the research bulletinthe research bulletin, august 2003, volume 21, no 1 published by the research...

TRANSCRIPT

THE RESEARCH BULLETIN

August 2003

RESEARCH DEPARTMENT

BANK OF BOTSWANA Volume 21 No. 1

ii

The Research Bulletin, August 2003, Volume 21, No 1

Published byThe Research Department, Bank of BotswanaP/Bag 154, Gaborone, Botswana.

ISSN 1027-5932

This publication is also available at the Bank of Botswana website:www.bankofbotswana.bw

Copyright © Individual contributors, 2003

Typeset and designed byLentswe La Lesedi (Pty) LtdTel: 3903994, Fax: 3914017, e-mail: [email protected]

Printed and bound byPrinting and Publishing Company Botswana (Pty) Ltd

iii

CONTENTS

Bank of Botswana Monetary Policy Statement 2003.................. 1

Bank of Botswana

Portfolio Capital Flows to Developing Countries 1980–1996:An Empirical Investigation ...................................................... 9

Lesedi Senatla

Money Laundering and Electronic Banking – Challenges forSupervisory Authorities in The Southern AfricanDevelopment Community (SADC) Region ............................ 21

Goememang Baatlholeng & Esther Mokgatlhe

GARCH Modelling of Volatility on Option Pricing:An Application to the Botswana Market ................................ 31

Pako Thupayagale

Blank page iv

The purpose of The Research Bulletin is to provide a forum where research relevant to theBotswana economy can be disseminated. Although produced by the Bank of Botswana, theBank claims no copyright on the content of the papers. If the material is used elsewhere, anappropriate acknowledgement is expected. In all cases, the views expressed in the papers arethose of the individual authors and are not necessarily associated with the official policies ofthe Bank of Botswana.

Additional copies of the Research Bulletin are available from The Librarian of the ResearchDepartment at the above address. A list of the Bank’s other publications, and their prices, aregiven below.

BANK OF BOTSWANA PUBLICATIONS

SADC Rest ofDomestic Members the World

1. Research Bulletin (per copy) P11.00 US$5.00 US$10.002. Annual Report (per copy) P22.00 US$10.00 US$15.003. Botswana Financial Statistics Free US$25.00 US$40.00

(annual: 12 issues)4. Aspects of the Botswana Economy: P82.50 US$29.00 US$42.00

Selected Papers

Please note that all domestic prices cover surface mail postage and are inclusive of VAT. Otherprices include airmail postage and are free of VAT. Cheques, drafts, etc., should be drawn infavour of Bank of Botswana and forwarded to the Librarian, Bank of Botswana, Private Bag154, Gaborone, Botswana.

vi

Blank page vi

BANK OF BOTSWANA MONETARY POLICY STATEMENT 2003

1

Bank of BotswanaMonetary Policy Statement– 2003

Bank of Botswana

1. INTRODUCTION

1.1 The annual Monetary Policy Statement issuedby the Bank of Botswana serves several purposes.First, it provides an opportunity for the Bank to reporton inflation and monetary policy developments in theprevious year, and to present its assessment of theoutlook for inflation in the current year. Second, itenables the Bank to outline policy issues and theapproach that will be taken in formulating its policystance in response to inflation-related developmentsthroughout the year. Third, since 2002, the Statementhas contained the Bank’s annual objectives forinflation and credit growth, and an explanation ofhow these were derived. The Monetary PolicyStatement, therefore, plays an important role inconveying to stakeholders and the public at large arange of information relating to one of the Bank’score functions, the formulation and implementationof monetary policy. While the transparency entailedin the presentation of the Statement is important inits own right, it is also important in influencingeconomic and financial expectations and, therefore,the behaviour of economic agents. In this regard, theBank’s aim is to engender a public expectation ofsustainable low inflation consistent with the broadobjective of macroeconomic balance as a basis forsustainable growth.

1.2 Consistent with past practice, this year’sMonetary Policy Statement reviews the trends ininflation and their underlying causes, and assessesthe extent to which monetary policy succeeded inachieving its objectives in 2002. This is followed bya presentation of the Bank’s analysis of prospec-tive developments during 2003 and, based on that,the policy outlook for the current year. The State-ment concludes that although developments in2002 took inflation to over 11 percent, some wayabove the desired range of 4–6 percent for the year,this was largely due to exceptional transitory de-velopments, especially the introduction of ValueAdded Tax (VAT), and that after discounting theimpact of VAT, inflation was close to the upper endof the Bank’s policy goal. In light of this, as well asthe tightening of monetary policy towards the endof 2002 and the more restrained fiscal policy an-nounced in the 2003 Budget, it is considered thatthere are good prospects of achieving a substantialreduction in inflation during 2003. The aim of mon-etary policy going forward will be to ensure thatthe reduction is consistent with the Bank’s infla-tion objective for the year.

2. THE BANK’S MONETARY POLICY

FRAMEWORK AND OBJECTIVES

2.1 The principal objective of monetary policy inBotswana is the control of inflation. Specifically, itis the achievement of a sustainable, low andpredictable level of inflation that will, among others,enable the maintenance of internationalcompetitiveness. In the context of an exchange ratepolicy that aims to keep the nominal effectiveexchange rate of the Pula stable, this implies thatBotswana’s inflation rate should, at a minimum,be no higher than the average inflation rate of itsmajor trading partners, if stability of the realexchange rate is to be achieved. This yields theBank’s annual inflation objective, which isdescribed in detail in Section 7 below.

2.2 To achieve its inflation objective, the Bankuses interest rates to influence inflationary pres-sures in the economy. This is achieved indirectlythrough the impact of interest rates on credit andother components of domestic demand. Changesin interest rates, along with other factors such asthe exchange rate, balance of payments and theGovernment’s fiscal policy, affect the overall levelof demand for goods and services in the economy,relative to a given level of output. Inflationary pres-sures are likely to emerge when expenditure growsat a faster rate than available goods and services.

2.3 In formulating its monetary policy stance, theBank looks closely at the sources of any changesin inflation. In particular, the policy responds pri-marily to changes in inflation that are due to do-mestic demand pressures, rather than those thatmay be due to transitory factors or supply fluctua-tions on which monetary policy would have no di-rect influence. Therefore, in addition to headlineinflation data published by the Central StatisticsOffice, the Bank also examines the underlying in-flation trend, or core inflation, which excludes theimpact of transitory factors and exceptional changesin administered prices and/or indirect taxes. TheBank, however, recognises the need to respond toany impact that these excluded items might haveon underlying inflation through inflation expecta-tions and second-round effects.

2.4 When implementing monetary policy, theBank focuses on the intermediate targets that in-fluence the main components of domestic demand.The principal intermediate target in the monetarypolicy framework is the rate of growth of commer-cial bank credit to the private sector, which is con-sidered an important contributor to the growth ofprivate consumption and investment and, impor-tantly, can be directly influenced by monetary policythrough interest rates. The rate of growth of Gov-ernment spending is also an important determi-nant of domestic demand, since a large proportionof this demand is derived from expenditure on pub-lic consumption and investment. The continuing

BANK OF BOTSWANA

2

large role of the Government in the economy un-derscores the need for complementarity betweenfiscal and monetary policies in achieving the infla-tion objective.

3. DEVELOPMENTS IN INFLATION IN 2002

3.1 The 2002 Monetary Policy Statement specifiedthe Bank’s objective of achieving inflation during2002 in the range of 4–6 percent. In determiningthe inflation objective, the Bank was guided by anoutlook of stable global inflation as world economicactivity remained subdued, albeit with highergrowth rates compared to 2001. Throughout theyear, the world’s major central banks maintainedloose monetary policy with the aim of stimulatingeconomic activity. Given excess capacity and thecontinuing credibility of monetary policy in thesecountries, inflation was largely controlled. InBotswana, however, domestic demand remainedstrong, with growth rates for both commercial bankcredit and government expenditure higher than thedesired rates indicated in the 2002 Monetary PolicyStatement. In this context, it was considered thatthe existing tight monetary policy stance wouldcontribute to a reduced rate of growth of credit,while the specification of the inflation objective andclear indications of the Bank’s response to anyinflationary developments were expected to anchorinflation expectations downwards.

3.2 Since the slowdown that began in the secondhalf of 2000, annual inflation stabilised at around6 percent in the first half of 2002, the upper end ofthe target range for the year (Chart 1). However,headline inflation rose from 5.9 percent in June to

11.2 percent in December1, largely as a result ofthe introduction of VAT in July. For the whole of2002, inflation averaged 8.1 percent, compared to6.6 percent in 2001 and 8.5 percent in 2000.

