the relationship between esg & socially responsible...

TRANSCRIPT

THE RELATIONSHIP BETWEEN ESG & SOCIALLY RESPONSIBLE

INVESTING AND ALPHA GENERATION IN THE LONG-RUN

by

YuXuan (David) Jiang

BMgt in Business Economics, University of Alberta, 2016

and

ChenTao (Tony) Zhu

BA in Economics, Simon Fraser University (SFU), 2018

PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF

THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF SCIENCE IN FINANCE

In the Master of Science in Finance Program

of the

Faculty

of

Business Administration

© YuXuan Jiang and ChenTao Zhu 2019

SIMON FRASER UNIVERSITY

Fall 2019

All rights reserved. However, in accordance with the Copyright Act of Canada, this work

may be reproduced, without authorization, under the conditions for Fair Dealing.

Therefore, limited reproduction of this work for the purposes of private study, research,

criticism, review and news reporting is likely to be in accordance with the law,

particularly if cited appropriately.

1

Approval

Name: YuXuan (David) Jiang, ChenTao (Tony) Zhu

Degree: Master of Science in Finance

Title of Project: THE RELATIONSHIP BETWEEN ESG &

SOCIALLY RESPONSIBLE INVESTING AND

ALPHA GENERATION IN THE LONG-RUN

Supervisory Committee:

___________________________________________

Title and Name Senior Supervisor

Correct Title – (i.e. Associate Professor)

___________________________________________

Title and Name

Second Reader

Correct Title

Date Approved: ___________________________________________

Note (Don’t forget to delete this note before printing): The Approval page must be only one page

long. This is because it MUST be page “ii”, while the Abstract page MUST begin on page “iii”. Finally,

don’t delete this page from your electronic document, if your department’s grad assistant is producing

the “real” approval page for signature. You need to keep the page in your document, so that the

“Approval” heading continues to appear in the Table of Contents.

2

Abstract

The number of ethical investments have increased dramatically over the past few

years due to the rising demands from investors. But do these investments really generate

alpha over the long run? This paper seeks to examine the relationship between long-term

alpha and investment vehicles with either an ESG or an SRI mandate. The analysis is

broken down by both geography and by different time periods. In terms of geography,

investments with either an ESG or SRI mandate are separately analyzed for both U.S. and

Canada; and in terms of times periods, this paper examines historical monthly returns from

both a longer time frame (12/31/2009 – 12/31/2018) and a medium time frame (12/31/2014

– 12/31/2018). The returns of the different investments are then benchmarked against the

overall market index from the country where these investments are located. The alpha of

these investments is calculated by using both the Capital Asset Pricing Model (CAPM) and

a modified Carhart Multifactor Model.

Our analysis indicates that there is no relationship between alpha and the socially

responsible or ESG funds. The majority of time, these funds actually underperform the

market. We present our findings that the ethical investments are less superior to a passive

market index in this paper.

Keywords: Mutual Funds; Socially Responsible Investing (SRI); Environmental, Social

& Governance (ESG); Alpha

3

Acknowledgements

First and foremost, we would like to express our sincere gratitude towards our

supervisor Dr. Christina Atanasova for her generous support and encouragement

throughout our research process. Her patience and insightful comments are greatly

appreciated. It has been an amazing and rewarding experience working with Dr. Christina

Atanasova.

Secondly, we would also like to thank Dr. Victor Song for providing us the

additional valuable advice and assistance in our research and writing process.

Finally, we would like to thank our families, friends and fellow classmates for their

encouragement and help during our research.

4

Table of Contents

Approval ..................................................................................................................................... 1

Abstract ...................................................................................................................................... 2

Acknowledgements ..................................................................................................................... 3

Table of Contents ........................................................................................................................ 4

Glossary ..................................................................................................................................... 5

1: Introduction .......................................................................................................................... 6

2: Literature Review ................................................................................................................. 9

3: Data and Methodology ........................................................................................................ 11

3.1 Data Selection Process...................................................................................................... 11

3.2 Data Analysis Process ...................................................................................................... 12

4: Empirical Findings .............................................................................................................. 15

4.1 Analysis of Indices ........................................................................................................... 15

4.2 Canadian SRI Mutual Funds and Alpha ............................................................................ 16

4.3 U.S. SRI Mutual Funds and Alpha .................................................................................... 17

4.4 Canadian ESG Mutual Funds and Alpha ........................................................................... 17

4.5 U.S. ESG Mutual Funds and Alpha................................................................................... 18

5: Conclusion ........................................................................................................................... 19

Appendix ................................................................................................................................. 21

Bibliography ............................................................................................................................ 49

5

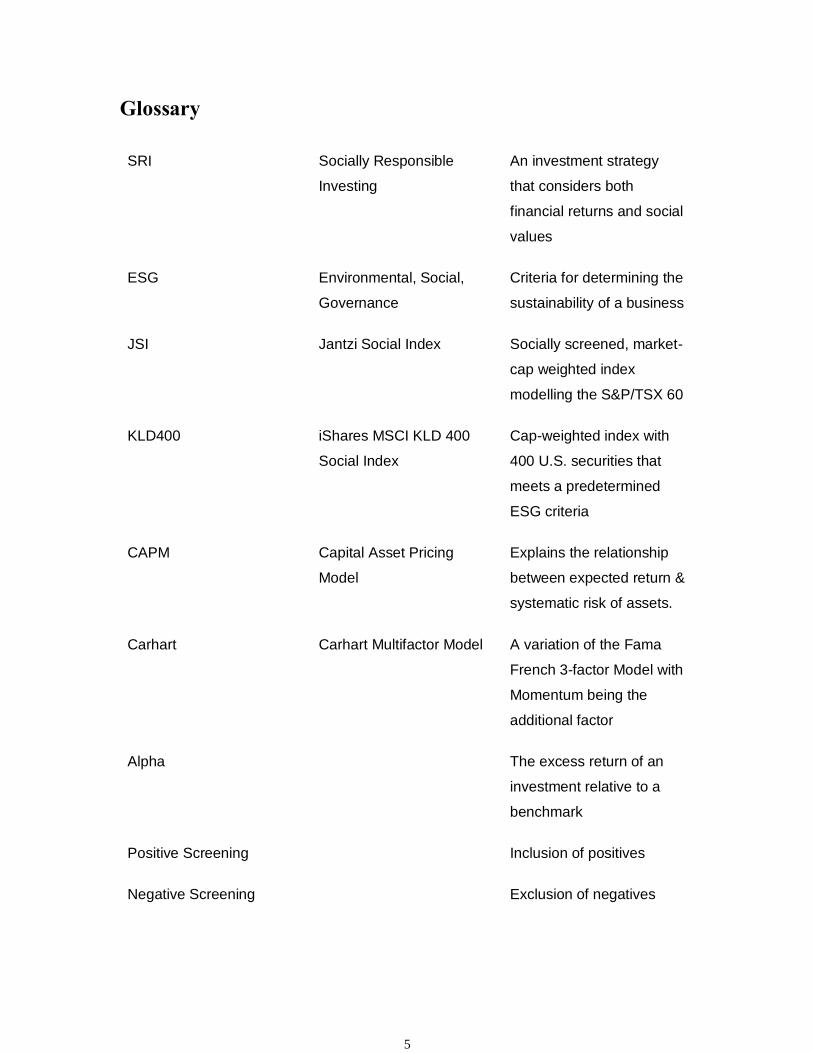

Glossary

SRI Socially Responsible

Investing

An investment strategy

that considers both

financial returns and social

values

ESG Environmental, Social,

Governance

Criteria for determining the

sustainability of a business

JSI Jantzi Social Index Socially screened, market-

cap weighted index

modelling the S&P/TSX 60

KLD400 iShares MSCI KLD 400

Social Index

Cap-weighted index with

400 U.S. securities that

meets a predetermined

ESG criteria

CAPM Capital Asset Pricing

Model

Explains the relationship

between expected return &

systematic risk of assets.

Carhart Carhart Multifactor Model A variation of the Fama

French 3-factor Model with

Momentum being the

additional factor

Alpha The excess return of an

investment relative to a

benchmark

Positive Screening Inclusion of positives

Negative Screening Exclusion of negatives

6

1: Introduction

Socially responsible investing (SRI), also known as ethical and sustainable

investing, refers to an active investment strategy seeks to combine financial results with

social values. Although still small, ethical investing has been a fast-growing segment in

the international finance market. Over the last 19 years, the total number of ethical mutual

funds is nearly doubled, especially for France, which has grown from 14 in 2000 to 232 in

2019, becoming the second most popular ethical investment countries next to United

States.

COMPARING THE ETHICAL MUTUAL FUND MARKETS

# OF ETHICAL MUTUAL FUNDS # OF SRI FUNDS

COUNTRY 2000 2019 2019 BELGIUM 26 46 26 FRANCE 14 232 122 GERMANY 22 72 28 ITALY 5 18 10 SWEDEN 42 75 59 SWITZERLAND 22 82 48 THE NETHERLANDS 11 45 13 UNITED KINGDOM 55 105 63 UNITED STATES 230 260 71

Overview of the ethical mutual fund market in 2019

Country # of Ethical Mutual Funds

# of SRI Mutual Funds

SRI as a % of Total Ethical Mutual Funds

Belgium 46 26 57%

France 232 122 53%

Germany 72 28 39%

Italy 18 10 56%

Sweden 75 59 79%

Switzerland 82 48 59%

The Netherlands 45 13 29%

United Kingdom 105 63 60%

United States 260 71 27%

7

It should be noted that SRI is not interchangeable with ESG investing, although the

latter is also plays an important role in finance. The idea of environmental, social and

governance (ESG) in asset management did not gain much attention until 2005, when the

United Nations hosted the “Who Cares Wins” Conference. While SRI Funds apply

exclusionary screenings to the securities based on specific ethical guidelines, ESG takes a

more positive approach in considering the opportunities and risks associated with

environmental, social and governance factors, and the potential economic values behind it.

This paper will evaluate the performance of the United States MSCI KLD 400

Social index with the benchmark S&P 500 Index, and the Canadian Jantzi Social Index

with the benchmark SPTSX Index. By imposing SRI and ESG screens on investments, this

paper creates 8 portfolios, which are Canadian 4/9 years SRI funds, United States 4/9 years

SRI funds, Canadian 4/9 years ESG funds, and United states 4/9 years ESG funds. All of

the 8 funds are equally weighted and screened using the Bloomberg Terminal. The results

are analyzed using both the single factor CAPM model for Jensen’s Alpha and Carhart’s

(1997) 4 factor model with the first three Fama-French factors and an extra factor to capture

momentum. The complex model can explain more in the fund returns, especially the style

of the fund in a particular period.

The aim of this study is the comparison of the main risk-return characteristics in

the long run of ethical investing by imposing different methods of screenings. The public

are consistently debating whether or not involving in positive screening in selecting stock

can adversely affect the return. There are two screen method, positive screen and negative

screen. Negative screen is excluding the non-ethical factors, and positive screen only

contains positive ethical factors in the fund. This paper is using positive screening method,

8

selecting two types of screening criteria, which is the SRI and ESG, thus the positive screen

can be measured directly and compared with different geography locations.

By examining both the Capital Asset Pricing Model (CAPM) as well as the Carhart

4-Factor (CFF) Model, we found that there is no significant relationship between alpha and

ESG or SRI funds, regardless of their country of domicile and the time periods. However,

style alpha did appear to be significant for both the JSI and KLD 400 indexes. For the JSI,

alpha is small and negative; and for KLD 400, alpha is large but still negative at -2.58%.

We also examine the Sharpe ratio of each of the mutual fund portfolios compared to the

benchmark. The Sharpe ratio for the 9-year S&P 500 is 0.84, where the 4-year is 0.54. For

Canada, the 9-year S&P/TSX has a Sharpe ratio of 0.39, and the 4-year has a Sharpe ratio

of 0.17. For our mutual fund portfolios, the 9-year U.S. ESG portfolio has a Sharpe ratio

of 0.66, and the 4-year portfolio has a Sharpe ratio of 0.48. For the U.S. SRI portfolios, the

9-year portfolio has a Sharpe ratio of 0.76, and the 4-year portfolio has a Sharpe ratio of

0.61, which actually outperformed the benchmark by 7 basis points. In the Canadian

context, the 9-year ESG portfolio has a Sharpe ratio of 0.50, which outperformed the

benchmark by 11 basis points, and the 4-year portfolio has a Sharpe ratio of 0.41, which

significantly outperformed the market by 24 basis points. The SRI portfolio also

outperformed the market when measured by the Sharpe ratio. The 9-year portfolio has a

Sharpe ratio of 0.61, which is 23 basis points higher than that of the market; and the 4-year

portfolio has a Sharpe ratio of 0.31, which is also higher than the benchmark by 14 basis

points.

9

2: Literature Review

Hamilton et al. (1993) suggests three hypotheses on the comparing risk-adjusted

return of SRI fund to the conventional fund. The first is that SRI does not add value or

destroy value since it’s not possible to correctly price corporate social responsibility.

Which is the closest to the traditional financial market framework, where factors are not

proxies for risks will not affect the return.

The second hypothesis is the social responsible fund underperform the conventional

fund, this implies contradiction to the first hypothesis as the market does price the risk for

SRI, the theory of SRI cost is also advanced to explain the underperformance of SRI, the

cost can be divided into two categories, the selection cost to select which stocks belongs to

the SRI fund, and the active management cost, and according to Markowitz’s (1952)

portfolio theory, the selection constraint will not lead to optimal maximization, thus the

SRI will underperform compare with conventional investment due to lack of diversification

benefit, Minor’s (2007) study on financial cost of SRI has mentioned other fundamental

economic principles such as the Supply and Demand theory related to underperformance

of SRI, which implies that the demand of unethical stock will be higher than the ethical

stock, thus increase the return, So the SRI fund that reject the unethical stock suffers lower

performance relative to the benchmark. Minor’s (2007) study has another view of

externalities to explain the lower return, the negative externality on the unethical stock will

only affect the SR investor but not to the conventional investor, thus the SR investor is

going to have a lower return.

The third hypothesis is the expected return of SRI will be higher than the

conventional portfolio, Hamilton mentioned investors tends to underestimate the impact of

10

negative information on non-SR companies. This is also explained by Bauer et al.

(2005,2006) the ‘learning effect’ of SRI, that the SRI will underperform in the short-term,

and closing the gap in the mid-term, then outperform the conventional portfolio in the long

run.

