the north american ride control aftermarket

TRANSCRIPT

The North American Ride Control Aftermarket

How to Handle Upcoming Challenges and Corner the

Market

Matthew Scruggs, Industry Analyst

Automotive & TransportationAutomotive & Transportation

December 14, 2010

Today’s Presenter

Matthew Scruggs, Industry Analyst

Frost & Sullivan

2

Experience covering a broad range of sectors, leveraging long-standing

working relationships with leading industry participants’ Senior Executives in

the following sectors:

•OE Product Development Strategies

•Aftermarket Powertrain Control Electronics

•Aftermarket Legislative Impact Forecasting

•Aftermarket Body Electronics

Focus Points

Agenda

Total North American Ride Control Aftermarket Data

Standard Replacement Ride Control Aftermarket

• Market Data

• Analysis of Drivers, Restraints, Opportunities, and Challenges by Product Type

3

• Analysis of Distribution Channels

Performance Ride Control Aftermarket

• Market Data

• Analysis of Consumer Behavior Data

Strategic Recommendations

Total North American Ride Control Aftermarket

4

Total North American Ride Control Aftermarket

8.5%

91.5%

Revenues by Geographic Region (North America), 2009Top Three Participant Revenue Shares (North America), 2009

44%

19%

15%

5N732-18

91.5%

Source: Frost & Sullivan

20162009

Units (Millions)45.07

Revenues ($ Millions)621.70

Units (Millions)45.66

Revenues ($ Millions)632.11

CAGR 0.19%

CAGR 0.24%

Ride Control Aftermarket Product Segments and Splits by Percentage of Revenue

Performance

17%

Entry-level Shock Absorbers 36% Premium Twin-Tube

Shock Absorbers

4%

Premium Monotube

Shock Absorbers

3%

Entry-level Struts 23% Pre- Premium Premium

6

Entry-level Struts 23% Pre-Assembled Struts 6%

Premium Twin-Tube

Struts

3%

Premium Monotube

Struts

1%

Coil Springs 3%

Strut Mounts 4%

100%

Standard Replacement Ride Control Aftermarket

7

Standard Replacement Aftermarket Unit Shipment and Revenue Forecast

Total Standard Replacement Aftermarket: Unit

Shipment and Revenue Forecast (North America) 2006-

2016

41.00

42.00

43.00

44.00

Un

its (

Mil

lio

n)

540

560

580

600

Reven

ues (

$ M

illi

on

s)

Steady market declines increased dramatically with

the 2008 recession.

Growth from 2010 to 2013, driven by

deferred repair jobs. Growth in this period

also supported by increase in the average

VIO age.

8N732-18

38.00

39.00

40.00

41.00

2006 2008 2010 2012 2014 2016

Un

its (

Mil

lio

n)

480

500

520

540

Reven

ues (

$ M

illi

on

s)

Slight decline after 2013 due to a decline in unit shipments as deferred demand evaporates and OE warranty

terms and part quality increases.