3.3 Following the introduction of the 10 percentVAT, it was anticipated that prices would rise ingeneral by between 4 percent and 6 percent, overand above underlying inflation. The Bank indicatedin a press release in June 2002 that any VAT-re-lated price increases would be a one-off temporaryadjustment, which in the absence of any signifi-cant second-round effects, would not result in asustained rise in inflation. In the event, and in linewith expectations, the month-on-month rate ofchange in prices rose from an average of 0.5 per-cent over the previous twelve months to 3.2 per-cent in July, and progressively slowed down in thesubsequent months (1.2 percent in August, 0.6 per-cent in September and 0.4 percent in October), aclear indication of the one-off impact of VAT. Al-though some monthly price increases were higherin the last quarter of 2002, this was mostly due totechnical adjustments to components of the Con-sumer Price Index (CPI) basket2. Overall, althoughinflation increased sharply in the second half ofthe year, an analysis of the inflation trend that dis-counts the impact of VAT and price data adjust-ments suggests an underlying rate of between 6percent and 7 percent for 2002, just above theupper end of the Bank’s policy goal.

3.4 Most categories of com-modities experienced higherinflation in 2002 comparedto 2001, which was to be ex-pected given the wide-rang-ing impact of VAT. Foodprices, however, rose muchfaster than those of mostother commodities, duepartly to drought conditionsin the region. Food price in-flation rose from 4.1 percentin December 2001 to 14.3percent in December 2002;this increase alone ac-counted for almost half of therise in overall inflation dur-ing the year. This reinforcesthe view that, after takingaccount of the impact of VATand other exceptional factorssuch as food prices, under-lying inflation was largelycontained during 2002.

0

2

4

6

8

10

12

1999 Apr Jul Oct 2000 Apr Jul Oct 2001 Apr July Oct 2002 Apr July Oct

Per

cent

CHART 1: BOTSWANA INFLATION

1Unless otherwise indicated, inflation rates are shownas the year-on-year change for the period noted.

2Mainly the adoption of a new billing system byBotswana Telecommunications Corporation.

BANK OF BOTSWANA MONETARY POLICY STATEMENT 2003

3

3.5 Inflation was alsohigher in 2002 compared to2001 in respect of goodsand services classified bytradeability. Prior to the in-troduction of VAT in July2002, inflation for non-tradeables and importedtradeables had fallen, butthereafter it rose sharply.Inflation for non-tradeablesfell to 6.9 percent in June2002, from 7.7 percent inDecember 2001, but rose to11.7 percent in December2002. Inflation for importedtradeables fell to 3.8 percentin June 2002, from 4.6 per-cent in December 2001, ris-ing to 8.2 percent inDecember 2002. In con-trast, inflation for domestictradeables showed a con-sistent and more rapid up-ward trend, reaching 15.2percent in December 2002, from 8.2 percent in June2002 and 5.9 percent in December 2001.

4. INFLUENCES ON DOMESTIC INFLATION

4.1 The international environment wascharacterised by moderately rising inflation in 2002(Chart 2). Inflation in advanced economies rose from1.2 percent in 2001 to 2 percent in 2002, as allmajor economies experienced higher inflation,mostly resulting from rising energy prices,especially oil. However, witheconomic growth remainingweak, albeit improvingslightly, major world centralbanks maintainedaccommodative monetarypolicies to support growth,taking the view thatinflationary pressures werenot generally of concern andnoting the existence ofexcess production capacity,restrained consumerdemand and benigninflation expectations. InSouth Africa, inflation rosesharply in 2002, largelyreflecting the effects of thedepreciation of the randtowards the end of 2001,and increases in food pricesand labour costs. Coreinflation in South Africa was12.2 percent in December2002, considerably higher

than the 5.8 percent at the end of December 2001.The combined effect of all of these developmentswas that average inflation across Botswana’strading partners rose from 4.2 percent at the endof 2001 to 8.6 percent at the end of 2002. Botswanainflation briefly fell below that of its trading partnersin mid-year but ended the year higher, largely dueto the impact of VAT.

4.2 Commercial bank credit to the private sectorgrew, on average, at an annual rate of 18 percent,up from 13.2 percent in 2001, well above the tar-

0

2

4

6

8

10

12

14

1999

M

arM

ay JulSep

tNov

2000 M

arM

ay JulSep

tNov

2001 M

arM

ay JulSep

tNov

2002 M

arM

ay JulSep

tNov

Per

cent

SA (core)

Botswana

SDR countries

Trading partner

CHART 2: INTERNATIONAL INFLATION

0

10

20

30

40

50

60

1999

M

arM

ay JulSep

tNov

2000 M

arM

ay JulSep

tNov

2001 M

arM

ay JulSep

tNov

2002 M

arM

ay JulSep

tNov

Per

cent

Total credit (adj)

Total credit

Govt. Spending(annual)

CHART 3: GROWTH RATES OF CREDIT AND GOVERNMENT SPENDING (YEAR ON YEAR)

BANK OF BOTSWANA

4

get range of 12.5–14.5 percent (Chart 3). However,once an adjustment is made to take account of theextension and subsequent early repayment of loans,using offshore funds, by some large borrowers, un-derlying credit growth in 2002 was 21.3 percent,compared to 18.6 percent in 2001.

4.3 Government expendi-ture is estimated to havegrown by 18 percent during2002, slightly below the 20percent growth recorded in2001 (Chart 3). The highrate of growth of govern-ment spending continued tobe of concern from a mon-etary policy perspective,since it was not consistentwith the inflation objectivebeing pursued and was re-sulting in an undesirableimbalance between fiscaland monetary policies.

4.4 Economic growth for2001/02 was 2.3 percent,markedly lower than the 8.4percent recorded during the2000/01 national accountsyear3. The significantslowdown in growth largelyreflected developments inthe mining sector, where output contracted by 3.1percent, compared to growth of 17.2 percent in theprevious year. However, in many other sectors therewas robust growth, and the growth rate of non-mining GDP was a healthy 5.5 percent, up from 4percent in the previous year. This outturn is closeto the trend growth rate of 6 percent for non-min-ing GDP envisaged over the eighth National Devel-opment Plan (NDP 8) period of 1997–2003.

4.5 During 2002, the Pula appreciated in nomi-nal terms against major international currencies,following the recovery of the rand from losses sus-tained towards the end of 2001 (Chart 4). The 29percent appreciation of the rand against the SDR4

is largely attributable to a prudent macroeconomicpolicy in South Africa, a more favourable assess-ment of South Africa vis-a-vis other emerging mar-kets by international investors, a perception thatthe rand had become undervalued and the weak-ness of the US dollar. As a result of the link to therand through the currency basket5, the Pula

strengthened by 27.9 percent against the US dol-lar and 18.6 percent against the SDR during 2002,while depreciating by 8 percent against the rand.

4.6 The trade-weighted nominal effective exchangerate of the Pula was largely stable in 2002; it appreci-

ated by 0.5 percent, as the impact of appreciationagainst the SDR was offset by depreciation againstthe rand. As inflation was higher in Botswana thanin trading partner countries, mainly due to the im-pact of VAT, the real effective exchange rate of thePula appreciated by 2.9 percent in the year to De-cember 2002 (Chart 5), thus eroding competitiveness.

5. MONETARY POLICY IMPLEMENTATION

DURING 2002

5.1 The objective of monetary policy in 2002 wasto sustain the downward trend in inflation and tokeep it within the desired range of 4–6 percent. Thiswas to be achieved by adopting a monetary policystance designed to restrain the growth of domesticdemand, especially demand arising from growth indomestic credit. This policy stance was re-emphasised in the mid-year review of the 2002Monetary Policy Statement.

5.2 As noted earlier, domestic demand continuedto be expansionary. The growth rate of commercialbank credit remained at levels above the desiredrange throughout 2002, and the growth of govern-ment expenditure was similarly inconsistent withthe inflation objective. Although underlying infla-tion is estimated to have been between 6 percentand 7 percent by the end of 2002, close to the de-

3The national accounts year runs from July to June

4The IMF’s Special Drawing Right, which is a weightedcomposite of the US dollar, Japanese yen, euro andpound sterling.

5The nominal value of the Pula is fixed to a trade-weighted basket of currencies comprising the SouthAfrican rand and SDR.

50

60

70

80

90

100

110

120

130

140

1999 M

arM

ay JulSep Nov

2000 M

arM

ay JulSep Nov

2001 M

arM

ay JulSep Nov

2002 M

arM

ay JulSep Nov

Inde

x (

Nov

embe

r 19

96 =

100

)NEER

Rand/Pula

SDR/Pula

CHART 4: NOMINAL EXCHANGE RATE (NOVEMBER 1996 = 100)

BANK OF BOTSWANA MONETARY POLICY STATEMENT 2003

5

sired range for inflation, it was, nevertheless, clearin the second half of 2002 that public expectationsof a more sustained increase in inflation were start-ing to build up.

5.3 Looking ahead, the Bank considered that thecontinued high rates of growth of credit and gov-ernment spending would add to inflationary pres-sures, leading in due course to an increase inunderlying inflation significantly above the desiredrange. Therefore, in order to reduce demand pres-sures, especially those emanating from credit ex-pansion, and to influenceexpectations of low infla-tion, the Bank Rate was in-creased by a total of 100basis points in October andNovember (50 basis pointseach time) to 15.25 percent.

