the renaissance in mergers and acquisitions compendium_2014.pdf · 2014-12-18 · mergers and...

TRANSCRIPT

The renaissance in mergersand acquisitions

Copyright © 2014 Bain & Company, Inc. All rights reserved.

About the authors

David Harding is a partner with Bain & Company in Boston and co-leader of Bain’s Global M&A practice.

Richard Jackson is a partner in London and leader of Bain’s M&A practice in EMEA.

Phil Leung is a partner with Bain & Company in Shanghai and leader of Bain’s M&A practice in Asia-Pacifi c.

Matthias Meyer is a director of Bain’s EMEA/Asia-Pacifi c M&A practices and is based in Munich.

Karen Harris is director of the Bain Macro Trends Group and is based in New York.

1

Preface

Mergers and acquisitions are about to undergo a renaissance.

Deal making has always been cyclical, and the last few years have felt like another low point in the cycle. But the historical success of M&A as a growth strategy comes into sharp relief when you look at the data. Bain & Company’s analysis strongly suggests that executives will need to focus even more on inorganic growth to meet the expectations of their investors.

The fi rst installment of this three-part series on the coming M&A renaissance, “The surprising lessons of the 2000s,” looks back at the last 11 years of deal activity and fi nds that it was a very good time for deal makers who followed a repeatable model for acquisitions. The accepted wisdom paints the decade as a period of irra-tional excess ending in a big crash. Yet companies that were disciplined acquirers came out the biggest win-ners. Another surprise: Materiality matters. We found the best returns among those companies that invested a signifi cant portion of their market cap in inorganic growth.

The second part of the series, “What to do with all that cash?” looks forward and argues that the confl uence of strong corporate balance sheets, a bountiful capital environment, low interest rates and eight great macro trends will combine to make M&A a powerful vehicle for achieving a company’s strategic imperatives. The fuel—abundant capital—will be there to support M&A, and the pressure on executives to fi nd growth will only increase as investors constantly search for higher returns. Some business leaders argue that organic growth is always better than buying growth, but the track record of the 2000s should make executives question this conventional view.

The fi nal part of the series, “How to make your deals successful,” highlights the importance of discipline in a favorable environment for M&A. Deal making is not for everyone. If your core business is weak, the odds that a deal will save your company are slim. But if you have a robust core business, you may be well positioned. All successful M&A starts with great corporate strategy, and M&A is often a means to realize that strategy. Under pressure to grow, many companies will fi nd inorganic growth faster, safer and more reliable than organic investments.

As M&A comes back, some executives will no doubt sit on the sidelines thinking it is safer not to play. Experience suggests that their performance will suffer accordingly. The winners will be those who get in the game—and learn how to play it well.

1. The renaissance in mergers and acquisitions: The surprising lessons of the 2000sBy David Harding, Phil Leung, Richard Jackson and Matthias Meyer

Looking back at the first decade of this century, it is clear that many companies succeeded in delivering superior share-holder returns using M&A as a weapon for competitive advantage. Executives had to be smart about it, and they had to be committed. But for those with a repeatable model, the rewards were exceptional.

The surprising lessons of the 2000s

5

when the cumulative value of their acquisitions

over the 11-year period amounted to a large percent-

age of their market capitalization.

• The gold standard of M&A is a repeatable model.

Companies that built their growth on M&A—those

that acquired frequently and at a material level—

recorded TSR nearly two percentage points higher

than the average.

The research supporting these numbers is robust, and

it points the way to a powerful tool for growth. If your

company has a successful strategy, you can use the

balance sheet to strengthen and extend that strategy.

M&A can help you enter new markets and product

lines, fi nd new customers and develop new capabilities.

They can help you boost your earnings and turbocharge

your growth.

The trick, as always, is to do M&A right.

Which deal makers succeed?

M&A can be a slippery subject to study. Businesspeople,

trained in the case method, often try to draw lessons

from individual examples. M&A fans point to successes

such as Anheuser-Busch InBev, whose mergers and

acquisitions have made it the world’s largest brewer.

Skeptics point to classic deal-making busts such as

AOL-Time Warner. The trouble is, you can fi nd a story

to fit virtually any hypothesis about M&A, including

the argument that a company can prosper without

relying on deals (look at IKEA or Hankook Tire).

Case-study evidence is always helpful in understanding

M&A specifics, but as a guide to the territory it can

be misleading.

To establish a foundation on the overall results of deal

making, we launched a worldwide research project

involving more than 1,600 publicly traded companies

and covering more than 18,000 deals from 2000 through

2010. We assessed the performance of companies that

engaged in M&A and those that did not. We compared

results for companies that did a lot of acquisitions with

those that did relatively few. We also looked at whether

the cumulative size of deals relative to a company’s

April 2007 was a remarkable high-water mark for M&A.

That month, companies around the world announced

deals worth more than half a trillion dollars in total

value—the highest ever. For the year, worldwide deals

would surpass 40,000 for the fi rst time; their cumu-

lative value would hit $4.6 trillion, 40% above the dot-

com peak in 2000. It seemed like the M&A party might

never stop.

But when the fi scal crisis brought the boom to an abrupt

end, the hangover set in. Many business leaders again

grew leery of any kind of deal making. M&A was too

risky, they felt. It destroyed more value than it created.

Some agreed with the often-quoted 2004 pronounce-

ment of a CEO named Ellis Baxter, who responded to

a Harvard Business School article questioning the wis-

dom of acquisitions. “In the end,” wrote Baxter, “M&A

is a fl awed process, invented by brokers, lawyers and

super-sized, ego-based CEOs.”

The reaction was understandable. But a sober assess-

ment of M&A activity over the past decade puts deal

making in a different light. Companies that were active

in M&A, the data shows, consistently outperformed

those that stayed away from deals. Companies that did

the most deals, and whose cumulative deal making

accounted for a larger fraction of their market capital-

ization, turned in the best performance of all.

M&A, in short, was an essential part of successful strat-

egies for profi table growth. Many management teams

that avoided deals paid a price for their reticence.

Consider the data. From 2000 through 2010, total share-

holder return (TSR) averaged 4.5% per year for a large

sample of publicly traded companies around the world.

Dividing this sample according to companies’ M&A

activity, here’s what we observe:

• Players outperformed bystanders. As a group, com-

panies that engaged in any M&A activity averaged

4.8% annual TSR, compared with 3.3% for those

that were inactive.

• Materiality mattered—a lot. Companies that did a

lot of deals outperformed the average most often

6

The renaissance in mergers and acquisitions

did between one and six acquisitions boosted their

performance signifi cantly, to 4.5%, and those that did

more than six topped 5% TSR. These seemingly modest

differences in annual TSR add up to signifi cant dispar-

ities over a decade. The top group, for example, had 21%

higher returns than the inactive group.

The difference between frequent acquirers and occa-

sional ones is hardly a mystery. Experience counts. A

company that does more acquisitions is likely to identify

the right targets more often. It is likely to be sharper

in conducting the due diligence required to vet the deals.

It is also likely to be more effective at integrating the

acquired company and realizing potential synergies.

Stanley Works, for example—now Stanley Black & Decker

(SB&D)—embarked on an aggressive M&A program

beginning in 2002, and over the next several years it

acquired more than 25 companies. It used operational

capabilities such as the Stanley Fulfi llment System to

improve the acquired businesses, and it grew more and

more successful at realizing synergies through post-

merger integration. After acquiring key competitor

Black & Decker in 2010, more than doubling its size,

market capitalization made a difference. (For more on

the research, see the sidebar, “What we studied and how

we gauged performance.”)

Data from this study shows unequivocally that deal mak-

ing paid off during that 11-year period. Companies that

were actively engaged in M&A outperformed inactive

companies not only in TSR but in sales growth and

profit growth as well. The data also underscored the

fact that the world of M&A is not uniform and shouldn’t

be treated as such. Some companies were able to use

deals to power consistently higher performance. Others

were far less successful, and often pursued deals that

failed to pay off.

