the punjab provincial cooperative bank limited - state bank … · 2008-01-22 · the punjab...

TRANSCRIPT

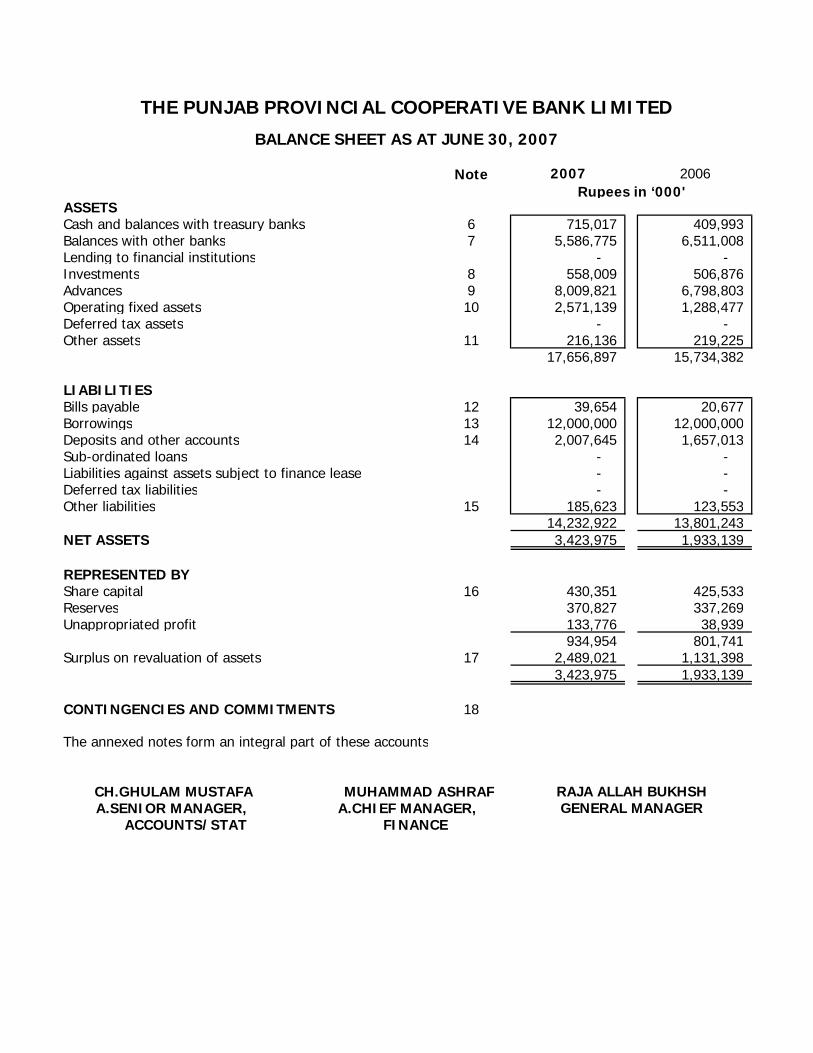

Note 2007 2006Rupees in ‘000'

ASSETSCash and balances with treasury banks 6 715,017 409,993 Balances with other banks 7 5,586,775 6,511,008 Lending to financial institutions - - Investments 8 558,009 506,876 Advances 9 8,009,821 6,798,803 Operating fixed assets 10 2,571,139 1,288,477 Deferred tax assets - - Other assets 11 216,136 219,225

17,656,897 15,734,382

LIABILITIESBills payable 12 39,654 20,677 Borrowings 13 12,000,000 12,000,000 Deposits and other accounts 14 2,007,645 1,657,013 Sub-ordinated loans - - Liabilities against assets subject to finance lease - - Deferred tax liabilities - - Other liabilities 15 185,623 123,553

14,232,922 13,801,243 NET ASSETS 3,423,975 1,933,139

REPRESENTED BYShare capital 16 430,351 425,533 Reserves 370,827 337,269 Unappropriated profit 133,776 38,939

934,954 801,741 Surplus on revaluation of assets 17 2,489,021 1,131,398

3,423,975 1,933,139

CONTINGENCIES AND COMMITMENTS 18

The annexed notes form an integral part of these accounts

ACCOUNTS/STAT FINANCE

THE PUNJAB PROVINCIAL COOPERATIVE BANK LIMITED

BALANCE SHEET AS AT JUNE 30, 2007

CH.GHULAM MUSTAFA MUHAMMAD ASHRAF RAJA ALLAH BUKHSHA.SENIOR MANAGER, A.CHIEF MANAGER, GENERAL MANAGER

Note 2007 2006Rupees in ‘000'

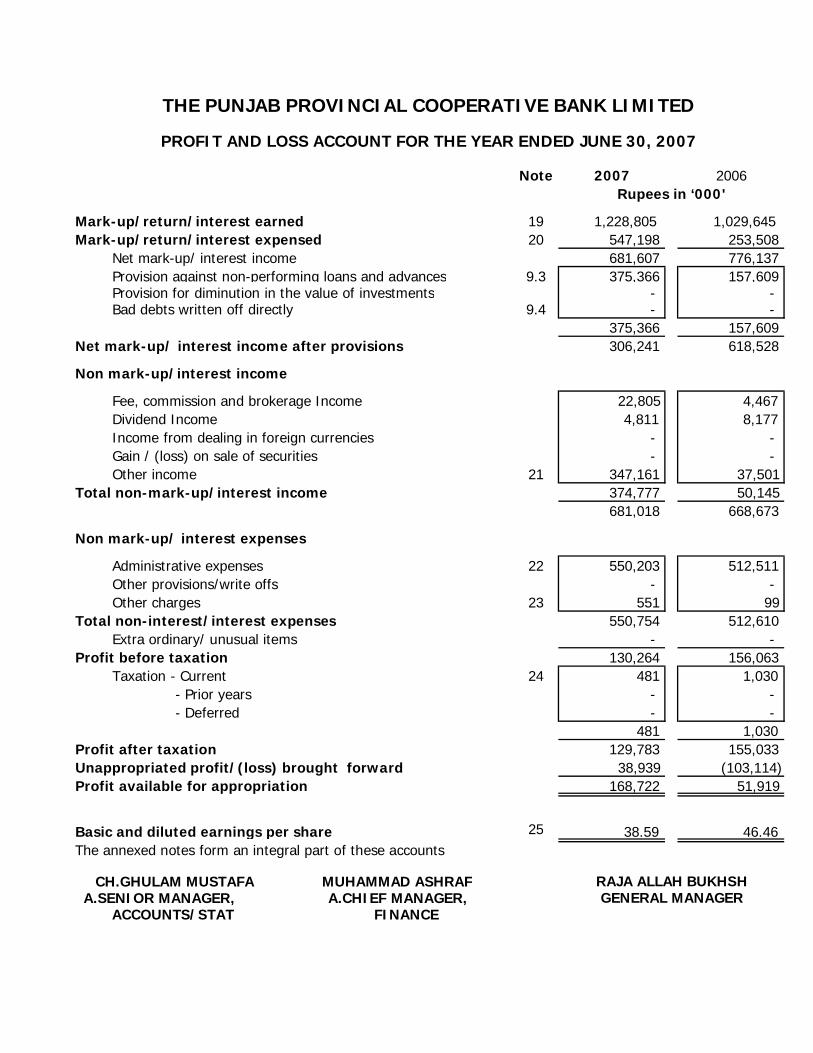

19 1,228,805 1,029,645 20 547,198 253,508

Net mark-up/ interest income 681,607 776,137 Provision against non-performing loans and advances 9.3 375,366 157,609 Provision for diminution in the value of investments - - Bad debts written off directly 9.4 - -

375,366 157,609 306,241 618,528

Fee, commission and brokerage Income 22,805 4,467 Dividend Income 4,811 8,177 Income from dealing in foreign currencies - - Gain / (loss) on sale of securities - - Other income 21 347,161 37,501

374,777 50,145 681,018 668,673

Administrative expenses 22 550,203 512,511 Other provisions/write offs - - Other charges 23 551 99

550,754 512,610 Extra ordinary/ unusual items - -

130,264 156,063 Taxation - Current 24 481 1,030 - Prior years - - - Deferred - -

481 1,030 129,783 155,033

Unappropriated profit/(loss) brought forward 38,939 (103,114)Profit available for appropriation 168,722 51,919

25 38.59 46.46 The annexed notes form an integral part of these accounts

RAJA ALLAH BUKHSHGENERAL MANAGER

Profit before taxation

Profit after taxation

Basic and diluted earnings per share

Total non-mark-up/interest income

Total non-interest/interest expenses

ACCOUNTS/STAT FINANCE

CH.GHULAM MUSTAFA MUHAMMAD ASHRAFA.SENIOR MANAGER, A.CHIEF MANAGER,

Non mark-up/ interest expenses

THE PUNJAB PROVINCIAL COOPERATIVE BANK LIMITED

PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED JUNE 30, 2007

Mark-up/return/interest earned

Non mark-up/interest income

Net mark-up/ interest income after provisions

Mark-up/return/interest expensed

Note 2007 2006Rupees in ‘000'

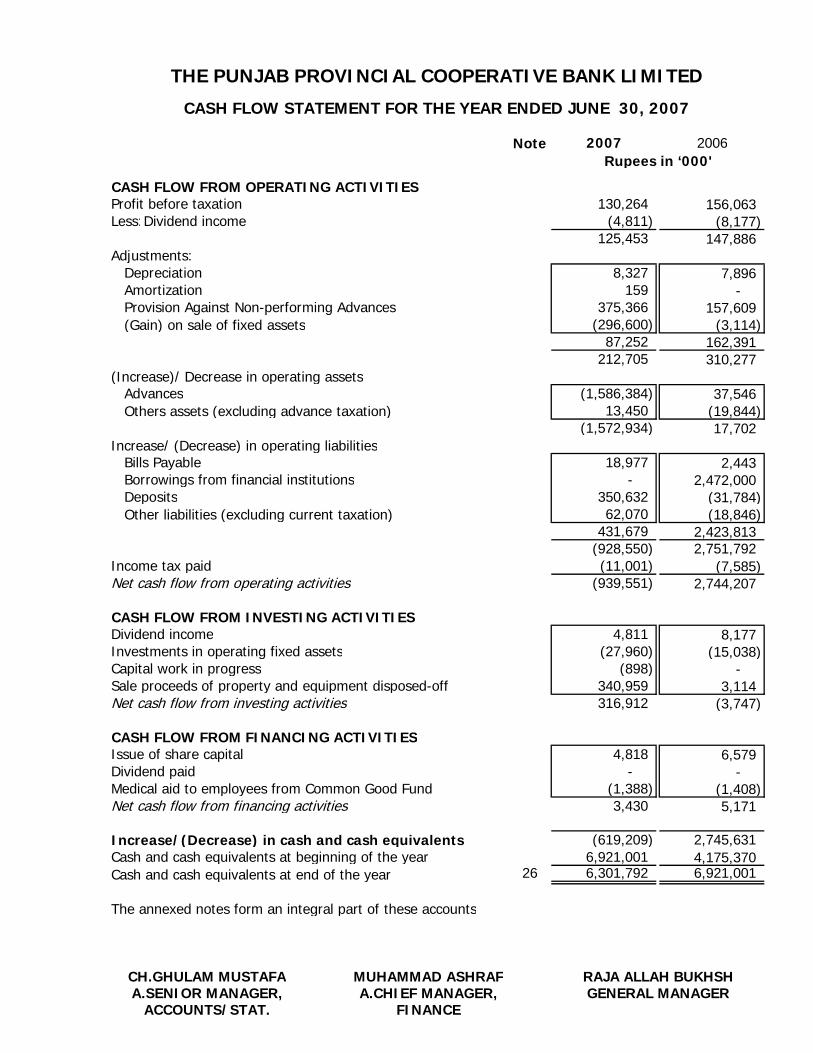

CASH FLOW FROM OPERATING ACTIVITIESProfit before taxation 130,264 156,063 Less:Dividend income (4,811) (8,177)

125,453 147,886 Adjustments: Depreciation 8,327 7,896 Amortization 159 - Provision Against Non-performing Advances 375,366 157,609 (Gain) on sale of fixed assets (296,600) (3,114)

87,252 162,391 212,705 310,277

(Increase)/ Decrease in operating assets Advances (1,586,384) 37,546 Others assets (excluding advance taxation) 13,450 (19,844)

(1,572,934) 17,702 Increase/ (Decrease) in operating liabilities Bills Payable 18,977 2,443 Borrowings from financial institutions - 2,472,000 Deposits 350,632 (31,784) Other liabilities (excluding current taxation) 62,070 (18,846)

431,679 2,423,813 (928,550) 2,751,792

Income tax paid (11,001) (7,585) Net cash flow from operating activities (939,551) 2,744,207

CASH FLOW FROM INVESTING ACTIVITIESDividend income 4,811 8,177 Investments in operating fixed assets (27,960) (15,038) Capital work in progress (898) - Sale proceeds of property and equipment disposed-off 340,959 3,114 Net cash flow from investing activities 316,912 (3,747)

CASH FLOW FROM FINANCING ACTIVITIESIssue of share capital 4,818 6,579 Dividend paid - - Medical aid to employees from Common Good Fund (1,388) (1,408) Net cash flow from financing activities 3,430 5,171

Increase/(Decrease) in cash and cash equivalents (619,209) 2,745,631 Cash and cash equivalents at beginning of the year 6,921,001 4,175,370 Cash and cash equivalents at end of the year 26 6,301,792 6,921,001

The annexed notes form an integral part of these accounts

RAJA ALLAH BUKHSHGENERAL MANAGER

ACCOUNTS/STAT. FINANCE

THE PUNJAB PROVINCIAL COOPERATIVE BANK LIMITED

CASH FLOW STATEMENT FOR THE YEAR ENDED JUNE 30, 2007

CH.GHULAM MUSTAFA MUHAMMAD ASHRAFA.SENIOR MANAGER, A.CHIEF MANAGER,

Share Statutory Common Reserve for Unappropriated/ Totalcapital reserve Good Consumer profit/(loss)

Fund Finance

Balance as on June 30, 2005 418,954 318,748 5,469 1,480 (103,114) 641,537

Profit for the year - - - 155,033 155,033

Transfer to statutory reserve - 12,980 - - (12,980) -

- - - - - -

Issue of share capital 6,579 - - - - 6,579

Medical aid to staff - - (1,408) (1,408)

Balance as on June 30, 2006 425,533 331,728 4,061 1,480 38,939 801,741

Profit for the year - - - - 129,783 129,783

Transfer to statutory reserve - 32,446 - - (32,446) -

- - 2,500 (2,500) -

Issue of share capital 4,818 4,818

Medical aid to staff (1,388) (1,388)

Balance as on June 30, 2007 430,351 364,174 5,173 1,480 133,776 934,954

The annexed notes form an integral part of these accounts

Note:Common Good Fund is created for the welfare/medical aid to staff under Section 42 of Cooperative societies Act, 1925.

