the oil sands: canada’s world scale hydrocarbon...

TRANSCRIPT

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

1

The Oil Sands: Canada’s World Scale Hydrocarbon Resource

Calgary PMAC Professional Speaker Series Dinner Event

Alberta Institute Purchasing Management Association of Canada

12-1

Photo Source: Syncrude Canada Limited

April 25, 2012Calgary, Alberta

Bob DunbarStrategy West Inc.

Presentation Outline

Reserves and Historical Production

Bitumen Production and Upgrading

Markets and Market Access

Challenges and Industry Outlook

2

Industry Outlook

Economic Impacts and the Supply Chain

Conclusions

Photo Source: Syncrude Canada Ltd.

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

2

Resources and Reserves (ERCB)

Initial volume in place (bitumen): 1,804 billion barrels

Initial established reserves: 176.8 billion barrels

Cumulative production:7.5 billion barrels

Remaining established reserves:established reserves: 169.3 billion barrels

Remaining established reserves under active development: 26.0 billion barrels

3 Oil Sands Areas (OSAs) comprising 15 major Oil Sands Deposits (OSDs)

142,000 square kilometres (54,000 square miles) Data at year-end 2010

Source: ERCB ST98-2011; Alberta’s Energy Reserves 2010 and Supply/Demand Outlook 2011-2020; June 2011

Mineable and In SituResources and Reserves

Mineable Resources/Reserves

< 65m (~215 ft) to top of oil sands

In Situ Resources/Reserves

> 65m (~215 ft) to top of oil sands

Athabasca Oil Sands Area only

7% of initial volume in place

22% of initial established reserves

64% of cumulative production to year-end 2010

Athabasca, Cold Lake and Peace River Oil Sands Areas

93% of initial volume in place

78% of initial established reserves

36% of cumulative production to year-end 2010

Source: ERCB ST98-2011; Alberta’s Energy Reserves 2010 and Supply/Demand Outlook 2011-2020; June 2011

