the retailer - ey’s publication in consumer products and retail sector april - june ·...

TRANSCRIPT

The retailerEY’s publication in consumer products and retail sector

April - June 2015

ForewordDear reader,

We are delighted to present the April-June 2015 edition of The retailer, our quarterly publication in the consumer products and retail sector.

In the first article, we have provided an overview of Goods & Services Tax (GST), which is one of the most significant tax reforms in India’s tax history, and highlighted key business considerations for GST readiness.

The second article provides a perspective on franchising in traditional segments in health care, taking alternate therapies as an example. The article highlights possible models, which these businesses could evaluate to expand their offering.

Our third article is a snapshot of our annual Enterprise IT Trends and Investments Survey titled “SMAC 3.0: Digital is Here” and covers the journey of the Social, Media, Analytics and Cloud (SMAC), areas that have been

the latest buzzwords among IT strategists.

Finally, we continue our featured section, the “Innovation board”, where we aim to present snapshots of recent innovations, which have emerged in the Indian and global luxury market.

We hope you enjoy reading this issue of the retailer and look forward to your valuable comments and feedback.

Pinakiranjan Mishra

Partner and National Leader, Retail and Consumer Products EY, India

Celebrating six years of The retailer

Contents

Involve yourself:

We look forward to hearing your feedback and suggestions.To contribute to editorial content, please contact Ashish KakwaniT: +91 22 6192 0423 E: [email protected]

ABC of GST and the key business considerations 04

Franchising opportunities in alternate therapy healthcare services - perspectives 12

Summary: SMAC 3.0: Digital is Here 18

Innovation board 24

4 | The retailer

ABC of GST and the key business considerations

1

What is GST?

The Goods and Services Tax (GST) is expected to be the most significant tax, or more so, business transformation reform in the fiscal history of India. It is likely to impact prices, business processes, investments and profitability in all segments of the economy.

GST is a comprehensive tax levied on manufacture, sale and consumption of goods and service at a national level. Under GST there will be no difference between goods and services. Only the final consumer will bear the tax on value addition at every stage from producer/service provider to the retailer. It tries to eliminate indirect taxes and mitigate cascading or double taxation issues and leads to a common national market, with elimination of state boundaries.

Source: EY analysis

Evolution of GST

2006

2007

2007 2008

2008

Phasing out of CST began from April, 2007 with the reduction in CST rate from 4% to 3%.

.

Budget 2006-07 – FM proposed introduction of GST from April, 1 2010.

Study Paper on GST authored by Dr. Parthasarathy Shome was released.

Empowered Committee of State Finance Ministers constituted Joint Working Group in May, 2007

CST rate was further reduced from 3% to 2% in June, 2008

EC finalized its views on broad GST structure – consensus on Dual GST (Central and state GST),separate legislation, levy and administration.

2009 2013

2013

First Discussion Paper on GST was released by EC.

The 13th Finance Commission released its Report on GST in Dec, 2009

EC rejected Central Govt’s proposal to include petroleum products under GST in Nov, 2013

Standing Committee on Finance tabled its Report on GST Bill in August, 2013

2009

Constitution Amendment Bill to enable roll out of GST was tabled in Parliament.

.

2011

2014

June 2014 - Passed in Lok Sabha (awaiting Rajya Sabha approval

2007

5The retailer |

GST is a need of the hour

The need to implement GST arises from the inherent complexity in the existing tax system in India. GST is needed to simplify the existing complex tax structure; minimize the cascading effects of double taxation, streamline interstate transactions and make doing business in India easier for Indian as well as multinational companies (MNCs).

Why GST since VAT is there?

GST is a destination-based consumption tax (similar to VAT). VAT was implemented first in 2005. Despite the success of VAT, there are still certain shortcomings in its structure, both at the center and the state level.

Source: EY analysis

Source: EY analysis

Why is GST needed?

Shortcomings of VAT

Double taxation

Center

• Elimination of cascading effect of taxes at various stages

• Tax computation to become simpler in cases where value of goods and services need to be split for separate taxation

• Full input tax credit possible at the Central and state level

• Smoothen the tax structure and make tax return filing less cumbersome

• Input credit is available only on the excise duty paid on raw material.

• No input credit is paid on other taxes and duties on post-manufacturing activities.

• Although, there is CENVAT, other taxes, e.g., surcharges, additional customs duties is not included.

• Services are taxed selectively and only at the center; input credit on service tax paid is allowed only to a limited extent.

International standards

Inter-state

• GST – an international standard

• Important factor in investment decisions for MNCs

• Non-implementation of GST – a major disadvantage for India vis-à-vis other destinations with GST

• Would help attract more FDIs and FIIs

• Inter-state tax (CST) is levied on inter-state transfer of goods. There is no provision for input credit on CST. Manufacturers producing goods in one state and distributing them in other states, end up paying taxes in each state.

Interstate transactions

State

• Ease in getting full input tax credit

• Will streamline compliance and administrative procedures across states, and between states and the Center

• Reduce administrative costs and help develop a common national market

• Doing business is likely to become easy and boost overall economic growth

• States charge VAT on the excise duty paid to the Center.

• CENVAT is allowed on goods remains included in the value of goods to be taxed.

• Many states still charge various indirect taxes, such as luxury tax, entertainment tax, and there is no input tax credit in case of CENVAT paid on certain items.

6 | The retailer

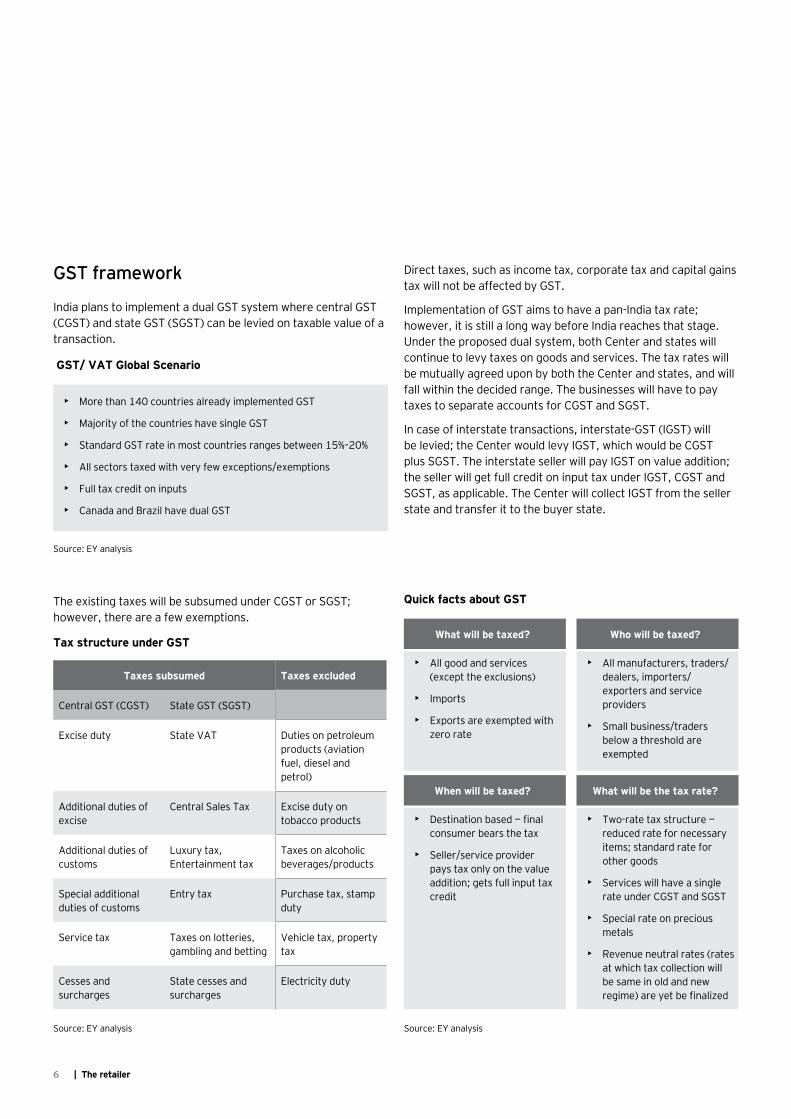

GST framework

India plans to implement a dual GST system where central GST (CGST) and state GST (SGST) can be levied on taxable value of a transaction.

