the public dsa framework for market access countries

TRANSCRIPT

The Public DSA Framework for The Public DSA Framework for Market Access CountriesMarket Access Countries

Instructor: Adina Popescu (IMF)

LEARNING OBJECTIVES ANDUnit 1

LEARNING OBJECTIVES AND STRUCTURE OF PART 2

“This training material is the property of the International Monetary Fund and is intended for use in IMF Institute for Capacity Development courses. Any reuse requires the permission of the IMF. The views expressed in this material are those of the course staff and do not necessarily represent those of the IMF or IMF policy.”

U1 V1U1.V1

Content and Goals of Part 2

U1 V2U1.V2

A History of Debt and Growth:Understand the past, chart theUnderstand the past, chart the

Future (IMF Video)

DEBT SUSTAINABILITY IN MARKETUnit 2

DEBT SUSTAINABILITY IN MARKET ACCESS COUNTRIES

U2 V1U2.V1

What is the MAC DSA ?

What is the MAC DSA ?What is the MAC DSA ?

Description ApproachTimelineDescription

� Part of the IMF’s framework for debt sustainability analysis

ApproachTimeline

debt sustainability analysis

� Designed and followed by the IMF to assess public debtIMF to assess public debt sustainability in market access countries (MACs)

� In the context of both surveillance and program d i / idesign/reviews

MAC DSA TimelineMAC DSA Timeline

Definition ApproachTimelineDefinition ApproachTimeline

The MAC DSA AproachThe MAC DSA Aproach

Definition ApproachTimeline

�A formal and

Definition ApproachTimeline

A formal and standardized tool

� Implemented through an gExcel based template

Who are Market Access Countries?Who are Market Access Countries?

C t i ith• Countries with significant access to international capitalinternational capital markets on a durable and sustainable basis

• De facto all advanced economies and mostemerging markets

U2 V2U2.V2

Assessing Sustainability in the MAC DSA

How is Debt Sustainability Assessed in the MAC DSA ?

• Solvency

• Liquidity

• Realistic adjustmentadjustment

What is Solvency ?

Th t d bt t k i f ll Th t ill b bl t

What is Solvency ?

The current debt stock is fully covered by the present discounted value of all expected future primary

balances

The government will be able to service the debt in the short,

medium and long run without renegotiating or defaultingbalances renegotiating or defaulting

SOLVENCY

The debt burden indicators are

SOLVENCY

The debt burden indicators are projected to either stabilize or

decline - in the baseline scenario and under plausible shock scenarios

What is Liquidity ?

L l d t j t f d bt b d

What is Liquidity ?

Available financing and liquid assets are sufficient to meet maturing

obligations

Level and trajectory of debt burden indicators facilitate continued

market access and rollover risk is lowlow

LIQUIDITY

h d b f l ll b l d

LIQUIDITY

The debt profile is well balanced in terms of: maturity, currency

composition, and investor base

What is Realistic Adjustment ?What is Realistic Adjustment ?

Realistic macroeconomic assumptions and projections for the

primary balance adjustment

Adjustment is economically and politically feasible

REALISTIC ADJUSTMENT

Potential growth is preserved at a satisfactory level

Caveats …Caveats …

• DSAs involve probabilistic judgments• DSAs involve probabilistic judgments about the trajectory of debt and the availability of financing on favorable terms

• DSAs should not be interpreted in a mechanistic or rigid fashionmechanistic or rigid fashion

• DSAs should take into considerationDSAs should take into consideration country-specific circumstances

U2 V3U2.V3

What are the Benchmarks in the MAC DSA?

Main Features of the MAC DSA TemplateMain Features of the MAC DSA Template

• A complex and multifaceted exerciseA complex and multifaceted exercise

• Highlights the risks and uncertaintyHighlights the risks and uncertainty surrounding the central forecast

• Is “risk-based” - more analysis required for countries with greater q gvulnerabilities

Lower versus Higher ScrutinyLower versus Higher Scrutiny

• Lower scrutiny

Countries are classified as:

Lower scrutiny

• Higher scrutiny

on the basis of:

• a set of benchmarks of debt burden and other indicatorsburden and other indicators

• access to Fund resources

What Are the Benchmarks for Classification ?What Are the Benchmarks for Classification ?

f fPublic debt level

> 50% of GDP for EMs> 60% of GDP for AEs> 10% of GDP for EMs

Public gross financing needs> 10% of GDP for EMs> 15% of GDP for AEs

Exceptional access to IMFExceptional access to IMF

Early Warning ModelsEarly Warning Models

• Benchmarks estimated from “early warning models”

• These identify the level of the• These identify the level of the indicators which best predict the occurrence of a crisis

• The MAC DSA benchmarks are conservative estimates (about 15conservative estimates (about 15 percent less than the model estimates)

However …However …

• Debt problems ma emerge• Debt problems may emerge at lower debt burden levels than the ones suggestedthan the ones suggested above (particularly for EMs)

• Other indicators may point to emerging vulnerabilitiesto emerging vulnerabilities

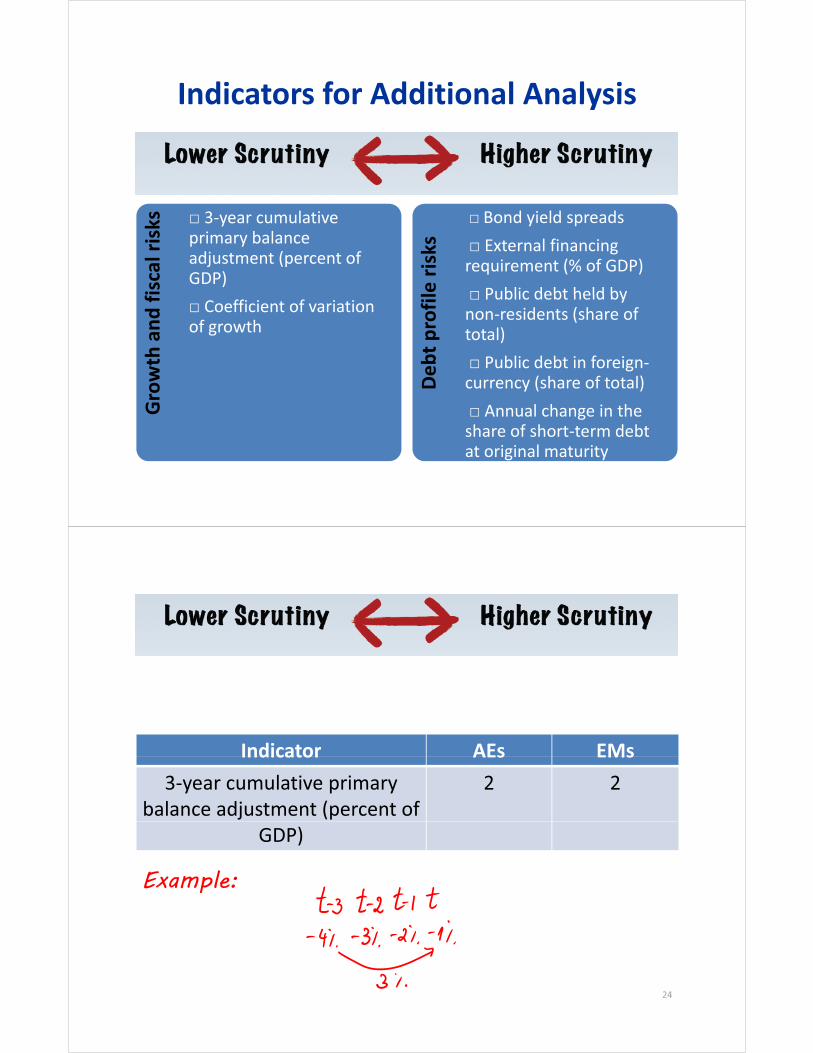

Indicators for Additional AnalysisIndicators for Additional Analysis

sks � 3-year cumulative � Bond yield spreads

isca

l ris primary balance

adjustment (percent of GDP)