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

3

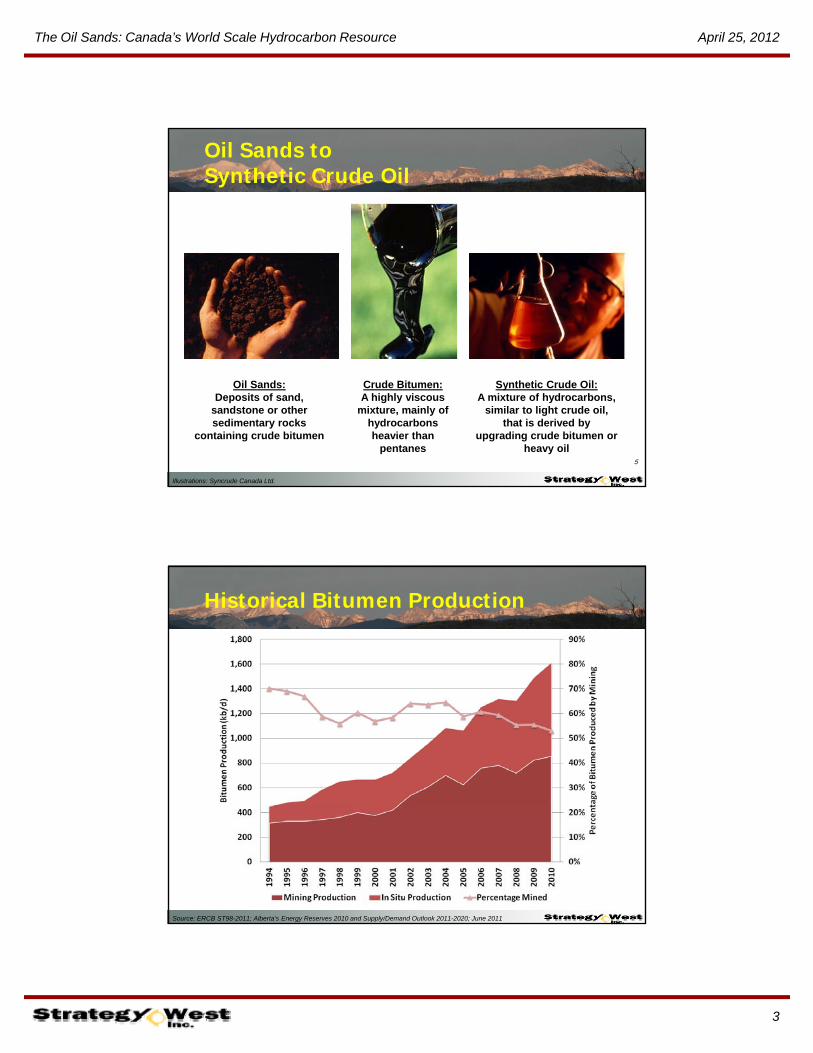

Oil Sands to Synthetic Crude Oil

5

Oil Sands:Deposits of sand,

sandstone or other sedimentary rocks

containing crude bitumen

Synthetic Crude Oil:A mixture of hydrocarbons,

similar to light crude oil, that is derived by

upgrading crude bitumen or heavy oil

Crude Bitumen:A highly viscous

mixture, mainly of hydrocarbons heavier than

pentanes

Illustrations: Syncrude Canada Ltd.

Historical Bitumen Production

Source: ERCB ST98-2011; Alberta’s Energy Reserves 2010 and Supply/Demand Outlook 2011-2020; June 2011

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

4

Historical Oil Sands Supply

Source: ERCB ST98-2011; Alberta’s Energy Reserves 2010 and Supply/Demand Outlook 2011-2020; June 2011

Historical Oil Sands Industry Expenditures

Source: Canadian Association of Petroleum Producers

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

5

In Situ Recovery

Primary Recovery Secondary Recovery

T ti R Tertiary Recovery• Steam Injection Cyclic Steam Stimulation

(CSS) Steam Assisted Gravity

Drainage (SAGD)• In Situ Combustion Toe-to-Heel Air Injection

(THAI)(THAI)• Solvent Injection VAPEX N-Solv

• Hybrid (Steam/Solvent & Steam/Gas) Processes

• Electric Heating9

In Situ Recovery: Dealing with Viscosity

10

Sources: Enerplus; Syncrude Canada Limited

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

6

Cyclic Steam Stimulation (CSS)

Source: Canadian Association of Petroleum Producers

Established Cold Lake and Peace River CSS Projects

Operating Imperial Cold Lake

Under Construction Imperial Cold LakeImperial Cold Lake

Phases 1-13 (1985) CNRL Primrose/Wolf

Lake (1985) Shell Cadotte Lake

(1986) Southern Pacific

Imperial Cold Lake Phases 14-16 (2014)

(North Peace Energy) Red Earth Pilot (2009)

Source: Project Applications and Announcements

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

7

Steam Assisted Gravity Drainage (SAGD)

Source: Canadian Association of Petroleum Producers

Operating SAGD Projects

South Athabasca Cenovus Foster Creek

Phases A (2001), B, C, D & E Cenovus Christina Lake

North Athabasca Suncor MacKay River

Phase 1 (2002) Suncor Firebag Cenovus Christina Lake

Phase A (2002), B & C JACOS Hangingstone Pilot (2002) ConocoPhillips Surmont

Pilot (2006) & Phase 1 Connacher Great Divide

Pod 1 (2007) & Pod 2 (Algar) Devon Jackfish Phase 1 & 2 (2007) MEG Energy Christina Lake

Phase 1 Pilot (2008) & Phase 2A

Suncor Firebag Phases 1 (2004), 2, & 3 and Cogeneration Expansion

Cold Lake Husky Tucker Phase 1 (2006) Shell Orion Phase 1 (2007) Pengrowth Lindberg Pilot (2012)

North Athabasca Nexen Long Lake Phase 1 (2008) Statoil Leismer Demonstration

(2010) BlackPearl Blackrod Pilot (2011)

North AthabascaOperations Suspended Total Joslyn

Phases 1 (2004) & 2

Source: Project Applications and Announcements

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

8

SAGD Projects under Construction

South Athabasca Cenovus Christina Lake

Phase D (2012)

North Athabasca Southern Pacific STP McKay

Phase 1 (2012) CNRL Kirby South (2013) Grizzly Algar Lake Phase 1

(2013) MEG Energy Christina Lake

Phase 2B (2013) Cenovus Foster Creek Phase F

(2014) Harvest Black Gold Phase 1

(2014)

Suncor Firebag Phase 4 (2013)

Husky Sunrise Phase 1 (2014)

Cold Lake None

(2014) ConocoPhillips Surmont

Phase 2 (2015) Devon Jackfish Phase 3 (2015) Laricina Germain Phase 1

(2015)

