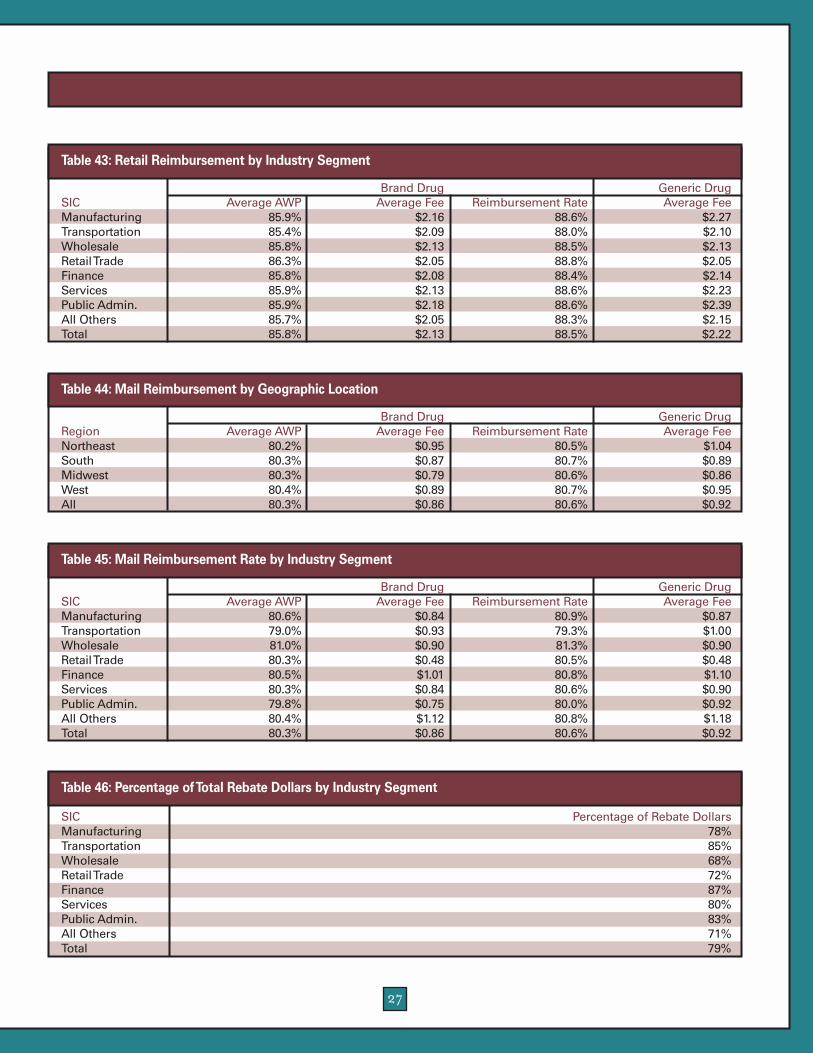

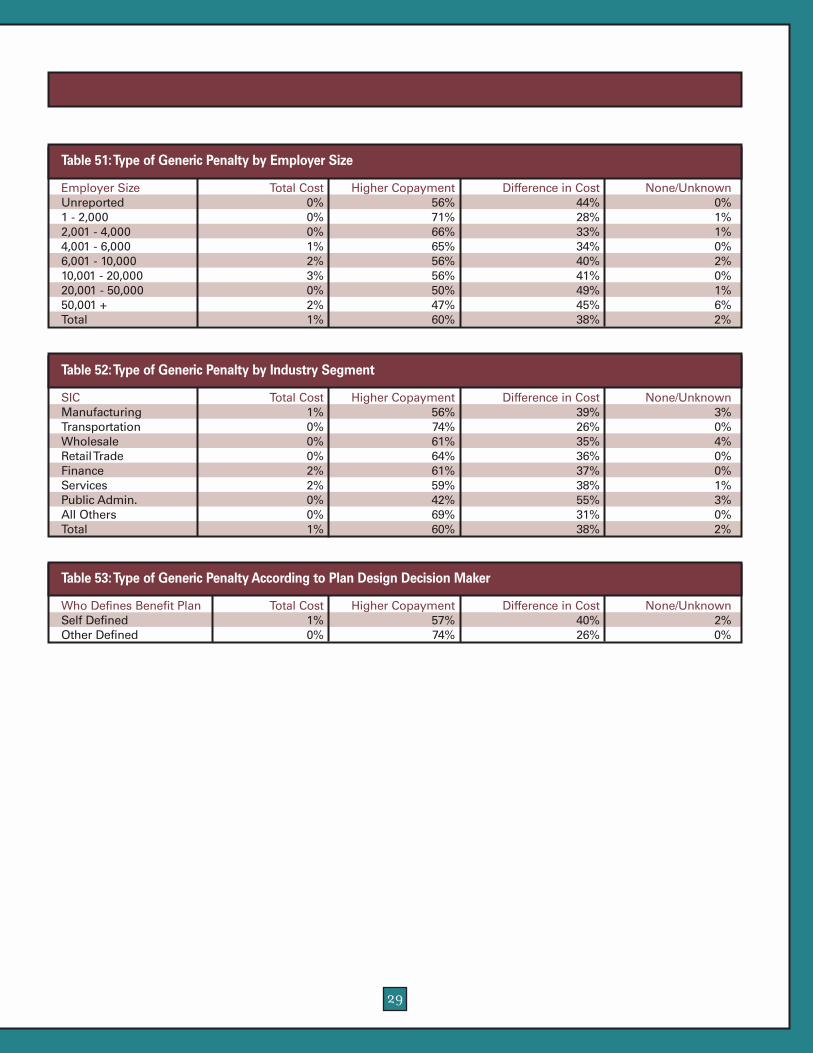

the prescription drug benefit cost and plan design …/media/images/publications/archi… · i dear...

TRANSCRIPT

The Prescription Drug BenefitCost and Plan Design Survey Report

provided by Takeda

2003 Edition

Creating Opportunities With Healthcare Solutions

i

Dear Healthcare Professional:

Takeda Pharmaceuticals America, Inc. is pleased to present you with the 2003 Prescription

Drug Benefit Cost and Plan Design Survey Report. Conducted annually by the Pharmacy Benefit

Management Institute, Inc., the report is based on data collected from 535 employers

(representing approximately 17.4 million beneficiaries). This information provides you

with a comprehensive overview of prescription drug coverage, utilization, and costs. In

addition, we hope you will garner a greater understanding of the current management

trends and issues in pharmacy benefit design.

We value our relationships with healthcare leaders and strive to provide quality products

and services to help you meet your needs. We hope you find the information in this report

useful to your organization. As always, we measure our success based on your success.

Sincerely,

Steve Shockley

National Director of Managed Care Markets

Takeda Pharmaceuticals North America, Inc.

CreatingOpportunities with HealthcareSolutions

Takeda Pharmaceuticals North America, Inc. is creating opportunities to help enhance patient care by providing:

• A comprehensive approach to research and development

• Resources and services designed to meet your needs

• Ongoing support for an evolving healthcare environment

For more information about healthcare solutions that are uniquely Takeda,please call 1-877-872-3700. We look forward to creating a partnership that helps you meet the challenges of healthcare now and in the future.

©2003 Takeda Pharmaceuticals North America, Inc. MC01-0144-1 6/03 Printed in U.S.A.

CONTENTS

Message From Takeda Pharmaceuticals North America, Inc. ............................................................................iMessage From The National Business Coalition on Health ............................................................................viiMessage From The American College of Occupational and Environmental Medicine (ACOEM) ............................x Executive Summary....................................................................................................................................1

Introduction ......................................................................................................................................1Key Findings ......................................................................................................................................1Implications of Findings ......................................................................................................................2

Methodology ............................................................................................................................................3Respondent Demographics ..................................................................................................................3

Research Findings ....................................................................................................................................5Pharmacy Reimbursement....................................................................................................................5

Retail Pharmacy Reimbursement........................................................................................................6Mail Service Pharmacy Reimbursement................................................................................................7

Administrative Fees ............................................................................................................................8Formularies and Rebates......................................................................................................................8

Formulary ....................................................................................................................................8Employer Initiated Formulary Changes ..............................................................................................9Rebates ......................................................................................................................................10

Cost Sharing ....................................................................................................................................10Three-Tier Copayments ................................................................................................................12Four-Tier Copayments ..................................................................................................................12Coinsurance ................................................................................................................................12

Drug Exclusions ................................................................................................................................13OTC Conversions ........................................................................................................................14Mandatory Mail Service ..................................................................................................................14Governmental Requirements ..........................................................................................................14Drug Access Controls ....................................................................................................................14

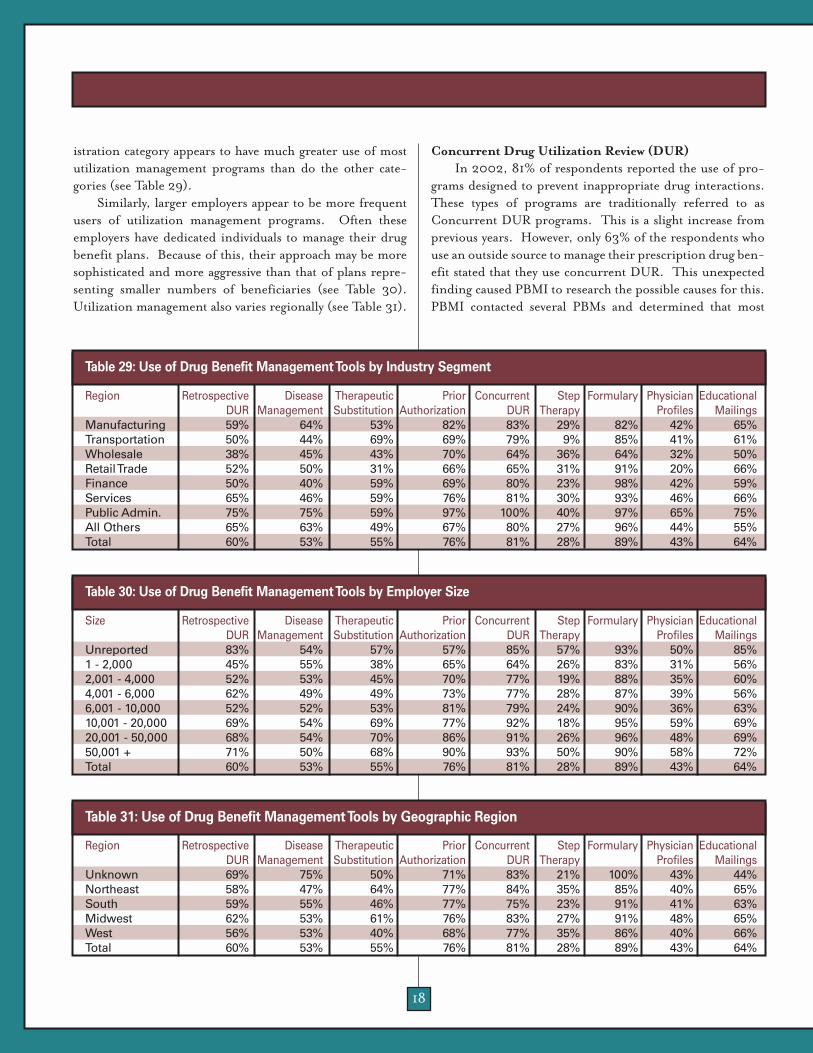

Utilization Management Tools ............................................................................................................16Concurrent Drug Utilization Review..................................................................................................18Retrospective Drug Utilization Review ................................................................................................19Step Therapy................................................................................................................................19Prior Authorization ......................................................................................................................19Therapeutic Substitution ................................................................................................................19Disease Management ......................................................................................................................19

