the retirement minefield an overview of the most common ira mistakes – and how to avoid them....

TRANSCRIPT

The Retirement MinefieldAn overview of the most common IRA mistakes

– and how to avoid them.

AMTRMPP0113

Brought to you by Transamerica’s Advanced Markets team

Variable Annuities issued by Transamerica Life Insurance Company in Cedar Rapids, Iowa, and Transamerica Financial Life Insurance Company in Harrison, New York (Transamerica). Annuities are underwritten and distributed by Transamerica Capital, Inc. Transamerica Financial Life Insurance Company is licensed in New York.

2

Disclosure slideBefore investing, consider a variable annuity’s investment objectives, risks, charges and expenses. Call 1-800-525-6205 for a contract and fund prospectus containing this and other information. Please read it carefully. Securities may lose value and are not insured by the FDIC or any federal government agency. May lose value. Not a deposit or guaranteed by any bank, bank affiliate or credit union.

3

Retirement Planning

How things have changed!

• Between 1982 and 2009, the number of defined benefit (DB) plans decreased 73% (from 174,998 plans to 47,137)1

• By 2009, 93% of employer sponsored retirement plans were defined contribution (DC) plans1

• 46% of plan participants expect their DC plan to be their most important source of retirement income2

• Social Security is projected to pay full benefits until 20333

When it comes to retirement – It’s up to you!

¹ Employee Benefits Security Administration “Private Pension Plan Bulletin Historical Tables and Graphs”2 Blackrock “Shifting Focus: From Retirement Savings to Retirement Income”3 Social Security Administration. “Social Security Board of Trustees: Projected Trust Fund Exhaustion Three Years Sooner Than Last Year.”

4

Retirement Planning

Managing Risks – things we can’t control

• Inflation – erodes the value of savings and purchasing power• Market volatility – unpredictable returns• Longevity – outliving your assets• Catastrophic events – a significant impact to your income or savings• Legislative changes – Social Security, Medicare, taxes

Avoiding Mistakes – things we can control

• Emotional errors – making investment decisions based on emotion• Failure to plan properly – relying on “rules of thumb” • IRS taxes and penalties – unnecessarily erodes the value of retirement savings

5

IRA Planning

Avoiding IRA Mistakes – things we can control

• Failure to plan properly – overlooking personal circumstances• IRS taxes and penalties – unnecessarily erodes the value of retirement savings

Neither Transamerica nor any of its financial professionals provide tax or legal advice. You should consult a qualified tax advisor for questions regarding your particular situation.

6

Broken Window: Rollover Horror Stories- By making trustee-to-trustee transfers, one can avoid triggering the 60-day requirement

- Ed Slott, July 17,2011

Survivors’ Biggest Mistakes- Widows and Widowers often lose money needlessly; the IRA Rollover penalty

- Kelly Greene, Wall Street Journal, November 12, 2011

Distribution Nightmare- Make this mistake with an IRA and there’s no second chance.

- Gregory Bresiger, Financial Advisor magazine, March 2007

The Retirement Minefield – IRAs

IRA Rules Get Trickier- Uncle Sam is cracking down on common retirement account errors

- Kelly Greene, Wall Street Journal, June 23, 2012

7

The IRA “Rule Book”• More than 100 pages • Updated annually

Transfers

Age 70 ½ Rule

Partial Rollovers

Penalties

Inherited IRAs

Conversions

Spousal IRA

Age 59 ½ Rule

Required Beginning Date

Early Distributions

Form 8606

Form 5329

Form 1040

60-Day Period for Rollovers

20% Withholding

10% Additional Tax

2-Year Rule

Beneficiaries

The Retirement Minefield – IRAs

8

The Retirement Minefield – IRAs

• IRA Rollovers

• Pros, cons and what’s right for you

• Withdrawing Income

• Understanding the taxes, penalties, and deadlines

• Beneficiary Planning

• Important considerations for you and your beneficiaries

We’ll address common mistakes that people make in each of these areas

9

What is a Rollover?

