the outlook for energy - ihs markit · youtlook for nigeria? iraq? iran? venezuela? ... shell...

TRANSCRIPT

Copyright 2007 © Global Insight, Inc.

The Outlook for Energy

Toronto, Ontario, Canada19 September 2007

Mary NovakManaging DirectorEnergy Services

2Copyright 2007 © Global Insight, Inc.

Oil Markets: Uncharted Waters Ahead

Uncertainties are greater than ever(demand, supply, costs of development, geopolitics, etc.)

Demand: Some signs of slowing in the short term, but the impact of rising income in developing countries will underpin growth over the long term

End of spare capacity (upstream and downstream) means new demandwill need new supply

Supply mix will become more diverse and more complex

Crude oil supply/demand balance plus OPEC attitudes point to continuing firm prices into the long term

Global Insight base-case forecast shows nominal prices are expected to flatten/rise, real-terms prices to decline

Downside price sensitivities are mostly related to demand, upside mostly to supply

3Copyright 2007 © Global Insight, Inc.

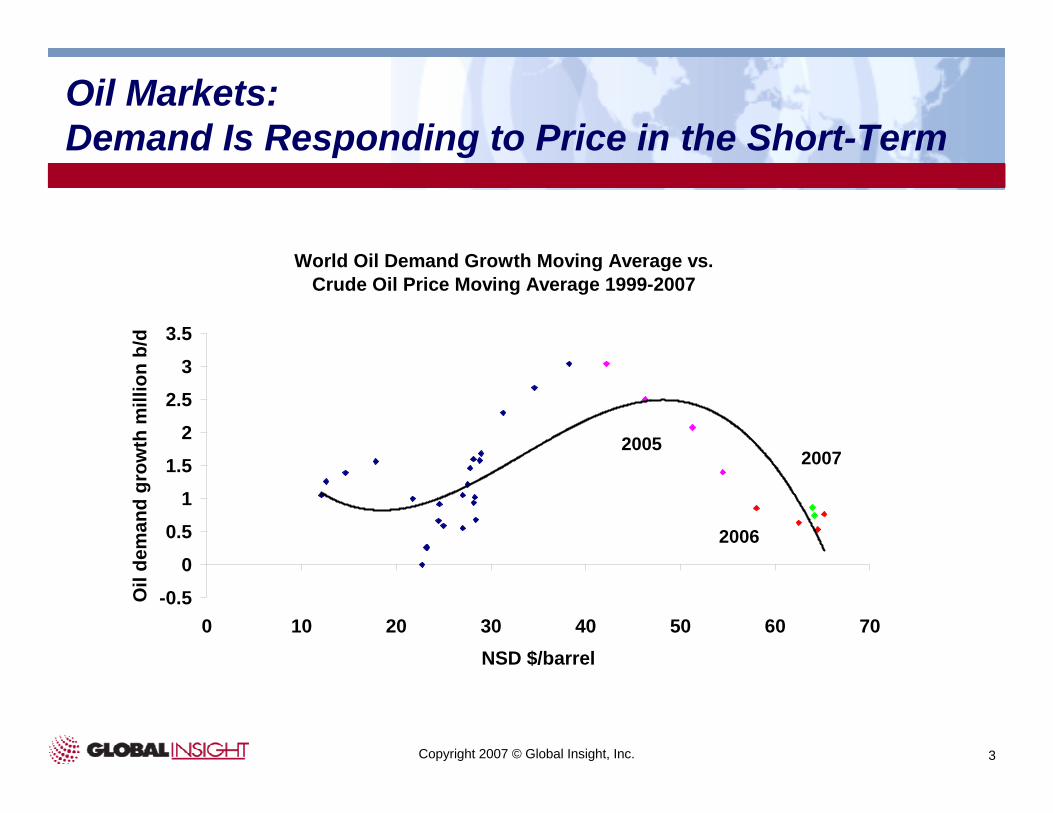

Oil Markets: Demand Is Responding to Price in the Short-Term

World Oil Demand Growth Moving Average vs. Crude Oil Price Moving Average 1999-2007

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

0 10 20 30 40 50 60 70NSD $/barrel

Oil

dem

and

grow

th m

illio

n b/

d

2005

2006

2007

4Copyright 2007 © Global Insight, Inc.