The existing taxes will be subsumed under CGST or SGST; however, there are a few exemptions.

Taxes subsumed Taxes excluded

Central GST (CGST) State GST (SGST)

Excise duty State VAT Duties on petroleum products (aviation fuel, diesel and petrol)

Additional duties of excise

Central Sales Tax Excise duty on tobacco products

Additional duties of customs

Luxury tax, Entertainment tax

Taxes on alcoholic beverages/products

Special additional duties of customs

Entry tax Purchase tax, stamp duty

Service tax Taxes on lotteries, gambling and betting

Vehicle tax, property tax

Cesses and surcharges

State cesses and surcharges

Electricity duty

Direct taxes, such as income tax, corporate tax and capital gains tax will not be affected by GST.

Implementation of GST aims to have a pan-India tax rate; however, it is still a long way before India reaches that stage. Under the proposed dual system, both Center and states will continue to levy taxes on goods and services. The tax rates will be mutually agreed upon by both the Center and states, and will fall within the decided range. The businesses will have to pay taxes to separate accounts for CGST and SGST.

In case of interstate transactions, interstate-GST (IGST) will be levied; the Center would levy IGST, which would be CGST plus SGST. The interstate seller will pay IGST on value addition; the seller will get full credit on input tax under IGST, CGST and SGST, as applicable. The Center will collect IGST from the seller state and transfer it to the buyer state.

GST/ VAT Global Scenario

Tax structure under GST

Quick facts about GST

Source: EY analysis

Source: EY analysis Source: EY analysis

• More than 140 countries already implemented GST

• Majority of the countries have single GST

• Standard GST rate in most countries ranges between 15%–20%

• All sectors taxed with very few exceptions/exemptions

• Full tax credit on inputs

• Canada and Brazil have dual GST

What will be taxed? Who will be taxed?

• All good and services (except the exclusions)

• Imports

• Exports are exempted with zero rate

• All manufacturers, traders/dealers, importers/ exporters and service providers

• Small business/traders below a threshold are exempted

• Destination based — final consumer bears the tax

• Seller/service provider pays tax only on the value addition; gets full input tax credit

• Two-rate tax structure — reduced rate for necessary items; standard rate for other goods

• Services will have a single rate under CGST and SGST

• Special rate on precious metals

• Revenue neutral rates (rates at which tax collection will be same in old and new regime) are yet be finalized

When will be taxed? What will be the tax rate?

7The retailer |

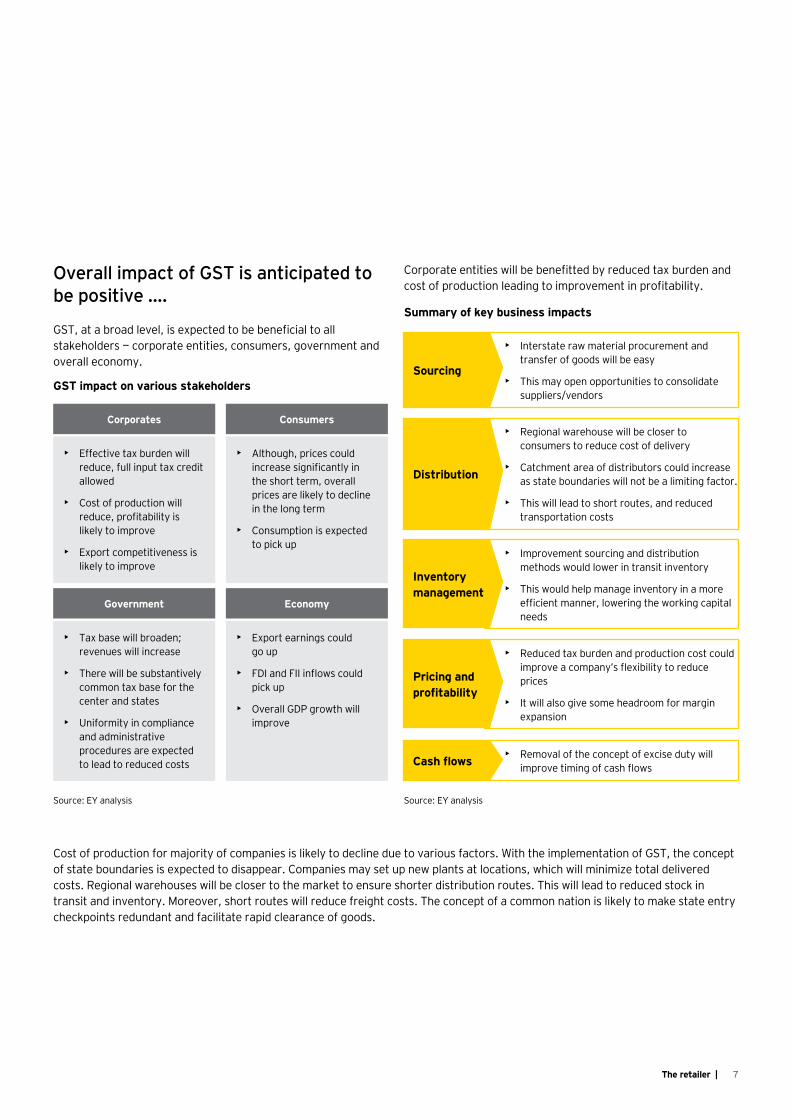

Overall impact of GST is anticipated to be positive ….

GST, at a broad level, is expected to be beneficial to all stakeholders — corporate entities, consumers, government and overall economy.

GST impact on various stakeholders

Source: EY analysis Source: EY analysis

Corporates Consumers

• Effective tax burden will reduce, full input tax credit allowed

• Cost of production will reduce, profitability is likely to improve

• Export competitiveness is likely to improve

Government Economy

• Tax base will broaden; revenues will increase

• There will be substantively common tax base for the center and states

• Uniformity in compliance and administrative procedures are expected to lead to reduced costs

• Export earnings could go up

• FDI and FII inflows could pick up

• Overall GDP growth will improve

Corporate entities will be benefitted by reduced tax burden and cost of production leading to improvement in profitability.

Summary of key business impacts

• Interstate raw material procurement and transfer of goods will be easy

• This may open opportunities to consolidate suppliers/vendors

Sourcing

• Regional warehouse will be closer to consumers to reduce cost of delivery

• Catchment area of distributors could increase as state boundaries will not be a limiting factor.

