the outlook for the gulf projects market - oecd.org outlook for the gulf projects market the...

TRANSCRIPT

The outlook for the Gulf projects

market

The Confederation of Danish Industry’s

Middle East Day, Copenhagen

7 December, 2011

Angus Hindley,

MEED Research Director

MEED Insight

MEED Insight is a bespoke research service brought to you by the MEED group (www.meed.com). Providing tailor-made research, data and analysis, MEED Insight draws on our data-rich archives and unique

relationships with key business decision-makers across the Middle East.

For information on MEED Insight, please contact [email protected]

GCC WASTEWATER

2009

SELECTED REPORTS

POWER & WATER

IN GCC

OUR EXPERTISE

INDUSTRY &

SECTOR

SCOPING

MARKET

SURVEYSEVALUATION &

FORECASTING

MARKET

ENTRY

STRATEGY

PROJECT

OVERVIEW &

COMPETITIVE

ANALYSIS

Agenda

The impact of the Arab spring

The drivers for capital investment in infrastructure

The opportunities, challenges and procurement trends

The recent performance of the Gulf projects market

Closing remarks

2011, the year of the Arab spring

Morocco

Political reforms

announced

Tunisia

Revolution and

regime change

Egypt

Revolution and

regime change

Syria

Serious civil unrest

Kuwait

Minor

demonstrations

Bahrain

Serious civil

unrest

Jordan

Political reforms

announced

Libya

Revolution and

regime change

Yemen

Serious civil

unrest

Saudi Arabia

Minor

demonstrations

Oman

Minor

demonstrations

In the GCC, serious political unrest has been confined to, and contained in, Bahrain. In

the rest of the Middle East and North Africa, regime change has taken place in three

states and civil war in two more

The carrot and stick approach in the Gulf

GCC troops sent into Bahrain in March 2011 to effectively seal the island state, in