Every transaction has its own characteristics. In general,

however, the difference boiled down to two main factors:

Frequency. As a rule, the more experience a company

has doing M&A, the greater the likelihood that its deals

will be successful. Companies in our study that were

inactive—no mergers or acquisitions during the period—

recorded 3.3% annual TSR (see Figure 1). Those that

Figure 1: Companies that acquire more frequently tend to outperform signifi cantly in the long term

Notes: n=1,616 companies; number of deals includes deals with undisclosed value Sources: Bain M&A Study 2012; Dealogic; Thomson; Bain SVC Database 2011

Translates into21% higher

shareholder returngenerated between

2000–2010

0

2

4

6%

0 1–6

4.5%

7–11

5.1%

12+

Number of acquisitions (2000–2010)

Annual total shareholder returns (CAGR 2000–2010)

5.1%

3.3%

The surprising lessons of the 2000s

7

What we studied and how we gauged performance

Bain has been studying M&A for more than 10 years. In 2011 and 2012, we conducted a large-scale quantitative study of company performance as it related to M&A. We also surveyed more than 350 executives around the globe (in partnership with the Economist Intelligence Unit) about their views of M&A.

The quantitative research reviewed the fi nancial performance and M&A activity of 1,616 publicly listed manufacturing and service companies from 2000 through 2010. The sample initially included all companies from 13 developed and emerging countries for which we were able to obtain full fi nan-cial data; these countries account for nearly 90% of world GDP attributable to the top 20 economies. We then excluded companies with revenues of less than $500 million in 2000, those with major swings in earnings before interest and taxes (EBIT) margin around 2000 or 2010, and natural resource and fi nancial companies, which exhibit different industry dynamics. We also examined the effect of “survivorship bias”—the exclusion of companies that had ceased to exist during this period—and found that whatever bias may exist did not affect our performance benchmarks.

To compare company performance, we used total shareholder return (TSR), defi ned as stock price changes assuming reinvestment of cash dividends. We calculated average annual TSR using annual total investor return (TIR) provided by Thomson Worldscope for year-ends 1999 to 2010. We ana-lyzed M&A activity by including all acquisitions—more than 18,000 in all—announced by the com-panies in the sample between the beginning of 2000 and the end of 2010. The data was based on information provided by Dealogic and included all deals in which a company had made an outright purchase, an acquisition of assets or acquisition of a majority interest. For deals with an undisclosed deal value, we assumed a deal size of 1.3% of the acquirer’s market capitalization, the median value.

Source: Bain analysis; Dealogic

TSR CAGR2000–2010 4.5%

100

150

$200

Inactives

$143

Large Bets

$154

Serial Bolt-Ons

$163

Selected Fill-Ins

$163

Mountain Climbers

$197

Sampleaverage:$163

3.3% 6.4%4.0% 4.5% 4.6%

$100 invested in 2000 returned at the end of 2010...

Successful deal makers: The difference

8

The renaissance in mergers and acquisitions

position to do deals. But the implications are clear re-

gardless. A company with a strong business is likely to

boost its performance by consistently pursuing M&A,

to the point where its deals account for a large fraction

of its value. If a company’s business is weak, however,

it is highly unlikely that one big deal will turn it around.

Put frequency and materiality together and you get a

clear picture showing which companies have been most

successful at M&A (see Figure 3). Viewing M&A

through this lens also reveals what kind of deal making

produces the greatest rewards.

The first takeaway: The average annual TSR for all

1,600-plus companies that we studied was 4.5%.

Two groups fell below this average. One was the by-

standers or inactives, the companies that sat on the M&A

sidelines. Some companies in this group, of course,

were committed to organic growth and performed well

despite a lack of M&A: Hankook’s TSR was a remark-

able 26.3%. But many others may have been too weak

it was able to exceed its original savings estimates for

the deal by more than 40%. From 2000 through 2010,

SB&D recorded annual TSR of 10.3%.

Materiality. Previous studies, including our own, have

noted the importance of frequency in determining a

company’s likely return from M&A. Our research high-

lights the importance of another variable: the cumula-

tive size of a company’s deals relative to its value. The

more of a company’s market cap that comes from its

acquisitions, the better its performance is likely to be.

In fact, companies making acquisitions totaling more

than 75% of their market cap outperformed the inactives

by 2.3 percentage points a year, and they outperformed

the more modest acquirers by one percentage point a

year (see Figure 2).

It can be difficult to untangle cause and effect when

studying M&A. Companies whose acquisitions add up

to a large fraction of their market cap may be success-

ful because they can fi nd the right deals to do, or it may

be that already successful companies are in a better

Figure 2: Companies that are material acquirers over time tend to outperform

Notes: n=1,616 companies; cumulative relative deal size 2000–2010 is the sum of relative deal sizes vs. respective prior year-end market capitalizationSources: Bain M&A Study 2012; Dealogic; Thomson; Bain SVC Database 2011

Annual total shareholder returns (CAGR 2000–2010)

0

2

4

6%

Inactives

3.3

4.6

5.6

M&A with cumulativerelative deal size as a

percentage of market cap ofup to 75%

M&A with cumulativerelative deal size as a

percentage of market cap ofmore than 75%

The surprising lessons of the 2000s

9

Corp. in 2003 and USF Corp. in 2005. YRC’s total share-

holder return over the decade was negative 35%, and the

company avoided bankruptcy in late 2009 only through

a complex bond-swap agreement with creditors.

Two other groups of companies engaged in a modest

level of M&A, not a material amount. We have labeled

these companies “Serial Bolt-Ons” and “Selected Fill-

Ins” depending on the frequency of their deals, but the

results for both groups were much the same: about

average. These companies’ deals, however numerous,

were simply too small in the aggregate to move the

needle on performance. Here, too, however, there is

variation. Apple—usually held up as a model of organic

growth—has in fact acquired a series of small compa-

nies, adding critical skills and capabilities (such as voice

recognition) that it otherwise lacked. Amazon has added

new product categories through the acquisition of Zappos,

Diapers.com and others; it has also added back-offi ce

capabilities, such as the warehouse robotics provided

by its purchase of Kiva Systems. But for every Apple or

Amazon there are many companies whose M&A strat-

or too reticent to get in the game, and their performance

suffered accordingly. Interestingly, even companies that

avoid M&A during periods of rapid expansion may fi nd

themselves turning to deal making as organic growth

possibilities cool off. By 2012, for instance, Hankook

was scouting for deals in the automotive parts market.

The other below-average group appears in the box la-

beled Large Bets. These companies made relatively few

acquisitions, averaging less than one a year, but the

total value of the deals still accounted for more than 75%

of their market cap. In other words, they were swing-

ing for the fences, hoping to improve their business

with a couple of big hits. Such deals are the riskiest of

all. Though they sometimes work, big bets as a strategy

usually fail to pay off. Tata Motors has been successful

so far in its acquisition of Jaguar and Land Rover—a

remarkably ambitious large bet that contributed to Tata’s

TSR of 18.4% between 2000 and 2010. More common,

however, are unsuccessful big bets, such as the bid by YRC

Worldwide Inc. to assemble a major transportation and

freight handling company with acquisitions of Roadway

Figure 3: M&A creates the most value when it is frequent and material over time

Notes: n=1,616 companies; number of deals includes all deals; relative deal size for deals with undisclosed value assumed at median sample deal size of 1.3% of marketcapitalization; cumulative relative deal size 2000–2010 based on sum of relative deal sizes vs. respective prior year-end market capitalizationSources: Bain M&A Study 2012; Dealogic; Thomson; Bain SVC Database 2011

Annual total shareholder returns (CAGR 2000–2010)

Inactives3.3%

Above-averagedeal activity

(>1 deals per year)

Below-averagedeal activity

(<1 deal per year)

Acquisitionfrequency

Serial Bolt-Ons4.5%

Large Bets4.0%

Mountain Climbers6.4%

Selected Fill-Ins4.6%

<_ 75% of buyer’s market cap >75% of buyer’s market cap

Cumulative relative deal size

AverageTSR for allcompaniesin sample:

4.5%

10

The renaissance in mergers and acquisitions

ample, at Anheuser-Busch InBev, which has built its

remarkable growth on a foundation of successful merg-

ers and acquisitions. Each major deal has allowed the

company not only to expand but to increase its EBITDA

margin, using well-honed skills both in integrating the

merger parties and boosting productivity throughout

the new organization.

