the report of foreign bank and financial accounts: tough new

TRANSCRIPT

CLICK ON EACH FILE IN THE LEFT HAND COLUMN TO SEE INDIVIDUAL PRESENTATIONS.

If no column is present: click Bookmarks or Pages on the left side of the window.

If no icons are present: Click View, select Navigational Panels, and chose either Bookmarks or Pages.

If you need assistance or to register for the audio portion, please call Strafford customer service at 800-926-7926 ext. 10

The Report of Foreign Bank and Financial Accounts: Tough New RequirementsPreparing for FBAR's Increased Data Demands on

More Businesses and Investorspresents

Today's panel features:Brent Lipschultz, Principal, Personal Wealth Advisors Practice Group, Eisner, New York

Thomas Sykes, Partner, McDermott Will & Emery, Chicago

Thursday, November 5, 2009

The conference begins at:1 pm Eastern12 pm Central

11 am Mountain10 am Pacific

A Live 110-Minute Teleconference/Webinar with Interactive Q&A

For CLE purposes, please let us know how many people are listening at your location by

• closing the notification box, • clicking the chat button in the upper

right corner, • and typing in the chat box your

company name and the number of attendees.

• Then click send.

The Report Of Foreign Bank and Financial Accounts: Tough New

Requirements Webinar

Nov. 5, 2009

Brent Lipschultz Thomas Sykes Eisner LLP McDermott Will & Emery [email protected] [email protected]

2

Today’s Program

• Review Of Changes To Form TD F 90.22-1, slides 3 through 24 (Brent Lipschultz and Thomas Sykes)

• IRS FBAR Enforcement So Far, slides 25 through 26 (Brent Lipschultzand Thomas Sykes)

• Emerging FBAR Issues To Date, slides 27 through 35 (Thomas Sykes and Brent Lipschultz)

• Future Legislation, slides 36 through 39 (Brent Lipschultz)

3

Review Of Changes To Form TD F 90.22-1

4

FBAR Overview

4

• FBAR (Form TD F 90-22.1) is a Treasury annual report under USC Title 31, the Bank Secrecy Act of 1970 (the “BSA”). BSA addressed concerns that U.S. persons were using foreign bank secrecy laws to conceal illegal activities

• Since FBAR is not a tax return, Tax Court has no jurisdiction over FBAR penalties (Williams, 131 TC No. 6 (10/2/08))

FBAR report is in addition to a taxpayer’s obligation to indicate the existence of a foreign account on:

Form 1040, Schedule B, Part IIIForm 1041, Schedule GForm 1065, Schedule BForm 1120, Schedule N, Question 6

5

Authority To Administer FBAR

• FinCen delegated its authority to enforce the FBAR to the IRS in 2003, reflecting the fact that a major purpose of the FBAR was to identify potential tax evasion

• The IRS can investigate FBAR non-compliance, and assess and collect civil penalties for failure to comply

• The authority delegated to the IRS included the authority to revise Form 90-22.1 and instructions

• Currently, the IRS is set to release a publication in early December clarifying the rules, and has a regulation projection

5

6

Who Must File FBAR?

Any U.S. person who has a financial interest or signature authority over foreign financial accounts with an aggregate value exceeding $10,000 at any time during the year must file an FBAR for such year

A person or required to file an FBAR also must check the appropriate box of his tax return

6

77

Key Changes To Form TD F 90.22-1

– Requirement for persons in or doing business in U.S. to file FBAR– “Doing business” standard delayed

• IRS guidance forthcoming– Expanded definition of reportable financial accounts– Expanded definition of “financial interest” through ownership in

corporations, partnerships or trusts– Expanded definition of “covered trusts”– Broadened standards for who holds signatory authority over foreign

accounts– Expanded list of domestic corporation officers and employees who are

exempt from filing requirement

8

“U.S. Person,” For FBAR Purposes• Prior to 2008, a “U.S. person” was:

– A U.S. citizen or resident; or– Any domestic legal entity such as a partnership, corporation, estate

or trust

• Pursuant to the revised FBAR (October 2008), a “U.S. person” is:– A U.S. citizen or resident (including entities); or– A person in and doing business in the U.S. – Review of U.S. person definition in Internal Revenue Manual (July

2008)

• Revised definition is significantly expanded, with guidance lacking regarding the “in and doing business” standard

8

9

“U.S. Person,” For FBAR Purposes (Cont.)