a move accompanied by a $10bn aid package

Massive pay increases announced for government employees across most of the

GCC

Major spending programmes announced to remove any potential flashpoints

- Saudi Arabia launches 500,000 unit housing programme and new

employment rules to create 1.1 million jobs by 2014

- Oman unveils anti-corruption drive and pledges to create 40,000 jobs a year

- the UAE pledges to improve infrastructure in the northern emirates, which is

well below the standards in Abu Dhabi and Dubai

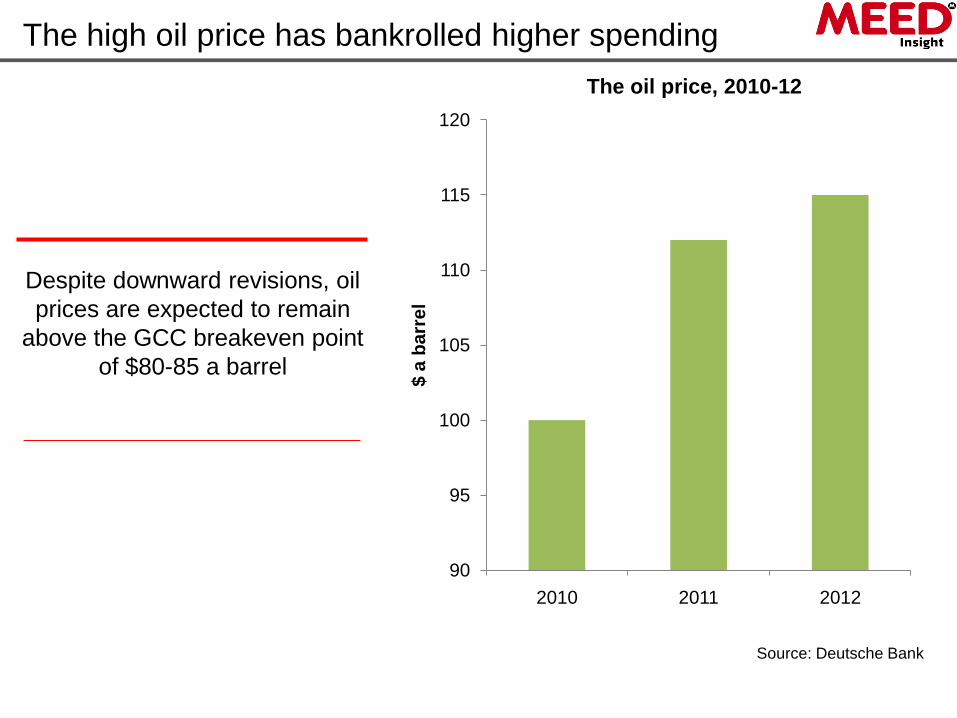

The high oil price has bankrolled higher spending

Despite downward revisions, oil

prices are expected to remain

above the GCC breakeven point

of $80-85 a barrel

Source: Deutsche Bank

90

95

100

105

110

115

120

2010 2011 2012

$ a

ba

rre

l

The oil price, 2010-12

The economic impact of the Arab spring

Outside the regime change states of Egypt, Tunisia and Libya, economic

growth will rise in 2011 due to increased public spending and higher oil

prices

Source: IMF

GDP growth in selected MENA countries, 2010-12

0

2

4

6

8

10

12

14

16

18

20

Egypt Iraq Jordan Kuwait Oman Qatar Saudi Arabia

Tunisia UAE

%

2010 2011 2012

The drivers for increased public expenditure

All MENA states have high

demographic rates, most

notably in Qatar where the

population doubled in the five

years to 2009

Source: IMF

Population growth in selected MENA states, 2010

0

2

4

6

8

10

12

Iraq Kuwait Libya Oman Qatar Saudi Arabia

UAE

%

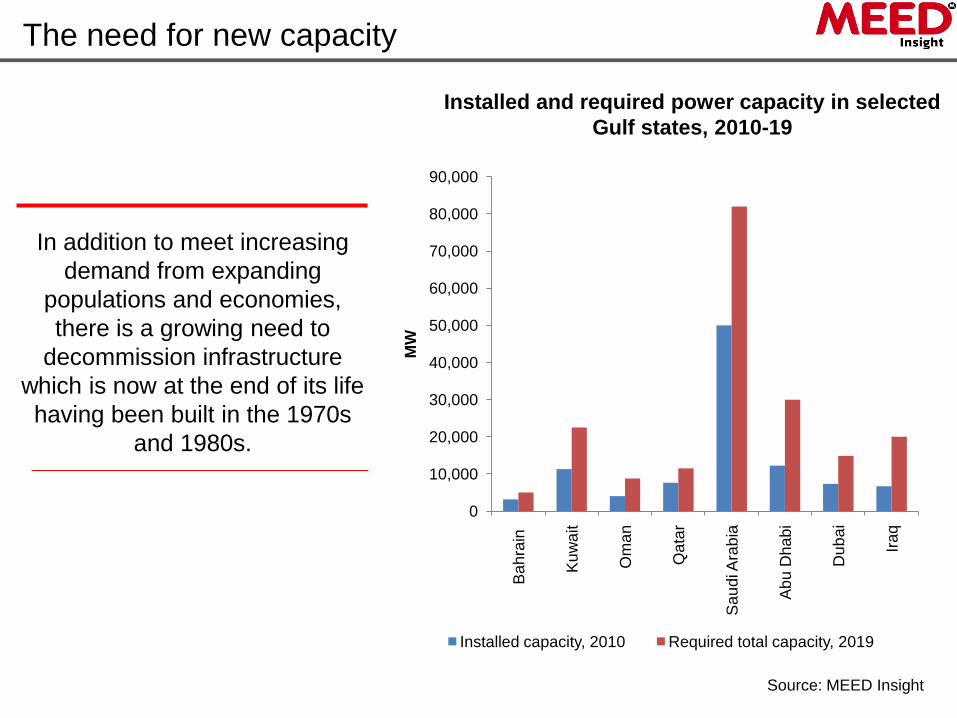

The need for new capacity

In addition to meet increasing

demand from expanding

populations and economies,

there is a growing need to

decommission infrastructure

which is now at the end of its life

having been built in the 1970s

and 1980s.