Oil Markets: Longer-Term, Demand Growth Will Be Dominated by Asia and Transport Uses

0

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020 2025

Mill

ion

Bar

rels

a D

ay

FSUAfricaMiddle EastAsia/PacificS. AmericaE. EuropeW. EuropeN. America

-2

0

2

4

6

8

10

12

NorthAmerica

WestEurope

EasternEurope

SouthAmerica

Asia/Pacific

Middle East

Africa FSU

Mill

ion

Bar

rels

per

Day

Others Power Generation Transportation Petrochemical Feedstock Industrial Sector Domestic Sector

Global Oil Demand by Region Oil Demand Growth (2005–25)

5Copyright 2007 © Global Insight, Inc.

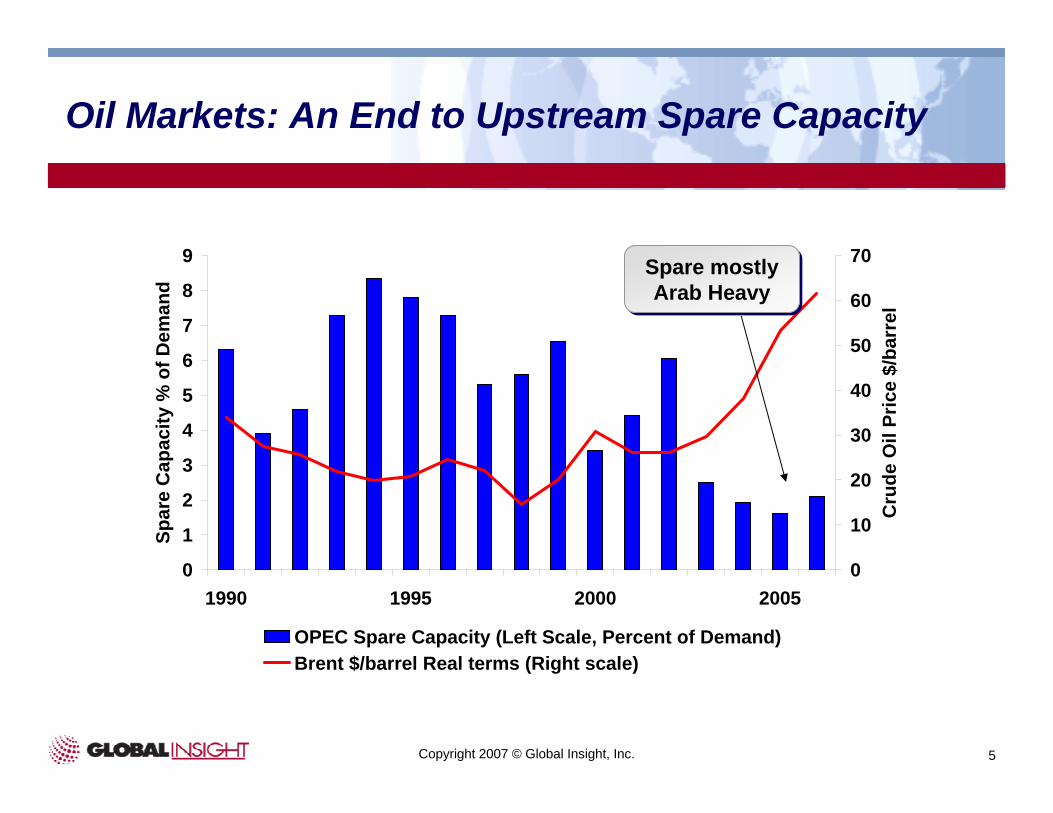

Oil Markets: An End to Upstream Spare Capacity

0

1

2

3

4

5

6

7

8

9

1990 1995 2000 2005

Spar

e C

apac

ity %

of D

eman

d

0

10

20

30

40

50

60

70

Cru

de O

il Pr

ice

$/ba

rrel

OPEC Spare Capacity (Left Scale, Percent of Demand)Brent $/barrel Real terms (Right scale)

Spare mostly Arab Heavy

Spare mostly Arab Heavy

6Copyright 2007 © Global Insight, Inc.