A “Rollover” is the transfer of retirement assets from one retirement plan to another retirement plan

• To transfer money from an employer sponsored retirement plan(e.g. 401(k) plan) to an IRA, you must be eligible to withdraw assets from the employer sponsored plan1

- Triggering events• You can rollover or transfer assets in your own IRA to another IRA at any

time without requiring a triggering event*

IRA Rollovers

1401(k)(2)(B); 403(b)(11)

Rollovers and transfers may be subject to differences in features and expenses. Indirect transfers may be subject to taxation and penalties. Consult your tax advisor regarding your situation.

*Only one IRA rollover per 12 months is permitted.

10

When can you elect a rollover to an IRA?

Triggering events for employer sponsored plans1:• Separation of Service

- You no longer work for the employer- You may not have to wait! 72% of employer sponsored plans allow you to roll over your 401(k) assets while you’re still employed2

- Request your employer’s Summary Plan Description for additional information

• Attainment of Age 59 ½- May be required for “in-service” rollovers

• Disability - You must qualify as disabled

• Death-This applies to your beneficiary(s)

You can rollover or transfer assets in your own IRA to another IRA at any time without requiring a triggering event*

1 Treas. Regs. 1.401-1(b), 1.401(a)-14, 1.403(b)-62 Plan Sponsor Council of America, 54th Annual Survey of Profit Sharing and 401(k) plans, 2010 plan year.

IRA Rollovers

*Only one IRA rollover per 12 months is permitted.

11

Why an IRA Rollover Might be Right for YouYou have more than one retirement account

• Consolidation of accounts can be easier than managing multiple accounts

Your plan has limited investment options• You can expand your investment options to include alternative investments or

annuities

Your plan does not offer a retirement income program • IRAs can provide guaranteed lifetime income, bond laddering and bucketing options

Your plan has limited beneficiary planning options• IRAs can offer customized, pre-selected or “stretch” beneficiary options

You may need or want to access your retirement assets prior to 59 ½• IRAs offer additional exceptions to the 10% additional federal tax for health insurance

premiums if unemployed, qualified higher education expenses, and first time home buyers¹

¹IRC Section 72(t)

IRA Rollovers

There is no additional tax-deferral benefit derived from placing IRA or other tax-qualified funds into an annuity. Features other than tax-deferral should be considered in the purchase of a qualified annuity.

Withdrawals of taxable amounts are subject to ordinary income tax and, if taken prior to age 59½ a 10% additional federal tax may apply.

Consolidation does not guarantee a profit or guard against a loss. All guarantees are backed by the claims-paying ability of the issuing insurance company.

12

Common Mistakes People Make Overlooking personal circumstances before rolling money over

to an IRA Electing an Indirect Rollover instead of a Direct Rollover Paying the 10% additional federal tax on pre-59 ½ withdrawals Failure to manage required minimum distributions at age 70 ½ Overlooking death benefit distribution options They don’t seek professional guidance

IRA Rollovers

13

Is an IRA Rollover Right for You, Right Now?Will you need a loan?

• Your employer sponsored retirement plan may have a loan feature1

• Loans are not permitted from IRAs2

Did you separate from service at or after age 55?

• There is an exception to the 10% additional federal tax for distributions from a qualified plan for employees who separate from service during or after the year in which they attain age 553

Do you plan on working past age 70?

• If you continue to work past 70 ½ you may be eligible to defer RMD’s on qualified plan assets attributable to the current employer’s plan4

Were the plan assets awarded via a divorce?

• There is an exception to the 10% additional federal tax for an ex-spouse who received qualified plan assets as an alternate payee under a Qualified Domestic Relations Order (QDRO)5

¹IRC Sec. 72(p)(2)2IRC Sec. 4975(c)(1)(B); 408(e)(2)(A).3 IRC Sec 72(t)(2)(A)(v); 72(t)(3)4 IRC Sec. 401(a)(9)©

IRA Rollovers

5IRC Sec. 72(t)(2)(c)

14

Common Mistakes People Make Overlooking personal circumstances before rolling money over

to an IRA Electing an Indirect Rollover instead of a Direct Rollover Paying the 10% additional federal tax on pre-59 ½ withdrawals Failure to manage required minimum distributions at age 70 ½ Overlooking death benefit distribution options They don’t seek professional guidance

IRA Rollovers

Rollovers and transfers may be subject to differences in features and expenses. Indirect transfers may be subject to taxation and penalties. Consult your tax advisor regardingyour situation.