le ri

sks � External financing

requirement (% of GDP)� Public debt held by

th a

nd f � Coefficient of variation

of growth

bt p

rofil � Public debt held by

non-residents (share of total)� Public debt in foreign

Gro

wt

Deb � Public debt in foreign-

currency (share of total)� Annual change in the h f h d bshare of short-term debt

at original maturity

Indicator AEs EMsIndicator AEs EMs3-year cumulative primary

balance adjustment (percent of 2 2

GDP)

Example:Example:

24

Indicator AEs EMsCoefficient of variation of

growth1 1

Coeff. of variation = Standard deviation�Mean

Indicator AEs EMsBond yield spreads or EMBI global spreads (basis points)

600 600

Spread over US or German

JP Morgans'sEMBI

bondsEMBI

Indicator AEs EMsExternal financing

requirements (percent of GDP)25 15

Externall financingg requirementss =External financing requirements ST External debt + Amortization of MLT external debt - Current account balance

Indicator AEs EMsPublic debt held by non- 45 45yresidents (share of total)

Public debt in foreign currency n.a. 60(share of total)

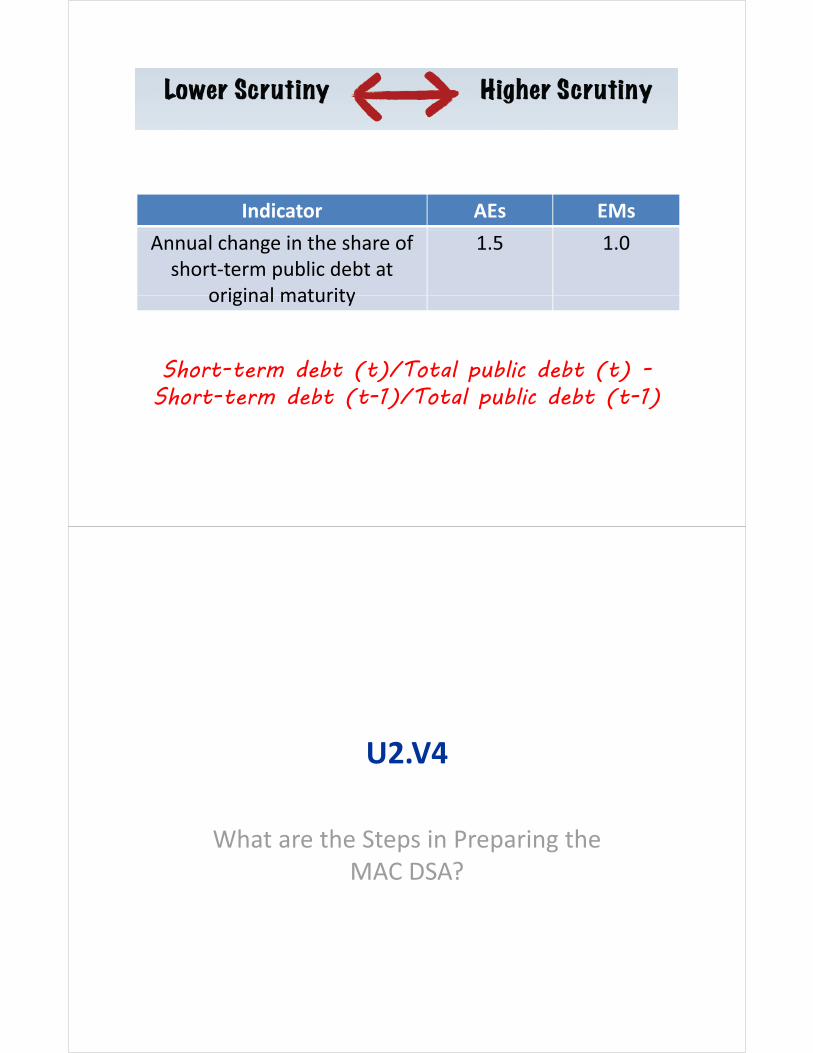

Indicator AEs EMsAnnual change in the share of

short-term public debt at original maturity

1.5 1.0

original maturity

S d dShort-term debt (t)/Total public debt (t) -Short-term debt (t-1)/Total public debt (t-1)

U2 V4U2.V4

What are the Steps in Preparing the MAC DSA?

Roadmap: the MAC DSA Template

Lowerr scrutinyLower scrutinycountries

Higherr scrutinyHigher scrutinycountries

Basic DSA

Customized

Standardized alternative

alternative scenarios

Baseline scenario

alternative scenarios

(contingent liabilities)

Risk Identification and Analysisy

Vulnerability

Sensitivity

Contingent liabilities

yof the debt profile

Realism of baseline

Sensitivity to macro-fiscal risks

baseline scenario

Risk ReportingRisk Reporting

Write-up

Fan charts

p

Heat map

DATA: COVERAGE, ISSUES, SOURCESUnit 3

DATA: COVERAGE, ISSUES, SOURCES

U3 V1U3.V1

Data Coverage and Issues

Issues Related to Coverage of Public Debt

Coverage of the publicCoverage of the public

Issues Related to Coverage of Public Debt

Coverage of the public Coverage of the public sectorsector

Gross versus net debtGross versus net debtGross versus net debtGross versus net debt

LongLong--term spending term spending pressures pressures

The Coverage of the Public Sector: hThe Issue

Sub-national governments

Contingent li bilitigovernments liabilities

Bailouts

State-owned enterprises (SOEs)

Bailouts

Offset fiscalenterprises (SOEs)Public-private

partnerships (PPPs)

Offset fiscal adjustments efforts

Example: PortugalExample: PortugalThe reclassification of reclassifications of SOEs and PPPs into the general government has weighed on the sizableinto the general government has weighed on the sizable increase in general government debt

Source: IMF

Public Sector Coverage: GuidelinesPublic Sector Coverage: Guidelines

The coverage of public debt in the DSA g pshould be:

• as broad as possible, ideally based on the entire public sector

• one should try to add, at least, high-risk public enterprisespublic enterprises

