the resource revolution

TRANSCRIPT

McKinsey Global InstituteSustainability and Resource Productivity Practice

October 19, 2011

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

The Resource Revolution: Meeting the needs of the next 3 billion middle class consumers

McKinsey & Company 1|

Summary

▪ The next twenty years will see an 35% increase in resource demand, driven by 3 billion new middle-class consumers

▪ A resource revolution is needed with 3 main components1. Aggressively going after currently available productivity

opportunities2. Enhancing access to resource supply3. Accelerating the next frontier of resource innovation

▪ There are 7 priority areas for action to realize this resource revolution

– 4 areas relate to “classic” market failures – e.g., lack of property rights, pricing of externalities, capital market failures, dealing with the public good nature of innovation

– The other 3 areas go beyond standard market failures, and include the need for new, integrated institutional approaches toresource governance, building awareness of resource-related risks, and shaping mindsets and consumer behaviour

McKinsey & Company 2|

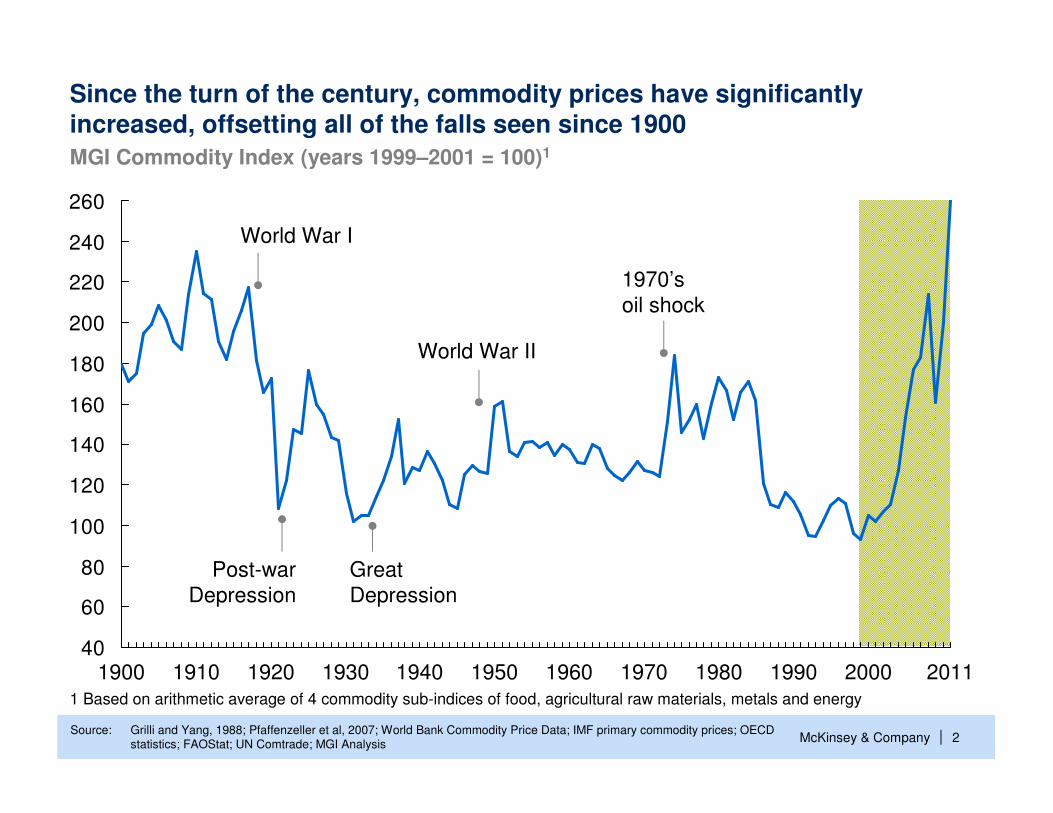

Since the turn of the century, commodity prices have significantly increased, offsetting all of the falls seen since 1900

40

60

80

100

120

140

160

180

200

220

240

260

201120001990198019701960195019401930192019101900

World War I

Post-warDepression

Great Depression

World War II

1970’soil shock

MGI Commodity Index (years 1999–2001 = 100)1

Source: Grilli and Yang, 1988; Pfaffenzeller et al, 2007; World Bank Commodity Price Data; IMF primary commodity prices; OECD statistics; FAOStat; UN Comtrade; MGI Analysis