15

Ensure You do it the Right Way

Rollover (Indirect Rollover)• The distribution is made payable to you in cash• You have 60 days to contribute the proceeds to another retirement plan or IRA

Direct Rollover/Transfer• The distribution is made directly to your new retirement plan or IRA• Employer sponsored retirement plans are required to offer this option¹

¹ IRC Sec. 401(a)(31), 403(b)(10), 457(d)(1)(C)

IRA Rollovers

16

$100,000

$80,000 in cash

$80,000 to IRA

$20,000

401(k) Plan

IRS

YOU

Indirect Rollover

$20,000

60 Day Time Limit²

$20,000

20% Mandatory Withholding¹

$80,000

$80,000 Rolled Over,$20,000 Taxable Distribution

STEP 3 $20,000

Tax Refund

IRA

STEP 1

STEP 2

IRA

-

+¹ IRC Sec. 3405(c)(1)² IRC Sec. 402(c)(3); Treas. Reg.1.402(c)-2, A-11

IRA Rollovers

This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of fees or expenses. The chart is shown for illustrative purposes only.

17

Deadline • 60 day time limit¹

Qualified Plan to IRA• 20% mandatory withholding²

• Amount withheld must be added to avoid taxable distribution and potential 10% additional tax

IRA to IRA• Only one tax-free rollover during one-year period is permitted, applicable to both IRAs.³

Ensure you do it the Right Way – Important differences

Indirect Rollover

¹ IRC Sec. 402 (c)(3)² IRC Sec. 3405(c)(1)³ IRC Sec. 408(d)(3)(B)

Direct Rollover

IRA Rollovers

18

20%$20,000

IRS

YOU

$100,000

IRA

$100,000

Direct,No 60 Day Time Limit

Direct Rollover401(k) Plan

20%$20,000

No Make-Up

No Withholding

No Waiting for Tax Refund

IRA Rollovers

This is a hypothetical illustration and is for illustrative purposes only.

19

Deadline • 60 day time limit¹ • No 60-day time limit

Qualified Plan to IRA• 20% mandatory withholding²

• Amount withheld must be added to avoid taxable distribution and potential 10% additional tax

• No withholding

• Fewer tax concerns

IRA to IRA• Only one tax-free rollover during one-year period is permitted, applicable to both IRAs.³

• No once per year limit

Ensure you do it the Right Way – Important differences

Indirect Rollover

¹ IRC Sec. 402 (c)(3)² IRC Sec. 3405(c)³ IRC Sec. 408(d)(3)(B)