• This will lead to short routes, and reduced transportation costs

Distribution

• Improvement sourcing and distribution methods would lower in transit inventory

• This would help manage inventory in a more efficient manner, lowering the working capital needs

Inventory management

• Reduced tax burden and production cost could improve a company’s flexibility to reduce prices

• It will also give some headroom for margin expansion

Pricing and profitability

• Removal of the concept of excise duty will improve timing of cash flowsCash flows

• Although, prices could increase significantly in the short term, overall prices are likely to decline in the long term

• Consumption is expected to pick up

Cost of production for majority of companies is likely to decline due to various factors. With the implementation of GST, the concept of state boundaries is expected to disappear. Companies may set up new plants at locations, which will minimize total delivered costs. Regional warehouses will be closer to the market to ensure shorter distribution routes. This will lead to reduced stock in transit and inventory. Moreover, short routes will reduce freight costs. The concept of a common nation is likely to make state entry checkpoints redundant and facilitate rapid clearance of goods.

8 | The retailer

… however, there are some concerns

Spike in inflation over the short term

There is a risk of price hikes in the short run if tax rates are very high. “If rates are high, these will lead to inflation, which will be detrimental to consumers. The empowered committee had suggested a revenue-neutral rate of 27%; it should ideally be below 20%. Earlier studies had suggested that it should be between 12%–16%, if goods have to be competitively priced and there is no inflationary pressure,” said Harsh Mariwala, Chairman of Marico .

Consumers are expected to benefit from reduced prices of goods and services, which in turn increase consumption. Improved demand, and simplified tax structure will help attract increased FDIs and FIIs and boost overall economic growth. At the same time state and Central governments are likely to benefit from a broader tax base.

Other benefits for businesses

Source: EY analysis

Moreover, companies from sectors such as automobiles, pharmaceuticals, consumer products and food processing, which enjoy benefits of tax (excise, VAT, income tax) concessions by setting up factories in the states, which offer concessions, will be affected adversely by GST. Their cost of production could go up, in turn, leading to increased prices.

The phenomenon of spike in inflation was observed in other countries where GST was implemented. In these countries, prices shot up in the short run. Inflation stabilized as the implementation gained pace and there was more clarity among consumers and manufacturers. In India, sharp increase in inflation is likely to be tricky.

Direct dispatches

Opportunities in imports

Depot RoadmapSavings in

manufacturing

CSTService

tax credits

9The retailer |

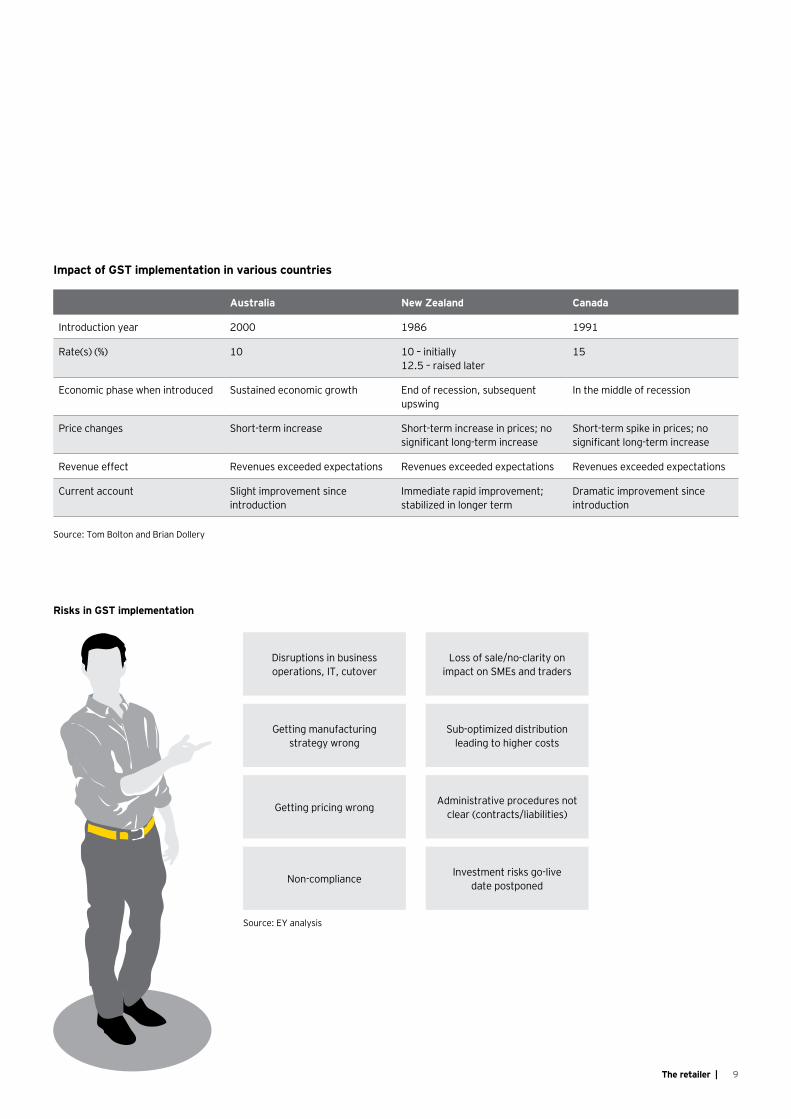

Impact of GST implementation in various countries

Australia New Zealand Canada

Introduction year 2000 1986 1991

Rate(s) (%) 10 10 – initially 12.5 – raised later

15

Economic phase when introduced Sustained economic growth End of recession, subsequent upswing

In the middle of recession

Price changes Short-term increase Short-term increase in prices; no significant long-term increase

Short-term spike in prices; no significant long-term increase

Revenue effect Revenues exceeded expectations Revenues exceeded expectations Revenues exceeded expectations

Current account Slight improvement since introduction

Immediate rapid improvement; stabilized in longer term

Dramatic improvement since introduction

Source: Tom Bolton and Brian Dollery

Risks in GST implementation

Disruptions in business operations, IT, cutover

Getting manufacturing strategy wrong

Getting pricing wrong

Non-compliance

Loss of sale/no-clarity on impact on SMEs and traders

Sub-optimized distribution leading to higher costs

Administrative procedures not clear (contracts/liabilities)

Investment risks go-live date postponed

Source: EY analysis

10 | The retailer

Protect customer experience

Reduce disruptions to day-to-day business operations

Maximize input tax credit

Minimize cash flow impact

Tap on utilize technology platform to automate GST

Produce timely GST reporting

Ensure compliance to GST regulations

Be GST enabled on-tme

In conclusion, a company could look at the following 8 principles while implementing GST.

The implementation of GST could impact the existing processes, people and technology.

0102030405060708

Process People Technology

11The retailer |

Nitesh is a Director with EY’s Advisory Practice focusing on Retail & Consumer Products. He has 14 years of work experience advising clients on key business processes, Enterprise Risk Management (ERM), Governance Risk & Compliance (GRC), data analytics and business transformation. He joined EY in 2003 and is currently based out of Mumbai.

Nitesh has assisted leading companies across Retail & Consumer Product (RCP) sector in India, South Africa, China, Russia, UK & USA in the area of business processes and operations transformation.

Nitesh has been working with one of India’s largest FMCG companies for its GST readiness.