1 Based on arithmetic average of 4 commodity sub-indices of food, agricultural raw materials, metals and energy

McKinsey & Company 3|

39

14

38

56

471513

212220

Resource price volatility is at an all time high, with the exception of energy in the 1970s Annual price volatility1

%

32

6

21

93

13171110

25

7

28

102120

89151514

87

26

131110917

11202424

15

89796959493929191909 201199

Energy

Food

Metals

Agricultural materials

SOURCE: Grilli and Yang; Pfaffenzeller; World Bank; International Monetary Fund; Organisation for Economic Co-operation and Development statistics; UN Food and Agriculture Organization; UN Comtrade; McKinsey analysis

1Calculated as the standard deviation of the commodity subindex divided by the average of the subindex over the time frame.

McKinsey & Company 4|

The emergence of 3 billion middle-class consumers will drive future demandGlobal middle class1

Billions of people

Middle East and North Africa

Sub-Saharan Africa

2030

3.23Central and South America

4.88

3 billion

Asia-Pacific

North America

Europe

0.68

0.32

0.310.23

0.11

2020

3.25

1.74

0.70

0.33

0.250.170.06

2009

1.85

0.53

0.66

0.340.18

0.11 0.03

SOURCE: Organisation for Economic Co-operation and Development (OECD) Development Centre

1 Global middle class defined as daily expenditures between $10 and $100 per person in purchasing parity terms.

McKinsey & Company 5|

0

50

100

150

200

250

Per capita energy consumptionMillion British thermal units/person, 1970–2008

Per capita GDPReal $ PPP/person

45,00040,00035,00030,00025,00020,00015,00010,0005,0000

Many countries have shown that as incomes rise, demand for resource increases—and a similar curve is likely in China and India