Direct Rollover

IRA Rollovers

20

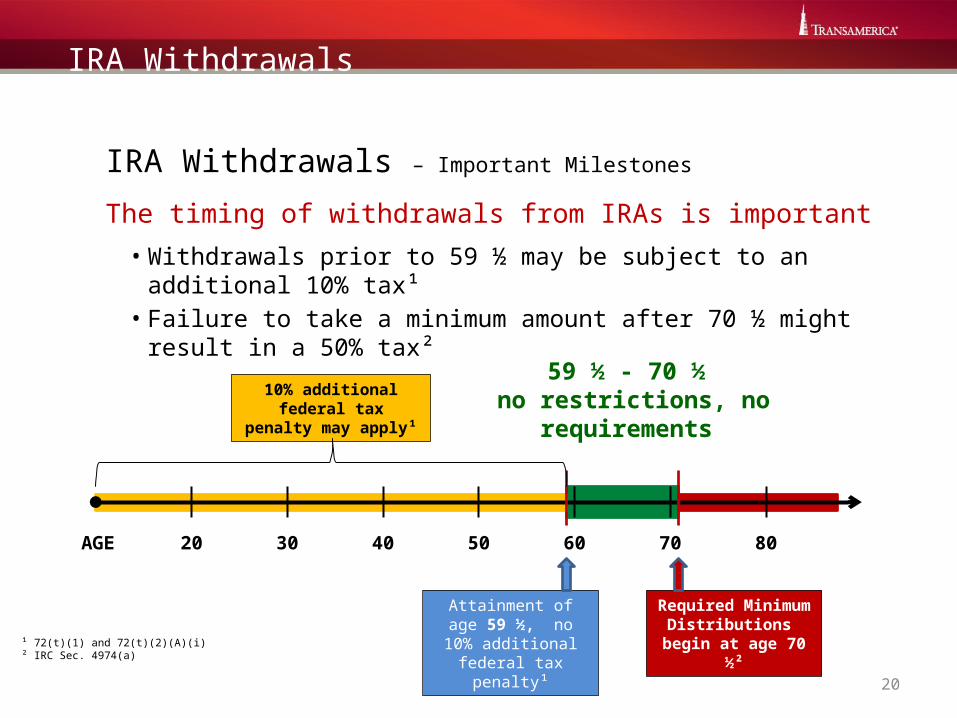

IRA Withdrawals – Important Milestones

The timing of withdrawals from IRAs is important

• Withdrawals prior to 59 ½ may be subject to an additional 10% tax¹• Failure to take a minimum amount after 70 ½ might result in a 50% tax²

20 30 40 50 60 70 80AGE

Attainment of age 59 ½, no 10% additional federal tax penalty¹

10% additional federal tax penalty may apply¹

Required Minimum Distributions

begin at age 70 ½²

59 ½ - 70 ½ no restrictions, no

requirements

¹ 72(t)(1) and 72(t)(2)(A)(i)² IRC Sec. 4974(a)

IRA Withdrawals

21

Common Mistakes People Make Electing an Indirect Rollover instead of a Direct Rollover Overlooking personal circumstances before rolling money over

to an IRA Paying the 10% additional federal tax on pre-59 ½ withdrawals Failure to manage required minimum distributions at age 70 ½ Overlooking death benefit distribution options They don’t seek professional guidance

IRA Withdrawals

22

20 30 40 50 60 70 80AGE

Attainment of age 59 ½ exception to 10%

additional federal tax penalty

IRA exceptions to 10% additional federal tax penalty²- Higher education expenses- First time home buyer- Health insurance premiums if unemployed

Qualified plan exceptions to 10% additional federal tax penalty³- Divorce (QDRO)- Separate from service at or after age 55

General exceptions to 10% additional federal tax penalty for withdrawals prior to 59 ½¹- Death- Disability- Medical expenses > 7.5% of AGI- Substantially equal periodic payments

Withdrawals made prior to 59 ½

¹ IRC Sec. 72(t)(2)(A)(i)² IRC Sections 72(t)(2)(D), (E), and (F)³ IRC Sec. 72(t)(3); 72(t)(2)(A)(v); 72(t)(2)(C)

IRA Withdrawals

23

Pre-59 ½ Withdrawals

The SEPP Exception to the 10% Additional Federal Tax¹

• The one exception that is available to anyone at any age• CAUTION! – The terms can be onerous

• The amount that can be withdrawn is limited and must be determined by using one of three IRS approved calculation methods¹

• Payments must continue for at least 5 years and the employee must have attained 59 1/2 when the payments cease, if later²

• Failure to abide by the rules could result in retroactive taxes, interest and penalties

Seek professional guidance!¹ IRC Sec. 72(t)(2)(A)(iv); Rev. Ruling 2002-62² IRC Sec. 72(t)(4)(A); Rev. Ruling 2002-62

IRA Withdrawals

24

Common Mistakes People Make Electing an Indirect Rollover instead of a Direct Rollover Overlooking personal circumstances before rolling money over to an IRA Paying the 10% additional federal tax on pre-59 ½ withdrawals Failure to manage required minimum distributions at age 70 ½ Overlooking death benefit distribution options They don’t seek professional guidance

IRA Withdrawals

25

1/1/12

70 ½

AGE

DATE 1/1/13 4/1/13 12/31/13

The year you turn 70 ½ is the first “distribution year” for IRA

required minimum distributions (RMD)

4/1 of the year following the first “distribution year” is the

“required beginning date”

An RMD for the next distribution year, and each year

thereafter, must be taken by 12/31 of that year

The RMD for the first “distribution year” can be deferred until 4/1 of the following year