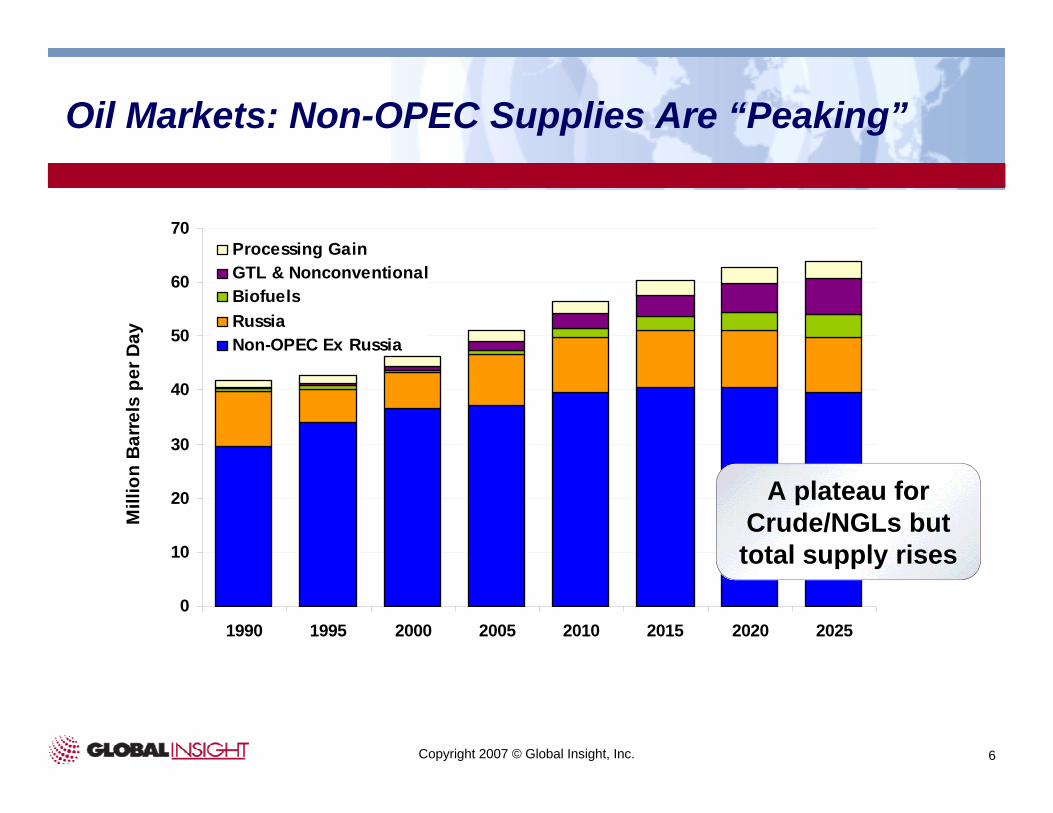

Oil Markets: Non-OPEC Supplies Are “Peaking”

0

10

20

30

40

50

60

70

1990 1995 2000 2005 2010 2015 2020 2025

Mill

ion

Bar

rels

per

Day

Processing GainGTL & NonconventionalBiofuelsRussiaNon-OPEC Ex Russia

A plateau for Crude/NGLs but total supply rises

7Copyright 2007 © Global Insight, Inc.