Understanding the elements of this repeatable model

in detail shows the variety of skills that frequent ac-

quirers develop.

First, successful acquirers understand their strategy and

create an M&A plan that reinforces the strategy. The

strategy provides a logic for identifying target companies.

Second, they develop a deal thesis based on that strat-

egy for every transaction. The thesis spells out how the

deal will add value both to the target and to the acquir-

ing company. For example, it may expand the acquirer’s

capabilities, create new opportunities for existing capa-

bilities, generate signifi cant cost synergies or give the

acquirer access to new markets. Early development of

a meaningful deal thesis derived from a company’s

strategy pays off. In earlier interviews with 250 executives

around the world, we found that 90% of successful

deals started with such a thesis, compared with only

50% of failed deals.

Third, they conduct thorough, data-based due diligence

to test their deal thesis, including a hard-nosed look at

the price of the business they are considering. There

will always be a conventional-wisdom price for a target

company, usually an average of whatever industry ex-

perts and Wall Street analysts think it is worth. A fre-

quent acquirer knows exactly where it can add value

and is therefore able to set its own price—and to walk

away if the price isn’t right. Inadequate diligence is

high on the list of reasons for disappointing deal out-

comes. In a 2012 survey of more than 350 executives,

the top two reasons for perceived deal failure were,

fi rst, that due diligence failed to highlight critical issues

(59% of respondents) and, second, that the company

had overestimated potential synergies in the deal (55%

of respondents).

egy simply didn’t add much. Unless the experience ul-

timately leads to larger deals, these companies were

very likely squandering resources on deals that made

little or no difference to their fi nancial results.

The only companies with deal-making returns signifi -

cantly above average are the “Mountain Climbers.” These

companies are the M&A stars, with returns almost two

percentage points above the average and more than

three points above the inactives. They acquire frequently.

Their acquisitions add up in terms of materiality. Their

deals are generally well conceived, reinforcing their

strategy. They develop strong capabilities, both for

executing deals and for post-merger integration, and

they can use these capabilities effectively in pursuing

large, complex transactions.

Look, for instance, at companies such as Schneider

Electric (based in France), Wesfarmers (Australia) or

Precision Castparts (US). All have used serial acquisitions

effectively to expand into new geographies, new markets

or both, thus boosting their growth. Such companies

often hone their acquisition skills on smaller deals,

enabling them to move quickly to acquire a larger

target when the time is right. Wesfarmers, for example,

did about 20 deals in the decade prior to its 2007

acquisition of Coles Group, the large Australian retailer

(which more than doubled its market cap). Wesfarmers’

TSR averaged 13.4% a year from 2000 through 2010.

Developing a repeatable model

Most successful companies develop a repeatable model—

a unique, focused set of skills and capabilities that they

can apply to new products and new markets over and

over. As our colleagues Chris Zook and James Allen

show in their 2012 book, Repeatability, repeatable mod-

els are key to generating sustained growth. Our own

analysis and experience confi rm the power of repeat-

ability in the world of M&A. An acquirer’s expertise in

fi nding, analyzing and executing the transaction, and

then in integrating the two companies when the deal

is done, determines the success of the typical deal. Fre-

quent acquirers create a repeatable M&A model, one

that they return to again and again to launch and ne-

gotiate a successful deal (see Figure 4). Look, for ex-

The surprising lessons of the 2000s

11

cantly greater return, on average, than their opportu-

nistic counterparts. One reason may be that the Large

Bettors tended to stick to scale deals, staying in the same

business but increasing their scale of operations; more

than three-quarters of the group’s transactions fell into

this category. Scale deals are presumably safer, prom-

ising measurable cost synergies, but they rarely provide

any top-line growth and may require fl awless integration

to capture the potential value. Meanwhile, the Mountain

Climbers were able to execute scope deals, which accounted

for nearly half of their transactions in our study. These

deals expanded the range of the Mountain Climbers’

business and helped boost their performance.

The pressure to grow is only going to increase with

time. Looking back at the fi rst decade of this century,

it is clear that many companies succeeded in delivering

superior shareholder returns using M&A as a weapon

for competitive advantage. Executives had to be smart

about it, and they had to be committed. But for those

with a repeatable model, the rewards were exceptional.

Over the next several years we believe the environment

Fourth, successful acquirers plan carefully for merger

integration. They determine what must be integrated

and what can be kept separate, based on where they

expect value to be created. This is one area that we ob-

serve has improved measurably during the past decade:

Companies are devoting far more time, attention and

resources to integration. In 2002, executives we sur-

veyed said the No. 1 reason for disappointing deal re-

sults was because they “ignored potential integration

challenges.” In 2012, integration challenges had dropped

to No. 6 among the causes cited by executives for dis-

appointing deal results.

Finally, they mobilize to capture value, quickly nailing the

short list of must-get-right actions and effectively execut-

ing the much longer list of broader integration tasks.

Developing a repeatable model gives frequent acquirers

advantages that opportunistic acquirers lack. Look, for

example, at the difference between Mountain Climbers

and the Large Bettors. Both were engaged in substantial

acquisitions, yet Mountain Climbers enjoyed a signifi -

Figure 4: If done right, M&A creates value—especially with a repeatable model built upon a disciplined M&A capability

Source: Bain & Company

• Make M&A an extension of your growth strategy – Clear logic to identify targets – Clarity on how M&A strategy will create value

• Mobilize in a focused fashion to capture high-priority sources of value – Nail the short list of critical actions you have to get right – Execute the long list of integration tasks stringently

• Require clarity on how each deal creates value – Apply or leverage capabilities to add value to the target – Expand capabilities or fill capability gaps to create opportunities you didn’t have

• Know what you really need to integrate (and what not to) – Articulate value creation road map – Plan to integrate where it matters

• Test the deal thesis vs. conventional wisdom— set a walk-away price – Justify the winning bid – Determine where you can add value

M&Astrategy

M&Acapability

Dealthesis

Mergerintegrationexecution

Mergerintegrationplanning

Diligence and

valuation

12

The renaissance in mergers and acquisitions

will become increasingly conducive to well-conceived

deal making. In the second part of this series, we will

look at how the market environment, company balance

sheets and the emerging need to fi nd new capabilities

to expand the scope of competition will all feed the

M&A cycle. In that environment, inorganic growth is

likely to be a key to unlocking strategic imperatives for

many, many companies. Then, in the third part, we will

examine in detail how individual companies capitalize

on such an environment by creating repeatable models,

thereby increasing their odds of deal-making success.

Not every company can do it. But the rewards are sub-

stantial for those that can.

2. The renaissance in mergers and acquisitions: What to do with all that cash?By David Harding, Karen Harris, Richard Jackson and Phil Leung

The confl uence of strong corporate balance sheets, a bountiful capital environment, low interest rates and eight great macro trends will combine to make M&A a powerful vehicle for achieving a company’s strategic imperatives.

What to do with all that cash?

15

The world is awash in capital. By Bain’s estimate, about

$300 trillion in global fi nancial holdings is available for

investment. The time is right to put this money to work,

and a lot of it should fund the renaissance in M&A.

Why? One reason is pent-up demand. The slowdown

in M&A since 2007 was triggered by the fi nancial crisis,

and will reverse itself as the world economy recovers.

Each M&A boom tends to outstrip the previous one—

both in the number of deals and in the total value of

acquisitions (see Figure 1).

This time around, however, three additional factors will

turbocharge the deal-making renaissance:

• Financial capital is plentiful and cheap, and will

likely remain so. With real interest rates well below

historical levels, the pursuit of higher returns will

be unrelenting.

• A series of trillion-dollar trends are opening up

major new opportunities for growth.

• Many companies are fl ush with cash and well po-

sitioned to capitalize on these opportunities—but

organic growth alone is unlikely to produce the

returns investors expect.

Together, these factors are likely to push deal making

to record levels. Let’s look more closely at the eco-

nomic environment and the reasons for our belief in

an M&A renaissance.