Several studies have given empirical evidence on all three alternative hypotheses

by evaluating the performance on the expected return of SRI, Blanchett (2010) and Bauer

et al. (2007) has found evidence supporting on the first hypothesis that using both single

factor model and Carhart multi factor model include momentum factor has no significant

performance difference between SRI and conventional mutual fund. While Brzeszczynski

(2014) exams the SRI fund returns and British FTSE100 index return and found

significance outperform in all his three comparisons. And yet Bauer et al. (2005) found

negative performance in Germany and US SRI fund. However, such studies are based on

different methodology, dates, filters and geography locations. These factors may explain

the contradicting results, so further studies will need to conduct to justify whether or not

SRI will provide extra value to the traditional investing.

Previous literatures have also improved in performance valuation. Hamilton et al.

(1993) and Statman (2000) is using Jensen’s Alpha, Sharp ratio and Treynor ratio to

compare the risk-adjusted performance between SRI mutual fund to both U.S. S&P 500

index and KLD 400 Social Index. And Bauer et al. (2005) build upon on the Carhart (1997)

four-factor model on performance valuation, which represents the current standard

methodology on mutual fund performance. The first three factors are from Fama-French

(1993) three factor model, and the fourth factor captures momentum effect. More complex

finance performance model can be benefited to understand SR return effectively.

11

3: Data and Methodology

Based on prior literatures, we have decided to separately analyze the long-term

alpha generating abilities of funds with an ESG mandate and also funds with an SRI

mandate. We break down our analysis by countries, where we first compare two country-

specific SRI indices with their respective market benchmarks; we then separately pool

together all SRI and ESG mutual funds of each country, and examine the significance of

their long-term alpha individually.

3.1 Data Selection Process

The data used for analysis in this paper is based on two sources: the Data Library

of Kenneth R. French and Bloomberg. The frequency of the data used is monthly, this is

done to match the previously literatures studied. The datasets for chosen for both a long-

and a medium period of time, so that not only the entire economic cycles are included, but

any changes in the near-term market sentiments are also captured.

The types of investments considered include an index fund, an ETF, and mutual

funds. The index fund used is the Jantzi Social Index (JSI), which models the S&P/TSX

60 and consists of 50 Canadian companies that passes a set ESG criteria. The ETF used is

the MSCI KLD 400 Social Index, which uses both positive and negative screenings to

include U.S. companies with high MSCI ESG ratings and excludes companies with

negative ESG impacts, regardless of the sizes of their market capitalization. For the mutual

funds, we grouped all available mutual funds on Bloomberg with SRI and ESG mandates

into two funds, separated by their country of domiciles, and compared them with their

12

respective market indices. We also separated funds with an SRI mandate from funds with

an ESG mandate.

In terms of factors considered, we obtained all of our factors from the Data Library

of Kenneth R. French. For the Capital Asset Pricing Model (CAPM) and the Carhart 4-

Factor (CFF) model, the (Rm-Rf), SMB, HML, and WML are all North American Proxies,

meaning that they are applicable to use in the analysis of either U.S. or Canadian funds.

We break down our data samples by 4 categories. Geographical locations, the

investment types, the type of mandate and the time periods. For geographical locations, we

consider investments in both United States and Canada. For the type of investments, we

first examine an ESG index for each country, more specifically, the JSI of Canada and the

KLD 400 the U.S. We then select monthly returns of all mutual funds from each country

with SRI and ESG mandates. We separate the funds by their mandates. Finally, we analyze

these monthly returns in two separate time periods: a long-term and a medium-term.

The total returns of mutual funds and the market index of both countries are also

presented. This is done to examine the absolute percentage of alpha attained by these

mutual funds in any particular periods. The beginning returns for both mutual funds and

the market indices of either long- or medium-term periods will be set to zero, and the

performance over time will be analyzed.

3.2 Data Analysis Process

In this paper, two common asset pricing models are used in analysing the datasets.

In particular, the Capital Asset Pricing Model (CAPM) is used to calculate Jensen’s Alpha;

13

and the Carhart 4-Factor Model (CFF), with the addition of a momentum factor, is also

employed to determine alpha. The details of the equations are as follows:

Capital Asset Pricing Model:

Rit – Rft = αit + βit*(Rmt – Rft) + εit (1)

From (1), Jensen’s Alpha is determined as:

αit = (Rit – Rft) – βit*(Rmt – Rft) + εit (2)

Carhart 4-Factor Model:

Rit – Rft = αpt + β1*(Rm – Rf) + β2*SMBt + β3*HMLt + β4WMLt + εit (3)

Where: Ri represents the return on a portfolio of securities, Rf represents the risk-

free rate, and Rm represents the return on market. ”t” represents a given time period. β

represents the coefficient of a particular factor. In CAPM, β specifically relates to the

volatility in relation to the market.

The CFF can be seen as an expansion of the CAPM, where the CFF not only takes

into account the excess return on the market, but also incorporates 3 additional factors that

are used to evaluate the performance of an investment. More specifically, SMBt stands for

“Small minus Big”, which considers the outperformance of small-cap stocks to large-cap

stocks. HMLt, or “High minus Low”, is a value premium that recognizes the

outperformance of value stocks (characterized by their high book value) to growth stocks

(characterized by their low book value). Finally, WMLt, which stands for “Win minus

Loss”, adjusts for the tendency that both a winning and a losing stock will continue their

momentums in each respective directions.

14

The alpha for a given period, denoted by αit, is obtained by subtracting the returns

of the investment, net of the risk free return, and the returns predicted either by the market

(under CAPM), or by the factors used (under CFF). We also analyzed the total alphas

generated by the mutual funds over the market indices of their respective countries in

different periods of time.

15

4: Empirical Findings

We present our findings in the following five subsections. In the first section, we

examine the alphas of country-specific ESG Indices (JSI and KLD400) using both the

CAPM and the CFF. In the sections two to five, we analyze the alpha-generating abilities

of both SRI and ESG Mutual Funds for Canada and the U.S. using the CAPM and the CFF.

We will also compare these funds against the market indices in their respective countries

to see the changes in alpha over time.

4.1 Analysis of Indices

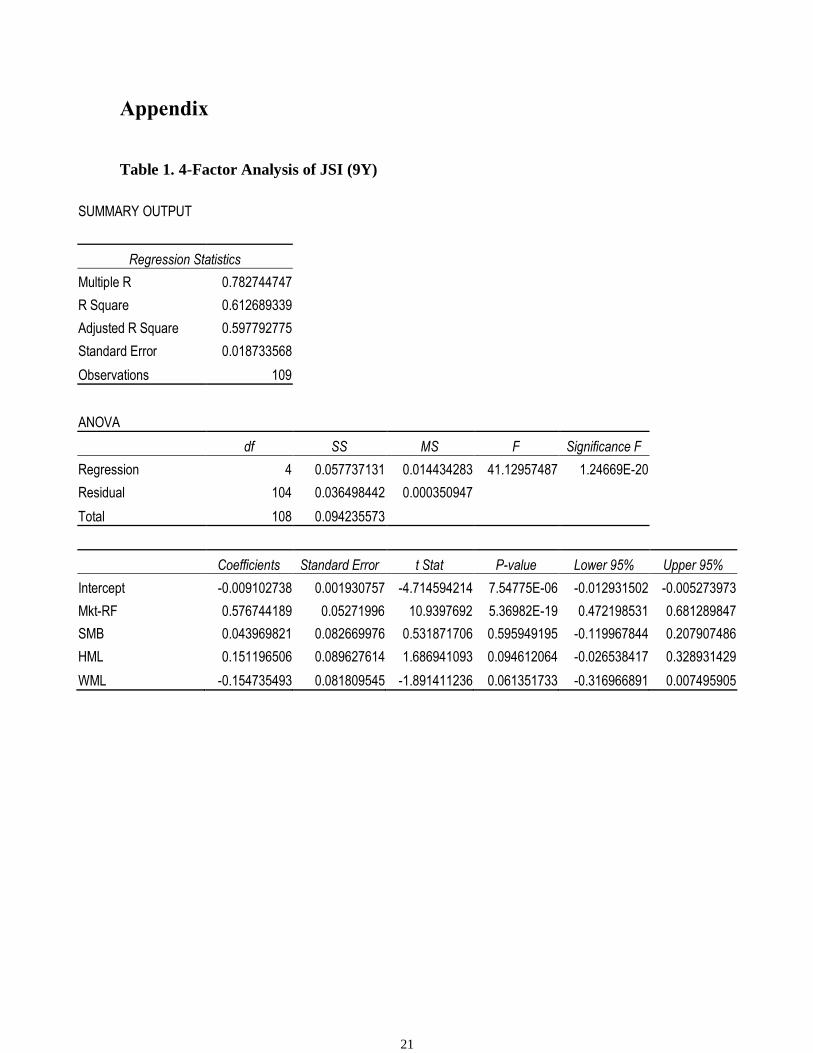

Looking at the regression results from Table 1, the relatively low adjusted R-square

indicates low explanatory power, since the CFF uses a North American proxy, with most

securities coming from the U.S., it might not fit the Canadian data as well. The negative

intercept entails a negative alpha of JSI when comparing to the SPTSX, however this alpha

is not significant. In addition, besides the factor on market returns, all other 3 Carhart

factors are not significant, showing that most of JSI’s return os explained by the market.

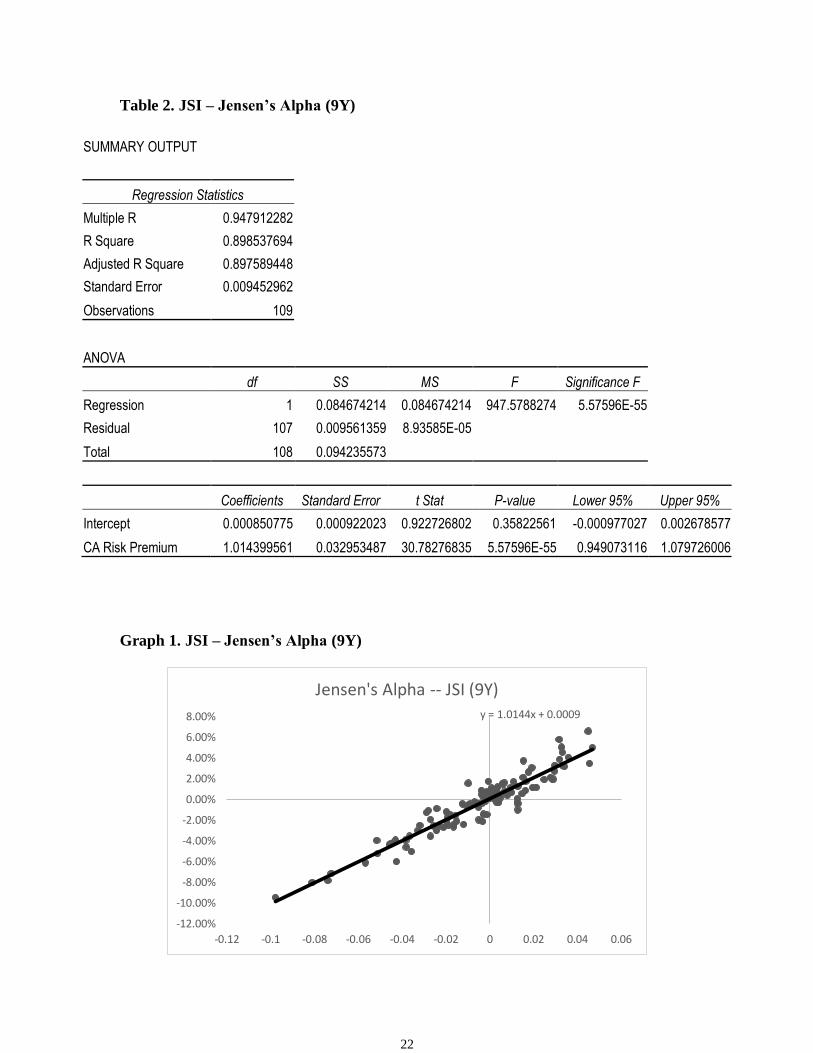

When examining the regression for Jensen’s Alpha of JSI in Table 2, the high R-

square of 0.898 indicates a significant explanatory power, the regression results indicates

that the JSI is slightly risky than the SPTSX by having beta equals to 1.014. The intercept

which represent alpha is only 0.08%, and it is again not significant.

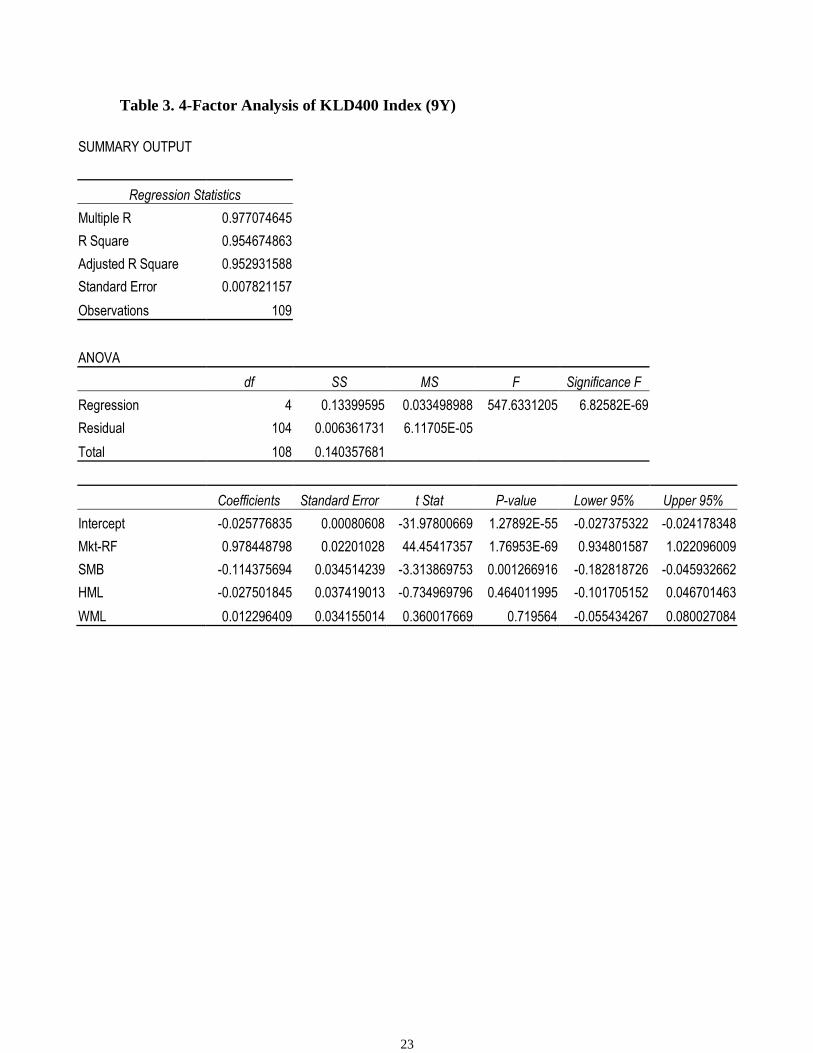

The explanatory power of CFF is superior in the KLD 400 Index, it is surprising to

find that the KLD400 has significantly underperformed the S&P 500 by 2.5%. The

significance in the negative SMB factor also indicates that the KLD400 contains more

large-cap companies.

