the role of bank indonesia in development of micro, small...

TRANSCRIPT

By:By:Endang SedyadiEndang Sedyadi

Banking Research and Regulation Directorate Banking Research and Regulation Directorate Bank IndonesiaBank Indonesia

The Role of Bank Indonesia in Development The Role of Bank Indonesia in Development of Micro, Small, and Medium Enterprises of Micro, Small, and Medium Enterprises

(MSMEs) and Customer Due Diligence (MSMEs) and Customer Due Diligence (CDD)(CDD)

Workshop for Enhancing the Effectiveness of Bilateral Remittance Transfers in South East Asia

World BankDenpasar, 9 – 11 June 2008

2

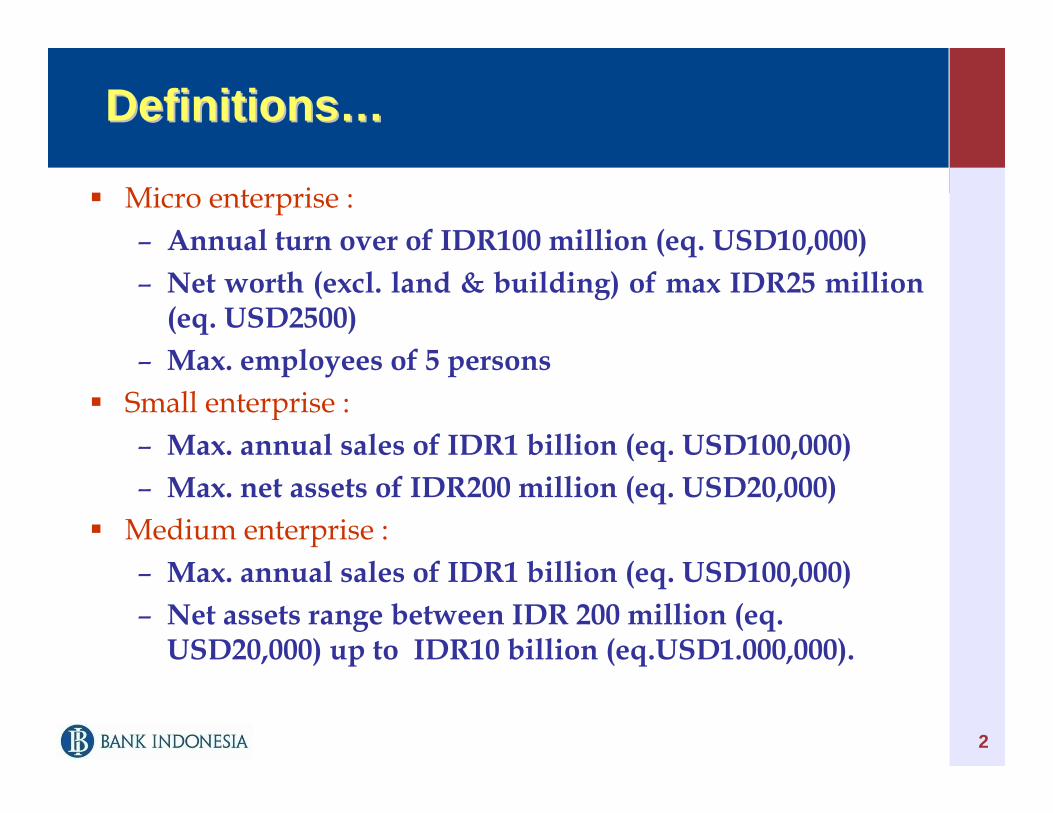

DefinitionsDefinitions……

Micro enterprise :– Annual turn over of IDR100 million (eq. USD10,000) – Net worth (excl. land & building) of max IDR25 million

(eq. USD2500) – Max. employees of 5 persons

Small enterprise :– Max. annual sales of IDR1 billion (eq. USD100,000) – Max. net assets of IDR200 million (eq. USD20,000)

Medium enterprise :– Max. annual sales of IDR1 billion (eq. USD100,000) – Net assets range between IDR 200 million (eq.

USD20,000) up to IDR10 billion (eq.USD1.000,000).