Utilization Patterns...........................................................................................................................20Mail Service Utilization..................................................................................................................20Generic Utilization ......................................................................................................................20

Emerging Cost Containment Strategies ......................................................................................................23Employers Embrace Sophisticated Cost Sharing Designs ..........................................................................23OIG Compliance Guidelines for Drug Industry May be Boon to Employers ................................................24

Appendix: Supplemental Figures and Tables ................................................................................................26Notes....................................................................................................................................................30

iii

Sponsored by:Takeda Pharmaceuticals North America, Inc. 475 Half Day RoadSuite 500Lincolnshire, IL 60069General Offices: (847) 383-3000Customer Service: (877) 582-5332 or (877) 5TAKEDA

For questions relating to the report, please call:Michael H. Deskin, PresidentThe Pharmacy Benefit Management Institute, Inc.PO Box 27831Tempe, AZ 85285-7831Phone: (480) 730-0814Fax: (602) 241-6914Email: [email protected]

For further information relating to this publication, please contact:Kikaku America International2600 Virginia Avenue NW, Suite 517Washington, DC 20037Phone: (202) 338-8256Fax: (202) 337-3496Email: [email protected]

Published by:Wellman Publishing, Inc.6933 Lamar Ave NWAlbuquerque, NM 87120 USAPhone: (505) 890-6723Fax: (505): 899-4008Email: [email protected]

© Copyright 2003 by PBMI, Inc.All rights reserved. No portion of this publication may bereproduced in any format, print, electronic, or otherwise,without the express written permission of PBMI.

Made possible by a grant from Takeda PharmaceuticalsNorth America, Inc.

iv

CO-CHAIRS

EMPLOYER ASSOCIATIONS

v

Kelli MolerDirector, Membership and Government Relations ServicesNational Business Coalition on Health (NBCH)1015 18th Street NW, Suite 730Washington, DC 20036(202) 775-9300Fax: (202) 775-1569Email: [email protected]

Kathleen Y. KleinWEB Executive Director(214) 369-2219Fax: (214) [email protected]

Susan MamolaDirector of Membership American College of Occupational andEnvironmental Medicine (ACOEM)1114 N. Arlington Heights RoadArlington Heights, IL 60004(847) 818-1800, extension 383Fax: (847) 818-9266Email: [email protected]

Raymond J. BruscaVice President of BenefitsThe Black & Decker Corporation

Wayne N. Burton, MDSenior Vice PresidentCorporate Medical DirectorBank OneChicago, Illinois

Tracy CasteubleDirector, HDMA Research & InformationHealthcare Distribution Management AssociationReston, VA

Charles ConnollyClient ExecutiveMarsh USA Inc. Baltimore, MD

Joseph A. DiMasi, PhDDirector of Economic AnalysisTufts Center for the Study of Drug DevelopmentBoston, MA

Christopher V. Goff, JDPresident & CEOEmployers Health PurchasingCorporation of OhioCanton, OH

Paul HansenPrincipalTowers PerrinNew York, NY

Ed KaplanVice-PresidentThe Segal CompanyNew York, NY

Debbie MartinWilliam M. MercerNew York, NY

Laurel Pickering, MPHManaging DirectorThe NY Business Group on Health, Inc.New York, NY

Kevin B. (Kip) Piper, MA, CHEPresidentHealth Results Group LLCFalls Church, VA

Dr. Dennis Richling, MDPresident, Midwest Business Group on HealthChicago, IL

Kenneth G. RobbertNational PresidentWorldwide Employee Benefits Network (WEB)Potomac Falls, VA

Debra Stern, RPhRxperts Managed Care ConsultingIrvine, CA

F. Randy Vogenberg, RPh, PhDVice President & National Practice LeaderAon ConsultingWellesley, MA

Andrew WebberPresident & CEONational Business Coalition on Health (NBCH)1015 18th Street N.W., Suite 730Washington, DC 20036202-775-9300FAX 202-775-1569 Email: [email protected]

Barry S. Eisenberg Executive Director American College of Occupational andEnvironmental Medicine (ACOEM)1114 N. Arlington Heights RoadArlington Heights, IL 60004(847) 818-1800Fax: (847) 818-9266Email: [email protected]

We would like to thank the following individuals for their invaluable expertise in the review of this document:

For additional information please contact:

vi

May 2003

Dear Reader:

As our organization interacts with employers across the country, there seems to be a clear disconnect between how employerspay for health care and the strategies they use to manage health care. Targeted interventions, such as disease management, areincreasingly effective strategy for improving the quality and accountability of health care as well as the cost.

Members of the National Business Coalition on Health (NBCH) have been exploring the business case for disease manage-ment, including the barriers for high-risk populations, employer return on investment, as well as the impact on the national

health care system. In fact, last spring NBCH published "Changes in How Employers ManageHealth Care–A Closer Look at Disease Management," which provides in-depth employer per-spective on workable solutions to care management issues and finding financial and humanresource value in those solutions.

While NBCH is a national authority on how employers buy, manage and pay for health care, it isour employer coalition members who in their local market are paving the way toward betterhealth care outcomes.

The South Central Michigan Health Alliance (SCMHA) in Ann Arbor started a safety and qual-ity project last year in which stakeholders are examining the prevalence of errors and qualityimprovement opportunities in outpatient prescriptions. The project will organize inter-planstrategies for error prevention and quality improvement opportunities for the outpatient in the

pharmacy setting. SCMHA found that the relatively high rate of errors present in the seemingly controlled hospital settingresulted in inter-plan interest in documenting the extent of suspected errors and launching interventions in the outpatientsetting, where coordination of services is virtually non-existent and mistakes are more frequent than the hospital setting,resulting in harm to consumers.

SCMHA along with participating member employers, providers, pharmacy benefit managers, retail pharmacy chains and all ofthe dominant Michigan health plans, have finalized categories of error that merit formal outpatient intervention. Reviewingthe literature and analyzing existing pharmacy established these categories and medical claims data to determine errors andimprovement opportunities prevalent in the outpatient setting.

The project will cover the most severe outpatient drug interactions as the group found this to be the most straightforward andeasy intervention, since virtually all plans have in place internal or PBM-based electronic mechanisms to check for drug inter-actions at the point of service, as well as retrospectively. Drug-age contraindications will also be an area of concentration sinceresearch has shown prevalence of potentially inappropriate medication use in community-dwelling elderly persons. For thiscategory of potential error, plans will be asked to identify the number of elderly members as well as the number of elderly fill-ing prescriptions for any of the listed drugs during the period of measurement. Other areas of intervention potentially includedrug-gender contraindications, drug duplication, misuse and abuse, diagnostic conflicts, inappropriate dosage, clinicalguideline adherence, hospitalizations, and drug safety updates.

In Canton, Employers Health Purchasing Corporation of Ohio (EHPCO) is a group purchasing pharmacy benefits on behalfof over eighty participating member companies representing 450,000 covered lives. Through the sheer volume and utiliza-tion of this program, EHPCO accesses prescription drug data for participating employers, which is updated monthly. Thecoalition has found that these reports have resulted in more effective management of benefit design and cost, as well asimproved heath care outcomes for employees.

vii

National Business Coalition on Health

1015 18th Street N.W., Suite 730Washington, DC 20036FAX 202-775-1569202-775-9300

Andrew Webber

viii

Reports to members vary as EHPCO has the ability to broadly aggregate utilization data or focus on drug-specific analysis. Byusing this warehouse, the coalition has provided extensive information helping employer members make informed decisionsregarding plan design and trend management, including the identification of top prescribers. EHPCO regularly aggregates allemployers’ data, which enables trend analysis of local prescribing patterns and provides employers with comparative bench-marking data. In turn, this data also allows EHPCO to monitor the effectiveness of its prescription drug program. Accordingto EHPCO, the capabilities of the data warehouse are enormous and have provided considerable value to their employer mem-bers.

A few years ago, the governing board of the Employers' Coalition on Health (ECOH) of Rockford, Illinois wanted to measurethe effectiveness of ECOH and its programs on the delivery of health care in the Rockford area using information andresources already available. This led to the development of a project in which the ECOH negotiated a contract with primarycare physicians of two local hospitals. The contracts provide incentive for the physicians to meet certain thresholds in the treat-ment of ECOH's diabetic population. ECOH uses the contract thresholds as well as claims data to measure the health status ofthe diabetic population within its employer membership. At the time, diabetics in general comprised six percent of the ECOHpopulation, but accounted for approximately fifteen percent of total health care costs.

The coalition decided to measure the health of the diabetic population against the overall ECOH population using claims data.The primary measurement tools are the Health Care Quality Improvement Project (HCQIP), and the Illinois Foundation forQuality Health Care's Health "Project-in-a-Box," which is comprised of a diabetic flow chart, intervention suggestions andliterature reprints.

This project began in January 1, 1999 as an effort to move local diabetes practice patterns toward "best practices" developedthrough clinical research. ECOH will use accumulated data for the period of January 1, 1999 through June 30, 2000 as thebenchmark for measuring ECOH's impact for the following three years, 2001-2003. It is anticipated that over time such indi-cators as admissions per 1000 covered lives and hospital days per 1000 will be reduced as better treatment is delivered throughthe "project-in-a-box." The benchmark data may also reveal that indicators such as number of services for the diabetic patientsmay rise during the early years of the study, and decline as treatment and health status improve later on in the study.

According to Sam Schmitz, the coalition’s executive director, the influence of the ECOH on local health care delivery systemshas gained momentum in the past few years. With ever-increasing enrollment, the coalition now has approximately ten per-cent of the market and represents some of the larger and most influential employers in the market place. The combination ofsize and representation has afforded the coalition the opportunity to be creative in its attempts to drive quality and cost in thelocal market.

In addition to completing the data collection and measurement aspect of the diabetic project, ECOH also is exploring newopportunities to carry this incentive model to a higher level in diabetic care by changing the way a diabetic receives care at thephysician’s office.

Oregon Coalition of Health Care Purchasers near Portland is spearheading a state chronic disease data clearinghouse for bet-ter management of asthma and diabetes with the goal of eventual application to other chronic disease states. According toD’Anne Turner Gilmore, executive director of the Oregon Coalition of Health Care Purchasers, the pilot phase of this proj-ect is approximately 60 percent complete. The project, led by a joint working group of the Oregon Health Care QualityCorporation, created by the Oregon Coalition of Health Care Purchasers, the Oregon Diabetes Coalition, and the OregonAsthma Network, was developed to prototype a clearinghouse that interacts with physician and plan tracking systems.