CH.GHULAM MUSTAFA MUHAMMAD ASHRAFA.SENIOR MANAGER, A.CHIEF MANAGER,

ACCOUNTS/STAT FINANCE

THE PUNJAB PROVINCIAL COOPERATIVE BANK LIMITED

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED JUNE 30, 2007

Rupees in '000'

Transfer to reserve for ConsumerFinance

Transfer to reserve for CommonGood Fund

RAJA ALLAH BUKHSHGENERAL MANAGER

Under the Bylaw No.57 of the Bank not less than one quarter of the net profit shall be carried to the statutory reserve.

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

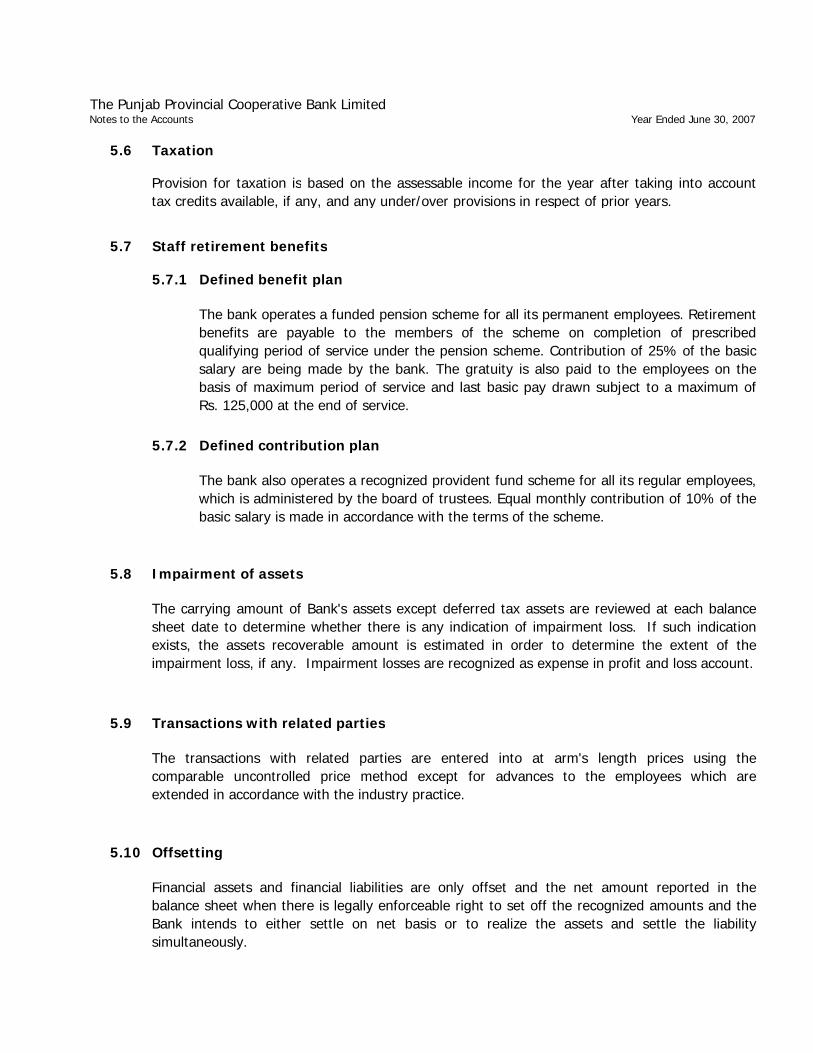

5.6 Taxation

5.7 Staff retirement benefits

5.7.1 Defined benefit plan

5.7.2 Defined contribution plan

5.8 Impairment of assets

5.9 Transactions with related parties

5.10 Offsetting

The carrying amount of Bank's assets except deferred tax assets are reviewed at each balancesheet date to determine whether there is any indication of impairment loss. If such indicationexists, the assets recoverable amount is estimated in order to determine the extent of theimpairment loss, if any. Impairment losses are recognized as expense in profit and loss account.

The transactions with related parties are entered into at arm's length prices using thecomparable uncontrolled price method except for advances to the employees which areextended in accordance with the industry practice.

Provision for taxation is based on the assessable income for the year after taking into accounttax credits available, if any, and any under/over provisions in respect of prior years.

The bank operates a funded pension scheme for all its permanent employees. Retirementbenefits are payable to the members of the scheme on completion of prescribedqualifying period of service under the pension scheme. Contribution of 25% of the basicsalary are being made by the bank. The gratuity is also paid to the employees on thebasis of maximum period of service and last basic pay drawn subject to a maximum ofRs. 125,000 at the end of service.

The bank also operates a recognized provident fund scheme for all its regular employees,which is administered by the board of trustees. Equal monthly contribution of 10% of thebasic salary is made in accordance with the terms of the scheme.

Financial assets and financial liabilities are only offset and the net amount reported in thebalance sheet when there is legally enforceable right to set off the recognized amounts and theBank intends to either settle on net basis or to realize the assets and settle the liabilitysimultaneously.

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

Note 2007 2006Rupees in '000'

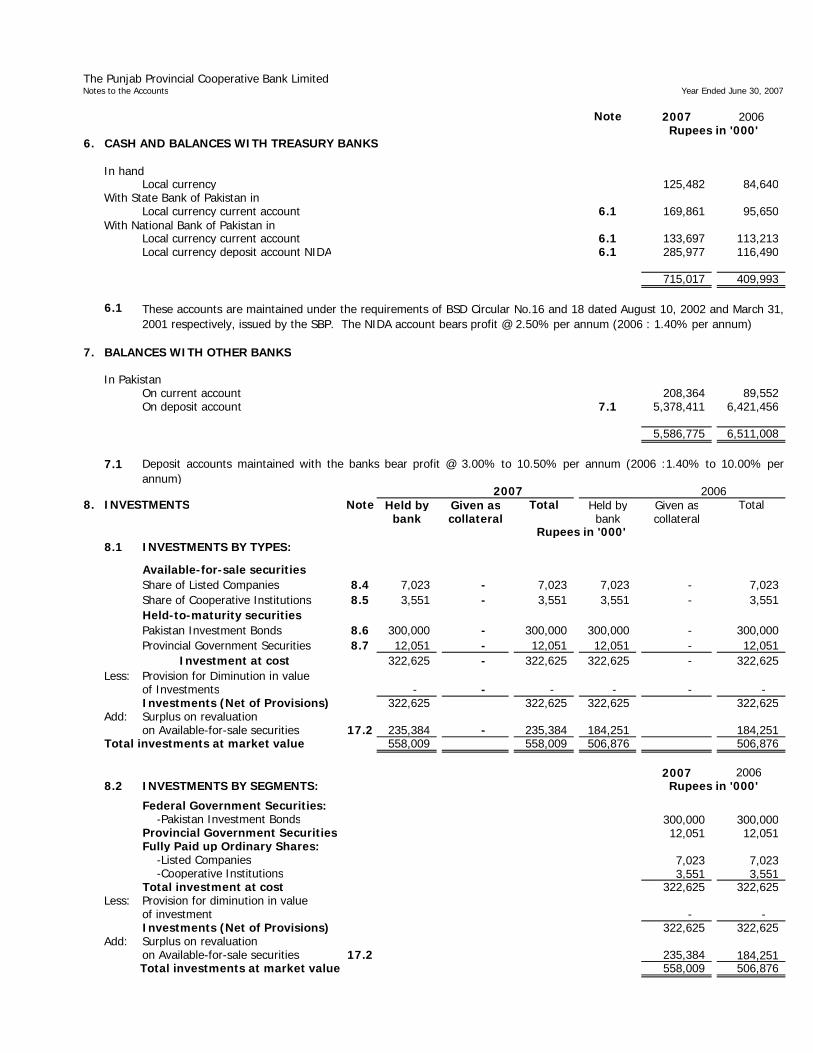

6. CASH AND BALANCES WITH TREASURY BANKS

In handLocal currency 125,482 84,640

With State Bank of Pakistan inLocal currency current account 6.1 169,861 95,650

With National Bank of Pakistan inLocal currency current account 6.1 133,697 113,213 Local currency deposit account NIDA 6.1 285,977 116,490

715,017 409,993

6.1

7. BALANCES WITH OTHER BANKS

In PakistanOn current account 208,364 89,552 On deposit account 7.1 5,378,411 6,421,456

5,586,775 6,511,008

7.1

2007 20068. INVESTMENTS Note Held by Given as Total Held by Given as Total

bank collateral bank collateralRupees in '000'

8.1 INVESTMENTS BY TYPES:

Available-for-sale securitiesShare of Listed Companies 8.4 7,023 - 7,023 7,023 - 7,023 Share of Cooperative Institutions 8.5 3,551 - 3,551 3,551 - 3,551 Held-to-maturity securitiesPakistan Investment Bonds 8.6 300,000 - 300,000 300,000 - 300,000 Provincial Government Securities 8.7 12,051 - 12,051 12,051 - 12,051 Investment at cost 322,625 - 322,625 322,625 - 322,625

Less: Provision for Diminution in value of Investments - - - - - - Investments (Net of Provisions) 322,625 322,625 322,625 322,625

Add: Surplus on revaluation on Available-for-sale securities 17.2 235,384 - 235,384 184,251 184,251

Total investments at market value 558,009 558,009 506,876 506,876

20078.2 INVESTMENTS BY SEGMENTS:

Federal Government Securities: -Pakistan Investment Bonds 300,000 300,000 Provincial Government Securities 12,051 12,051 Fully Paid up Ordinary Shares: -Listed Companies 7,023 7,023 -Cooperative Institutions 3,551 3,551 Total investment at cost 322,625 322,625

Less: Provision for diminution in value of investment - - Investments (Net of Provisions) 322,625 322,625

Add: Surplus on revaluation on Available-for-sale securities 17.2 235,384 184,251 Total investments at market value 558,009 506,876

These accounts are maintained under the requirements of BSD Circular No.16 and 18 dated August 10, 2002 and March 31,2001 respectively, issued by the SBP. The NIDA account bears profit @ 2.50% per annum (2006 : 1.40% per annum)

Rupees in '000'2006

Deposit accounts maintained with the banks bear profit @ 3.00% to 10.50% per annum (2006 :1.40% to 10.00% perannum)

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

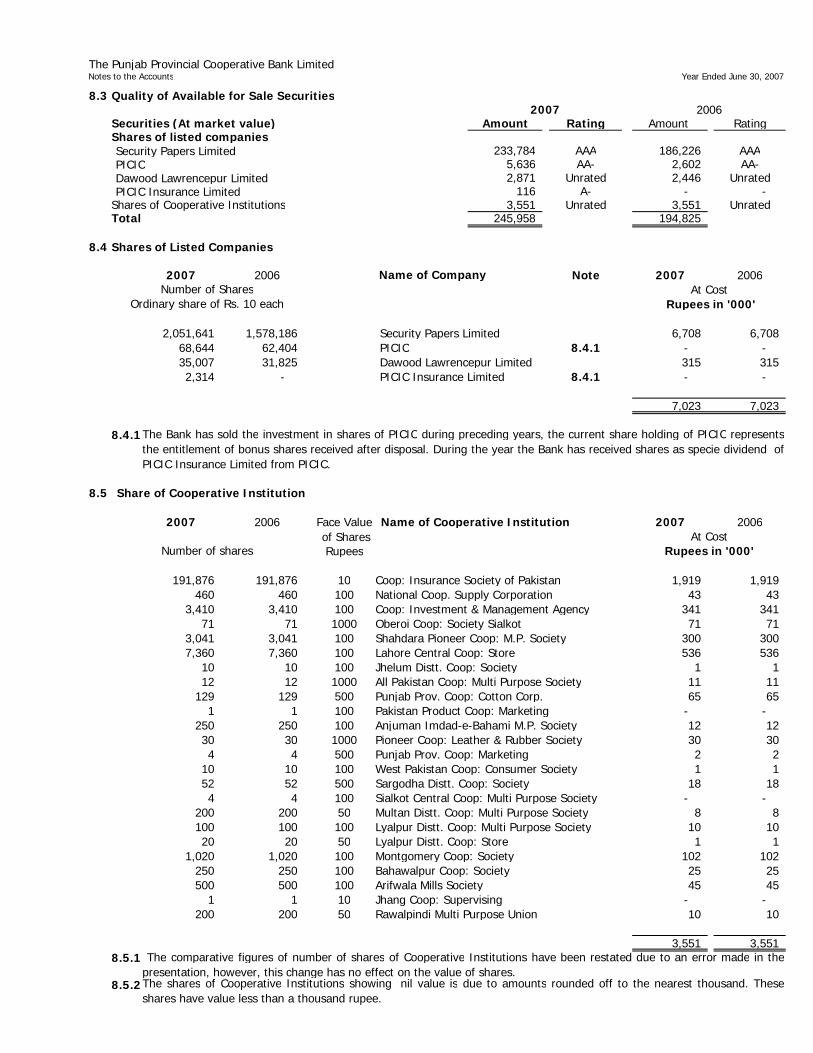

8.3 Quality of Available for Sale Securities

Securities (At market value) Amount Rating Amount RatingShares of listed companiesSecurity Papers Limited 233,784 AAA 186,226 AAAPICIC 5,636 AA- 2,602 AA-Dawood Lawrencepur Limited 2,871 Unrated 2,446 UnratedPICIC Insurance Limited 116 A- - -