3

Strategic Role of MSMEs in Indonesian Economy, Strategic Role of MSMEs in Indonesian Economy, 20062006

Sources: Ministry of Cooperation & MSMEs and Statistic Bureau, 2006

Non oil export: IDR778,3 billionMSMEs20%

Large Corp80%

Number of Entity: 48.9 million unit Large Corp

1%

MSMEs99%

GDP: IDR3,338.2 billion

MSMEs53%

Large Corp

47%

Investment: IDR800.1 billion

Large Corp

54%

MSMEs46%

Employment: 88.8 million person

MSMEs96%

Large Corp4%

4

Contribution to GDP by Sector Economy, 2006Contribution to GDP by Sector Economy, 2006

Sources: Ministry of Cooperation & MSMEs and Statistic Bureau, 2006

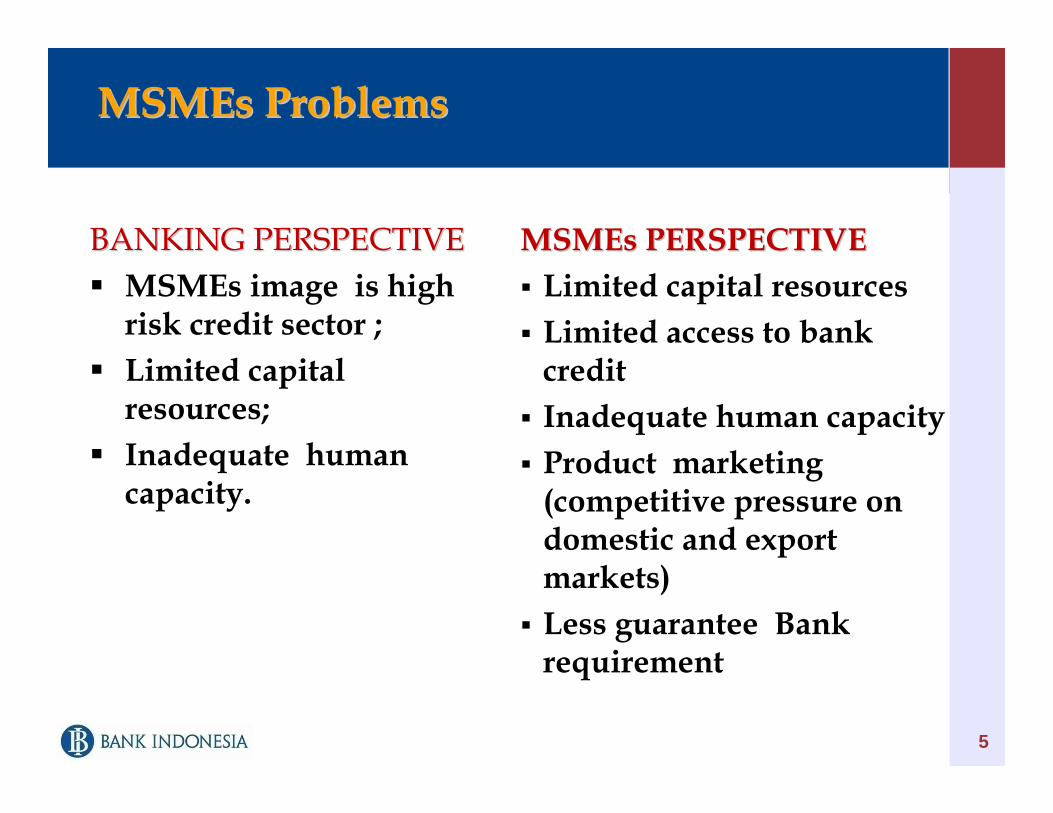

BANKING PERSPECTIVEBANKING PERSPECTIVEMSMEs image is high risk credit sector ;Limited capital resources;Inadequate human capacity.

5

MSMEs ProblemsMSMEs Problems

MSMEs PERSPECTIVEMSMEs PERSPECTIVELimited capital resourcesLimited access to bank creditInadequate human capacityProduct marketing (competitive pressure on domestic and export markets) Less guarantee Bank requirement

6

Central Bank Act No. 13/ Central Bank Act No. 13/ 19681968Providing liquidity credits (financial assistance) to SMEs through the banks;Technical Assistance.

1999

To Create Sound and Sustainable Banking System, To Create Sound and Sustainable Banking System,

BIBI’’s Financing MSMEs s Financing MSMEs

Central Bank Act No. 23/1999; Central Bank Act No. 23/1999; Technical Assistance;Provision of Information;Bank Persuasive PolicyCentral Bank Act No 23/1999 amended Central Bank Act No 23/1999 amended by Act No 3/2004by Act No 3/2004

Since 1999-2008• Technical Assistance; • Institutional Support; • Bank Credit Policy; and • Cooperation with the Government and

Other Relevant Agencies.Since 2004 -2008

The Indonesian Banking Architecture The Indonesian Banking Architecture (API) Program(API) Program

7

•• Technical AssistanceTechnical Assistance (PBI No. 7/39/PBI/2005 concerning Technical Assistance for the development of MSMEs).–– Training for Banks, MSMEs Financial Institutions, and Business Training for Banks, MSMEs Financial Institutions, and Business

Development Services Provider (BDSP) as well as Bank Partner Development Services Provider (BDSP) as well as Bank Partner Financial Consultant (KKMBFinancial Consultant (KKMB) ; Training topic cover: MSMEs Development Strategy, Survey of Micro and Small Enterprises using Rapid Rural Appraisal Method, MSMEs Credit Analysis, MSMEs Non Performing Credit Handling and Credit by Group with Pola Hubungan Bank and Non Governmental Organization (PHBK)

–– Research ActivitiesResearch Activities fostering the decisions on direction and policy of BI in facilitating technical assistance and providing information.