5.4 Open market opera-tions were conducted duringthe year to ensure that yieldson Bank of Botswana Cer-tificates (BoBCs) were con-sistent with the policystance. Between Januaryand September 2002, thethree-month BoBC rate6

ranged between 12.52 per-cent and 12.55 percent, in-creasing to 14.03 percent bythe end of the year, follow-

ing the increase in the BankRate. Open market opera-tions were used to sterilisea substantial increase inmarket liquidity during2002, largely due to the P4.9billion funding of the PublicOfficers Pension Fund bygovernment and the generalincrease in government ex-penditure. These two factorswere reflected in a 30 per-cent decrease in govern-ment deposits at the Bankof Botswana and an in-crease of 49 percent inBoBCs outstanding to P7664 million at end-2002.

5.5 As a result of the in-crease in the Bank Rate,which signals the desireddirection and levels of inter-est rates, commercialbanks raised their lending

and deposit rates. The average 88-day deposit raterose from 9.81 percent to 10.15 percent, while theprime-lending rate rose from 15.75 percent to 16.75percent. Real interest rates in Botswana were gen-erally relatively high and stable during the first halfof the year, but declined sharply in the second halfof the year as inflation rose. As at the end of theyear, the real three-month BoBC rate declined to2.5 percent, from 6.5 percent in January and 6.2percent in June. Despite the decrease, real inter-est rates in Botswana were higher than those ofmajor economies and South Africa (Chart 6).

70

80

90

100

110

120

130

140

1999 M

arM

ay JulSep Nov

2000 M

arM

ay JulSep

tNov

2001 M

arM

ay JulSep

tNov

2002 M

arM

ay JulSep

tNov

Inde

x

RER-ZAR

RER-SDR

RER-Effective

CHART 5: REAL EXCHANGE RATE (NOVEMBER 1996 = 100)

-2

-1

0

1

2

3

4

5

6

7

8

9

1999 M

arM

ay JulSep

tNov

2000 M

arM

ay JulSep

tNov

2001 M

arM

ay JulSep

tNov

2002 M

arM

ay JulSep

tNov

Per

cent

SA(core)

UK

USA

Botswana

CHART 6: INTERNATIONAL REAL INTEREST RATES

6Figures refer to the BoBCmid-rate, as published inthe Botswana FinancialStatistics.

BANK OF BOTSWANA

6

6. OUTLOOK FOR INFLATION IN 2003

6.1 Global economic performance is expected toimprove further in 2003, with world output forecastto grow by 2.5 percent, up from an estimated 1.7percent for 2002. Global inflation is expected,nevertheless, to remain stable and low as worldoutput growth remains below trend. There is,however, uncertainty surrounding oil prices due toa possible war in Iraq. As inflation continues to belargely under control, it is anticipated that the majoreconomies will maintain stimulative monetarypolicy which, in some instances, will be supportedby expansionary fiscal policy.

6.2 Inflation in South Africa, which is the mostimportant external influence on inflation inBotswana, rose sharply during 2002; but it is ex-pected to slow down in 2003, reflecting the recentstrengthening of the rand, the tight monetary policystance and supportive fiscal policy. It is, however,unlikely that South Africa’s inflation target of 3 – 6percent will be met during 2003. Nevertheless, it isnot expected that monetary policy will be tightenedfurther unless new inflationary threats emerge, dueto concerns about economic growth. Core inflationin South Africa is forecast to fall to between 7 per-cent and 8 percent in 2003, from 12.2 percent in2002. For the SDR countries, inflation is forecastat 2 percent in 2003, the same as at the end of2002. If the nominal effective exchange rate of thePula is unchanged, Botswana’s imported inflationis likely to be lower in 2003 than it was in 2002,although there may be a lagged impact of the 2002inflation increase in South Africa and globally.

6.3 Although domestic demand, as indicated bythe growth in commercial bank credit and govern-ment expenditure, remains undesirably high, it isexpected that the increase in interest rates in thelast quarter of 2002 will, in due course, moderatethe demand for credit. Furthermore, the 2003budget indicates that government expenditure willgrow at a much slower rate of 4.1 percent in 2003,which will, together with an expected reduction incredit growth, help to moderate inflationary pres-sures. The Government’s decision not to award apublic sector pay rise in 2003 will further help torestrain demand pressures, and it is hoped thatthis will not be undermined by the findings of theongoing Salary Structure Review Commission. Pros-pects in 2003 are of a better balance between mon-etary and fiscal policies in restraining overallexpenditure growth.

6.4 Overall, it is expected that inflation in the firsthalf of 2003 will be around present levels of be-tween 10 percent and 12 percent, before falling sig-nificantly in the middle of the year to between 6percent and 7 percent. This projection reflects thedropping out of the inflation calculation of the VAT-related increase in prices in mid-2002. It also as-sumes that monetary policy is successful in

restraining credit growth, that the growth of gov-ernment spending is reduced in 2003, and thatthere are no further undue external inflationarypressures generated by further large increases infood or oil prices.

7. MONETARY POLICY STANCE IN 2003

7.1 As indicated in Section 2 above, the Bankseeks to achieve a rate of inflation that, at aminimum, will maintain relative stability in the realexchange rate and avoid the need for a devaluationof the Pula. The inflation objective, therefore, reflectsan assessment of forecast inflation for tradingpartner countries. Given that forecast tradingpartner inflation for 2003 is higher than similarforecasts for 2002, on which the inflation objectivewas based, this could imply a slightly higher rangefor the inflation objective in the current year thanin 2002.

7.2 There are, nevertheless, strong reasons tomaintain the inflation objective in 2003 at the rangeof 4–6 percent. First, by helping to bring Botswa-na’s inflation rate below that of trading partners, itprovides an opportunity to regain some of the com-petitiveness lost last year as a result of the higherrate of inflation in Botswana. Second, excludingthe impact of VAT, underlying inflation remainsclose to the upper end of this objective. In this re-spect, the 4 – 6 percent range remains a feasibleobjective. Third, looking ahead and in light of con-cerns about the risks of a further VAT-includedincrease in inflationary expectations, the Bank be-lieves that it is important to maintain expectationsof sustainable low inflation.

7.3 The range for the growth rate of private creditthat is considered to be compatible with achievingthis inflation outcome is 12 – 14 percent. As in thepast, this range is derived from the expected an-nual capacity for growth (aggregate supply) of thenon-mining sector of the economy, as presented inthe ninth National Development Plan (NDP 9), anddesired inflation for the year, with an allowance forthe process of financial deepening as the economydevelops.

8. SUMMARY AND CONCLUSIONS

8.1 Inflation was higher in 2002 compared to2001, and was above the inflation objective indicatedin the 2002 Monetary Policy Statement. The higherinflation was largely explained by the temporaryimpact of VAT on prices in the second half of theyear, while underlying inflation was at the upperend of the 2002 target range. Inflation was alsoaffected by drought conditions in Southern Africa,which had an impact on food prices. Nevertheless,overall domestic expenditure growth was high,raising concerns about future inflation trends.

BANK OF BOTSWANA MONETARY POLICY STATEMENT 2003

7

8.2 During 2003, it is expected that outputgrowth will improve in major industrial countries,while inflation will remain under control. Exceptfor a possible increase in oil prices due to conflictin the Middle East, a possible war in Iraq and thelagged impact of the previous year’s increase inSouth African inflation, there is minimal risk ofexternal pressures on inflation. Domestically, it isanticipated that credit demand will slow in responseto the increase in interest rates in 2002, helping toalleviate demand pressures. Fiscal restraint, asshown in the much reduced growth rate for gov-ernment spending announced in the 2003 Budget,should also contribute to reducing inflationary pres-sures in 2003.

8.3 The task for monetary policy in 2003 will beto ensure that underlying inflation does not increaseand the expected decline in overall inflation is con-sistent with the Bank’s desired range of 4–6 per-cent by the end of the year. The Bank took a steplate last year to increase the cost of credit and,therefore, moderate its growth, as well as curtailhigher inflationary expectations. While the Bankwill continue to respond appropriately to monetaryand inflation developments, the fiscal restraint thatcharacterises the 2003 Government Budget shouldhelp to ensure that the burden of containing infla-tion will be shared in a more balanced manner be-tween monetary and fiscal policies during 2003.