Source: MEED Insight

Installed and required power capacity in selected

Gulf states, 2010-19

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Ba

hra

in

Ku

wa

it

Om

an

Qa

tar

Sa

ud

i Ara

bia

Ab

u D

ha

bi

Du

ba

i

Iraq

MW

Installed capacity, 2010 Required total capacity, 2019

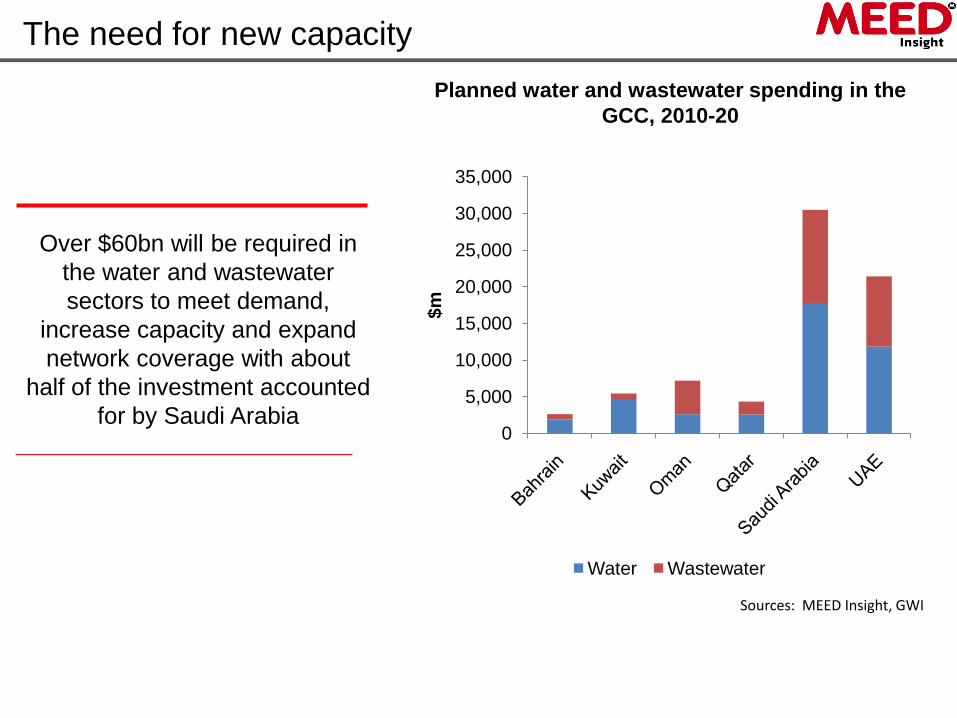

The need for new capacity

Over $60bn will be required in

the water and wastewater

sectors to meet demand,

increase capacity and expand

network coverage with about

half of the investment accounted

for by Saudi Arabia

Sources: MEED Insight, GWI

Planned water and wastewater spending in the

GCC, 2010-20

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

$m

Water Wastewater

The need for new capacity

Aviation Rail Roads Ports Total

Bahrain 4,900 7,900 1,217 860 14,877

Kuwait 3,389 14,000 8,159 2,660 28,208

Oman 12,604 2,500 9,992 7,928 33,024

Qatar 15,246 36,875 7,167 11,474 70,762

Saudi

Arabia 19,567 40,656 4,132 9,100 73,455

UAE 8,732 17,498 25,831 3,783 55,844

Planned transportation projects by GCC state ($m)