–– Facilitation for Banking Intermediation BazaarFacilitation for Banking Intermediation Bazaar provide:Information and communication forum between Banks and business community and the public. The intermediation bazaar took place alternately in several BI Regional Offices (KBI).

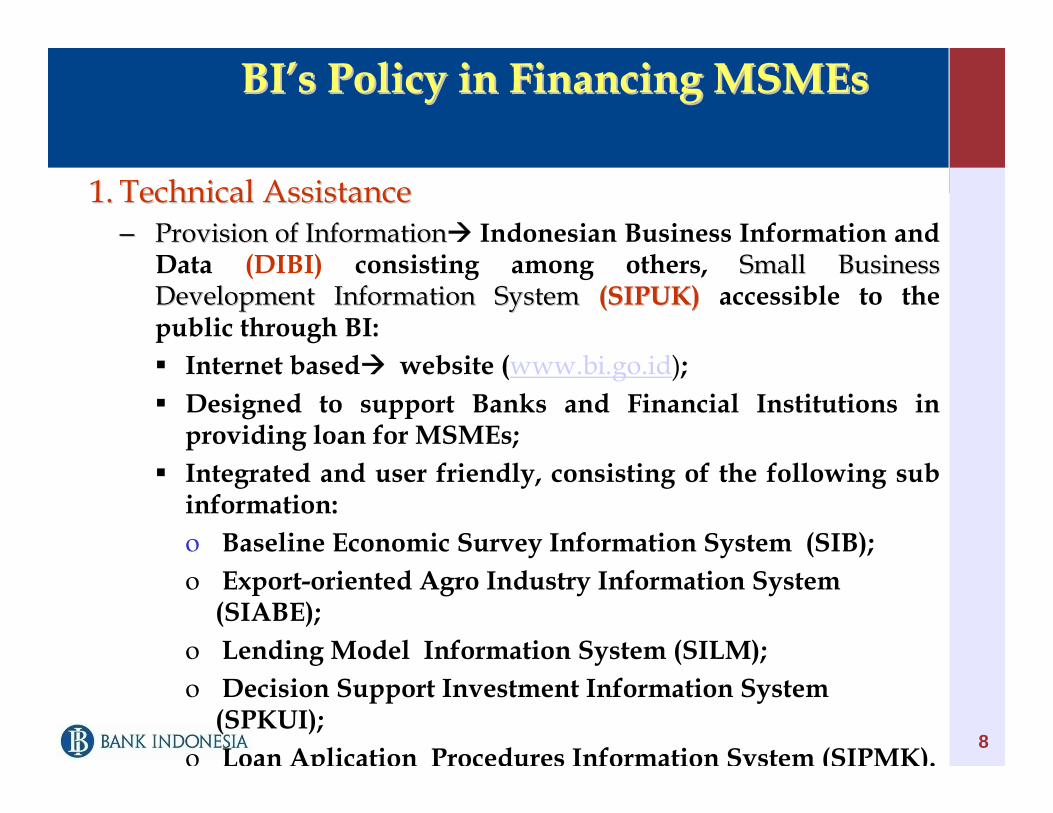

BIBI’’s Policy in Financing MSMEs s Policy in Financing MSMEs

8

1.1. Technical AssistanceTechnical Assistance–– Provision of InformationProvision of Information Indonesian Business Information and

Data (DIBI) consisting among others, Small Business Small Business Development Information System Development Information System (SIPUK)(SIPUK) accessible to the public through BI:

Internet based website (www.bi.go.id);Designed to support Banks and Financial Institutions in providing loan for MSMEs;Integrated and user friendly, consisting of the following sub information:o Baseline Economic Survey Information System (SIB);o Export-oriented Agro Industry Information System

(SIABE);o Lending Model Information System (SILM);o Decision Support Investment Information System

(SPKUI);o Loan Aplication Procedures Information System (SIPMK).