Blank page 8

PORTFOLIO CAPITAL FLOWS TO DEVELOPING COUNTRIES 1980–1996: AN EMPIRICAL INVESTIGATION

9

Portfolio Capital Flows toDeveloping Countries1980–1996: An EmpiricalInvestigation

Lesedi Senatla1

INTRODUCTION

There has been a noticeable increase in equity in-vestment flows (both portfolio and direct) as wellas bond holdings towards developing countriessince the late 1980s. Contributing to this increasewere financial institutions, institutional investorsand individuals who were important purchasers ofemerging markets’ securities. Portfolio investmentstook the form of debt and equity instruments. Debtinstruments, in turn, comprised bonds, certificatesof deposit and commercial paper issues. Of thesecategories bonds accounted for the largest share(World Bank, 1994). Equity instruments consistedof company shares, depository receipts, investmentfund units and purchases by foreigners of equityinstruments in local stock markets (World Bank,1994). Curiously, these capital flows were not wide-spread but rather mostly went to the middle-in-come countries (the so-called emerging markets)in Latin America and East Asia. Indeed, the WorldBank (1994, p.14) observed that ‘Latin America andEast Asia together accounted for more than 90 per-cent of the gross portfolio equity flows to develop-ing countries between 1989 and 1993.’ The promi-nent recipients of these capital flows were Argen-tina, Brazil, Chile, Mexico, Indonesia, South Ko-rea, Malaysia, Philippines and Thailand. Interest-ingly, researchers are not in agreement about thedeterminants of these portfolio capital flows. Somebelieve that external factors are responsible, i.e.,the ‘push’ view (see Calvo et al., 1993; Fernandez-Arias, 1996; Cardoso and Goldfajn, 1997 and Kim,2000, among others). Others, however, are con-vinced of the potency of domestic economic factorsin attracting capital flows i.e., the ‘pull’ view (seeLensink and Van Bergeijk, 1991b and Bekaert,1995). Research findings from the ‘push’ view typi-cally attribute portfolio inflows to the decline innominal interest rates in OECD countries. On theother hand, the pull view proponents emphasisethe improved domestic creditworthiness of the hosteconomies, following their economic adjustmentsand liberalisation efforts.

Beneath the push and pull views’ divergence of

opinion lies the question of the degree of controlon foreign savings inflows. The push view implieslack of influence given the exogenous nature of thedeterminants. Conversely, the pull view suggestssome degree of influence on account of the possi-ble control of the domestic economic factors.

This paper contributes to the economic debateabout the relative importance or dominance of thepush and pull factors. However, it advances thedebate further by investigating whether the inter-action of external and domestic factors might pro-vide an additional explanation of portfolio flows. Inorder to proceed in this investigation a study ismade of portfolio flows (bonds and equities) from apanel of nine developing countries for the period1980–1996 consisting of four Latin American econo-mies (Argentina, Brazil, Chile and Mexico) and fiveAsian economies (Indonesia, Korea, Malaysia, Phil-ippines and Thailand).

The paper is structured as follows: Section 2provides a brief review and analysis of the theo-retical and empirical studies of portfolio flows. Thetheoretical arguments of portfolio flows are dividedinto those that highlight perfect capital markets,those stressing imperfect capital markets and thosethat emphasise capital (or credit) rationing. On theother hand, the empirical studies are divided intothose that pursue the push view interpretation ofportfolio flows, those following the pull view andothers that see a role for both the push and pullfactors. Section 3 provides a description of trendsand developments in portfolio flows to countriesunder study during the 1980–1996 period2.

Section 4 tests a simple empirical model de-rived from a neoclassical theoretical framework3.It then carries out a comparative policy analysiswith the previous empirical papers. In brief, thispaper discovers that both domestic and externalfactors explain portfolio capital flows to developingcountries but that there are important regional dif-ferences. Domestic factors dominate in LatinAmerica, while external factors dominate in Asiancountries.

The results here contradict those of Taylor andSarno (1997) and Chuhan et al. (1998). Taylor andSarno (1997) find that external factors are rela-tively more important for Latin America than Asia;while Chuhan et al. (1998) discover that domesticfactors are comparatively more influential thanexternal factors in Asia. The use of different datasets (from those of the previous literature) may ac-count for the differences in the findings. It is be-lieved that the findings here offer a new insight into

1Principal Economist in the Research Department ofthe Bank of Botswana. The paper draws on variouschapters of the author’s 2001 PhD thesis presentedto the University of Nottingham entitled ‘The Deter-minants and Behaviour of Capital Flows in EmergingMarket Economies’.

2Adding data points beyond 1996 made no substan-tive difference to the results here, and, for the pur-pose of this paper, data points covering the capitalflows crisis periods of 1997 and 1998 are not included.

3Due to space limitations the full theoretical model isnot specified here. Only the empirical version of themodel is shown.

LESEDI SENATLA

10

the causes of portfolio flows and thus represent animportant contribution to the literature.

Section 4 also advances the literature by exam-ining the role of the interactive effects in drivingportfolio flows. It finds strong evidence for theseeffects. Previous literature has thus far not inves-tigated the role of the interactive effects. The con-clusion is in Section 5.

A BRIEF REVIEW OF RELEVANT THEORETICAL

AND EMPIRICAL STUDIES

(a) Theoretical Treatment of Portfolio CapitalFlowsTheoretical analysis of portfolio capital flows canconveniently be subdivided into those that empha-sise perfect capital markets, those stressing im-perfect capital markets and those highlightingcredit rationing.

Theories with Perfect Capital Markets

Theories with perfect capital markets rely princi-pally on the ‘efficient market hypothesis’ whichposits that investors base their investment deci-sions on the information with which they are pro-vided (e.g., the price of securities or the perform-ance of the stock market). This information is thenused as a basis for pursuing high returns while, atthe same time, seeking to minimise risks.

As the name implies, the ‘efficient market hy-pothesis’ envisages a well-functioning capital mar-ket that is free of distortions and other barriers,which thus affords investors an opportunity to ra-tionally use all the available information at theirdisposal in their investment decisions.

Theories with Imperfect Capital Markets

It might not be helpful, though, to disregard theimpediments to the free flow of portfolio capital flowsthat exist in practice. Thus, theories with imper-fect capital markets attempt to redress this possi-ble shortcoming of theories that assume perfectcapital markets by incorporating different kinds ofimperfections in their models. Imperfections mightbe in the form of legal barriers such as discrimina-tory taxation or restrictions on ownership of for-eign securities (Jorion and Schwartz, 1986; Eunand Janakiramanan, 1986); or they could be in theform of lack of information about foreign firms; orthe fear of expropriation among others (Adler andDumas, 1975; Eun and Janakiramanan, 1986). Asfor legal barriers, Eun and Janakiramanan (1986)observe that host countries may impose these onfirms regarded to be strategically important to na-tional interests. Regarding lack of adequate or reli-able information, Leland and Pyle (1977) observedthat borrowers may not be expected to honestlysupply correct information to investors, hoping thatby over-stating the performance of their firms theymight obtain more investment funds from the in-

vestors. Verifying the information received can onlybe achieved at a cost (Townsend, 1979).

The existence of imperfections implies that theinternational capital market might not be com-pletely integrated. But Jorion and Schwartz (1986)caution that the existence of barriers of a legal na-ture, in particular, might not ensure segmentationsince investors may find innovative ways of avoid-ing barriers to capital flows.

Eun and Janakiramanan (1986) studied theeffect of the legal barriers that limited domesticinvestors to owning a certain fraction of shares offoreign firms. Their model suggested that a con-straint of this nature would lead to a higher pre-mium being paid by domestic investors on the priceof foreign securities over the price without restric-tions. This is because the restrictions lead to de-mand for foreign shares exceeding supply. Also le-gal barriers force domestic investors to hold moredomestic shares than they would if such restric-tions did not exist. Other studies have also shownthat legal restrictions tend to lead to substitutionaway from the restricted assets into unrestrictedones.

Consistent with others emphasising problemsof imperfect markets, Gertler and Rogoff (1990) andBoyd and Smith (1997) showed that capital flowsto developing countries tend to be depressed bylack of adequate information.

Capital Rationing Literature

The capital rationing literature takes the view thatbecause of the real possibility that the entrepre-neur or borrower might default on his/her contract,leading to losses for the investor he/she, therefore,has to find ways of limiting this possibility. Thissuggests that an investor would withhold loans tothe entrepreneur after a certain point has beenreached irrespective of how high the yield the en-trepreneur promises to pay. Literature notes thatpart of the problem the lender has is the inabilityto distinguish a ‘bad’ borrower from a ‘good’ one. Ifhe/she could, a bad borrower would never get aloan at any interest rate.

Faced with imperfect information regarding thenature of the borrower, the lender tends to resortto credit rationing; loan demand is not equal toloan supply, thus excess demand results. This be-haviour, it is argued, is a perfectly rational responsein view of the risk considerations involved.

When faced with an excess demand situation,the lender will be reluctant to raise interest ratesto accommodate excess demand since this will leadto adverse selection and moral hazard problems.The adverse selection effect arises in that as theinterest rate rises good borrowers, who have everyintention of paying back, would drop out of themarket leaving only the bad risks. Moral hazardproblems arise in that the high interest rate itselfwould lead borrowers to engage in excessive risktaking behaviour that promises high returns. Thus

PORTFOLIO CAPITAL FLOWS TO DEVELOPING COUNTRIES 1980–1996: AN EMPIRICAL INVESTIGATION

11

excess demand is an equilibrium solution.

(b) Empirical Studies of Portfolio FlowsAs stated above the empirical studies of portfolioflows can be divided into the push and pull factors’categories. The push factor argument states thatportfolio capital flows are driven (or pushed) out ofplace of origin (home) into another (host) countryby the macroeconomic conditions in the home coun-try. For example, a decline in interest rates in OECDcountries might push portfolio capital flows to de-veloping countries in pursuit of relatively higherreturns. On the other hand, the pull factor argu-ment attributes portfolio capital inflows to favour-able macroeconomic conditions in the hosteconomy.