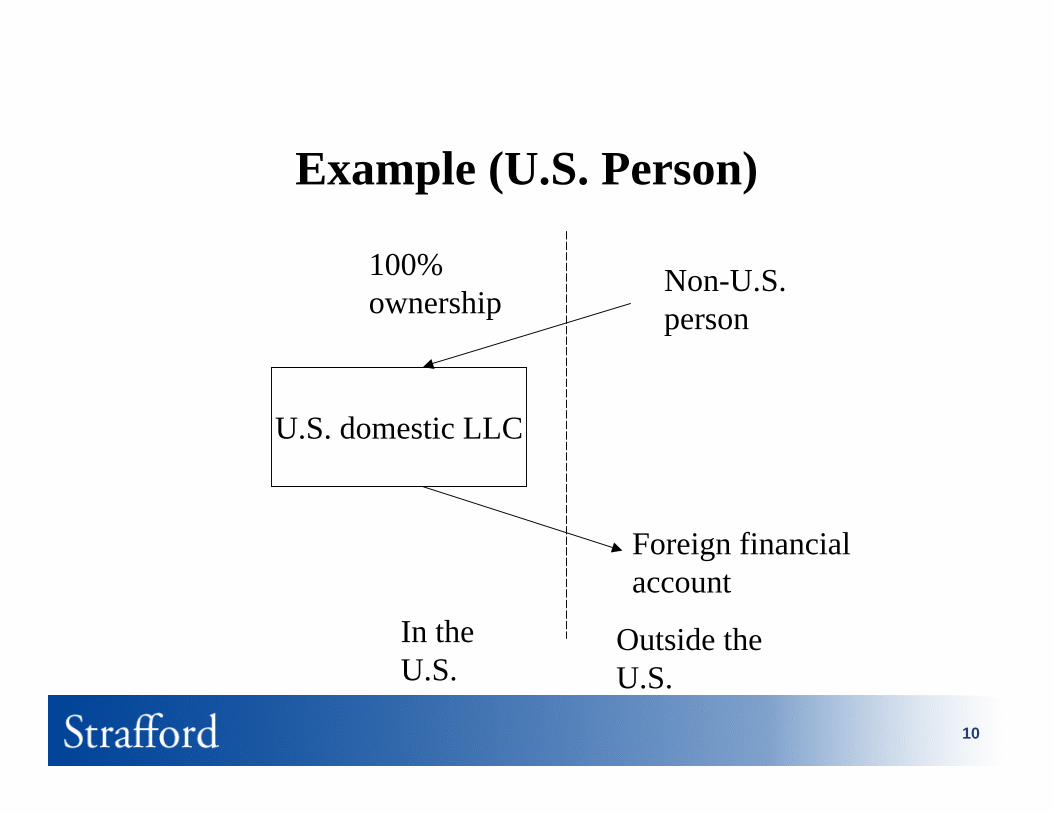

Must a single member LLC file an FBAR? FAQ 8 (6/29/09) reads:

• Q. Is a single member LLC, which is a disregarded entity for US tax purposes, a United States person for FBAR purposes?

A. Yes, the tax rules concerning disregarded entities do not apply with respect to the FBAR reporting requirement. FBARs are required under Title 31, not under any provision of the Internal Revenue Code.

9

10

a. US Person (cont.)

U.S. domestic LLC

In the U.S.

Outside the U.S.

Non-U.S. person

100% ownership

Foreign financial account

Example (U.S. Person)

11

Key Changes To Form TD F 90.22-1“In and Doing Business in U.S.”

• Based on an analysis of the facts and circumstances of each case• A person is not considered to be in and doing business in the U.S. unless that

person is conducting business within the U.S. on a regular and continuousbasis

• Persons who “sporadically conduct business in the United States” are not in and doing business in the U.S.

• The following examples of persons who are not considered to be in and doing business in the U.S. are included in IRS guidance issued in February – Non-resident aliens (NRAs) who are engaged in a business but only

occasionally visit the U.S. to meet customers or business associates– NRA artists, athletes and entertainers who only occasionally come to the

U.S. to participate in exhibits, sporting events or performances; and– NRAs who visit the U.S. to manage their personal investments, such as

rental property, and conduct no other business in the U.S.– Announcement 2009-51 provides that all persons may rely on the

definition of U.S. person found in the 2000 instructions and for filings in 2010 added “a person in and doing business in the United States”

11

12

“Foreign” Foreign” financial accounts

A “foreign” financial account is one maintained outside the U.S.