BIBI’’s Policy in Financing MSMEs s Policy in Financing MSMEs

9

BIBI’’s Policy in Financing MSMEs s Policy in Financing MSMEs

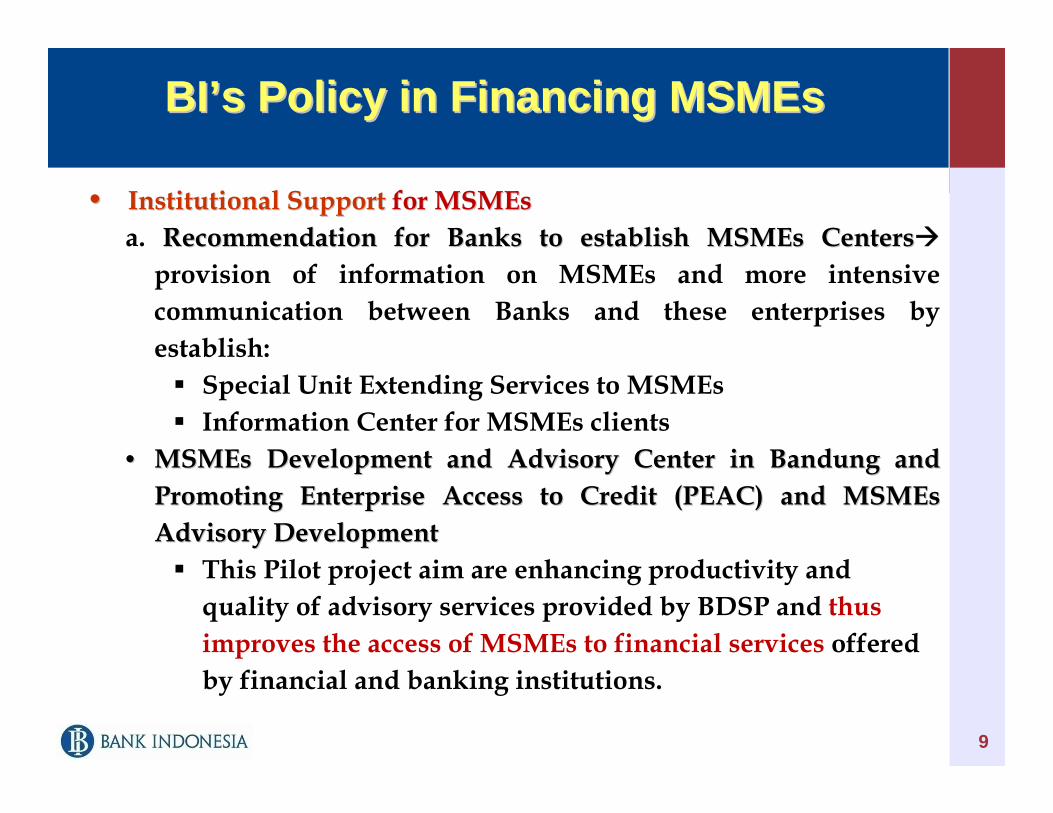

•• Institutional Support Institutional Support for MSMEsfor MSMEsa. Recommendation for Banks to establish MSMEs CentersRecommendation for Banks to establish MSMEs Centers

provision of information on MSMEs and more intensive communication between Banks and these enterprises by establish:

Special Unit Extending Services to MSMEsInformation Center for MSMEs clients

•• MSMEs Development and Advisory Center in Bandung and MSMEs Development and Advisory Center in Bandung and Promoting Enterprise Access to Credit (PEAC) and MSMEs Promoting Enterprise Access to Credit (PEAC) and MSMEs Advisory Development Advisory Development

This Pilot project aim are enhancing productivity and quality of advisory services provided by BDSP and thus improves the access of MSMEs to financial services offered by financial and banking institutions.

10

•• Bank Credit Policy Bank Credit Policy Regulation on MSMEs CreditRegulation on MSMEs Credit– Recommend Banks Recommend Banks to allocate part of its lending to MSMEs lending to MSMEs

and Banks should publish the quarterly report on realization of business planbusiness plan.

BIBI’’s Policy in Financing MSMEs s Policy in Financing MSMEs

Source: Bank Indonesia, December 2007

174.6%

143.5%

85.2%

111.8%

0.0

20.0

40.0

60.0

80.0

100.0

Rp billion

0.0%

40.0%

80.0%

120.0%

160.0%

200.0%

Prosentase

Business Plan (Rpbillion)

38.5 60.4 68.1 86.0

Realization (Rpbillion)

67.2 86.7 58.0 96.2

Prosentase 174.6% 143.5% 85.2% 111.8%

2004 2005 2006 2007

December 2007, December 2007, net credit net credit expansion expansion disbursed disbursed by by banking systems to banking systems to MSMEs reached MSMEs reached IDR 96.2 trillion IDR 96.2 trillion (111.8%) from 2007 (111.8%) from 2007 total business plan total business plan amounting to IDR amounting to IDR 86 trillion.86 trillion.