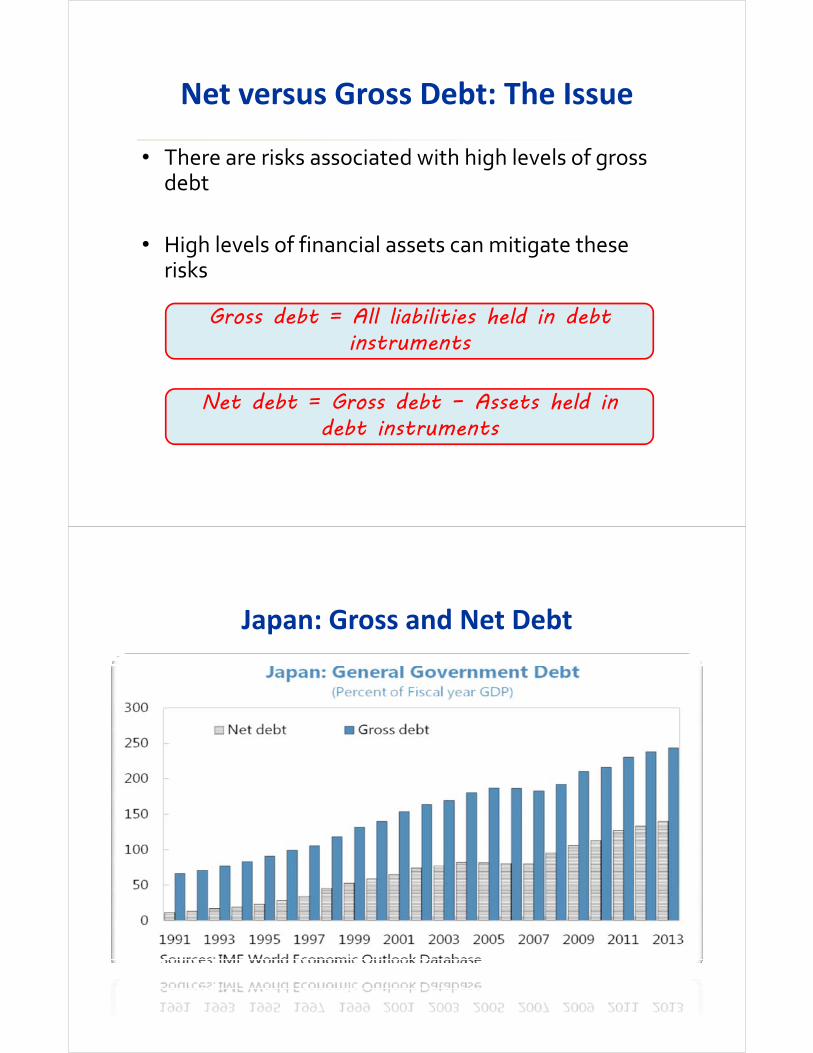

Net versus Gross Debt: The IssueNet versus Gross Debt: The Issue

• There are risks associated with high levels of gross g gdebt

• High levels of financial assets can mitigate these risks

Gross debt = All liabilities held in debt instruments

Net debt = Gross debt – Assets held in d bt in t um ntdebt instruments

Japan: Gross and Net DebtJapan: Gross and Net Debt

Net versus Gross Debt: GuidelinesNet versus Gross Debt: Guidelines

Th MAC DSA i b d• The MAC DSA is based on gross debt

• Net debt – complementary p ymeasure

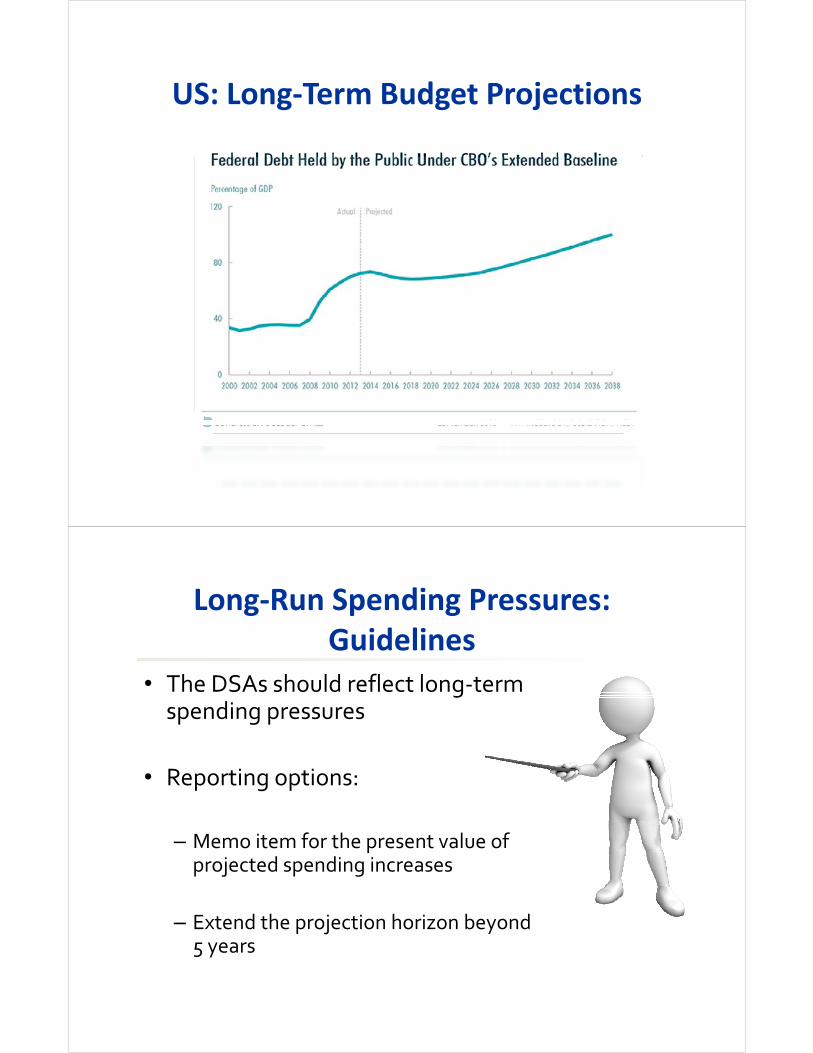

Long-Run Spending Pressures: The IssueLong Run Spending Pressures: The Issue

Long-run spending pressurespressures

Pensions Health-care

US: Long-Term Budget ProjectionsUS: Long Term Budget Projections

Long-Run Spending Pressures: d lGuidelines

• The DSAs should reflect long-term gspending pressures

• Reporting options:

– Memo item for the present value of projected spending increases

– Extend the projection horizon beyond 5 years5 years

U3 V2U3.V2

MAC DSA Template: Introductory Video

THE BASELINE SCENARIOUnit 4

THE BASELINE SCENARIO

U4 V1U4.V1

How to Construct the Baseline Scenario ?

Constructing a Baseline ScenarioConstructing a Baseline Scenario

Macroeconomic framework

the most likely scenario - for surveillance countries - based on

current and projected governmentcurrent and projected government policies

the programmed macroeconomic adjustment - for program countries

Generic Debt Dynamics Equationautomatic debt dynamics

Generic Debt Dynamics Equationresidual

ttttt resopbdd ������ �1* )1(�

debt/GDP ratio

primary balance

th id tifi d

o Privatization receipts o Recognition of implicit

other identified debt-creating

flows

g por contingent liabilities

o Other (e.g. bank recapitalization)p )

What Drives the Debt-to-GDP Dynamics ?What Drives the Debt to GDP Dynamics ?