A short summary of the empirical findings alongthe push and pull interpretations of portfolio capi-tal flows is presented here. Particular attention ispaid to the studies carried out in the 1990s andcurrent studies since they address causes of in-creases in portfolio capital flows to emerging mar-kets after the late 1980s.

(i) Push-Factor Studies

Table 1 provides a summary of studies that pur-sue the push-factor argument. The informationcontained in the table will not be repeated in thecomment on the studies to avoid repetition. Millerand Whitman (1970) experimented with a set ofUS economic variables and discovered that a fallin US income pushes portfolio flows out. Kreicher(1981) found evidence suggesting that a fall in thechange in real interest rates may also push portfo-lio flows out of the country.

Calvo et al. (1993) examined a list of US vari-ables in their investigations of the determinants ofportfolio capital flows in Latin American economies.They discovered that a decline in these externalfactors led to an increase in portfolio capital in-flows to Latin American economies.

The use of change in external reserves by theCalvo et al. (1993) study to proxy for capital flowsis, however, potentially problematic. This is becauseit tends to confuse cause and effect since reservescould be more appropriately viewed as a determi-nant (cause) of capital flows and not as proxies forcapital flows themselves. Fernandez-Arias (1996)and Chuhan et al. (1998) also make an observa-tion similar to the one being made here. Other prob-lems include ignoring domestic factors which havethe potential to influence capital flows. Quite likelytheir estimations suffer from the omitted variablebias problem as Kim (2000) also notes. Further-more, there is no mention of tests for unit rootswhich could limit the usefulness of the results be-cause of potential spurious correlation effects.

Fernandez-Arias (1996) used the country-spe-cific intercept term in a fixed effects model to cap-ture the domestic investment climate, theannualised ten-year US bond nominal yields tocapture international returns and the debt second-ary market prices – where available – to capturecountry creditworthiness, as explanatory variables.He found that external factors, as represented bythe international interest rate, had much more pow-erful effects in driving capital flows to emergingmarkets than domestic factors.

The two major weaknesses in the Fernandez-Arias method of analysis consist of using the in-

Study Data HomeCountry

Host Method Measure

Miller andWhitman(1970)

1957:2 -1966:3, T USA10 OECD

1 OLS A change in the ratio offoreign to total riskyassets

Kreicher(1981)

1967:4 -1974:4, T

1966:2 -1974:4, T

1967:2 -1974:4, T

1967:4 -1974:4, T

IT, GE

UK

GE, USA

UK, IT

UK

GE

IT

USA

OLS A change in long termportfolio liabilities toforeigners from privatesector agents

Calvo et al.(1993)

1988:1 -1991:12, T USA10 LDCs

2 Principalcomponent andVAR

Changes in reserves

Fernandez-Arias (1996)

1990:1-1993:2, P OECD13 LDCs

3 Fixed effectsmodel

Equity and debt as ratioof GDP

Cardoso &Goldfajn(1997)

1988:1-1995:12, T OECD Brazil OLS Equity and debt as ratioof GDP

Kim (2000) 1958:3 -1995:3, T

1982:2 -1995:1, T

1961:2 -1995:3, T

1972:2 -1995:1, T

OECD Mexico

Chile

Korea

Malaysia

VAR Capital account balanceas a ratio of GDP

TABLE 1: PUSH-FACTOR STUDIES

Notes: T denotes time series, P is panel data and OLS is ordinary least squares. GE is Germany and IT is Italy.

1 Australia, Canada, Denmark, France, Germany, Japan Netherlands, Norway, UK and Switzerland.

2

Argentina, Bolivia, Brazil, Chile, Columbia, Ecuador, Mexico, Peru, Uruguay and Venezuela.

3Algeria, Argentina, Brazil, Chile, Korea, Malaysia, Mexico, Panama, Philippines, Poland, Thailand, Uruguay and Ven-

ezuela.

LESEDI SENATLA

12

tercept to capture important domestic factors ratherthan explicitly finding proxy variables to capturedomestic factors. Secondly, the sample period cov-ered is much too short (i.e., four years) which weak-ens the statistical analysis.

Cardoso and Goldfajn (1997) sought to explaincapital inflows in Brazil and discovered that US in-terest rate had a dominating role as an explana-tory factor, thus implying a push interpretation.The basic problem with Cardoso and Goldfajn’sanalysis is the OLS procedure which may give riseto spurious results.

Kim (2000) used a set of US economic variablesas well as domestic ones as explanatory variables.The VAR estimation procedure showed the exter-nal factors as the dominant explanatory variables.The problem with the analysis, though, is the useof the overall capital account balance to measurecapital flows. This balance is too broad to be use-ful for policy-making purposes. Rather, an analy-sis based on the individual elements of the capitalaccount might be more helpful.

(ii) Pull-Factor Studies

Lensink and Van Bergeijk (1991) used a Logit modelto study a country’s probability of accessing pri-vate funds in the international capital market dur-ing the years 1985, 1986 and 1987 by examiningdata for 96 developing countries from Asia, LatinAmerica, Africa and Europe. The results showedthe significance of a variety of domestic macroeco-nomic factors in enabling a country to access in-ternational capital markets. The findings were alsothat Asian countries have a much higher probabil-ity of accessing international capital than Sub-Sa-haran African countries since Asian countries havemuch better economic fundamentals. However,since this study does not experiment with foreignfactors, it is impossible to assess how importantthey were relative to domestic factors. Hence, thisomission would seem to be a major weakness ofthe study.

Bekaert (1995) sought to discover whether itwas global factors or domestic country factors thatcould account for the gradual integration of theemerging markets economies with the internationalcapital markets using monthly data for 1986–1992.The results showed that the domestic factors wereoverwhelmingly more important in the integrationprocess relative to the global factors. This studysupports the pull view.

(iii) Other Studies

Taylor and Sarno (1997) studied the relative im-portance of the push and pull factors in drivingportfolio capital flows to nine Latin American andnine Asian economies using monthly data for Janu-ary 1988 to September 1992. The results showedthat both push and pull factors were significantdeterminants of portfolio flows (both equity andbond flows). In general, they found that US inter-

est rates had a much more powerful effect on port-folio flows to Latin American economies than toAsian economies. They also found that bond flowsare determined more by global factors (US interestrates) than by domestic factors while equity flowsare responsive to country-specific factors. Thisstudy seems to be hampered by the use of a shortsample period. 1988–1992 sample period is tooshort a time frame for the purpose of cointegrationmethods (which were used) and the associated longrun relationship analysis; consequently such ashort period could generate doubt as to the robust-ness of the results.

Chuhan et al. (1998) used the same data set asTaylor and Sarno but made use of a panel dataapproach. The results showed the equal importanceof both the push and pull factors in explaining capi-tal flows. In particular, they found that the pushfactors were much more important in explainingportfolio flows to Latin America, while the pull fac-tors were the dominating force in explaining port-folio flows compared with the global (push) factorsin Asian countries. In contrast to Taylor and Sarno,Chuhan et al. found that bond flows are determinedmore by domestic factors than by global factorswhile equity flows are more responsive to globalfactors.

The shortcomings of these two papers seem toconsist of the following: Portfolio flows from non-US sources was ignored. This is potentially prob-lematic since it is known, for example, that Japa-nese investors favour investing in Asia (see Ahmedand Gooptu, 1993); secondly, with regard toChuhan et al., most of the variables are potentiallyendogenous, except the foreign variables. Notwith-standing the fact that GLS or panel data methodwas used, it would have been appropriate to do aninstrumental variable (or two stage least squares)estimation to find out whether similar results willhold.

While the debate about the push and pull fac-tors is still ongoing, evidence so far seems to at-tribute the causes of portfolio capital flows to theexternal factors. Edwards (1999), however, opinesthat capital flows are a reflection of more than theinternational financial and economic factors butare also an indication of the attractiveness of thehost country’s economic conditions. He argues thatcapital inflows generally take place in countries thathave carried out or are carrying out economic re-forms (e.g., Latin American countries). Further-more, the push-factor proponents are unable toexplain why capital flows are not evenly spreadthroughout all the developing countries since, pre-sumably, all the developing countries are equallyaffected by external economic developments(Ahmed and Gooptu, 1993).

PORTFOLIO CAPITAL FLOWS TO DEVELOPING COUNTRIES 1980–1996: AN EMPIRICAL INVESTIGATION

13

3. DATA DESCRIPTION

The late 1980s saw an increase in capital flows toemerging market economies in the form of equityflows (i.e., both FDI and portfolio investment). Thiswas in contrast to the 1970s period, which wasdominated by commercial bank loans (Baer andHargis, 1997). Equity financing from the 1980s on-wards was viewed (by developing countries, in par-ticular) as a more preferable form of external fi-nancing since it leads to the sharing of risk be-tween the international investor and the host coun-try (Ahmed and Gooptu, 1993). But, equity financ-ing went mainly to middle income countries in LatinAmerica and Asia during the 1980s and 1990s pe-riod because they were considered more creditwor-thy. This section tentatively attributes the causesof portfolio capital flows to both domestic policychanges and/or foreign factors, thus laying thefoundation for formal tests.