11

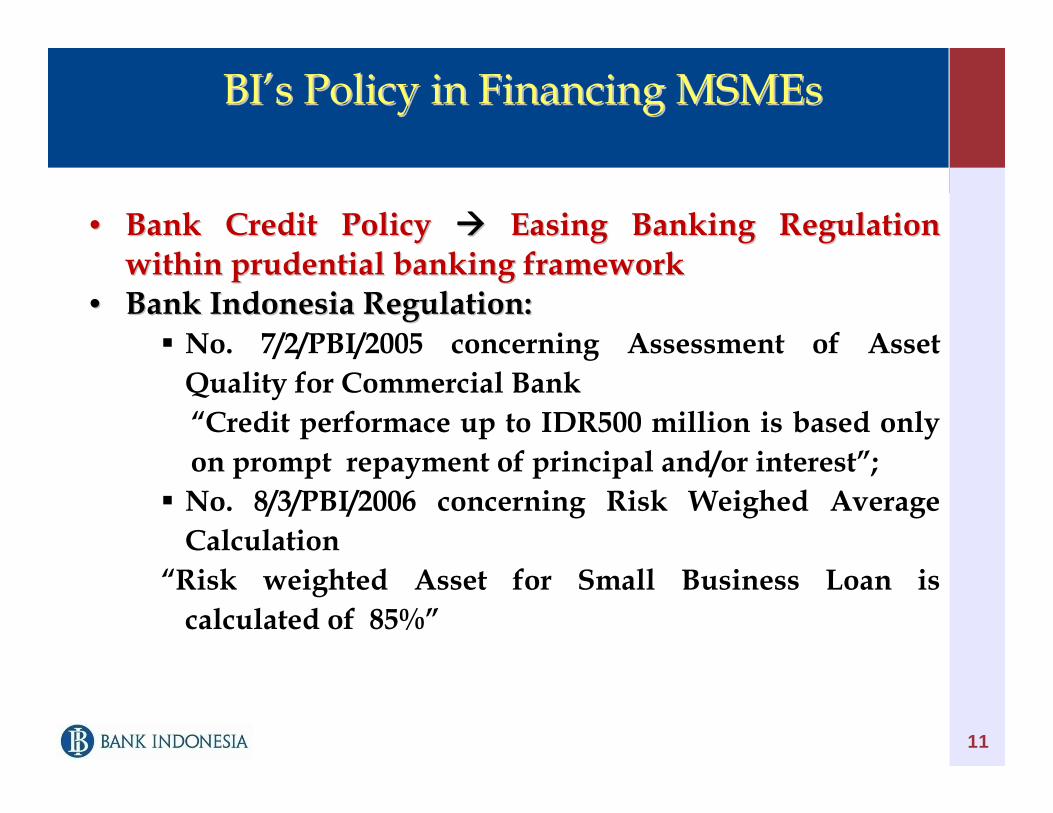

BIBI’’s Policy in Financing MSMEss Policy in Financing MSMEs

•• Bank Credit Policy Bank Credit Policy Easing Banking Regulation Easing Banking Regulation within prudential banking frameworkwithin prudential banking framework

•• Bank Indonesia Regulation:Bank Indonesia Regulation:No. 7/2/PBI/2005 concerning Assessment of Asset Quality for Commercial Bank“Credit performace up to IDR500 million is based only on prompt repayment of principal and/or interest”;No. 8/3/PBI/2006 concerning Risk Weighed Average Calculation

“Risk weighted Asset for Small Business Loan is calculated of 85%”

12

BIBI’’s Policy in Financing MSMEss Policy in Financing MSMEs

• Bank Credit Policy Debtor Information Systema. Bank Indonesia Regulation No. 7/8/PBI/2005 concerning

Debtor Information System (SID) To assist reporting entities in expediting the process of provision of fund, facilited the application of risk management, and assist Banks in identification of assist Banks in identification of debitor quality debitor quality for purposes of legal compliancelegal compliance;Since December 2005, Banks should report all of Bank debtors >IDR1 to Bank Indonesia

13

BIBI’’s Policy in Financing MSMEs prior 2004s Policy in Financing MSMEs prior 2004

• Cooperation between Bank Indonesia and Government Cooperation between Bank Indonesia and Government and Relevant Agenciesand Relevant Agencies•• Cooperation with Government on poverty alleviation Cooperation with Government on poverty alleviation

Bank Indonesia signed a MoU with the Coordinating Minister of Social Welfare on poverty alleviation through the promotion and development of MSMEs

•• Cooperation with Ministry of Cooperatives and Small Cooperation with Ministry of Cooperatives and Small and Medium Enterprises and Medium Enterprises In collaboration with the Ministry of Cooperatives and MSME, Bank Indonesia signed an MoU with the goal of improving MSMEs access to banking system through training programs for BDSP.

