo;ve endowment

2012 North American Automaker & Part Supplier Footprint

Source: Automotive News; CAR Research

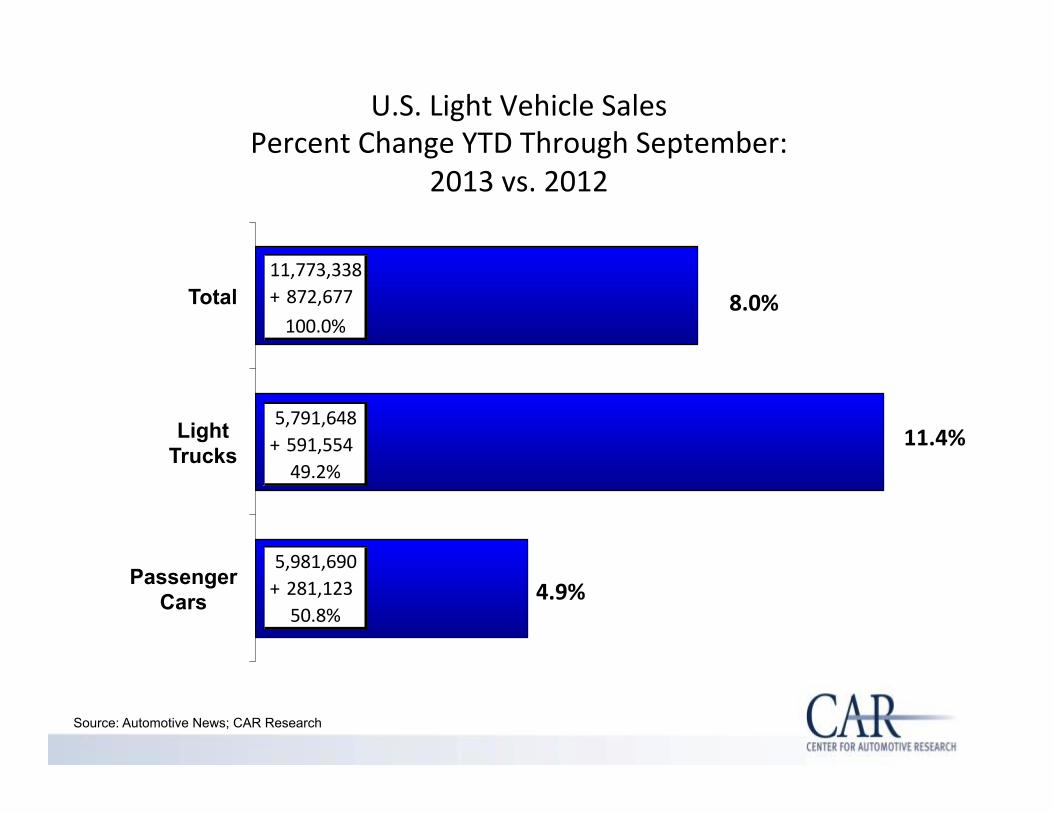

U.S. Light Vehicle Sales Percent Change YTD Through September:

2013 vs. 2012

4.9%

11.4%

8.0%

Passenger Cars

Light Trucks

Total + 872,67711,773,338

100.0%

+ 591,5545,791,648

49.2%

+ 281,1235,981,690

50.8%

0.6%

9.5%

9.6%

9.8%

10.3%

11.0%

12.8%

9.5%

0% 5% 10% 15%

Hyundai-Kia

Toyota

Honda

Nissan

GM

Fiat-Chrysler

Ford

TOTAL

Source: Automotive News; CAR Research

+ 924,391

+ 192,606

+ 104,202

+ 79,671

+ 172,794

+ 134,208

+ 105,357

+ 4,898871,496

8.2%

10,636,091

1,703,220

1,053,449

854,248

1,930,2648.0%

9.9%

16.0%

100%

1,213,986

11.4%

14.4%

18.1%1,533,722

0.6%

9.5%

9.6%

9.8%

10.3%

11.0%

12.8%

9.5%

0% 5% 10% 15%

Hyundai-Kia

Toyota

Honda

Nissan

GM

Fiat-Chrysler

Ford

TOTAL + 924,391

+ 192,606

+ 104,202

+ 79,671

+ 172,794

+ 134,208

+ 105,357

+ 4,898871,496

8.2%

10,636,091

1,703,220

1,053,449

854,248

1,930,2648.0%

9.9%

16.0%

100%

1,213,986

11.4%

14.4%

18.1%1,533,722

Percent Change in Sales of Light Vehicles Per OEM: YTD Through September: 2013 vs. 2012