A world awash in capital

Capital is no longer scarce; it’s superabundant. The $300

trillion in fi nancial holdings is about six times larger

than the market value of all publicly traded companies

in the world. By the end of the decade, capital held by

financial institutions will increase by approximately

$100 trillion (measured in 2010 prices and exchange

rates)—an amount more than six times the US GDP.

All that money needs to be put to work.

Figure 1: The global M&A market is cyclical

Recession:1980Q1−1980Q21981Q2−1982Q3

Recession:1990Q3−1991Q1

Recession:2001Q1−2001Q3

Recession:2007Q4−2009Q4

0

1

2

3

4

$5T

Global announced M&A deal value Global deal count

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Deal value ($T) Deal count (k)

10

20

30

40

50K

0

Source: Thomson Financial (until 2000); Dealogic (from 2000)

16

The renaissance in mergers and acquisitions

From 1973 to 1981, the most recent period of sus-

tained high infl ation, supply constraints in energy

and other sectors combined with buoyant demand

from the young baby boomer generation led to

continuing upward pressure on prices. In the 2010s,

supply growth in most sectors is readily available;

many industries have signifi cant overcapacity. Yet

demand is tepid and is likely to remain so for

decades, partly because of long-term trends such

as the aging of the population. Given these two

factors, producers will fi nd it diffi cult to pass price

increases on to consumers.

Although abundant capital and easy borrowing will

probably not feed general inflation, they are almost

certain to have one kind of inflationary effect: They

will feed the growth of asset bubbles. In a global econ-

omy, some assets somewhere are likely to be increasing

in price at any given time; it might be metals, agricul-

tural commodities, fuels, farmland, other real estate

or indeed nearly any other class of assets. As investors

around the world pour their money into these assets

their prices rise still higher, and the stage is set for a

classic bubble. In the environment we have described,

the bubbles will likely last longer and grow bigger

before they inevitably burst.

High investor expectations

Capital is superabundant, interest rates are correspond-

ingly low, demand is muted and growth sluggish. Does

all this mean that investors expect only modest returns?

Not quite. The data indicates that investors expect

companies to grow considerably faster than their his-

torical growth rates. In the US, where this growth gap is

most pronounced, companies increased their earnings

at an average annual rate of 6% in the period from

1995 through 2013 (see Figure 2). Yearly growth in

nominal GDP during the period 2014 to 2016 is likely

to be much the same as it was then—but investors

expect their companies to grow at about 11% a year.

Executives thus fi nd themselves in a challenging situ-

ation. Capital is widely available at relatively low cost,

including on their own companies’ balance sheets.

Capital is widely available at relatively low cost. The job is to put all this money to work with the goal of creating alpha—performance that outstrips market indexes.

Capital superabundance produces low interest rates. In

the years following the global fi nancial crisis, interest

rates in many countries hit new lows, with real rates

on low-risk investments hovering around zero. We

expect rates to remain low for some time, primarily

because of supply and demand: Financial assets have

grown considerably faster than real output between

the early 1990s and today, a trend that has led to a drop

of 4 to 5 percentage points in the global average lending

rate during this period. Three interrelated factors

reinforce that long-term trend:

• Historically, rates remain low after a crisis of the

sort that began in 2007. Households and businesses

reduce their borrowing. Growth is sluggish. These

long-cycle periods of unusually low interest rates

can extend for decades. In the Great Depression

and more recently in Japan’s Lost Decade, rates re-

mained low for up to 20 years after the initial crisis.

• Central banks around the world are committed to

keeping interest rates low for the foreseeable future.

The US Federal Reserve Board has said that it will

maintain low rates as long as unemployment stays

above 6.5% and infl ation remains below 2.5%. The

European Central Bank and the Bank of Japan are

pursuing similar policies. Central banks are not

only setting their own rates low; they are also

helping to keep market rates down by pumping

money into their economies.

• Despite all this money—and contrary to much

conventional wisdom—inflationary pressures

around the world are likely to remain weak. The

reason is that today’s economy is constrained by

the slow pace of growth in demand, not by supply.

What to do with all that cash?

17

targets while curtailing investment and sacrifi cing top-

line growth—not a formula for making shareholders

happy over the long term. CFOs face a further challenge

as well. Though they are punished by the market for

failing to protect against risk, they aren’t rewarded for

using the balance sheet strategically to strengthen the

business—particularly since such an approach wasn’t

necessary prior to the global fi nancial crisis.

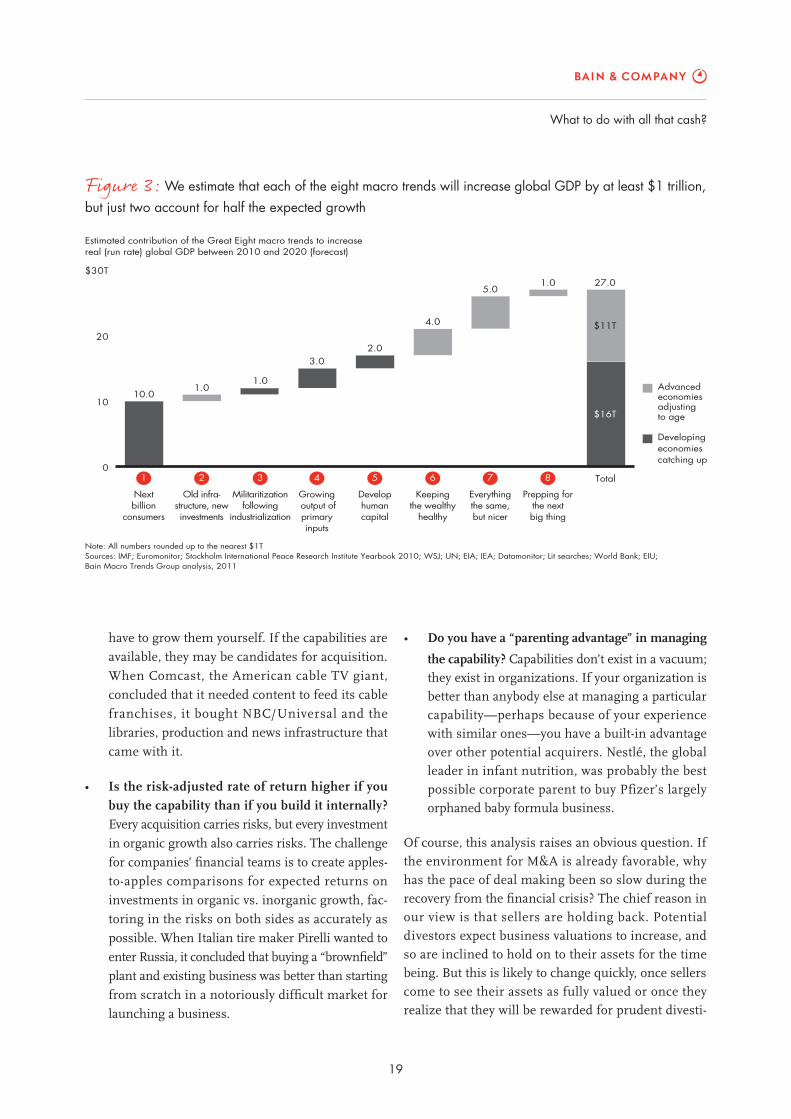

Macro trends—and the opportunitiesfor growth

Against the backdrop of this business climate, we see

eight macro trends in the global economy that open

up major new growth opportunities (see Figure 3). We

won’t discuss them in detail here—for a full account, see

our report, “The great eight: Trillion-dollar growth trends

to 2020.” This brief summary, with the “great eight”

shown in italics, indicates the potential for growth.

Consumers. By 2020, the next billion consumers in devel-

oping nations will join the ranks of the global middle

class, earning more than $5,000 a year. Their purchasing

Companies with investment-grade ratings often fi nd

that they can borrow at a lower cost than many sovereign

nations, whose bonds were once thought to be nearly

risk-free. Companies in zones with highly valued

currencies—Europe, for instance—can take advantage

of their currency’s strength to invest overseas at bargain

rates. The job is to put all this money to work with the

goal of creating alpha—performance that outstrips

market indexes. By the same token, sitting on cash can

be a high-risk strategy when rivals are repositioning

themselves for growth.