14

BIBI’’s Policy in Financing MSMEss Policy in Financing MSMEs

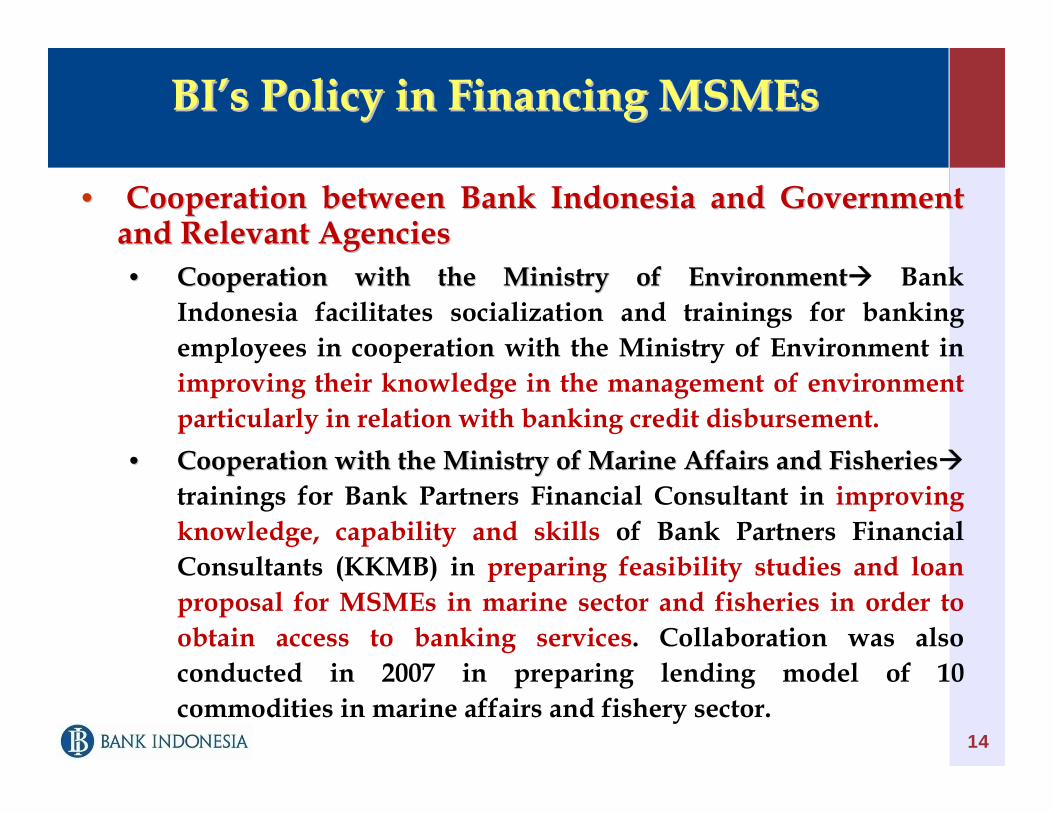

•• Cooperation between Bank Indonesia and Government Cooperation between Bank Indonesia and Government and Relevant Agenciesand Relevant Agencies•• Cooperation with the Ministry of EnvironmentCooperation with the Ministry of Environment Bank

Indonesia facilitates socialization and trainings for banking employees in cooperation with the Ministry of Environment in improving their knowledge in the management of environment particularly in relation with banking credit disbursement.

•• Cooperation with the Ministry of Marine Affairs and FisheriesCooperation with the Ministry of Marine Affairs and Fisheriestrainings for Bank Partners Financial Consultant in improving knowledge, capability and skills of Bank Partners Financial Consultants (KKMB) in preparing feasibility studies and loan proposal for MSMEs in marine sector and fisheries in order to obtain access to banking services. Collaboration was also conducted in 2007 in preparing lending model of 10 commodities in marine affairs and fishery sector.

15

The Indonesia Banking Architecture (API)The Indonesia Banking Architecture (API)

The Indonesian Banking Architecture (API) The Indonesian Banking Architecture (API) is a comprehensive basic framework for Indonesian banking system, outlining the direction, outline, and structure of the banking industry for next five to ten years; It launching on January 9, 2004 as crisis recovery programThe visionThe vision: “building a sound, strong, and efficient banking building a sound, strong, and efficient banking industry in order to create financial system stability for industry in order to create financial system stability for promotion of national economic growthpromotion of national economic growth””;;The programsThe programs: set out a more concrete direction and strategy for the consolidation of banking system, longterm consolidation of banking system, longterm development of sharia banking, expantion in financing development of sharia banking, expantion in financing MSMEs and institutional strengthening of Rural Banks MSMEs and institutional strengthening of Rural Banks (BPRs)(BPRs)

16

6 Pillars of API6 Pillars of API

“Building a sound, strong, and efficient banking industry in order to create financial system stability for promotion of

national economic growth”.