Email: [email protected] Tel: +91 22 6192 3787

Nitesh Mehrotra Director

Inputs from Nivedita Ukidwe, Strategic Market Intelligence, EY Knowledge

12 | The retailer

Franchising opportunities in alternate therapy healthcare services - perspectives

2

Introduction

India is more than a trillion dollar economy and has been one of the fastest growing economies over the last five years. One of the key factors in India’s remarkable growth story is the emergence of a middle class as the largest consuming segment, which propelled domestic consumption.

With the economy opening up, new avenues of earning high levels of income have opened up for the educated and young middle class. This has led to this key consumer segment to have high levels of disposable income and purchasing parity.

Wellness is a prominent industry, which has benefitted from increased consumer spends on wellness products and services. The wellness market in India is estimated to be around US$12–15 billion in 2013 and growing at a CAGR of around 15%.

The wellness offerings in the Indian market can be segmented along hygiene, curative and enhancement needs of the consumer. Curative needs are aligned to prevent diseases, cure ailments and maintain a healthy lifestyle. Alternate therapy products and services intend to satisfy the curative/preventive needs of the consumer and account for approximately 20% of the wellness market in India.

Overview: Alternate therapy market in India

The alternate therapy market in India is estimated at US$2.5 billion in 2013. Reduced cost of alternate therapy treatments and consumers’ perception of alternate medicine causing fewer side effects than allopathic medicine have generated widespread acceptance of alternate therapies among the large cross-section of the population.

Ayurveda is the most widely accepted form of alternate therapy today among Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homeopathy (AYUSH) segments.

Alternate therapy product space is more evolved and organized than services currently. The service delivery market in alternate therapy is fragmented. Retail clinic health care services are riding high on acceptance particularly in Ayurveda. However, presence of trustworthy brands delivering high quality yet cost-effective consumer experience is limited in the Indian market.

Therefore, there is a significant opportunity in the alternate therapy services space given rising consumer awareness on the side effects of allopathic medicine and growing propensity to shift from curative to preventive health care.

Alternate therapy market size (value) in 2013

72%

25%

2%1%

Ayurveda

Homepathy

Unani

Others

13The retailer |

1 Company news reports

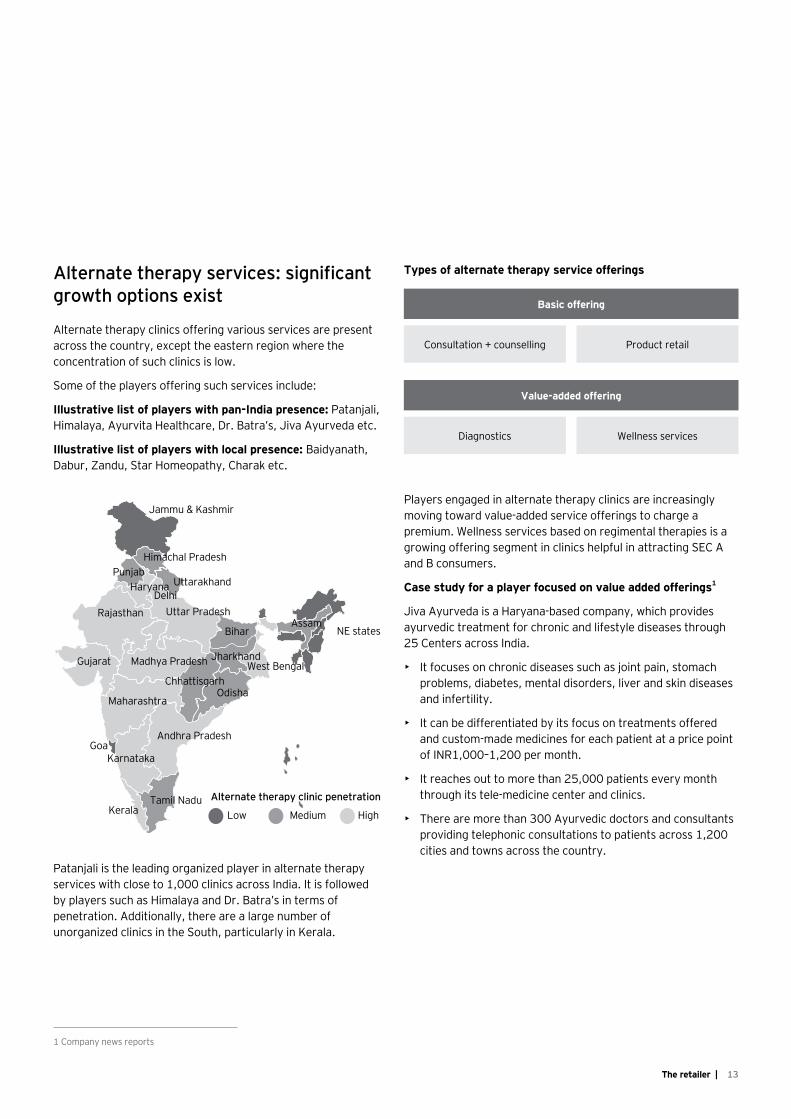

Alternate therapy services: significant growth options exist

Alternate therapy clinics offering various services are present across the country, except the eastern region where the concentration of such clinics is low.

Some of the players offering such services include:

Illustrative list of players with pan-India presence: Patanjali, Himalaya, Ayurvita Healthcare, Dr. Batra’s, Jiva Ayurveda etc.

Illustrative list of players with local presence: Baidyanath, Dabur, Zandu, Star Homeopathy, Charak etc.

Patanjali is the leading organized player in alternate therapy services with close to 1,000 clinics across India. It is followed by players such as Himalaya and Dr. Batra’s in terms of penetration. Additionally, there are a large number of unorganized clinics in the South, particularly in Kerala.

Players engaged in alternate therapy clinics are increasingly moving toward value-added service offerings to charge a premium. Wellness services based on regimental therapies is a growing offering segment in clinics helpful in attracting SEC A and B consumers.

Case study for a player focused on value added offerings1

Jiva Ayurveda is a Haryana-based company, which provides ayurvedic treatment for chronic and lifestyle diseases through 25 Centers across India.

• It focuses on chronic diseases such as joint pain, stomach problems, diabetes, mental disorders, liver and skin diseases and infertility.

• It can be differentiated by its focus on treatments offered and custom-made medicines for each patient at a price point of INR1,000–1,200 per month.

• It reaches out to more than 25,000 patients every month through its tele-medicine center and clinics.

• There are more than 300 Ayurvedic doctors and consultants providing telephonic consultations to patients across 1,200 cities and towns across the country.

Types of alternate therapy service offerings

Rajasthan

Gujarat

Maharashtra

Madhya Pradesh

Uttar Pradesh

Andhra Pradesh

Odisha

Bihar

Jharkhand

UttarakhandPunjab

Jammu & Kashmir

Himachal Pradesh

Tamil Nadu

Karnataka

Kerala

Goa

ChhattisgarhWest Bengal

Haryana

Assam

HighMediumLow

Alternate therapy clinic penetration

Delhi

NE states

Basic offering

Value-added offering

Consultation + counselling

Diagnostics

Product retail

Wellness services

14 | The retailer

Business models for alternate therapy services

Alternate therapy clinics are operated in various models though franchisee route is most preferred for scaling up operations.

Patanjali and Dr. Batra’s seem relevant examples for growth of alternate therapy clinics through the franchisee route. Both players could ramp up to a sizeable extent across the country due to adoption of the franchisee–owned, franchisee-operated model.