Hurdle rates for corporate investments symbolize this

challenge. In our experience, many chief fi nancial offi -

cers (CFOs) have kept hurdle rates high relative to interest

rates in the post-crisis years, explaining that their caution

refl ects the general risks of an uncertain world and the

specifi c risk that interest rates would return to historically

normal levels. But lowering hurdle rates may actually

be a more appropriate move for an era of capital super-

abundance. Lowering them too far is always a danger, but

so is leaving them high. A company with high hurdle

rates may wind up perpetually meeting its earnings

Figure 2: The challenge: Investors expect companies to grow faster than the historical growth embedded in their business

US Europe Asia- Pacific

0

5

10

15

20

25%

Earnings growth (in %)

Note: Based on respective aggregate EPS consensus forecasts for S&P 500 (US), MSCI Europe (Europe), and FTSE Pacific (APAC)Source: Thomson Financial I/B/E/S; Bain analysis

6.1%

11.2%

5.4%

10.4%

7.5%

10.8%

Historicalearnings

Forecastedearnings

Historicalearnings

Forecastedearnings

Historicalearnings

Forecastedearnings

1995–2013 2014–2016

Growth expectations > historical performance

18

The renaissance in mergers and acquisitions

add as much as $2 trillion to world GDP. Additionally,

rapid growth in these emerging markets has created a

global shortage of management talent that is only going

to get worse. In developed nations, meanwhile, new

healthcare spending—keeping the wealthy healthy—will

likely add $4 trillion to GDP.

The next big thing—and the resources to support all

of these trends. Major innovations come in waves,

and fi ve potential platform technologies—nanotech-

nology, genomics, artifi cial intelligence, robotics and

ubiquitous connectivity—show promise of fl owering

over the next decade. New technologies tend to rein-

force one another. Prepping for the next big thing should

open up unexpected opportunities in both consumer

goods and industrial processes. When the next big

things arrive, they are likely to accelerate growth.

All of these trends require growing output of primary

inputs, meaning large investments in basic resources

such as food, water, energy and ores. Growing demand

will stimulate new investment, but will also lead to

spot shortages and price volatility. All told, the primary

goods sector will likely add $3 trillion to global GDP.

Why M&A?

For leadership teams, one vital challenge is how to

best position their businesses to take advantage of

these emerging trends. A strategy focused on organic

growth alone is unlikely to deliver the expanded capa-

bilities or market penetration they need. Most companies

will have to rely on a balanced strategy, pursuing M&A as

well. In many cases it is faster and safer to buy an asset

than to invest in building your own (see Figure 4).

Three essential questions can help companies determine

when buying rather than building makes sense for them:

• Does someone else have a capability that would

enhance your business? There are many different

kinds of capabilities—technologies, sales channels,

operations in particular geographic areas and so

forth. If no one else has the capabilities you need

to strengthen or adapt your business, you obviously

power and preferences will be different from those of

middle-class consumers in developed nations, but taken

as a group they will add an additional $10 trillion to

world GDP by 2020. Companies targeting this group

need lower cost structures than in use today—and

they can’t assume these consumers will move up the

price ladder over time.

Consumers in developed countries will be looking for

more of what they have enjoyed in the recent past—

everything the same but nicer, better and more carefully

tailored to their tastes and lifestyles. Along with tech-

nological innovations such as tablet computers will

come “soft” innovations, such as the ability to deliver

a new outfi t to an online shopper’s doorstep the same

day she orders it. Soft innovations enhance and stimu-

late consumption by providing extra value that buyers

are willing to pay for. They are likely to transform

whole categories of consumer goods and services,

from fashion to food.

Government and infrastructure. In developed nations,

old infrastructure, new investments will translate into a

surge of spending by governments on replacements

and upgrades of physical infrastructure. With public

funds limited, some of these jobs will be undertaken

by public-private partnerships, and are likely to con-

tribute about $1 trillion to world GDP. Meanwhile,

militarization following industrialization—arms buildup

in the developing world—presents an opportunity for

arms developers but, more important, a risk to global

business. China has an overarching interest in protect-

ing its supply chain, but the supply chains are shared

by Japan and (to some extent) by India. The risk of an

attenuated supply chain, in turn, puts a premium on

building capacity closer to end markets, which leads

many companies to consider moving operations back

to the US and Europe.

Developing nations face the challenge of developing

human capital, and their social infrastructure is likely

to require even more investment than their physical

infrastructure. The combination of broadening access

to education, building effective healthcare delivery

systems and strengthening the social safety net will

What to do with all that cash?

19

• Do you have a “parenting advantage” in managing

the capability? Capabilities don’t exist in a vacuum;

they exist in organizations. If your organization is

better than anybody else at managing a particular

capability—perhaps because of your experience

with similar ones—you have a built-in advantage

over other potential acquirers. Nestlé, the global

leader in infant nutrition, was probably the best

possible corporate parent to buy Pfizer’s largely

orphaned baby formula business.

Of course, this analysis raises an obvious question. If

the environment for M&A is already favorable, why

has the pace of deal making been so slow during the

recovery from the fi nancial crisis? The chief reason in

our view is that sellers are holding back. Potential

divestors expect business valuations to increase, and

so are inclined to hold on to their assets for the time

being. But this is likely to change quickly, once sellers

come to see their assets as fully valued or once they

realize that they will be rewarded for prudent divesti-

have to grow them yourself. If the capabilities are

available, they may be candidates for acquisition.

When Comcast, the American cable TV giant,

concluded that it needed content to feed its cable

franchises, it bought NBC/Universal and the

libraries, production and news infrastructure that

came with it.

• Is the risk-adjusted rate of return higher if you

buy the capability than if you build it internally?

Every acquisition carries risks, but every investment

in organic growth also carries risks. The challenge

for companies’ fi nancial teams is to create apples-

to-apples comparisons for expected returns on

investments in organic vs. inorganic growth, fac-

toring in the risks on both sides as accurately as

possible. When Italian tire maker Pirelli wanted to

enter Russia, it concluded that buying a “brownfi eld”

plant and existing business was better than starting

from scratch in a notoriously diffi cult market for

launching a business.

Figure 3: We estimate that each of the eight macro trends will increase global GDP by at least $1 trillion, but just two account for half the expected growth

Note: All numbers rounded up to the nearest $1TSources: IMF; Euromonitor; Stockholm International Peace Research Institute Yearbook 2010; WSJ; UN; EIA; IEA; Datamonitor; Lit searches; World Bank; EIU;Bain Macro Trends Group analysis, 2011

1 2 3 4 5 6 7 8 Total

Advancedeconomiesadjustingto age

Developingeconomiescatching up

Estimated contribution of the Great Eight macro trends to increasereal (run rate) global GDP between 2010 and 2020 (forecast)

Nextbillion

consumers

Develophumancapital

Militaritizationfollowing

industrialization

Growing output ofprimaryinputs

Keepingthe wealthy

healthy

Old infra�structure, newinvestments

Everythingthe same,but nicer

Prepping forthe nextbig thing

0

10

20

$30T

10.01.0

1.0

3.02.0

4.0

5.01.0

$11T

$16T

27.0

20

The renaissance in mergers and acquisitions

Five are likely to be signifi cant:

1. The prevalence of asset bubbles. As we suggested

earlier, the number, size and duration of asset

bubbles are all likely to increase. Asset bubbles

carry three unmistakable signs: a kernel of real

opportunity followed by a rapid run-up in prices,

valuations unsupported by underlying cash fl ows

and plenty of explanations that purport to show

why “things are different this time.” Part of the

discipline of any kind of investing is recognizing

the warning signs of a bubble. Like avoiding a rip

current by swimming parallel to shore, investors

have to steer clear rather than trying to fi ght or ride

the deadly tide.

Bubble detection capabilities are important for every

company, not just financial intermediaries and

investors. The key is to separate out the factors that

drive long-term, sustainable growth from specula-

tive shorter-term infl uences. To do so, executives

tures. When a company is planning divestitures, attempts

to time the market should take a back seat to a rigorous

assessment of strategy and the highest-yielding invest-

ment priorities, a topic we examine more fully in our

article “How the best divest,” published by Harvard

Business Review in 2008.