Source: Project Applications and Announcements

Surface Mining & Bitumen Extraction

Surface Oil Sands BitumenSurfaceMining

Oil SandsTransport

BitumenExtraction

16

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

9

Established Athabasca Mining Projects

Operating

Suncor (1967)

Under Construction

CNRL Horizon Suncor (1967) Millennium Mine

Syncrude (1978) North Mine and Aurora North Mine

AOSP Muskeg River

CNRL Horizon Tranche 2 (2012)

Suncor North Steepbank Extension (2012)

Imperial/ExxonMobil AOSP Muskeg River (2002) and Jackpine Phase 1A (2010)

CNRL Horizon Phase 1 (2008)

Imperial/ExxonMobil Kearl Lake Phase 1 (2012) and Phase 2 (2015)

Truck and Shovel Mining

18

Source: Syncrude Canada Ltd.

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

10

Double Roll Crusher

Source: Shell Canada Limited

Slurry Preparation

Source: Shell Canada Limited

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

11

Hydrotransport

21

Source: Syncrude Canada Ltd.

Albian Primary Separation Vessels

22

Photo Courtesy Shell Canada Limited

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

12

Tailings Disposal

Tailings are an aqueous waste product of the bitumen extraction processT ili t i Tailings contain:• Unrecovered bitumen• Sand, silts and clays• Residual solvents and

chemicals from bitumen extraction

Fluid fine tailings are difficult to consolidate

Alberta’s inventory of fluid Alberta s inventory of fluid fine tailings that require long term containment is now 840 106 m3

Tailings ponds today are approximately 170 km2

Source: Pembina Institute; Alberta Energy Resources Conservation Board

Segregation of Tailings Within a Tailings Pond

In tailings ponds, segregation occurs with the heaviest material, sand, settling to the bottom of the pond. The water will rise to the top of the pond and be recycled back to the extraction process. Within the pond, several y p p ,layers will start to form. Thin fine tailings (TFT) will start to form almost immediately. TFT is a combination of fines and water less than 30% solids. TFT will consolidate and within approximately a three-year period and will start to form mature fine tailings (MFT).

Source: Suncor Energy Inc.

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

13

Suncor’s Tailings Reduction Operations (TRO)

Source: Suncor Energy Inc.

Reclamation

Disturbed Lands are to be returned to a t t th t i

Gateway Hill Reclaimed Land

state that is as biologically productive as the state that existed before operations commenced

S

26

Image Source: Canadian Oil Sands Trust.

Syncrude received the first oil sands reclamation certificate in March 2008

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

14

Upgrading

Approximately 60% of produced bitumen is being “upgraded” to synthetic

d il (SCO) d th

The remaining 40% is being blended with diluents before being hi d t d tcrude oil (SCO) and other

products before being shipped to downstream markets (refineries)

shipped to downstream markets (refineries)

Photo Courtesy Shell Canada Limited

27

Upgrading Overview

Purpose: Mechanisms:

28

Purpose:• Produce higher value

liquid hydrocarbon products

• Produce valuable byproducts

Mechanisms:• Remove or breakdown

bitumen residues

• Remove contaminants

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

15

Established Upgraders

Operating

Suncor Base (1967) &

Under Construction

CNRL Horizon Tranche 2 ( )Millennium (2001)

Syncrude Mildred Lake (1978)

AOSP Scotford Upgrader 1 (2003)

CNRL Horizon Phase 1

(2012)

Construction Suspended

Suncor Voyageur

North West Upgrading CNRL Horizon Phase 1

(2008)

Nexen Long Lake Phase 1 (2008)