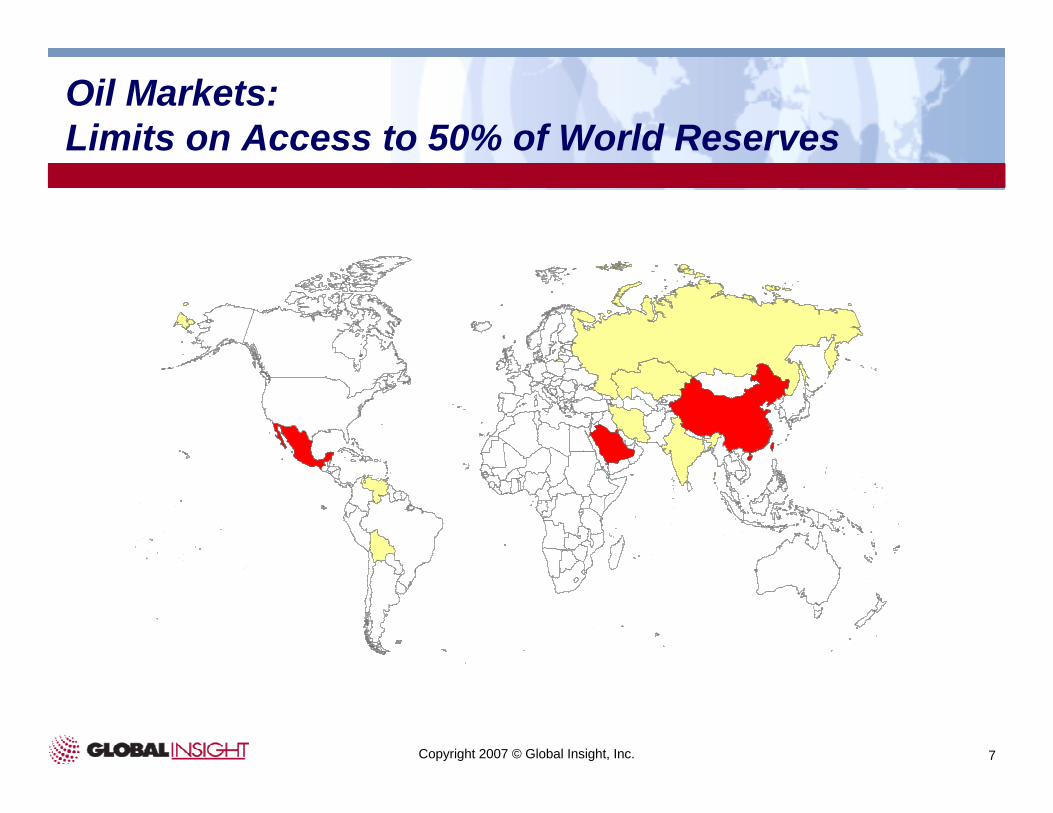

Oil Markets: Limits on Access to 50% of World Reserves

8Copyright 2007 © Global Insight, Inc.