Trends and Developments in Portfolio Flowsto Latin America and AsiaChart 1 plots the time series of portfolio flows4 as aratio of GDP for the Latin American economies (Ar-gentina, Brazil, Chile and Mexico), while Chart 2plots the series for the South East Asian econo-mies (Malaysia, Indonesia, Philippines, South Ko-rea and Thailand) during1980–1996.

Chart 1 show a sus-tained increase in portfolioflows to most Latin Ameri-can economies beginning1989. This increase coin-cided with the resolution ofearlier debt problems. Thechart also shows that LatinAmerican economies werefaced with a virtual cessa-tion of external financingduring the debt crisis pe-riod of the early 1980s. Thisled to major economic re-form programmes to regainaccess to external financing(El-Erian, 1992), includingabolishing exchange con-trols, trade liberalisation,tax reforms and liberalisingthe financial sector(Edwards, 1999). Possibly,these reforms had the effectof reducing perceptions of

country transfer risk (El-Erian, 1992).Chile is different from the other Latin Ameri-

can economies, however, in that it had the longestrecord of reforms dating back to the 1970s (UN,1996). It embraced economic reforms in the 1970sfollowing accession to power by a pro-market gov-ernment. Still, Chile experienced an increase inportfolio flows coincidental with others possiblyreflecting ‘bandwagon effects’ (Schadler et al., 1993).In other words, Chile had to await the return ofconfidence of investment potential in the LatinAmerican region. Indeed, foreign investors are of-ten accused of acting in a herd-like behaviour(Edwards, 1999).

Besides economic reforms there were other eco-nomic developments taking place in the region.These were, first, the gradual liberalisation of stockmarkets although some restrictions remained insome countries5. Opening domestic stock marketsallows foreign savings to enter through this me-dium although domestic companies may access for-eign capital in international capital markets. Sec-ond, there was the implementation of the Bradyplan in the 1980s, which entailed the negotiationof debt between the debtor and the creditor banksleading to debt buy-backs, the exchange of bankclaims for bonds at a lower face value and/or therescheduling of debt servicing on loans (UN, 1994).

The reduction of debt burdens through the Bradyplan might have generated perceptions of the im-

4The International Financial Statistics (IFS) describesportfolio flows as constituting ‘transactions with non-residents in financial securities of any maturity (suchas corporate securities, bonds, notes, money marketinstruments and financial derivatives) other than thoseincluded in direct investment’. In effect portfolio flowslump together bonds and equities.

-10

-5

0

5

10

15

20

25

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

Per

cent

Argent. Brazil

Chile Mexico

CHART 1: PORTFOLIO FLOWS IN LATIN AMERICA AS A RATIO OF GDP

5For instance, in Chile as at 1995, foreign investorswere required to register with the authorities beforethey could buy domestic listed stocks (UNCTAD,1997).

LESEDI SENATLA

14

proved creditworthiness of the debtor countries (El-Erian, 1992). However, the Brady plan was openonly to countries that undertook serious economicreforms. Finally, regulatory changes in developedcountries in 1990 particularly ‘Regulation S’ and‘Rule 144A’ (in the US) which helped reduce trans-actions costs because foreign securities were ex-empted from registration requirements, may alsohave played a part in the increase of capital flowsto emerging markets (El-Erian, 1992).

Chart 1 shows interesting discrete jumps in thedata. The increases and falls in the data follow im-portant events such as privatisation episodes, theintroduction of inflation stabilisation policies andthe flight of foreign inves-tors. For example, the sud-den jump in portfolio flowsto Argentina in 1993 cap-tures increases in portfolioequity inflows resultingfrom the privatisation of thestate oil and gas company6,and the increase in portfo-lio flows to Brazil in 1994followed the replacement ofthe cruzeiros reais with thereal currency. This helpedreduce inflation from 2500percent in 1993 to singledigits by January 1995 (UN,1995). The reduction inmonthly inflation ratescould help explain the at-tractiveness of real-denomi-nated assets to foreign in-vestors in 1994 (Turner,1995). The decline in port-folio flows to Mexico in 1995was precipitated (mainly) by

the devaluation7 of the Mexican peso in December1994, although increases in US interest rates mightalso have had an influential effect. Increases in USinterest rates (in 1994) might have made US secu-rities relatively more attractive8 (UN, 1995). Chil-ean portfolio flows data show less dramatic in-creases owing perhaps to the less dramatic reformsthat were needed during the 1980s and 1990s.

Chart 2 shows portfolio inflows to South EastAsia. Factors mentioned above such as the liber-alisation of stock markets9 and regulatory changesin the industrial countries could have played a rolein inducing portfolio flows to Asian economies.Furthermore, falls in international interest rates

in the 1990s possibly also played a part in height-ening investor interest in Asian countries’ securi-ties (Ishii and Dunaway, 1995). These factors mighthave been particularly important in explaining theapparent increases in portfolio flows to Thailand,Korea and Indonesia from 1990 onwards10. MostAsian economies did not experience debt prob-lems11– except the Philippines, which announcedits difficulties in paying its external debt in 1983.Indeed, while Latin American economies were facedwith a virtual absence of portfolio flows in the early1980s, most of the Asian economies were enjoyingrelatively moderate increases in portfolio flows. Still,even the Asian countries were not unaffected by

6See also Claessens and Gooptu (1994).

7The devaluation of a currency increases the local cur-rency cost of a country’s foreign liabilities and thusputs an extra burden on the country’s external posi-tion. This exchange-rate-induced debt burden makesit more likely that a country could default on its ex-ternal obligations (IMF, 1998). Unsurprisingly, there-fore, a currency devaluation causes uneasinessamong foreign investors and normally leads to theflight of their money.

8Mexico also experienced political problems in 1994,which included the assassination of a leading presi-dential candidate. But these political problems ‘…didnot seem to shake investor confidence in the Mexi-can economy…’ (UN, 1995, pp. 78).

9As at 1995, foreign investors were required to regis-ter with the authorities to buy domestic stocks in In-donesia, Korea and Thailand. In the Philippines,foreign investors were restricted to certain classes ofstocks specifically designated for them. Malaysia, onthe other hand, did not have restrictions on foreignpurchase of domestic stocks in 1995 (World Invest-ment Report, 1997).

-4

-2

0

2

4

6

8

10

12

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

Per

cent

Phillipines Malaysia

Thailand Indonesia

Korea

CHART 2

10We explain portfolio flows’ movements in Malaysia andPhilippines separately in what follows.

11The question of why Asian countries did not have adebt problem is outside the scope of this paper. Foran attempt at answering this question see Singh(1995).

PORTFOLIO CAPITAL FLOWS TO DEVELOPING COUNTRIES 1980–1996: AN EMPIRICAL INVESTIGATION

15

the general withdrawal of foreign investors fromdeveloping countries in the early 1980s.

Since the Philippines (in tandem with LatinAmerican economies) had experienced debt pay-ment difficulties in the early 1980s, it too facednegligible inflows of portfolio capital in the 1980sleading to economic reforms in order to regain ac-cess to capital flows. Malaysia experienced a dra-matic fall in portfolio capital flows since 1985. Thepersistent negative inflows beyond 1985 and intothe 1990s may reflect the authorities’ inclinationto discourage portfolio flows in order to mitigatetheir potentially harmful effects12. For example, in1994 Malaysia prohibited its residents from sell-ing short-term monetary instruments to non-resi-dents, although such a prohibition was rescindedlater in the same year (Corbo and Hernandez, 1996).Still, despite the cancellation of this prohibition,foreign portfolio investors might nevertheless havefelt uneasy about investing in Malaysia.

In brief, this section has suggested that domes-tic policy changes, e.g., privatisation and declinesin international interest rates are the key factorsaccounting for foreign capital inflows to emergingmarkets.

4. EMPIRICAL SPECIFICATION AND RESULTS

This section applies panel data econometrics to amodel of portfolio capital flows for a longer time-span than most of the previous studies mentionedin Section 213. The model to be used is a hybridbetween a flow and a stock concept consistent withsome of the literature (e.g. Leamer and Stern, 1970,Calvo et al., 1993 and Chuhan et al., 1998).

The dependent variable is portfolio investment(or flows) as a proportion of gross domestic prod-uct (PIRD). The data is annual and covers nine de-veloping countries14. The explanatory variables arethe following: nominal US interest rates (USRT, i.e.medium-term government bond yields) were usedto capture the return on a safe asset in the ad-vanced country. We further experiment with thesix-month London Inter-Bank Offer Rate (LIBOR)to test the robustness of the findings. Similarly, wealso test the impact of measures of real returns (as

opposed to nominal returns) on portfolio flows. Twopossible measures of real returns are used: (1) thereturn on UK ten-year indexed bonds15 (UKBONDS)and (2) the nominal return on a ten-year US bonddeflated by consumer price inflation over the fol-lowing two years (RUSRT). We anticipate negativesigns on the coefficients of interest rate variablesfollowing from the fact that declines in interest rates‘push’ portfolio capital flows to emerging marketeconomies.