Source: Frost & Sullivan

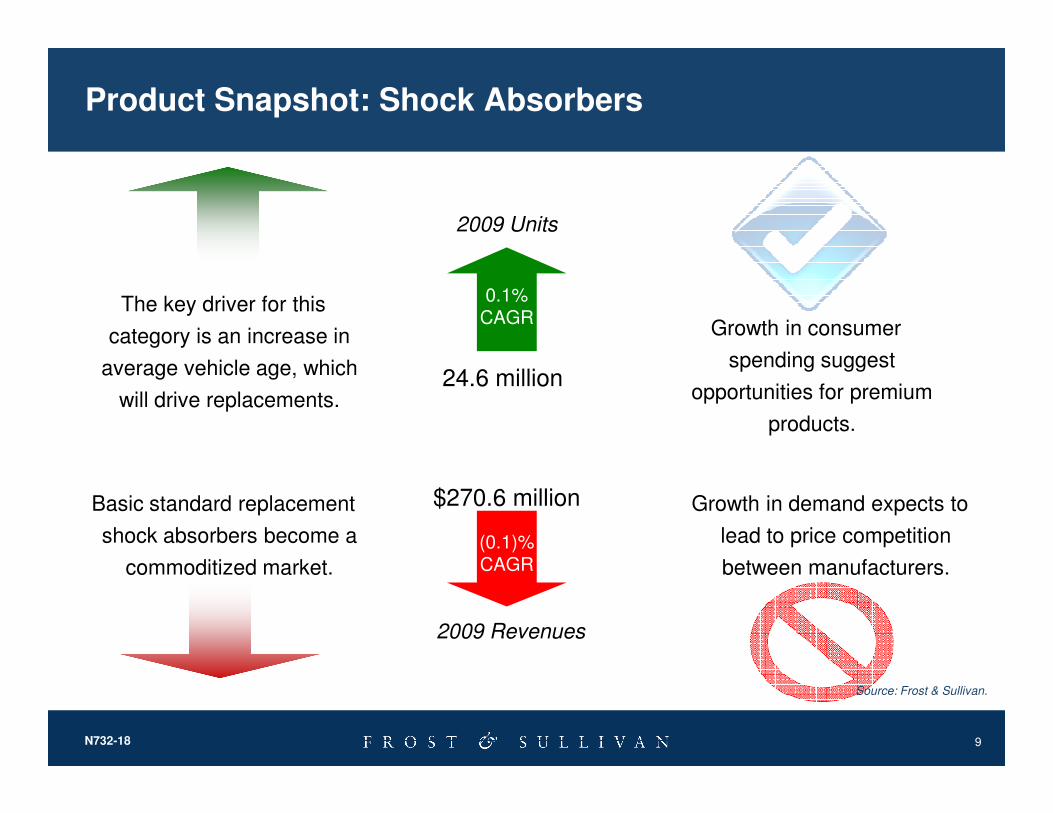

Product Snapshot: Shock Absorbers

The key driver for this

category is an increase in

average vehicle age, which

will drive replacements.

Growth in consumer

spending suggest

opportunities for premium

2009 Units

0.1%CAGR

24.6 million

9N732-18

will drive replacements.

Basic standard replacement

shock absorbers become a

commoditized market.

products.

Growth in demand expects to

lead to price competition

between manufacturers.

Source: Frost & Sullivan.

2009 Revenues

(0.1)%CAGR

$270.6 million

Product Snapshot: Struts

Installed base expects to

increase as small vehicles are

sold more often than light

trucks.

Pre-assembled struts have an

opportunity to cannibalize sales of

coil springs in certain segments.

2009 Units

0.3%CAGR

9.4 million

10N732-18

Extended OE warranty terms

reduces replacements through

the independent aftermarket

Manufacturers must accommodate

growth in product line and growth in

SKUs for retailers as vehicle

applications expand.

Source: Frost & Sullivan.

2009 Revenues

$205.9 million

0.2%CAGR

Product Snapshot: Coil Springs

A shift toward small cars will

increase the installed base of

vehicles with coil springs.

Mild demand growth combined

with low cost for raw materials

creates the potential for

2009 Units

0.94 million

(0.1)%CAGR

11N732-18

Coil springs have a very low

replacement rate, as they are

usually a life-of-the-vehicle part.

enhanced margins.

Steel prices are expected to

increase across the forecast

period, negatively impacting

margins or average pricing.

Source: Frost & Sullivan.

2009 Revenues

(0.2)%CAGR

$20.7 million

Product Snapshot: Strut Mounts

An increase in strut suspension-

equipped vehicles will increase

the installed base.Package sales of struts and strut

mounts drives value proposition

for replacing both components.

2009 Units

0.2%CAGR

5.5 million

12N732-18

Increased OE warranty terms

reduces replacements in the

independent aftermarket.

Manufacturers are challenged to

incorporate product differentiation to

avoid market commoditization.

Source: Frost & Sullivan.

2009 Revenues

$24.8 million

0.2%CAGR

Analysis of Revenues by Distribution Channel

Revenues Split by Distribution Channel (North America), 2009

OES Channel 13% Retail Channel 14% Warehouse Distribution Channel 73%

• Product shift in this channel from shocks to struts

• Extended OE warranty terms on

• Sales come primarily from DIFM installations

• DIY drives retail channel in certain

• WD channel will continue to control the vast majority of revenues

• Slight erosion in some product

13N732-18

Source: Frost & Sullivan

warranty terms on new vehicles

• Strong revenue support from independent installers

Slight growth through

2015

channel in certain segments

• Product shift from coil springs to pre-assembled struts

some product segments to OES channel

• Declines offset by aging vehicle parc

Stability expected

through 2015

Slight decline through

2015

Performance Ride Control Aftermarket

14

Performance Aftermarket Unit Shipment and Revenue Forecast

Total Performance Product Aftermarket: Unit Shipments

and Revenue Forecast (North America) 2006-2016

4.65

4.70

4.75

4.80

4.85

4.90

Un

its (

Mil

lio

n)

100

102

104

106

108

110

Reven

ues (

$ M

illi

on

s)

The performance suspension market

experienced a sharp decline in 2008, as the economic recession restricted consumer

spending.

