the promise of natural gas as a transportation fuel · beliefs of westport’s management and...

TRANSCRIPT

The Promise of Natural Gas as a Transportation Fuel

Forward Looking Statements•

This presentation contains forward‐looking statements that are based on the

beliefs of Westport’s management and reflect Westport’s current expectations.

Investors are cautioned that all forward‐looking statements involve risks and

uncertainties that could cause actual results to differ materially from those

expressed in these forward‐looking statements, including, without limitation,

Westport’s ability to develop viable fuel systems; Westport’s ability to provide the

capital required for research, product development, operations, and marketing;

product development, production and commercial launch delays; changing

environmental regulations; Westport’s ability to attract and retain key personal

and business partners; competition from conventional diesel fueled

engines; and

Westport’s ability to protect its intellectual property. These factors should be

considered carefully and investors should not rely on any forward‐looking

statements. Investors are encouraged to review Management’s Discussion and

Analysis and the Risk Factors section in Westport’s most recently filed Annual

Information Form and filings with securities regulators for a more complete

discussion of factors that could affect Westport’s future performance. We

undertake no obligation to update or revise any forward‐looking statements,

whether as a result of new information, future events or otherwise, except as

required by law.

2

3

Westport at a Glance•

Headquartered in Vancouver, B.C.•

Exchange

Symbols:

Toronto

Stock

Exchange:

“WPT”NASDAQ: “WPRT”

•

Market cap:

~$400 million (~US$370 million)

•

Market focus:

Transformation of markets for petroleum‐fueled

engines to alternative fuels

•

Position:

Global leader in medium and heavy‐duty

commercial vehicle engines operating on

alternative fuels such as natural gas

•

Strategy:

Market penetration via partnerships and JV’s; All

manufacturing outsourced

4

11

$0

$25

$50

$75

$100

$125

FY 2005 FY 2006 FY 2007 FY 2008 FY2009N. America Asia Rest of World Westport HD

4

Summary Historical Financial Overview

1,277 1,327

2,001

2,720

4,038

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY 2005 FY 2006 FY 2007 FY 2008 FY2009

Total Unit SalesRevenue

(CAN$ millions; Westport Fiscal Year Mar 31)