The primary object of the clearinghouse is to deliver essential, timely information to physicians about their patients withchronic diseases so that they can provide the better patient outcomes. This data platform also will facilitate better health deci-sions by health plans and policy makers by providing a more accurate picture of utilization and treatment. This is an area thatis lacking in Oregon’s health care system.

ix

The only universally collected data sets are those used for billing purposes, which notoriously lack key clinical information, andare not integrated with other information systems that could improve treatment decisions. By comparison, even one of thestate’s largest health plan providers, with an internally integrated system that incorporates all clinical information for its ownpatients, does not have the data to make comparisons with the "outside" patient community.

Although some doctor groups and health plans have independently developed or adopted several separate diabetes and asthmatracking systems in Oregon, they do not share or integrate information among systems. Automated information is frequent-ly received on paper and re-entered into another computer. Without a coordinated collaborative effort, the adoption of track-ing systems by physicians and providers will be slow, will not capitalize on the potential for cross-communication and connec-tivity, and will not efficiently capture the information that physicians need.

This pilot project was intended to create a clearinghouse that interacts with four to six major functioning tracking systems thathelp physicians provide comprehensive quality care for their patients with diabetes or asthma. The exploration, testing andresolution of legal, technical and software solutions developed by these pilots will be available for implementation in physicianpractices throughout Oregon and the nation.

In January 2003, the Dallas Fort Worth Business Group on Health started a new disease management intervention project withthe Federal Reserve Bank of Dallas and TXU. Once a month, Federal Reserve and TXU employees who have enrolled in theprogram attend an educational "Lunch & Learn" session taught by a Certified Diabetes Educator from Baylor University’sDiabetes Center. The monthly diabetes education series continued until June for a total of six sessions. In addition to thelunchtime consultations, program participants also receive weekly reinforcement messages via email to help them stay on trackwith glucose monitoring and healthy diet and exercise habits. Participants at both companies have received baseline health riskassessments (HRAs) and blood tests for glucose, lipids and Hemoglobin A1C. Participants will be re-tested at the completionof the intervention phase in order to assess the effectiveness and ROI of this type of multifaceted worksite disease managementprogram.

NBCH is pleased to provide employers and consumers access to HEALTHSMART.org, an Internet–based health educationwebsite. Through unrestricted educational grants, NBCH has carefully developed this site using a variety of academic and pro-fessional health care resources. Available for both Intranet and Internet use, HEALTHSMART is consumer–friendly provid-ing thorough, high quality information. With the principal objective of preparing consumers for interaction with the healthcare system, HEALTHSMART equips them with tools to communicate more confidently with providers, as well as informa-tion on what to do in the event of diagnosis with a disease or health condition.

Clinical, economic and workplace studies provide revealing and persuasive evidence that chronic disease has a major impacton workplace productivity, significantly linking burdensome direct and indirect costs to our nation’s employers. Consequently,common needs have arisen among employers as they strive to manage productivity and labor costs while at the same time retain-ing and attracting employees in an uncertain labor market.

Most employers now understand the future benefits gained by empowering consumers through technology and providing thetools and skills to effectively interact within our nation’s complex health care system. Consumer education, disease preven-tion and health care intervention should be key strategies of policymakers, public and private purchasers, and providers toimprove our nation’s productivity and reduce health care spending.

Sincerely,

Andrew WebberPresident & CEO

Dear Reader:

On behalf of the American College of Occupational and Environmental Medicine (ACOEM), I am pleased to serve as Co-Chair for the Prescription Drug Benefit Cost and Plan Design Survey. ACOEM, as the nation’s largest society of occupation-al and environmental medicine physicians, is committed to advancing the optimal health and safety of workers, workplaces,and environments by working with employers, health care delivery and financing organizations, pharmaceutical companies,

and other health care professionals to ensure the health of workers. I am confident thatACOEM’s involvement will enhance the Survey’s value because of our occupational and environ-mental medicine (OEM) expertise. ACOEM hopes to partner with the pharmaceutical industryto measure workforce productivity increases related to the proper management of diseases inworking-aged individuals.

Occupational and environmental medicine is the medical specialty devoted to prevention andmanagement of occupational and environmental injury, illness and disability, and promotion ofhealth and productivity of workers, their families, and communities. Health and productivityand disease management are major components of occupational and environmental medicine.Traditionally, employers have turned to OEM professionals to increase productivity by manag-ing occupational injuries and illnesses. Today, the continual emergence of new chemicals, com-plex tools, manufacturing methodologies, pollution and environmental impacting activities, and

health care reform have focused on and mandated a greater need for trained occupational and environmental medical spe-cialists. ACOEM members are knowledgeable and skilled in treating job-related diseases, recognizing and resolving workplacehazards, instituting rehabilitation methods, and providing well-managed care. In addition, their unique training enablesoccupational and environmental physicians to appreciate and understand business needs, ergonomics, industrial hygiene,clinical/preventive medicine, epidemiology, and biostatistics.

Employers are increasingly concerned about the burden of illness in their workforce and its impact on productivity. The totalcost of ill health to business and industry is comprised of not only direct medical costs, but of health-related productivity costsdue to absenteeism and presenteeism. Employers are recognizing that their employees are their most valuable asset and thattheir health is the key to a healthy bottom line.

Since its inception in 1916, ACOEM has been involved in many initiatives that aim to improve employee health, wellness, andproductivity through disease management. A number of these initiatives have been directed through the corporate medicaldirector members of ACOEM who have taken on an increasingly important role within industry in guiding key health policydecisions.

In the fall of 2002, ACOEM partnered with The Benfield Group to conduct a survey on health and productivity management.The survey instrument was distributed to more than 1,200 employer-based physicians and health management professionals,and was supplemented with selected interviews. The survey and interviews have provided valuable information on the status ofhealth and productivity management among U.S. employers, as well as the perspectives, opinions, and priorities of physicianswho are guiding and managing employer-based health programs.

These results will help ACOEM design programs and services that best support mutual interests in health, wellness, and pro-ductivity management efforts. The survey results show that while corporations have a great interest in health initiative pro-grams, several areas with great potential to both improve health, and to generate a substantial return on investment for corpo-rations are relatively unexplored. Areas such as disease management, return-to-work-programs, safety programs, and absence

x

Barry S. Eisenberg

management are all seen as being of great importance in improving health and productivity.

In recent years, disease management in the workplace has been a particular focus of ACOEM education efforts. Last year, theCollege developed an educational session and a CD-ROM on the public health aspects of hepatitis C. This session addressedthe natural history of hepatitis C; its epidemiology; the clinical history of patients; guidelines and cost effectiveness of screen-ing for chronic hepatitis C; advances in treatment; and the financial and legal implications of hepatitis C in the workplace.Members were offered educational materials and a patient management program for hepatitis C that they could use for theiremployees.

These resources were intended to create among employers an awareness of hepatitis C hazards and to assist employees who maybe suffering from the disease. Managing hepatitis C in the workplace will not only improve employees’ health and quality oflife but can result in great benefits to employers by reducing long-term costs, including per person claims for both lifetimemedical and lifetime indemnity insurance claims. In fact, Milliman USA, an Actuarial Consultancy firm, found "a 4:1 returnon investment for dollars paid for treatment today against future medical care dollars" (Sherrie Dulworth, RN, MillimanUSA).

This effort was highly rated by the membership and is an example of the effectiveness of multiple communications efforts thatare based on the very best clinical and scientific information available. The methods developed in this session can be tailoredto a variety of other medical conditions.

In January 2002, ACOEM convened an Expert Panel to identify which productivity instruments best measured work loss dueto migraines. The Expert Panel identified the numerous components of productivity and identified the key elements of lostproductivity measurement to be absenteeism, presenteeism, and employee turnover or replacement costs. This study can assistemployers and health care decision-makers in developing sustainable strategies to measure the impact of migraine headacheon workplace productivity loss. Employers need to have a better understanding of the impact of medical conditions such asmigraine headache on employees’ productivity to assist in more knowledgeable and effective decision-making regarding theirinvestment in health-related productivity improvement initiatives. For those employers wishing to implement a health-relat-ed productivity measurement program within their company, this project provides information to help determine the instru-ment most appropriate for their program.

The Panel also determined that areas within the field of health-related workplace productivity measurement that need furtherstudy include the:➢ Identification of the necessary metrics for effective business decision-making and the explicit incorporation of those met-

rics into workplace productivity measurement tools,➢ Creation of a standardized definition of employee turnover and replacement costs, and Examination of the impact of an

individual’s absenteeism and presenteeism on team dynamics and interdependent work groups within the workplace envi-ronment.

For more detail on this study, please refer to "Health-Related Workplace Productivity Measurement: General and MigraineSpecific Recommendations from ACOEM Expert Panel" in the Journal of Occupational and Environmental Medicine, April2003.

In addition, over the last two years, ACOEM has initiated, fostered, and participated in strategic alliances in order to furtherhealth and productivity research by:➢ Developing metrics for the measurement of health and productivity.➢ Enhancing the "business case" for health and productivity.➢ Educating its members on health and productivity management and measurement.➢ Partnering with other organizations working on health and productivity initiatives.Workforce demographics continue to change. By 2010, the proportion of the workforce over age 54 will equal the proportionunder 25. Out of necessity, corporations must address the increasing effects of chronic diseases associated with aging on the

xi

ability to perform work. The prevention and treatment of chronic diseases – such as diabetes – is especially important as theworking population ages.

However, employers also desire health management that cares for all of their employees and families, rather than only the selectfew who are touched by specific disease management programs. Therefore, there needs to be more initiatives involving analy-sis of employee populations to ascertain not only which employees have an existing medical condition that needs management,but also to identify those employees who are at risk of developing future medical conditions so they can be prevented. Theremust be attempts to build on the strengths of disease management, but also to integrate health and disability management andcoordinate the care for the whole person and an entire employee population. Best practice guidelines from evidence-basedmedicine can empower patients and providers. With the emerging consumer movement in health care, individuals desire coor-dination across the health care continuum with quality-driven, outcomes-based, patient-centered care.

Health and productivity are inextricably linked. Due to increasing medical costs, health-related productivity losses, and limit-ed available resources, employers need to be able to determine the value or return on investment of the health care interven-tions that they purchase and their employees receive.

Potential benefits from employer-purchased health care interventions such as disease management, disability management,optimal pharmaceutical utilization, and health promotion programs include reduced medical costs and decreased productiv-ity losses associated with the firm’s workforce. We believe that by working together, we can develop the tools that will contributeto a healthier nation and healthier economy.

Respectfully,

Barry S. EisenbergExecutive DirectorAmerican College of Occupational and Environmental Medicine

xii

1

INTRODUCTIONThe Pharmacy Benefit

Management Institute, Inc.has conducted a survey of thenation’s large employers toassess trends in pharmacy

benefit management, plan design, and cost issues every yearsince 1995. Survey data are collected, compared, and ana-lyzed to provide employers with a comprehensive overview ofthe current state of prescription drug coverage costs and plandesign issues.

Each year, PBMI receives valuable input from respon-dents that is used to improve the scope of the survey andreport. PBMI has expanded its report to include updates oncost sharing strategies, the importation of drugs fromCanada, drug discount card programs, and the impact ofrecent OIG guidance on the PBM industry.