Source: Automotive News; CAR Research

Units: 941,116

Units: 964,601

Units: 1,159,012

Units: 1,357,003

Units: 1,698,179

Units: 1,887,672

Units: 2,117,459

8.0%

8.2%

9.8%

11.5%

14.4%

16.0%

18.0%

Nissan

Hyundai-Kia

Honda

Fiat-Chrysler

Toyota

Ford

GM

U.S. Market Share: YTD September 2013

Big 7 Monthly U.S. Market Share 1999 – 2013 YTD (September)

Source: Automotive News; CAR Research

24.7%

16.0%

29.4%

18.0%

15.6%

11.5%

6.4%

9.8%

1.8%

8.2%

4.0%

8.0% 8.7%

14.4%

0%

5%

10%

15%

20%

25%

30%

35%

Percen

t of U

.S. M

arket S

ales

Year

Ford GM Chrysler Honda Hyundai-‐Kia Nissan Toyota

Source: Automotive News; CAR Research

U.S. Light Vehicle Monthly Sales and SAAR September 2011 – September 2013

1.1 1.0 1.0

1.2

0.9

1.1

1.4

1.2

1.3 1.3

1.2

1.3 1.2

1.1 1.1

1.4

1.0

1.2

1.5

1.3

1.4 1.4 1.3

1.5

1.1

13.1 13.3 13.6 13.6 14.2

15.1 14.4 14.4 13.8

14.1 14.1 14.5 14.9 14.3

15.6 15.4 15.2 15.3

15.3 15.2

15.5

15.9 15.8

16.1

15.3

0

2

4

6

8

10

12

14

16

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8 Se

p-11

O

ct-1

1 N

ov-1

1 D

ec-1

1 Ja

n-12

Fe

b-12

M

ar-1

2 A

pr-1

2 M

ay-1

2 Ju

n-12

Ju

l-12

Aug

-12

Sep-

12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3 A

ug-1

3 Se

p-13

Mon

thly SAA

R

Mon

thly Sales (M

illions)

SALES SAAR

Source: Automotive News; CAR Research

Detroit Three at 45.3% in September 2013 U.S. Market Share:

September 2013 & YTD Total

7.6%

8.2%

9.3%

12.6%

14.5%

16.2%

16.5%

8.0%

8.2%

9.8%

11.5%

14.4%

16.0%

18.0%

0% 5% 10% 15% 20%

Nissan

Hyundai-Kia

Honda

Fiat-Chrysler

Toyota

Ford

GM

YTD 2013

September 2013

Unemployment Rate January 2008 – July 2013

7.1%

14.2%

10.6%

8.7%

4.7%

10.8%

8.4%

5.7%

10.6%

8.8%

7.2%

5.0%

10.0%

7.4%

4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15%

Michigan Indiana Ohio U.S.

Source: Bureau of Labor Sta/s/cs

Motor Vehicle & Parts Manufacturing Employment 1999 – July 2013

316,300

148,500

105,100

70,200

153,500

81,500

1,130,900

681,500

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 July 2013

U.S.

State Level

Michigan Indiana Ohio U.S.

50% change

64% change

53% change

47% change

Source: BLS, U.S. DOL

Auto Sales and Economic Growth are Disconnected U.S. GDP Growth Rate and Vehicle Sales Growth Rate

1952 – Q2 2013

-‐30

-‐20

-‐10

0

10

20

30

40

-‐4.0

-‐2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

52 57 62 67 72 77 82 87 92 97 02 07 12

Vehicle Sales G

rowth Rate

GDP Grow

th Rate

Sales Growth GDP Growth

Source: Bureau of Economic Analysis

Household Net Worth and Vehicle Sales 1978-2013*

0

2

4

6

8

10

12

14

16

18

1975 1980 1985 1990 1995 2000 2005 2010 0

10

20

30

40

50

60

70

80

90

Light V

ehicle Sales

Househ

old Net W

orth in Trillio

ns

Light Vehicle Sales Household Net Worth Net Worth (Real $)

Source: Federal Reserve Sta/s/cal Release , Z.1, Flow of Funds Accounts of the Unite States *Net worth as of Q1 2013; sales as of 1H 2013 SAAR. Real Household net worth is deflated by CPI.