16

The single-factor model in estimating Jensen’s Alpha for KLD 400 has superior

explanatory power than the CFF. However, the alpha is almost zero and insignificant

compares to the previous model.

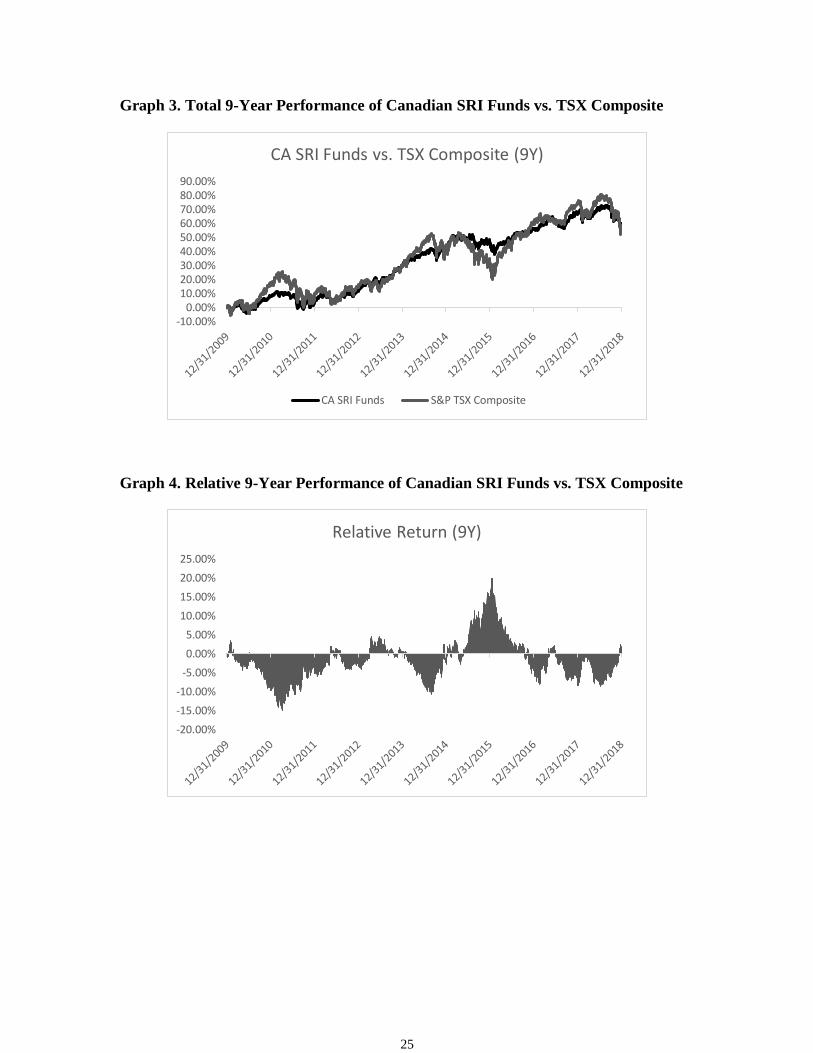

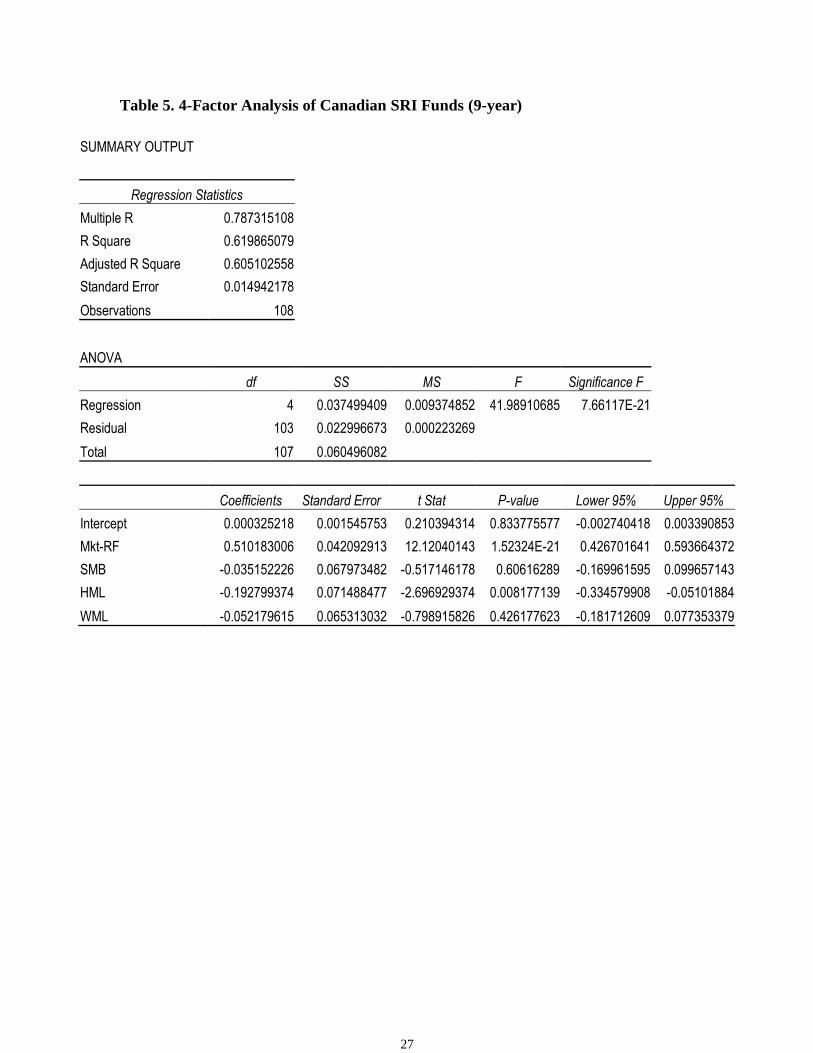

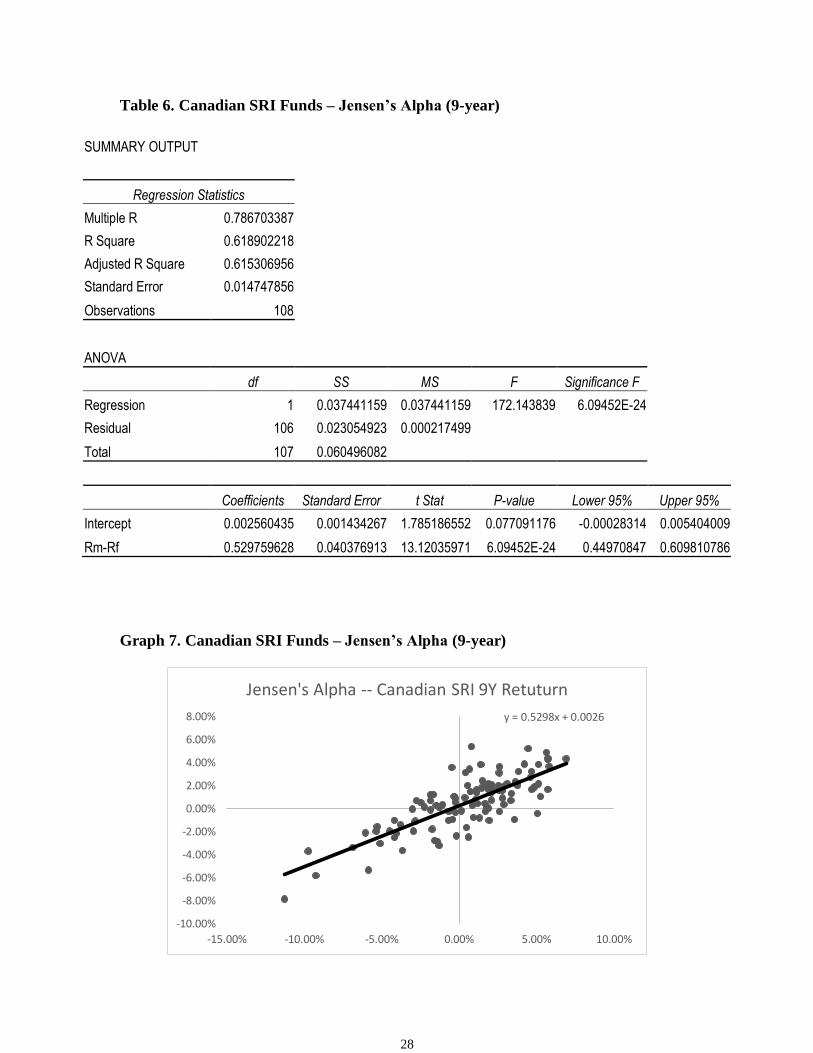

4.2 Canadian SRI Mutual Funds and Alpha

By examining Graphs 3-6 for relative returns against the SPTSX, it is shown that the

Canadian SRI funds have outperformed its benchmark in the periods from the end of 2014

to the end of 2016, which is during the Canadian oil market downturn. However, no further

conclusions can be made without the additional support of data. The adjusted R-square of

nine years Canadian SRI funds is relatively low, with only the Mkt-RF and the HML being

the significant factors, while alpha is almost zero and insignificant. It is interesting to see

the Canadian SRI Funds holds more stocks with low book values. Beta of the Canadian

SRI portfolio is only 0.51, which is much lower than that of market index, suggesting the

portfolio has a lower volatility compared to the market. The single factor model for

Jensen’s Alpha has almost the same explaining power with multifactor model, the Jensen’s

alpha is higher in single factor model but still insignificant.

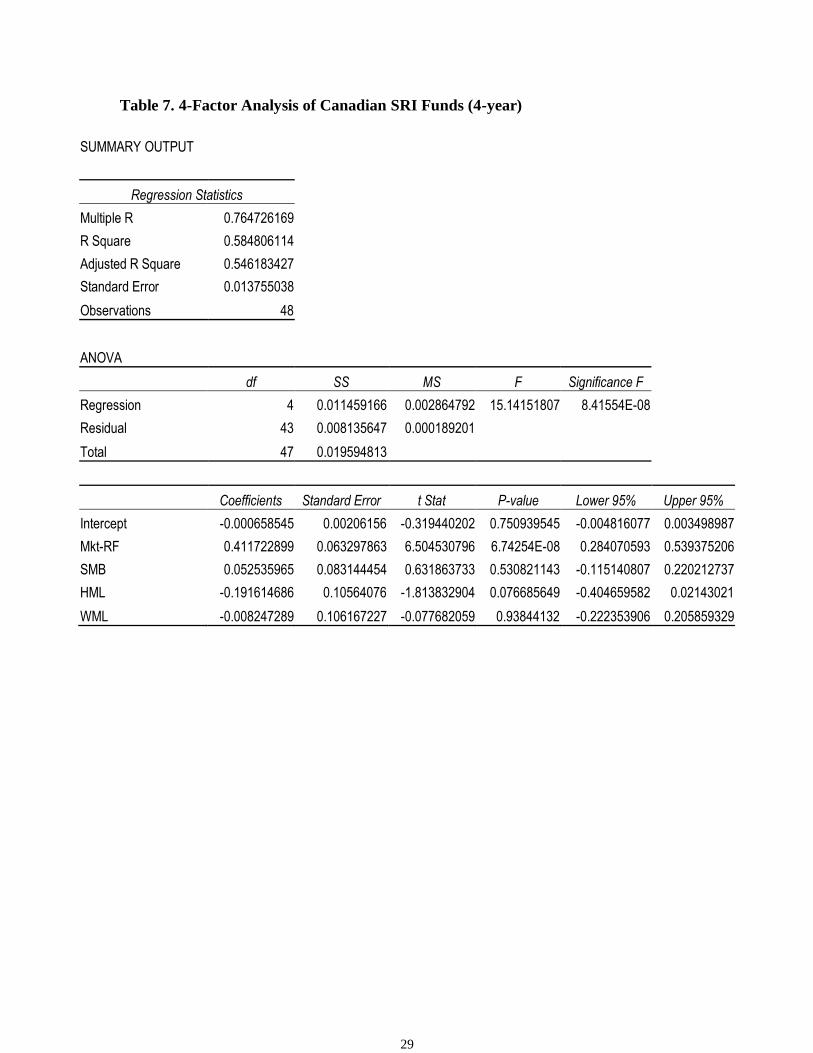

The 4-year Canadian SRI portfolio has an even lower R-square than the 9-year

Canadian SRI Portfolio, with a beta of only 0.4117, which is also lower than that of the

Canadian 9-year SRI Portfolio. And the HML factor in the 4-year analysis is insignificant

relative to the 9-year. The single factor model of 4 year Canadian SRI Portfolio also has

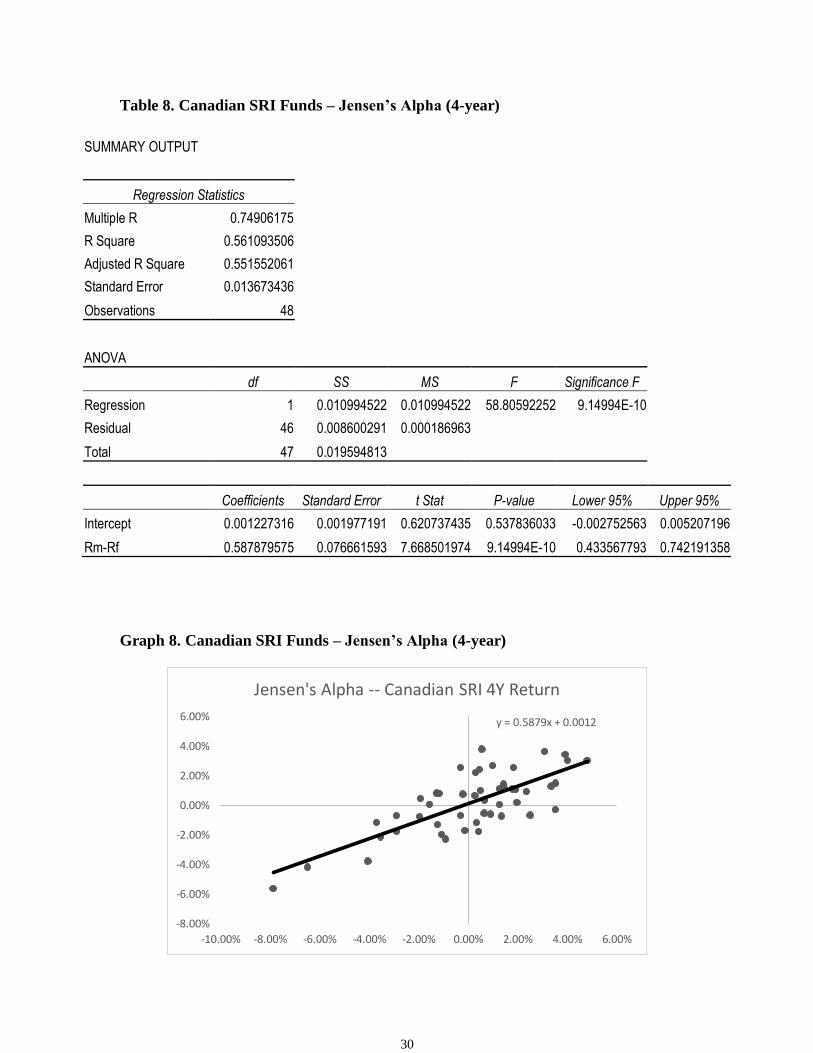

low explanatory power, with an insignificant alpha.