Shares of Cooperative Institutions 3,551 Unrated 3,551 UnratedTotal 245,958 194,825

8.4 Shares of Listed Companies

2007 2006 Note 2007 2006

Rupees in '000'

2,051,641 1,578,186 Security Papers Limited 6,708 6,708 68,644 62,404 PICIC 8.4.1 - - 35,007 31,825 Dawood Lawrencepur Limited 315 315 2,314 - PICIC Insurance Limited 8.4.1 - -

7,023 7,023

8.4.1

8.5 Share of Cooperative Institution

2007 2006 Face Value Name of Cooperative Institution 2007 2006 of Shares

Rupees

191,876 191,876 10 Coop: Insurance Society of Pakistan 1,919 1,919 460 460 100 National Coop. Supply Corporation 43 43

3,410 3,410 100 Coop: Investment & Management Agency 341 341 71 71 1000 Oberoi Coop: Society Sialkot 71 71

3,041 3,041 100 Shahdara Pioneer Coop: M.P. Society 300 300 7,360 7,360 100 Lahore Central Coop: Store 536 536

10 10 100 Jhelum Distt. Coop: Society 1 1 12 12 1000 All Pakistan Coop: Multi Purpose Society 11 11

129 129 500 Punjab Prov. Coop: Cotton Corp. 65 65 1 1 100 Pakistan Product Coop: Marketing - -

250 250 100 Anjuman Imdad-e-Bahami M.P. Society 12 12 30 30 1000 Pioneer Coop: Leather & Rubber Society 30 30 4 4 500 Punjab Prov. Coop: Marketing 2 2

10 10 100 West Pakistan Coop: Consumer Society 1 1 52 52 500 Sargodha Distt. Coop: Society 18 18 4 4 100 Sialkot Central Coop: Multi Purpose Society - -

200 200 50 Multan Distt. Coop: Multi Purpose Society 8 8 100 100 100 Lyalpur Distt. Coop: Multi Purpose Society 10 10 20 20 50 Lyalpur Distt. Coop: Store 1 1

1,020 1,020 100 Montgomery Coop: Society 102 102 250 250 100 Bahawalpur Coop: Society 25 25 500 500 100 Arifwala Mills Society 45 45

1 1 10 Jhang Coop: Supervising - - 200 200 50 Rawalpindi Multi Purpose Union 10 10

3,551 3,551 8.5.1

8.5.2

2007 2006

Name of Company

Ordinary share of Rs. 10 eachNumber of Shares At Cost

Number of shares

The Bank has sold the investment in shares of PICIC during preceding years, the current share holding of PICIC representsthe entitlement of bonus shares received after disposal. During the year the Bank has received shares as specie dividend ofPICIC Insurance Limited from PICIC.

The comparative figures of number of shares of Cooperative Institutions have been restated due to an error made in thepresentation, however, this change has no effect on the value of shares. The shares of Cooperative Institutions showing nil value is due to amounts rounded off to the nearest thousand. Theseshares have value less than a thousand rupee.

Rupees in '000'At Cost

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

8.6

8.7

2007 20069. ADVANCES Rupees in '000'

Loans, cash credits, running finances, etc. In Pakistan 9,453,551 7,867,167 Bills discounted and purchased (excluding treasury bills) Payable in Pakistan 184 184 Advances - gross 9,453,735 7,867,351 Provision for non-performing advances 1,443,914 1,068,548

Advances - net of provision 8,009,821 6,798,803

9.1 Particulars of advances (Gross)

9.1.1 In local currency 9,453,735 7,867,351

9.1.2 Short Term ( for upto one year) 4,961,136 3,889,903 Long Term ( for over one year) 4,492,599 3,977,448

9,453,735 7,867,351

9.2

Domestic Overseas TotalCategory of Classification

Other Assets Especially Mentioned 630,725 - 630,725 - - Substandard 584,540 - 584,540 117,446 117,446 Doubtful 543,106 - 543,106 271,553 271,553 Loss 1,496,005 - 1,496,005 1,496,005 1,054,915

3,254,376 - 3,254,376 1,885,004 1,443,914

9.3 Particulars of provision against non-performing advances

Specific General Total Specific General Total

Opening balance 1,068,548 - 1,068,548 910,939 - 910,939 Charge for the year 375,366 - 375,366 157,609 - 157,609

Closing balance 1,443,914 - 1,443,914 1,068,548 - 1,068,548

9.3.1 Particulars of provisions against non-performing advances

Specific General Total Specific General Total

In local currency 1,443,914 - 1,443,914 1,068,548 - 1,068,548

Advances include Rs. 3,254,376 (thousand) (2006 : 3,085,018 thousand) which have been placed under non-performingstatus as detailed below:-

Pakistan Investment Bonds are for the period of 10 years starting from December 14, 2000 with the yield 14% per annum(2006: 14% per annum).

Provincial Government securities comprise of Punjab Loan issued by the Government of Punjab on December 07, 1998 forthe period of 10 years with the yield 17.5% per annum (2006: 17.5% per annum).

20062007

Provision HeldRupees in '000'

2007

Rupees in '000'

Rupees in '000'

Classified Advances Provision Required

2007 2006

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

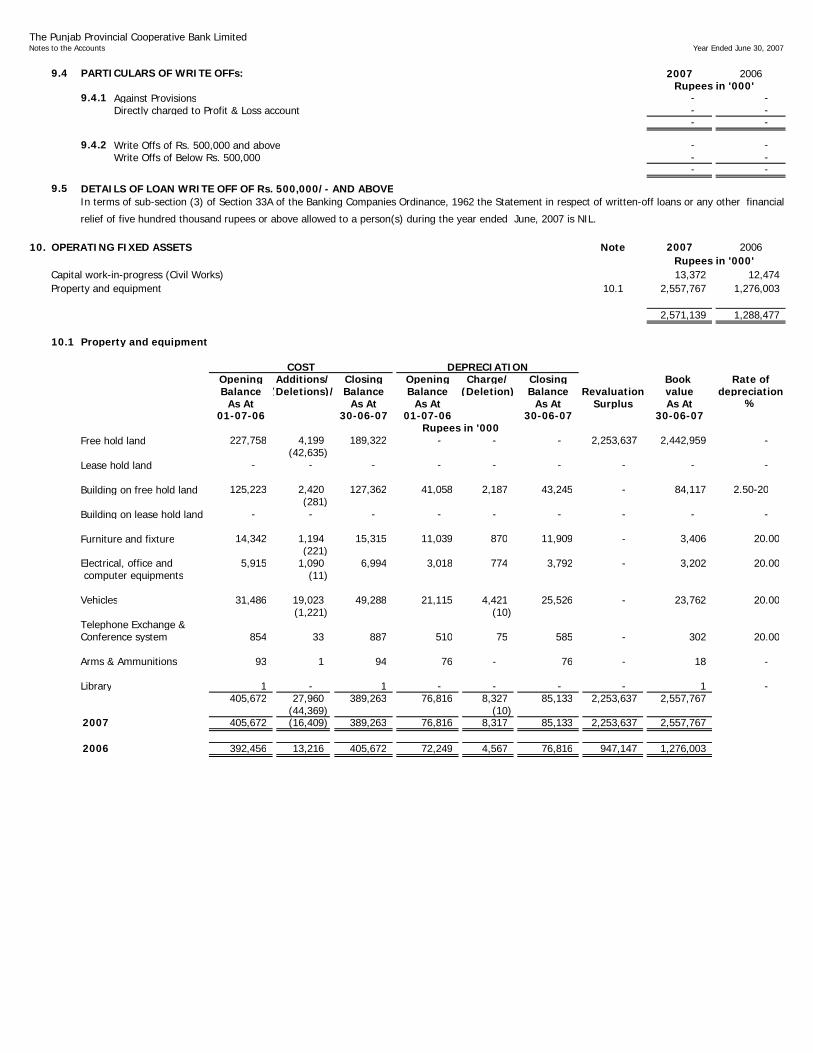

9.4 PARTICULARS OF WRITE OFFs: 2007 2006Rupees in '000'

9.4.1 Against Provisions - - Directly charged to Profit & Loss account - -

- -

9.4.2 Write Offs of Rs. 500,000 and above - - Write Offs of Below Rs. 500,000 - -

- -

9.5 DETAILS OF LOAN WRITE OFF OF Rs. 500,000/- AND ABOVE

10. OPERATING FIXED ASSETS Note 2007 2006Rupees in '000'

Capital work-in-progress (Civil Works) 13,372 12,474 Property and equipment 10.1 2,557,767 1,276,003

2,571,139 1,288,477

10.1 Property and equipment

COST DEPRECIATIONOpening Additions/ Closing Opening Charge/ Closing Book Rate ofBalance (Deletions)/ Balance Balance (Deletion) Balance Revaluation value depreciation

As At As At As At As At Surplus As At %01-07-06 30-06-07 01-07-06 30-06-07 30-06-07

Rupees in '000Free hold land 227,758 4,199 189,322 - - - 2,253,637 2,442,959 -

(42,635) Lease hold land - - - - - - - - -

Building on free hold land 125,223 2,420 127,362 41,058 2,187 43,245 - 84,117 2.50-20(281)

Building on lease hold land - - - - - - - - -

Furniture and fixture 14,342 1,194 15,315 11,039 870 11,909 - 3,406 20.00 (221)

Electrical, office and 5,915 1,090 6,994 3,018 774 3,792 - 3,202 20.00 computer equipments (11)

Vehicles 31,486 19,023 49,288 21,115 4,421 25,526 - 23,762 20.00 (1,221) (10)

Telephone Exchange &Conference system 854 33 887 510 75 585 - 302 20.00

Arms & Ammunitions 93 1 94 76 - 76 - 18 -

Library 1 - 1 - - - - 1 - 405,672 27,960 389,263 76,816 8,327 85,133 2,253,637 2,557,767

(44,369) (10) 2007 405,672 (16,409) 389,263 76,816 8,317 85,133 2,253,637 2,557,767

2006 392,456 13,216 405,672 72,249 4,567 76,816 947,147 1,276,003

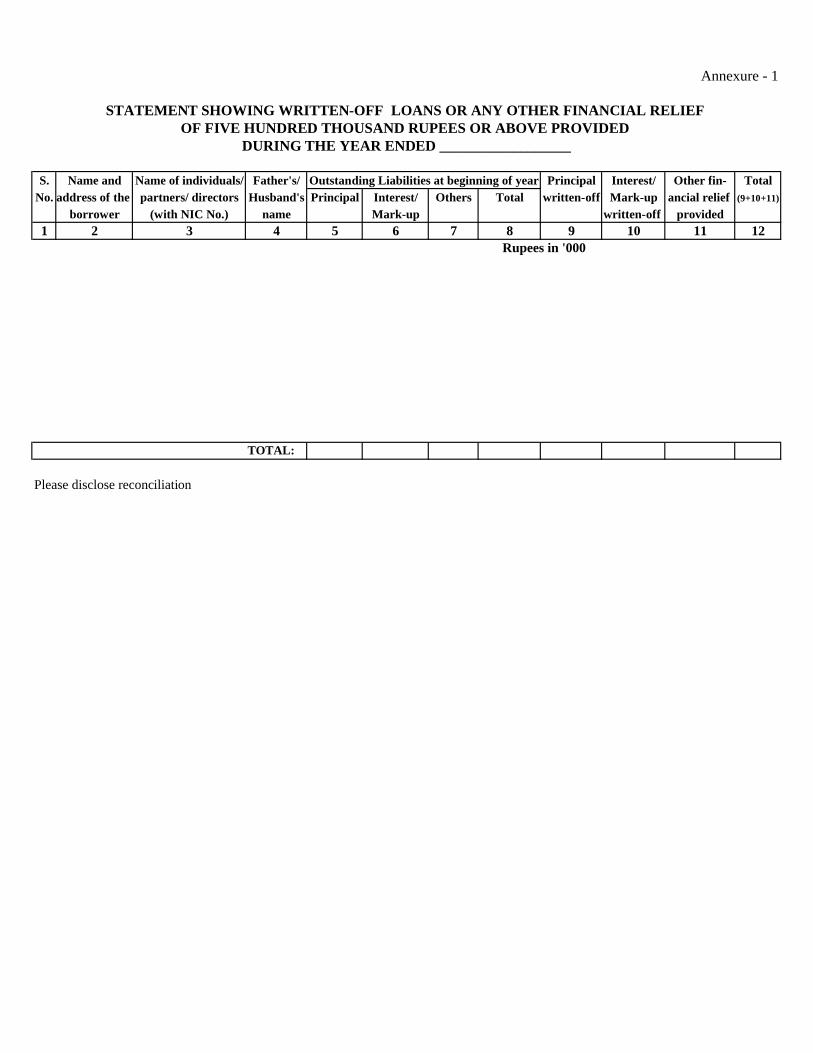

In terms of sub-section (3) of Section 33A of the Banking Companies Ordinance, 1962 the Statement in respect of written-off loans or any other financial

relief of five hundred thousand rupees or above allowed to a person(s) during the year ended June, 2007 is NIL.