KEY FINDINGSPharmacy Reimbursement Decreases

Discounts for both retail and mail service pharmacyreimbursement continue to increase. The average AWP andthe average dispensing fee paid to retail pharmacies for branddrugs is now 85.9% and $2.13, respectively. The averageAWP and the average dispensing fee for paid to mail servicepharmacies for brand drugs is now 80.3% and $0.87,respectively.

In addition to decreases in the absolute value of the dis-pensing fee, the value of the fee relative to the ingredient costhas decreased over time. As the average ingredient cost hasincreased year after year, the dispensing fee has not.

PBM Administrative Fees DecreasePBM administrative fees for both retail and mail service

also are decreasing. In 2001, the average administrative feepaid for each retail claim was $0.38. In 2002, it decreasedto $0.28. The average administrative fee paid per mail serv-ice pharmacy claim in 2002 was $0.16, as compared to $0.23in 2001.

Formulary Use On the RiseThe use of formularies continues to increase. In 1995,

only 54% of respondents reported using a formulary. Thispercentage increased to 89% in 2002. The traditional openformulary has been replaced by the incented formulary con-cept, which has grown from just 25% of employers in 1999 toalmost two-thirds (63%) of employers in 2002. During this

time, the percentage of employers offering closed formula-ries decreased from 8% in 1999 to 2% in 2002.

PBMI added a survey question this year asking therespondents to indicate whether they had requested theirPBM change the formulary status of a drug (e.g., from pre-ferred status to nonpreferred status). Surprisingly, 19% ofthe respondents indicated they had requested a change. Infollow-up calls to a number of respondents, PBMI learnedthat some of the requested changes were for simple issuessuch as making sure that the brand version of drugs that hadbecome available generically was moved to nonpreferred sta-tus. Other changes were related to employer requests toinclude a step-therapy edit or a prior-authorization require-ment on a preferred product. Finally, some employers askedtheir PBMs to change the drugs included on the preferredproduct list.

Plan Sponsors Capturing More Rebate DollarsEmployers are receiving a greater percentage of the

rebate pie, on average, with receipts of 79% of the total rebatedollars collected as compared to 73% in 2001. Employersreceiving the greater of a percentage and a fixed amountreported receiving 86% of total rebate dollars collected.Employer size appears to have the greatest impact on the per-centage of rebates received with the largest employers receiv-ing 91% of rebates and the smallest employers only receiving64%.

Retail, Mail Cost Sharing Moves Upward at Different Rates

Retail copayments increased by approximately 10% forall tiers from 2001 to 2002. However, these increases aremore pronounced in mail. From 2001 to 2002, averagefirst-tier mail service copayments increased by 16%, second-tier increased by 20%, and third-tier by 10%. Because mailservice copayments have increased more quickly than retailcopayments for the last few years, the mail service second-tiercopayment is now 1.8 times the retail second-tier copaymentas compared to 1.6 times in 2001.

The percentage of employers using coinsurance for sec-ond-tier retail cost sharing increased from 22% in 2001 to26% in 2002. Although most employers who use coinsur-ance generally use coinsurance for all drug categories, someemployers use coinsurance only for second- or third-tierdrug prescriptions, with flat dollar first-tier copayments.This approach for the second- and third-tiers gives plansmore flexibility to ensure patients pay a consistent portion of

EXECUTIVE SUMMARY

2

the benefit cost, while providing an additional incentive touse generic drugs.

Prior Authorization Continues to IncreaseThe percentage of employers using prior authorization

programs to control costs and manage access to certain drugshas increased from 43% in 1996 to 76% in 2002. Theseprograms are similar to step therapy programs in that accessto selected drugs is restricted to those individuals who canmost benefit from their use. The difference is that theapproval process is manual rather than automatic.

Utilization Patterns Change With TimePBMI collects a limited amount of utilization data to

quantify the impact of various benefit plan design elementson utilization. On average, 13% of prescriptions are filledthrough a mail service pharmacy. However, a mandatory mailservice use requirement generates 3 times more mail serviceutilization than does the voluntary mail service option, withutilization rates of 34% and 11% respectively.

Average retail generic utilization increased from 40.4%in 2001 to 41.5% in 2002. Average mail service generic uti-lization increased from 30.4% in 2001 to 31.8% in 2002.Having a greater difference between the generic and branddrug copayments, and requiring patients to pay the differ-ence between the generic and brand drug costs appear toincrease generic drug use slightly.

IMPLICATIONS OF FINDINGSEmployers’ prescription drug costs rose 16.9% in 2002,

according to a recent survey by Mercer Human ResourceConsulting. This increase follows an increase of 17.8% in2001 and an 18.3% increase in 2000. Plan sponsors arelooking for ways to reduce these increases. The methodsavailable to plan sponsors to control drug benefit costs aregenerally grouped in the following baskets:➢ Reducing reimbursement,➢ Changing drug mix, and➢ Decreasing utilization.

Our research indicates plan sponsors use all of theseapproaches to varying degrees in their drug benefit programsto manage this trend.

Every year, pharmacy reimbursement rates decreaseincrementally. Plan sponsors, through their PBM partners,

constantly negotiate deeper discounts. These reimburse-ment discounts save plan sponsors significant amounts ofmoney. However, in terms of the trend rate, they have onlya minimal impact.

Plan sponsors also use cost sharing to manage pharmacyreimbursement and the trend rate. Cost sharing reduces theamount the plan sponsor pays. To the extent a plan sponsorcan determine in advance the expected growth in benefitcosts for any given year, the cost sharing can be modified toattain specific cost goals. Recognizing that one side effect ofincreases in cost sharing is decreases in utilization, cost shar-ing can be viewed as a cost trend management tool. However,its primary use is to mitigate cost increases.

Strictly speaking, rebates do not reduce reimbursement.They may more appropriately be viewed as reimbursementrefunds. The plan sponsor is returned money previouslyused to pay for certain drugs. Although valuable, these pay-ments also have little impact on the trend rate.

The primary causes of the drug benefit cost increases, asreported by many sources, have been changes in drug mixand increases in utilization. Beneficiaries are using moredrugs and higher cost drugs. The management tools havingthe greatest impact on the trend rate are those that affectthese factors. Plan sponsors:➢ Encourage generic drug use to replace the use of iden-

tical, expensive brand products,➢ Use formularies to encourage the use of lower cost pre-

ferred brand drug products rather than higher costnonpreferred products,

➢ Implement drug exclusions, quantity limits and othersystem edits to curb excessive utilization, and

➢ Implement utilization management programs toencourage appropriate use.Most plan sponsors use a variety of utilization manage-

ment tools—DUR, step therapy, and prior authorization—toidentify inappropriate utilization or restrict utilization tothose individuals that can clinically benefit from a particularproduct.

PBMI recommends plan sponsors continue to use all ofthese tools to affect their trend rates. It is equally importantfor PBMs to clearly communicate the impact of these tools onthis trend. Although many plan sponsors use these tools,measuring the success of these activities has been difficultgiven the ongoing increases in drug benefit costs.

3

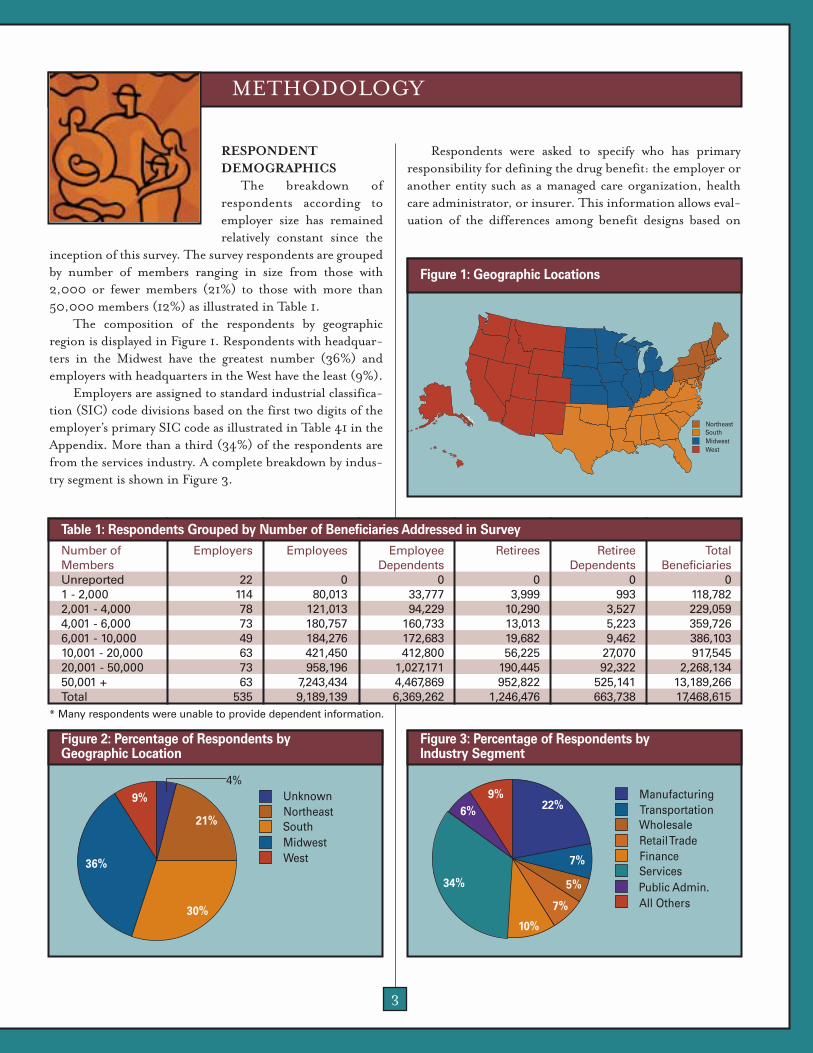

RESPONDENT DEMOGRAPHICS

The breakdown ofrespondents according toemployer size has remainedrelatively constant since the

inception of this survey. The survey respondents are groupedby number of members ranging in size from those with2,000 or fewer members (21%) to those with more than50,000 members (12%) as illustrated in Table 1.

The composition of the respondents by geographicregion is displayed in Figure 1. Respondents with headquar-ters in the Midwest have the greatest number (36%) andemployers with headquarters in the West have the least (9%).

Employers are assigned to standard industrial classifica-tion (SIC) code divisions based on the first two digits of theemployer’s primary SIC code as illustrated in Table 41 in theAppendix. More than a third (34%) of the respondents arefrom the services industry. A complete breakdown by indus-try segment is shown in Figure 3.