We employ the real share price index (SHP) torepresent expected returns. This follows the effi-cient markets hypothesis that any news with thepotential to affect expected returns should be re-flected in equity prices. Such news may be in theform of the announcement of policy reforms orchanges in the probability of such an announce-ment. We expect a positive coefficient on this vari-able.

We include a range of country-specific macr-oeconomic indicators to capture creditworthiness.Haque et al. (1996, 1998) demonstrated that thesemacroeconomic factors were useful measures ofcreditworthiness. These factors comprise currentaccount balance as a share of GDP (CA) and for-eign exchange reserves as a ratio of imports (FRIM).

Following Brewer and Rivoli (1990), we use thecurrent account as a ratio of GDP (CA) to capturetrade performance. The idea is that countries dis-playing strong trade performance are in a goodposition to obtain the hard currency they need toservice their external obligations. Indeed they maybe paid in foreign currency since much of worldtrade is conducted in US dollars. CA should have apositive coefficient.

Foreign exchange reserves – measured here asa proportion of imports – (FRIM) enable a countryto service its external obligations in the event of aliquidity problem. Indeed, countries hold foreignreserves principally to cushion them during hardtimes and avoid unwanted pressure on fixed ex-change rates. We anticipate a positive sign on thecoefficient of this variable. Other variables experi-mented with were the growth rate of GDP, exportto GDP ratio, external debt to export ratio and vola-tility in the exchange rate. These were found to bestatistically insignificant.

The empirical model to be estimated is the fol-lowing:

F b b a B R b a B H

b a B M ut t t

t t

= + − + − +− +

0 1 1 2 2

4 4

1 1

1

( ) ( )

( ) (1)

F b b a B R b a B H

b a B R H b a B M ut t t

t t t t

= + − + − +− + − +

0 1 1 2 2

3 3 4 4

1 1

1 1

( ) ( )

( ) ( ) (2)

where Ft represents portfolio capital flows in

12A full discussion of the potentially harmful effects ofportfolio flows is outside the scope of this paper. How-ever, it is to be noted that portfolio capital inflowsmay disturb macroeconomic stability through, forexample, increasing domestic demand and exertingpressure on prices of goods and financial assets (seeSchadler et al., 1993).

13Note that Kim’s (2000) study is an exception since itconsidered a longer time period than ours. See de-tails in Chapter 2.

14The data is published in various issues of IFS. Ex-planatory variables were sourced from various issuesof IFS, Bank of England, IFC Emerging Stock Mar-kets’ Factbook, Bloomberg Investment Machine andWebec.

15Since the UK only began issuing indexed bonds in1981, we assumed that the 1981 bond returns werethe same as in 1980.

LESEDI SENATLA

16

year t to a particular country, R represents inter-est rate measures described above, H is the coun-try real share price index, M with a bottom bar is avector of country-specific macroeconomic indica-tors and B is the backward shift operator (i.e. Bxt =xt-1). Equations (1) and (2) differ only to the extentthat the latter includes the interactive term betweeninterest rates and real share price indices.

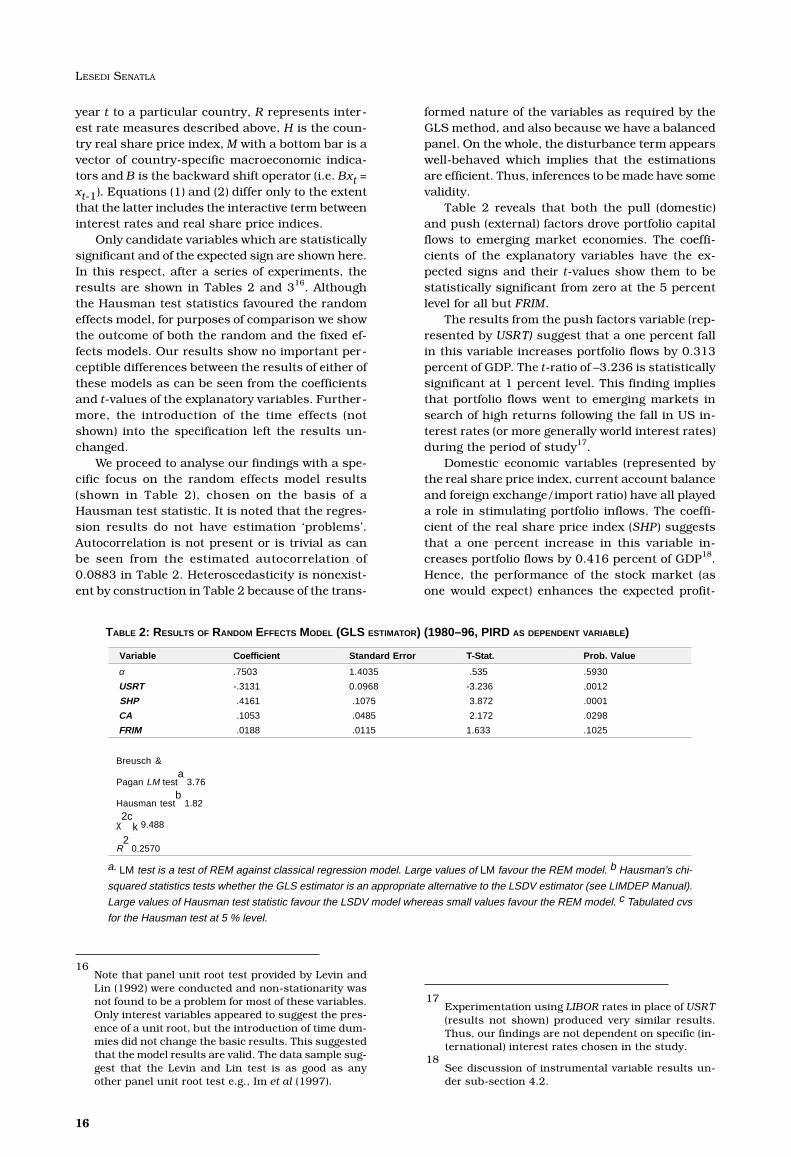

Only candidate variables which are statisticallysignificant and of the expected sign are shown here.In this respect, after a series of experiments, theresults are shown in Tables 2 and 316. Althoughthe Hausman test statistics favoured the randomeffects model, for purposes of comparison we showthe outcome of both the random and the fixed ef-fects models. Our results show no important per-ceptible differences between the results of either ofthese models as can be seen from the coefficientsand t-values of the explanatory variables. Further-more, the introduction of the time effects (notshown) into the specification left the results un-changed.

We proceed to analyse our findings with a spe-cific focus on the random effects model results(shown in Table 2), chosen on the basis of aHausman test statistic. It is noted that the regres-sion results do not have estimation ‘problems’.Autocorrelation is not present or is trivial as canbe seen from the estimated autocorrelation of0.0883 in Table 2. Heteroscedasticity is nonexist-ent by construction in Table 2 because of the trans-

formed nature of the variables as required by theGLS method, and also because we have a balancedpanel. On the whole, the disturbance term appearswell-behaved which implies that the estimationsare efficient. Thus, inferences to be made have somevalidity.

Table 2 reveals that both the pull (domestic)and push (external) factors drove portfolio capitalflows to emerging market economies. The coeffi-cients of the explanatory variables have the ex-pected signs and their t-values show them to bestatistically significant from zero at the 5 percentlevel for all but FRIM.

The results from the push factors variable (rep-resented by USRT) suggest that a one percent fallin this variable increases portfolio flows by 0.313percent of GDP. The t-ratio of –3.236 is statisticallysignificant at 1 percent level. This finding impliesthat portfolio flows went to emerging markets insearch of high returns following the fall in US in-terest rates (or more generally world interest rates)during the period of study17.

Domestic economic variables (represented bythe real share price index, current account balanceand foreign exchange/import ratio) have all playeda role in stimulating portfolio inflows. The coeffi-cient of the real share price index (SHP) suggeststhat a one percent increase in this variable in-creases portfolio flows by 0.416 percent of GDP18.Hence, the performance of the stock market (asone would expect) enhances the expected profit-

16Note that panel unit root test provided by Levin andLin (1992) were conducted and non-stationarity wasnot found to be a problem for most of these variables.Only interest variables appeared to suggest the pres-ence of a unit root, but the introduction of time dum-mies did not change the basic results. This suggestedthat the model results are valid. The data sample sug-gest that the Levin and Lin test is as good as anyother panel unit root test e.g., Im et al (1997).

17Experimentation using LIBOR rates in place of USRT(results not shown) produced very similar results.Thus, our findings are not dependent on specific (in-ternational) interest rates chosen in the study.

18See discussion of instrumental variable results un-der sub-section 4.2.