17

4.3 U.S. SRI Mutual Funds and Alpha

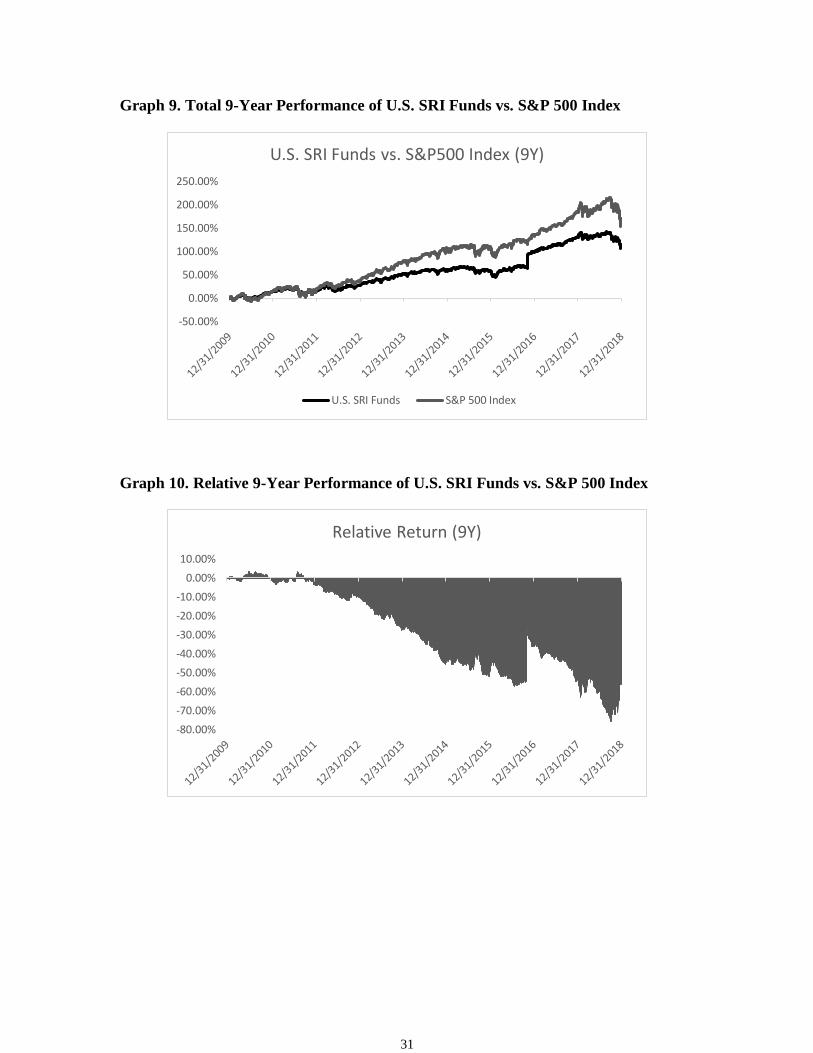

The SRI Funds of U.S. has been underperforming its benchmark since the recovery

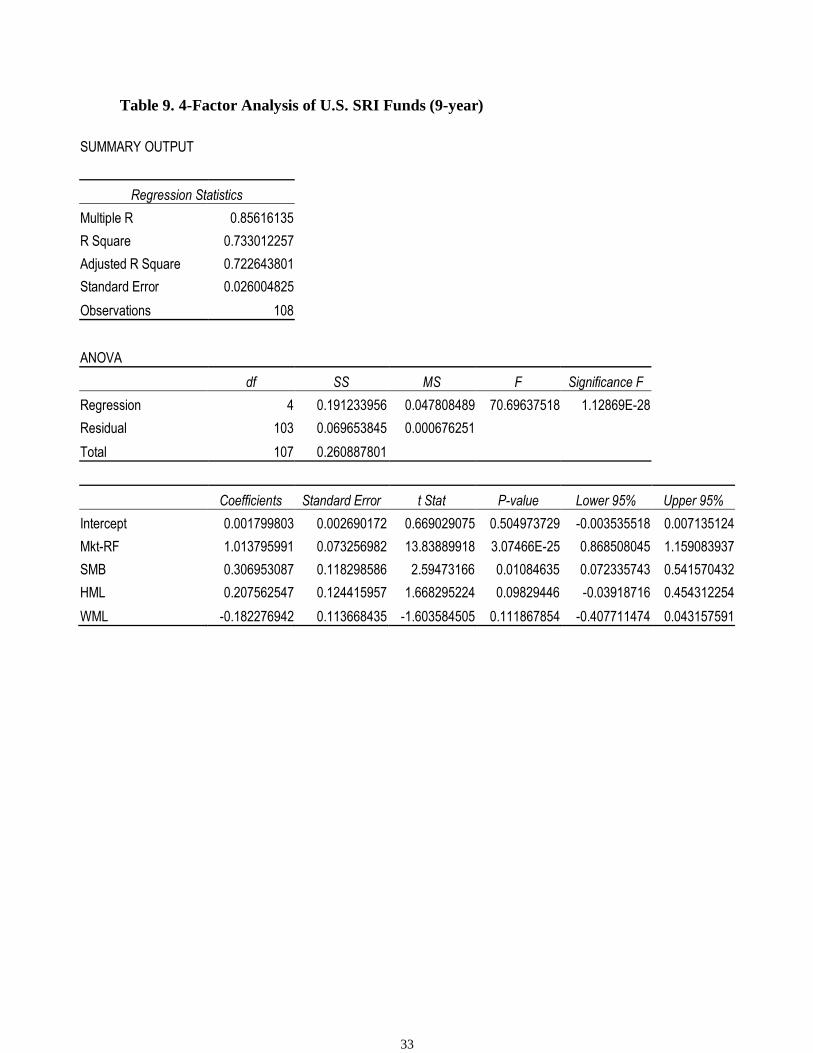

of the financial crisis. The explanatory power of the CFF for the 9-year U.S SRI Portfolio

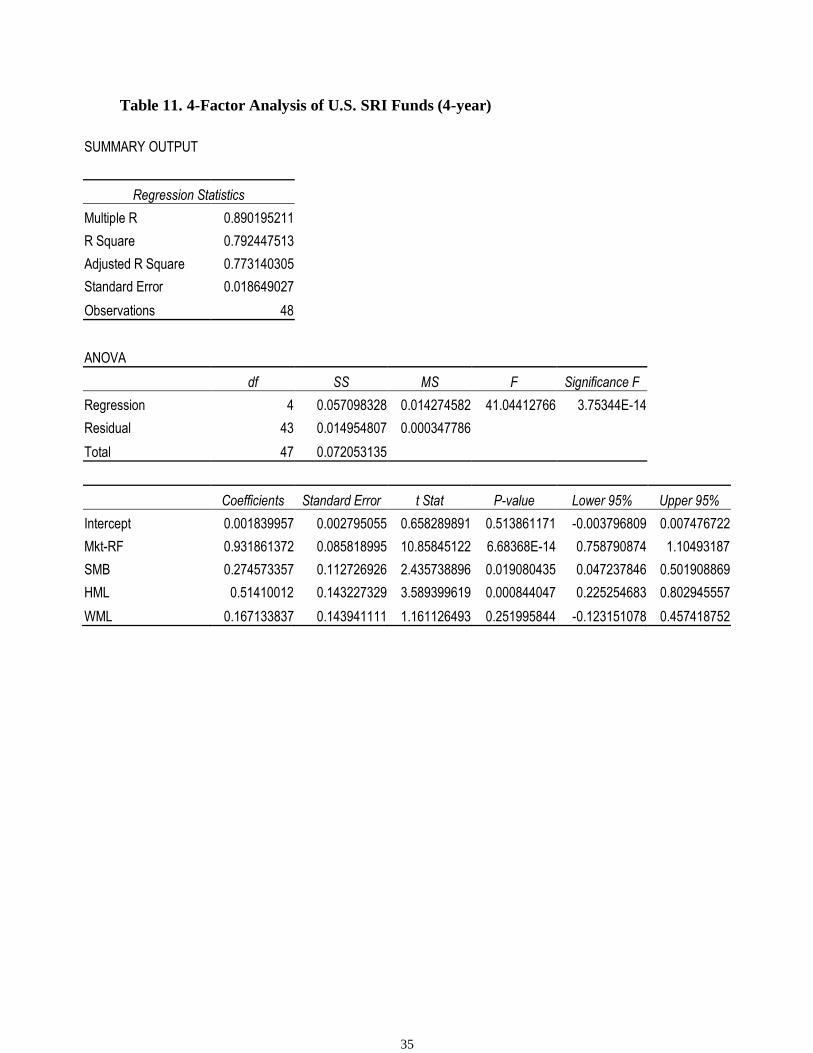

is higher than that of the CFF for the Canadian 9-year portfolio. The U.S. SRI Funds has a

0.17% alpha but still shows no significant at the 95% level. In contrast to its Canadian

counterpart, the Mkt-Rf for the U.S. Portfolio is 1.013, which is larger than the market

index, and the significant SMB factor indicates that the portfolio is holding more small-

cap stocks which have been outperforming the market. The beta in the single factor model

is lower than the CFF’s, at 0.635.

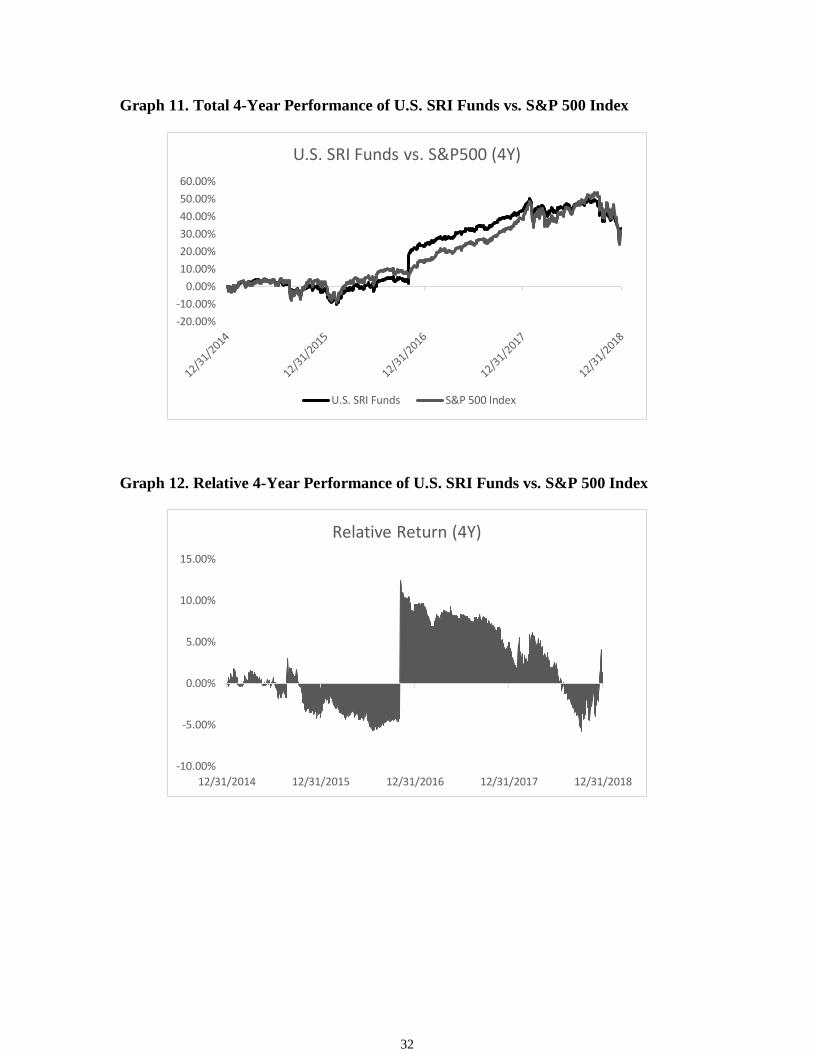

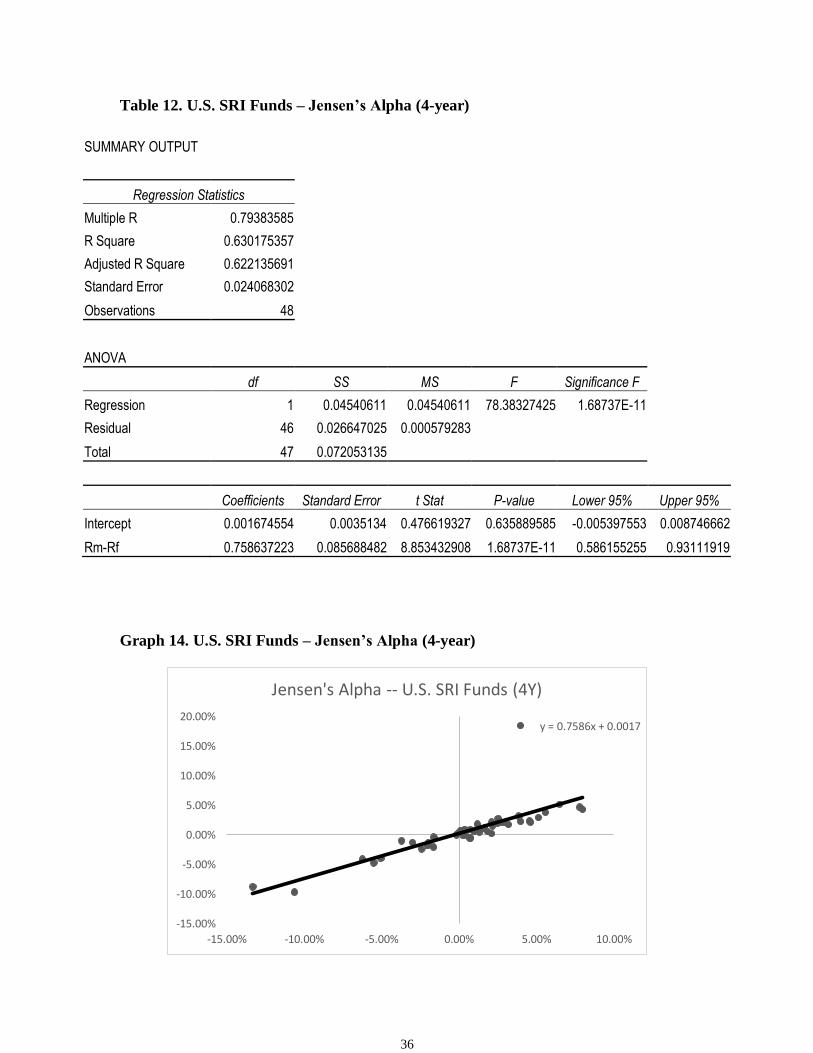

The 4-year U.S SRI Portfolio has higher R-square than the 9-year, with an

insignificant alpha. However, it has a lower beta than the 9-years Portfolio, with both SMB