Contribution of Contribution real GDP growth of the primary

balance

�� td��

����

)1)(1()1(

tt

ttwt

ggi

)1)(1( tt

t

gg

��� 1

1

)1)(1()1(

��

��

���

� ttt

fttt d

gi

��...�� tpb

Contribution of Cont ibution ofContribution of effective real interest rate

Contribution of exchange ratedepreciation

ExampleExample10

Debt-Creating Flows (i t f GDP)

30

40

5(in percent of GDP)

10

20

0

-20

-10

0

-5

-40

-30

-10t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10Primary deficit Real GDP growthReal interest rate Exchange rate depreciation

-50cumulative

Real interest rate Exchange rate depreciationOther debt-creating flows ResidualChange in gross public sector debt

Where Do Residuals Come From ?

sales/purchases of financial

changes in gross debt arising from below-the-line

sales/purchases of financial assets

from below the line operations

“one-off” factors affecting the stock of debt

th f diff t d fi itithe use of different definitions for the stock of debt and the

fiscal balance

cross-currency movements

U4 V2U4.V2

MAC DSA Template: The Baseline Scenario

REALISM OF THE BASELINEUnit 5

REALISM OF THE BASELINE ASSUMPTIONS

U5 V1U5.V1

How to Evaluate the Forecast Track Record ?

Realism Tools Does in the MAC DSA

R li f ti

Realism Tools Does in the MAC DSA

Realism of macro-assumptions• Examines the track record in

projecting macroeconomicprojecting macroeconomic variables

Realism of fiscal adjustment• Assesses the realism of projected

fiscal adjustments

Boom-bust analysis• Assesses growth projections in

countries that may have entered acountries that may have entered a boom-bust cycle

Realism of Macro-AssumptionsRealism of Macro Assumptions

The DSA template automatically produces

• charts• statistics

The DSA template automatically produces

statistics

for the forecast track record for

• real GDP growth• primary balance• inflation• inflation

by comparing forecast errors for a country to the distribution of forecast errors for other MACs

What is the Forecast Track Record ?

Forecast error (t) = Actual (t,t+2) - Projection (t,t-1)

Summary StatisticsSummary Statistics

in the distribution of median forecastof median forecast errors of all MACs

How to Interpret the Forecast Errors ?p

SuggestSuggest systematic

projection bias

Calibrate li tirealistic

baselineprojectionsp j

U5 V2U5.V2

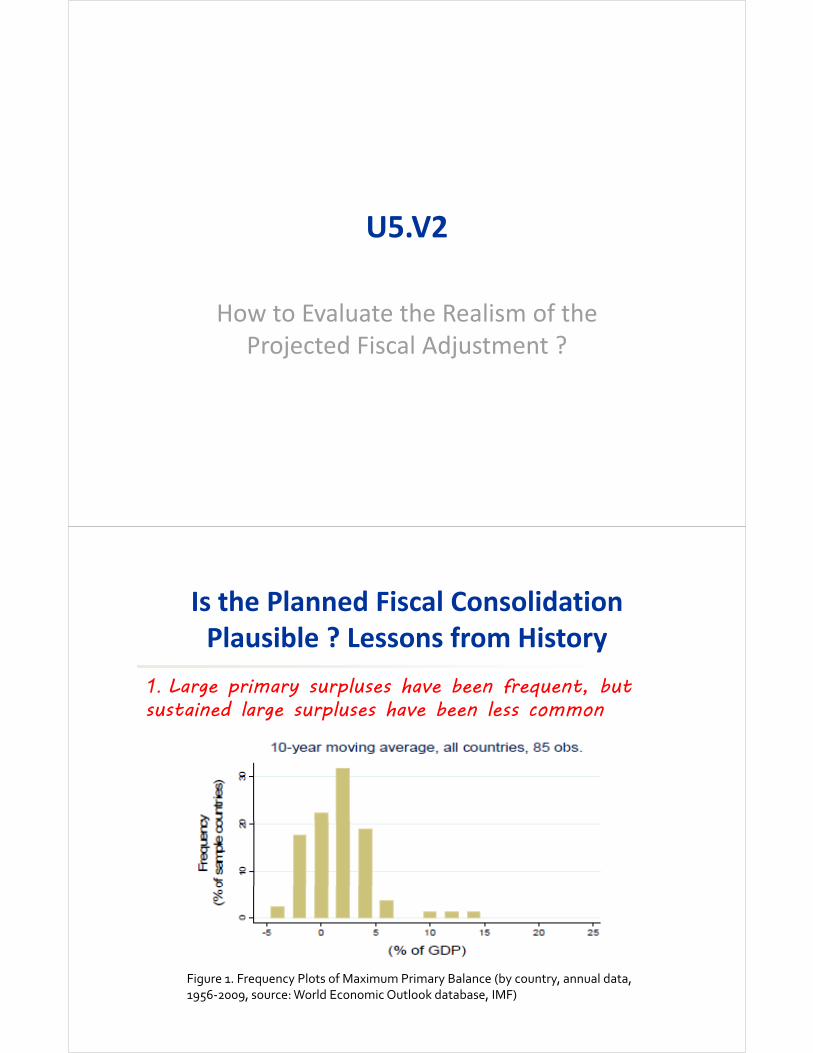

How to Evaluate the Realism of the Projected Fiscal Adjustment ?

Is the Planned Fiscal Consolidation l ibl ? f iPlausible ? Lessons from History

1. Large primary surpluses have been frequent, but1. Large primary surpluses have been frequent, but sustained large surpluses have been less common

Figure 1. Frequency Plots of Maximum Primary Balance (by country, annual data, 1956-2009, source: World Economic Outlook database, IMF)

Is the Planned Fiscal Consolidation l ibl ? f iPlausible ? Lessons from History

2. Large fiscal corrections are usually associated with2. Large fiscal corrections are usually associated with worse starting fiscal positions

Figure 2. Largest Primary Balance Turnaround (source: World Economic Outlook database, IMF)

Some Simple Rules-of-ThumbSome Simple Rules of Thumb

Close scrutiny of assumptions warranted if planned fiscal adjustment is located close to the right-hand tail of the cross-country distributions

maximum 3-yearmaximum 3-year yaverage leveladjustment

Country-Specific InformationCountry Specific Information

The analysis would

past record of fiscal adjustment

would take account of

extent of political commitment

the design of the authorities’ fiscalof the design of the authorities fiscal adjustment plans

experience regarding budget forecastexperience regarding budget forecast errors

legal and institutional mechanisms

U5 V3U5.V3

How to Use the Boom-Bust Tool ?

What are the Triggers for the Boom-Bust l ?Tool ?

Countries are identified to be in a boom if either of theCountries are identified to be in a boom, if either of the following conditions is met:

A positive output gap• during the last 3

A 3-year cumulative level change in private sector credit-to-GDP • during the last 3

consecutive years exceeding• 15 percent for EMs• 30 percent for AEs3 p

Output gap =

Example: Private sector credit-to-GDPt t+1 t+2 t+3p g p

Actual output –Potential output

t t+1 t+2 t+330% 35% 45% 50%

20%

The Boom-Bust ToolThe Boom Bust Tool

• Compares growth Boom-Bust Analysis Compares growth assumptions for a particular country to 8

Real GDP growth

Example

(in percent)

the historical experience of b b t 0

2

4

6

boom-bust cases

I t til 6

-4

-2

0Boom-bust inter-quartile range around crisis events (t)

Interquartile range= 75th percentile -25th percentile

-6t-5 t-4 t-3 t-2 t-1 t t+1 t+2 t+3 t+4 t+5

Median

U5.V4

MAC DSA Template: Realism Tools

DEALING WITH UNCERTAINTY 1:Unit 6

DEALING WITH UNCERTAINTY 1: ALTERNATIVE SCENARIOS

U6 V1U6.V1

Sensitivity Analysis in the MAC DSA

Sensitivity Analysis in the MAC DSASensitivity Analysis in the MAC DSA

lHistorical scenario

Constant primary

Standardized sensitivity analysis

Constant primary balance scenario

Standardized macro-fiscal stress tests

Financial sector ti tcontingent

liabilities shock

Customized sensitivity Customized sensitivity

analysis scenarios

Historical ScenarioHistorical Scenario

Set at historical average• real GDP growth • the primary balance• real interest rates

Oth i bl iBaseline

Other variables same as in baseline

Constant Primary Balance (CPB) ScenarioConstant Primary Balance (CPB) Scenario

The primary balance assumed to remain unchanged at current level

Other variables same as inBaseline

Other variables same as in baseline

How to Analyze the Historical and CPB i ?Scenarios ?