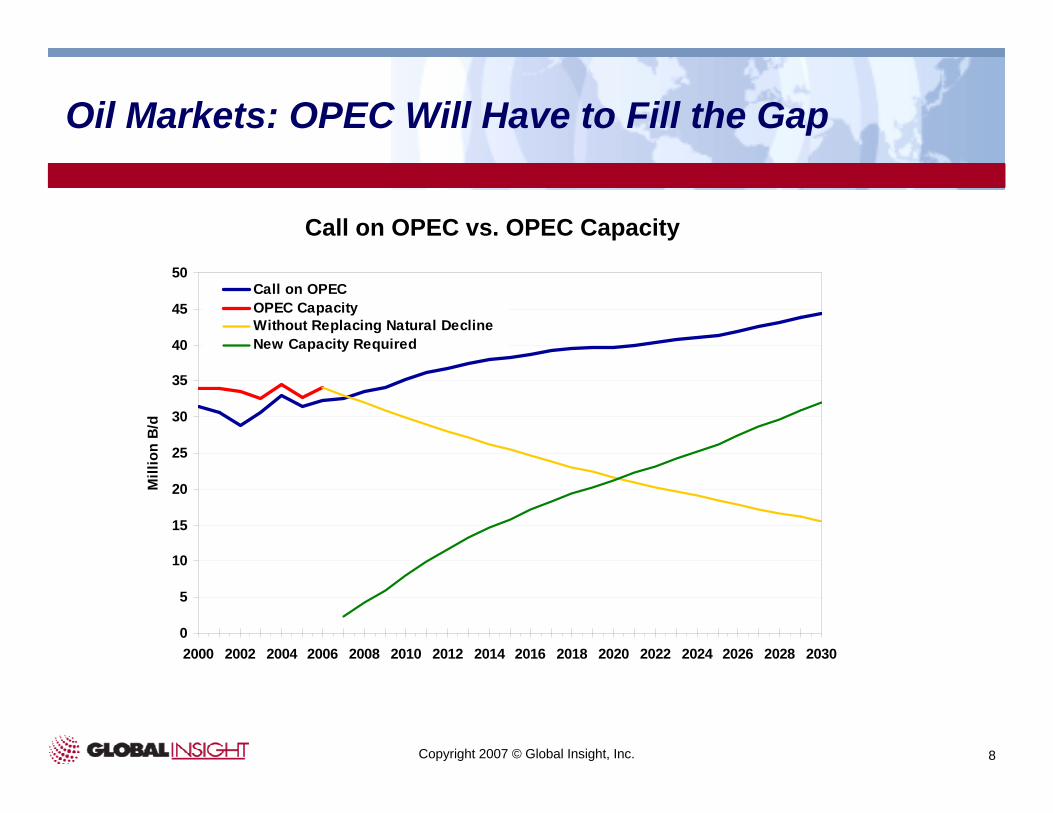

Oil Markets: OPEC Will Have to Fill the Gap

0

5

10

15

20

25

30

35

40

45

50

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Mill

ion

B/d

Call on OPECOPEC Capacity Without Replacing Natural DeclineNew Capacity Required

Call on OPEC vs. OPEC Capacity

9Copyright 2007 © Global Insight, Inc.

Oil Markets: Planned Capacity Seems Adequate…

0

500

1000

1500

2000

2500

2007 2008 2009 2010 2011

Thou

sand

b/d

NigeriaLibyaIndonesiaAlgeriaUAEQatarIranKuwaitSaudi Arabia

REDSweet, mostly lighter crude

REDSweet, mostly lighter crude

BLUESour, mostly heavier crude

BLUESour, mostly heavier crude

10Copyright 2007 © Global Insight, Inc.

Oil Markets: …But, Will Supply Respond?

Peak oil? Could the pessimists be right?

OPEC reserves? OPEC policies/aspirations?

Outlook for Nigeria? Iraq? Iran? Venezuela?

Non-OPEC: not much on the shelf beyond 2009?

Increasing resource nationalism and access?

Outlook for “non-conventionals” (tar sands, biofuels, GTLs)

Technological/cost breakthroughs?

11Copyright 2007 © Global Insight, Inc.

Oil Markets: Cost of Developing New Supplies Is Rising

0

10

20

30

40

50

60

Mid 1990s F&D Costs$4/barrel. Requires oil price

of $18/barrel

2001-2003 F&D Costs$7/barrel. Requires oil price

of $28/barrel

2006 F&D Costs $13/barrel. Requires oil price

of $48/barrel

$/B

arre

l

Net income to achieve 13% ROCEIncome tax @ 40%Depletion (DD&A) (= F&D)Operating (Lifting) costsProduction taxDifferential to average well-head price

Full Costs and Required Oil Price to Achieve 13% ROCE.

12Copyright 2007 © Global Insight, Inc.

Oil Markets: Global Insight’s Crude Oil Price Scenarios

0

20

40

60

80

100

120

140

160

1986 1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 2030 2034

2006

$/b

bl

Supply ConstrainedMarket RemanagedDemand ConstrainedShock

13Copyright 2007 © Global Insight, Inc.

