the philippines’ performance in doing business 2008 kim s. jacinto-henares september 26, 2007

TRANSCRIPT

The Philippines’ Performance in Doing Business 2008

Kim S. Jacinto-HenaresSeptember 26, 2007

2

IFC and the World Bank: Part of the World Bank Group

IFC and the World Bank: Part of the World Bank Group

International Bank for Reconstruction and

Development (IBRD orWorld Bank), 1945

International Development Association, 1960

Multilateral Investment Guarantee Agency, 1988

IFC is owned by its 179 member countries, which collectively determine policies.

International Centre for Settlement of

Investment Disputes, 1966

International Finance Corporation

3

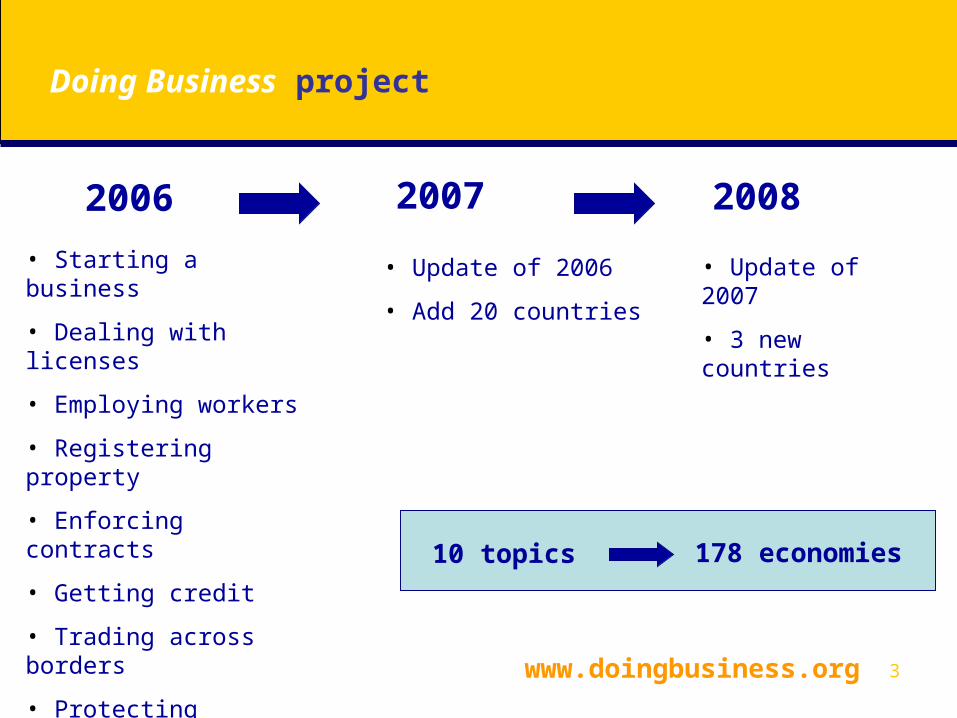

Doing Business project

• Starting a business

• Dealing with licenses

• Employing workers

• Registering property

• Enforcing contracts

• Getting credit

• Trading across borders

• Protecting investors

• Paying taxes

• Closing a business

2006 2007 2008

www.doingbusiness.org

• Update of 2006

• Add 20 countries

• Update of 2007

• 3 new countries

10 topics 178 economies

4

What is the Doing Business report?

• Presents quantitative indicators, empirical data set on business regulations & their enforcement

• Highlights the extent of obstacles to doing business

• Helps identifies the source of those obstacles• Helps identifies what reforms are needed and

provides advice on how to start the process • Highlights best practices in how to reform• An objective benchmark against which to

measure regulatory performance in comparison to other economies

5

Doing Business indicators measure

• Degree of regulation (e.g. no. of procedures to start a business or register commercial property)

• Regulatory outcomes (e.g. time & cost to enforce a contract, go through bankruptcy or trade across borders)

• Extent of legal protections of property (e.g. protections of investors against looting by company directors or the range of assets that can be used as collateral)

• Flexibility of employment regulation

• Tax burden on businesses

6

What Doing Business indicators don’t measure

• Macroeconomic policy

• Currency volatility

• Ease of access to markets

• Proximity to large markets

• Quality of infrastructure services (other than those related to ‘Trading across borders’)

• Investor perceptions

• Crime rate

• Security of property from theft & looting

• Transparency of government procurement

• Bribes

• Underlying strength of institutions

7

Doing Business 2008 Overall Ranking

TopicPhils

RankingWorld’s Best

Ease of doing business 133 Singapore

Trading across borders 57 Singapore

Dealing with licenses 77 St. Vincent & the Grenadines

Registering property 86 New Zealand

Getting credit 97 United Kingdom

Enforcing contracts 113 Hong Kong, China

Employing workers 122 United States

Paying taxes 126 Maldives

Protecting investors 141 New Zealand

Starting a business 144 Australia

Closing a business 147 Japan

Overall Doing Business ranking is based on an

average of the averages of the 10 topics.

Ranking on each topic is the simple average of

rankings on its component indicators.