Are baseline Are policy actions b i l hAre baseline

assumptions unrealistic (overly

i i i ) ?

substantial enough to make a credible break from past oroptimistic) ? break from past or

current trends?

Standardized Macro-Fiscal ShocksStandardized Macro Fiscal Shocks

Primary balance

Real GDP

Standardized macro fiscal

growth

Interest ratemacro-fiscal stress tests

Interest rate

E h tExchange rate

CombinedCombined macro-fiscal

Primary Balance ShockPrimary Balance Shock

Size and duration of shockSize and duration of shock

Minimum shock equivalent to the maximum of:- 50% of planned cumulative adjustment in the baseline- baseline minus half of the 10-year historical standard deviation of the primary balance

Default interactions

- Increase in interest rates

Real GDP Growth ShockReal GDP Growth Shock

Size and duration of shockSize and duration of shock

Real GDP growth is reduced by 1 standard deviation for 2 consecutive years

Default interactions

- Deterioration in the primary balanceDeterioration in the primary balance - Increase in interest rates - Decrease in inflation

Interest Rate ShockInterest Rate Shock

Size and duration of shockSize and duration of shock

Interest rate increases by the maximum of:- the difference between average real interest rate level over the projection period and maximum real historical level, or- 200bps

fDefault interactions

- None

Exchange Rate ShockExchange Rate Shock

Size and duration of shockSize and duration of shock

Exchange rate increases by the maximum of:- estimated overvaluation- maximum historical movement of the exchange rate

Default interaction

- pass-through to inflation (default elasticity of 0.25 for EMs and 0.03 for AEs)

change in domestic i fl ti d tinflation due to a

change in the exchange rate

Combined Macro-FiscalCombined Macro Fiscal

Size and duration of shock

Based on the underlying shocks

Default interactions

h l ff f i di id l h k llIncorporates the largest effect of individual shocks on all relevant variables (real GDP growth, inflation, primary balance, exchange rate, and interest rate)g

U6 V2U6.V2

MAC DSA Template: Introduction to the Alternative Scenarios, the Historical Scenario and the No Policy ChangeScenario and the No-Policy Change

Scenario

U6 V3U6.V3

MAC DSA Template: The Standardized Macro-fiscal Stress

Tests

DEALING WITH UNCERTAINTY 2: Unit 7

CUSTOMIZED SCENARIOS AND FAN CHARTSCHARTS

U7 V1U7.V1

MAC DSA Template: Customized Alternative Scenarios

U7 V2U7.V2

Fan Charts

What Does the Fan Chart Tool Do?What Does the Fan Chart Tool Do?

provides a probabilistic view of theprovides a probabilistic view of the uncertainty around the baseline

shows a spectrum of possible outcomes based on the stochastic properties the data

incorporates interaction between macroeconomic variables

relies on historical data to calibrate the persistence of shockspersistence of shocks

How Are Fan Charts Constructed ?How Are Fan Charts Constructed ?

RGDP,RIRw,PRER,PB

Historicaldata

�,� N(�,�)

DrawsProjectionsConfidence

b ndsbands

What are the Types of Fan Charts ?What are the Types of Fan Charts ?

Symmetric

• upside risks match downside risks • centered around the baseline

Asymmetric

• downside risks higher than upsidet th l t’ b t t f th• capture the analyst’s best assessment of the

likely balance of risks

Symmetric Fan ChartsSymmetric Fan Charts

idupside and

downside45

Fan ChartEvolution of Debt-to-GDP ratio

downside risks are equally l k l

35

40

likely30

25t t+1 t+2 t+3 t+4 t+5 t+6 t+7

10th-25th 25th-50th 50th-75th 75th-90th Baseline

Asymmetric Fan Chartsy

t ff thcut off the upward or downward

45

Fan ChartEvolution of Debt-to-GDP ratio

distribution of shocks in order to represents 35

40

to represents the analyst’s

best t f

30

assessment of the likelihood

of shocks

25t t+1 t+2 t+3 t+4 t+5 t+6 t+7

10th-25th 25th-50th 50th-75th 75th-90th Baseline

U7 V3U7.V3

MAC DSA Template: Fan Charts

CONTINGENT LIABILITIESUnit 8

CONTINGENT LIABILITIES

U8 V1U8.V1

What are Contingent Liabilities ?

What are Contingent Liabilities (CLs) ?What are Contingent Liabilities (CLs) ?Government financial

public entities (including sub-national t t t d t i (SOE ) dfinancial

interventions which arise out of

governments, state-owned enterprises (SOEs) and state banks)

bli i hi ( )explicit and implicit guarantees to

public-private partnerships (PPPs)

to

depositors (deposit insurance)

support to private companies deemed too big to pp p p gfail, etc.

Explicit LiabilitiesExplicit Liabilities

Recognizedd byy aa laww orr contractExamples State guarantees for non-sovereign borrowing and

obligations issued by subnational governments

Recognized by a law or contract

obligations issued by subnational governments and public or private sector entitiesState guarantees for various types of loans and

i t i t tprivate investments

Trade and exchange rate guaranteesTrade and exchange rate guarantees

St t i hState insurance schemes

Implicit LiabilitiesImplicit LiabilitiesAssumed due to public and interest-group

Examples Defaults on non-guaranteed debt and other obligations by b ti l t bli i t t i

p g ppressures

subnational governments or public or private enterprises

Financial system bailout

Corporate sector bailout

Clean-up of liabilities of entities being privatized

Implicit insurance for disaster relief

Contingent Liabilities Are SignificantContingent Liabilities Are Significant

Contingent Liabilities in the DSAContingent Liabilities in the DSA

The DSA envisages Treatment in thegseveral types of CL

shocks

Treatment in the MAC DSA

Guaranteed debt (of SOEs and

PPPs)

d

Natural disasters

Customized scenariosNot standardized

Banking/financialBuilt-in financial CL

Banking/financial crisis

scenarioStandardized

U8 V2U8.V2

Contingent Liabilities Stemming from a Financial Crisis

Costs of Banking CrisesCosts of Banking Crises

Median gross fiscal costs (net of any subsequent recoveries)

13% fwere 13% of banking system assets

Source: Laeven and Valencia (2012)