and HML significant. The 4-year single factor model used to calculate Jensen’s Alpha has

a lower explanatory power than the CFF, as evident by the adjusted R-square of 0.622.

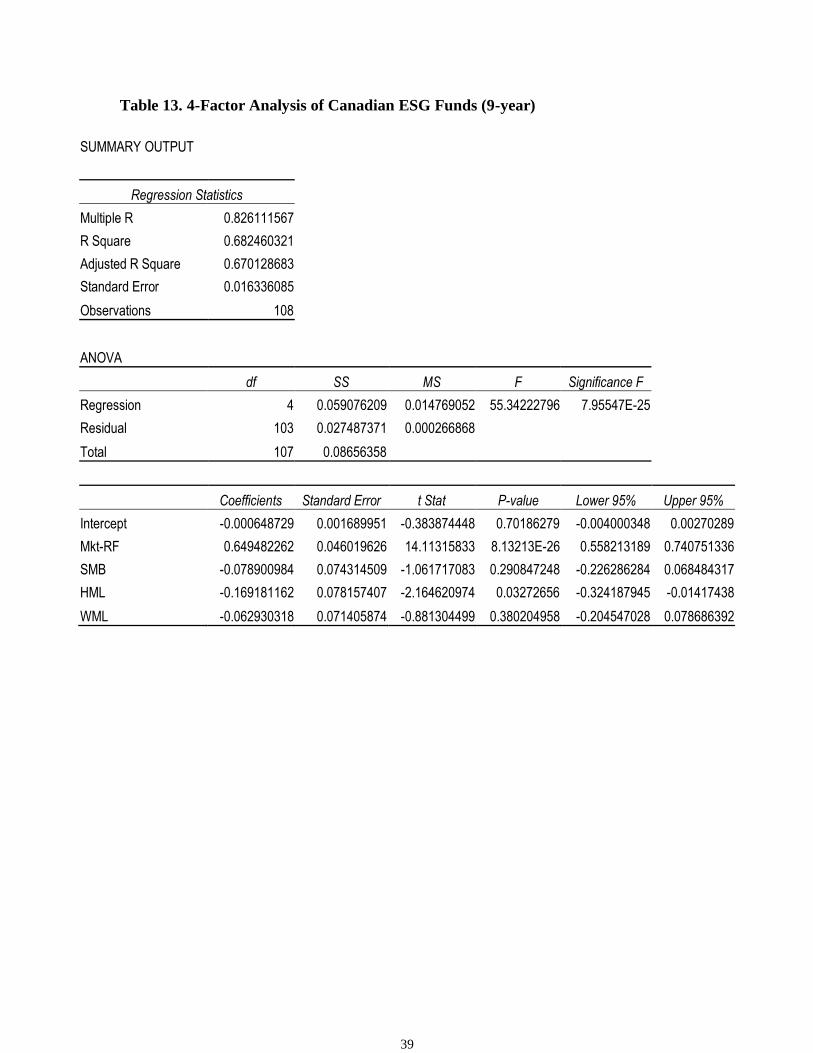

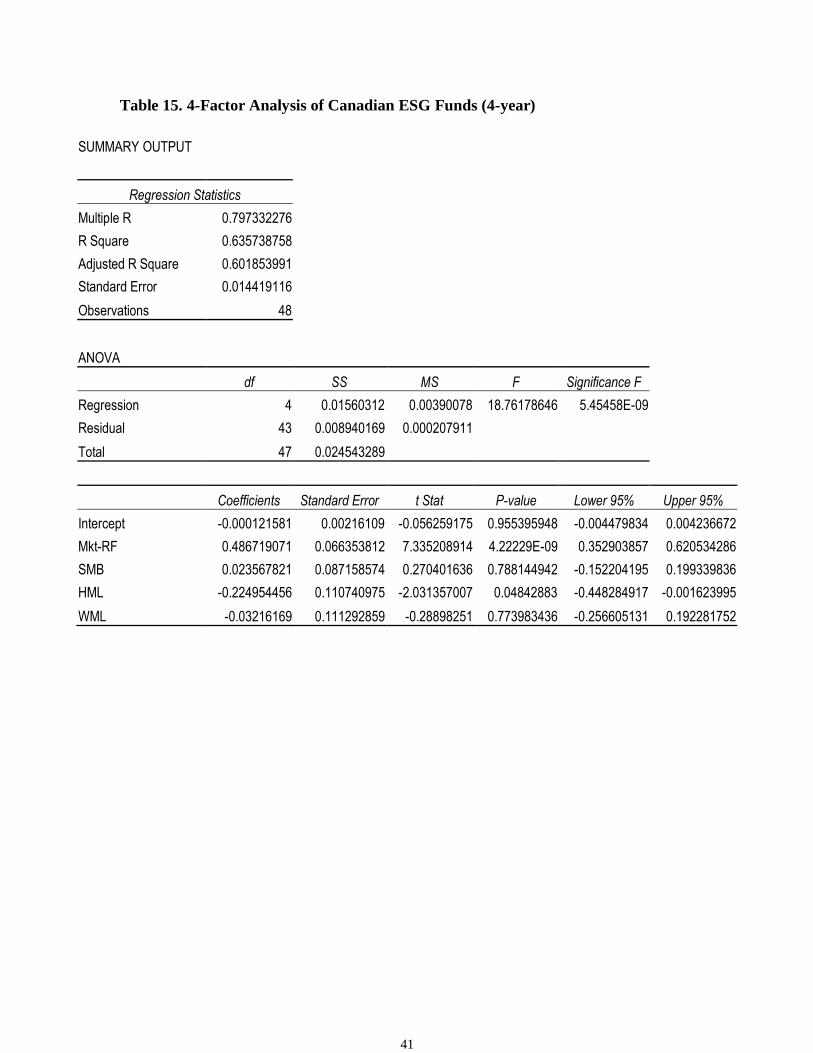

4.4 Canadian ESG Mutual Funds and Alpha

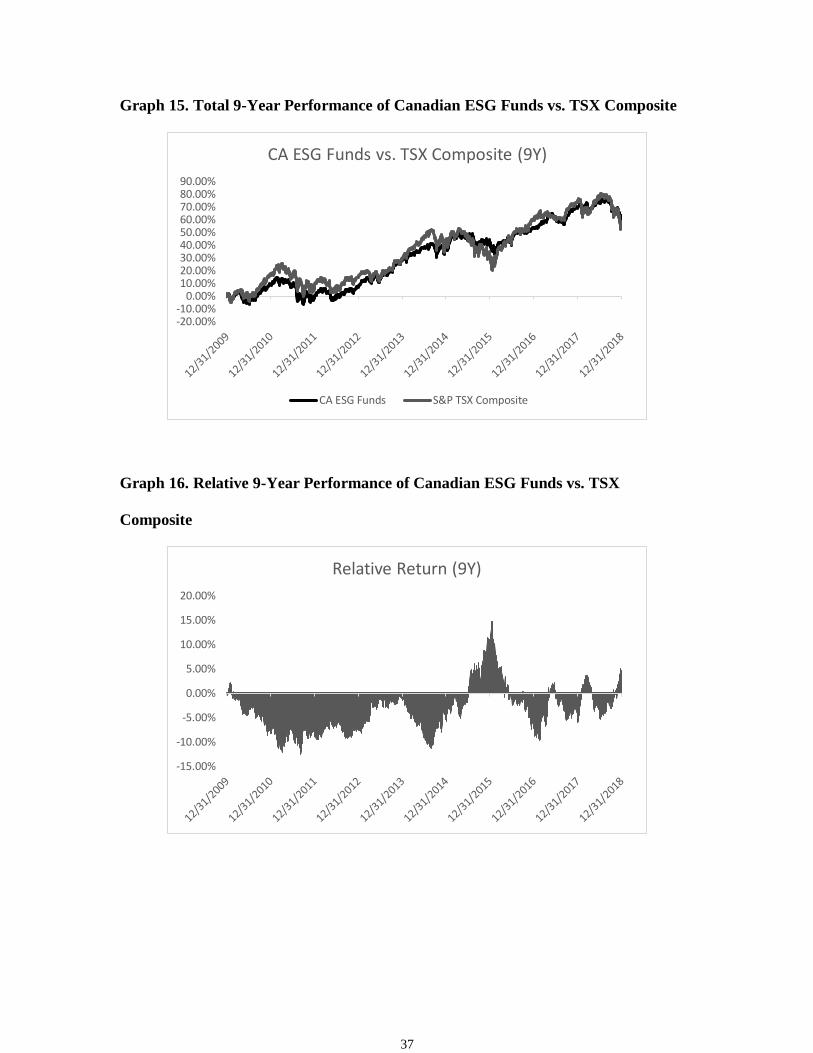

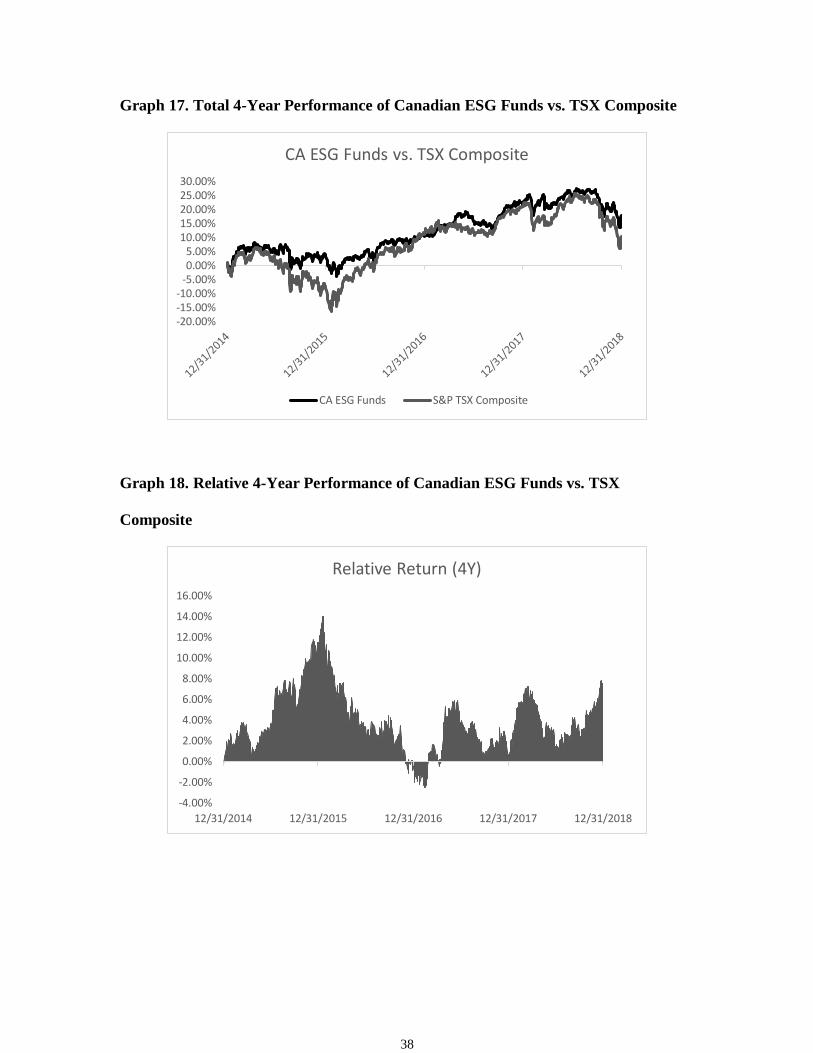

When analyzing the relative returns of the Canadian ESG funds in Graphs 18, it is

interesting to note that unlike the Canadian SRI funds, the Canadian ESG funds has actually

outperformed the SPTSX in the last 4 years. Table 15 shows that the adjusted R-square of

the CFF is lower in the 4-year Canadian ESG fund (0.602) than that of Canadian 9-year

ESG fund (0.670). The beta is also lower in the 4-year, with 0.49 compared to 0.65 in the

9-year portfolio. The HML factor is still significant with the negative coefficient suggesting

that the Canadian ESG portfolio prefers to hold low book value stock in both long- and

short-run. The single factor model for the Canadian ESG funds shows that the alpha has

little explanatory power.