Sturgeon

Value Creation (BA Energy) Heartland

Source: Project Applications and Announcements

Bitumen Based Feedstocks to Refined Products

Canadian & USRefineries

Refined Petroleum Products

Mines &In Situ

Projects

Blen

ded

B

itum

en

Blended Bitumen

Refineries

30

GasolineDieselJet FuelFuel OilsLubricantsAsphaltOthers

Synthetic Crude Oil

Upgraders

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

16

Oil Sands Industry Value Chain and Supply Chain Management

Exploration Bitumen Production Upgrading Transportation Refining Distribution

and Marketing

Source: Strategy West Inc.; PMAC

Market Demand for Western Canadian Crude Oil

Source: CAPP; Crude Oil Forecasts, Markets and Pipelines; June 2011

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

17

Existing and Proposed Canadian and US Crude Oil Pipelines

Source: CAPP; Crude Oil Forecasts, Markets and Pipelines; June 2011

Economic Uncertainties• Oil Prices and Oil Price

ff

Oil Sands Industry Economic Challenges

Project Reliability• Upgrader Outages

Differentials

• Market Demand

Market Access

Capital Costs• Project Management

• Availability/Capability of

Capital Needs• Capital Markets

• Collaboration

• Joint Ventures

• Mergers & Acquisitions

Regulatory TimelinesAvailability/Capability of Skilled Labour and Services

• Material and Equipment Costs

Operating Costs

Regulatory Timelines

Regulatory Uncertainties• Greenhouse Gas

Emission Regulations

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

18

Oil Sands Industry Societal Challenges

Public Image

Public Services

First Nations

Employee Health Public Services• Health

• Education

• Other

Public Infrastructure

Employee Health and Safety

Regulatory Agencies• Staffing

• Workload• Road

• Water & Sewer

• Rail

• Other

• Workload

• Funding

Air Emissions• Greenhouse Gases

Impacts on Land• Flora and Fauna

Oil Sands Industry Environmental Challenges

Greenhouse Gases

• Criteria Air Contaminants (SOx, NOx, PM, VOCs, CO, NH3)

Solid Wastes

Flora and Fauna

Impacts on Surface Waterways

Water Use• Consumption

R l• Tailings

• Other Solid Wastes

Liquid Wastes

• Recycle

Reclamation and Abandonment

Cumulative Effects

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

19

Oil Sands GHG Emissions

In 2010, Canada’s oil sands industry emitted 46 Mt of GHGs accounting for:• 30% of Canadian oil and gas sector GHG emissions

• 6.6% of total Canadian GHG emissions

• 0.1% of total global GHG emissions

Source: Environment Canada

GHG Emissions – Wells to Wheels

Source: Alberta Energy Research Institute/Jacobs Consultancy; June 2009

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

20

Oil Sands Industry Outlooks

The ERCB and CAPP release comprehensive oil sands industry outlooks in June of each year • They may be downloaded at www.strategywest.com

Other organizations (NEB, IHS CERA, CERI, IEA, EIA) release industry outlooks periodically

The ERCB and CAPP outlooks project that:• Alberta bitumen production will more than double by 2020

from about 1.6 million b/d (mb/d) in 2010 to about 3.3-3.5 mb/d

• Bitumen production from in situ projects will surpass bitumen production from mining projects within the next few years

• The percentage of bitumen that is upgraded before it leaves• The percentage of bitumen that is upgraded before it leaves Alberta will decline – i.e., there will be limited investment in new upgrading capacity

More than 6.0 mb/d of new bitumen capacity has been proposed• Many projects will experience delays• Other projects will be cancelled

ERCB Bitumen Production Outlook

70%

80%

3,500

4,000

oduc

ed)

20%

30%

40%

50%

60%

1 000

1,500

2,000

2,500

3,000

Min

ed (

% o

f Tot

al B

itum

en P

ro

Bit

umen

Pro

duct

ion

(kb/

d)

0%

10%

20%

0

500

1,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Bit

umen

M

Mining In Situ Percentage Mined

Source: ERCB ST98-2011; Alberta’s Energy Reserves 2010 and Supply/Demand Outlook 2011-2020; June 2011

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

21

ERCB Oil Sands Supply Outlook

60%

70%

3,000

3,500

20%

30%

40%

50%

1,000

1,500

2,000

2,500

Percentage of B

itumen Upgraded

Oil Supply (kb/d)

0%

10%

0

500

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

P

Synthetic Bitumen Percentage Upgraded

Source: ERCB ST98-2011; Alberta’s Energy Reserves 2010 and Supply/Demand Outlook 2011-2020; June 2011

Economic Benefits of Oil Sands Sector over 2010-2035 Period

Source: CERI; CAPP

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

22

Economic Benefits of Oil Sands Sector over 2010-2035 Period The estimated investments,

reinvestments, and revenues from operation of the new oil sands projects are approximately $2 077projects are approximately $2,077 billion (2010 $C) during the period 2010-2035. $253 billion is considered strategic initial capital for construction and $1,824 billion for operation, maintenance and sustaining capital.