Over $275bn of transportation projects are planned with rail accounting for

the largest share of the total at $120bn

Source: MEED Projects

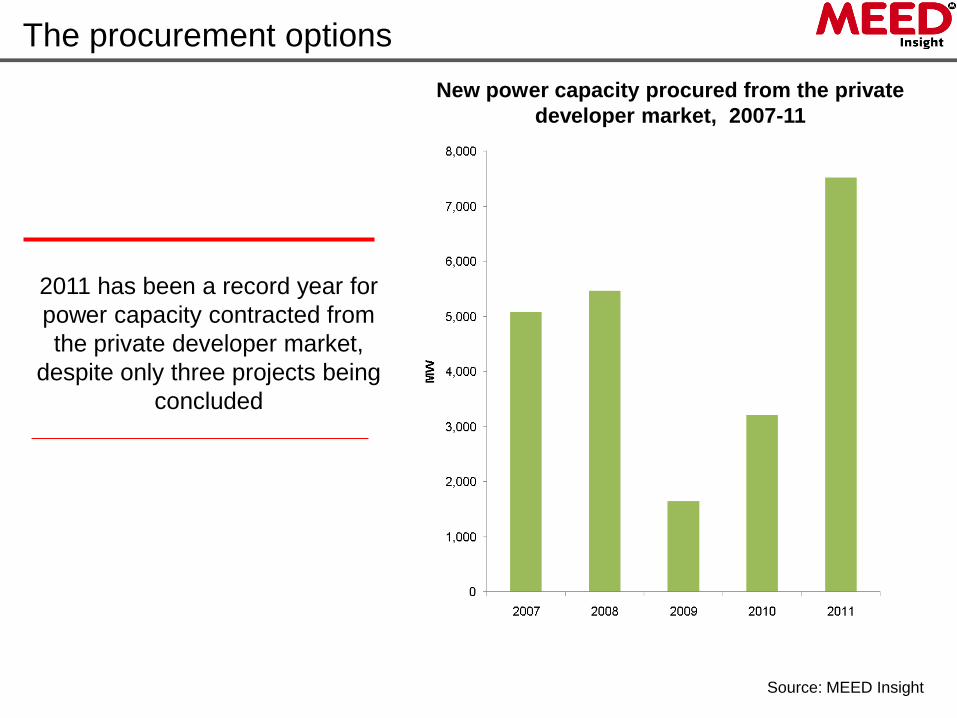

The procurement options

2011 has been a record year for

power capacity contracted from

the private developer market,

despite only three projects being

concluded

Source: MEED Insight

New power capacity procured from the private

developer market, 2007-11

The procurement options

Outside the power and desalination sector, the prospects for private

procurement are very mixed

Successful PPP type projects have been few and far between in the last two

years with the notable exceptions of the Al-Muharraq STP in Bahrain and

Medina airport in Saudi Arabia

Abu Dhabi has effectively abandoned the approach for its social infrastructure

programme, as well on flagship transportation projects such as the midfield

terminal and Mafraq-Ghuweifat highway

Kuwait’s Partnerships Technical Bureau (PTB) has over 30 large-scale

infrastructure projects planned as PPPs but much will depend on how the Al-

Zour north IWPP proceeds

National Water Company (NWC) is revisiting the BOT model for its $30bn

capital investment programme, with the aim of tendering its first project in 2013