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

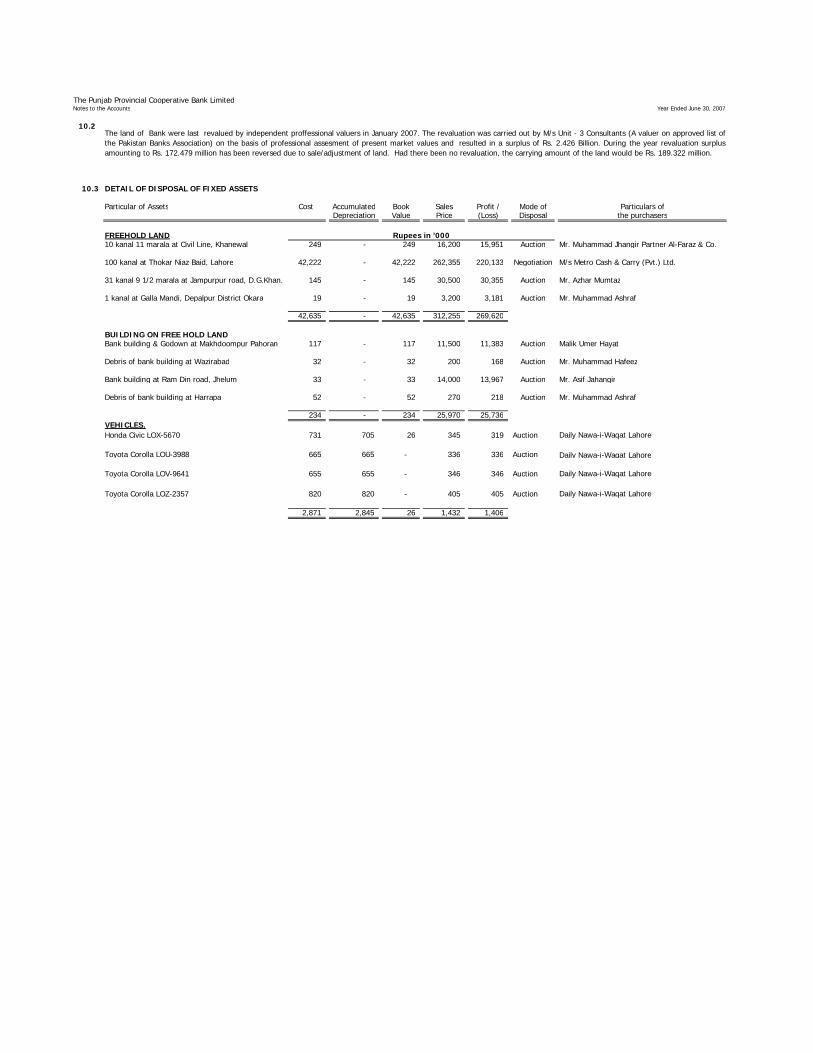

10.2

10.3 DETAIL OF DISPOSAL OF FIXED ASSETS

Particular of Assets Cost Accumulated Book Sales Profit / Mode of Particulars ofDepreciation Value Price (Loss) Disposal the purchasers

FREEHOLD LAND10 kanal 11 marala at Civil Line, Khanewal 249 - 249 16,200 15,951 Auction Mr. Muhammad Jhangir Partner Al-Faraz & Co.

100 kanal at Thokar Niaz Baid, Lahore 42,222 - 42,222 262,355 220,133 Negotiation M/s Metro Cash & Carry (Pvt.) Ltd.

31 kanal 9 1/2 marala at Jampurpur road, D.G.Khan. 145 - 145 30,500 30,355 Auction Mr. Azhar Mumtaz

1 kanal at Galla Mandi, Depalpur District Okara 19 - 19 3,200 3,181 Auction Mr. Muhammad Ashraf

42,635 - 42,635 312,255 269,620

BUILDING ON FREE HOLD LANDBank building & Godown at Makhdoompur Pahoran 117 - 117 11,500 11,383 Auction Malik Umer Hayat

Debris of bank building at Wazirabad 32 - 32 200 168 Auction Mr. Muhammad Hafeez

Bank building at Ram Din road, Jhelum 33 - 33 14,000 13,967 Auction Mr. Asif Jahangir

Debris of bank building at Harrapa 52 - 52 270 218 Auction Mr. Muhammad Ashraf

234 - 234 25,970 25,736 VEHICLES.Honda Civic LOX-5670 731 705 26 345 319 Auction Daily Nawa-i-Waqat Lahore

Toyota Corolla LOU-3988 665 665 - 336 336 Auction Daily Nawa-i-Waqat Lahore

Toyota Corolla LOV-9641 655 655 - 346 346 Auction

Toyota Corolla LOZ-2357 820 820 - 405 405 Auction Daily Nawa-i-Waqat Lahore

2,871 2,845 26 1,432 1,406

The land of Bank were last revalued by independent proffessional valuers in January 2007. The revaluation was carried out by M/s Unit - 3 Consultants (A valuer on approved list ofthe Pakistan Banks Association) on the basis of professional assesment of present market values and resulted in a surplus of Rs. 2.426 Billion. During the year revaluation surplusamounting to Rs. 172.479 million has been reversed due to sale/adjustment of land. Had there been no revaluation, the carrying amount of the land would be Rs. 189.322 million.

Daily Nawa-i-Waqat Lahore

Rupees in '000

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

Note 2007 2006Rupees in '000

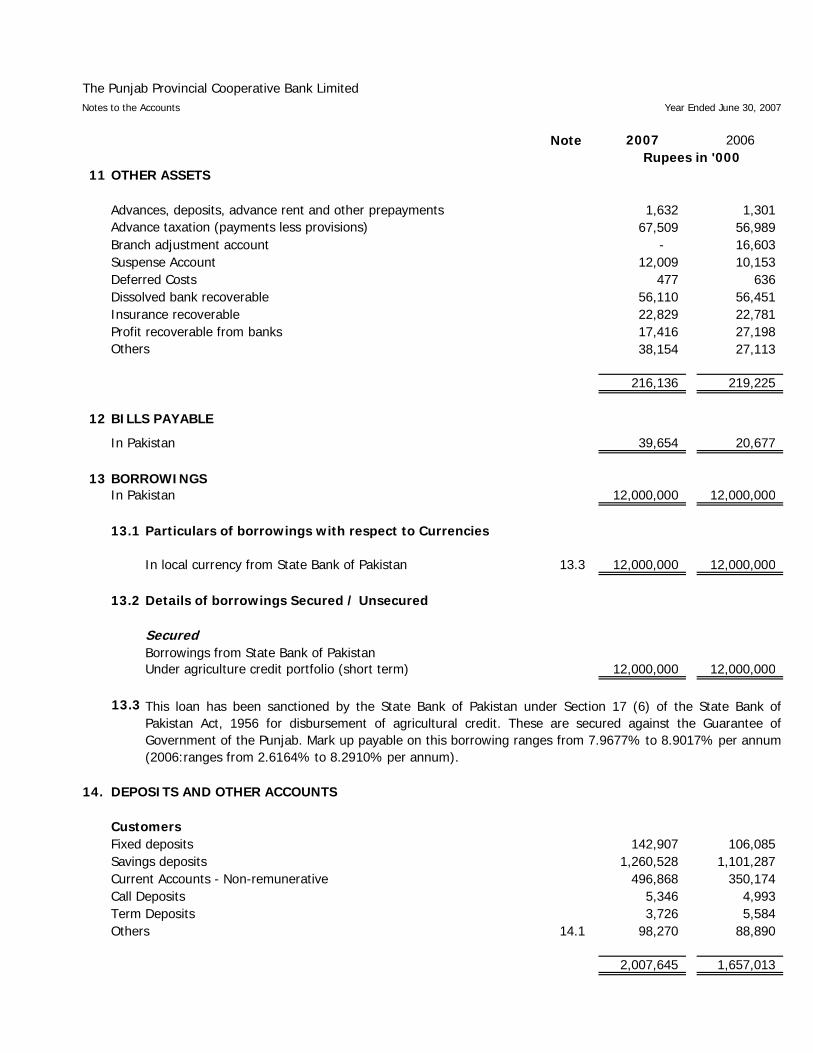

11 OTHER ASSETS

Advances, deposits, advance rent and other prepayments 1,632 1,301 Advance taxation (payments less provisions) 67,509 56,989 Branch adjustment account - 16,603 Suspense Account 12,009 10,153 Deferred Costs 477 636 Dissolved bank recoverable 56,110 56,451 Insurance recoverable 22,829 22,781 Profit recoverable from banks 17,416 27,198 Others 38,154 27,113

216,136 219,225

12 BILLS PAYABLE

In Pakistan 39,654 20,677

13 BORROWINGSIn Pakistan 12,000,000 12,000,000

13.1 Particulars of borrowings with respect to Currencies

In local currency from State Bank of Pakistan 13.3 12,000,000 12,000,000

13.2 Details of borrowings Secured / Unsecured

SecuredBorrowings from State Bank of Pakistan Under agriculture credit portfolio (short term) 12,000,000 12,000,000

13.3

14. DEPOSITS AND OTHER ACCOUNTS

CustomersFixed deposits 142,907 106,085 Savings deposits 1,260,528 1,101,287 Current Accounts - Non-remunerative 496,868 350,174 Call Deposits 5,346 4,993 Term Deposits 3,726 5,584 Others 14.1 98,270 88,890

2,007,645 1,657,013

This loan has been sanctioned by the State Bank of Pakistan under Section 17 (6) of the State Bank ofPakistan Act, 1956 for disbursement of agricultural credit. These are secured against the Guarantee ofGovernment of the Punjab. Mark up payable on this borrowing ranges from 7.9677% to 8.9017% per annum(2006:ranges from 2.6164% to 8.2910% per annum).

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

Note 2007 2006Rupees in '000'

14.1 Others include staff provident fund and staff security deposits.

14.2 Particulars of deposits

In local currency 2,007,645 1,657,013

15 OTHER LIABILITIES

Mark-up/ Return/ Interest payable in local currency 13,889 13,545 Accrued expenses 1,083 1,580 Branch adjustment account 34,194 - Sundry creditors 89,952 66,421 Dissolved banks payable 35,544 35,544 Others 10,961 6,463

185,623 123,553

16 SHARE CAPITAL

16.1 Authorized Capital

2007 2006

Unlimited Unlimited Ordinary shares of Rs.100/- each Unlimited Unlimited

16.2 Issued, subscribed and paid up

Ordinary shares of Rs. 100/- each3,927,780 3,879,600 Fully paid in cash 392,778 387,960

375,730 375,730 Issued as bonus shares 37,573 37,573

4,303,510 4,255,330 430,351 425,533

17 SURPLUS ON REVALUATION OF ASSETS

17.1 Surplus on revaluation of Fixed Assets 2,253,637 947,147 Land

17.2 Surplus on revaluation of Available-for-sale securitiesShares in Listed Companies 235,384 184,251

2,489,021 1,131,398

18 CONTINGENCIES AND COMMITMENTS

18.1 Guarantee Acceptances 18.1.1 461 461 Show cause notices by sales tax-under appeal 18.1.2 5,041 5,041

5,502 5,502

(Number of shares)

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

18.1.1

18.1.2

18.2

2007 2006Rupees in '000'

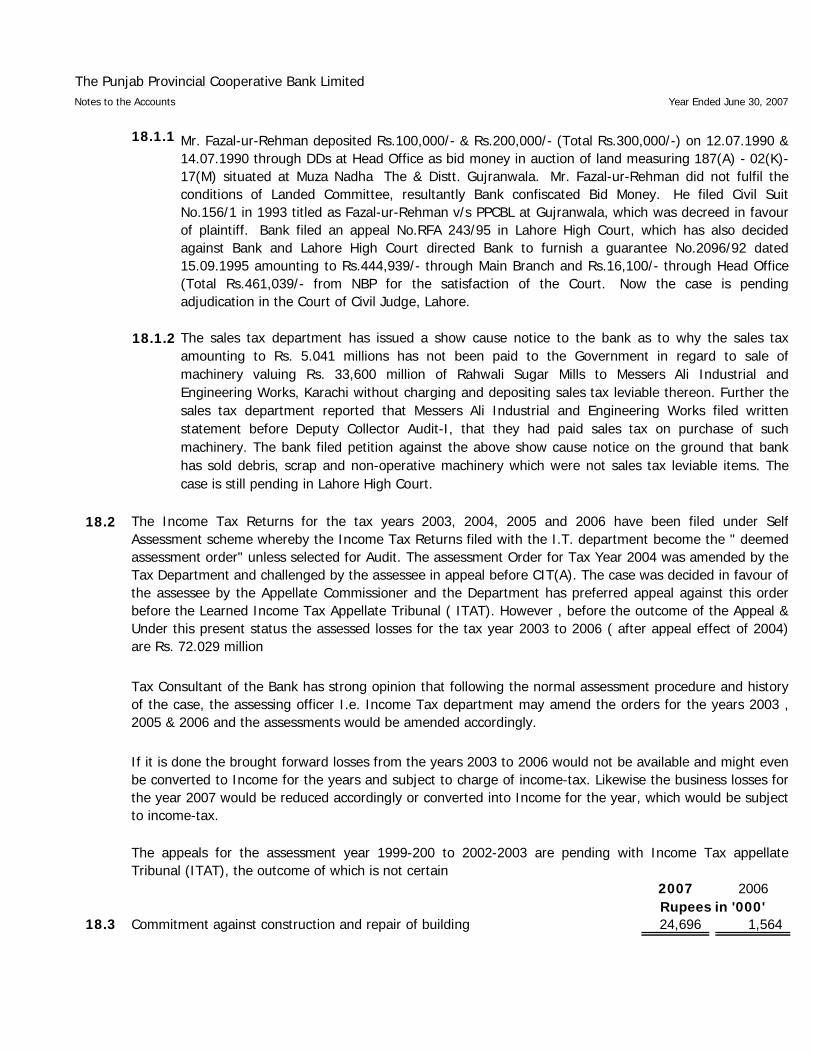

18.3 Commitment against construction and repair of building 24,696 1,564

The sales tax department has issued a show cause notice to the bank as to why the sales taxamounting to Rs. 5.041 millions has not been paid to the Government in regard to sale ofmachinery valuing Rs. 33,600 million of Rahwali Sugar Mills to Messers Ali Industrial andEngineering Works, Karachi without charging and depositing sales tax leviable thereon. Further thesales tax department reported that Messers Ali Industrial and Engineering Works filed writtenstatement before Deputy Collector Audit-I, that they had paid sales tax on purchase of suchmachinery. The bank filed petition against the above show cause notice on the ground that bankhas sold debris, scrap and non-operative machinery which were not sales tax leviable items. Thecase is still pending in Lahore High Court.