Inherent advantages of the franchising option include

• Scalability within a short timeframe and efficiently

• Franchisees are aware of the local sensitivities and can provide constant inputs to business

• Reduced investment commitment needed as franchisees share the investments

• Increased expected ROI for the player

However, franchisee–owned, franchisee-operated model presents several challenges and bottlenecks

• Channel conflicts arise due to price competition among channel partners including franchises

• Brand name of the company can be diluted by franchisee activities

• Franchisees do not share the long-term vision of the brand

• There could be integrity issues with the franchisee entering a competing businesses and distribution/ re-sale of goods to other retailers

Company owned company operated (COCO)

Company owned franchisee operated (COFO)

Franchisee owned franchisee operated (FOFO)

Franchisee owned company operated (FOCO)

Linear

Hybrid

Characteristics Prevalence Examples

• Company owns and sets up clinic

• Company manages operations and bears manpower costs

• Company owns and sets up clinic

• Franchisee manages operations

• Moderate

• Low

• Jiva Ayurveda

• Himalaya

• Dr. Batra

• Patanjali

• Ayurvita

• Dr. Batra

• Himalaya

• Franchisee owns and sets up clinic

• Franchisee manages operations

• Company typically bears manpower

• Franchisee owns and sets up clinic

• Company manages operations and bears manpower costs

• High

• Low

15The retailer |

Strategies to develop a successful franchisee model in alternate therapy services

Some of the key learnings and ideas from industry reveal that franchisee management needs continuous focus for success.

In order to answer the key questions for a franchisee model, there are some imperatives that a player needs to adopt. These are:

• Designing a sound franchisee business proposition: Provide a clear and transparent view of the short to long-term opportunity to a prospective in terms of investments, ROI, responsibilities franchisee will have to take up, key risks and losses in worse-case-scenario and monetary as well as non-monetary support. A pre-requisite would also be to identify the right franchisee partner through stringent selection criteria.

• Development of a franchisee management program: This includes creating a dedicated team to assist and engage with partners to monitor franchisee performance and profitability. Typically, this also includes supporting the partner in store launch, training, marketing and system support.

• Aligning franchisee performance and compensation to company goals: This includes creating a clear view on franchisee operational parameters such as lease agreement, credit policy, product returns, SLOB management and termination policy. Defining a transparent terms of trade related to revenue, capital and operating expenses is critical for success.

• Designing robust systems and processes: Processes need to be defined for recruitment and selection of partner to closure so that standardization is ensured across clinics for various services. This includes processes related to recruitment and selection, onboarding, goal setting and performance monitoring and lastly consolidation and closure.

• Ensuring manpower quality: Hiring of manpower by franchisee partners need to be monitored as the service delivery is affected by the quality of hiring. Practitioner selection and training is a critical success factor for ensuring seamless and standardized operations across partners.

Linear

Wha

t sh

ould

the

fran

chis

ee b

usin

ess

mod

el b

e?

How do we ensure that we select the best franchisees to join the venture?

What should the terms of trade be?

What are the risks we face in the franchising business and how do we mitigate them?

What operational changes will we have to make for the business?

How do we ensure the consumer gets the same experience at the company as well as franchisee store?

How should financial and operational responsibilities be split between the company and the franchisee?

16 | The retailer

Alternate therapy services through a franchisee model thereby present significant opportunities for a company intending to scale up efficiently and rapidly. Companies that adopt some of the right strategies can expect to benefit significantly from the untapped potential of the segment over the next five years.Co

nclu

sion

Inputs from Gaurav Goyal

17The retailer |

Ravi is a Director with the Performance Improvement practice of EY India. He has over 15 years of work experience, out of which he has spent 8 years in the consumer products & and financial services sectors with organizations such as Colgate Palmolive, PepsiCo and ICICI Bank.

He has advised several local & and MNC consumer companies in the Indian market and has assisted in, developing their growth strategy strategies and transforming their supply chain, and sales and distribution functions.

Email: [email protected] Tel: +91 22 6192 1595

Ravi Kapoor Director

Krishnaprasad is a Senior Manager in Advisory practice and is based out of Mumbai. He holds an MBA degree from SP Jain Institute of Management & Research, Mumbai and has about 9 years of work experience. He has been with EY for 2 years, prior to which he spent about 7 years in Sales Operations and Distribution Management in the FMCG sector & alternate therapies. Krishnaprasad has led several engagements on value chain assessment and designing of go to market strategy in the Indian market.

Email: [email protected] Tel: +9122 6192 3165

Krishnaprasad M Senior Manager

Inputs from Gaurav Goyal, Senior Consultant

18 | The retailer

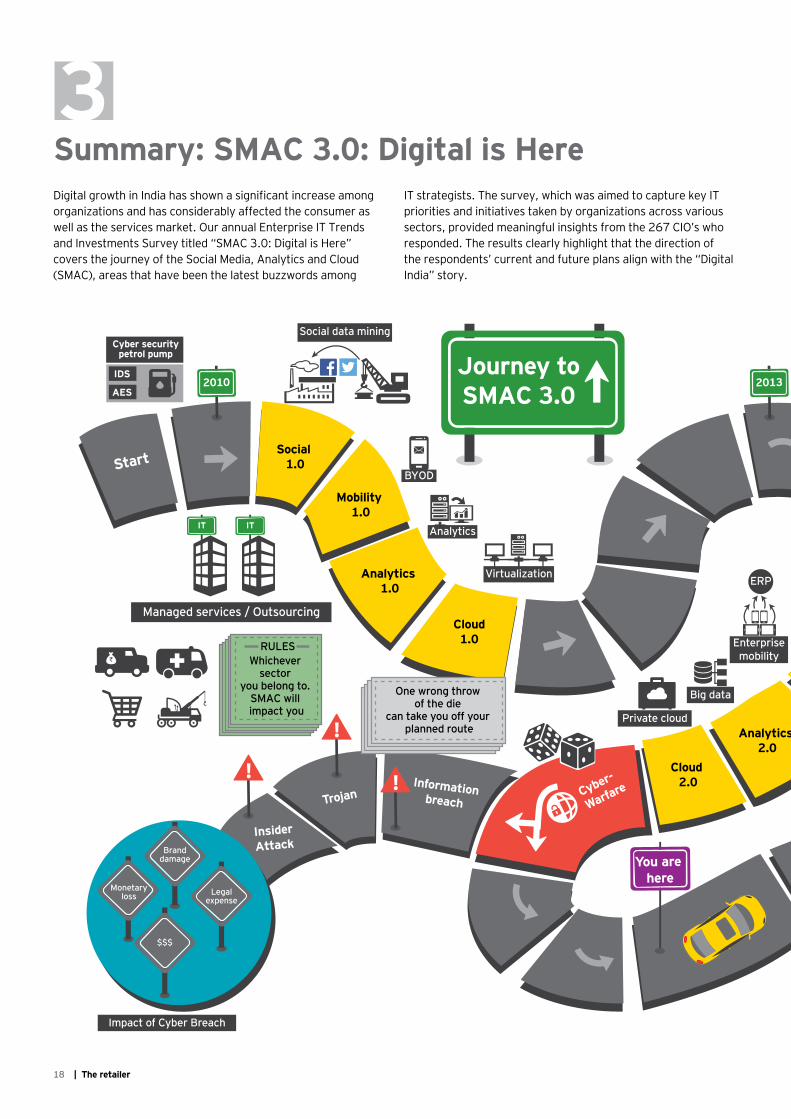

Summary: SMAC 3.0: Digital is Here3

Digital growth in India has shown a significant increase among organizations and has considerably affected the consumer as well as the services market. Our annual Enterprise IT Trends and Investments Survey titled “SMAC 3.0: Digital is Here” covers the journey of the Social Media, Analytics and Cloud (SMAC), areas that have been the latest buzzwords among

IT strategists. The survey, which was aimed to capture key IT priorities and initiatives taken by organizations across various sectors, provided meaningful insights from the 267 CIO’s who responded. The results clearly highlight that the direction of the respondents’ current and future plans align with the “Digital India” story.