SOURCE: International Energy Agency; Global Insight; McKinsey analysis

Historical range for energy consumption evolution

China 2030 projected

India 2030 projected

India

China

South Korea

Japan

Germany

France

United Kingdom

Australia

United States

ENERGY EXAMPLE

McKinsey & Company 6|

30

35

80

Land 10-15

Water

Energy

Steel

Demand is projected to grow by 10 to 80 percent across resources

Demand increase, 2010-30% 2030 projected demand

2,290 million metric tons of iron ore

664 QBTU

5.9 trillion cubic meters

1.715-1.755 billionhectares of cropland

60% of growth in energy demand to come from

India and China

McKinsey & Company 7|Source: McKinsey analysis

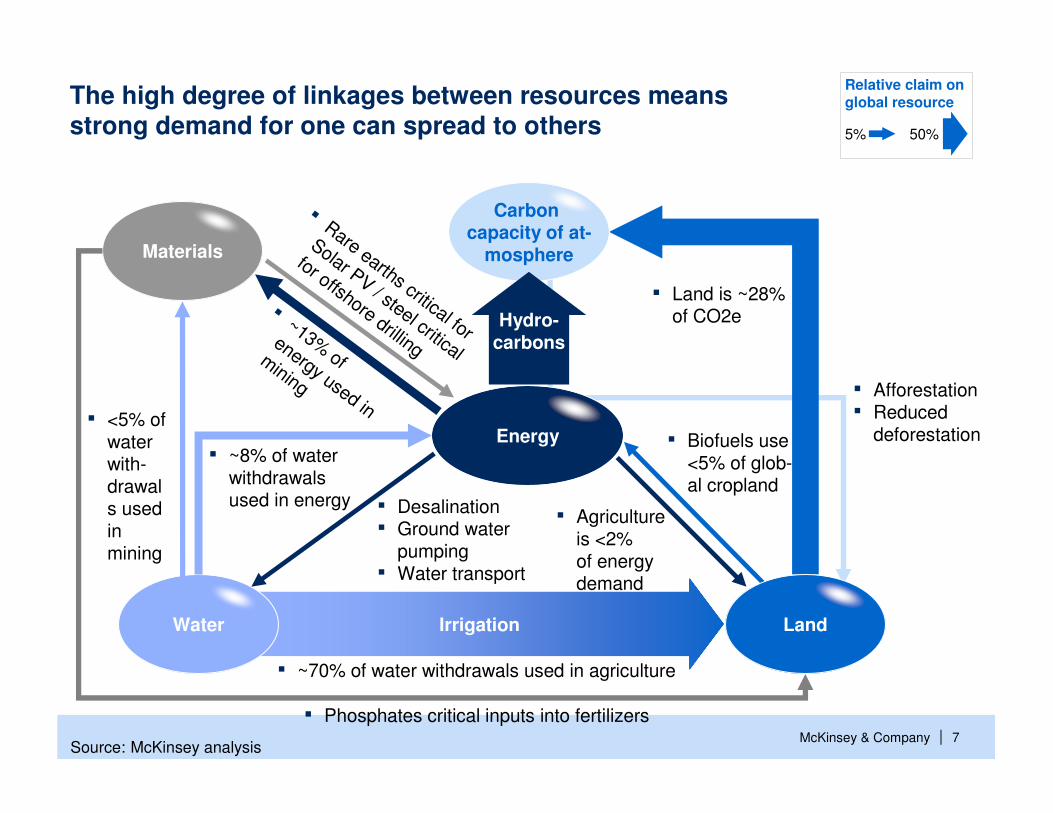

The high degree of linkages between resources means strong demand for one can spread to others

Relative claim on global resource

5% 50%

Energy

Water Irrigation

▪ Desalination▪ Ground water

pumping▪ Water transport

▪ Biofuels use<5% of glob-al cropland

▪ Land is ~28% of CO2e

▪ Afforestation▪ Reduced

deforestation

▪ ~70% of water withdrawals used in agriculture

Materials

▪ ~8% of waterwithdrawals used in energy

▪~13%

of

energy used in

mining

▪Rare earths critical for

Solar PV / steel critical

for offshore drilling

▪ Agriculture is <2%of energy demand

▪ <5% of water with-drawals used in mining

▪ Phosphates critical inputs into fertilizers

Carbon capacity of at-

mosphere

Land

Hydro-carbons

McKinsey & Company 8|

IMF estimates that a 10 percent increase in the price of crude reduces global GDP by 0.2%-0.3% in one year

World Bank estimates that recent food price increases drove 44 million people into poverty

The world is currently subsidizing its resources by at least $0.9 to $1.3 trillion. At least 8 countries commit 5% or more of their GDP to energy subsidies

These resource trends pose several risks to global growth and welfare

Just four countries—Iran, Iraq, Saudi Arabia, and Venezuela—hold almost 50 percent of known oil reserves

The Stern Review forecasts climate change scenarios which could result in economic losses equivalent to a 20 percent reduction in current per capita consumption

McKinsey & Company 9|

There are productivity opportunities that could meet 13 to 28 percent of resources demand