Respondents were asked to specify who has primaryresponsibility for defining the drug benefit: the employer oranother entity such as a managed care organization, healthcare administrator, or insurer. This information allows eval-uation of the differences among benefit designs based on

METHODOLOGY

Number of Employers Employees Employee Retirees Retiree TotalMembers Dependents Dependents BeneficiariesUnreported 22 0 0 0 0 01 - 2,000 114 80,013 33,777 3,999 993 118,7822,001 - 4,000 78 121,013 94,229 10,290 3,527 229,0594,001 - 6,000 73 180,757 160,733 13,013 5,223 359,7266,001 - 10,000 49 184,276 172,683 19,682 9,462 386,10310,001 - 20,000 63 421,450 412,800 56,225 27,070 917,54520,001 - 50,000 73 958,196 1,027,171 190,445 92,322 2,268,13450,001 + 63 7,243,434 4,467,869 952,822 525,141 13,189,266Total 535 9,189,139 6,369,262 1,246,476 663,738 17,468,615

Table 1: Respondents Grouped by Number of Beneficiaries Addressed in Survey

WestMidwestSouthNortheast

Figure 1: Geographic Locations

WestMidwestSouthNortheastUnknown

36%

21%

30%

4%9%

Figure 2: Percentage of Respondents by Geographic Location

All OthersPublic AdministrationServices

FinanceRetail TradeWholesaleTransportationManufacturing

All OthersPublic Admin.ServicesFinanceRetail TradeWholesaleTransportationManufacturing

6%

34%

22%

7%

5%

7%

10%

9%

Figure 3: Percentage of Respondents by Industry Segment

* Many respondents were unable to provide dependent information.

4

whether the employer or a third party is responsible fordefining the drug benefit. It is important to note that thedata provided by the respondent are for a single plan forwhich the employer has chosen to respond, and is not neces-sarily representative of the employer’s entire book of business

The vast majority of respondents describe their pharma-cy benefits as self-defined as shown in Table 2. In general,whether benefits are self-defined or not resulted in little dif-ference in design. These differences are discussed, wherebelieved to be relevant, in applicable sections of this report.

Respondents also were asked to identify whether theypurchase PBM services as part of a coalition. The majority ofemployers (83%) do not buy these services as part of a coali-tion as illustrated in Table 3. In general, whether theemployer participated in a coalition or not resulted in littledifference in design. These differences are discussed, wherebelieved to be relevant, in applicable sections of this report.

Plan Design Decision Maker Percentage of EmployersEmployer 82%External Organization 18% (e.g., HMO, insurer, third-party administrator)

Table 2: Percentage of Respondents by Plan Design Responsibility

Coalition Member Status Percentage of EmployersCoalition Member 17%Coalition Nonmember 83%

Table 3: Percentage of Employers Participating in Coalitions

5

PHARMACY REIMBURSEMENT

Discounts in retail,brand-drug AWP continue toincrease. Overall, the AWPdiscount increased by 2.3%

from 1995 to 2002. During this time, the average retail dis-pensing fee also decreased from a high of $2.50 per script in1995 to its current low of $2.13 in 2002. The average reim-bursement rate, which is a combination of average AWP and

average dispensing fee, declined from 96.5% in 1995 to88.5% in 2002—a reduction of 8.0%. (See sidebar for amore detailed discussion regarding pharmacy reimburse-ment rate.) These trends are shown in Table 4.

A similar trend was evident in mail, although thedecreases in mail reimbursement were greater as shown inTable 5. The average, brand-mail AWP discount increasedby almost 5% from 85.0% in 1995 to 80.3% in 2002.Average mail dispensing fees also have declined from a highof $1.82 in 1995 to $0.87 in 2002. This is more than a 50%

RESEARCH FINDINGS

Calculating Pharmacy Reimbursement RatesFor purposes of measuring the

impact of both aspects of pharmacyreimbursement, PBMI created avalue that combines the discountedAWP and dispensing fee. This valuehas been labeled or referred to as"Reimbursement Rate". To createthis value, PBMI converts the dis-pensing fee into an AWP value andadds it to the discounted AWP. Thesecalculations are performed for bothretail and mail service brand pre-scriptions.

In previous reports, the conver-sion of the dispensing fee was calcu-lated using an assumed ingredientcost that has been held constant since1995. This methodology evaluateschanges in reimbursement in theabstract assuming no inflation.

Although PBMI does not believe theaverage ingredient cost is the bestmeasure of inflation, it believes cal-culating the reimbursement ratevalue using an ingredient cost num-ber that changes over time providesmore information than the previousmethodology.

Because the average dispensingfee is decreasing while the averageingredient cost is increasing, theimpact of the dispensing fee on thereimbursement rate has alsodecreased. Using an ingredient costthat increases over time causes theimpact of the dispensing fee on thereimbursement rate value to decreaseover time. The reimbursement ratevalue decreases over time regardlesswhether the discounted AWP or dis-

pensing fee decreases by virtue of aningredient cost that increases.Although not a true measure of gen-eral inflation, this reflects a de factoimpact of inflation.

Tables 4 and 5 show the retailand mail information for brand pre-scriptions. The average reimburse-ment rate is calculated Average AWP+ (Average Dispensing Fee/AverageIngredient Cost). Because theAverage Dispensing Fee is decreasingwhile the Average Ingredient Cost isincreasing, the impact of the dis-pensing fee on the reimbursementrate has also decreased. The AverageIngredient Cost value used is basedupon industry information. Thesecalculations can be replicated usingany average ingredient cost.

Year Average Average Average AverageAWP Dispensing Ingredient Reimbursement

Fee Cost Rate2002 85.9% $2.13 $79.80 88.5%2001 86.1% $2.21 $69.39 89.3%2000 86.5% $2.31 $60.34 90.3%1999 86.9% $2.30 $52.47 91.3%1998 86.8% $2.35 $45.63 91.9%1997 87.4% $2.32 $39.68 93.2%1996 87.9% $2.47 $34.50 95.1%1995 88.2% $2.50 $30.00 96.5%

Table 4: Retail Brand Reimbursement

Year Average Average AverageAWP Dispensing Reimbursement

Fee Rate2002 80.3% $0.86 81.1%2001 81.1% $1.09 82.2%2000 81.5% $1.15 82.7%1999 82.6% $1.38 84.0%1998 82.9% $1.51 84.4%1997 83.4% $1.61 85.0%1996 84.4% $1.71 86.1%1995 85.0% $1.82 86.8%

Table 5: Mail Service Brand Reimbursement

6

decrease in the dispensing fee over the past seven years.When AWP discounts and dispensing fees are combined,there was an overall 6.2% reduction in the average mail reim-bursement rate from 86.8% in 1995 to 80.6% in 2002.Because of increased competition among mail service phar-macies to increase their overall volume, mail reimbursementis expected to continue to decrease.

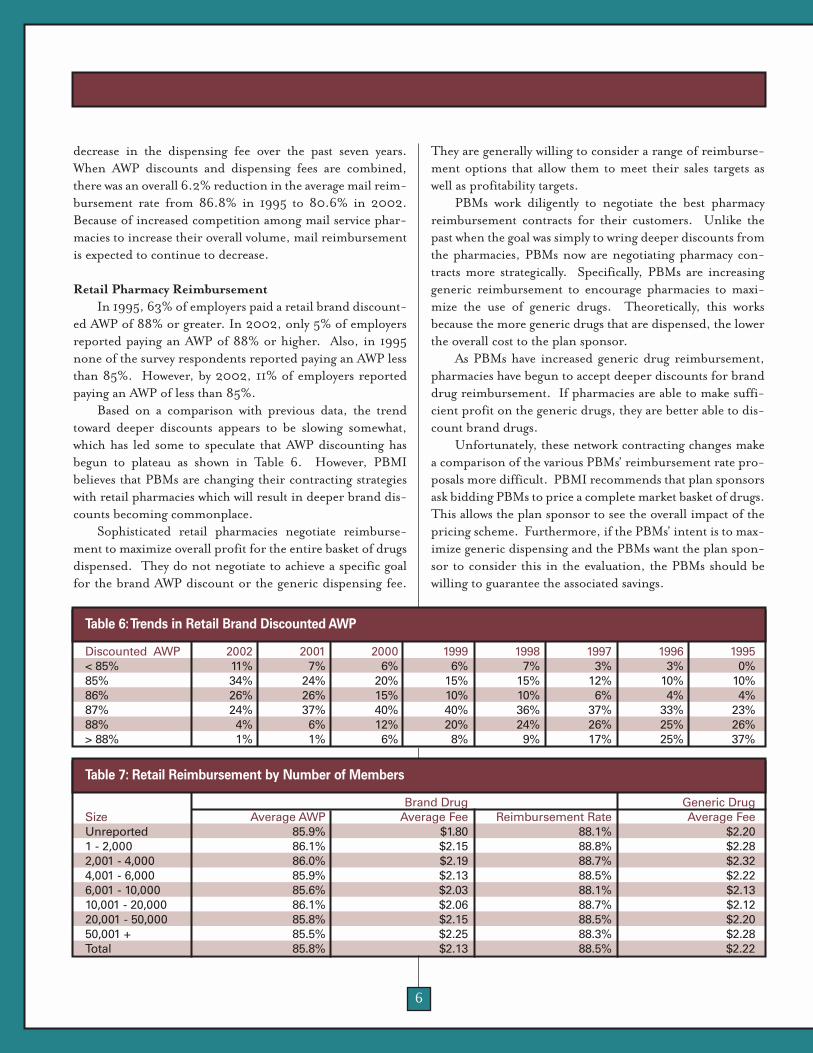

Retail Pharmacy ReimbursementIn 1995, 63% of employers paid a retail brand discount-

ed AWP of 88% or greater. In 2002, only 5% of employersreported paying an AWP of 88% or higher. Also, in 1995none of the survey respondents reported paying an AWP lessthan 85%. However, by 2002, 11% of employers reportedpaying an AWP of less than 85%.

Based on a comparison with previous data, the trendtoward deeper discounts appears to be slowing somewhat,which has led some to speculate that AWP discounting hasbegun to plateau as shown in Table 6. However, PBMIbelieves that PBMs are changing their contracting strategieswith retail pharmacies which will result in deeper brand dis-counts becoming commonplace.

Sophisticated retail pharmacies negotiate reimburse-ment to maximize overall profit for the entire basket of drugsdispensed. They do not negotiate to achieve a specific goalfor the brand AWP discount or the generic dispensing fee.

They are generally willing to consider a range of reimburse-ment options that allow them to meet their sales targets aswell as profitability targets.

PBMs work diligently to negotiate the best pharmacyreimbursement contracts for their customers. Unlike thepast when the goal was simply to wring deeper discounts fromthe pharmacies, PBMs now are negotiating pharmacy con-tracts more strategically. Specifically, PBMs are increasinggeneric reimbursement to encourage pharmacies to maxi-mize the use of generic drugs. Theoretically, this worksbecause the more generic drugs that are dispensed, the lowerthe overall cost to the plan sponsor.

As PBMs have increased generic drug reimbursement,pharmacies have begun to accept deeper discounts for branddrug reimbursement. If pharmacies are able to make suffi-cient profit on the generic drugs, they are better able to dis-count brand drugs.

Unfortunately, these network contracting changes makea comparison of the various PBMs’ reimbursement rate pro-posals more difficult. PBMI recommends that plan sponsorsask bidding PBMs to price a complete market basket of drugs.This allows the plan sponsor to see the overall impact of thepricing scheme. Furthermore, if the PBMs’ intent is to max-imize generic dispensing and the PBMs want the plan spon-sor to consider this in the evaluation, the PBMs should bewilling to guarantee the associated savings.