Mr. Fazal-ur-Rehman deposited Rs.100,000/- & Rs.200,000/- (Total Rs.300,000/-) on 12.07.1990 &14.07.1990 through DDs at Head Office as bid money in auction of land measuring 187(A) - 02(K)-17(M) situated at Muza Nadha The & Distt. Gujranwala. Mr. Fazal-ur-Rehman did not fulfil theconditions of Landed Committee, resultantly Bank confiscated Bid Money. He filed Civil SuitNo.156/1 in 1993 titled as Fazal-ur-Rehman v/s PPCBL at Gujranwala, which was decreed in favourof plaintiff. Bank filed an appeal No.RFA 243/95 in Lahore High Court, which has also decidedagainst Bank and Lahore High Court directed Bank to furnish a guarantee No.2096/92 dated15.09.1995 amounting to Rs.444,939/- through Main Branch and Rs.16,100/- through Head Office(Total Rs.461,039/- from NBP for the satisfaction of the Court. Now the case is pendingadjudication in the Court of Civil Judge, Lahore.

The appeals for the assessment year 1999-200 to 2002-2003 are pending with Income Tax appellateTribunal (ITAT), the outcome of which is not certain

The Income Tax Returns for the tax years 2003, 2004, 2005 and 2006 have been filed under SelfAssessment scheme whereby the Income Tax Returns filed with the I.T. department become the " deemedassessment order" unless selected for Audit. The assessment Order for Tax Year 2004 was amended by theTax Department and challenged by the assessee in appeal before CIT(A). The case was decided in favour ofthe assessee by the Appellate Commissioner and the Department has preferred appeal against this orderbefore the Learned Income Tax Appellate Tribunal ( ITAT). However , before the outcome of the Appeal &Under this present status the assessed losses for the tax year 2003 to 2006 ( after appeal effect of 2004)are Rs. 72.029 million

Tax Consultant of the Bank has strong opinion that following the normal assessment procedure and historyof the case, the assessing officer I.e. Income Tax department may amend the orders for the years 2003 ,2005 & 2006 and the assessments would be amended accordingly.

If it is done the brought forward losses from the years 2003 to 2006 would not be available and might evenbe converted to Income for the years and subject to charge of income-tax. Likewise the business losses forthe year 2007 would be reduced accordingly or converted into Income for the year, which would be subjectto income-tax.

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

Note 2007 2006Rupees in '000

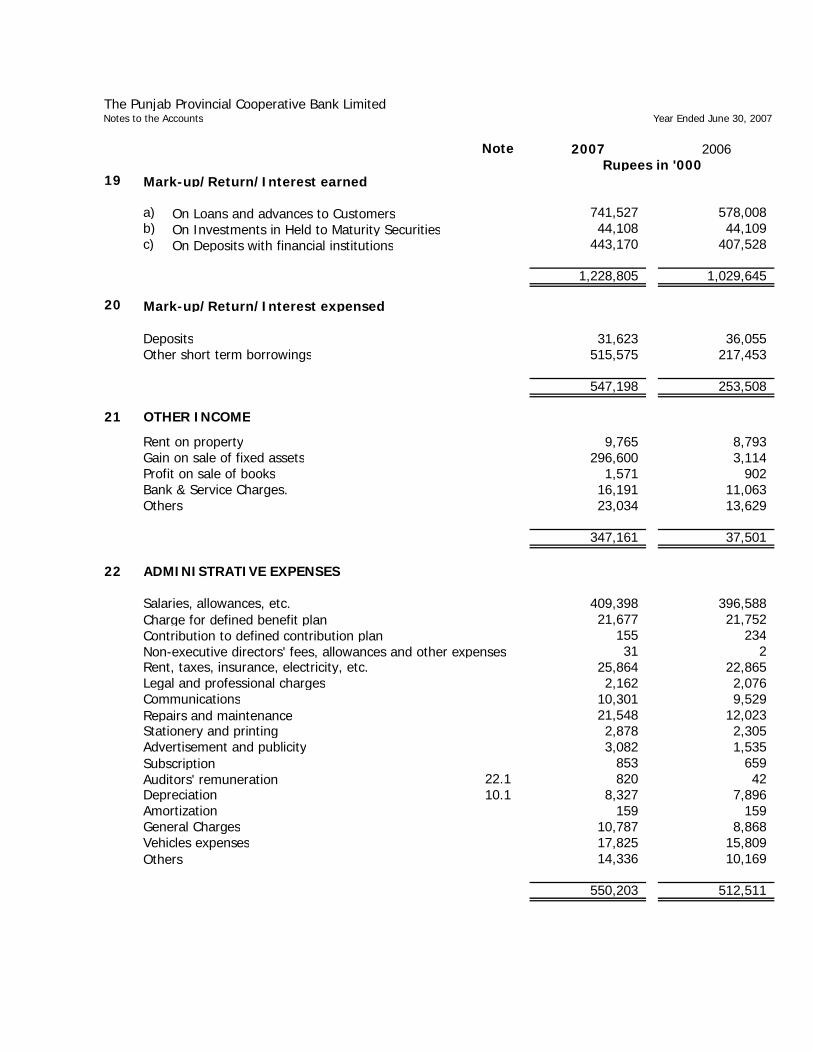

19 Mark-up/Return/Interest earned

a) 741,527 578,008 b) 44,108 44,109 c) 443,170 407,528

1,228,805 1,029,645

20 Mark-up/Return/Interest expensed

Deposits 31,623 36,055 Other short term borrowings 515,575 217,453

547,198 253,508

21 OTHER INCOME

Rent on property 9,765 8,793 Gain on sale of fixed assets 296,600 3,114 Profit on sale of books 1,571 902 Bank & Service Charges. 16,191 11,063 Others 23,034 13,629

347,161 37,501

22 ADMINISTRATIVE EXPENSES

Salaries, allowances, etc. 409,398 396,588 Charge for defined benefit plan 21,677 21,752 Contribution to defined contribution plan 155 234 Non-executive directors' fees, allowances and other expenses 31 2 Rent, taxes, insurance, electricity, etc. 25,864 22,865 Legal and professional charges 2,162 2,076 Communications 10,301 9,529 Repairs and maintenance 21,548 12,023 Stationery and printing 2,878 2,305 Advertisement and publicity 3,082 1,535 Subscription 853 659 Auditors' remuneration 22.1 820 42 Depreciation 10.1 8,327 7,896 Amortization 159 159 General Charges 10,787 8,868 Vehicles expenses 17,825 15,809 Others 14,336 10,169

550,203 512,511

On Loans and advances to Customers

On Deposits with financial institutionsOn Investments in Held to Maturity Securities

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

2007 2006Rupees in '000

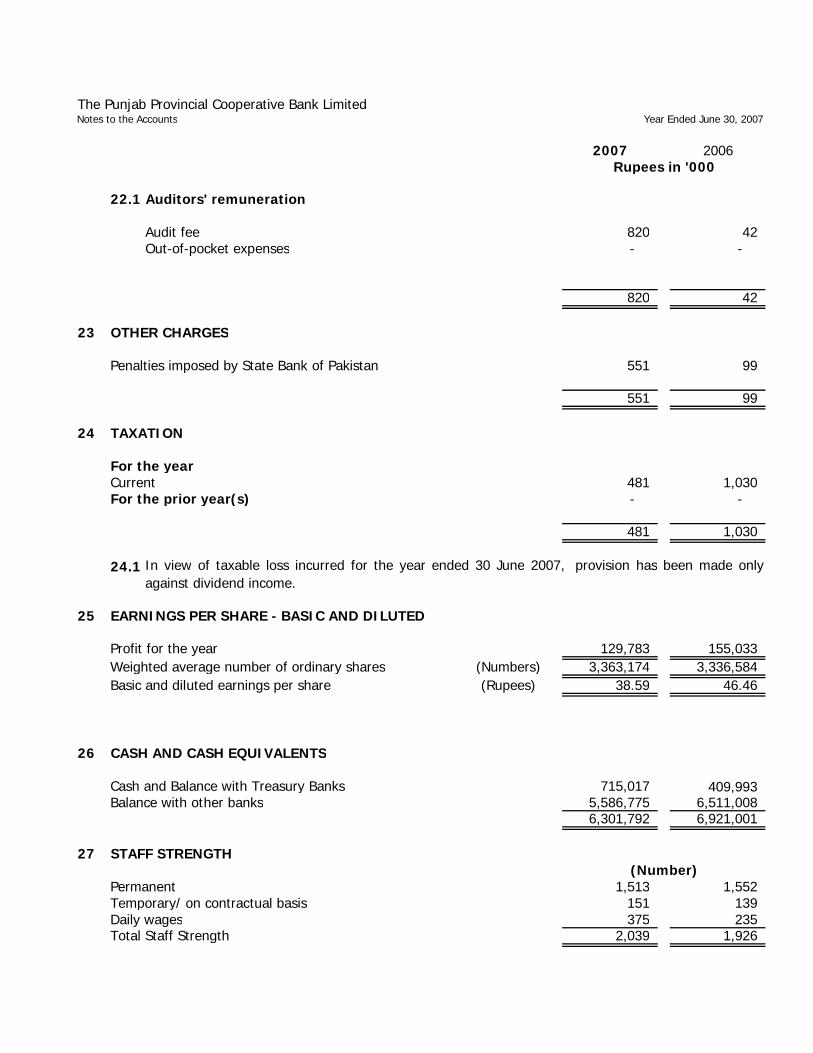

22.1 Auditors' remuneration

Audit fee 820 42 Out-of-pocket expenses - -

820 42

23 OTHER CHARGES

Penalties imposed by State Bank of Pakistan 551 99

551 99

24 TAXATION

For the yearCurrent 481 1,030 For the prior year(s) - -

481 1,030

24.1

25 EARNINGS PER SHARE - BASIC AND DILUTED

Profit for the year 129,783 155,033 Weighted average number of ordinary shares (Numbers) 3,363,174 3,336,584 Basic and diluted earnings per share (Rupees) 38.59 46.46

26 CASH AND CASH EQUIVALENTS

Cash and Balance with Treasury Banks 715,017 409,993 Balance with other banks 5,586,775 6,511,008

6,301,792 6,921,001

27 STAFF STRENGTH(Number)

Permanent 1,513 1,552 Temporary/ on contractual basis 151 139 Daily wages 375 235 Total Staff Strength 2,039 1,926

In view of taxable loss incurred for the year ended 30 June 2007, provision has been made onlyagainst dividend income.

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

28 COMPENSATION OF DIRECTORS AND EXECUTIVES

President / Chief Executive Directors Executives 2007 2006 2007 2006 2007 2006

Fees - - - - - - Managerial remuneration - - - - - - Charge for defined benefit plan - - - - - - Contribution to defined contribution plan - - - - - - Rent and house maintenance - - - - - - Utilities - - - - - - Medical - - - - - - Conveyance - - - - - -

- - - - - -

Number of persons 1 1 - - - -

28.1

29 FAIR VALUE OF FINANCIAL INSTRUMENTS

29.1 On-balance sheet financial instruments

Book value Fair value Book value Fair value

AssetsCash balances with treasury banks 715,017 715,017 409,993 409,993 Balances with other banks 5,586,775 5,586,775 6,511,008 6,511,008 Lending to financial institutions - - - - Investments 558,009 558,009 506,876 506,876 Advances 8,009,821 8,009,821 6,798,803 6,798,803 Other assets 92,040 92,040 105,597 105,597

14,961,662 14,961,662 14,332,277 14,332,277

LiabilitiesBills payable 39,654 39,654 20,677 20,677 Borrowings 12,000,000 12,000,000 12,000,000 12,000,000 Deposits and other accounts 2,007,645 2,007,645 1,657,013 1,657,013 Sub-ordinated loans - - - - Liabilities against assets subject to finance lease - - - - Other liabilities 185,623 185,623 123,553 123,553

14,232,922 14,232,922 13,801,243 13,801,243

29.2

29.3

30 RELATED PARTY TRANSACTIONS2007 2006

Balances outstanding Rupees in '000'

Loans and Advances - 14,152 Deposits - 4,940

Transactions during the yearLoans and advances given - 11,634 Loans and advances adjusted/ received - 11,064 Mark up received on loans and advances - 1,218 Mark up on deposits - 32

30.1 The transactions and contracts with related parties, other than those under the terms of employment, are carried out on anArm's length basis determined in accordance with the " Comparable Uncontrolled Price Method

In the opinion of the management, the fair value of the remaining financial assets and liabilities are not significantly differentfrom their carrying values since assets and liabilities are either short term in nature or in the case of customer loans anddeposits are frequently repriced.