18

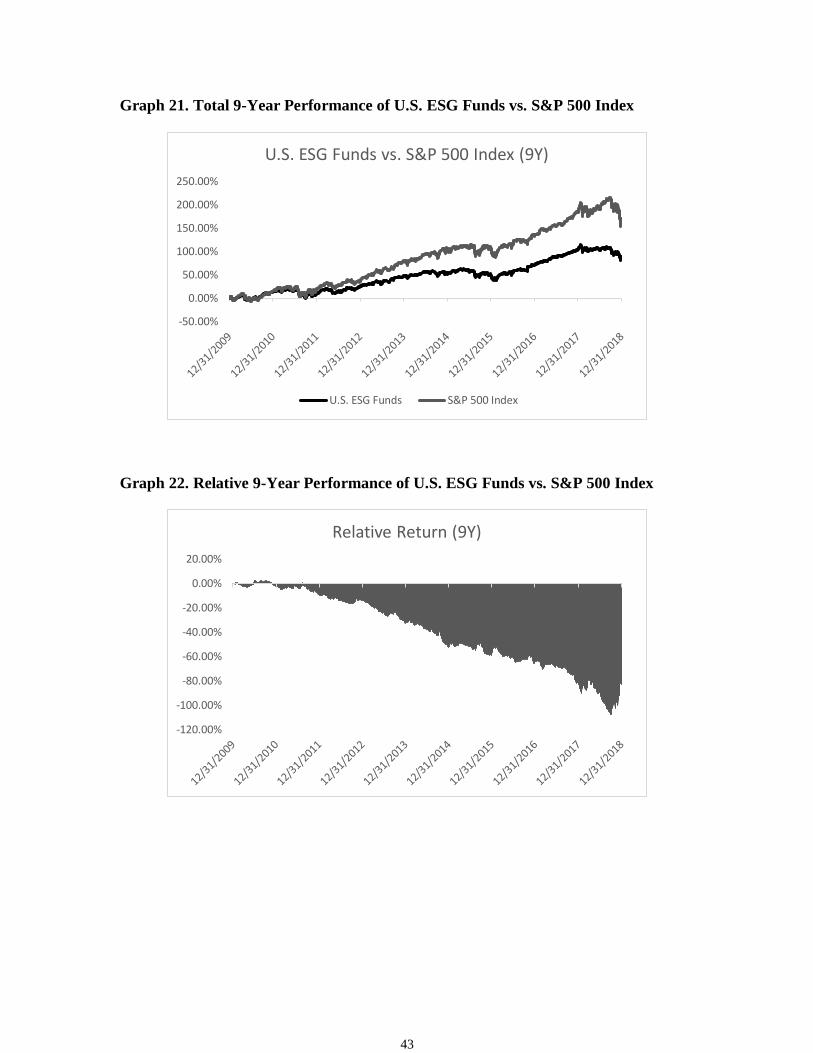

4.5 U.S. ESG Mutual Funds and Alpha

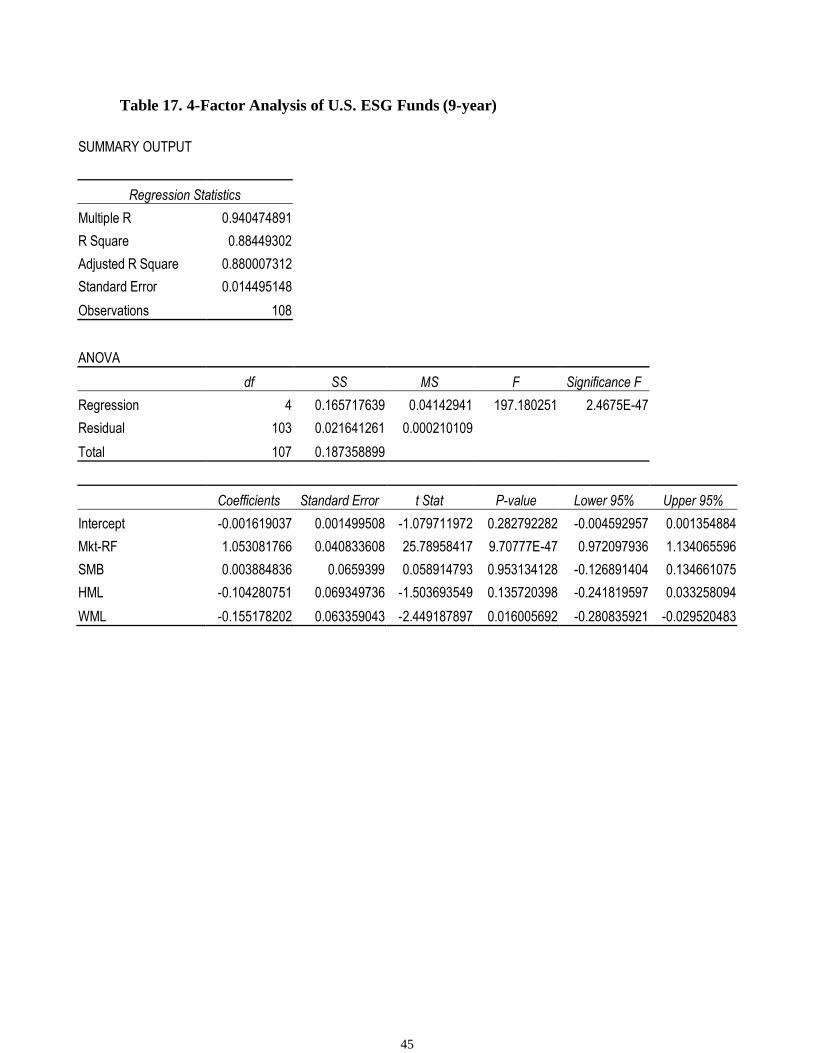

From Table 17, it is shown that the U.S ESG portfolio has an adjusted R-square of

0.88, which is higher than both the U.S SRI portfolio (0.72) and the Canadian ESG

portfolio (0.602). The beta of the 9-year U.S. ESG fund is slightly higher than the market

(1.053), with the momentum factor being negatively significant, indicating that the U.S.

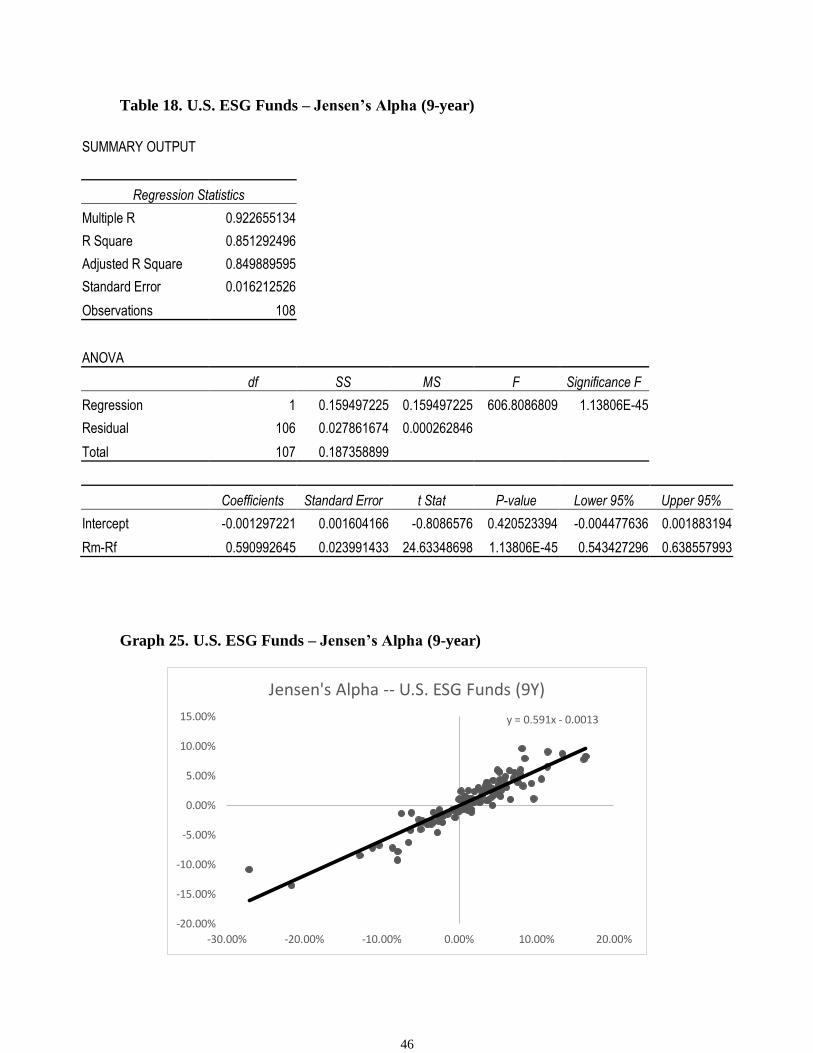

ESG fund tends to hold on to more losers in the 9-year period. In the single factor model,

the beta of the fund is relatively smaller (0.59) than the beta calculated in the multifactor

model (1.05).

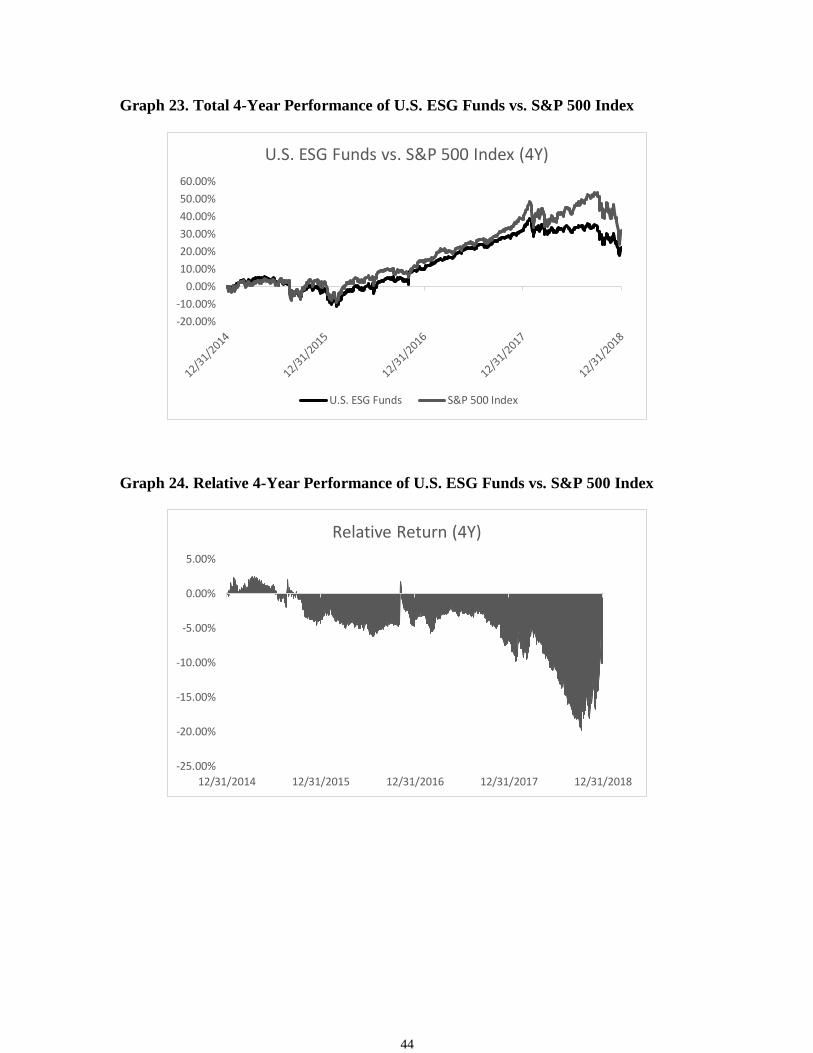

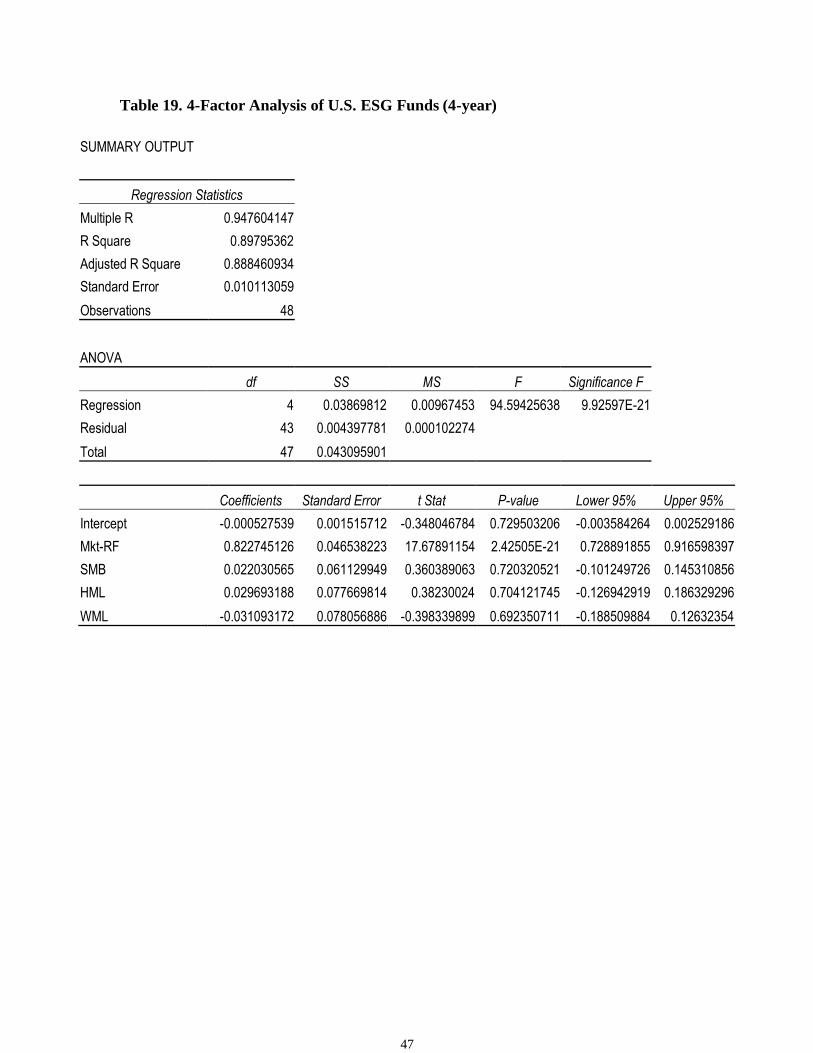

The 4-year ESG fund has almost the same adjusted R-square compared to the 9-

year U.S. ESG portfolio. The 4-year portfolio also has a lower beta (0.823) compared to

the beta (1.05) in 9-year portfolio. WML is no longer significant in the 4-year portfolio.