8

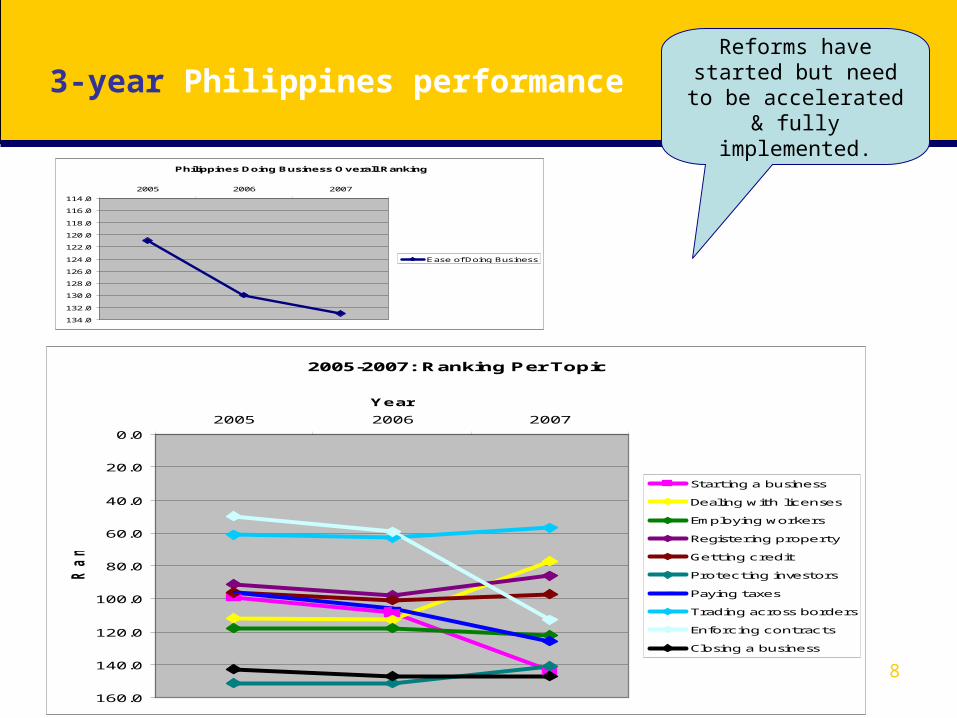

3-year Philippines performanceReforms have started

but need to be accelerated & fully

implemented.

2005-2007: Ranking Per Topic

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2005 2006 2007

Year

Ra

nk

Starting a business

Dealing with licenses

Employing workers

Registering property

Getting credit

Protecting investors

Paying taxes

Trading across borders

Enforcing contracts

Closing a business

Philippines Doing Business Overall Ranking

114.0

116.0

118.0

120.0

122.0

124.0

126.0

128.0

130.0

132.0

134.0

2005 2006 2007

Ease of Doing Business

9

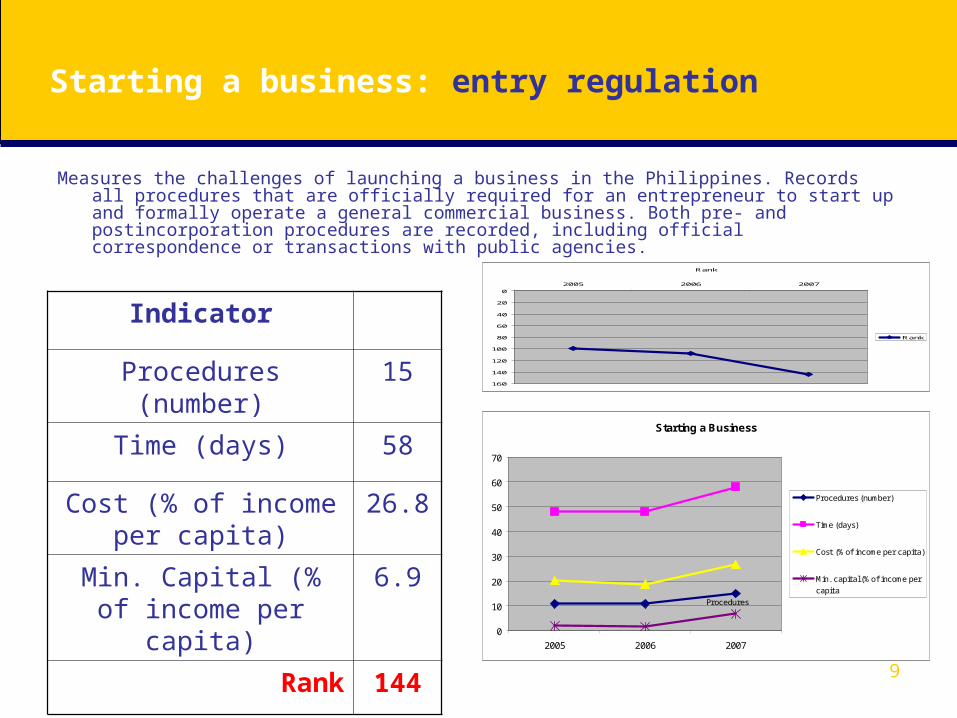

Starting a business: entry regulation

Measures the challenges of launching a business in the Philippines. Records all procedures that are officially required for an entrepreneur to start up and formally operate a general commercial business. Both pre- and postincorporation procedures are recorded, including official correspondence or transactions with public agencies.

Indicator

Procedures (number) 15

Time (days) 58

Cost (% of income per capita)

26.8

Min. Capital (% of income per capita)

6.9

Rank 144

Rank

0

20

40

60

80

100

120

140

160

2005 2006 2007

Rank

Starting a Business

0

10

20

30

40

50

60

70

2005 2006 2007

Procedures (number)

Time (days)

Cost (% of income per capita)

Min. capital (% of income per

capita

Procedures

Time

Cost

Min. capital

10

Dealing with licenses: operations regulations

Measures the requirements for ongoing operations in the Philippines.Records all procedures that are officially required for a business in

the construction industry to build a standardized warehouse.