Rupees in '000

Rupees in '000

20062007

At present, the Chairman, Planning and Development, government of the Punjab is the administrator of the bank, who hasfull powers and duties that of a Board of Directors.

The fair value of available for sale investments other than those classified as held to maturity is based on quoted marketprice.

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

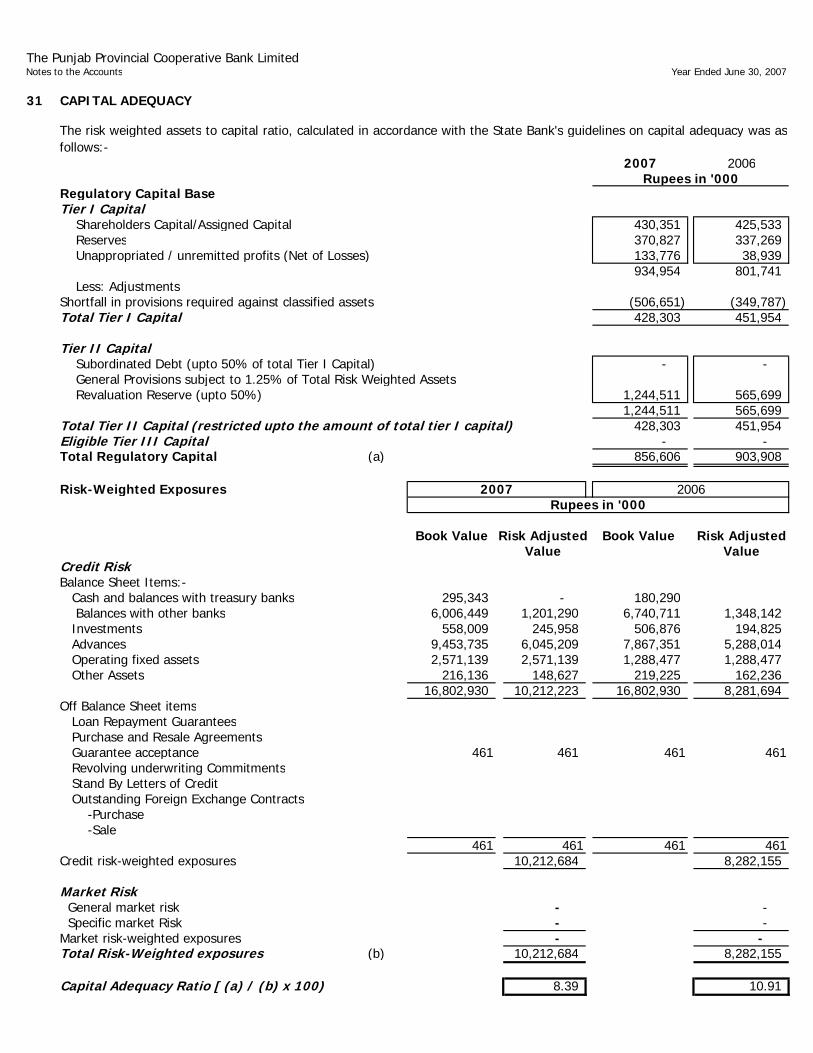

31 CAPITAL ADEQUACY

2007 2006Rupees in '000

Regulatory Capital BaseTier I Capital Shareholders Capital/Assigned Capital 430,351 425,533 Reserves 370,827 337,269 Unappropriated / unremitted profits (Net of Losses) 133,776 38,939

934,954 801,741 Less: AdjustmentsShortfall in provisions required against classified assets (506,651) (349,787) Total Tier I Capital 428,303 451,954

Tier II Capital Subordinated Debt (upto 50% of total Tier I Capital) - - General Provisions subject to 1.25% of Total Risk Weighted Assets Revaluation Reserve (upto 50%) 1,244,511 565,699

1,244,511 565,699 Total Tier II Capital (restricted upto the amount of total tier I capital) 428,303 451,954 Eligible Tier III Capital - - Total Regulatory Capital (a) 856,606 903,908

Risk-Weighted Exposures

Book Value Risk Adjusted Book Value Risk AdjustedValue Value

Credit RiskBalance Sheet Items:- Cash and balances with treasury banks 295,343 - 180,290 Balances with other banks 6,006,449 1,201,290 6,740,711 1,348,142 Investments 558,009 245,958 506,876 194,825 Advances 9,453,735 6,045,209 7,867,351 5,288,014 Operating fixed assets 2,571,139 2,571,139 1,288,477 1,288,477 Other Assets 216,136 148,627 219,225 162,236

16,802,930 10,212,223 16,802,930 8,281,694 Off Balance Sheet items Loan Repayment Guarantees Purchase and Resale Agreements Guarantee acceptance 461 461 461 461 Revolving underwriting Commitments Stand By Letters of Credit Outstanding Foreign Exchange Contracts -Purchase -Sale

461 461 461 461Credit risk-weighted exposures 10,212,684 8,282,155

Market Risk General market risk - - Specific market Risk - - Market risk-weighted exposures - - Total Risk-Weighted exposures (b) 10,212,684 8,282,155

Capital Adequacy Ratio [ (a) / (b) x 100) 8.39 10.91

20062007Rupees in '000

The risk weighted assets to capital ratio, calculated in accordance with the State Bank's guidelines on capital adequacy was asfollows:-

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

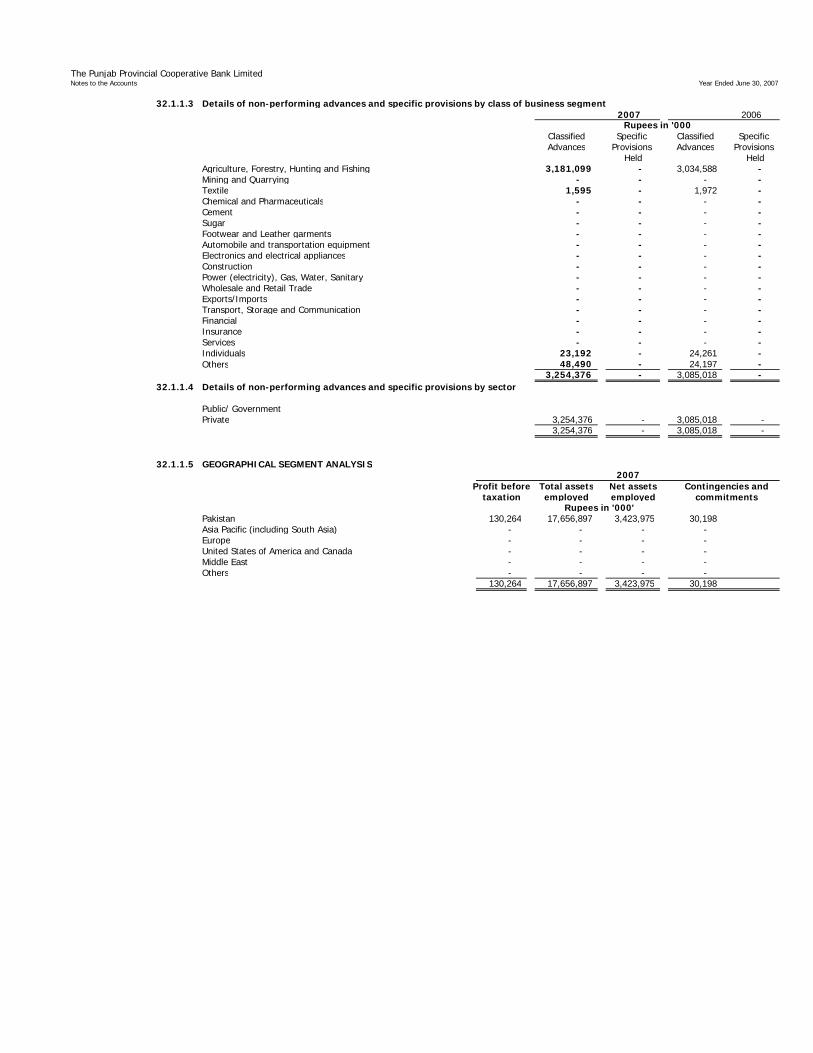

32.1.1.3 Details of non-performing advances and specific provisions by class of business segment 2007 2006

Classified Specific Classified Specific Advances Provisions Advances Provisions

Held HeldAgriculture, Forestry, Hunting and Fishing 3,181,099 - 3,034,588 - Mining and Quarrying - - - - Textile 1,595 - 1,972 - Chemical and Pharmaceuticals - - - - Cement - - - - Sugar - - - - Footwear and Leather garments - - - - Automobile and transportation equipment - - - - Electronics and electrical appliances - - - - Construction - - - - Power (electricity), Gas, Water, Sanitary - - - - Wholesale and Retail Trade - - - - Exports/Imports - - - - Transport, Storage and Communication - - - - Financial - - - - Insurance - - - - Services - - - - Individuals 23,192 - 24,261 - Others 48,490 - 24,197 -

3,254,376 - 3,085,018 - 32.1.1.4 Details of non-performing advances and specific provisions by sector

Public/ GovernmentPrivate 3,254,376 - 3,085,018 -

3,254,376 - 3,085,018 -

32.1.1.5 GEOGRAPHICAL SEGMENT ANALYSIS

Profit before Total assets Net assets Contingencies andtaxation employed employed commitments

Rupees in '000'Pakistan 130,264 17,656,897 3,423,975 30,198 Asia Pacific (including South Asia) - - - - Europe - - - - United States of America and Canada - - - - Middle East - - - - Others - - - -

130,264 17,656,897 3,423,975 30,198

Rupees in '000

2007

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

32.2 Market Risk

32.2.1 Foreign Exchange Risk2007

Assets Liabilities Off-balance Net foreignsheet itemscurrency exposure

Rupees in '000Pakistan rupee 17,656,897 14,232,922 - - United States dollar - - - - Great Britain pound - - - - Deutsche mark - - - - Japanese yen - - - - Euro - - - -

17,656,897 14,232,922 - -

32.2.2 Currency risk is the risk that the value of a financial instrument will fluctuate due to change in foreign exchange risk

32.2.3 Mismatch of Interest Rate Sensitive Assets and Liabilities

Effective TotalOver 1 Over 3 Over 6 Over 1 Over 2 Over 3 Over 5 Non-interest

Yield/ Upto 1 to 3 to 6 Months to 1 to 2 to 3 to 5 to 10 Above bearing financial Interest Month Months Months Year Years Years Years Years 10 Years instruments

rate Rupees in '000'On-balance sheet financial instruments

AssetsCash and balances with treasury banks 1.40% 715,017 287,992 - - - - - - - - 427,025 Balances with other banks 9.16% 5,586,775 5,430,552 - - - - - - - - 156,223 Lending to financial institutions - Investments 10.50% 558,009 245,958 - - - 12,051 - 300,000 - - - Advances 13.50% 9,453,735 805,840 307,258 341,965 3,111,817 1,024,671 1,069,510 1,822,767 816,205 153,403 299 Other assets 92,040 - - - - - - - - - 92,040

16,405,576 6,770,342 307,258 341,965 3,111,817 1,036,722 1,069,510 2,122,767 816,205 153,403 675,587 LiabilitiesBills payable 39,654 - - - - - - - - - 39,654 Borrowings 8.82% 12,000,000 - 3,000,000 - 5,000,000 4,000,000 - - - - - Deposits and other accounts 3.75% 2,007,645 1,459,434 277,584 9,738 26,533 16,172 6,547 77,512 - 86,973 47,152 Sub-ordinated loans - Liabilities against assets subject to finance lease - Other liabilities 185,623 - - - - - - - - - 185,546

14,232,922 1,459,434 3,277,584 9,738 5,026,533 4,016,172 6,547 77,512 - 86,973 272,352

On-balance sheet gap 2,172,654 5,310,908 (2,970,326) 332,227 (1,914,716) (2,979,450) 1,062,963 2,045,255 816,205 66,430 403,235

Off-balance sheet financial instruments

Forward Lending - - - - - - - - - - - (including call lending, repurchase agreement lending,commitments to extend credit, etc.)

Forward borrowings - - - - - - - - - - - (including call borrowing, repurchase agreementborrowing, etc.)Off-balance sheet gap - - - - - - - - - - -

Total Yield/Interest Risk Sensitivity Gap 2,172,654 5,310,908 (2,970,326) 332,227 (1,914,716) (2,979,450) 1,062,963 2,045,255 816,205 66,430 403,235

Cumulative Yield/Interest Risk Sensitivity Gap 2,172,654 7,483,562 4,513,236 4,845,463 2,930,747 (48,703) 1,014,260 3,059,515 3,875,720 3,942,150 4,345,385

Yield Risk is the risk of decline in earnings due to adverse movement of the yield curve.Interest rate risk is the risk that the value of the financial instrument will fluctuate due to changes in the market interest rates.