Bubble detection capabilities areimportant for every company, not just fi nancial intermediaries and investors.

The risks

While the environment for M&A will be generally

favorable, would-be acquirers have to watch for a number

of macroeconomic risks and manage them accordingly.

Figure 4: Buy vs. build: Standing pat is not an option

Source: Bain & Company

Most companies likely to pursue a balanced strategy

Three acid questions

Does someone else have a capability that would

enhance your business?

Is the ROI higher to buy it than to

develop it internally?

Can you articulate a parenting advantage?

What to do with all that cash?

21

keep domestic consumption relatively low and

investment levels high. Because of these policies,

China will likely have excess capital for both domes-

tic and international investment; indeed, Bain’s

Macro Trends Group expects it to contribute an

estimated $87 trillion to the growth in financial

assets by 2020, more than any other single country.

This will put upward pressure on domestic Chinese

assets available for sale to foreign investors. It may

also contribute to a variety of asset bubbles.

5. Increased supply chain risk. The world has grown

comfortable—possibly too comfortable—with the

decades-long trend toward ever-longer supply chains.

In the coming years, a variety of forces may com-

bine to reverse the trend. On the macroeconomic

front, productivity is increasing and the labor-cost

gap between developed and developing nations is

shrinking. On the microeconomic side, companies

are beginning to realize better returns from locating

production closer to consumer markets. Add in the

increased militarization of some Asian nations,

and you have several forces that may send the supply

chain trend in the opposite direction. The risk for

would-be acquirers, of course, is buying production

assets in faraway places just as the world is moving

in the opposite direction.

While M&A is a good strategy for most companies,

it is not easy or simple. The companies best positioned

to work through the issues described above in a disci-

plined manner are those with deep experience in M&A.

In Part III of this series, we return to our theme of the

virtues of a repeatable M&A model for success, which

we will lay out in further detail.

need deep knowledge of a business’s fundamentals

and its interaction with the broader environment.

In the recent US housing bubble, for instance,

homebuilders could have examined the demo-

graphics of the population and trends in income

growth. The widening gulf between income and

population growth (on the one hand) and the

market value of housing (on the other) was a clear

signal of an emerging bubble. The bigger, broader

and longer-lasting bubbles produced by abundant

capital may lead companies to assume that a two-

year or even three-year trend is real and permanent.

Businesses may then deploy real resources only

to have the bottom fall out before they can grace-

fully exit their position. The effects can quickly

become catastrophic.

2. Currency volatility. Currency is one of the largest

traded commodities in the world. It is subject

both to massive intervention by governments and

to long-term structural forces that alter its value

relative to other currencies and to underlying

baskets of goods and services. Every company’s

deal modeling should reflect both upside and

downside currency scenarios.

3. Captured cash. Though the world is awash in

capital, a large fraction may not be accessible to

home-market companies because of tax policies

and currency controls. This can lead to the odd

phenomenon of companies with signifi cant cash

on the balance sheet needing to borrow to complete

transactions or even to pay dividends. JPMorgan

Chase, which studied 600 US companies that

break out how much cash they hold overseas,

notes that foreign holdings represent about 60%

of these companies’ cash, much of it in US dollars.

Some companies have resorted to setting up listed

overseas affi liates to better use the captured cash

and tap into local liquidity. According to the same

bank, 50% of recent listings in Hong Kong have

been by overseas companies.

4. China as an exporter of capital. The Chinese gov-

ernment has deliberately pursued policies that

3. The renaissance in mergers and acquisitions: How to make your deals successful By David Harding, Richard Jackson and Phil Leung

Many leading companies have created a repeatable M&A capability and then turbo-charged their growth through a series of acquisitions. What all these acquirers have in common is sustained institutional invest-ment in this capability, much as if they were building a marketing or manufacturing func-tion from scratch.

How to make your deals successful

25

If you set out to build a globe-spanning, market-leading

beer company, you might not pick Johannesburg (South

Africa) or São Paulo (Brazil) as the launching pad. Yet

those two cities are exactly where the world’s two largest

brewers, SABMiller and Anheuser-Busch InBev, got

their start. The two companies have grown from mod-

est origins to world-straddling giants, with about 30%

of the global beer market between them.

The remarkable trajectories of these two businesses

hold a number of lessons. One is the fast-growing pres-

ence of companies from emerging markets. Another is

the power of cross-border acquisitions, and not just in

the direction of developed to developing countries. But

perhaps the most compelling lesson lies in how the

two companies achieved their current positions. Both

arrived where they are today using similar business

models: a repeatable method of mergers and acquisi-

tions (M&A) supported by a disciplined management

system. SABMiller, for instance, branched out from its

South African home into other African nations, Europe,

India, Latin America, the US and China—all by acquir-

ing local brewers.

In a world of superabundant capital, low interest rates and high investor expectations, M&A is one of the best tools available to companies to help them hit their growth targets.

In many ways, the two companies’ approach represents

the new normal for high-performing companies. Bain

has long tracked the activities of what we call sustained

value creators (SVCs)—companies that increase reve-

nue and earnings at least 5.5% a year over an 11-year

period, such as 2000 to 2010, while earning their cost

of capital. Our study of mergers and acquisitions dur-

ing this time frame showed that 9 out of 10 SVCs were

active in the deal market, and companies in this group

were more than twice as likely as other companies to

derive at least 75% of their market cap from M&A. That

fact is consistent with the broader fi ndings outlined in

Part I of this series, which show that frequent material

acquirers earn higher returns than bystanders. The use

of M&A, moreover, is likely to grow. In a world of super-

abundant capital, low interest rates and high investor

expectations, M&A is one of the best tools available to

companies to help them hit their growth targets, as we

detailed in Part II of the series.

If you agree that M&A creates shareholder value and

that the deal-making environment is likely to be favor-

able for some time to come, you can turn your attention

to three important questions:

• First, how can you tell when a prospective transaction

is a good one for your company? Most companies

will have many likely candidates; the challenge is

to fi nd the right deal for your business.

• Second, should you be looking for scale deals or

scope deals? As we’ll see, the balance between the

two depends partly on your experience in M&A.

• Third, how can you create a repeatable model for

M&A success? As SABMiller and Anheuser-Busch

InBev have learned, along with many others, the

“virtuous circle of M&A repeatability” requires a

signifi cant investment in training, culture and ana-

lytics. But the rewards are also substantial.

How do you recognize a good deal for your company?

A merger or an acquisition can succeed if and only if

it supports your company’s strategy.

Strategy defi nes how you realize your ambition for the

company (see Figure 1). A company needs to deter-

mine the markets in which it will compete. It must

develop the differentiated capabilities that enable it to

outperform the competition. Most often, winning strat-

egies aim to create leadership economics. Market leaders

generally have lower costs than their competitors. They

often enjoy greater pricing power, brand recognition

and differentiation. These advantages translate into

26

The renaissance in mergers and acquisitions

it may be perfect in another’s, thanks to what is known

as parenting advantage. Volkswagen, for example, has

acquired several auto manufacturers, including SEAT,

Skoda, Bentley and Porsche, and has added value to the

acquisitions through cross-brand technologies, such as

its new modular transverse matrix. The matrix allows

the company to use common platforms for several dif-

ferent brands, reducing both cost and production time.

For many acquirers, viewing a deal through the lens of scale vs. scope yields critical insights about the long-term value of a potential acquisition.

There are several other questions to ask about a merger

or an acquisition prospect, including the predictability

better performance. Measured by return on capital, for

instance, leaders typically outperform followers by a

factor of two.

If an acquisition can help your company attain a lead-

ership position in its markets, it may be a good deal.

Nestlé’s acquisition of Pfi zer’s infant nutrition busi-

ness, for example, greatly improved the acquirer’s mar-

ket position in a number of strategic Asian markets,

including China, Indonesia, the Philippines and Thai-

land. The deal helped Nestlé take an already strong

infant formula business and consolidate its leading

position worldwide.

Another defi ning characteristic of a good deal: It pro-

vides you with critical capabilities that plug a gap or

address a weakness in your existing business. An acqui-

sition can strengthen or extend your product portfolio.