StartSocial

1.0

Mobility 1.0

Analytics 1.0

Cloud1.0

Social 2.0

Mobility 2.0

Analytics 2.0

Cloud 2.0Information

breachTrojan

InsiderAttack

Cyber-

Warfare

Social 3.0

Mobility 3.0 Analytics

3.0

Cloud 3.0

Futureof IT

Cyber securitypetrol pump

IDS

AES

Social data mining

Hootsuite

Virtualization

Monetaryloss

Branddamage

$$$

Legalexpense

Journey toSMAC 3.0

BYOD

Analytics

Enterprisemobility

ERP

Private cloud

Impact of Cyber Breach

Big data

Unified enterpriseplatform

Social mediaCRMS

SMCWeb

serviceCustomeranalytics Hybrid

Wireless HUBVirtual reality

3D Printing

PrivatePublic

Managed services / Outsourcing

Managed services / Outsourcing

2010 Cyber securitypetrol pump

DLP

APT

2013

You are here

ITIT

IT IT IT IT IT IT

Managed services / Outsourcing

IT IT IT IT

Future

One wrong throw of the die

can take you off your planned route

Periodically refill your cyber defense solutionsto be ever

ready for a cyber attack

Universal Remote

Internet of

Things

WILD CARD

With the evolution

of IT, your outsourcing

partner holds a vital key

to your future sucess

Whichever sector

you belong to. SMAC will impact you

RULES

19The retailer |

StartSocial

1.0

Mobility 1.0

Analytics 1.0

Cloud1.0

Social 2.0

Mobility 2.0

Analytics 2.0

Cloud 2.0Information

breachTrojan

InsiderAttack

Cyber-

Warfare

Social 3.0

Mobility 3.0 Analytics

3.0

Cloud 3.0

Futureof IT

Cyber securitypetrol pump

IDS

AES

Social data mining

Hootsuite

Virtualization

Monetaryloss

Branddamage

$$$

Legalexpense

Journey toSMAC 3.0

BYOD

Analytics

Enterprisemobility

ERP

Private cloud

Impact of Cyber Breach

Big data

Unified enterpriseplatform

Social mediaCRMS

SMCWeb

serviceCustomeranalytics Hybrid

Wireless HUBVirtual reality

3D Printing

PrivatePublic

Managed services / Outsourcing

Managed services / Outsourcing

2010 Cyber securitypetrol pump

DLP

APT

2013

You are here

ITIT

IT IT IT IT IT IT

Managed services / Outsourcing

IT IT IT IT

Future

One wrong throw of the die

can take you off your planned route

Periodically refill your cyber defense solutionsto be ever

ready for a cyber attack

Universal Remote

Internet of

Things

WILD CARD

With the evolution

of IT, your outsourcing

partner holds a vital key

to your future sucess

Whichever sector

you belong to. SMAC will impact you

RULES

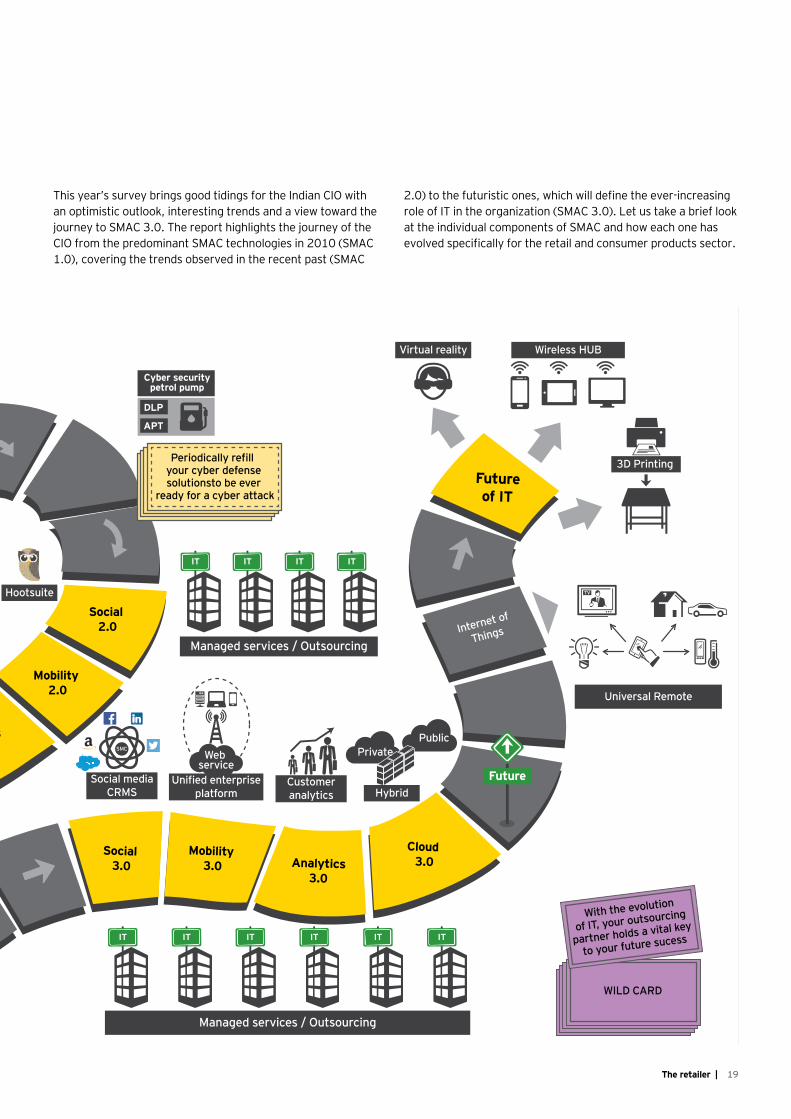

This year’s survey brings good tidings for the Indian CIO with an optimistic outlook, interesting trends and a view toward the journey to SMAC 3.0. The report highlights the journey of the CIO from the predominant SMAC technologies in 2010 (SMAC 1.0), covering the trends observed in the recent past (SMAC

2.0) to the futuristic ones, which will define the ever-increasing role of IT in the organization (SMAC 3.0). Let us take a brief look at the individual components of SMAC and how each one has evolved specifically for the retail and consumer products sector.

20 | The retailer

Social Media describes a shift in how people discover, read and share news, information and content.

It fosters the human connection by transforming a monolog (one-to-many) into a dialog (many to-many). Social media tools make it easier to create and distribute content, and discuss the things we care about. The use of social media is growing at breakneck speed. According to Mediavision, as of 2014, there are 1.32 billion active Facebook users and more than 1 billion YouTube users. The spontaneity and pervasive influence of social media have transformed the relationship between companies and their customers, employees, suppliers and regulators.