SOURCE: McKinsey analysis

WaterCubic meters

LandMillion ofcropland hectares

Primary energyQBTU

SteelMillion of tonnesof steel equivalent

146 518664

-22%494

1,9952,290

-13%2951,270

6,3505,000–5,200 -18–21%

1,150–1,3504,500

1,215–1,320 -25–28%

Remaining 2030 demand

Productivity improvements

435–500

2030 base case demand

1,715–1,755

2010 demand

1,535

McKinsey & Company 10|

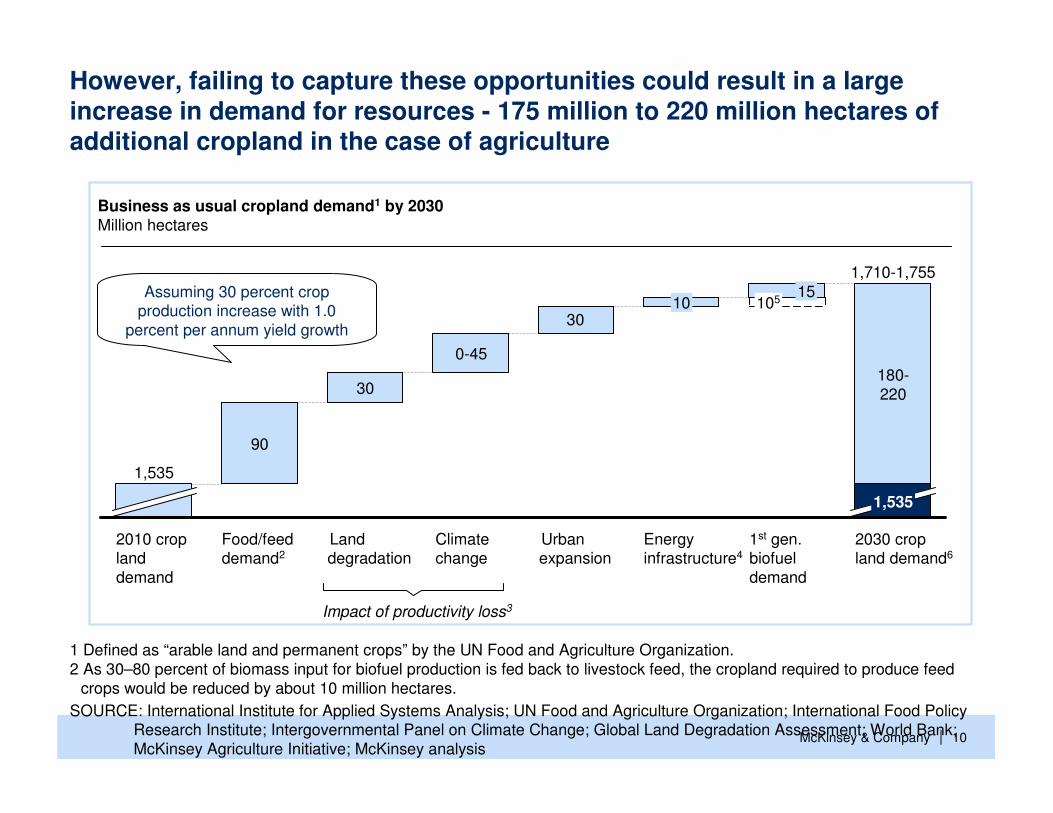

However, failing to capture these opportunities could result in a large increase in demand for resources - 175 million to 220 million hectares of additional cropland in the case of agriculture

Business as usual cropland demand1 by 2030Million hectares

30

2030 crop land demand6

1,710-1,755

1,535

180-220

1st gen. biofueldemand

10515

Energy infrastructure4

10

Urban expansion

Climatechange

0-45

Land degradation

30

Food/feed demand2

90

2010 crop landdemand

1,535

Impact of productivity loss3

Assuming 30 percent crop production increase with 1.0

percent per annum yield growth

SOURCE: International Institute for Applied Systems Analysis; UN Food and Agriculture Organization; International Food Policy Research Institute; Intergovernmental Panel on Climate Change; Global Land Degradation Assessment; World Bank; McKinsey Agriculture Initiative; McKinsey analysis

1 Defined as “arable land and permanent crops” by the UN Food and Agriculture Organization. 2 As 30–80 percent of biomass input for biofuel production is fed back to livestock feed, the cropland required to produce feed

crops would be reduced by about 10 million hectares.

McKinsey & Company 11|

Developing countries account for 70 to 85 percent of the productivity opportunities

Latin America

Europe (OECD/ EU-27)

United States and Canada

Rest of developing Asia1

IndiaMiddle East

Russia and Eastern Europe

11

7

13

8

Global air and sea (energy only)

5

5

3

6 China

Developed Asia-Pacific

40

14

10

32

5

8

2

2

3

10

20

16

8

3

8

10

8

9

7

8

10

7

8

9

6

5

14

14

6

% of total productivity opportunity by resource and region

Developed Developing

Total opportunityPercent

28

27

72

73Steel

Water 16 84

Land 17 83

Energy

1

15

22

3Africa

1 Rest of developing Asia includes Central Asia (e.g., Uzbekistan), South Asia (e.g., Bangladesh), Southeast Asia (e.g., Laos), and North Korea.2 Includes water savings from water-specific levers as well as water savings from improved agricultural productivity.3 For steel, the chart represents all the demand-side levers and the scrap recycling lever, but excludes supply- and conversion-side levers.