Total GDP impact of oil sands investment and operations over a 25‐year period is estimated to be y p$2,106 billion for Canada, and $521 billion for the US.

Strategy West believes that expenditures will be higher than indicated by CERI (see graphs to right), particularly beyond 2025, and that economic benefits will be greater than CERI’s estimates. 43

Source: CERI; Strategy West

Employment Generated and Economic Benefits Outside Alberta 2010-2035 • Employment in Canada as a result of new oil sands investments is

expected to grow from 75,000 jobs in 2010 to 905,000 jobs in 2035 with 126,000 jobs being sourced in provinces other than Alberta.

• Although Alberta receives about 94% of the economic benefits from oil sands, the economic impact across Canada is significant.

Source: CERI; CAPP

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

23

Oil Sands Industry Purchases 2010-2035

The goods, materials and services used to construct and

operate in situ oil sandsoperate in situ oil sands projects, mines and upgraders

come from across North America. Many of the

components – tires, trucks, gauges, valves, pumps etc. –are produced in central and

eastern Canada.

It is estimated that the oil

$117 billion is close to the

GDP contribution of

Canada’s manufacturing

Source: Canadian Association of Petroleum Producers; CERI; Statistics Canada

It is estimated that the oil sands industry will purchase

roughly $117 billion in supplies and services from Canadian provinces outside

Alberta over the next 25 years – about $5 billion/year.

manufacturing industry in

2010.

Suppliers and Service Providers

Accommodations

General Oilfield Contractors

Drilling Services

Electrical Instrumentation/

Financial Safety Products & Services

Accounting Site Preparation

Air Charter Services

Building Products and Services

Contractors Instrumentation/ Controls

Environmental Products & Services

Site Preparation & Restoration

Speciality Services

Equipment

Information Services/Software

Chemicals

Catalysts

Industrial Gases

EPCM Contractors

Site Preparation & Restoration

Maintenance & Turnaround

Services Staffing

Construction

Consultants

Drilling Products

Equipment Fabrication

Land Agents

Legal

Equipment Manufacturing

Welding Products & Services

Pipeline Products & Services

Rig Moving

Equipment Rentals Trucking

Well Service

Dredging

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

24

Maximizing Free Cash Flow/Value Creation

RevenueProducts Produced• Products Produced

• Prices Realized• Production Rates• Reliability/On-stream Factor

Expenditures• Capital• Operating• Working Capital/Timing• Royalties and Taxes• Abandonment and Reclamation

Value Creation Levers

Outside our Control Within our Control

Revenue Product Prices

Products Produced

Production Rates

Reliability

C it l

Expenditures

Royalty and Tax Regulations

Abandonment & Reclamation

Requirements

Capital Expenditures

Operating Expenditures

Working Capital/Timing

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

25

CAPP Canadian Crude Oil Supply Outlook

4 000

4,500

5,000Oil Sands In Situ

Oil Sands Mining

E Canada

WCanada Condensate

1 500

2,000

2,500

3,000

3,500

4,000

Oil Supply (kb/d)

W Canada Condensate

W Canada Heavy

W Canada L&M

Source: CAPP; Crude Oil Forecast, Markets & Pipelines; June 2011

0

500

1,000

1,500

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

US

Saudi Arabia

Russian Federation

World’s Largest Oil Producers

Iraq

Venezuela

Kuwait

United Arab Emirates

Mexico

Canada

China

IranBy 2025?

0 2,000 4,000 6,000 8,000 10,000 12,000

Angola

Norway

Brazil

Nigeria

2010 Oil Production (kb/d)

Source: BP Statistical Review of World Energy; June 2011

Total World Oil Production in 2010

82,095 kb/d

The Oil Sands: Canada’s World Scale Hydrocarbon Resource April 25, 2012

26

Conclusions

Canada’s oil sands deposits are among the world’s largest hydrocarbon accumulations.

The oil sands industry is well established and The oil sands industry is well established and making a significant contribution to global oil supply.

The 2008/2009 financial crisis caused project deferrals and cancellations.

Industry growth has resumed; the growth rate will depend on oil prices and how industry and

dd h h ll hp p y

government address the many challenges the industry faces.

The industry is expected to add more than $2 trillion of economic benefits to the Canadian economy over the 2010-2035 period.

Thank You

Please visit t t t f il

Questions?

52

www.strategywest.com for oil sands project lists and other detailed oil sands industry

information