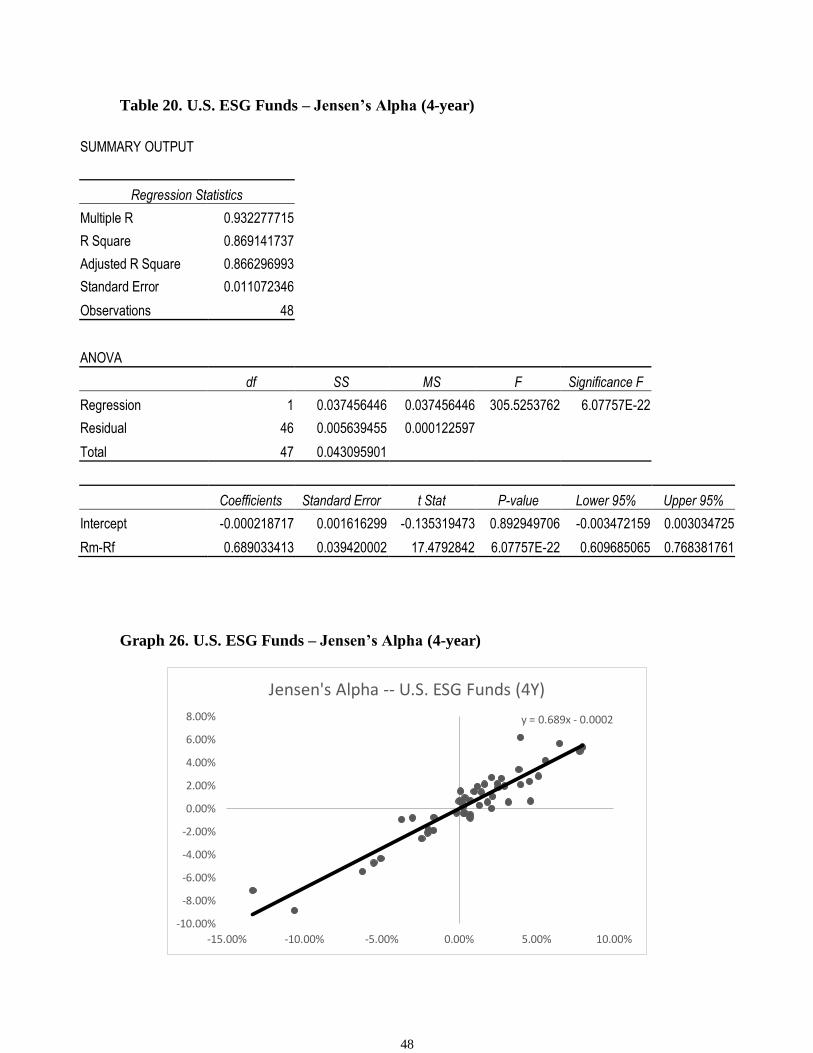

Jensen’s alpha is still not significant in the 4-year fund, as shown in Table 20.

19

5: Conclusion

Using a wide range of statistical models, we first compared the risk-adjusted

performance of Social indices of Canada and the United States with their benchmarks, we

also compare the risk-adjusted performance from different periods, with different

screenings of the Canadian and United States ethical mutual funds relative to their

conventional portfolio. While most previous work on ethical mutual fund performance has

limited its attention to single-factor benchmark models and only using Fama French 3-

factor model, we utilize the single factor CAPM model as well as the Carhart 4-factor

performance evaluation models. The multifactor specifications has greater explaining

power which not only improves performance measurement, but also conduct the ethical

mutual fund investment styles analysis in greater detail.

Firstly, our results in Single-Factor model showed no significant performance

between each ethical and conventional portfolio. However, after controlling for the style

factor in the multi-factor model, we found only the U.S. 9 years KLD 400 Social Index has

underperform the market by almost 2.57%, and it is statistically significant at 95%. In this

case, an investment in SRI equity indices does impose additional cost in terms of lower

returns for the investors. We also found the Small minus Big factor in the multifactor model

is significant, indicating the KLD 400 Social Index are holding too much small cap stocks

which significantly underperform during this market period. Unfortunately, our result in

the study does not show the ‘catch-up’ effect Bauer et al. (2005) mentioned that the SRI

indices will underperform in the short-term then catch up in the mid-term.

Secondly, another interesting empirical fact we found is that the Canadian SRI fund

consistently have lower beta than the U.S. SRI fund. The U.S. SRI fund is closer to the

20

benchmark with similar beta equaling almost 1, while the Canadian SRI fund has lower

systematic risk in both mid-term and long-term period compares to the benchmark. The

style analysis has explained the different styles between the Canadian and U.S. 9-years SRI

fund, the Canadian SRI fund invests in high book value, while the U.S. SRI fund has more

tilted towards small cap stocks. For the 4-year period, the U.S. SRI fund has both

significance in SMB and HML factor, while the mid-term Canadian SRI fund show no

particular style in its holdings.

Finally, for the other screening method, the ESG fund has neither underperformed

nor outperformed in both single- and multi-factor model. Similar to the Canadian SRI fund,

the Canadian ESG fund also has a low systematic risk with only around half the volatility

as that of the market. The styles in the Canadian ESG fund is similar to that of Canadian

SRI fund, in which both funds are holding more high book value stocks. While U.S. ESG

fund is holding more losing stocks during the 9 years horizon.

21

Appendix

Table 1. 4-Factor Analysis of JSI (9Y)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.782744747

R Square 0.612689339

Adjusted R Square 0.597792775

Standard Error 0.018733568

Observations 109

ANOVA

df SS MS F Significance F

Regression 4 0.057737131 0.014434283 41.12957487 1.24669E-20

Residual 104 0.036498442 0.000350947

Total 108 0.094235573

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.009102738 0.001930757 -4.714594214 7.54775E-06 -0.012931502 -0.005273973

Mkt-RF 0.576744189 0.05271996 10.9397692 5.36982E-19 0.472198531 0.681289847

SMB 0.043969821 0.082669976 0.531871706 0.595949195 -0.119967844 0.207907486

HML 0.151196506 0.089627614 1.686941093 0.094612064 -0.026538417 0.328931429

WML -0.154735493 0.081809545 -1.891411236 0.061351733 -0.316966891 0.007495905

22

Table 2. JSI – Jensen’s Alpha (9Y)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.947912282

R Square 0.898537694

Adjusted R Square 0.897589448

Standard Error 0.009452962

Observations 109

ANOVA

df SS MS F Significance F

Regression 1 0.084674214 0.084674214 947.5788274 5.57596E-55

Residual 107 0.009561359 8.93585E-05

Total 108 0.094235573

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.000850775 0.000922023 0.922726802 0.35822561 -0.000977027 0.002678577

CA Risk Premium 1.014399561 0.032953487 30.78276835 5.57596E-55 0.949073116 1.079726006

Graph 1. JSI – Jensen’s Alpha (9Y)

y = 1.0144x + 0.0009

-12.00%

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

-0.12 -0.1 -0.08 -0.06 -0.04 -0.02 0 0.02 0.04 0.06

Jensen's Alpha -- JSI (9Y)

23

Table 3. 4-Factor Analysis of KLD400 Index (9Y)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.977074645

R Square 0.954674863

Adjusted R Square 0.952931588

Standard Error 0.007821157

Observations 109

ANOVA

df SS MS F Significance F

Regression 4 0.13399595 0.033498988 547.6331205 6.82582E-69

Residual 104 0.006361731 6.11705E-05

Total 108 0.140357681

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.025776835 0.00080608 -31.97800669 1.27892E-55 -0.027375322 -0.024178348

Mkt-RF 0.978448798 0.02201028 44.45417357 1.76953E-69 0.934801587 1.022096009

SMB -0.114375694 0.034514239 -3.313869753 0.001266916 -0.182818726 -0.045932662

HML -0.027501845 0.037419013 -0.734969796 0.464011995 -0.101705152 0.046701463

WML 0.012296409 0.034155014 0.360017669 0.719564 -0.055434267 0.080027084

24

Table 4. KLD400 Index – Jensen’s Alpha (9Y)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.989789281

R Square 0.97968282

Adjusted R Square 0.97949294

Standard Error 0.005162474

Observations 109

ANOVA

df SS MS F Significance F

Regression 1 0.137506009 0.137506009 5159.478937 2.29774E-92

Residual 107 0.002851672 2.66511E-05

Total 108 0.140357681

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.000349171 0.000540553 -0.645952287 0.51969321 -0.001420754 0.000722411

U.S. Risk Premium 0.990806304 0.013793861 71.829513 2.29774E-92 0.963461584 1.018151025

Graph 2. KLD400 Index – Jensen’s Alpha (9Y)

y = 0.9908x - 0.0003

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

-0.15 -0.1 -0.05 0 0.05 0.1

Jensen's Alpha -- KLD400 Index (9Y)

25

Graph 3. Total 9-Year Performance of Canadian SRI Funds vs. TSX Composite

Graph 4. Relative 9-Year Performance of Canadian SRI Funds vs. TSX Composite

-10.00%0.00%

10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%90.00%

CA SRI Funds vs. TSX Composite (9Y)

CA SRI Funds S&P TSX Composite

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Relative Return (9Y)

26

Graph 5. Total 4-Year Performance of Canadian SRI Funds vs. TSX Composite

Graph 6. Relative 4-Year Performance of Canadian SRI Funds vs. TSX Composite

-20.00%-15.00%-10.00%

-5.00%0.00%5.00%

10.00%15.00%20.00%25.00%30.00%

CA SRI Funds vs. TSX Composite (4Y)

CA SRI Funds S&P TSX Composite

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

12/31/2014 12/31/2015 12/31/2016 12/31/2017 12/31/2018

Relative Return (4Y)

27

Table 5. 4-Factor Analysis of Canadian SRI Funds (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.787315108

R Square 0.619865079

Adjusted R Square 0.605102558

Standard Error 0.014942178

Observations 108

ANOVA

df SS MS F Significance F

Regression 4 0.037499409 0.009374852 41.98910685 7.66117E-21

Residual 103 0.022996673 0.000223269

Total 107 0.060496082

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.000325218 0.001545753 0.210394314 0.833775577 -0.002740418 0.003390853

Mkt-RF 0.510183006 0.042092913 12.12040143 1.52324E-21 0.426701641 0.593664372

SMB -0.035152226 0.067973482 -0.517146178 0.60616289 -0.169961595 0.099657143

HML -0.192799374 0.071488477 -2.696929374 0.008177139 -0.334579908 -0.05101884

WML -0.052179615 0.065313032 -0.798915826 0.426177623 -0.181712609 0.077353379

28

Table 6. Canadian SRI Funds – Jensen’s Alpha (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.786703387

R Square 0.618902218

Adjusted R Square 0.615306956

Standard Error 0.014747856

Observations 108

ANOVA

df SS MS F Significance F

Regression 1 0.037441159 0.037441159 172.143839 6.09452E-24

Residual 106 0.023054923 0.000217499

Total 107 0.060496082

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.002560435 0.001434267 1.785186552 0.077091176 -0.00028314 0.005404009

Rm-Rf 0.529759628 0.040376913 13.12035971 6.09452E-24 0.44970847 0.609810786

Graph 7. Canadian SRI Funds – Jensen’s Alpha (9-year)

y = 0.5298x + 0.0026

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

-15.00% -10.00% -5.00% 0.00% 5.00% 10.00%

Jensen's Alpha -- Canadian SRI 9Y Retuturn

29

Table 7. 4-Factor Analysis of Canadian SRI Funds (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.764726169

R Square 0.584806114

Adjusted R Square 0.546183427

Standard Error 0.013755038

Observations 48

ANOVA

df SS MS F Significance F

Regression 4 0.011459166 0.002864792 15.14151807 8.41554E-08

Residual 43 0.008135647 0.000189201

Total 47 0.019594813

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.000658545 0.00206156 -0.319440202 0.750939545 -0.004816077 0.003498987

Mkt-RF 0.411722899 0.063297863 6.504530796 6.74254E-08 0.284070593 0.539375206

SMB 0.052535965 0.083144454 0.631863733 0.530821143 -0.115140807 0.220212737

HML -0.191614686 0.10564076 -1.813832904 0.076685649 -0.404659582 0.02143021

WML -0.008247289 0.106167227 -0.077682059 0.93844132 -0.222353906 0.205859329

30

Table 8. Canadian SRI Funds – Jensen’s Alpha (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.74906175

R Square 0.561093506

Adjusted R Square 0.551552061

Standard Error 0.013673436

Observations 48

ANOVA

df SS MS F Significance F

Regression 1 0.010994522 0.010994522 58.80592252 9.14994E-10

Residual 46 0.008600291 0.000186963

Total 47 0.019594813

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.001227316 0.001977191 0.620737435 0.537836033 -0.002752563 0.005207196

Rm-Rf 0.587879575 0.076661593 7.668501974 9.14994E-10 0.433567793 0.742191358

Graph 8. Canadian SRI Funds – Jensen’s Alpha (4-year)

y = 0.5879x + 0.0012

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

-10.00% -8.00% -6.00% -4.00% -2.00% 0.00% 2.00% 4.00% 6.00%

Jensen's Alpha -- Canadian SRI 4Y Return

31

Graph 9. Total 9-Year Performance of U.S. SRI Funds vs. S&P 500 Index

Graph 10. Relative 9-Year Performance of U.S. SRI Funds vs. S&P 500 Index

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

U.S. SRI Funds vs. S&P500 Index (9Y)

U.S. SRI Funds S&P 500 Index

-80.00%

-70.00%

-60.00%

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

Relative Return (9Y)

32

Graph 11. Total 4-Year Performance of U.S. SRI Funds vs. S&P 500 Index

Graph 12. Relative 4-Year Performance of U.S. SRI Funds vs. S&P 500 Index

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

U.S. SRI Funds vs. S&P500 (4Y)

U.S. SRI Funds S&P 500 Index

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

12/31/2014 12/31/2015 12/31/2016 12/31/2017 12/31/2018

Relative Return (4Y)

33

Table 9. 4-Factor Analysis of U.S. SRI Funds (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.85616135

R Square 0.733012257

Adjusted R Square 0.722643801

Standard Error 0.026004825

Observations 108

ANOVA

df SS MS F Significance F

Regression 4 0.191233956 0.047808489 70.69637518 1.12869E-28

Residual 103 0.069653845 0.000676251

Total 107 0.260887801

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.001799803 0.002690172 0.669029075 0.504973729 -0.003535518 0.007135124