It can open up new geographic regions, customer groups

and distribution channels. It can provide you with supply

chain assets or access to proprietary research. While a

business may not fi t well in one company’s portfolio,

Figure 1: Strategy refl ects your choices about where to play and how to win

Priorities

Road map to deliver results

Ambition

Whereto play

How towin

Source: Bain & Company

How to make your deals successful

27

Today, the verdict is in. Inexperienced acquirers tend to

focus mainly on scale deals, those that improve or con-

solidate their position in a given market. Experienced

acquirers average a 50-50 mix of scale and scope deals,

improving their market positions while also adding

product lines, geographic reach or other important

capabilities. Figure 2 highlights that contrast: It com-

pares what we call “Mountain Climbers”—frequent

acquirers whose acquisitions amount to at least 75% of

their market cap—with “Large Bets,” companies mak-

ing occasional big acquisitions. A recent Bain survey

shows how much more confident these experienced

acquirers are: Asked about moving into an adjacent

market, 73% felt that M&A was likely to be as success-

ful or more successful than building a business from

scratch. Only 55% of inexperienced acquirers felt the

same way. And it is the experienced acquirers, as our

research shows, that usually turn in the best results.

Different patterns of risk and reward accompany each

kind of deal. Scale deals, historically, have put cost

of the target’s cash fl ows and how the market views the

asset. (See the sidebar, “What makes an asset worth buy-

ing? A checklist.”) Your own company’s situation affects

the answers, however, because a deal that makes sense

for a strong company may not have good odds of success

for a weaker one. Financially healthy companies can

afford the time required for careful due diligence. They

can invest more in successful post-merger integration.

Scale or scope?

For many acquirers, viewing a deal through the lens of

scale vs. scope yields critical insights about the long-

term value of a potential acquisition. Scale deals involve

a high degree of business overlap between the target

and acquirer, fueling a company’s expansion in its ex-

isting business. In scope deals, the target is a related

but distinct business, enabling an acquirer to enter a

new market, product line or channel. Both can be use-

ful—and “scale vs. scope” has been a great debate in

the M&A world.

What makes an asset worth buying? A checklist

Though M&A is a part of most winning companies’ success, disciplined acquirers pursue only those deals that satisfy a list of key strategic criteria. A typical list includes questions like these:

• Can the asset generate leadership economics—that is, returns above the industry average due to superior costs, customers, capabilities or leverage?

• How predictable are the cash fl ows, and how are you discounting potential variability of return (risk)?

• What is the conventional wisdom associated with the asset? Where is that conventional wisdom wrong? How does that infl uence the price?

• What must you believe to be true to capture cost and revenue synergies?

• What is the option value that owning the business generates?

• What is your parenting advantage, and how will you manage the business?

• How will the market react to the announcement of the acquisition?

28

The renaissance in mergers and acquisitions

What the most successful acquirers have in common is sustained institutional investment in an M&A capability, much as if you were building a marketing or manufacturing function from scratch.

SABMiller illustrates the advantages of experience, par-

ticularly in cross-border deals. The company has moved

into more than 30 countries in the last 20 years, in

nearly every case by acquiring local brands. It main-

tains and develops these brands, refl ecting the industry

axiom that all beer is local. (“You can’t be a real country

unless you have a beer and an airline,” declared the late

rocker Frank Zappa, a quote SABMiller used in a 2013

presentation highlighting its broad portfolio of brands.)

At the same time it has created a disciplined business

synergies at the top of the deal thesis: If we buy this

company, we will have a larger presence in the market and

realize greater economies of scale. The risk is that the acquirer

winds up creating a slow-moving behemoth and the

synergies never materialize. Scope deals, by contrast,

usually put growth at the top of the deal thesis: Buying

this company gives us access to new and faster-growing

markets. The risk here is that the acquirer will stumble

as it learns to manage an unfamiliar business. Because

of the intrinsic differences between scale deals and scope

deals, every element of the deal cycle, from strategy

through integration, has to be managed differently. Scale

deals succeed on the basis of rapid overall integration,

capture of cost synergies and full cultural integration.

Scope deals succeed when the acquirer preserves the

unique attributes of the company it has just bought,

integrating the two only where it matters—and when

the two businesses begin to cross-pollinate, creating

platforms for future growth. As an acquiring company

becomes more experienced, it learns the differences

between scale and scope deals, and can thereby manage

the risks and maximize the benefi ts.

Figure 2: Almost half the deals done by “Mountain Climbers” are scope deals

Note: Analysis of deals valued at more than $250 million by 194 companies classified as “Mountain Climbers” (n=117) and “Large Bets” (n=77) from 2000–2010Sources: Bain M&A study 2012; Dealogic; Thomson; Bain SVC database 2011; Bain analysis

0

20

40

60

80

100%

Percentage of deals by primary deal rationale

Large Bets

Scale78%

Scope22%

124

Mountain Climbers

Scale54%

Scope46%

388

How to make your deals successful

29

services. Its business development offi ce ensures

a strong, ongoing connection between M&A and

strategy, linking the company’s accumulated deal-

making experience to strategic decisions. The offi ce

asks three critical questions about each potential

acquisition: Does it build on or extend a capability

IBM already has? Does it have scalable intellectual

property? Can it take advantage of our reach into

170 countries?

IBM’s offi ce is also responsible for working with

M&A service providers and maintaining liaisons

with business units. It also measures and tracks

the results of each deal, essentially creating an M&A

learning organization.

2. Accountability for new business activity lodged with

the business units. Business units can come to cor-

porate with ideas for deals, but they must own the

process of managing the business. At Illinois Tool

Works, a diversifi ed manufacturer that routinely

buys small and medium-sized companies to expand

its operations, business unit leaders are tasked with

identifying new M&A opportunities to pursue in

their respective business lines. In recent years, for

example, the company built its car-care business

group with acquisitions of a number of brands of

car wash, wax and other maintenance products.

3. A commitment to differentiated due diligence.

Many companies don’t start due diligence on an

acquisition target until they receive an offering

memorandum from an investment bank. H.J. Heinz

takes a different approach. On key strategic areas,

the company systematically assesses potential ac-

quisitions before they are actively shopped. That

way, executives have a sophisticated point of view

on the asset’s value when it comes on the market.

Heinz’s disciplined process leads to a higher per-

centage of proprietary deals. The company also

establishes a fi rm walk-away price for each prospec-

tive deal, and it plans post-merger integration from

the beginning. Heinz’s due diligence is linked to

its deal thesis at all times, which helps to maintain

discipline during the entire process.

system that enables it to add value to each acquisition.

Global procurement and shared brewing techniques

reduce cost. An innovation tool called SmartGate facil-

itates the introduction of new products in each market.

Eight cooperatively developed “SABMiller Ways” defi ne

best practices in marketing, brand management, talent

development and other facets of the business, and are

rigorously applied to local operations.1

Anheuser-Busch InBev, which traces its managerial

origins to a small Brazilian brewer, incorporates similar

disciplines and has been equally successful with its M&A

strategy. The two companies have become experts at

what are essentially scope deals, because most moves

into a new country are likely to involve new value prop-

ositions, new supply chains, new distribution channels

and so on. No coincidence, both companies have re-

markable records of profi table growth.

Building a repeatable M&A capability

The brewers are hardly alone. Many leading companies

have created a repeatable M&A capability and then turbo-

charged their growth through a series of acquisitions.

What all these acquirers have in common is sustained

institutional investment in this capability, much as if

they were building a marketing or manufacturing func-

tion from scratch.