Is the Auto Industry Back?

Product? Yes. Producavity? Yes.

Profitability? Yes.

Producaon? Not quite yet.

Sales? Not quite yet.

Employment? No.

Investment? Yes.

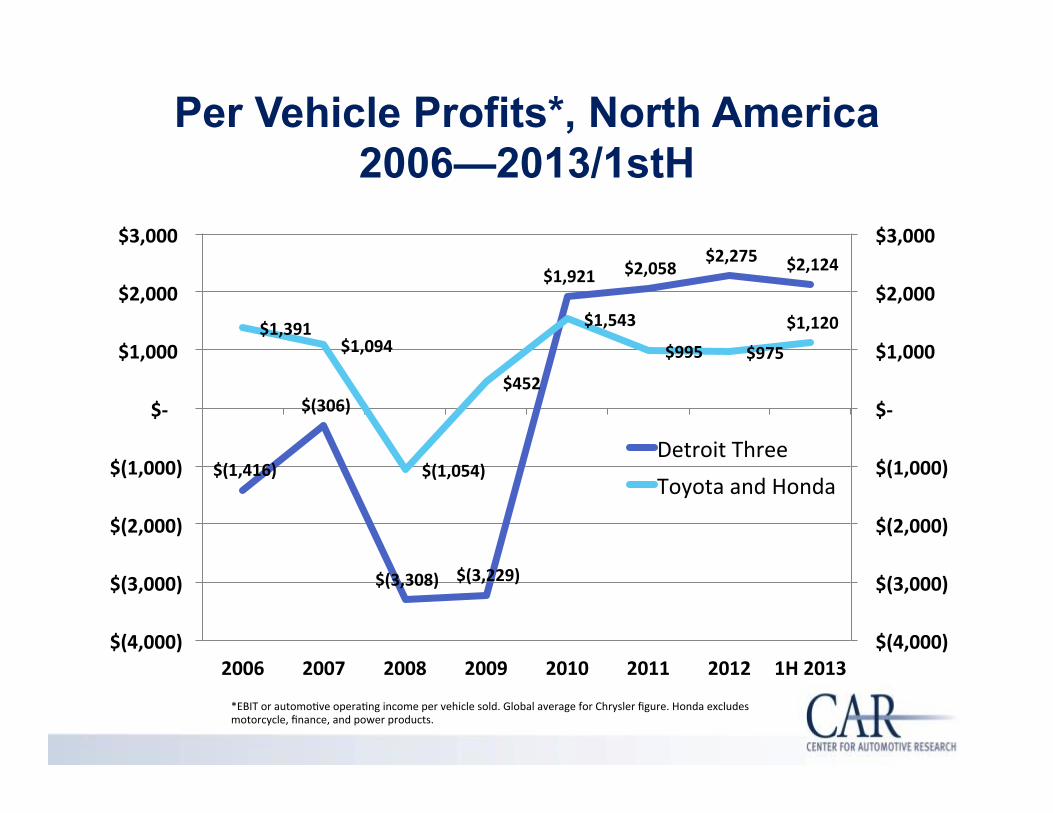

Per Vehicle Profits*, North America 2006—2013/1stH

$(1,416)

$(306)

$(3,308) $(3,229)

$1,921 $2,058 $2,275 $2,124

$1,391 $1,094

$(1,054)

$452

$1,543

$995 $975

$1,120

$(4,000)

$(3,000)

$(2,000)

$(1,000)

$-‐

$1,000

$2,000

$3,000

$(4,000)

$(3,000)

$(2,000)

$(1,000)

$-‐

$1,000

$2,000

$3,000

2006 2007 2008 2009 2010 2011 2012 1H 2013

Detroit Three Toyota and Honda

*EBIT or automo;ve opera;ng income per vehicle sold. Global average for Chrysler figure. Honda excludes motorcycle, finance, and power products.