The geographical location of the account, not the nationality of the financial institution, determines whether an account is “foreign”

A financial account with a non-U.S. branch of a U.S. bank or other U.S. financial institution is “foreign”

A financial account with a U.S. office of a foreign bank or other foreign institution is a U.S. account

An insurance policy is foreign if issued by a non-U.S. office of insurer

– Examples:• Royal Bank of Canada in New York – no • Citibank in Toronto – FBAR requirement • U.S. mutual fund with foreign investments – no FBAR requirement• Foreign mutual fund with all U.S. investments – FBAR requirement

12

13

What Is A Financial Account?• A “financial account” includes a bank, securities, derivatives or other financial

instrument account, including any savings, demand, checking, deposit, time deposit, debt card and prepaid credit card account. Safe deposit boxes are not financial accounts unless the institution provides services

• Individual bonds, notes or stock certificates held by the filer, however, are not financial accounts; nor is an unsecured loan to a foreign trade or business that is not a financial institution

• “Financial account” is any “account in which the assets are held in a commingled fund, and the account owner holds an equity interest in the fund (including mutual funds)”

• IRS view is that a cash surrender value insurance policy is a financial account, and thus if the policy is “foreign” and the value exceeds $10,000, must be reported

13

14

“Commingled Fund”- The Controversy IRS official's position (IRS FBAR Forum 06/12/09) is that a foreign hedge

fund (and a foreign feeder or private equity fund) is a foreign “financial account” 2009 TNT 122-3 (06/29/09)

IRS official said IRS position was always that FBARs were required to be filed for foreign hedge funds (WSJ, 06/25/09), which raises prior-year non-compliance issues

Under IRS official's stated position, FBARs apparently must be filed by:

−U.S. owners of foreign hedge funds

−U.S. managers of foreign hedge funds and their U.S. employees with authority; and

−U.S. institutions (and their U.S. employees) that have authorityover foreign hedge funds of their clients

14

15

What Is A Financial Interest?

A person has a financial interest in a foreign financial account if:

Such person is the owner of record of, or has legal title to, the account

The owner of record or holder of legal title is acting as an agent, nominee or attorney, or in some other capacity, on behalf of such person; or

Such person is deemed to have a financial interest by attributionfrom a corporation, partnership or trust

15

16

Financial Interest Through Company A person has a financial interest in a foreign financial account by

attribution from a corporation, if such person owns directly or indirectly more than 50% of the value or vote of a corporation that owns the foreign financial account

Thus, if A, a U.S. person, owns 51% of B, a U.S. corporation with a foreign financial account, both A and B must report the (same) account

Similarly, if A, a U.S. person, wholly owns B, a foreign corporation (i.e., it is a “CFC”), and B has a foreign financial account, A must report the account on his FBAR

16

17

Financial Interest Through Partnership

A person has a financial interest in a foreign financial account by attribution from a partnership, if such person owns an interest in more than 50% of the profits or capital of a partnership that owns the foreign financial account

Profits are defined as the distributive share of partnership income, taking into account any special allocations

Like the corporate attribution rules, the partnership attribution rules require a U.S. partnership and a 50%-plus partner to trigger reporting by the partner of the partnership’s foreign financial account

17

18

Financial Interest Through Trust A person has a financial interest in a foreign financial account by

attribution from a trust that owns the account if such person (1) has a present beneficial interest, directly or indirectly, in more than 50% of the assets of that trust; or (2) receives more than 50% of the trust’s current income

Under this rule, certain actual or potential U.S. beneficiaries of a U.S. or foreign trust may be required to file an FBAR reporting the trust’s foreign financial accounts

IRS official’s position is that a beneficiary who can receive 50+% of the income or assets should file an FBAR (6/12/09 IRS FBAR Forum)

18

19

Financial Interest Through Trust (Cont.)