Indicator

Procedures (number) 21

Time (days) 177

Cost (% of income per capita)

75.9

Rank 77

Dealing with Licenses

0

50

100

150

200

250

2005 2006 2007

Procedures (number)

Time (days)

Cost (% of income per capita)

Procedures

Time

Cost

Rank

0

20

40

60

80

100

120

2005 2006 2007

Rank

11

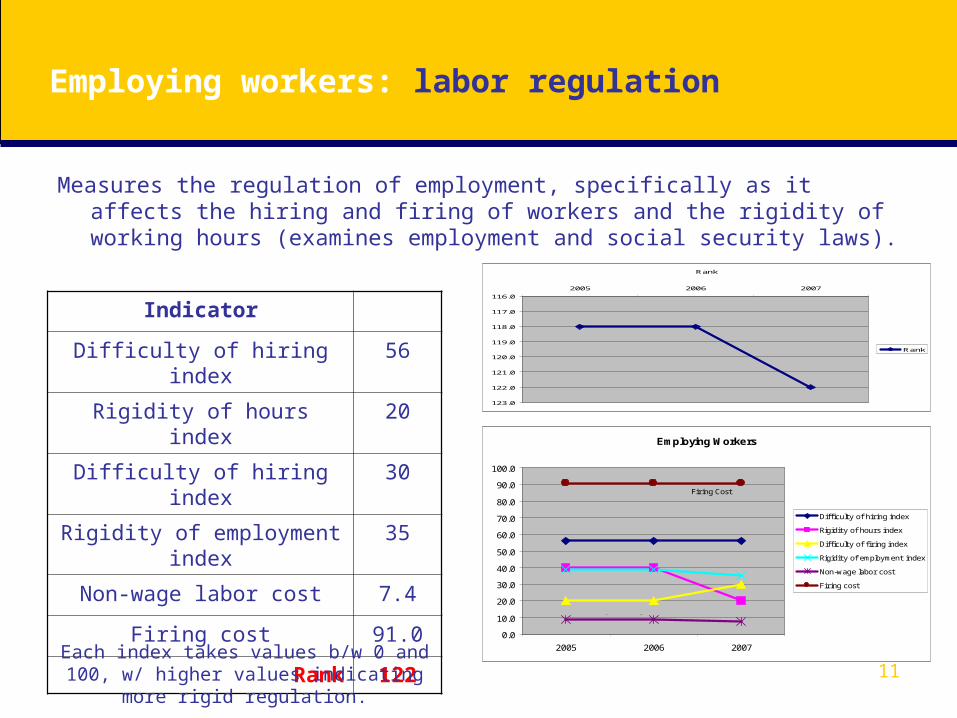

Employing workers: labor regulation

Measures the regulation of employment, specifically as it affects the hiring and firing of workers and the rigidity of working hours (examines employment and social security laws).

Indicator

Difficulty of hiring index 56

Rigidity of hours index 20

Difficulty of hiring index 30

Rigidity of employment index

35

Non-wage labor cost 7.4

Firing cost 91.0

Rank 122

Each index takes values b/w 0 and 100, w/ higher values indicating more rigid

regulation.

Employing Workers

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

2005 2006 2007

Difficulty of hiring index

Rigidity of hours index

Difficulty of firing index

Rigidity of employment index

Non-wage labor cost

Firing cost

Firing Cost

Difficulty of Hiring Index

Rigidity of employment Index

Rigidity of hours index

Difficulty of Firing Index

Non-wage Labor Cost

Rank

116.0

117.0

118.0

119.0

120.0

121.0

122.0

123.0

2005 2006 2007

Rank

12

Registering property: regulation of property transfers

Measures the ease of registering property based on a standard case of an entrepreneur who wants to purchase land and a building. Records the full sequence of procedures necessary to transfer the title from the seller to the buyer.

Indicator

Procedures (number) 8

Time (days) 33

Cost (% of property value)

4.2

Rank 86

Registering Property

0

5

10

15

20

25

30

35

2005 2006 2007

Procedures (number)

Time (days)

Cost (% of property value)

Procedures

Cost

Time

Rank

80

82

84

86

88

90

92

94

96

98

100

2005 2006 2007

Rank

13

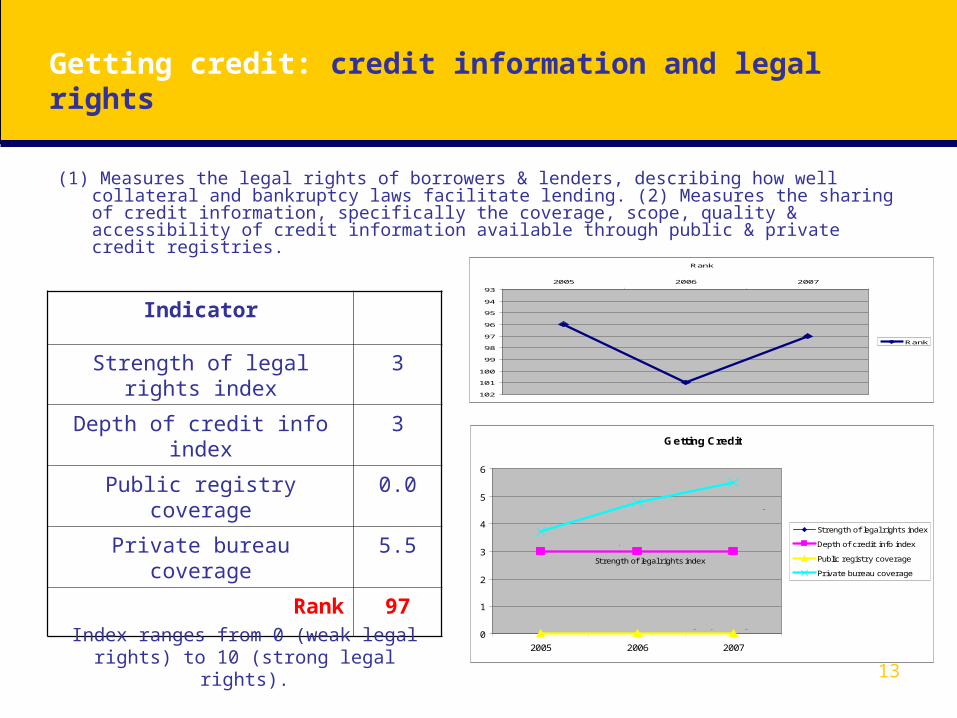

Getting credit: credit information and legal rights

(1) Measures the legal rights of borrowers & lenders, describing how well collateral and bankruptcy laws facilitate lending. (2) Measures the sharing of credit information, specifically the coverage, scope, quality & accessibility of credit information available through public & private credit registries.

Indicator

Strength of legal rights index

3

Depth of credit info index 3

Public registry coverage 0.0

Private bureau coverage 5.5

Rank 97

Index ranges from 0 (weak legal rights) to 10 (strong legal rights).