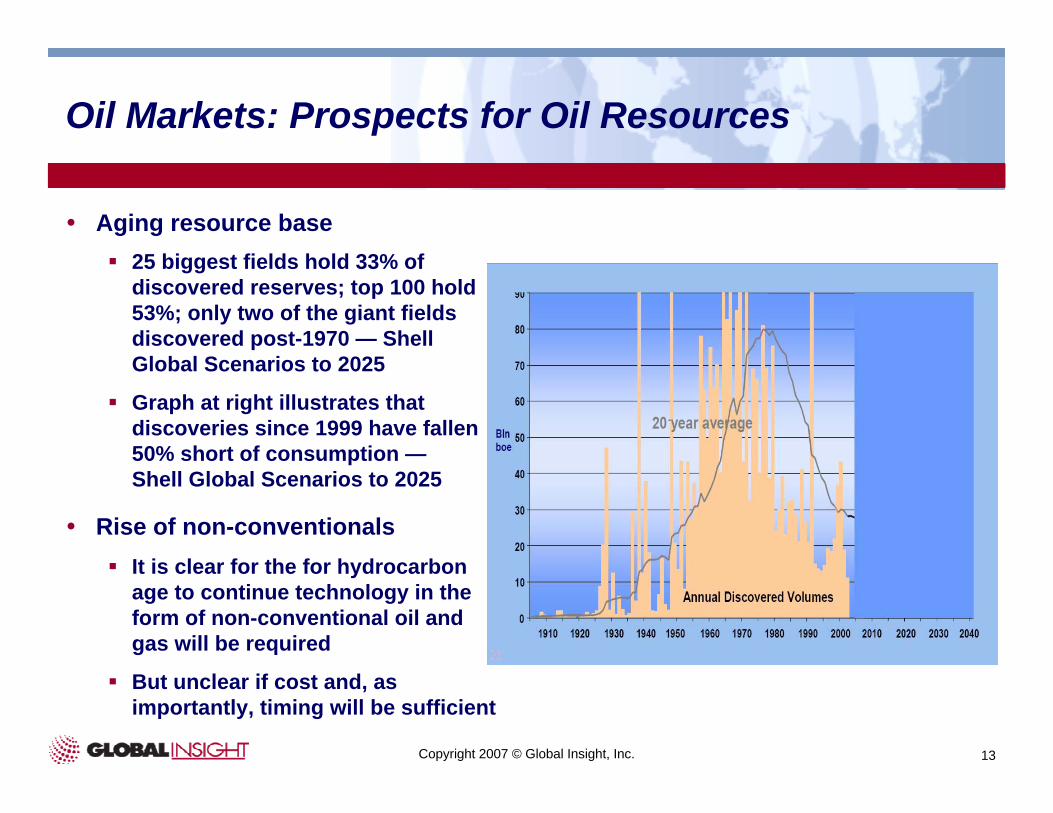

Oil Markets: Prospects for Oil Resources

Aging resource base25 biggest fields hold 33% of discovered reserves; top 100 hold 53%; only two of the giant fields discovered post-1970 — Shell Global Scenarios to 2025

Graph at right illustrates that discoveries since 1999 have fallen 50% short of consumption —Shell Global Scenarios to 2025

Rise of non-conventionalsIt is clear for the for hydrocarbon age to continue technology in the form of non-conventional oil and gas will be required

But unclear if cost and, as importantly, timing will be sufficient

14Copyright 2007 © Global Insight, Inc.

Oil Markets: Conventional Crude Oil: Produced and Remaining Reserves

0

500

1,000

1,500

2,000

2,500

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

Bil

lio

ns

of

Ba

rre

ls

Remaining Reserves Produced Reserves

15Copyright 2007 © Global Insight, Inc.

Oil Markets: World Oil Reserves

North America5%

South America9%

EuropeEurasia12%

Middle East61%

Africa10%

Asia3%

16Copyright 2007 © Global Insight, Inc.

Oil Markets: Accelerating Declines?

Part of the reason for the struggle of non-OPEC production to grow has been the apparent acceleration of decline rates

Acceleration can perhaps best be illustrated in areas with relatively little new field development

The graph at the right shows acceleration from 1% p.a. decline to nearly 5% in a relatively few short years

Aging fields, better technology and rate acceleration economics appear to be the culprits

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006-6.00%

-5.00%

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

MB

OP

D

Year-on

-Year D

ecline (%

)

17Copyright 2007 © Global Insight, Inc.