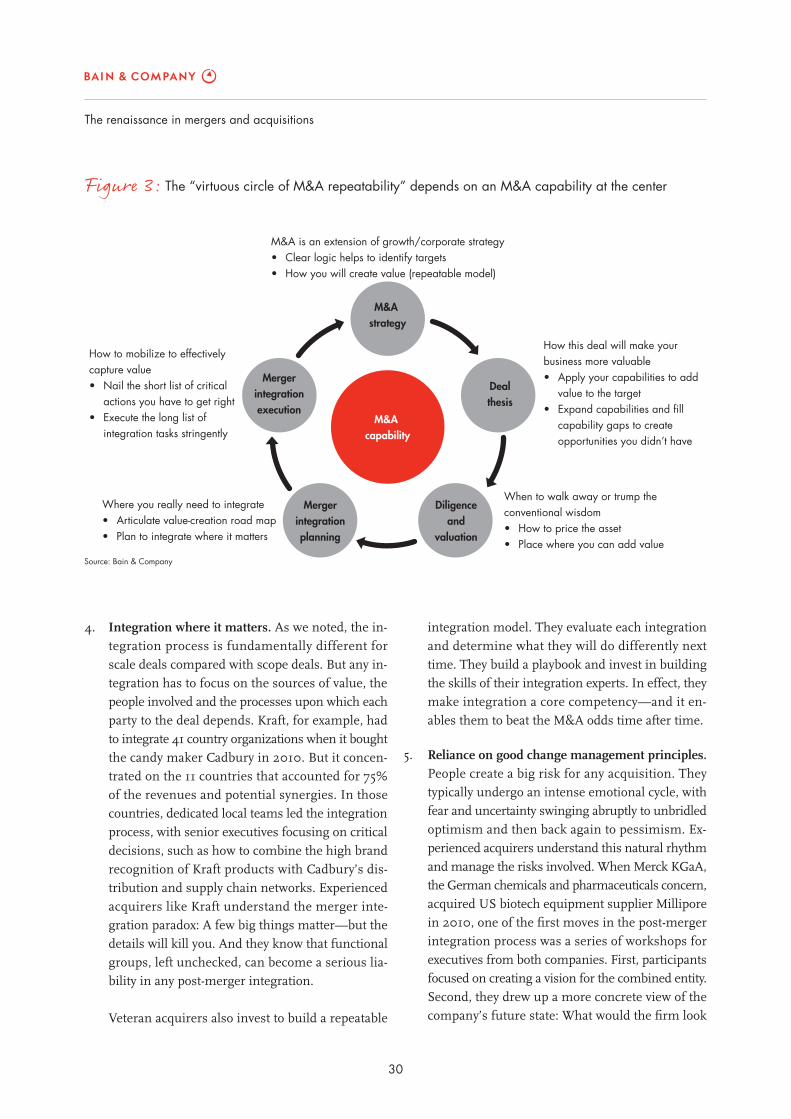

One way of picturing the capability is to think of the

acquisition process as a cycle of steps repeated with

each deal—a virtuous cycle of M&A repeatability, so to

speak (see Figure 3). The key for the purposes of this

article is the red circle in the middle of the figure,

without which the other steps are more likely to fail.

Let’s look at the elements a company must put in place

if it wants to build this kind of M&A capability:

1. A strong business development offi ce at the center,

typically with close links to the company’s strategy

group, CEO and board. IBM’s offi ce is a great ex-

ample. The company has completed more than

140 deals since 2000, acquisitions that played an

important role in redirecting the company’s busi-

ness toward higher-value, more profi table technol-

ogies and market opportunities in software and

30

The renaissance in mergers and acquisitions

integration model. They evaluate each integration

and determine what they will do differently next

time. They build a playbook and invest in building

the skills of their integration experts. In effect, they

make integration a core competency—and it en-

ables them to beat the M&A odds time after time.

5. Reliance on good change management principles.

People create a big risk for any acquisition. They

typically undergo an intense emotional cycle, with

fear and uncertainty swinging abruptly to unbridled

optimism and then back again to pessimism. Ex-

perienced acquirers understand this natural rhythm

and manage the risks involved. When Merck KGaA,

the German chemicals and pharmaceuticals concern,

acquired US biotech equipment supplier Millipore

in 2010, one of the fi rst moves in the post-merger

integration process was a series of workshops for

executives from both companies. First, participants

focused on creating a vision for the combined entity.

Second, they drew up a more concrete view of the

company’s future state: What would the fi rm look

4. Integration where it matters. As we noted, the in-

tegration process is fundamentally different for

scale deals compared with scope deals. But any in-

tegration has to focus on the sources of value, the

people involved and the processes upon which each

party to the deal depends. Kraft, for example, had

to integrate 41 country organizations when it bought

the candy maker Cadbury in 2010. But it concen-

trated on the 11 countries that accounted for 75%

of the revenues and potential synergies. In those

countries, dedicated local teams led the integration

process, with senior executives focusing on critical

decisions, such as how to combine the high brand

recognition of Kraft products with Cadbury’s dis-

tribution and supply chain networks. Experienced

acquirers like Kraft understand the merger inte-

gration paradox: A few big things matter—but the

details will kill you. And they know that functional

groups, left unchecked, can become a serious lia-

bility in any post-merger integration.

Veteran acquirers also invest to build a repeatable

Figure 3: The “virtuous circle of M&A repeatability” depends on an M&A capability at the center

Source: Bain & Company

M&A is an extension of growth/corporate strategy• Clear logic helps to identify targets • How you will create value (repeatable model)

How to mobilize to effectivelycapture value• Nail the short list of critical actions you have to get right• Execute the long list of integration tasks stringently

M&A capability

M&A strategy

Dealthesis

Mergerintegrationexecution

Diligenceand

valuation

Mergerintegrationplanning

How this deal will make yourbusiness more valuable• Apply your capabilities to add value to the target• Expand capabilities and fill capability gaps to create opportunities you didn’t have

Where you really need to integrate• Articulate value-creation road map• Plan to integrate where it matters

When to walk away or trump theconventional wisdom• How to price the asset• Place where you can add value

How to make your deals successful

31

Looking ahead

Our three-part analysis of M&A points to a few key insights.

One is this: You ignore deal making at your peril. Com-

panies that did no acquisitions between 2000 and 2010

turned in poorer performance than the deal makers.

The more deals a company did, and the more material

those deals were, the better its performance was likely

to be.

A second conclusion is that the business environment

has rarely been more favorable for M&A. Capital is

superabundant and interest rates are low. The world

economy abounds with big opportunities. Buying into

a market is often a company’s best tool for tapping into

that growth potential.

The third conclusion—the subject of this article—is that

M&A winners develop a repeatable model. They can do

one deal after another and integrate each one success-

fully because they have created the necessary capability

in their organizations. SABMiller and Anheuser-Busch

InBev show what’s possible: Both companies launched

their business in relatively small developing markets,

and then expanded into one country after another.

Today they straddle the globe.

Not every company has what it takes to pursue M&A

successfully. The best have a deep understanding of their

strategy and begin from a position of strength. They

commit to developing a repeatable model, and they make

the necessary investments. Their reward, as we have

seen, is growth—in revenue, earnings and total share-

holder return—that far outstrips the competition.

like fi ve years down the road? Third, they defi ned

the initiatives required to achieve full potential.

When the vision, the future state and the fi rm’s full

potential are crafted with full participation by all

members of the leadership team, the odds of suc-

cess increase dramatically.

These fi ve components are the building blocks of a re-

peatable M&A model that can foster steady, profi table

growth. It’s been a successful formula for Godrej Con-

sumer Products, the India-based maker of household

and personal-care items. Recognizing that M&A was

essential to its global growth goals, the company pre-

pared for two years before setting foot in the deal mar-

ket. It assembled a strong M&A team. It developed a

playbook that included a rigorous screening process to

identify appropriate acquisition candidates. It followed

a disciplined M&A approach based on a strong under-

standing of each market, a robust deal thesis and det-

ailed due diligence. Godrej focuses on emerging market

deals and just three categories of products (household

insecticides, hair color and personal cleanliness). It targets

companies with leading positions in their markets,

knows how it expects to create value from each deal

and takes a tailored approach to integration. The company’s

11 acquisitions outside India since 2005 include large

deals such as Megasari, Indonesia’s second-biggest

household insecticides company.

This disciplined M&A strategy contributed to Godrej’s

consistently strong performance between 2002 and 2012:

sales growth averaging 27% a year and earnings growth

averaging 33%. The share price rose 42% over the same

period, outperforming peers and resulting in a more than

45-fold increase in the company’s market capitalization.

1 See SABMiller Annual Report 2008, http://www.sabmiller.com/fi les/reports/ar2008/2008_annual_report.pdf