Getting Credit

0

1

2

3

4

5

6

2005 2006 2007

Strength of legal rights index

Depth of credit info index

Public registry coverage

Private bureau coverage

Strength of legal rights index

Depth of credit info index

Public registry coverage

Private bureau coverage

Rank

93

94

95

96

97

98

99

100

101

102

2005 2006 2007

Rank

14

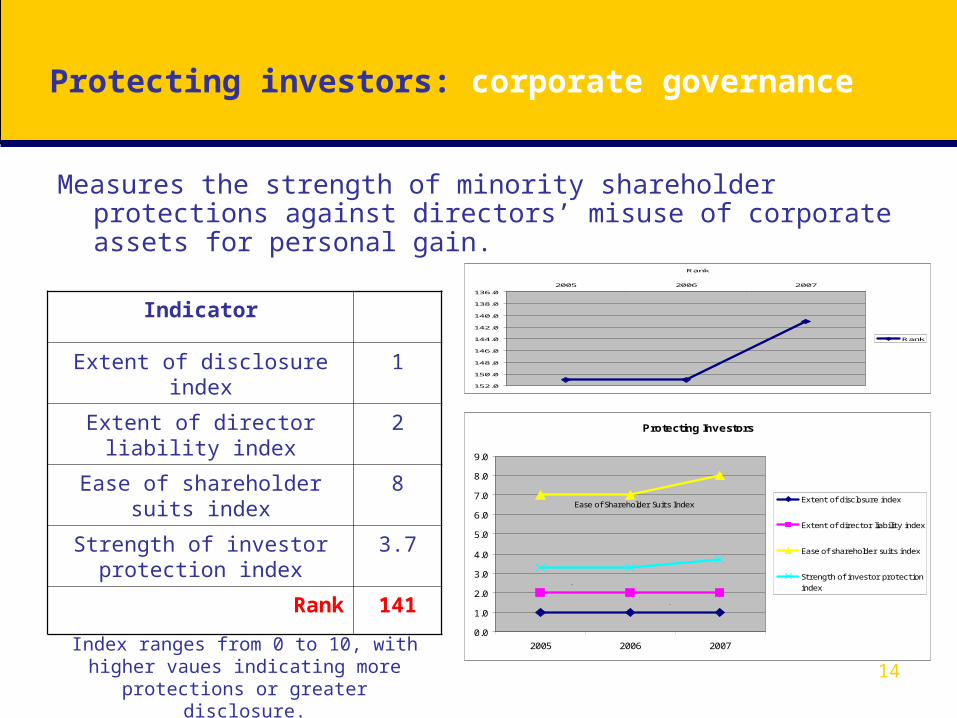

Protecting investors: corporate governance

Measures the strength of minority shareholder protections against directors’ misuse of corporate assets for personal gain.

Indicator

Extent of disclosure index 1

Extent of director liability index

2

Ease of shareholder suits index

8

Strength of investor protection index

3.7

Rank 141

Index ranges from 0 to 10, with higher vaues indicating more protections or

greater disclosure.

Protecting Investors

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2005 2006 2007

Extent of disclosure index

Extent of director liability index

Ease of shareholder suits index

Strength of investor protection

index

Ease of Shareholder Suits Index

Strength of Investor Protection Index

Extent of Director Liability Index

Extent of Disclosure Index

Rank

136.0

138.0

140.0

142.0

144.0

146.0

148.0

150.0

152.0

2005 2006 2007

Rank

15

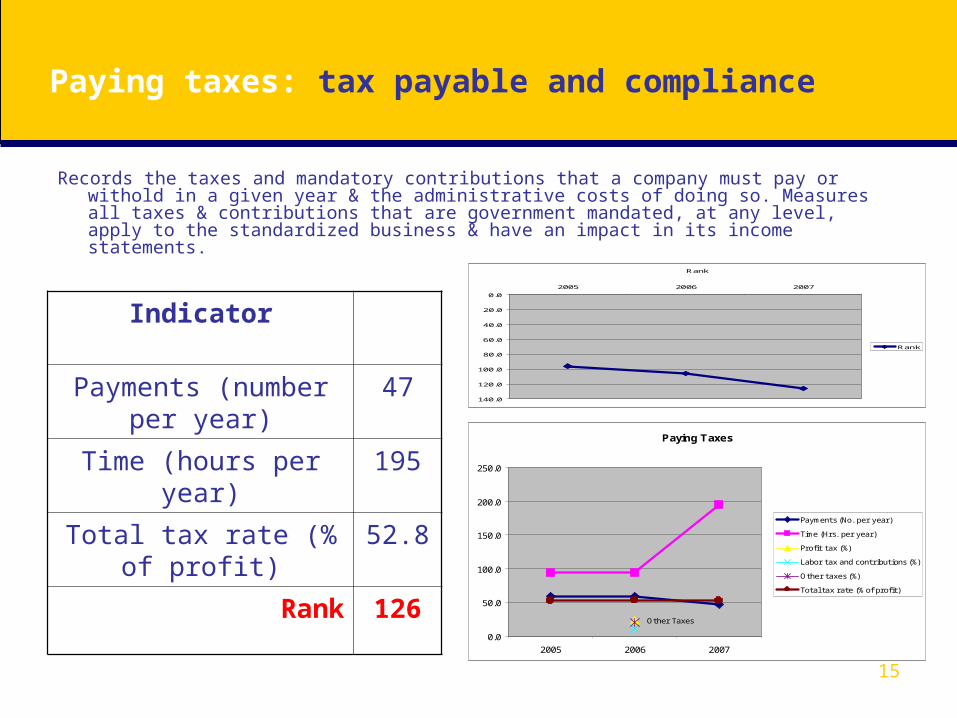

Paying taxes: tax payable and compliance

Records the taxes and mandatory contributions that a company must pay or withold in a given year & the administrative costs of doing so. Measures all taxes & contributions that are government mandated, at any level, apply to the standardized business & have an impact in its income statements.