15N732-18

4.45

4.50

4.55

4.60

2006 2008 2010 2012 2014 2016

Un

its (

Mil

lio

n)

94

96

98

100

Reven

ues (

$ M

illi

on

s)

Beginning in 2009, this market was expected to return to the growth state it enjoyed prior to 2008,

due to economic recovery and a return of consumer spending.

Relevant information from Frost and Sullivan’s Vehicle Modification Study

• Suspension modification rose from 32% to 48% • 61% classify their skill set as “advanced”• 90% modify their vehicles for performance• 56% define themselves as light truck/SUV enthusiasts

• 82% spend $1,000 to $5,000+ on total vehicle modifications

• 51% purchase performance parts from an automotive retailer

• 46% purchase from a custom/speed shop

Source: Frost & Sullivan.

16N732-18

• 64% of modifications are DIY • 52% of modifications are performed on Luxury/Specialty

vehicles• 51% of modifications are performed on SUVs or CUVs

• 30% plan to modify a Chevrolet or Ford vehicle for their next vehicle

• 44% plan to modify a vehicle model year of 2008 or newer

Strategic Recommendations

17

Total Ride Control Aftermarket: Actionable Opportunities in the Forecast Period

Renewed growth in consumer maintenance

spending

Consumer focus on value Consumers are expected to become very price-conscious going forward, especially in commodity markets like standard

replacement ride control.

Spending levels are returning to normal, driven by economic recovery; this will result in a slight increase in repair rates over

normal levels.

18

Increase in average vehicle age

Strategic Recommendation

Average vehicle age is expected to jump due to lower-than-average new vehicle sales and continued economic difficulty.

Develop products that compete on a features/functionality basis, rather than a price-only basis:

• The increase in consumer maintenance spending will support this move.

• As the average vehicle age increases, consumer willingness to invest in preventative maintenance is expected to increase.

Source: Frost & Sullivan

Total Ride Control Aftermarket: Actionable Challenges in the Forecast Period

Serious lack of consumer education

Vehicle population shifting

Imported products competing on a price basis

Imported products that compete in the standard replacement market can create downward price pressure on other

competitors.

Consumer education about the impact of ride control equipment on vehicle safety and comfort has historically been

lacking.

The dramatic jump in fuel prices in mid-2008 began a trend of vehicle downsizing. The result will be a larger proportion of

19

Vehicle population shifting towards passenger cars

Strategic Recommendation

vehicle downsizing. The result will be a larger proportion of passenger cars in the key replacement age range near the end

of the forecast period.

Adjust product line to deliver suitable applications for the vehicles forecast to enter the target replacement age:

• Offer value-added features and functionality • Capitalize on the manufacturer’s reputation for quality through

extended warranty support for entry-level products• Launch aggressive consumer education campaigns, both on-

location and through social media and internet outlets

Source: Frost & Sullivan

Next Steps

� Request a proposal for or Growth Partnership Services or Growth Consulting Services to support you and your team to accelerate the growth of your company. ([email protected]) 1-877-GoFrost (1-877-463-7678)

� Join us at our annual Growth, Innovation, and Leadership 2011: A Frost & Sullivan Global Congress on Corporate Growth (www.gil-global.com)

20

� Register for the next Chairman’s Series on Growth: Driving Innovation – The What, Why & How of Visions and Benchmarks

(December 20, 2010) (http://www.frost.com/growth)

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keepabreast of innovative growth opportunities(www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

21

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

Frost & Sullivan’s Growth Consulting can assist with your growth strategies

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/pages/Frost-Sullivan/249995031751?ref=ts

http://www.linkedin.com/companies/4506

22

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Sarah Saatzer

Corporate Communications

(210) 477-8427

Craig Hays

Director of Sales

Automotive & Transportation

(210) 247-2460

23

Mary-Beth Kellenberger

Global Program Manager

Automotive & Transportation

(416) 490-1997