Triggers for the Financial CL Shock

Contingent Liabilities: Quantitative Triggers for Baking Crises

EMs AEs

Private sector credit-to-GDP (3-yearcumulative level change), in percent

15 30

Loan to deposit ratio

Additi l

Loan-to-deposit ratio 1.5 1.5

average annual increase in nominal housing prices over the preceding 5-

Additional

ov h p i gyear period in excess of

7.5%

The Financial CL in the MAC DSA

The standard contingent

A financial CL shock of 10% of banking sectorIf a quantitative contingent

liability shock also includes

banking sector assets is

automatically generated

trigger is breached

• negative shock to growth

•Or other financial vulnerabilities are growth

• resulting deterioration of the primary balance

• increase in interest rates

identified

rates • decrease in inflation

U8 V2U8.V2

MAC DSA Template: The Financial Contingent Liabilities Shock

VULNERABILITIES STEMMING FROM Unit 9

THE DEBT LEVEL AND FINANCING PROFILEPROFILE

U9 V1U9.V1

Vulnerabilities Stemming from the Level of Debt

Why is High Debt an Issue ?Why is High Debt an Issue ?

i hHigh debt

requires large primary fiscal surpluses to service it

exacerbates an economy’s vulnerability to shocks

exposes a country to a higher risk of a rollover crisisg

may be detrimental to economic growtheconomic growth

Benchmarks for the Debt Burden diIndicators

• Based on “early warning models” whichBased on early warning models which trigger higher scrutiny in the MAC DSA

• To assess risks to debt-to-GDP: indicative benchmarks derived from the signal approach are increased by about 20 percent (to 70 for EMs and 85 for AEs)

Debt Burden Benchmarks for Risk-i hAssessment in the Heat Map

Debt Burden Benchmarks for Risk Assessment Debt profile indicators Debt-to-GDP GFN-to-GDP

EM 70 15EMs 70 15

AEs 85 20

U9 V2U9.V2

The Assessment of Debt Profile Risks in the MAC DSA

Risks from the Debt Financing ProfileRisks from the Debt Financing Profile

Currency Composi

Maturity

Creditor

Composition

base

Debt ProfileDebt Profile Vulnerabilities

Indicators of Debt Profile VulnerabilitiesIndicators of Debt Profile Vulnerabilities

D bt Bond yield spreads (EMBI Global spreads forDebt profile i k

Bond yield spreads (EMBI Global spreads for EMs or Spread over US bonds for AEs)

External financing requirement (% of GDP)risks External financing requirement (% of GDP)

Public debt held by non-residents (share of ytotal)

Public debt in foreign-currency (share of total)

Annual change in the share of short-term debt at original maturityat original maturity

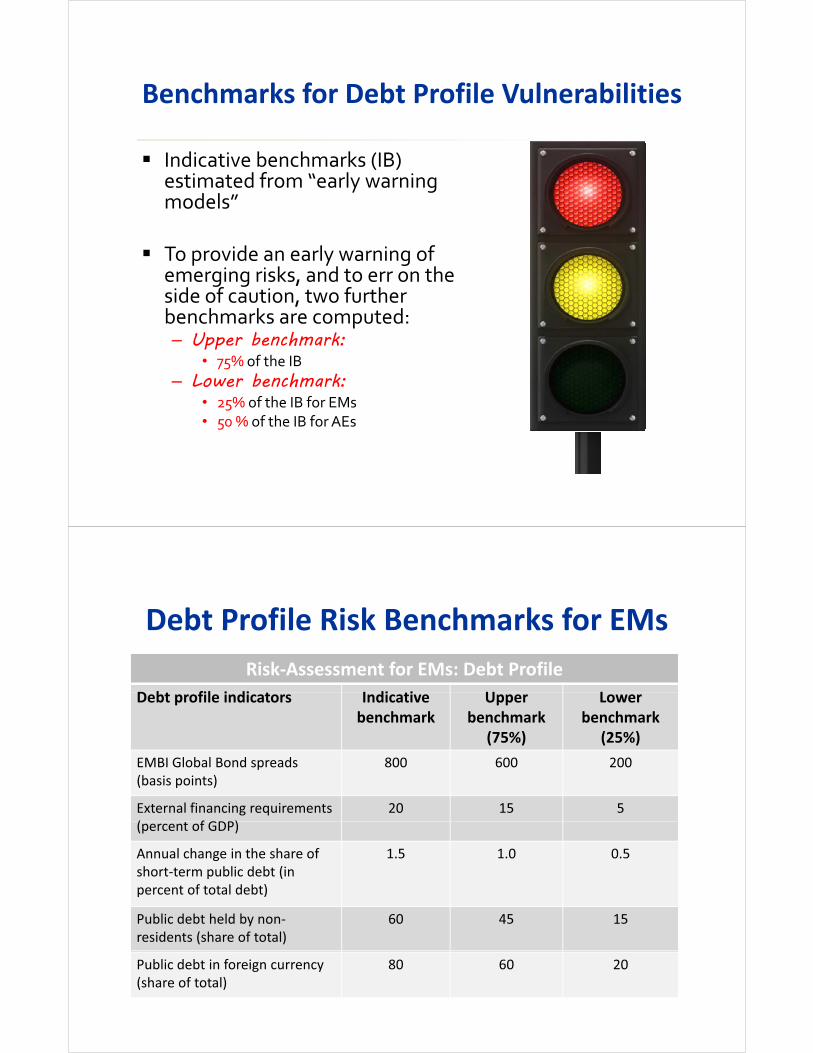

Benchmarks for Debt Profile VulnerabilitiesBenchmarks for Debt Profile Vulnerabilities

� Indicative benchmarks (IB)Indicative benchmarks (IB) estimated from “early warning models”

� To provide an early warning of emerging risks, and to err on the side of caution two furtherside of caution, two further benchmarks are computed:– Upper benchmark:

• 75% of the IB• 75% of the IB– Lower benchmark:

• 25% of the IB for EMs• 50 % of the IB for AEs50 % of the IB for AEs

Debt Profile Risk Benchmarks for EMsDebt Profile Risk Benchmarks for EMsRisk-Assessment for EMs: Debt Profile

D b fil i di I di i U LDebt profile indicators Indicative benchmark

Upper benchmark

(75%)

Lower benchmark

(25%) EMBI Global Bond spreads(basis points)

800 600 200

External financing requirements ( f GDP)

20 15 5(percent of GDP)

Annual change in the share of short-term public debt (in

t f t t l d bt)

1.5 1.0 0.5

percent of total debt)

Public debt held by non-residents (share of total)

60 45 15

Public debt in foreign currency (share of total)

80 60 20

Debt Profile Risk Benchmarks for AEsDebt Profile Risk Benchmarks for AEsRisk-Assessment for EMs: Debt Profile

D b fil i di I di i U LDebt profile indicators Indicative benchmark

Upper benchmark

(75%)

Lower benchmark

(50%) EMBI Global Bond spreads(basis points)

800 600 400

External financing requirements ( t f GDP)

35 25 17.5(percent of GDP)

Annual change in the share of short-term public debt (in percent of total debt)

2.0 1.5 1.0

percent of total debt)

Public debt held by non-residents (share of total)

60 45 30

Differences with EMs

Reporting of Debt Profile RisksReporting of Debt Profile Risks

U9 V3U9.V3

MAC DSA Template: Financing Assumptions and the Debt Profile

ASSESSMENT AND WRITE-UPUnit 10

ASSESSMENT AND WRITE UP

U10 V1U10.V1

The Heat Map

The Heat MapThe Heat Map

Conveys in aConveys in a standardized way the risks to d btdebt sustainability from the various modules in the template