SOURCE: McKinsey analysis

McKinsey & Company 12|

15 key groups of opportunities represent over 70% of the resource savings

68

83

87

98

Improved irrigation techniques

Improved power conversion

Petroleum and gas energy efficiency

Reducing land degradation

Iron and steel energy efficiency 117

Improved energy extraction 120

Smallholder farm yields 127

High strength steel adoption 132

Alternative drive trains 152

Transport efficiency 154

Reducing leakage 166

Urban densification 171

Food waste 221

Commercial farm yields 236

Building energy efficiency 691

Other 902

Total resource benefit1 by opportunity area2010 USD billion

Average cost efficiency2 “Metrics that matter” for monitoring progress

SOURCE: McKinsey Global Institute analysis

1 Based on current prices for energy, steel, and food plus unsubsidized water prices and a shadow cost for carbon 2 Annualised cost of implementation divided by annual total resource benefit3 Includes feed efficiency, industrial water, air transport, municipal water, steel recycling, waste water reuse, and other industrial energy efficiency

0.7

0.3

0.4

0.6

0.6

0.2

0.5

0.4

0.4

1.7

0.6

0.2

0.5

0.6

0.5

0.5 Weather adjusted building efficiency, kWH/m2/degree day

Food waste in value chain (e.g., post harvest), %

Commercial farm yield relative to agro-ecological potential, %

Public transport use, % of commuters metro/bus

Smallholder farm yield relative to agro-ecological potential, %

High strength steel penetration, %

Net rate of land degradation, hectares per year

Energy efficiency of steel production, QBTU/tonne

Conversion efficiency of coal and gas fired power plants, %

Recovery rate of a given reserve, %

Penetration of key alternative drive trains, %

Energy efficiency of P&G production, QBTU/tonne

Fuel efficiency, litres/kilometre

Municipal water leakage, %

Adoption of micro-irrigation technologies, %

2030 potential savingsWater

Steel Energy

Land

McKinsey & Company 13|

200 6000 1,4001,2001,000800

Cost efficiency of investmentUSD spent for implementation perUSD total resource benefit

3.0

2.0

2.5

-0.5

Total annualresource benefit1

2010 USD billions

3,4002,4002,2002,0001,8001,600 3,2003,0002,8002,600

0.5

1.0

400

1.5

0.0

Prevention of degraded land

Building envelope - retrofit, commercial

Water efficiency - Industrial

Appliances - residential

Leakage reduction

Appliances - residential

Enhanced oil recovery

High strength steel – construction, columns and beams

Improved commercial yields – developing, politically unstable, low infrastructure

Food waste reduction –processing/packaging/distribution

LDV gasoline plugin hybrid

Building envelope - package 2, residential

Efficiency package -new build, residential

Energy efficiency in other industries

Restoration of degraded land - Severe

These opportunities can be laid out in a integrated resource cost curve

SOURCE: McKinsey Global Institute analysis

1 Based on current prices for energy, steel, and food plus unsubsidized water prices and a shadow cost for carbon at a discount rate of 4% per annum

Water

Energy

Land

Steel

2030 total resource savings1

LDV electric vehicles

Lighting – switch from CFLs to LEDs

Improved feed efficiency

Electronics - consumer, residential

Smallholder yield improvement –politically stable, high infrastructure

Food waste reduction – post harvest, non-perishable crops

Savings can amount to up to $3.5 trillion with 90% having positive returns if the true cost of carbon and water are included

McKinsey & Company 14|

Achieving the main productivity opportunities will require overcoming a multitude of barriers

158

Reducing leakage 166

Urban densification 175

Food waste 221

Commercial farm yields 236

Building energy efficiency 691

Other2 867

Improved irrigation techniques 68

Petroleum and gas energy efficiency 87

Improved power conversion 91

Reducing land degradation 114

Improved energy extraction 120

Smallholder farm yields 127

High strength steel adoption 132

Iron and steel energy efficiency 144

Alternative drive trains 155

Transport efficiency

Total resource benefit1

by opportunity area2010 $ billion

SOURCE: McKinsey analysis

1 Based on current prices for energy, steel, and food plus unsubsidized water prices and a shadow cost for carbon. 2 Includes feed efficiency, industrial water, air transport, municipal water, steel recycling, waste water reuse, and other industrial energy efficiency.