Oil Markets: …the Resource Base Is Not the Issue

Conventional oil and gas reserves continue at stable levels of the last several years

Unconventional resources are huge with costs largely below oil prices of the last six months

Conventional oil supplies and reserves heavily concentrated in high risk countries

Low spare capacity has focused the market’s attention on real and perceived risk of oil exporters

18Copyright 2007 © Global Insight, Inc.

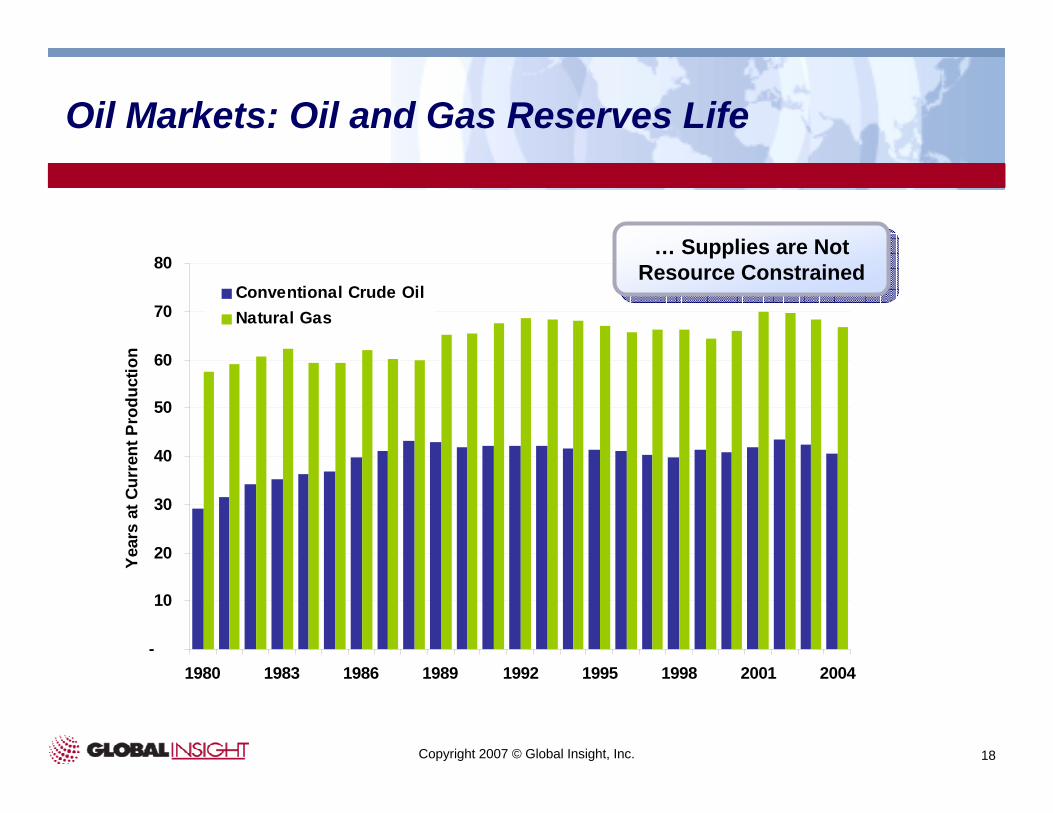

Oil Markets: Oil and Gas Reserves Life

-

10

20

30

40

50

60

70

80

1980 1983 1986 1989 1992 1995 1998 2001 2004

Year

s at

Cur

rent

Pro

duct

ion

Conventional Crude OilNatural Gas

… Supplies are Not Resource Constrained… Supplies are Not

Resource Constrained

19Copyright 2007 © Global Insight, Inc.

Oil Markets: Potential Canadian Heavy Oil Capacity: Market Re-Managed

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Hea

vy O

il Ef

fect

ive

Cap

acity

(M

BO

PD

)

MiningIn-Situ

Source: Canadian Association of Petroleum Producers, National Energy Board, various industry and company publications, ECG

FORECAST