Assessment of Risks from Macro-Fiscal d i i bili i h kand Contingent Liabilities Shocks

Risk Assessment: Macro-Fiscal Risks and Contingent Liabilities(d i ll f ll )(done automatically for all stress tests)

Baseline Stress-test

High (red) above benchmark above benchmark

Moderate (yellow) below benchmark above benchmarkModerate (yellow) below benchmark above benchmark

Low (green) below benchmark below benchmark

Assessment of Debt Profile Risks for EMsAssessment of Debt Profile Risks for EMsRisk-Assessment for EMs: Debt Profile

Debt profile indicators Low Moderate risk HighDebt profile indicators Low risk

Moderate risk High Risk

Bond spreads (basis points) Below Between 200 and Above 200 600 600

External financing requirements (percent of GDP)

Below 5 Between 5 and 15 Above 15

Annual change in the share of short-term public debt (in percent of total debt)

Below 0.5

Between 0.5 and 1.0

Above 1.0

)Public debt held by non-residents (share of total)

Below 15 Between 15 and 45

Above 45

Public debt in foreign currency Below 20 Between 20 and AbovePublic debt in foreign currency (share of total)

Below 20 Between 20 and 60

Above 60

Assessment of Debt Profile Risks for AEsAssessment of Debt Profile Risks for AEsRisk-Assessment for AEs: Debt Profile

Debt profile indicators Low Moderate risk HighDebt profile indicators Low risk

Moderate risk High Risk

Bond spreads (basis points) Below Between 400 and Above 400 600 600

External financing requirements (percent of GDP)

Below 17 Between 17 and 25

Above 25

Annual change in the share of short-term public debt (in percent of total debt)

Below 1.0

Between 1.0 and 1.5

Above 1.5

)Public debt held by non-residents (share of total)

Below 30 Between 30 and 45

Above 45

Summarizing Risks: Heat MapsSummarizing Risks: Heat Maps Public DSA Risk Assessment

Heat Map

Debt level Real GDP Growth Shock

Primary Balance Shock

Real Interest

Rate Shock

Exchange Rate Shock

Contingent Liability shock

Gross financing needs

Real GDP Growth Shock

Primary Balance Shock

Real Interest

Rate Shock

Exchange Rate Shock

Contingent Liability Shock

Market Perception

External Financing

Requirements

Change in the Share of Short-Term

Debt

Public Debt Held by

Non-Residents

Foreign Currency

DebtDebt profile

U10 V2U10.V2

The Write-Up and Risk-AssessmentNatalia NovikovaNatalia Novikova

Ireland: High Vulnerabilities from the Debt Level

Source: Ireland: Twelfth Review under the Extended Arrangement and Proposal for Post program Monitoring, December 2013.

Ireland: High Vulnerabilities from the Debt Level

• ‘…the planned reduction in the large cash buffer after a major p g ff f jdebt amortization in January 2014 allows gross public debt to decline from 2014… net public debt … falls to just below 100 percent of GDP by 2018 when the cash buffer is assumed topercent of GDP by 2018 when the cash buffer is assumed to shrink to more normal levels of about 7 percent of GDP.’

• ‘Debt reductions from asset sales present an upside risk. Current baseline assumptions do not incorporate proceeds from state asset disposals of up to €3 billion (around 1¾ percent of GDP) at least half of which are to be used for debt reductionGDP) …, at least half of which are to be used for debt reduction. Similarly, no allowance is made for further transactions reducing the cost incurred in supporting the banking system … ‘

Source: Ireland: Twelfth Review under the Extended Arrangement and Proposal for Post program Monitoring, December 2013.

Low Debt LevelLow Debt Level

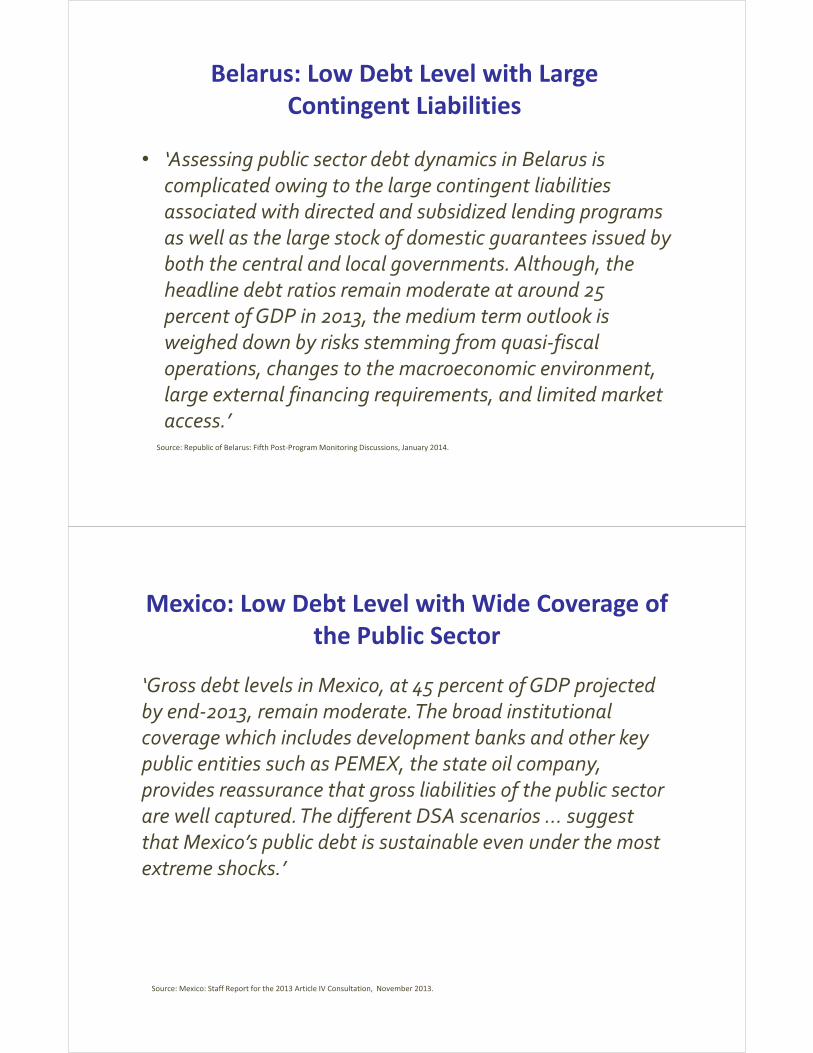

Belarus

Source: Republic of Belarus: Fifth Post-Program Monitoring Discussions, January 2014.

Mexico

Source: Mexico: Staff Report for the 2013 Article IV Consultation, November 2013.

Belarus: Low Debt Level with Large Contingent LiabilitiesContingent Liabilities

• ‘Assessing public sector debt dynamics in Belarus is ssess g pub c secto debt dy a cs e a us scomplicated owing to the large contingent liabilities associated with directed and subsidized lending programs

ll h l k f d i i d bas well as the large stock of domestic guarantees issued by both the central and local governments. Although, the headline debt ratios remain moderate at around 25headline debt ratios remain moderate at around 25 percent of GDP in 2013, the medium term outlook is weighed down by risks stemming from quasi-fiscal

h hoperations, changes to the macroeconomic environment, large external financing requirements, and limited market access ’

Source: Republic of Belarus: Fifth Post-Program Monitoring Discussions, January 2014.

access.