Variable Coefficient Standard Error T-Stat. Prob. Value

α .7503 1.4035 .535 .5930

USRT -.3131 0.0968 -3.236 .0012

SHP .4161 .1075 3.872 .0001

CA .1053 .0485 2.172 .0298

FRIM .0188 .0115 1.633 .1025

Breusch &

Pagan LM testa

3.76

Hausman testb

1.82

χ2c

k 9.488

R2

0.2570

TABLE 2: RESULTS OF RANDOM EFFECTS MODEL (GLS ESTIMATOR) (1980–96, PIRD AS DEPENDENT VARIABLE)

a. LM test is a test of REM against classical regression model. Large values of LM favour the REM model. b Hausman’s chi-

squared statistics tests whether the GLS estimator is an appropriate alternative to the LSDV estimator (see LIMDEP Manual).

Large values of Hausman test statistic favour the LSDV model whereas small values favour the REM model. c Tabulated cvs

for the Hausman test at 5 % level.

PORTFOLIO CAPITAL FLOWS TO DEVELOPING COUNTRIES 1980–1996: AN EMPIRICAL INVESTIGATION

17

ability of investment in the countries under inves-tigation, enticing foreign portfolio inflows in theprocess19. The apparent statistical significance ofthe current account balance and the ratio of re-serves to imports variables can be interpreted asadditional country-specific indicators of creditwor-thiness20.

Further experimentation involving both real andnominal interest rates was conducted (results notshown). Real interest rates used were UKBONDSand RUSRT as explained above. In the main, theresults from using real interest rates were not thatdissimilar from those using nominal rates only.However, the strength of real interest in drivingportfolio flows was somewhat inferior to that ofnominal interest rate variables. For the sake of con-sistency with the previous literature, it was decidedto stick with the nominal interest rate variables. Itis, however, fair to infer that using either real (par-ticularly UKBONDS) or nominal interest rates tomeasure the push factors may not make muchmaterial difference to the findings.

Table 4, which is based on the differencingmethod, shows the relative importance of the pulland push factors in explaining portfolio inflows ineach country. While the results discussed aboveprovide a general picture of the significance of ourexplanatory variables they cannot be used, in theirpresent form, to assess the impact each of our ex-planatory variables had on the dependent variablein each country. To construct Table 4, we differen-tiate each of our variables (in each country) be-tween 1984 and 1994 period and multiply this re-sultant difference by the estimated coefficient foreach variable using the results from Table 2. This

procedure allows us to determine the extent towhich portfolio flows were being explained by thechange in our regressors in each country.

Table 4 reveals regional differences in the re-sults. In Latin American economies, the pull fac-tors as represented (in particular) by the real shareprice index dominate the push factors. On the other

hand, the push factors are more influential thanthe pull factors in Asian economies. These resultsmight be reflecting the fact that Latin Americaneconomies were able to obtain portfolio capital in-flows following serious economic policy reforms.21

The performance of the stock market may haveindicated bright investment prospects in the LatinAmerican economies. On the other hand, mostAsian economies have not experienced domesticeconomic problems to the extent that Latin Ameri-can economies have22. As a result, domestic eco-nomic factors in Asian countries may not have beenissues of concern to investors. Thus we would ex-pect that since there was nothing new in domesticfactors, then changes in external factors would in-stead be more likely to be the dominant factors inAsia.

We created USHPI, obtained as a product ofUSRT and SHP, to gauge the influence of the inter-active effects. A negative statistically significantcoefficient of this term would suggest the impor-tant facilitating role of the pull factors to the pushfactors. On the other hand, an insignificant coeffi-cient of this term would imply that portfolio flowswould occur on the basis of developments in USinterest rates irrespective of the domestic economicconditions.

Table 5 provides estimation results with USHPIincluded. The multiplicative variable is highly sig-nificant, with the expected negative coefficient, butsome (domestic) macroeconomic variables (i.e., CAand FRIM) have much diminished importance. Theexternal factor variable (USRT) also loses its sig-nificance and has an unexpected positive sign.Nevertheless, the significance of the multiplicativevariable indicates strong support for the hypoth-

Variable Coefficient Standard Error T-stat Prob. value

USRT -.3013 0.0990 -3.043 .0028

SHP .4268 .1086 3.930 .0001

CA .1116 .0496 2.252 .0258

FRIM .0224 .0132 1.695 .0922

F[12, 140) = 6.19 R2 = .3467 R

2 = .2908

Estimated Autocorrelation = .088296

Akaike info. Criteria = 4.852

N = 153 Degrees of Freedom = 140

TABLE 3: RESULTS OF FIXED EFFECTS MODEL (1980–96, PIRD AS DEPENDENT VARIABLE)

19We experimented with real share price index adjustedfor stock market liberalisation. To do this we createddummy variables to capture dates in which stock mar-kets were liberalised. We then regressed real shareprice index on these dummies and consequently re-placed real share price index by the resultantresiduals. Our results were similar to those that wereobtained here.

20We experimented with dropping Malaysia from the re-gression (results not shown) since it was suggested inSection 3 that, unlike most other countries, it hadexperienced negative portfolio inflows during most ofthe study period. Our basic results were not affected.

21Edwards (1999) makes a similar point.

22East Asia’s financial crisis started (in earnest) in 1997,i.e. outside our period of study.

LESEDI SENATLA

18

esis of an interaction between domestic and exter-nal economic factors.

Instrumental Variable EstimationAlthough the interest rate variables can reason-ably be taken as exogenous there is possibleendogeneity between portfolio flows and the shareprice index, the current account and foreign ex-change reserves. It could be argued that the cur-rent account balance, foreign exchange reservesand the share price index variables increased as aresult of portfolio inflows. The problem ofendogeneity (or correlation between regressors andthe disturbance term), however, exists only in thefixed effects but not the random effects model. Thefixed effects model is calculated based on OLSmethod while the random effects model relies onGLS method.

We chose as instruments one-period lagged val-ues of CA, FRIM and SHP variables. Table 6 presentsthe instrumental variable estimation results. Thepicture that emerges is very much the same as inTable 3. Thus, consistency of the estimates doesnot seem to have been affected by the suspectedendogeneity of the regressors.

Comparative results implicationsComparative results implications with the previ-

ous literature are not easy because of differencesin countries covered, estimation techniques and soforth. Still, the central issue is the same, viz. thequestion of the relative importance of the push andpull factors in driving portfolio capital flows to Asianand Latin American economies.

Fernandez-Arias (1996) and Calvo et al. (1993)conclude that emerging market economies aremostly vulnerable to external economic develop-ments. They argue that a rise in US interest rateswould lead to an outflow of capital from emergingmarket economies. According to these authors,domestic economic factors play no role in capitalmovements. Our results do not entirely supportthese authors’ strong policy conclusions. We findthat both the push and pull factors have signifi-cant influences on portfolio capital flows. But, wealso find that the relative importance of the push

and pull factors differ by region. Indeed, as shownabove, our findings suggest that the domestic (pull)factors – through the real share price index, in par-ticular – dominate the external factors in LatinAmerican economies. Only in the Asian economies’case do our results appear to concur with theseauthors’ findings in stressing the dominating im-portance of the push over the pull factors. The rea-sons for the regional differences were explainedabove.

Push factor Pull factors

Country USRT SHP FRIM CA

Argentina 1.76 2.54 0.77 0.39

Brazil 1.76 2.31 0.55 0.03

Chile 1.76 1.85 0.95 -1.17

Mexico 1.76 2.65 -0.92 1.24

Philippines 1.76 1.36 0.34 0.16

Malaysia 1.76 0.48 0.35 0.02

Thailand 1.76 0.94 0.75 0.10

Indonesia 1.76 0.81 0.07 -0.17

Korea 1.76 0.82 0.30 -0.01

TABLE 4: DECOMPOSITION OF THE PUSH AND PULL FACTORS BASED ON DIFFERENCING (1984–1994, PERCENTAGE OF

GDP).

Variable Coefficient Standard Error T-Stat. Prob. Value

α -6.1385 2.4285 -2.528 .0115

USRT .4681 0.2465 1.899 .0575

USHPI -.1276 .0373 -3.421 .0006

SHP 1.6063 .3626 4.430 .0000

CA .0698 .0482 1.448 .1476

FRIM .0081 .0118 0.684 .0494

Breusch &

Pagan LM testa

2.62

Hausman testbc

1.70

R2

0.3199

TABLE 5: RESULTS OF RANDOM EFFECTS MODEL (GLS ESTIMATOR) INCLUDING USHPI (1980–96, PIRD AS DEPENDENT

VARIABLE)

Notes a and

b the same as in Table 2.

c Tabulated critical values are the same as in Table 3.

PORTFOLIO CAPITAL FLOWS TO DEVELOPING COUNTRIES 1980–1996: AN EMPIRICAL INVESTIGATION

19

Taylor and Sarno’s findings are most consist-ent with ours in emphasising the importance of boththe push and pull factors. But the details are dif-ferent. While their results suggested that interestrates are a more important determinant of portfo-lio flows to Latin America than to Asia, our resultssuggest the opposite.