Brand Drug Generic DrugSize Average AWP Average Fee Reimbursement Rate Average FeeUnreported 85.9% $1.80 88.1% $2.201 - 2,000 86.1% $2.15 88.8% $2.282,001 - 4,000 86.0% $2.19 88.7% $2.324,001 - 6,000 85.9% $2.13 88.5% $2.226,001 - 10,000 85.6% $2.03 88.1% $2.1310,001 - 20,000 86.1% $2.06 88.7% $2.1220,001 - 50,000 85.8% $2.15 88.5% $2.2050,001 + 85.5% $2.25 88.3% $2.28Total 85.8% $2.13 88.5% $2.22

Table 7: Retail Reimbursement by Number of Members

Discounted AWP 2002 2001 2000 1999 1998 1997 1996 1995< 85% 11% 7% 6% 6% 7% 3% 3% 0%85% 34% 24% 20% 15% 15% 12% 10% 10%86% 26% 26% 15% 10% 10% 6% 4% 4%87% 24% 37% 40% 40% 36% 37% 33% 23%88% 4% 6% 12% 20% 24% 26% 25% 26%> 88% 1% 1% 6% 8% 9% 17% 25% 37%

Table 6:Trends in Retail Brand Discounted AWP

7

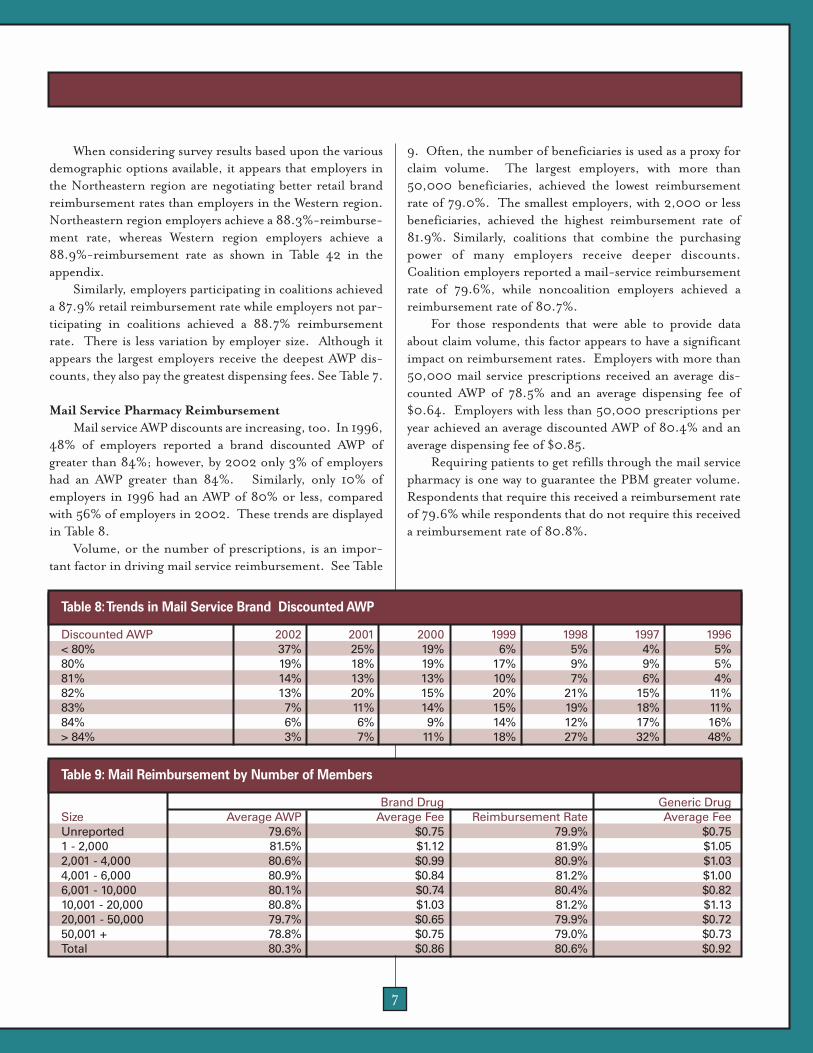

When considering survey results based upon the variousdemographic options available, it appears that employers inthe Northeastern region are negotiating better retail brandreimbursement rates than employers in the Western region.Northeastern region employers achieve a 88.3%-reimburse-ment rate, whereas Western region employers achieve a88.9%-reimbursement rate as shown in Table 42 in theappendix.

Similarly, employers participating in coalitions achieveda 87.9% retail reimbursement rate while employers not par-ticipating in coalitions achieved a 88.7% reimbursementrate. There is less variation by employer size. Although itappears the largest employers receive the deepest AWP dis-counts, they also pay the greatest dispensing fees. See Table 7.

Mail Service Pharmacy ReimbursementMail service AWP discounts are increasing, too. In 1996,

48% of employers reported a brand discounted AWP ofgreater than 84%; however, by 2002 only 3% of employershad an AWP greater than 84%. Similarly, only 10% ofemployers in 1996 had an AWP of 80% or less, comparedwith 56% of employers in 2002. These trends are displayedin Table 8.

Volume, or the number of prescriptions, is an impor-tant factor in driving mail service reimbursement. See Table

9. Often, the number of beneficiaries is used as a proxy forclaim volume. The largest employers, with more than50,000 beneficiaries, achieved the lowest reimbursementrate of 79.0%. The smallest employers, with 2,000 or lessbeneficiaries, achieved the highest reimbursement rate of81.9%. Similarly, coalitions that combine the purchasingpower of many employers receive deeper discounts.Coalition employers reported a mail-service reimbursementrate of 79.6%, while noncoalition employers achieved areimbursement rate of 80.7%.

For those respondents that were able to provide dataabout claim volume, this factor appears to have a significantimpact on reimbursement rates. Employers with more than50,000 mail service prescriptions received an average dis-counted AWP of 78.5% and an average dispensing fee of$0.64. Employers with less than 50,000 prescriptions peryear achieved an average discounted AWP of 80.4% and anaverage dispensing fee of $0.85.

Requiring patients to get refills through the mail servicepharmacy is one way to guarantee the PBM greater volume.Respondents that require this received a reimbursement rateof 79.6% while respondents that do not require this receiveda reimbursement rate of 80.8%.

Discounted AWP 2002 2001 2000 1999 1998 1997 1996< 80% 37% 25% 19% 6% 5% 4% 5%80% 19% 18% 19% 17% 9% 9% 5%81% 14% 13% 13% 10% 7% 6% 4%82% 13% 20% 15% 20% 21% 15% 11%83% 7% 11% 14% 15% 19% 18% 11%84% 6% 6% 9% 14% 12% 17% 16%> 84% 3% 7% 11% 18% 27% 32% 48%

Table 8:Trends in Mail Service Brand Discounted AWP

Brand Drug Generic DrugSize Average AWP Average Fee Reimbursement Rate Average FeeUnreported 79.6% $0.75 79.9% $0.751 - 2,000 81.5% $1.12 81.9% $1.052,001 - 4,000 80.6% $0.99 80.9% $1.034,001 - 6,000 80.9% $0.84 81.2% $1.006,001 - 10,000 80.1% $0.74 80.4% $0.8210,001 - 20,000 80.8% $1.03 81.2% $1.1320,001 - 50,000 79.7% $0.65 79.9% $0.7250,001 + 78.8% $0.75 79.0% $0.73Total 80.3% $0.86 80.6% $0.92

Table 9: Mail Reimbursement by Number of Members

8

ADMINISTRATIVE FEESPBM administrative fees are commonly paid on a per-

claim basis. In 2001, the average administrative fee paid foreach retail prescription was $0.38. As shown in Table 10, in2002, the average administrative fee paid for each retail pre-scription decreased to $0.28. The average administrative feepaid per mail service pharmacy claim in 2002 was $0.16,reflecting a $0.07 decrease from 2001

As administrative fees have become less importantsources of revenue for PBMs , these fees have decreased dra-matically. As the industry evolves, it will be interesting to seewhat role these fees play in the future.

Western employers reported paying the highest mailservice administrative fee of $0.28, whereas Midwesternemployers paid the lowest fee of $0.14 as demonstrated inTable 12. In retail, large employers (50,001+) paid the low-est fees while smaller employers paid the highest fees ($0.42versus $0.21) in retail. The administrative fees tend to followthe same rules as mail service AWP discounts, with employerswith the greatest number of beneficiaries paying lower fees asshown in Table 11.

Coalition members pay lower administrative fees forretail and mail claims than non-coalition members as shownin Table 13.

FORMULARIES AND REBATESFormulary

The use of formularies continues to increase over time.In 1995, only 54% of respondents reported using a formu-

lary; however, that percentage increased to 89% in 2002.See Table 14.

For analysis purposes, formularies are grouped intothree categories: closed, open, and incented formularies.The use of closed formularies has become nearly extinctwithin the employer-managed arena. In 2002, 2% of therespondents reported using a closed formulary as shown inFigure 4. A closed formulary excludes selected drugs withina category of otherwise covered drugs. This forces patients touse the preferred drugs within the category or incur theentire cost of the prescription.

The creation of the incented (or multi-tier formulary)provides plan members with a financial incentive to use thepreferred drugs while preserving access to the nonpreferreddrugs. Although, the patients may not be required to pay theentire cost of a non-preferred drug, they are usually requiredto pay a higher copayment for non-preferred products.

One of the interesting aspects of 2002 survey results isthe continued decline in the percentage of employers whoreport the use of an open formulary. This percentage has

Year Retail Mail2002 $0.28 $0.162001 0.38 0.23

Table 10: Average Administrative Fees Paid per Prescription

Size of Employer Retail MailUnreported $0.06 $0.051 - 2,000 $0.42 $0.192,001 - 4,000 $0.31 $0.304,001 - 6,000 $0.31 $0.176,001 - 10,000 $0.24 $0.1210,001 - 20,000 $0.28 $0.1620,001 - 50,000 $0.27 $0.1450,001 + $0.21 $0.10Total $0.28 $0.16

Table 11: Average Administrative Fees by Number of Members

Region Retail MailUnknown $0.20 $0.00Northeast $0.32 $0.16South $0.29 $0.17Midwest $0.25 $0.14West $0.32 $0.28Total $0.28 $0.16

Table 12: Average Administrative Fees by Geographic Region

Coalition Status Retail MailNon-Coalition Member $0.32 $0.20Coalition Member $0.23 $0.14

Table 13: Average Administrative Fees by Coalition Member Status

Year Percentage of Employers Using Any Type of Formulary

2002 89%2001 83%2000 85%1999 74%1998 74%1997 76%1996 58%1995 54%

Table 14: Percentage of Employers Using a Formulary

9

decreased from 67% of employers in 1999 to 35% of employ-ers today.

The traditional open formulary is being replaced by theincented formulary concept, which has grown from just 25%of employers in 1999 to almost two-thirds (63%) of employ-ers in 2002. During this time, the percentage of employerswho offered closed formularies decreased from 8% in 1999to 2% in 2002.