Mkt-RF 1.013795991 0.073256982 13.83889918 3.07466E-25 0.868508045 1.159083937

SMB 0.306953087 0.118298586 2.59473166 0.01084635 0.072335743 0.541570432

HML 0.207562547 0.124415957 1.668295224 0.09829446 -0.03918716 0.454312254

WML -0.182276942 0.113668435 -1.603584505 0.111867854 -0.407711474 0.043157591

34

Table 10. U.S. SRI Funds – Jensen’s Alpha (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.84026303

R Square 0.706041959

Adjusted R Square 0.70326877

Standard Error 0.026897792

Observations 108

ANOVA

df SS MS F Significance F

Regression 1 0.184197734 0.184197734 254.5956817 6.04383E-30

Residual 106 0.076690067 0.000723491

Total 107 0.260887801

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.00045256 0.002661431 0.170043704 0.865299887 -0.004823987 0.005729106

Rm-Rf 0.635108101 0.03980358 15.9560547 6.04383E-30 0.556193632 0.71402257

Graph 13. U.S. SRI Funds – Jensen’s Alpha (9-year)

y = 0.6351x + 0.0005

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

-30.00% -20.00% -10.00% 0.00% 10.00% 20.00%

Jensen's Alpha -- U.S. SRI Funds (9Y)

35

Table 11. 4-Factor Analysis of U.S. SRI Funds (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.890195211

R Square 0.792447513

Adjusted R Square 0.773140305

Standard Error 0.018649027

Observations 48

ANOVA

df SS MS F Significance F

Regression 4 0.057098328 0.014274582 41.04412766 3.75344E-14

Residual 43 0.014954807 0.000347786

Total 47 0.072053135

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.001839957 0.002795055 0.658289891 0.513861171 -0.003796809 0.007476722

Mkt-RF 0.931861372 0.085818995 10.85845122 6.68368E-14 0.758790874 1.10493187

SMB 0.274573357 0.112726926 2.435738896 0.019080435 0.047237846 0.501908869

HML 0.51410012 0.143227329 3.589399619 0.000844047 0.225254683 0.802945557

WML 0.167133837 0.143941111 1.161126493 0.251995844 -0.123151078 0.457418752

36

Table 12. U.S. SRI Funds – Jensen’s Alpha (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.79383585

R Square 0.630175357

Adjusted R Square 0.622135691

Standard Error 0.024068302

Observations 48

ANOVA

df SS MS F Significance F

Regression 1 0.04540611 0.04540611 78.38327425 1.68737E-11

Residual 46 0.026647025 0.000579283

Total 47 0.072053135

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.001674554 0.0035134 0.476619327 0.635889585 -0.005397553 0.008746662

Rm-Rf 0.758637223 0.085688482 8.853432908 1.68737E-11 0.586155255 0.93111919

Graph 14. U.S. SRI Funds – Jensen’s Alpha (4-year)

y = 0.7586x + 0.0017

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

-15.00% -10.00% -5.00% 0.00% 5.00% 10.00%

Jensen's Alpha -- U.S. SRI Funds (4Y)

37

Graph 15. Total 9-Year Performance of Canadian ESG Funds vs. TSX Composite

Graph 16. Relative 9-Year Performance of Canadian ESG Funds vs. TSX

Composite

-20.00%-10.00%

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%90.00%

CA ESG Funds vs. TSX Composite (9Y)

CA ESG Funds S&P TSX Composite

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Relative Return (9Y)

38

Graph 17. Total 4-Year Performance of Canadian ESG Funds vs. TSX Composite

Graph 18. Relative 4-Year Performance of Canadian ESG Funds vs. TSX

Composite

-20.00%-15.00%-10.00%

-5.00%0.00%5.00%

10.00%15.00%20.00%25.00%30.00%

CA ESG Funds vs. TSX Composite

CA ESG Funds S&P TSX Composite

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

12/31/2014 12/31/2015 12/31/2016 12/31/2017 12/31/2018

Relative Return (4Y)

39

Table 13. 4-Factor Analysis of Canadian ESG Funds (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.826111567

R Square 0.682460321

Adjusted R Square 0.670128683

Standard Error 0.016336085

Observations 108

ANOVA

df SS MS F Significance F

Regression 4 0.059076209 0.014769052 55.34222796 7.95547E-25

Residual 103 0.027487371 0.000266868

Total 107 0.08656358

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.000648729 0.001689951 -0.383874448 0.70186279 -0.004000348 0.00270289

Mkt-RF 0.649482262 0.046019626 14.11315833 8.13213E-26 0.558213189 0.740751336

SMB -0.078900984 0.074314509 -1.061717083 0.290847248 -0.226286284 0.068484317

HML -0.169181162 0.078157407 -2.164620974 0.03272656 -0.324187945 -0.01417438

WML -0.062930318 0.071405874 -0.881304499 0.380204958 -0.204547028 0.078686392

40

Table 14. Canadian ESG Funds – Jensen’s Alpha (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.826735182

R Square 0.683491061

Adjusted R Square 0.680505127

Standard Error 0.016077098

Observations 108

ANOVA

df SS MS F Significance F

Regression 1 0.059165433 0.059165433 228.9036529 3.08681E-28

Residual 106 0.027398147 0.000258473

Total 107 0.08656358

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.002138989 0.001563539 1.368043195 0.174191646 -0.00096088 0.005238859

Rm-Rf 0.665944808 0.044016132 15.12956222 3.08681E-28 0.578678545 0.753211071

Graph 19. Canadian ESG Funds – Jensen’s Alpha (9-year)

y = 0.6659x + 0.0021

-12.00%

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

-15.00% -10.00% -5.00% 0.00% 5.00% 10.00%

Jensen's Alpha -- Canadian ESG Funds (9Y)

41

Table 15. 4-Factor Analysis of Canadian ESG Funds (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.797332276

R Square 0.635738758

Adjusted R Square 0.601853991

Standard Error 0.014419116

Observations 48

ANOVA

df SS MS F Significance F

Regression 4 0.01560312 0.00390078 18.76178646 5.45458E-09

Residual 43 0.008940169 0.000207911

Total 47 0.024543289

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.000121581 0.00216109 -0.056259175 0.955395948 -0.004479834 0.004236672

Mkt-RF 0.486719071 0.066353812 7.335208914 4.22229E-09 0.352903857 0.620534286

SMB 0.023567821 0.087158574 0.270401636 0.788144942 -0.152204195 0.199339836

HML -0.224954456 0.110740975 -2.031357007 0.04842883 -0.448284917 -0.001623995

WML -0.03216169 0.111292859 -0.28898251 0.773983436 -0.256605131 0.192281752

42

Table 16. Canadian ESG Funds – Jensen’s Alpha (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.770582822

R Square 0.593797885

Adjusted R Square 0.584967404

Standard Error 0.01472172

Observations 48

ANOVA

df SS MS F Significance F

Regression 1 0.014573753 0.014573753 67.24411743 1.50127E-10

Residual 46 0.009969536 0.000216729

Total 47 0.024543289

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept 0.002074132 0.002128774 0.974331589 0.334988001 -0.002210868 0.006359131

Rm-Rf 0.67683981 0.082538913 8.200251059 1.50127E-10 0.510697595 0.842982024

Graph 20. Canadian ESG Funds – Jensen’s Alpha (4-year)

y = 0.6768x + 0.0021

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

-10.00% -8.00% -6.00% -4.00% -2.00% 0.00% 2.00% 4.00% 6.00%

Jensen's Alpha -- Canadian ESG Funds (4Y)

43

Graph 21. Total 9-Year Performance of U.S. ESG Funds vs. S&P 500 Index

Graph 22. Relative 9-Year Performance of U.S. ESG Funds vs. S&P 500 Index

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

U.S. ESG Funds vs. S&P 500 Index (9Y)

U.S. ESG Funds S&P 500 Index

-120.00%

-100.00%

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

Relative Return (9Y)

44

Graph 23. Total 4-Year Performance of U.S. ESG Funds vs. S&P 500 Index

Graph 24. Relative 4-Year Performance of U.S. ESG Funds vs. S&P 500 Index

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

U.S. ESG Funds vs. S&P 500 Index (4Y)

U.S. ESG Funds S&P 500 Index

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

12/31/2014 12/31/2015 12/31/2016 12/31/2017 12/31/2018

Relative Return (4Y)

45

Table 17. 4-Factor Analysis of U.S. ESG Funds (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.940474891

R Square 0.88449302

Adjusted R Square 0.880007312

Standard Error 0.014495148

Observations 108

ANOVA

df SS MS F Significance F

Regression 4 0.165717639 0.04142941 197.180251 2.4675E-47

Residual 103 0.021641261 0.000210109

Total 107 0.187358899

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.001619037 0.001499508 -1.079711972 0.282792282 -0.004592957 0.001354884

Mkt-RF 1.053081766 0.040833608 25.78958417 9.70777E-47 0.972097936 1.134065596

SMB 0.003884836 0.0659399 0.058914793 0.953134128 -0.126891404 0.134661075

HML -0.104280751 0.069349736 -1.503693549 0.135720398 -0.241819597 0.033258094

WML -0.155178202 0.063359043 -2.449187897 0.016005692 -0.280835921 -0.029520483

46

Table 18. U.S. ESG Funds – Jensen’s Alpha (9-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.922655134

R Square 0.851292496

Adjusted R Square 0.849889595

Standard Error 0.016212526

Observations 108

ANOVA

df SS MS F Significance F

Regression 1 0.159497225 0.159497225 606.8086809 1.13806E-45

Residual 106 0.027861674 0.000262846

Total 107 0.187358899

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.001297221 0.001604166 -0.8086576 0.420523394 -0.004477636 0.001883194

Rm-Rf 0.590992645 0.023991433 24.63348698 1.13806E-45 0.543427296 0.638557993

Graph 25. U.S. ESG Funds – Jensen’s Alpha (9-year)

y = 0.591x - 0.0013

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

-30.00% -20.00% -10.00% 0.00% 10.00% 20.00%

Jensen's Alpha -- U.S. ESG Funds (9Y)

47

Table 19. 4-Factor Analysis of U.S. ESG Funds (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.947604147

R Square 0.89795362

Adjusted R Square 0.888460934

Standard Error 0.010113059

Observations 48

ANOVA

df SS MS F Significance F

Regression 4 0.03869812 0.00967453 94.59425638 9.92597E-21

Residual 43 0.004397781 0.000102274

Total 47 0.043095901

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.000527539 0.001515712 -0.348046784 0.729503206 -0.003584264 0.002529186

Mkt-RF 0.822745126 0.046538223 17.67891154 2.42505E-21 0.728891855 0.916598397

SMB 0.022030565 0.061129949 0.360389063 0.720320521 -0.101249726 0.145310856

HML 0.029693188 0.077669814 0.38230024 0.704121745 -0.126942919 0.186329296

WML -0.031093172 0.078056886 -0.398339899 0.692350711 -0.188509884 0.12632354

48

Table 20. U.S. ESG Funds – Jensen’s Alpha (4-year)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.932277715

R Square 0.869141737

Adjusted R Square 0.866296993

Standard Error 0.011072346

Observations 48

ANOVA

df SS MS F Significance F

Regression 1 0.037456446 0.037456446 305.5253762 6.07757E-22

Residual 46 0.005639455 0.000122597

Total 47 0.043095901

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -0.000218717 0.001616299 -0.135319473 0.892949706 -0.003472159 0.003034725

Rm-Rf 0.689033413 0.039420002 17.4792842 6.07757E-22 0.609685065 0.768381761

Graph 26. U.S. ESG Funds – Jensen’s Alpha (4-year)

y = 0.689x - 0.0002

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

-15.00% -10.00% -5.00% 0.00% 5.00% 10.00%

Jensen's Alpha -- U.S. ESG Funds (4Y)

49

Bibliography

Bauer, R., K. Koedujk and R. Otten: 2005, ‘International Evidence on Ethical Mutual

Fund performance and Investment Style’, Journal of Banking and Finance,1751-1767.

Bauer, R., R. Otten and A. Tourani Rad: 2006, ‘Ethical Investing in Australia, is there a

financial Penalty?’, Pacific-Basin Finance Journal 14, 33-48.

Bauer, R., R. Otten and J. Derwall: 200, ‘The Ethical Mutual Fund Debate: The New

Evidence from Canada’, Journal of Business Ethics 70, 111-124.

Blanchett, D.M: 2010, ‘Exploring the Cost of Investing in Socially Responsible Mutual

Funds: An Empirical Study’, Journal of Investing 19, 93-103.

Brzeszczynski, J. and G.McIntose: 2014, ‘Performance of Portfolios Composed of British

SRI stocks’, Journal of Business Ethics 120, 355-362.

Carhart, M. M.: 1997, ‘On the persistence in Mutual Fund Performance’, Journal of

Finance 52, 57-82.

Fama, E. and K.R.French: 1992, ‘The Cross-Section of Expected Stock Returns’, Journal

of Finance 47, 427-465

Fama, E. and K.R.French: 1993, ‘Common Risk Factors in the Returns on Stocks and

Bonds’, Journal of Financial Economics 33, 3-53.

Fama, E. and K.R.French: 1996, ‘Multifactor Explanations of Asset Pricing Anomalies’,

Journal of Finance 51, 55-84.

Carhart Benchmark Factors: K.R. French library,

<https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html>

50

Jensen, M.C:1968, ‘The Performance of Mutual funds in the period 1945-1964’, Journal

of Finance 23, 389-415

KLD Research Analytics, Inc. The Domini 400 Social Index.

< https://www.msci.com/msci-kld-400-social-index>

Hamilton, S., H. Jo and M. Statman: 1993, ‘Doing well while doing good? The

Investment Performance of Social Responsible Mutual Funds’, Financial Analyst Journal

49, 62-66.

Minor, D.: 2007, ‘Find the Cost of Socially Responsible Investing’, Journal of Investing

16, 54-70

Sauer, D.A:1997, ‘The impact of Socially Responsibility Screens on Investment

Performance: evidence from the Domini Social Index and Domini Equity Mutual Fund’,

Review of Financial Economics 6, 137-149

Sharpe, W.F :1996, ‘Mutual Fund Performance’, Journal of Business 39, 119-138.

Statman, M.: 2000, ‘Socially Responsible Mutual Funds’, Financial Analysts Journal 56,

30-39.

Sustainanalytics, Jantzi Social Index.

< https://www.sustainalytics.com/jantzi-social-index/>

51