U.S. Auto Sales Are Still Improving Good: • Net Household Wealth is improving • Unemployment rate at 7.3% • Used Vehicle prices and age of fleet are s;ll high – scrappage low

Auto density increasing . . . • Sales up despite high prices – pent-‐up demand! Increased leasing • Credit is very available/interest rates almost record low • Consumer confidence steady… House prices improving • The Cliff turned out to be a molehill so did the Sequester: Deficit down

But . . . Bad: • Economy s;ll growing at “stall speed”? Or reaching “escape velocity?” More Fiscal Cliffs? • S;ll 12 million unemployed, or more . . . • States/Ci;es cuxng spending and employment • Corpora;ons nervous to hire • Developing economies in trouble • Europe is stagnant

They are Getting Old . . . U.S. Light Vehicle Age and

Scrappage Rate

8.6 8.8 8.8 8.9 8.9 9.0 9.1 9.4 9.5 9.7 9.8 10.0 10.3 10.6

10.9 11.2 11.4

6.78 5.88 5.76

6.74 6.40 6.19 5.50

4.76 4.35

5.03 5.24 5.66

4.12

5.21 4.90

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Average Age Scrappage Rate (%)

Source: R.L. Polk

2013 U.S. Sales Forecasts (Units in Millions)

15.5

15.7

15.6

15.6

15.5

15.2

15.4

16.0

(4/13)

(7/13)

(7/13)

(9/13)

(7/13)

(4/13)

(4/13)

(1/13)

15.5 (7/13)

(3/13)

15.5

15.3

(8/13)

2013 U.S. Sales Forecasts (Units in Millions)

15.25 (15.0 – 15.5)

15.75* (15.5 – 16.0)

14.8

15.3

* Includes heavy duty trucks

15.2

U.S. Light Vehicle CAR Sales Forecast: 2007-2016

16.1

13.2

10.4 11.6

12.8 14.5

15.7 16.0 16.2 16.2

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Source: CAR Research, Jan. 2013

10.4%

11.6%

13.3% 8.3%

CAR U.S. Vehicle Production Forecast: 2013-2016

10.8

8.7

5.8

7.8 8.7

10.4 10.9 11.2 11.4 11.3

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Source: CAR Research, July 2013

34.5%

11.6%

19.5% 4.8% 2.8%

Output increase: • Shorter summer

shutdown • High Cap. U;l. Rate • More lines added • Vehicle exports

increased

Economic Contribution Study: Michigan Assembly Plant

Michigan Assembly Plant and Purchases from Independent Suppliers

• In the past two years, Ford Motor Company has invested over $770 million at Michigan Assembly Plant (MAP) • convert the former truck plant to produce Focus and C-‐MAX

• The plant purchases over $1 billion in parts annually from Michigan-‐based businesses each year; – $1.8 billion throughout the U.S. – $3.2 billion total

• The Michigan Assembly Plant is served by 179 Tier 1 suppliers from across the United States – 80 of these firms located in Michigan.

Economic Contribution of MAP to the Michigan Economy

• Direct employment at MAP is over 5,000 • When supplier and spinoff jobs are taken into account, the

facility supports another 19,000 jobs within Michigan – 48,000 total jobs in the United States (coun;ng the assembly plant

employees)

• These jobs generate annual wages of $1.8 billion in the state of Michigan – $3.6 billion na;onally.

• MAP and its suppliers add $3 billion to the State Gross Product and almost $5.7 billion to na;onal GDP.

• MAP and its suppliers generate $70 million in Michigan state taxes annually

MAP Independent Supplier Spending by State (Millions of Dollars), 2011

Source: Center for Automo/ve Research analysis of data supplied by Ford Motor Company

Assessment of Tax Revenue Generated by the Automotive Sector

Study Findings

• Auto industry generated over $130 billion in government tax revenue in 2010, including $91.5 billion for state governments and $43 billion for the federal government.