Heathty Banking Structure

Effective Regulation

System

Effective & Independent Supervisory

System

Strong Banking Industry

Adequate Infrastructure

Robust Consumer Protection

Pillar 1 Pillar 2 Pillar 3 Pillar 4 Pillar 5 Pillar 6

17

The APIThe API’’s Program for supporting MSMEs s Program for supporting MSMEs

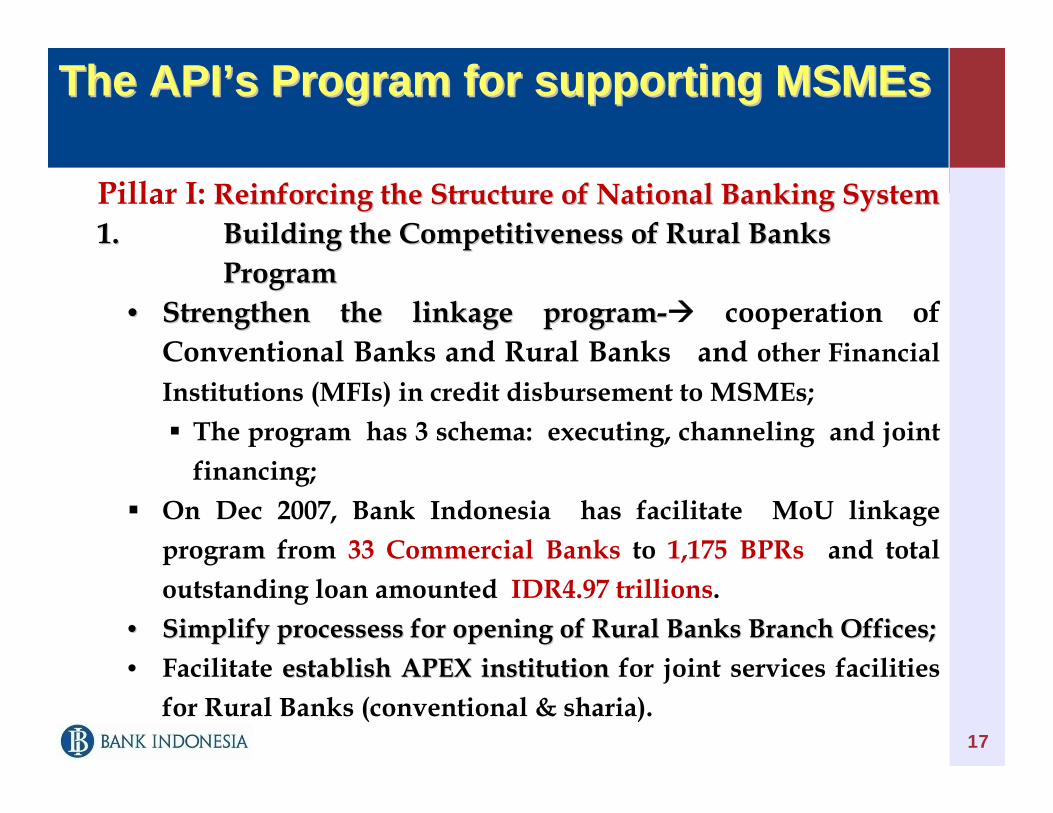

Pillar I: Reinforcing the Structure of National Banking SystemReinforcing the Structure of National Banking System1.1. Building the Competitiveness of Rural Banks Building the Competitiveness of Rural Banks

ProgramProgram•• Strengthen the linkage programStrengthen the linkage program-- cooperation of

Conventional Banks and Rural Banks and other Financial Institutions (MFIs) in credit disbursement to MSMEs;

The program has 3 schema: executing, channeling and joint financing;

On Dec 2007, Bank Indonesia has facilitate MoU linkage program from 33 Commercial Banks to 1,175 BPRs and total outstanding loan amounted IDR4.97 trillions.

•• Simplify processess for opening of Rural Banks Branch Offices;Simplify processess for opening of Rural Banks Branch Offices;• Facilitate establish APEX institution establish APEX institution for joint services facilities

for Rural Banks (conventional & sharia).

18

The APIThe API’’s Program for supporting MSMEs s Program for supporting MSMEs

Pillar I: Reinforcing the Structure of National Banking SystemPillar I: Reinforcing the Structure of National Banking System1.1. Improve Access to Credit ProgramImprove Access to Credit Program

Promotion of the Role of Credit Guarantee Institution to overcome constraints in accessing Bank credit to fulfill an additional collateral, BI is facilitating the development of a credit guarantee scheme involving Regional Government, Regional Banks and the guaranteeing company (PT Askrindo and PT. Sarana Pengembangan Usaha) Dec 2007, BI has facilitate 5 Regional Government, 12 Government Regency and 6 Government Municipal has participate in credit guarantee program with total value IDR61 miliar.