Indicator

Payments (number per year)

47

Time (hours per year)

195

Total tax rate (% of profit)

52.8

Rank 126

Paying Taxes

0.0

50.0

100.0

150.0

200.0

250.0

2005 2006 2007

Payments (No. per year)

Time (Hrs. per year)

Profit tax (%)

Labor tax and contributions (%)

Other taxes (%)

Total tax rate (% of profit)

Other TaxesLabor Tax and Contributions

Payments

Total Tax Rate

Time

Rank

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2005 2006 2007

Rank

16

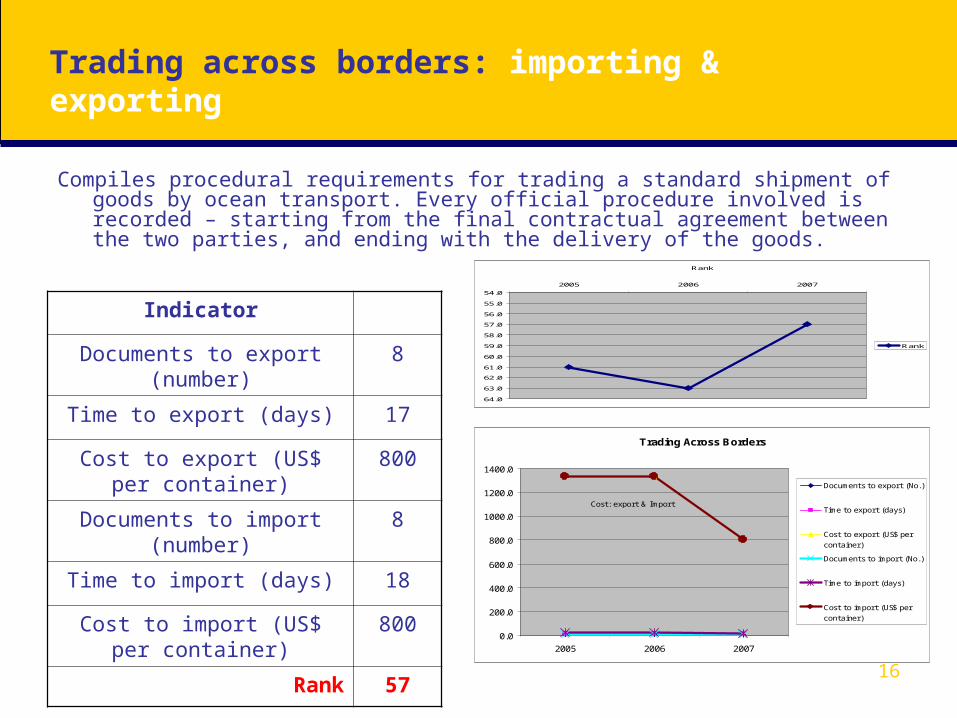

Trading across borders: importing & exporting

Compiles procedural requirements for trading a standard shipment of goods by ocean transport. Every official procedure involved is recorded – starting from the final contractual agreement between the two parties, and ending with the delivery of the goods.

Indicator

Documents to export (number)

8

Time to export (days) 17

Cost to export (US$ per container)

800

Documents to import (number)

8

Time to import (days) 18

Cost to import (US$ per container)

800

Rank 57

Trading Across Borders

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

2005 2006 2007

Documents to export (No.)

Time to export (days)

Cost to export (US$ percontainer)

Documents to import (No.)

Time to import (days)

Cost to import (US$ percontainer)

Cost: export & Import

Rank

54.0

55.0

56.0

57.0

58.0

59.0

60.0

61.0

62.0

63.0

64.0

2005 2006 2007

Rank

17

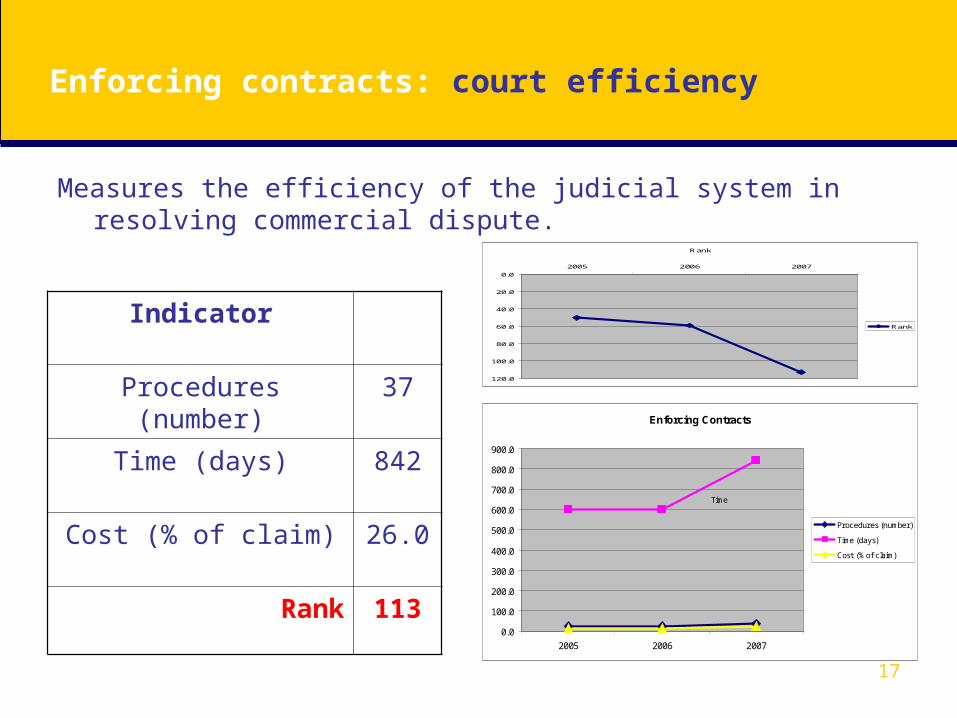

Enforcing contracts: court efficiency

Measures the efficiency of the judicial system in resolving commercial dispute.