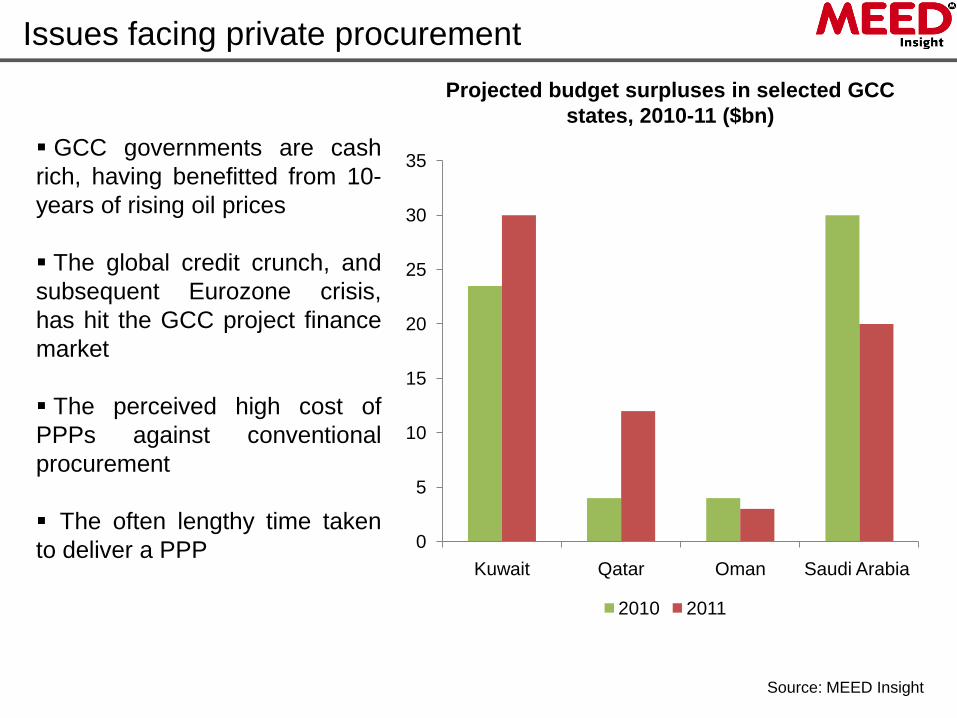

Issues facing private procurement

GCC governments are cash

rich, having benefitted from 10-

years of rising oil prices

The global credit crunch, and

subsequent Eurozone crisis,

has hit the GCC project finance

market

The perceived high cost of

PPPs against conventional

procurement

The often lengthy time taken

to deliver a PPP

Source: MEED Insight

Projected budget surpluses in selected GCC

states, 2010-11 ($bn)

0

5

10

15

20

25

30

35

Kuwait Qatar Oman Saudi Arabia

2010 2011

The recent performance of the Gulf projects market

Major contract awards in the Gulf, 2010-11*

2010* 2011*

Bahrain 2.4 1.3

Iraq 8.4 24.2

Kuwait 10.1 7.8

Oman 4.4 4.7

Qatar 10.5 10.9

Saudi Arabia 35.7 47.1

UAE 30.1 16.8

* first nine months

Source: MEED Projects

Saudi Arabia has maintained its position as the largest projects market in the MENA

region in 2011 while Iraq has seen the biggest growth

The challenges facing the Gulf market

Intense competition for new work, driven by the downturn in the UAE and

companies entering the region for the first time

Lower margins and potentially rising subcontractor and equipment costs in

selected markets

Slow decision-making in some markets particularly in Abu Dhabi

Increased risk being placed on the shoulders of contractors

Growing pressure to be local, especially in Oman and Saudi Arabia

The opportunities on offer in the Gulf

An estimated $1.1tn of project

work is at the planning, design

or tendering stage in the Gulf

Source: MEED Projects

Planned and unawarded projects in the Gulf,

November 2011 ($bn)

0

50

100

150

200

250

300

Bahra

in

Ira

q

Ku

wa

it

Om

an

Qa

tar

Sa

ud

i Ara

bia

UA

E

$b

n

The opportunities on offer

Infrastructure and construction

projects will account for the

majority of future work in the

Gulf followed by oil and gas

Planned and unawarded projects in the Gulf by

sector, November 2011 ($bn)

Source: MEED Projects

467

330

217

130

Oil & gas Construction Infrastructure Others

Closing Remarks

The outlook for the Gulf construction sector is reasonable, considering the

Arab spring, the global economic downturn and the European financial crisis

The engine of growth will be infrastructure, which will be largely

government-financed, provided oil prices remain above the critical $80

threshold

Saudi Arabia will be the most important market, with Iraq and Kuwait having

potential for strong growth

Competition for new work will remain intense and bureaucratic, localisation

and security/political issues will have to be overcome in some markets

Keys to contractor success will be a long-term commitment to the region,

competitive pricing and a willingness to go increasingly local

For more information on this presentation or any

MEED services, please contact:

Angus Hindley, Research Director, MEED

Mob: +44 7918 166446