$43.6

$60.5

$71.5

$34.4

$121.8

5

Deep and Comprehensive IP

•

One of Canada’s leading R&D

companies •

Global patent portfolio

pivotal to Westport’s market

leading position –

Covers all key areas of

engine deployment

•

59 issued U.S. patents as of

January, 2009; many new

applications pending under

the international Patent

Cooperation Treaty

Compressors

HPDI

Cryogenic Storage / Delivery

CNG Direct Injection

Technologies

Hydrogen Direct Injection

Aftertreatment Systems

Recognized Sustainability Leadership

6

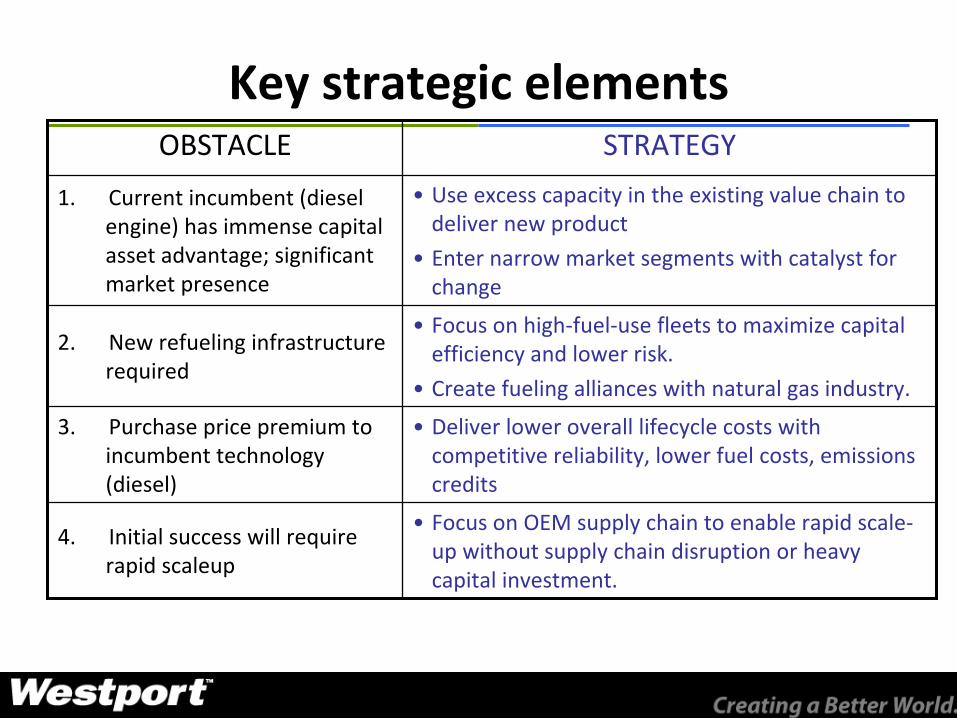

Key strategic elements OBSTACLE STRATEGY

1. Current incumbent (diesel

engine) has immense capital

asset advantage; significant

market presence

•

Use excess capacity in the existing value chain to

deliver new product

•

Enter narrow market segments with catalyst for

change

2. New refueling infrastructure

required

•

Focus on high‐fuel‐use fleets to maximize capital

efficiency and lower risk.

•

Create fueling alliances with natural gas industry.

3. Purchase price premium to

incumbent technology

(diesel)

•

Deliver lower overall lifecycle costs with

competitive reliability, lower fuel costs, emissions

credits

4. Initial success will require

rapid scaleup

•

Focus on OEM supply chain to enable rapid scale‐

up without supply chain disruption or heavy

capital investment.

An ‘Ocean’

of Opportunity for Natural GasPrice History for Crude Oil, Diesel Fuel, and NYMEX Natural Gas Contracts

$-

$20

$40

$60

$80

$100

$120

$140

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Dai

ly C

rude

Oil

Spot

Pric

e, C

ushi

ng, O

K W

TI S

pot P

rice

FOB

[Dol

lars

per

Ba

rrel

]

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

Ret

ail D

iese

l and

Nat

ural

Gas

Pric

es [D

olla

rs p

er D

iese

l-equ

ival

ent G

allo

n]

Cushing, OK WTI Spot Price FOB (EIA) [Dollars per Barrel]

U.S. No 2 Diesel Retail Sales by All Sellers (EIA) [Dollars per Gallon]

NYMEX Natural Gas Futures Contract 1 (EIA) [$/DEG]

data source: US DOE Energy Information Administration

last update Sept. 3, 2009

8

Global Leader: Natural Gas Bus and Truck Engines

Refuse HaulersTransit Buses Delivery Vehicles School Buses

9

Only certified manufacturer in North America

CWI Business Model

• 50:50 JV established in 2001

• Sells mid-range 5.9- to 8.9-liter engines to vehicle OEM’s globally

• 20,000+ natural gas engines sold to date

• 30% revenue CAGR since 2004 and profitable since 2004

• Cummins provides:

• base diesel engine, components, supply chain

• sells, produces, and services engines

• all working capital

A leader in gaseous fuel engine technology and

market creation

A leading independent builder of commercial

diesel engines with global production and distribution

Cummins Westport Inc

10

CWI OEM Applications TodayREFUSESPECIALTY BUSTRUCK

New ISL G Truck Availability 08‐09

Freightliner M2 – 112 May 2009

Mack Australia April 2009

Capacity September 2008

McNeilus May 2009

Mack June 2009

Peterbilt July 2009

Sterling Setback 113 June 2008

12

•Buses extremely fuel intensive

•Fuel is a major operating cost

•1995 –

2005: Environmental mandate

•Today: Economic savings

•Share taken from diesel to CNG

– CNG 10 year CAGR 28%

– Diesel 10 year CAGR 0.7%

Source: US DOE; APTA Data Book April 2007

Case Study: CNG Transit Bus Adoption in US 1995–2005

Diesel68%

Electricity15%

CNG12%

Gasoline5%

Diesel77%

Electricity15%

CNG1%

Gasoline7%

0

100

200

300

400

500

600

700

800

900

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 20050

20

40

60

80

100

120

140

Diesel Electricity Gasoline CNG

U.S. Transit Energy Consumption Mix - 1995 U.S. Transit Energy Consumption Mix - 2005

Total transit bus fuel consumption

(diesel gallon equivalent)

CNG transit bus fuel consumption

(diesel gallon equivalent)

13

CWI’s Future Objectives

•

Continue to profitably compound revenue at rolling 30% CAGR

•

2009: expected growth although considerably slower than 2008. Several bright spots:

–

New truck product launch (Freightliner, Mack, Peterbilt)

–

Bus engines in India: deliver Delhi order (through Apr/10)

and expand market –

US Stimulus programs (DOE Clean Cities, etc)