This is highlighted by our survey results, which indicate that 74% of the respondents from the Retail and Consumer Products sector agree that social media has been really effective in engaging with customers and enhancing collaboration.

Social Media – Shopping while Surfing, The next Big Bazaar?

74% of the respondents agree that social media has been really effective in engaging with customers and enhancing collaboration

# # # #It is estimated by Gartner that 1 billion smartphones will be added by 2014 and will grow 2.9x between 2011 and 2016. Mobile devices will reach 2,027m in number and by 2015, mobile app development projects will outnumber native PC projects by a ratio of 4:1.

Our survey results indicate a similar progression where 60% of the Retail and Consumer products CIO’s plan to spend on “new technologies” as compared to “business as usual” with mobility being one of them. This is further evidenced by our survey results, which indicate that 89.5% respondents mentioned that they have budgeted for mobility in the current financial year. This is a fairly large number of respondents keen on the advancement of mobility in their organizations.

Emerging technologies, such as mobile payments, peer-to-peer payments, and mobile apps, are creating a mobile ecosystem. The last decade has seen a significant increase in the usage of mobile devices, which led the top management of customer-centric companies to introduce the idea of using individual mobile devices to manage the work efficiently, bringing in the concept of bring your own device (BYOD). This was soon

Mobility: If you don’t shift, are you going to be rendered immobile?

89.5% respondents mentioned that they have budgeted for mobility in the current financial year.

followed by Enterprise mobility, which allowed workers to perform their business tasks using their mobile devices from anywhere outside the workplace. The next big step is the collaboration of organizations with cloud service technologies to enable users to work on their mobile devices, irrespective of the type of device, the platform on which the device runs, and the type of connectivity available.

Furthermore, 16% of the respondents feel that they will accrue benefits in the coming years.

Social media has evolved a long way from its original concept of connecting people all over the world. It has transformed the way we communicate with strangers and friends alike and has become a new platform where brands are marketing their products to reach out to their consumers.

This sphere of social media/Customer Relationship Management (CRM) technology is fast evolving and is likely to change the way companies deal with their customers. Futuristic CRMs will be able to produce trends for all those connected to you via advanced preference analytics algorithms. These devices will be able to clearly demarcate the difference between “data of interest” and “redundant data”. They will also increase the coverage of individuals for whom advertising products can be garnished based on the customer’s preferences.

21The retailer |

Cloud computing started off as a public cloud where cloud infrastructure is made available to the general public or a large industry group and is owned by an organization selling cloud services. Private cloud soon arrived where cloud infrastructure is operated solely for an organization. The next step in cloud computing is a hybrid cloud. A hybrid cloud is a composition of two or more clouds (private or public) that remain unique entities but are bound together by standardized or proprietary technology that enables data and application portability (e.g., cloud bursting for load balancing between clouds).

Cloud – The Highway or the “Cloud Way”The survey results show an interesting trend indicating that investment in cloud computing is delivering a range of benefits, including a shift from capital-intensive to operational cost models, reduced overall cost, increased agility, reduced complexity and increased security.

Of the respondents from the Retail and Consumer Products sector, 63% agreed that they are reaping the benefits of investments made in cloud-based technologies. Furthermore, 57% of the respondents plan to spend anywhere between 1% and 25% on new technologies, including cloud and another 41% plan to spend more than 25% on new technologies.

63.2% respondents agreed that cloud-based technologies have given them significant benefits

Analytics has evolved from providing statistical outputs for creating trends to predictive analytics, which filters out information from substantial existing datasets to identify patterns and predict future outcomes. The next level of analytics awaited is prescriptive analytics, which will help gain an insight into the lives of customers, understand their lifestyles, interests and behaviors, and provide them appropriate products or services that they need.

According to EY’s “The DNA of the CIO survey”, 60% of CIOs think they add strong value to their businesses by enabling analytics to make fact-based decisions. Evolving companies with an equal focus on sales as well as margins have categorized data analytics as “somewhat important.” This shows that some CIOs are still slightly skeptical about unstructured data, which is driving the back end of operational excellence. The survey confirms this — with 53% of CIOs from the Retail and Consumer products industry considering analytics to be very important and 32% of CIOs believe that analytics is somewhat important for their organization.

Analytics: stretching your customer reach using analytics

52.63% respondents categorized analytics as very important

22 | The retailer

Advanced technologies (cloud, big data, mobile, social media, etc.,) offer new capabilities and benefits, but they also introduce new risks. Different technologies are being introduced every day, often outpacing the ability to properly assess associated risks. We have seen that cybersecurity is a global concern. According to EY’s Global Information Security Survey (GISS), .37% of respondents say that real-time insight on cyber risk is not available. With organizations increasingly relying on digitized information and sharing considerable amounts of data across the globe, they have become easy targets for different forms of attack

Cybersecurity: act before you get hackedNew business models rely heavily on global digitization, making the attack much broad based, and exposing gaps in security, especially through the use of cloud, big data, mobile and social media. For example, cloud-based services and third-party data storage and management open up new channels of risk that did not exist previously.

The survey results reveal that 74% of the respondents from the Retail and Consumer Products feel that as a cybersecurity solution, a mix of preventive and detective solution is required.

Managed Services: do “IT” for me

We are in an era of targeted cyberattacks on various organizations. The threat landscape consists of highly capable, determined adversaries who target organizations to steal information, steal money and compromise critical business services.

Traditional security can no longer be solely relied upon to thwart the efforts of a highly capable and determined adversary. Early detection and smart response require network and end-point visibility, monitoring rules to identify attack indicators,

73.7% of survey respondents mentioned they will invest in both preventive and detective technologies

respondents have opted for managed or outsourcing services model

73.7%

enhanced business context, and the ability to apply resources appropriately. Here, the concept of managed services with highly mature, 24*7*365 monitoring and incident response capabilities comes into picture.

The survey results reveal that 56% of the CIO’s from the Retail and Consumer products will opt for a managed/outsourcing services model, which is at least 10% more than the average 43% of the respondents from all sectors who will opt for a managed/outsourcing services model.

23The retailer |

Inputs from Harshil Shah (Consultant), Bhagyesh Vora (Associate Consultant), Sunit Vyas (Associate Consultant)

Sneha is a Senior Manager with the IT Risk and Assurance (ITRA) service line within the Advisory Practice of Ernst and Young LLP. She has diversified experience across industries such as industrial products, chemicals, life sciences, automotive, financial services, FMCG, consumer product and technology.

She has more than eight years of experience in the IT industry, which includes a hybrid experience in Information Risk Consulting, security audits, designing and implementing security and network solutions and internal audits. As part of EY, she has lead multiple engagements that include ISO27001 framework development, data migration review, internal audits, IT roadmap development, PCI-DSS reviews, IT due diligence, Software Development Life Cycle review, ISAE3402/ SSAE16 engagements, Business continuity management review, Sarbanes Oxley readiness assistance etc.

Email: [email protected] Tel: +91 22 6192 1905

Sneha Gandhi Senior Manager

Nitin Mehta is a Director with EY Advisory and focuses on IT Risk and Assurance. He joined EY in 2005 in Philadelphia, US, and relocated to Mumbai, India, in June 2007. He has more than 17 years’ experience in business process and IT risk advisory in India, the US and the Middle East. Nitin is an engineering graduate and has a Master’s degree in management studies. In addition, he is a certified Information Systems Auditor (CISA) and a Certified Information Privacy Professional (CIPP).