Indicator

Procedures (number) 37

Time (days) 842

Cost (% of claim) 26.0

Rank 113

Enforcing Contracts

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

2005 2006 2007

Procedures (number)

Time (days)

Cost (% of claim)

Time

Procedures Cost

Rank

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2005 2006 2007

Rank

18

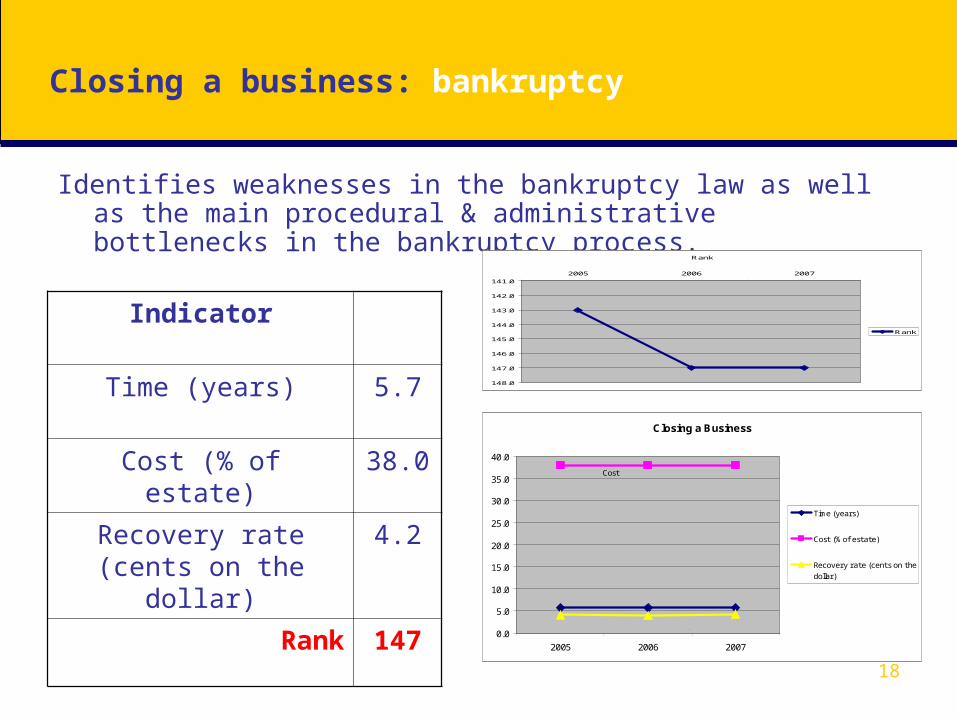

Closing a business: bankruptcy

Identifies weaknesses in the bankruptcy law as well as the main procedural & administrative bottlenecks in the bankruptcy process.

Indicator

Time (years) 5.7

Cost (% of estate) 38.0

Recovery rate (cents on the dollar)

4.2

Rank 147

Rank

141.0

142.0

143.0

144.0

145.0

146.0

147.0

148.0

2005 2006 2007

Rank

Closing a Business

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2005 2006 2007

Time (years)

Cost (% of estate)

Recovery rate (cents on thedollar)

Cost

Time

Recovery Rate

19

Philippines Reform

1. Starting a business – entry regulation2. Registering property – property registration3. Getting credit – access to credit

1. Dealing with licenses – operations regulation2. Trading across borders – importing &

exporting

1. Protecting investors – corporate governance2. Closing a business - bankruptcy

1. Paying taxes – tax payable & compliance2. Enforcing contracts – court efficiency3. Employing workers – labor regulation

Get basics right

Fully implement quick wins

Build on strategic priorities

Remain opportunistic

20

Philippines Reform: (1) Get basics right – TARGET NOW

• Cut the minimum capital req’t• Introduce a one-stop shop (e.g.

merge procedures, delegate tax registration to company registrar)

• Allow online start-up

• Simplify & lower fees• Introduce fast-track procedures• Make the registry electronic• Make the use of notaries optional

• Expand the range of information available in credit registries

• Eliminate legal obstacles to sharing credit information

• Allow all types of assets to be used as collateral

• Establish unified registries for all collaterals

• Phils Business Registry (DTI, NCC)

• SEC & BIR data exchange (pre-registered TIN) (SEC, BIR)

• Anti-Red Tape Law (June 2007) (ARTTF, PAGC)

• One Time Tax Transaction (ONETT) project (BIR)

• LAMP2 project* (DENR)• Land Administration and

Reform Act (LARA) bill; LEDAC priority*

• Credit Information System (CIS) bill; LEDAC priority

Starting a business

Registering property

Getting credit

Successful reformsPhils reform pipeline

*medium-long term reform executive action

Immediate/ short-term reforms; high impact.