• The sources of these revenues include:

• Sales taxes ($30 billion)

• Income taxes ($15 billion)

• Taxes and fees on use ($89 billion)

• Business taxes and fees ($750 million)

State Government Revenue Overview

• Auto industry generated at least $91.5 billion in state government tax revenue in 2010, which is 13 percent of state government tax revenues.

• $30 billion from taxes on vehicle sales and service

• $860 million from taxes on direct employment

• $60 billion from taxes and fees on use of vehicles

• $750 million from taxes on businesses

Automotive Tax Revenues as a Percentage of Total Taxes Paid to State Governments

< 5% 5 to 10% 10 to 15% 15 to 20% > 20%

Oklahoma 23.4%

Texas 19.3%

Florida 19.9%

Michigan 12.6%

Ohio 16.7%

Indiana 15.9%

Illinois 16.2%

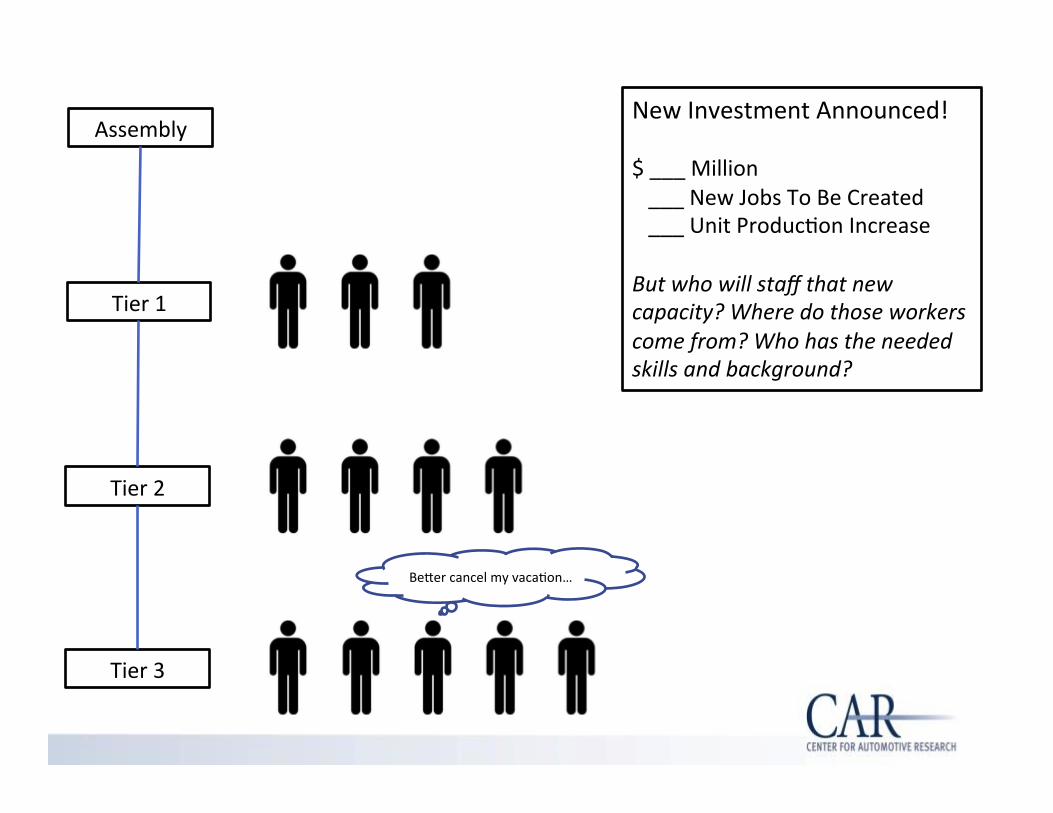

Small Suppliers: Backbone of the Industry, but Constrained

Assembly

Tier 1

Tier 2

Tier 3

Assembly

Tier 1

Tier 2

Tier 3

New Investment Announced! $ ___ Million ___ New Jobs To Be Created ___ Unit Produc;on Increase But who will staff that new capacity? Where do those workers come from? Who has the needed skills and background?

Be|er cancel my vaca;on…

Kim Hill Director, Sustainability and Economic Development Strategies Center for Automo;ve Research Ann Arbor, Michigan [email protected]

Questions?