The migration from open to incented formularies is theculmination of several factors. As the costs of prescriptiondrugs continue to increase, employers are looking for cre-ative ways to increase patient cost sharing. An effective strat-egy is the introduction of an incented formulary in which alist of nonpreferred drugs (e.g., high-cost, brand-nameproducts, lifestyle drugs, "me-too" drugs) is created. Byinstituting higher copayments for these nonpreferred drugs,employers collect a greater share of the drug cost from itsbeneficiaries.

Additionally, the use of an incented for-mulary has been shown to increase the marketshare of preferred drug products. As such, ifthe formulary is designed properly, theemployers can achieve lower costs through theincreased use of lower cost drug products and,in some cases, higher rebate collections.

Employer Initiated Formulary ChangesPBMI added a survey question this year

asking the respondents to indicate whetherthey had requested their PBM change the formulary status ofa drug (e.g., from a preferred status to nonpreferred status).Surprisingly, 19% of the respondents indicated they hadrequested a change.

PBMI called some of these respondents to gather moreinformation about the changes requested. PBMI learnedthat some of the requested changes were for simple issuessuch as making sure that the brand version of drugs that hadbecome available generically was moved to nonpreferred sta-tus. Other changes were related to employer requests toinclude a step-therapy edit or a prior-authorization require-ment on a preferred product. Finally, some employers askedtheir PBMs to change the drugs included on the preferredproduct list.

In the case of brand drugs becoming available generical-ly, the motivation was primarily related to performing duediligence and monitoring PBM activities. Moving brandname versions of drugs available generically to the third-tiershould result in increased generic drug use. In the case ofaccess limitation, the employer simply was trying to limitaccess or to encourage generic drug use. In the case of pre-

ferred product selection, two distinct motiva-tions were apparent. The first being to miti-gate the impact of a PBM’s frequent formula-ry changes on the beneficiaries. Each time thepreferred product changes patients must visittheir prescribers to get new prescriptions.Secondly, much less frequently, the employeris disagreeing with the PBM’s preferred prod-uct selection.

The circumstances in which employers getinvolved in preferred product selection arefairly limited. These employers believe a

review of the medical literature for certain drugs does notjustify the PBMs’ preferred placement. The drugs mostcommonly mentioned are drugs (e.g., Clarinex® orNexium®) with perceived limited improvement over the pre-vious generation drugs they are replacing (e.g., Claritin® orPrilosec®).

Most employers believe it is the responsibility of thePBM to manage the formulary. The employer pays the PBMto provide this service. Although a very small number ofemployers have contracted with or are evaluating third-partyorganizations for formulary management, the vast majorityof employers seem content to let their PBMs handle formu-lary decisions. One employer who had been very active inthis process recently decided to end this activity after reach-ing the conclusion that the expense and time involved out-weighed any savings achieved.

Incented

Open

Closed

63%

35%

2%

Figure 4:Type of Formulary Design Used by Employers

Most employersbelieve it is the

responsibility ofthe PBM to manage

the formulary.

10

RebatesEmployer-PBM contracts generally dictate that formula-

ry rebates are paid based upon one of three methods:➢ A guaranteed, fixed-dollar amount per script, ➢ A percentage of all rebates collected, or ➢ The greatest rebate after both calculation methods are

considered. Nearly 51% (vs. 60% in 2001) of the respondents report

receiving rebates as a percentage of all rebates collected, with39% (vs. 33% in 2001) of rebates based on a fixed dollaramount per prescription. Only 9% of respondents receivethe greater of these two amounts. Based upon only two yearsof data, it is unclear whether the increase in the percentage ofrespondents receiving a fixed-dollar amount is a marketplacetrend. Different PBMs tend to prefer one rebate calculationmethodology to the others. The percentage of respondentsusing one PBM or another can affect these survey results.

As Table 15 indicates, employers receiving a percentageof the rebates receive, on average, 79% of total rebate dollarscollected. This is an increase from 73% in 2001. Employersreceiving the greater of a percentage and a fixed amountreported receiving 86% of total rebate dollars collected.When comparing the different geographic regions, theNortheast region appears to receive a higher percentage ofrebate dollars than the Midwest and West as shown in Table

16. Additionally, as Table 17 indi-cates, larger employers receive amuch greater percent of rebates thanthe smaller employers: 91% for thelargest employers and 64% for thesmallest.

It is not possible to report an aver-age dollar amount collected byemployers who receive a guaranteedamount because of the many differ-ent variables affecting this value.Some employers receive differentrebate amounts for retail and mailservice claims. Some employersreceive rebates based upon the total

number of prescriptions filled, while others receive rebatesbased solely upon the number of prescriptions filled for pre-ferred drugs. The basis by which the data provided is calcu-lated is often unclear from the data provided.

COST SHARINGAs the industry has evolved, PBMI has noted changes in

how cost sharing is used in drug benefit programs.Employers and PBMs are developing new ways to categorizedrugs for cost sharing purposes. Table 18 illustrates howplan sponsors commonly group drugs for reimbursement.

Because only 11% of the respon-dents are not using a formulary, PBMIdecided to interview some of theseemployers to better understand theirreasons for not doing so. The inter-viewees tended to fall into two cate-gories. The first group, relativelysmall employers, does not have manyresources directed toward managingthe drug benefit. These employersplan to slowly work toward adopting a

formulary. The second category iscomprised of employers that believethey have been able to accomplishtheir benefit management goals with-out implementing a formulary. Theseemployers view formularies as having apotentially negative impact if imple-mented. These employers tend to bemore concerned about encouraginggeneric drug use than encouragingone branded drug over another.

Region Percentage of Total Rebate DollarsUnknown 75%Northeast 84%South 80%Midwest 76%West 76%Total 79%

Table 16: Percentage of Total Rebate Dollars by Geographic Region

Employer Size Percentage of Total Rebate DollarsUnreported 97%1 - 2,000 64%2,001 - 4,000 66%4,001 - 6,000 81%6,001 - 10,000 82%10,001 - 20,000 73%20,001 - 50,000 87%50,001 + 91%Total 79%

Table 17: Percentage of Total Rebate Dollars by Employer Size

11% of Respondents Do Not Use a Formulary

Year Percentage of Total Rebate Dollars2002 79%2001 73%

Table 15: Percentage of Total Rebate Dollars by Year

11

Retail copayments increased by approximately 10% forall tiers from 2001 to 2002. Average retail copayments aredisplayed in Table 19. These increases are more pronouncedin mail as shown in Table 20. From 2001 to 2002, averagefirst-tier mail service copayments increased by 16%, second-tier increased by 20%, and third-tier by 10% as shown inTable 20.

To provide the reader with some perspective about thescope of change over the past four years, PBMI has providedthe distribution of second-tier copayments for both retail(Table 21) and mail (Table 22). The use of retail second-tiercopayments of more than $20 is now 17%. For mail service,the percentage of copayments $40 or more is 39%.

Employers understand that cost sharing is a valuable toolto encourage patients to behave in certain ways. For example,one of the purposes of having multiple copayment tiers is toencourage generic drug use. Today, the retail third-tiercopayment (where most plans categorize multi-source branddrugs) is almost four times as high as the first-tier copay-

ment. This is compared to 1998 when the third-tier copay-ment was less than three times the first-tier copayment.

In the past, mail service copayments were kept low rela-tive to retail copayments to encourage mail service use. Thebelief was that mail service was a lower cost distribution pointfor prescriptions. However, employers have learned thatmail service will not produce savings unless copayments arestructured appropriately. Many employers discovered thatsetting mail copayments too low compared to retail copay-ments may result in mail service prescriptions costing moreto the employers after the cost-sharing amount is collectedthan retail prescriptions.

Because mail service copayments have increased morequickly than retail copayments for the last few years, this isnot as much an issue as in the past. The mail service second-tier copayment is now 1.8 times the retail second-tier copay-ment. This is as compared to 1.6 times in 2001.

Many experts believe, as a rule of thumb, mail servicecopayments should be at least twice the retail copayment.

Survey Average Copayment AmountsYear 1st Tier 2nd Tier 3rd Tier2002 $8.33 $17.57 $33.232001 $7.68 $16.06 $30.512000 $7.17 $14.14 $27.351999 $7.05 $12.82 $23.40

Table 19: Average Retail Copayment Amounts for All Respondents

Survey Average Copayment AmountsYear 1st Tier 2nd Tier 3rd Tier2002 $14.58 $31.18 $60.682001 $12.60 $26.01 $55.232000 $10.78 $21.29 $45.731999 $9.74 $17.96 $37.67

Table 20: Average Mail Service Copayment Amounts for All Respondents

Copayment by Dollar Amount 2002 2001 2000 1999 1998 1997< $10 7% 10% 13% 19% 26% 30%$10-$11 11% 12% 22% 30% 36% 37%$12-$13 4% 8% 8% 8% 8% 13%$14-$15 24% 27% 28% 26% 20% 18%$16-$20 38% 34% 25% 16% 10% 4%> $20 17% 10% 4% NC NC NCNC: Not Calculated indicates that value is previously included in other categories.

Table 21: Distribution of Employer Retail Second-Tier Copayments by Dollar Amount

Tier Two-Tier Design Three-Tier Design Three-Tier Design Four-Tier DesignFirst Tier Generic Generic Generic GenericSecond Tier Brand Single Source Brand Preferred Brand Preferred BrandThird Tier NA Multiple Source Brand Non-Preferred Brand Non-Preferred BrandFourth Tier NA NA NA Biotech drugs, lifestyle,

nonformulary, or other high cost drugs

NA=Not Applicable

Table 18: Common Plan Designs for Multi-Tier Copayments

12

However, PBMI believes this will change. PBMI noted manycopayments are now more than $25. If the 90-day mail serv-ice copayment is set as the equivalent of two 30-day retailcopayments, then the average mail service claim must savemore than $25 before the plan sponsor receives any savings.

Three-Tier CopaymentsThe use of a three-tier plan design, in which the tiers are

based on formulary status, continues to gain favor amongemployers. In 1998, only 6% of employers reported the useof this three-tier plan design. This number has increasedfrom 46% in 2001 to 63% in 2002. Likewise, the percent-age of employers who offer two-tier cost sharing schemesdeclined from 47% in 2001 to 30% in 2002. It is expectedthat the industry will continue to see growth in the percent-age of employers offering three-tier plan designs.Interestingly, the use of a three-tier plan based on the type ofdrug (e.g., generic, single-source brands, and multi-sourcebrands) has remained constant at 7% for the third year in arow. These percentages are based upon respondents who usecopayments rather than coinsurance percentages.

Four-Tier CopaymentsThis year, 19 respondents reported a fourth tier for cost

sharing. This copayment amount is in many instances equalto the entire cost of the drug. In some cases, this category isused for lifestyle drugs; in other cases the category representsnonformulary drugs. New this year, three respondents iden-tified biotech drugs as a specific copayment category.

CoinsuranceThe percentage of employers using coinsurance for sec-

ond-tier, retail cost sharing increased from 22% in 2001 to26% in 2002. Although most employers who use coinsur-ance generally use coinsurance for all drug categories, someemployers use coinsurance only for second- or third-tierdrug prescriptions, but not for first-tier drug prescriptions.This approach for the second- and third-tiers allows plansmore flexibility ensuring patients pay a consistent portion ofthe benefit cost, while providing an additional incentive touse generic drugs.