–

Port programs

•

2010: growth acceleration with economic recovery

World Truck Production 2007 ranked by >16t volumes

0 50 100 150 200 250 300 350 400 450 500

Daimler

Volvo

Paccar

CNHDTC

FAW

Dongfeng

MAN

Scania

Tata

Iveco

Shanxi Automobile

Kamaz

Navistar

Hino

SAIC

VW

Hyundai

Isuzu

Ford

Ashok Leyland

Beijing

GM

Anhui

Eicher Motors

Chengdu Wangpai

all others

World truck production 2007 [thousands]

6-16 tonnes>16 tonnes

data source: The World’s Truck Manufacturers, A strategic review of finance and operations, 11th Edition (2008), Edited by Jonathan Storey, Data by Polk-Marketing Systems, Published by Automotive World Ltd, www.automotiveworld.com

15

NG Products supplied by WPT/CWI

North America Heavy Duty Truck Volumes

Market for Heavy Duty Trucks – North America

140.1 146 141

203

252284

151 145

0

100

200

300

2001 2002 2003 2004 2005 2006 2007 2008

Num

ber o

f Tru

cks

/ Yea

r (00

0 un

its)

Source: www.nada.org

16

18

Direct Injection Fuel System

•

Proprietary and patented

technology; 9 years

development; >$100 million

R&D to date

•

Complete LNG fuel solution

integrated with engine

•

Only heavy‐duty truck natural

gas engine in the world with

diesel‐equivalent performance,

range, efficiency

Status 2009: Prepare for Growth

•

Significant on‐road HD presence in California for over 12 months including at Los Angeles Ports

•

Very good market feedback to date–

Truck performance “as good or better”

than diesel equivalent–

Mileage equivalent; fuel is cheaper–

Drivers prefer natural gas trucks

•

Primary obstacles: capital cost premium; shortage of infrastructure

–

Truck market generally remains extremely depressed; credit

challenges remain

–

Natural gas infrastructure maturing nationally; capable of

supporting 1,000’s of trucks; “Blue corridors”

emerging–

Capital cost: NATGAS ACT; Westport cost reduction

19

HD Engines in Europe

Freightliner M2 – 112 (Daimler) May 2009

Mack and Mack Australia (Volvo) Renault France

June 2009

20

•

Leading European diesel engine manufacturers

Daimler and Volvo have both launched products with

our CWI natural gas engines this year for North

America

•

Westport announced summer 2008 material

investment in engineering for the “leading European

engine company”

•

Unique European challenges: both oil and gas supply

concerns; greenhouse gas an immediate issue; fuel

prices high and rising

•

Biomethane

a promising energy source with

significant recent success

•

Recent focus on the truck opportunity for both

emissions and energy security benefits

•

Advantages for Westport are compelling if one or

more of the integrated major OEM’s partners with us

Weichai Westport: HD Engines in China

Hong Kong Peterson (CNG) Equipment Limited

35% share40% share

25% share

21

•

Joint venture announced to develop a new heavy‐duty engine

for the market in China with Westport’s HPDI technology•

Weichai highlights include:–

Biggest powertrain

manufacturer in China –

Owns the most integrated heavy‐duty vehicle value

chain in China

•

JV not yet legally approved but engineering

collaboration underway

Corporate Structure

22

•

Formed in October 2007–

Headquartered in

Vancouver, Canada

–

Joint venture between

Westport (49%) and OMVL

SpA

(51%), subsidiary of

SIT Group

•

Juniper will be the leading clean light‐

duty industrial engine provider–

Leveraging parent strengths and

competencies

–

Global focus, competitive pricing–

Long term supply partnership with

Hyundai of Korea

–

EPA & CARB 2010 certification

•

Start of Production target 2010

23

Looking Ahead

24

2009/10 Market Transition: Environmental Niche to Economic Mainstream

•

Global OEM’s increasingly seeing customer demand for lower‐cost fuel such as natural gas

•

New government policy encourages alternative fuel vehicle adoption and market penetration

–

U.S. NAT GAS Act proposing significant tax incentives for natural gas

trucks (Senate Bill 1408)

–

August 2009 DOE announcement awarding Clean Cities funding for up

to 2800 natural gas vehicles

•

Early markets reaching confidence in our products and solutions

Westport Strategy for 2009/101.

Continue to profitably grow CWI

2.

Expand product coverage to new markets, partners, product features to position for scaleable growth post‐

recession

3.

Accelerate commercialization of HD Truck business to demonstrate lower total economic cost per mile in this

huge global market.

4.

Maintain prudent, focused cash control and strong balance sheet. Review the many compelling emerging

opportunities; act on strategic priorities.

25

Thank you