21

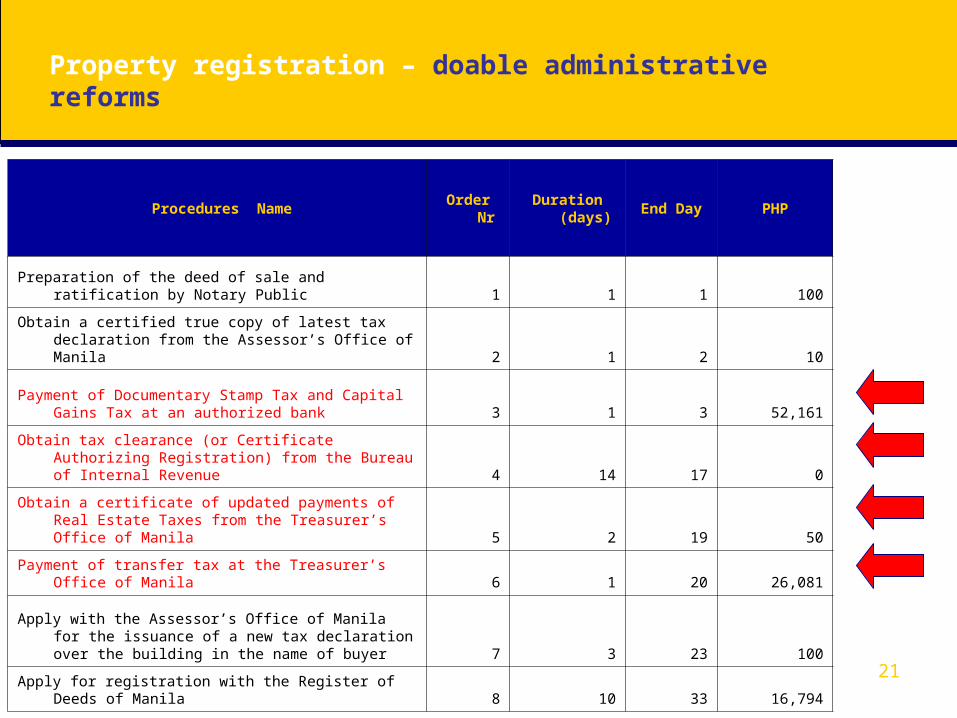

Property registration – doable administrative reforms

Procedures NameOrder

NrDuration

(days)End Day PHP

Preparation of the deed of sale and ratification by Notary Public 1 1 1 100

Obtain a certified true copy of latest tax declaration from the Assessor’s Office of Manila 2 1 2 10

Payment of Documentary Stamp Tax and Capital Gains Tax at an authorized bank 3 1 3 52,161

Obtain tax clearance (or Certificate Authorizing Registration) from the Bureau of Internal Revenue 4 14 17 0

Obtain a certificate of updated payments of Real Estate Taxes from the Treasurer’s Office of Manila 5 2 19 50

Payment of transfer tax at the Treasurer’s Office of Manila 6 1 20 26,081

Apply with the Assessor’s Office of Manila for the issuance of a new tax declaration over the building in the name of buyer 7 3 23 100

Apply for registration with the Register of Deeds of Manila 8 10 33 16,794

22

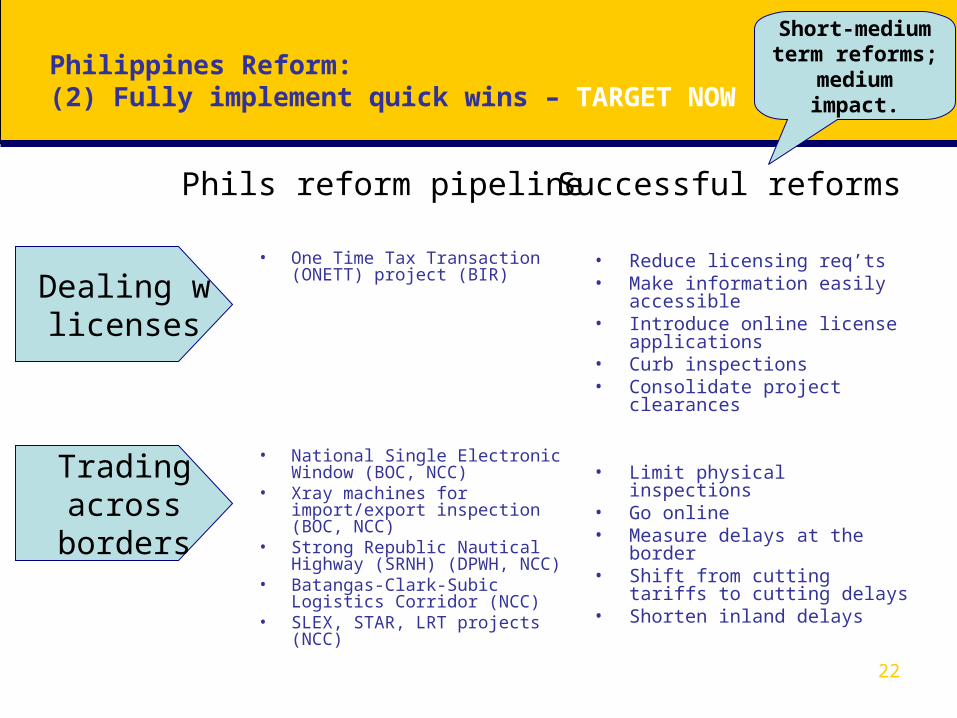

Philippines Reform: (2) Fully implement quick wins – TARGET NOW

• Reduce licensing req’ts• Make information easily

accessible• Introduce online license

applications• Curb inspections• Consolidate project clearances

• Limit physical inspections• Go online• Measure delays at the border• Shift from cutting tariffs to

cutting delays• Shorten inland delays

• One Time Tax Transaction (ONETT) project (BIR)

• National Single Electronic Window (BOC, NCC)

• Xray machines for import/export inspection (BOC, NCC)

• Strong Republic Nautical Highway (SRNH) (DPWH, NCC)

• Batangas-Clark-Subic Logistics Corridor (NCC)

• SLEX, STAR, LRT projects (NCC)

Dealing w licenses

Trading across borders

Successful reformsPhils reform pipeline

Short-medium term reforms;

medium impact.