Coinsurance often is used in combination with a mini-mum and/or maximum copayment amount. Some respon-

0%10%20%30%40%50%60%70%80%90%

100%

Third Tier

Second Tier

First Tier

MinimumAverageMaximum

50% 50%

100%

18%23%

41%

0% 0%

15%

Figure 6: Range of Mail Service Coinsurance Percentages for Each Tier

Copayment by Dollar Amount 2002 2001 2000 1999 1998<$15 11% 18% 28% 34% 47%$15-$19 7% 10% 15% 21% 18%$20-$24 15% 18% 21% 21% 19%$25-$29 7% 9% 7% 6% 16%$30-$34 18% 19% 16% 13% NC$35-$39 3% 27% 14% 5% NC$40-$44 24% NC NC NC NC> $44 15% NC NC NC NCNC: Not Calculated indicates that value is previously included in other categories.

Table 22: Distribution of Mail Service Second-Tier Copayments by Dollar Amount

0%10%20%30%40%50%60%70%80%90%

100%

Third Tier

Second Tier

First Tier

MinimumAverageMaximum

50% 50%

100%

19%23%

37%

0%10%

15%

Figure 5: Range of Retail Coinsurance Percentagesfor Each Tier

13

dents use one or the other and some use both. The averageminimum copayment is slightly less than the overall averagefor all respondents ($16.43 vs. $17.57). Although used lessfrequently, the average maximum copayment ($41.91) isalmost three times the average minimum copayment.

On average, beneficiaries pay about 19% of the cost oftheir retail prescription for drugs in the first tier, 23% fordrugs in the second tier, and 37% for drugs in the third tieras shown in Figure 5. The use of the three-tier copaymentstructure has encouraged employers to differentiate the coin-surance percentage among the three categories. Using ahigher percentage coinsurance for the third tier increases theincentive to use lower cost drugs in the first tier.

Coinsurance is used much less frequently for mail serv-ice. Only 12% of the respondents have a coinsurance com-ponent for second-tier mail service prescriptions. Althoughthe barriers related to using coinsurance in mail service havebeen eliminated at most mail service pharmacies, manyemployers are reluctant to require their patients to pay acopayment that may vary by prescription and over time. SeeFigure 6 for more information about the coinsurance per-centages reported.

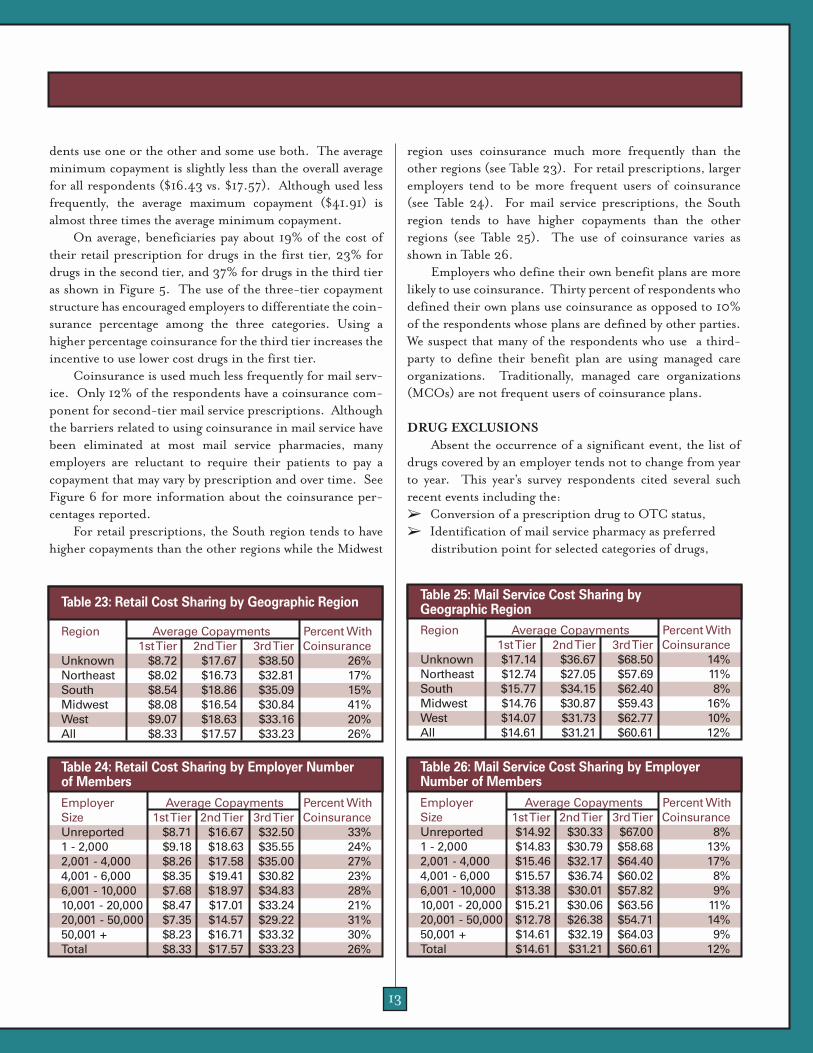

For retail prescriptions, the South region tends to havehigher copayments than the other regions while the Midwest

region uses coinsurance much more frequently than theother regions (see Table 23). For retail prescriptions, largeremployers tend to be more frequent users of coinsurance(see Table 24). For mail service prescriptions, the Southregion tends to have higher copayments than the otherregions (see Table 25). The use of coinsurance varies asshown in Table 26.

Employers who define their own benefit plans are morelikely to use coinsurance. Thirty percent of respondents whodefined their own plans use coinsurance as opposed to 10%of the respondents whose plans are defined by other parties.We suspect that many of the respondents who use a third-party to define their benefit plan are using managed careorganizations. Traditionally, managed care organizations(MCOs) are not frequent users of coinsurance plans.

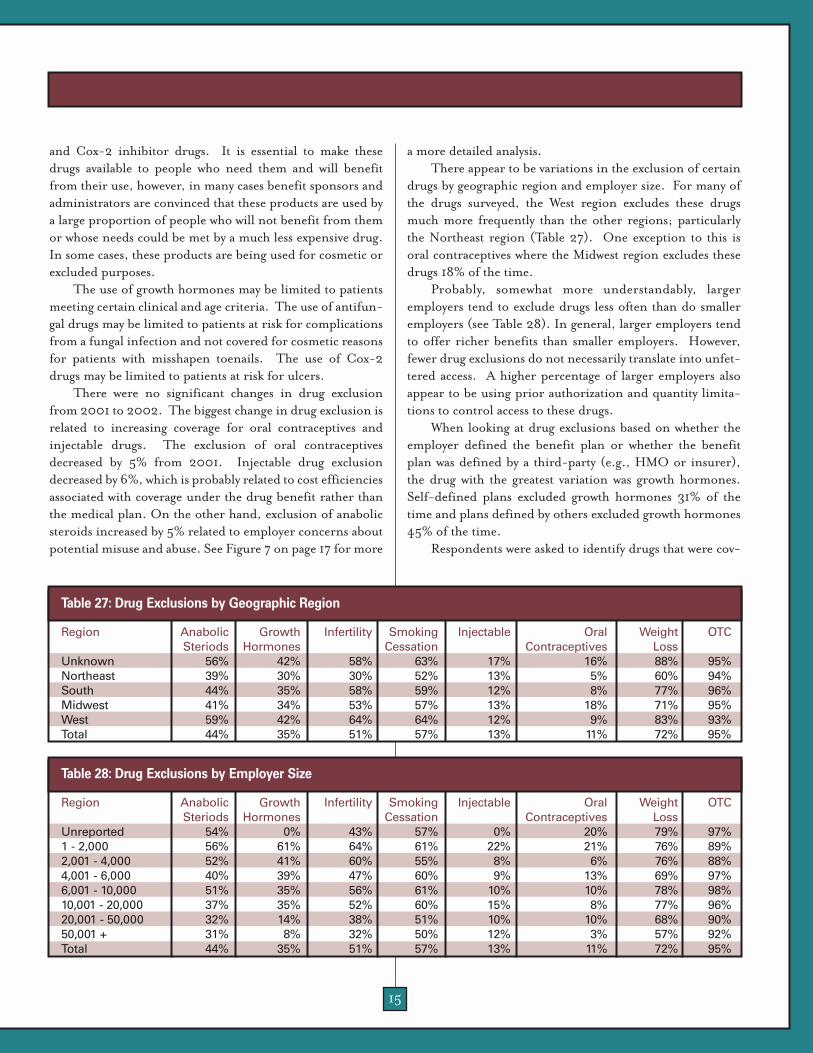

DRUG EXCLUSIONSAbsent the occurrence of a significant event, the list of

drugs covered by an employer tends not to change from yearto year. This year’s survey respondents cited several suchrecent events including the: ➢ Conversion of a prescription drug to OTC status, ➢ Identification of mail service pharmacy as preferred

distribution point for selected categories of drugs,

Employer Average Copayments Percent WithSize 1st Tier 2nd Tier 3rd Tier CoinsuranceUnreported $8.71 $16.67 $32.50 33%1 - 2,000 $9.18 $18.63 $35.55 24%2,001 - 4,000 $8.26 $17.58 $35.00 27%4,001 - 6,000 $8.35 $19.41 $30.82 23%6,001 - 10,000 $7.68 $18.97 $34.83 28%10,001 - 20,000 $8.47 $17.01 $33.24 21%20,001 - 50,000 $7.35 $14.57 $29.22 31%50,001 + $8.23 $16.71 $33.32 30%Total $8.33 $17.57 $33.23 26%

Table 24: Retail Cost Sharing by Employer Number of Members

Employer Average Copayments Percent WithSize 1st Tier 2nd Tier 3rd Tier CoinsuranceUnreported $14.92 $30.33 $67.00 8%1 - 2,000 $14.83 $30.79 $58.68 13%2,001 - 4,000 $15.46 $32.17 $64.40 17%4,001 - 6,000 $15.57 $36.74 $60.02 8%6,001 - 10,000 $13.38 $30.01 $57.82 9%10,001 - 20,000 $15.21 $30.06 $63.56 11%20,001 - 50,000 $12.78 $26.38 $54.71 14%50,001 + $14.61 $32.19 $64.03 9%Total $14.61 $31.21 $60.61 12%

Table 26: Mail Service Cost Sharing by Employer Number of Members

Region Average Copayments Percent With1st Tier 2nd Tier 3rd Tier Coinsurance

Unknown $8.72 $17.67 $38.50 26%Northeast $8.02 $16.73 $32.81 17%South $8.54 $18.86 $35.09 15%Midwest $8.08 $16.54 $30.84 41%West $9.07 $18.63 $33.16 20%All $8.33 $17.57 $33.23 26%

Table 23: Retail Cost Sharing by Geographic Region

Region Average Copayments Percent With1st Tier 2nd Tier 3rd Tier Coinsurance

Unknown $17.14 $36.67 $68.50 14%Northeast $12.74 $27.05 $57.69 11%South $15.77 $34.15 $62.40 8%Midwest $14.76 $30.87 $59.43 16%West $14.07 $31.73 $62.77 10%All $14.61 $31.21 $60.61 12%