2030 potential savings by feasibility

Readily achievable

Some challenges

Difficult

Overall feasibility of implementation

Cap

ital i

ntensi

ty

Ret

urn o

n inve

stm

ent

Supply c

hain b

ottlen

ecks

Cap

ital a

vaila

bility

Reg

ulato

ry is

sues

/

proper

ty ri

ghts

Technolo

gical

read

ines

s

Entren

ched

beh

avio

rs

Key barriers

Agen

cy is

sues

Politic

al fe

asib

ility

Info

rmat

ion fa

ilure

s

McKinsey & Company 15|

Carbon emissions footprint, 2030

Gt CO2e

Additional investments for 450ppm pathway

SOURCE: McKinsey Global GHG Cost Curve Version 2.1; Team analysis

A shift in energy mix and pursuing additional land carbon abatement can be used to close the remaining gap to a 450ppm pathway

6

10

9

6 35

68

Required emissions for 450 ppmpathway

Additional agriculture and forestry abatement

Shift in power mix plus CCS

Scale up of sugarcane and 2nd

generation biofuels

EnergyCroplandSteelBAUemissions

1

1

Carbon abatement from “Productivity Response”

McKinsey & Company 16|

Power mix shifts significantly in the climate change case, while mix assumed constant in productivity response

SOURCE: McKinsey analysis (carbon cost curve v3.0)

Share of global power production (TWh); Percent

Current state (2010)

2

100% =

2010

21,186

2 0

17

13

05

22

40

Supply expansion

21 21

42 43

25

100% =

2030

34,776

3 1

14

11

0 2

2020

28,114

14

15

12

0 3

Climate change response

Other RE

Solar

Wind

Hydro

Nuclear

CCS

Oil

Gas

Coal

Productivity response1

21 21

42 43

25

100% =

2030

29,363

3 1

14

11

0 2

2020

25,471

14

15

12

0 3

9

17

24

14

25

13

9

100% =

2030

29,363

7

15

18

61

2020

25,471

63

16

15

0 2

1 Production mix is based on total electricity demand and scaled in proportion to the BAU production mix

McKinsey & Company 17|

Capital investment will increase significantly under all three cases

SOURCE: McKinsey Global Institute analysis

Water

Land

Energy

Steel

2030 cases

Average annual capital expenditure requirements1; USD billions; 2010-2030; 2010 dollars

310

Climate change response

420-480

Productivity response

385-445

Supply expansion

345-405

2010 capex

1 Does not include capex for BAU productivity improvements; includes impact of Capex flareups due to supply constraints

445-475445-475500-550350

270 400-510400-510510-600

1,000

1,840-1,9151,415-1,490

2,400-2,465

McKinsey & Company 18|

Price signals drive productivity: The 40 percent variation in engine efficiency across many G-20 countries relates closely to the cost of fuel

~40%

1 Light-duty vehicles only.

0 30 60 90 120 150 180

Engine efficiency1

Kilometers per liter

9.5

9.0

12.5

12.0

11.0

10.5

10.0

0

Total gasoline and diesel tax at pump$ per barrel

United States

United Kingdom

South Africa

Russia

Mexico

Japan

Italy

India

Germany

FranceChina

Canada

Brazil

11.5

SOURCE: McKinsey analysis

McKinsey & Company 19|

Create efficient and integrated institutional approaches

Build awareness of risks

Develop skills and address mindsets

Address property rights and agency issues

Support access to capital

Ensure competitive investor returns

Accelerate and deepen innovation systems

Addressclassic “market failures”

Address “critical enablers”

There are 7 priority actions to capture this resource revolution

McKinsey & Company 20|

There is a need to tackle these issues in a holistic way: Agriculture example

Create efficient and integrated institutional approaches

Build awareness of risks

Develop skills and address mindsets

Address property rights and agency issues

Support access to capital

Ensure competitive investor returns

Accelerate and deepen innovation systems

Addressclassic “market failures”

Address “critical enablers”

Large barrier

Medium barrier

Small barrier

Lack of clear property rights make it difficult to invest in equipment and expand farm size

Over 70% of agriculture productivity opportunities have an IRR>10%

Public R&D to agriculture has fallen and is lower than in other sectors (e.g., automotive)

Annual investment in agriculture may need to increase by 50% and over 80% of opportunities are in developing countries

Lack of early warning systems on food availability, including linkages with other resources

Limited mechanisms to share best practice across countries; lack of core capabilities in many agriculture ministries

Large behavioral change needed to support new technologies (e.g., post-harvest waste)