Exposed to Yield/ Interest risk2007

The Punjab Provincial Cooperative Bank LimitedNotes to the Accounts Year Ended June 30, 2007

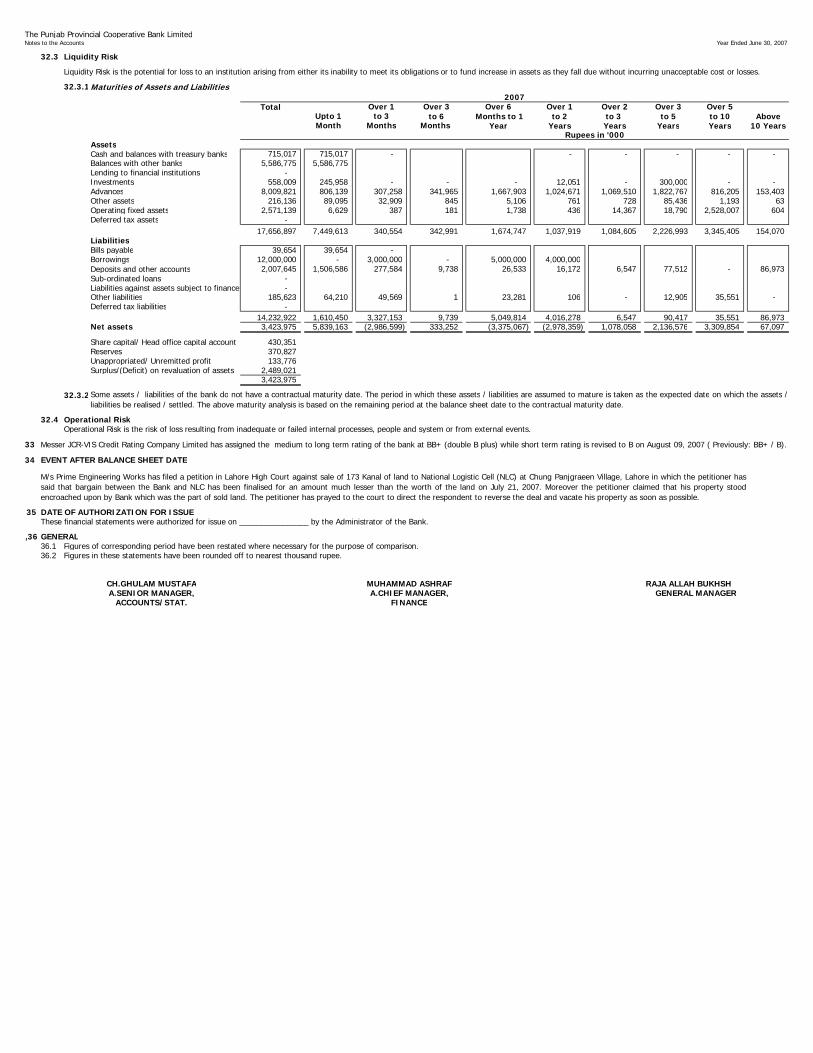

32.3 Liquidity Risk

Liquidity Risk is the potential for loss to an institution arising from either its inability to meet its obligations or to fund increase in assets as they fall due without incurring unacceptable cost or losses.

32.3.1Maturities of Assets and Liabilities

Total Over 1 Over 3 Over 6 Over 1 Over 2 Over 3 Over 5Upto 1 to 3 to 6 Months to 1 to 2 to 3 to 5 to 10 AboveMonth Months Months Year Years Years Years Years 10 Years

AssetsCash and balances with treasury banks 715,017 715,017 - - - - - - Balances with other banks 5,586,775 5,586,775Lending to financial institutions - Investments 558,009 245,958 - - - 12,051 - 300,000 - - Advances 8,009,821 806,139 307,258 341,965 1,667,903 1,024,671 1,069,510 1,822,767 816,205 153,403Other assets 216,136 89,095 32,909 845 5,106 761 728 85,436 1,193 63 Operating fixed assets 2,571,139 6,629 387 181 1,738 436 14,367 18,790 2,528,007 604 Deferred tax assets -

17,656,897 7,449,613 340,554 342,991 1,674,747 1,037,919 1,084,605 2,226,993 3,345,405 154,070LiabilitiesBills payable 39,654 39,654 - Borrowings 12,000,000 - 3,000,000 - 5,000,000 4,000,000 Deposits and other accounts 2,007,645 1,506,586 277,584 9,738 26,533 16,172 6,547 77,512 - 86,973 Sub-ordinated loans - Liabilities against assets subject to finance lease - Other liabilities 185,623 64,210 49,569 1 23,281 106 - 12,905 35,551 - Deferred tax liabilities -

14,232,922 1,610,450 3,327,153 9,739 5,049,814 4,016,278 6,547 90,417 35,551 86,973 Net assets 3,423,975 5,839,163 (2,986,599) 333,252 (3,375,067) (2,978,359) 1,078,058 2,136,576 3,309,854 67,097

Share capital/ Head office capital account 430,351 Reserves 370,827 Unappropriated/ Unremitted profit 133,776 Surplus/(Deficit) on revaluation of assets 2,489,021

3,423,975

32.3.2

32.4 Operational RiskOperational Risk is the risk of loss resulting from inadequate or failed internal processes, people and system or from external events.

33 Messer JCR-VIS Credit Rating Company Limited has assigned the medium to long term rating of the bank at BB+ (double B plus) while short term rating is revised to B on August 09, 2007 ( Previously: BB+ / B).

34 EVENT AFTER BALANCE SHEET DATE

35 DATE OF AUTHORIZATION FOR ISSUEThese financial statements were authorized for issue on ________________ by the Administrator of the Bank.

,36 GENERAL36.1 Figures of corresponding period have been restated where necessary for the purpose of comparison.36.2 Figures in these statements have been rounded off to nearest thousand rupee.

RAJA ALLAH BUKHSH

2007

Rupees in '000

CH.GHULAM MUSTAFAA.SENIOR MANAGER,

ACCOUNTS/STAT.

Some assets / liabilities of the bank do not have a contractual maturity date. The period in which these assets / liabilities are assumed to mature is taken as the expected date on which the assets /liabilities be realised / settled. The above maturity analysis is based on the remaining period at the balance sheet date to the contractual maturity date.

M/s Prime Engineering Works has filed a petition in Lahore High Court against sale of 173 Kanal of land to National Logistic Cell (NLC) at Chung Panjgraeen Village, Lahore in which the petitioner hassaid that bargain between the Bank and NLC has been finalised for an amount much lesser than the worth of the land on July 21, 2007. Moreover the petitioner claimed that his property stoodencroached upon by Bank which was the part of sold land. The petitioner has prayed to the court to direct the respondent to reverse the deal and vacate his property as soon as possible.

GENERAL MANAGERMUHAMMAD ASHRAFA.CHIEF MANAGER,

FINANCE

46 GENERAL46.1 The note numbers given are for reference purposes. Further details may be given, if considered necessary, by

way of additional note(s).46.2 Except for the first financial statements laid before the shareholders of the bank financial statements shall

also give the corresponding figures for the immediately preceding financial year. This requirement shall, in caseof banks required to prepare half yearly financial statements, be applicable to the immediately precedingcorresponding period.

46.3 The figures in the financial statements may be rounded off to the nearest thousand.46.4 The following shall be disclosed in the financial statements namely:

i) All material information necessary to make the financial statements clear and understandable;

ii) If a fundamental accounting assumption , namely, going concern, consistency and accrual is not followed in preparation of financial statement, that fact together with the reason thereof:

iii) Particulars of any charge on the assets of the bank to secure the liabilities of any other person including,where practicable, the amount so secured (particulars of beneficiary along with relationship to the bank ordirectors).

iv) Change in an accounting policy that has material effect in the current year or may have a material effect inthe subsequent years together with reasons for the change and the financial effect of the change, ifmaterial.

46.5 The surplus on revaluation of fixed assets shall be treated and shown as specified in section 235 of theCompanies Ordinance, 1984. Additions to, and deductions from, adjustments in or applications of the surplus onrevaluation, whether resulting from disposal of the revalued asset(s) or otherwise ( detail to be provided) shallalso be stated.

46.6 Where any material item shown in the financial statements or included in amounts shown therein cannot bedetermined with substantial accuracy, an estimated amount described as such shall be included in respect ofthat item together with the description of the item.

46.7 No liability shall be shown in the balance sheet or the notes thereto at a value less than the amount at which it isrepayable (unless the quantum of repayment is at the option of the bank) at the date of the balance sheet or if itis not then repayable, at the amount at which it will first become so repayable thereafter, less, where appropriate,reasonable deduction for discount until that date.

46.8 If in the opinion of the directors any of the current assets have, on realization in the ordinary course of thebank's business, a value less than the amount at which they are stated in the financial statements, a disclosure ofthe fact that the directors are of that opinion together with their estimates of the realizable value and the reasonsfor assigning higher values in the balance sheet shall be required.

46.9 Terms and expressions not defined in the Banking Companies Ordinance, 1962 have the same meaning as inthe Companies Ordinance, 1984 unless there is anything repugnant in the subject or context.

46.10 Wherever the words " to be specified " have been used in the Notes, it connotes that only such amounts areto be disclosed which are material.

46.11 Disclose, together with a commentary by management, the amount of significant cash and cash equivalentbalances held by the bank that are not available for use by the bank.

46.12 The amount at which any asset or liability is stated in the balance sheet should not be off-set by thededuction of another liability or asset unless a legal right of set off exists and the off-setting represents theexpectation as to the realization or settlement of the asset or liability.

46.13 Income and expense items should not be off-set except for those relating to hedges and to assets andliabilities which have been offset in accordance with note 46.12.

1

46.14 When income and expense items are presented on a net basis, even though the corresponding financialassets and financial liabilities on the balance sheet have not been offset, disclose the reason for thatpresentation if the effect is significant.

46.15 When the presentation or classification of items in the financial statements is amended and comparativeamounts are reclassified, disclose the nature, amount of, and reason for any reclassification. When thepresentation or classification of items in the financial statements is amended, but it is impracticable toreclassify comparative amounts, disclose the reason for not reclassifying and the nature of the changesthat would have been made if amounts were reclassified.

46.16 Where any property and equipment or asset, acquired with the funds of the bank, is not held in thename of the bank or is not in the possession and control of the bank, this fact shall be stated, and thedescription and value of the property or asset, the person in whose name and possession or control it isheld shall be disclosed.

46.17 Where information is required about the extent and nature, including significant terms and conditionsthat may affect the amount, timing and certainty of future cash flows, terms and conditions that maywarrant disclosure include:

a) the principal, stated, face or other similar amount which, for some derivative instruments, may bethe amount (referred to as the notional amount) on which future payments are based;

b) the date of maturity, expiry or execution;

c) early settlement options held by either party to the instrument, including the period in which, ofdate at which, the options may be exercised and the exercise price or range of prices;

d) options held by either party to the instrument to convert the instrument into, or exchange it for,another financial instrument or some other asset or liability, including the period in which, or date at which, the options may be exercised and the conversion or exchange ratio(s);

e) the amount and timing of scheduled future cash receipts or payments of the principal amount ofthe instrument, including installment repayments and any sinking fund or similar requirements;

f) stated rate or amount of interest/mark-up, dividend or other periodical return on principal and the timing of payments;

g) collateral held, in the case of a financial asset, or pledged, in the case of a financial liability;

h) in the case of an instrument for which cash flows are denominated in a currency other than thebank's reporting currency, the currency in which receipts or payments are required;

i) in the case of an instrument that provides for an exchange, information described in items (a) to (h) for the instrument to be acquired in the exchange; and

j) any condition of the instrument or an associated covenant that, if contravened, would significantlyalter any of the other terms (for example, a maximum debt-to-equity ratio in a bond covenant that,if contravened, would make the full principal amount of the bond due and payable immediately).

46.18 Any information required to be given in respect of any of the items in the financial statements shall, if itcannot be included in such statements, be furnished in a separate note, schedule or statement to beattached to, and which shall be deemed to form an integral part of the financial statements.

46.19 All banks operating in Pakistan (whether incorporated in Pakistan or outside Pakistan and whether listedor not) shall prepare their accounts in accordance with the directives issued by the State Bank ofPakistan from time to time, the Banking Companies Ordinance 1962, the International AccountingStandards and International Financial Reporting Standards as notified in the official Gazette by the Securities and Exchange Commission of Pakistan for listed companies under section 234(3)(i) of the Companies Ordinance 1984.

46.20 Captions in respect of which no amounts exist may not be reproduced in the financial statements except

1

in case of Balance Sheet and Profit & Loss account.

46.21 Banks are encouraged to disclose financial highlights of recent periods. Banks will decide the periods for disclosing the past financial highlights. They may also consider disclosing trends in key financial ratios from investors perspective and transparency in disclosure.