A person can also have a financial interest in a foreign financial account by attribution from a trust if:

Such person established a trust that actually or beneficially owns the foreign financial account; and

A “trust protector” has been appointed

A trust protector is a person who is responsible for monitoring the activities of a trustee, with the authority to influence the decisions of the trustee or to replace, or recommend the replacement of, the trustee

19

20

What Is “Signature Or Other Authority”

• A person has “signature authority” over an account if such person can control the disposition of money or other property in it by delivery of a document containing his or her signature (or his or her signature and that of one or more other persons) to the bank or other person with whom the account is maintained

• Other authority” over an account exists when a person can exercise comparable power over an account by oral or some other means of communication, either directly or through an agent, nominee, attorney or other person in similar capacity, to the bank or other person with whom the account is maintained

In the IRS 06/12/09 FBAR Forum, the “other authority” was described as including a substance-over-form standard

20

21

Exceptions To Filing FBAR

• NRAs

• If foreign account is in a U.S. military facility or operated by U.S. institution for the military

• Officers/employees of publicly U.S. corporations, or which has more than $10M and at least 500 SHs, if no personal financial interest, and receives letter from chief financial officer stating that the corporation has complied.

• Officers/employees of federally-regulated bank, if no personal financial interest

21

22

FBAR Filing Deadlines

• Filing deadlines– Brief history of original deadlines and changes along the way– IRS Announcement 2009- 62: Current June 30, 2010 extension for

U.S. persons with only signature authority over foreign financial accounts, and U.S. persons with beneficial ownership of foreign comingled funds

• Does this extend to U.S. persons who have owned hedge funds for the last six years?

• Expect IRS guidance first week of December 2009• IRS regulation project in progress

22

23

Is Information On FBAR Confidential?

Information provided on an FBAR may be provided to the officers and employees of any constituent unit of the Department of the Treasury who have a need for the records in the performance of their duties

The information also may be referred to any other department or agency of the U.S. upon the request of the head of such department or agency for use in a criminal, tax or regulatory investigation orproceeding

The information collected may also be provided to appropriate state, local and law enforcement and regulatory personnel in the performance of their official duties. Disclosure of this information is mandatory

By contrast, dissemination of information on a tax return is strictly limited. See IRC § 6103

23

24

FBAR- Penalty Regime Non-willful noncompliance:

Civil penalties of up to $10,000 for each violation, absent reasonable cause.

• Willful non-compliance

Civil penalties of up to the greater of $100,000 or 50% of the account value for each violation per person

Criminal penalties are up to a $250,000 fine and a five-year prison term, although under certain circumstances, it can be 10 years and up to a $500,000 fine

The IRS has the burden of proving willfulness

However, the Administration proposes (in the Green Book) certain rebuttable presumptions for civil proceedings, including that generally a failure to report an account would be presumed to be willful if that account exceeds $200,000 during the year and is held with a certain intermediary that is not required to report information with respect to U.S. account holders

24

25

IRS FBAR Enforcement So Far

2626

IRS FBAR Enforcement To Date

• Slow pace of handling forms filed so far• Extra auditors and compliance staff assigned to international• IRM penalty guidelines of July 2008 and applicability to quiet filings• Penalty structure: How FBAR penalty is determined, assessed and

collected (statute of limitations, JB Williams and Simonelli cases)• Too early to tell how IRS investigations will proceed from voluntary

disclosures though inconsistent penalty application apparent• Does an income tax examination automatically include an FBAR

examination?• May an FBAR violation be referred to criminal investigation?• What is the difference between “willfulness” used in a criminal

context, and in a civil context?

27

Emerging FBAR Issues To Date

2828

Hot Topics: Voluntary Disclosure And Voluntary Compliance

• Proper protocol if a taxpayer has already filed an FBAR and later discovers another account

– If so, need to consider filing an amended FBAR, using the 2008 tax form– If account relates to another year, use 2008 FBAR and that year’s

instructions• Suppose the taxpayer has unreported income

– If the taxpayer hasn’t filed an FBAR, taxpayer is outside the scope of the IRS voluntary compliance initiative

– Taxpayer would want to consider hiring legal counsel to evaluate whether taxpayer would come in through normal voluntary compliance process

2929

Hot Topics: Voluntary Disclosure And Voluntary Compliance (Cont.)

• Representing amnesty non-participants that instead came forward with “quiet” or “noisy” filing

– Cover letter– IRM Guidelines (July 1, 2008)

30

• Conflicts of interest among family members involved with unreported account, and with differing levels of involvement or culpability. One way to come in now under the normal protocol is the voluntary compliance process– Suppose some family members want to come in but others don’t– A conflict is likely to arise

• Disclosure

• Address in engagement letter

Hot Topics: Voluntary Disclosure And Voluntary Compliance (Cont.)