If the first RMD is deferred until the following year (e.g., April

1st), two RMDs must be taken in that tax year

The RMD for the first “distribution year” can be

taken that year

RMD Timeline

8/1/12

Source: IRS Publication 590, 2012

IRA Withdrawals

26

Required Minimum Distributions (RMDs)

Planning Considerations• A 50% tax applies to amounts that should have been withdrawn!1

• Automate your RMD payments- Ensures you won’t miss a payment- The percentage that needs to be withdrawn increases each year

• Plan for your RMD- If you don’t need it, how will you reinvest it?- Buy life insurance with it- Gift it to a loved one or trust- Donate the RMD you receive to a charity - Understand how it fits into your retirement income and estate plan

IRA Withdrawals

1IRC Sec. 4974(a)

27

Common Mistakes People Make Electing an Indirect Rollover instead of a Direct Rollover Overlooking personal circumstances before rolling money over

to an IRA Paying the 10% additional federal tax on pre-59 ½ withdrawals Failure to manage required minimum distributions at age 70 ½ Overlooking death benefit distribution options They don’t seek professional guidance

Beneficiary Planning

28

Beneficiary Planning

IRA Death Benefit Distribution Options

• Lump sum• All out in five years• Annuitization*• Maintain or rollover to own IRA – spouses only• Stretch

* Annuitization may be an option provided on annuity contracts

Source: IRS Publication 590, 2012

Beneficiary Planning

29

$100,000

$20,000$100,000 $20,000 $20,000 $20,000 $20,000

$100,000

Lump Sum

All out in 5 years

$75,000 $25,000

x 25% Tax Bracket*

IRS

$15,000 $5,000

Comparing Death Benefit Options

x 25% Tax Bracket*

IRS

Inherited IRA

Inherited IRA

* 25% tax bracket is hypothetical, your effective tax rate may be different

Beneficiary Planning

This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of any fees or expenses. The chart is shown for illustrative purposes only.

30

There is another way!

Stretch • Allows beneficiary to maintain tax deferral of inherited IRA and control the

taxation of distributions, to the extent permitted by law• To take advantage of this option it must be elected by 12/31 of the year

following the death of the original IRA owner.

Source: IRS Publication 590, 2012

Beneficiary Planning

31

$100,000 ÷ 30.5 =

Non-spouse Beneficiary: AGE 54IRS Table I: Single Life Table

Divisor = 30.5(Year 1)

Stretch Death Benefit Option

$3,279 x 25% Tax Bracket*

$2,459 $820 IRS

Inherited IRA

• Divisor reduced by 1 each year (e.g. 30.5, 29.5, 28.5, etc.)• Can always take a lump sum• Allows beneficiary to maintain tax deferral of inherited IRA and control

the taxation of distributions, to the extent permitted by law

Source: IRS Publication 590, 2012* 25% tax bracket is hypothetical, your effective tax rate may be different

Beneficiary Planning

This is a hypothetical illustration and is for illustrative purposes only.

32

Who are your Beneficiaries?

Spouse Beneficiaries • Can elect to roll an inherited IRA into their own IRA¹• Can elect to treat it as an inherited IRA2

Non-spouse Beneficiaries • Cannot elect to roll inherited IRA assets into their own IRA• Can elect to treat it as an inherited IRA

Seek professional guidance!

Source: IRS Publication 590, 2012¹ Treas. Reg. 1.408-8, A-5.2 Notice 2009-68

Beneficiary Planning

33

Common Mistakes People Make Electing an Indirect Rollover instead of a Direct Rollover Overlooking personal circumstances before rolling money over

to an IRA Paying the 10% additional federal tax on pre-59 ½ withdrawals Failure to manage required minimum distributions at age 70 ½ Overlooking death benefit distribution options They don’t seek professional guidance

34

Working with a Professional

IRA planning – avoiding mistakes

• What are your personal circumstances?• What are your personal needs?• What are your personal concerns?

What I would like you to do:

• Complete the IRA Rollover questionnaire• Obtain a copy of your employer’s summary plan description• Gather your beneficiary information• Schedule an appointment, so we can start planning today

35

Thank You for Attending!

Questions?

The Retirement MinefieldAn overview of the most common IRA mistakes

– and how to avoid them.

AMTRMPP0113

Brought to you by Transamerica’s Advanced Markets team