46.21 Following notes will be applicable when Basel II is implementedNote Title44.1 Capital Assessment and Adequacy Basel II Specific (will replace Note 44)45.1.2 Credit Risk-General Disclosures Basel II Specific45.2 Equity Position risk in the banking book Basel II Specific45.3.4 Yield/Interest Rate Risk in the Banking Book (IRRBB)-Basel II Specific45.5.1 Operational Risk-Disclosures Basel II Specific

1

Annexure - 1

STATEMENT SHOWING WRITTEN-OFF LOANS OR ANY OTHER FINANCIAL RELIEF OF FIVE HUNDRED THOUSAND RUPEES OR ABOVE PROVIDED

DURING THE YEAR ENDED __________________

S. Name and Name of individuals/ Father's/ Principal Interest/ Other fin- TotalNo. address of the partners/ directors Husband's Principal Interest/ Others Total written-off Mark-up ancial relief (9+10+11)

borrower (with NIC No.) name Mark-up written-off provided1 2 3 4 5 6 7 8 9 10 11 12

TOTAL:

Please disclose reconciliation

Outstanding Liabilities at beginning of year

Rupees in '000

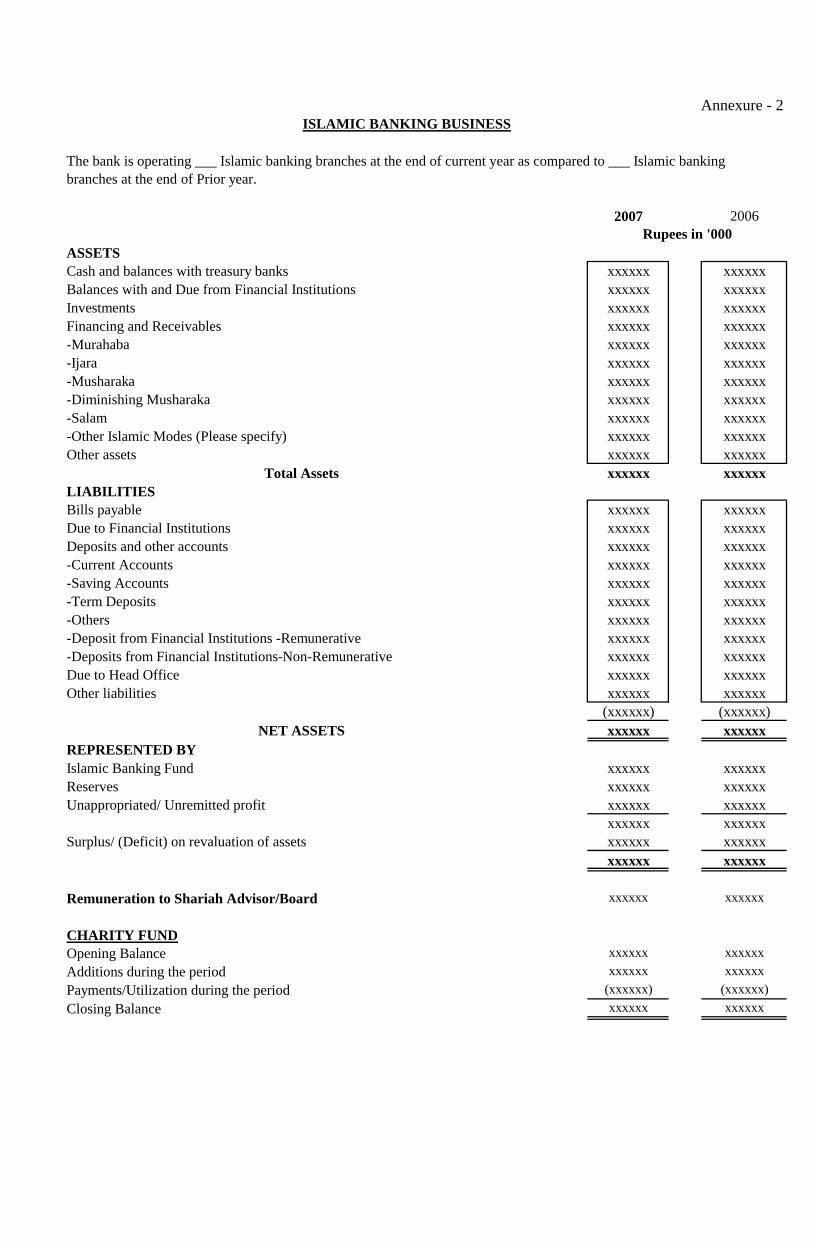

Annexure - 2

The bank is operating ___ Islamic banking branches at the end of current year as compared to ___ Islamic bankingbranches at the end of Prior year.

2007 2006

ASSETSCash and balances with treasury banks xxxxxx xxxxxxBalances with and Due from Financial Institutions xxxxxx xxxxxxInvestments xxxxxx xxxxxxFinancing and Receivables xxxxxx xxxxxx-Murahaba xxxxxx xxxxxx-Ijara xxxxxx xxxxxx-Musharaka xxxxxx xxxxxx-Diminishing Musharaka xxxxxx xxxxxx-Salam xxxxxx xxxxxx-Other Islamic Modes (Please specify) xxxxxx xxxxxxOther assets xxxxxx xxxxxx

Total Assets xxxxxx xxxxxxLIABILITIESBills payable xxxxxx xxxxxxDue to Financial Institutions xxxxxx xxxxxxDeposits and other accounts xxxxxx xxxxxx-Current Accounts xxxxxx xxxxxx-Saving Accounts xxxxxx xxxxxx-Term Deposits xxxxxx xxxxxx-Others xxxxxx xxxxxx-Deposit from Financial Institutions -Remunerative xxxxxx xxxxxx-Deposits from Financial Institutions-Non-Remunerative xxxxxx xxxxxxDue to Head Office xxxxxx xxxxxxOther liabilities xxxxxx xxxxxx

(xxxxxx) (xxxxxx)NET ASSETS xxxxxx xxxxxx

REPRESENTED BYIslamic Banking Fund xxxxxx xxxxxxReserves xxxxxx xxxxxxUnappropriated/ Unremitted profit xxxxxx xxxxxx

xxxxxx xxxxxxSurplus/ (Deficit) on revaluation of assets xxxxxx xxxxxx

xxxxxx xxxxxx

Remuneration to Shariah Advisor/Board xxxxxx xxxxxx

CHARITY FUNDOpening Balance xxxxxx xxxxxx

Additions during the period xxxxxx xxxxxx

Payments/Utilization during the period (xxxxxx) (xxxxxx)

Closing Balance xxxxxx xxxxxx

ISLAMIC BANKING BUSINESS

Rupees in '000

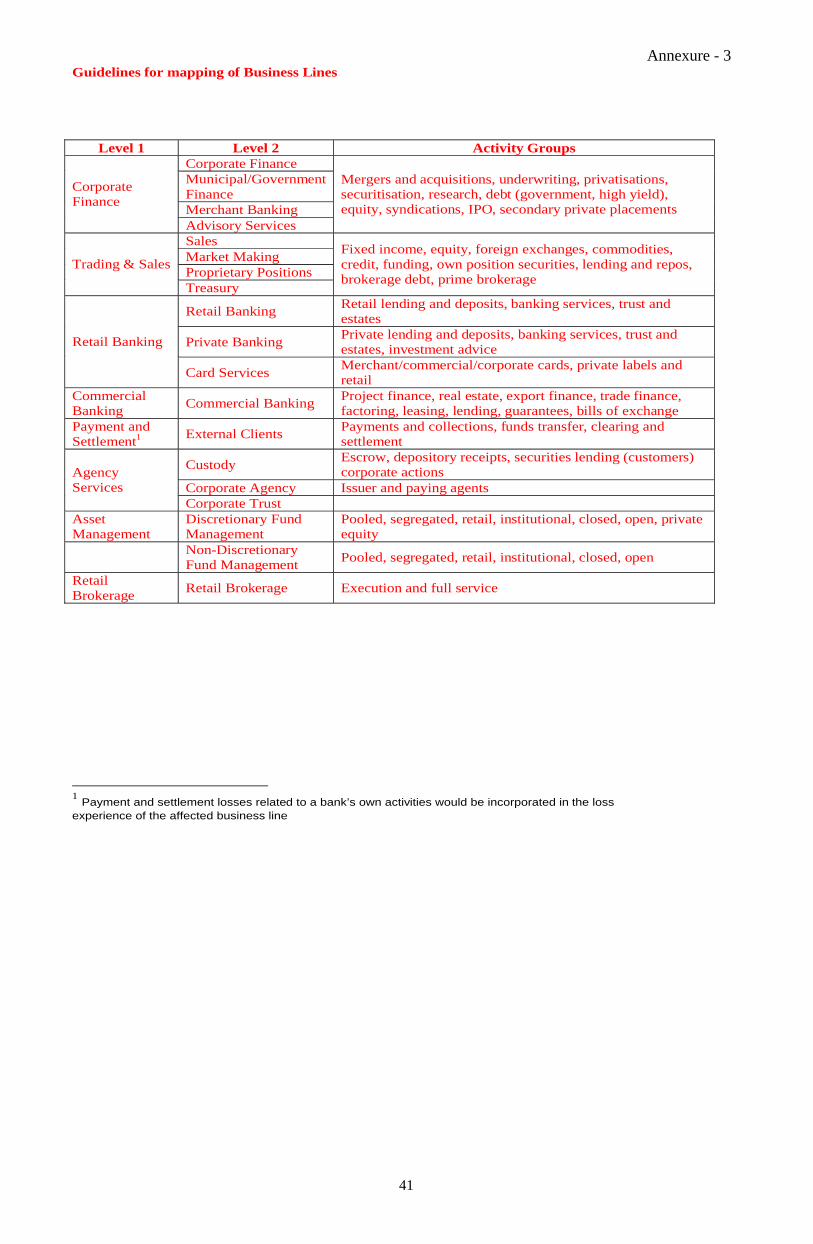

Annexure - 3Guidelines for mapping of Business Lines

Level 1 Level 2 Activity GroupsCorporate FinanceMunicipal/Government FinanceMerchant Banking

Corporate Finance

Advisory Services

Mergers and acquisitions, underwriting, privatisations, securitisation, research, debt (government, high yield), equity, syndications, IPO, secondary private placements

SalesMarket MakingProprietary Positions

Trading & Sales

Treasury

Fixed income, equity, foreign exchanges, commodities, credit, funding, own position securities, lending and repos, brokerage debt, prime brokerage

Retail BankingRetail lending and deposits, banking services, trust and estates

Private BankingPrivate lending and deposits, banking services, trust and estates, investment advice

Retail Banking

Card ServicesMerchant/commercial/corporate cards, private labels and retail

Commercial Banking

Commercial BankingProject finance, real estate, export finance, trade finance, factoring, leasing, lending, guarantees, bills of exchange

Payment and Settlement1 External Clients

Payments and collections, funds transfer, clearing and settlement

CustodyEscrow, depository receipts, securities lending (customers) corporate actions

Corporate Agency Issuer and paying agentsAgency Services

Corporate TrustAsset Management

Discretionary Fund Management

Pooled, segregated, retail, institutional, closed, open, private equity

Non-Discretionary Fund Management

Pooled, segregated, retail, institutional, closed, open

Retail Brokerage

Retail Brokerage Execution and full service

1

Payment and settlement losses related to a bank’s own activities would be incorporated in the loss experience of the affected business line

41

Principles for business line mapping1

(a) All activities must be mapped into the eight level 1 business lines in a mutually exclusive and jointly exhaustive manner.

(b) Any banking or non-banking activity which cannot be readily mapped into the business line framework, but which represents an ancillary function to an activity included in the framework, must be allocated to the business line it supports. If more than one business line is supported through the ancillary activity, an objective mapping criteria must be used.

(c) When mapping gross income, if an activity cannot be mapped into a particular business line then the business line yielding the highest charge must be used. The same business line equally applies to any associated ancillary activity.

(d) Banks may use internal pricing methods to allocate gross income between business lines provided that total gross income for the bank (as would be recorded under the Basic Indicator Approach) still equals the sum of gross income for the eight business lines.

(e) The mapping of activities into business lines for operational risk capital purposes must be consistent with the definitions of business lines used for regulatory capital calculations in other risk categories, i.e. credit and market risk. Any deviations from this principle must be clearly motivated and documented.

(f) The mapping process used must be clearly documented. In particular, written business line definitions must be clear and detailed enough to allow third parties to replicate the business line mapping. Documentation must, among other things, clearly motivate any exceptions or overrides and be kept on record.

1

Supplementary business line mapping guidanceThere are a variety of valid approaches that banks can use to map their activities to the eight business lines, provided the approach used meets the business line mapping principles. Following is an example of one possible approach that could be used by a bank to map its gross income:

Gross income for retail banking consists of net interest income on loans and advances to retail customers and SMEs treated as retail, plus fees related to traditional retail activities, net income from swaps and derivatives held to hedge the retail banking book, and income on purchased retail receivables. To calculate net interest income for retail banking, a bank takes the interest earned on its loans and advances to retail customers less the weighted average cost of funding of the loans (from whatever source - retail or other deposits).

Similarly, gross income for commercial banking consists of the net interest income on loans and advances to corporate (plus SMEs treated as corporate), interbank and sovereign customers and income on purchased corporate receivables, plus fees related to traditional commercial banking activities including commitments, guarantees, bills of exchange, net income (e.g. from coupons and dividends) on securities held in the banking book, and profits/losses on swaps and derivatives held to hedge the commercial banking book. Again, the calculation of net interest income is based on interest earned on loans and advances to corporate, interbank and sovereign customers less the weighted average cost of funding for these loans (from whatever source).

For trading and sales, gross income consists of profits/losses on instruments held for trading purposes (i.e. in the mark-to-market book), net of funding cost, plus fees from wholesale broking.

For the other five business lines, gross income consists primarily of the net fees/commissions earned in each of these businesses. Payment and settlement consists of fees to cover provision of payment/settlement facilities for wholesale counterparties. Asset management is management of assets on behalf of others.

42

(g) Processes must be in place to define the mapping of any new activities or products replicate the business line mapping. Documentation must, among other things, clearly motivate any exceptions or overrides and be kept on record.

(h) Processes must be in place to define the mapping of any new activities or products.

(i) Senior management is responsible for the mapping policy (which is subject to the approval by the board of directors).

(j) The mapping process to business lines must be subject to independent review.

43