31

• Innocent spouse relief– Tax– FBAR penalties -- reasonable cause

Hot Topics: Voluntary Disclosure And Voluntary Compliance (Cont.)

3232

Hot Topics: Voluntary Disclosure And Voluntary Compliance (Cont.)

• Need for criminal counsel if IRS investigates taxpayers that made filings outside “amnesty” program

3333

Hot Topics: Voluntary Disclosure And Voluntary Compliance (Cont.)

• Practical difficulties with future proceedings on non-filers that came forward under now-closed amnesty– Retrieval of records from offshore financial institution– Records needed to determine both (a) highest balances and (b)

income earned

34

Hot Topics: Voluntary Disclosure And Voluntary Compliance (Cont.)

• What is happening after one has submitted voluntary disclosure– Government information document request– Obtaining account records from foreign banks– Inconsistent penalty treatment is prevalent

3535

Hot Topics For Taxpayers, Advisors With FBAR – Bank Secrecy And

Offshore Tax Havens• Future of offshore tax havens, given that piercing has occurred• Exchange of information agreements

– Increased information-sharing among tax authorities• 84 OECD and non-OECD countries have implemented transparency and

effective exchange of information standards.• 3,600 bilateral tax conventions currently in force; 1,700 include provisions

that permit information exchange• 50 tax information exchange agreements are signed or in force

• Treasury announced tax information exchange agreement between U.S. and Monaco in September 2009

• Similar agreements reached with Gibraltar and Luxembourg (May 20, 2009)• Luxembourg agreement is the first one entered into by Luxembourg with an OECD

country that meets OECD standards for information exchange• U.S.-Swiss tax treaty to be amended to provide for increased exchange of tax

information• New tax information exchange agreement between U.K. and Liechtenstein announced

on Aug. 11, 2009

36

Future Legislation

3737

Foreign Account Tax Compliance Act Of 2009

• The Foreign Account Tax Compliance Act of 2009 (H.R. 3933, S. 1934), introduced in the House by Ways and Means Committee Chair Charles B. Rangel, D-N.Y., and in the Senate by Finance Committee Chair Max Baucus, D-Mont., would impose significant tax withholding penalties on foreign financial institutions that do not disclose holdings by U.S. individuals or firms and would create several new information-reporting requirements. According to the Joint Committee on Taxation, the legislation would raise $8.5 billion over 10 years

• Could likely be tacked on to an extenders bill or potentially the Health Care Bill

• Treasury Secretary Timothy Geithner endorsed the measure, saying in a release that it “fits well into the Administration’s dual-track strategy of improving our domestic tax laws while increasing global cooperation on tax information exchange”

38

Foreign Account Tax Compliance Act Of 2009 - Highlights

• Require foreign financial institutions to provide the identity of any U.S. individual or foreign entity with substantial U.S. owners, and relevant account information, to Treasury or face a 30% withholding tax on income from the bank’s U.S. assets

• Mandate that foreign corporations provide withholding agents with the name, address and tax identification number of any U.S. individual with at least 10% ownership in the firm, or face a 30% withholding tax

• Extend bearer-bond tax penalties to such bonds marketed to offshore investors,and prevent the U.S. government from offering any bearer bonds

• Subject dividend equivalent payments included in notional principal contracts and paid to overseas corporations to the same 30% withholding tax levied on dividends paid to foreign investors

38

39

Foreign Account Tax Compliance Act of 2009 – Highlights (Cont.)

• Impose penalties as high as $50,000 on U.S. taxpayers who own at least $50,000 in offshore accounts or assets but fail to report the accounts on their annual income tax return

• Levy a 40% on the amount of any understatement attributed to undisclosed foreign assets

• Extend to six years the statute of limitations for “substantial” omissions (exceeding $5,000 and 25% of reported income) derived from offshore assets

• Require tax or investment advisers to disclose the identities of any clients they assist in buying offshore assets, as well as the assets purchased

• Require that shareholders in passive foreign investment companies file annual returns, and also give Treasury authority to mandate that financial firms file returns dealing with withholding taxes, even if they file fewer than 250 returns annually

• Make it easier for Treasury to presume that foreign trusts have U.S. beneficiaries, and establish a $10,000 minimum failure-to-file penalty for certain foreign-trust-related information returns

39

Background – IRS FBAR Webe page http://www.irs.gov/newsroom/article/0,,id=210247,00.html?portlet=6