23

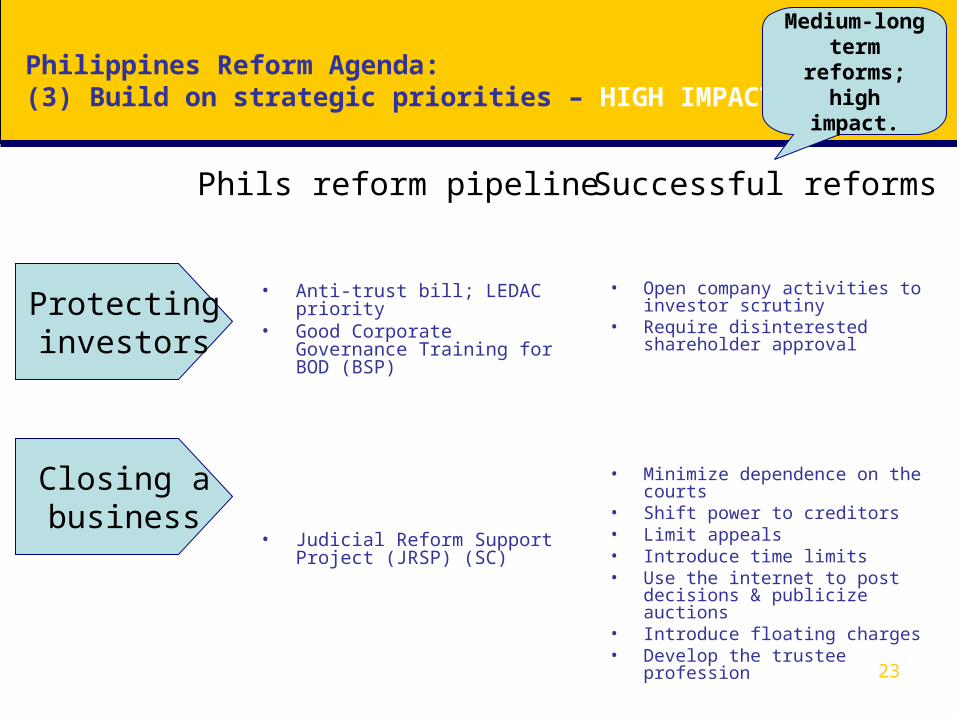

Philippines Reform Agenda: (3) Build on strategic priorities – HIGH IMPACT

• Anti-trust bill; LEDAC priority• Good Corporate Governance

Training for BOD (BSP)

• Judicial Reform Support Project (JRSP) (SC)

• Open company activities to investor scrutiny

• Require disinterested shareholder approval

• Minimize dependence on the courts

• Shift power to creditors• Limit appeals• Introduce time limits• Use the internet to post

decisions & publicize auctions• Introduce floating charges• Develop the trustee

profession

Successful reformsPhils reform pipeline

Closing a business

Protecting investors

Medium-long term reforms; high impact.

24

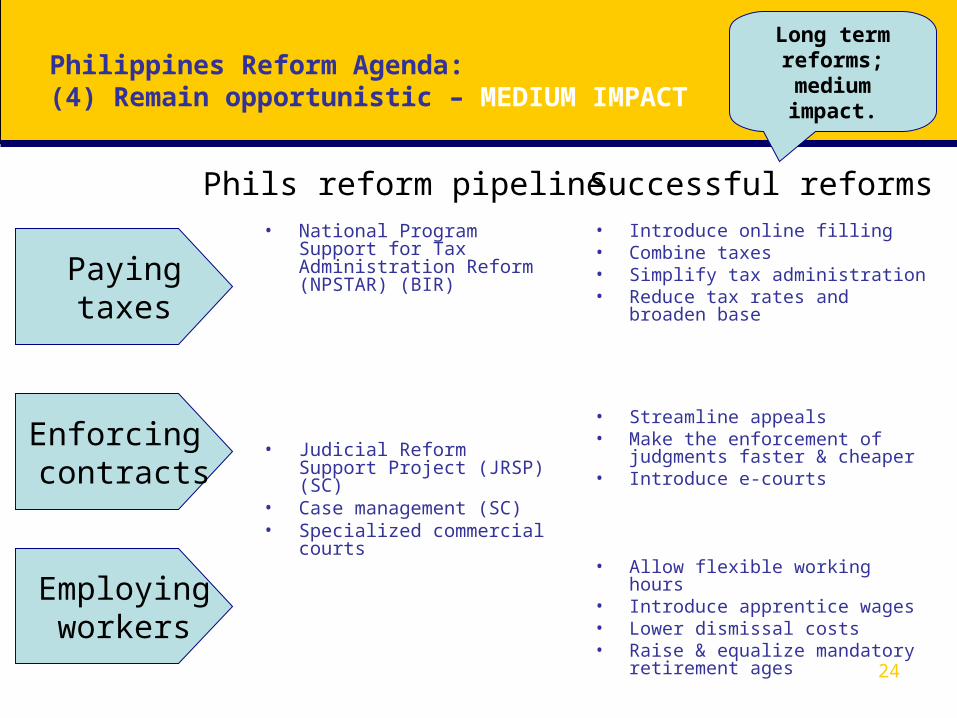

Philippines Reform Agenda: (4) Remain opportunistic – MEDIUM IMPACT

• National Program Support for Tax Administration Reform (NPSTAR) (BIR)

• Judicial Reform Support Project (JRSP) (SC)

• Case management (SC)• Specialized commercial

courts

• Introduce online filling• Combine taxes• Simplify tax administration• Reduce tax rates and broaden

base

• Streamline appeals• Make the enforcement of

judgments faster & cheaper• Introduce e-courts

• Allow flexible working hours• Introduce apprentice wages• Lower dismissal costs• Raise & equalize mandatory

retirement ages

Enforcing contracts

Employing workers

Successful reformsPhils reform pipeline

Paying taxes

Long term reforms; medium

impact.

Doing Business 2008

September 26, 2007

26

Doing Business methodology - some basics

1. Gather all the relevant laws, regulations, decrees, fee schedules

2. Follow the entrepreneur from the beginning to the end of a transaction

3. Record every step of the process, and its time and cost4. The data set for all sets of indicators in Doing Business

2008 are for June 20075. The standardized survey uses a simple business case to

ensure comparability across countries and over time6. Assumptions about the legal form of the business, its size,

location and the nature of its operations7. Surveys are administered through local intermediaries

27

“The need to make assumptions”

‘Starting a Business’

• Considers SME (between 10 and 50 employees)• 100% domestically owned• Start-up capital of 10 times income per capita• Turnover of at least 100 times income per capita• Operates in country’s most populous city• Legal form: limited liability company (LLC)• Simple business operation – general commercial activity• Does not qualify for any special benefits• Does not own real estate• All requirements to incorporate and commence operations

are recorded