Nitin primarily focuses on IT risk and assurance services in the consumer products and life sciences sectors. He has extensive experience in understanding complex information systems, assessing business and IT risks, and formulating control and governance frameworks. His areas of competence include information security, business continuity, application risks and controls, and IT governance.

Email: [email protected] Tel: +91 22 6192 1298

Nitin Mehta Director

24 | The retailer

Innovation board

Amazon India has been looking at new ways to bring kirana stores online. Now, the company has launched a new platform called Kirana Now. The new platform will let kirana stores upload their catalogs online. The deliveries are expected to take an hour or two, and will be taken care of by Amazon, the kirana owners and other third-party logistical companies roped in for this initiative. This initiative is expected to cater to the customer need of speedy delivery of grocery products.

http://www.tehelka.com/amazon-tie-ups-with-kirana-stores/, Link accessed on: 29May 2015

Cadbury invested £7.5 million in a campaign to launch its new Cadbury Dairy Milk Ritz and Lu products. As part of the “Moment of Joy” drive of the confectionary department of Cadbury, a seven-week campaign was launched focusing on driving the awareness and understanding of new snacking products. Majority spends and activity was focused during the afternoon time, i.e., “tea break moment” with a television advertisement and its digital version on YouTube and its Facebook page. The two product launches have proved to be of significant success, with a hit value of £500 million at the end of last year, and reported a great response to its real-time marketing. The company plans to continue its investment in real time marketing in television, digital and social media space.

http://www.thedrum.com/news/2014/02/27/cadbury-invests-75-million-ad-campaign-biggest-innovation-2014 Link accessed on: 15 May 2015`

“Connect + Develop” the new initiative of P&G, collaborates with individuals and companies around the world to develop innovative ideas and products. Open innovation at P&G works both ways (inbound and outbound), it includes considerably more than technology, i.e., from trademarks to packaging, marketing models to engineering, and business services to design. There is a global business development team dedicated to empowering this initiative, searching for innovations, working with prospective partners and directing innovations through the company and into the market. Recently it partnered with MonoSol of Indiana to revolutionize the laundry category by launching Tide Pods. This partnership was done with the objective of better product offering for customers, now the cleaning solution dissolves completely with no residue in a range of water temperatures, from hot to cold.

http://www.pgconnectdevelop.com/home/pg_open_innovation.html Link assessed on: 15 May 2015

Amazon tie-ups with kiranas

Cadbury invests in real-time multi-channel advertising

P&G’s open innovation strategy1

3

2

4

“Automobile, logistics companies to reap rich GST dividend,” http://www.business-standard.com/article/economy-policy/automobile-logistics-companies-to-reap-rich-gst-dividend-114121800921_1.html, accessed on 11 May 2015

“An Empirical Note on the Comparative Macroeconomic Effects of the GST in Australia, Canada and New Zealand, by Tom Bolton and Brian Dollery,” http://www.une.edu.au/__data/assets/pdf_file/0006/67947/econ-2004-17.pdf, accessed on 11 May 2015

Other references

“Reaping the GST opportunities,” http://www.sclc.in/pdf/india-after-gst-presentation/Godrej-Consumer-Products.pdf, accessed on 11 May 2015

“India’s Goods and Services Tax – A Primer,” http://www.stcipd.com/UserFiles/File/Indias%20Goods%20and%20Services%20Tax%20%20A%20Primer.pdf, accessed on 11 May 2015

“Towards the GST, An Approach Paper, April 2013,” http://www.ficci.com/spdocument/20238/Towards-the-GST-Approach-Paper-Apri-2013.pdf, accessed on 11 May 2015

“Officials race against time to roll out Goods and Service Tax Network,” http://articles.economictimes.indiatimes.com/2015-03-13/news/60086016_1_gstn-services-tax-network-tax-regime, accessed on 11 May 2015

“The brand value of GST,” http://www.livemint.com/Opinion/X0vBTWlmE8rbeKJcizQWrI/The-brand-value-of-GST.html, accessed on 11 May 2015

25The retailer |

Notes

26 | The retailer

Notes

27The retailer |

Our officesAhmedabad2nd floor, Shivalik Ishaan Near C.N. VidhyalayaAmbawadiAhmedabad - 380 015Tel: + 91 79 6608 3800Fax: + 91 79 6608 3900

Bengaluru12th & 13th floor“UB City”, Canberra BlockNo.24 Vittal Mallya RoadBengaluru - 560 001Tel: + 91 80 4027 5000 + 91 80 6727 5000 Fax: + 91 80 2210 6000 (12th floor)Fax: + 91 80 2224 0695 (13th floor)

1st Floor, Prestige Emerald No. 4, Madras Bank RoadLavelle Road JunctionBengaluru - 560 001Tel: + 91 80 6727 5000 Fax: + 91 80 2222 4112

Chandigarh1st Floor, SCO: 166-167Sector 9-C, Madhya MargChandigarh - 160 009 Tel: + 91 172 671 7800Fax: + 91 172 671 7888

ChennaiTidel Park, 6th & 7th Floor A Block (Module 601,701-702)No.4, Rajiv Gandhi Salai, Taramani Chennai - 600113Tel: + 91 44 6654 8100 Fax: + 91 44 2254 0120

HyderabadOval Office, 18, iLabs CentreHitech City, MadhapurHyderabad - 500081Tel: + 91 40 6736 2000Fax: + 91 40 6736 2200

Kochi9th Floor, ABAD NucleusNH-49, Maradu POKochi - 682304Tel: + 91 484 304 4000 Fax: + 91 484 270 5393

Kolkata22 Camac Street3rd floor, Block ‘C’Kolkata - 700 016Tel: + 91 33 6615 3400Fax: + 91 33 2281 7750

Mumbai14th Floor, The Ruby29 Senapati Bapat MargDadar (W), Mumbai - 400028Tel: + 91 022 6192 0000Fax: + 91 022 6192 1000

5th Floor, Block B-2Nirlon Knowledge ParkOff. Western Express HighwayGoregaon (E)Mumbai - 400 063Tel: + 91 22 6192 0000Fax: + 91 22 6192 3000

NCRGolf View Corporate Tower BNear DLF Golf CourseSector 42Gurgaon - 122002Tel: + 91 124 464 4000Fax: + 91 124 464 4050

6th floor, HT House18-20 Kasturba Gandhi Marg New Delhi - 110 001Tel: + 91 11 4363 3000 Fax: + 91 11 4363 3200

4th & 5th Floor, Plot No 2B, Tower 2, Sector 126, NOIDA 201 304 Gautam Budh Nagar, U.P. IndiaTel: + 91 120 671 7000 Fax: + 91 120 671 7171

PuneC-401, 4th floor Panchshil Tech ParkYerwada (Near Don Bosco School)Pune - 411 006Tel: + 91 20 6603 6000Fax: + 91 20 6601 5900

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in.

Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016

© 2015 Ernst & Young LLP. Published in India. All Rights Reserved.

EYIN1506-065 ED None

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

JS

Ernst & Young LLPEY | Assurance | Tax | Transactions | Advisory

EY refers to the global organization, and/or one or more of the independent member firms of Ernst & Young Global Limited