Mexico: Low Debt Level with Wide Coverage of h P bli Sthe Public Sector

‘Gross debt levels in Mexico, at 45 percent of GDP projected G oss debt e e s e co, at 45 pe ce t of G p ojectedby end-2013, remain moderate. The broad institutional coverage which includes development banks and other key

bli i i h PEMEX h ilpublic entities such as PEMEX, the state oil company, provides reassurance that gross liabilities of the public sector are well captured.The different DSA scenarios … suggestare well captured. The different DSA scenarios … suggest that Mexico’s public debt is sustainable even under the most extreme shocks.’

Source: Mexico: Staff Report for the 2013 Article IV Consultation, November 2013.

U10 V3U10.V3

Concluding remarks

Supplementary MaterialSupplementary Material

The Benchmarks in the MAC DSA: Methodology and Usages

How are the Benchmarks Derived ?How are the Benchmarks Derived ?

• Signal approach/ early warning modelsTh l i b h k

False alarms

• The early warning benchmarks are derived by finding the value of the threshold X that minimizes the:minimizes the:

ADB

B��ratio signal-to-Noise

Type II Type I

CAA�

g

Missed

135

yperrors = B/(B+D)

yperrors = C/(A+C)

crises

Use of the Benchmarks in the TemplateUse of the Benchmarks in the Template

Indicative/Early warning/Signal

approachapproach benchmarks

Classification Benchmarks forbenchmarks: lower vs higher

scrutiny

Benchmarks for assessing risks in

the heat mapscrutiny

Debt Burden Indicators

Indicative benchmarks Debt/GDP

-15% +20%

Classification benchmarks

Heat map benchmarksbenchmarks benchmarks

Debt-to-GDP Benchmarks

Debt-to-GDP

Indicative Classification Heat mapbenchmark benchmark benchmark

EM 60 -15%*60= 51� 50 +20%*60=72 � 705 5 5 7 7

AE 70 -15%*70= 59.5� 60 +20%*70=84� 85

GFN-to-GDP Benchmarks

GFN-to-GDP

Indicative benchmark

Classification benchmark

Heat mapbenchmarkbenchmark benchmark benchmark

EM 15 -15%*15=12.75 �10 15

AE 20 -15%*20=17� 15 20

Summary: Debt Burden Indicatorsh kBenchmarks

Benchmarks for Debt Burden IndicatorsEM EM EM AE AE AE

Heat HeatIndicator Unit Indic Classif

Heatmap Indic Classif

Heatmap

Gross government debt Percent of GDP 60 50 70 70 60 85Gross public sector financing

requirements Percent of GDP 15 10 15 20 15 20

Assessment of Risks from Macro-Fiscal d i i bili i h kand Contingent Liabilities Shocks

Debt-to-GDPBaseline < 70/85 < 70/85 > 70/85

Shock Scenario < 70/85 > 70/85 > 70/85

GFN-to-GDPBaseline < 15/20 < 15/20 > 15/20

Shock Scenario < 15/20 > 15/20 > 15/20

Benchmarks for Debt Profile Vulnerabilities

Indicative benchmarks

Lower early Upper early EMs:25% 75%warning

benchmarkswarning

benchmarks

EMs:25%AEs:50%

75%

ClassificationClassification benchmarks

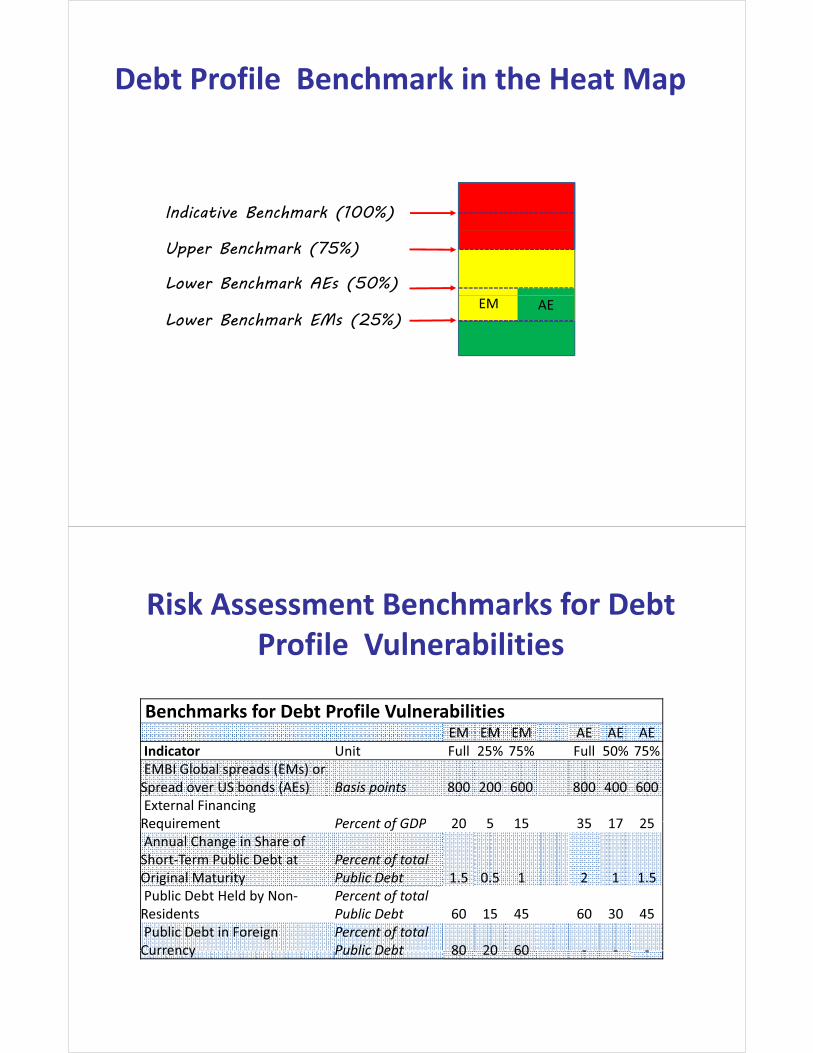

Debt Profile Benchmark in the Heat Map

Indicative Benchmark (100%)

Upper Benchmark (75%)

Lower Benchmark AEs (50%)

Lower Benchmark EMs (25%)EM AE

Risk Assessment Benchmarks for Debt Profile Vulnerabilities

Benchmarks for Debt Profile VulnerabilitiesEM EM EM AE AE AE

Indicator Unit Full 25% 75% Full 50% 75%EMBI Global spreads (EMs) or

Spread over US bonds (AEs) Basis points 800 200 600 800 400 600External Financing Requirement Percent of GDP 20 5 15 35 17 25Requirement Percent of GDP 20 5 15 35 17 25Annual Change in Share of

Short-Term Public Debt at Original Maturity

Percent of total Public Debt 1.5 0.5 1 2 1 1.5

Public Debt Held by Non-Residents

Percent of total Public Debt 60 15 45 60 30 45

Public Debt in Foreign Currency

Percent of total Public Debt 80 20 60 - - -Currency Public Debt 80 20 60 - - -