Pillar II: Improved Quality of Banking RegulationPillar II: Improved Quality of Banking RegulationFormalizing the Syndication Process in Policy Making ProgramFormalizing the Syndication Process in Policy Making Program BI

has facilitate establisment of 4 Regional Banking Research Institution (LRPD)

19

The APIThe API’’s Program for supporting MSMEs s Program for supporting MSMEs

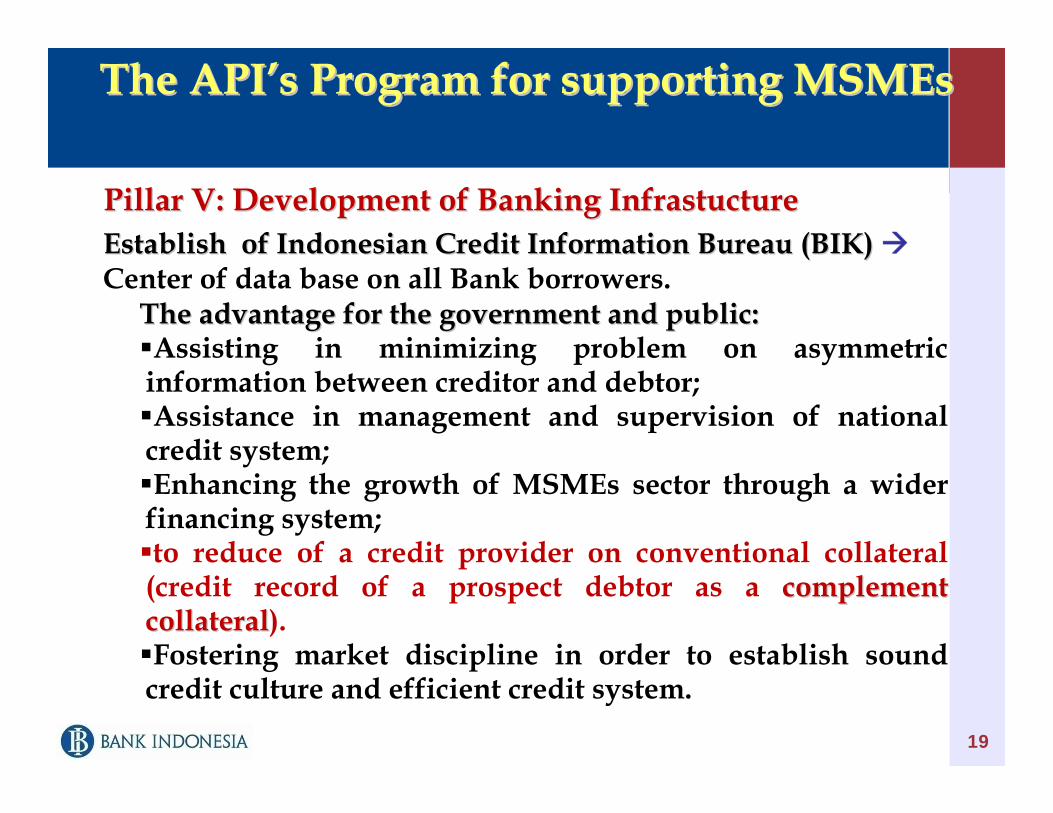

Pillar V: Development of Banking InfrastucturePillar V: Development of Banking InfrastuctureEstablish of Indonesian Credit Information Bureau (BIK) Establish of Indonesian Credit Information Bureau (BIK) Center of data base on all Bank borrowers.

The advantage for the government and public:The advantage for the government and public:Assisting in minimizing problem on asymmetric

information between creditor and debtor;Assistance in management and supervision of national

credit system;Enhancing the growth of MSMEs sector through a wider

financing system;to reduce of a credit provider on conventional collateral

(credit record of a prospect debtor as a complement complement collateralcollateral). Fostering market discipline in order to establish sound

credit culture and efficient credit system.

20

PILAR VI : Improvement of Consumer ProtectionPILAR VI : Improvement of Consumer Protection1.1. Prepare Standards for Customer Complaint MechanismPrepare Standards for Customer Complaint Mechanism

Bank Indonesia Regulation (PBI) No 7/7/PBI/2005 concerning Resolution of Customer Complaints: Bank should resolve the customer complaint, especially related with potential financial losses.

2.2. Establish Independent Mediation AgencyEstablish Independent Mediation AgencyBank Indonesia Regulation (PBI) No. 8/5/PBI/2006 concerning Banking Mediation: As alternative dispute resolution (by way of Mediation);The objectives are:

Help customers and Banks to settled in fair, efficient and speddy manner;Financial claim no more than IDR500 million;Voluntary resolve customers complaint.

The APIThe API’’s Program for supporting MSMEs s Program for supporting MSMEs

21

The APIThe API’’s Program for supporting MSMEs s Program for supporting MSMEs

Pillar VI : Improvement of Consumer ProtectionPillar VI : Improvement of Consumer Protection1.1. Prepare Regulation on Transparancy of Product Prepare Regulation on Transparancy of Product

InformationInformationBank Indonesia Regulation (PBI) No. 7/6/PBI/2005 concerning Transparency in Bank Product Information & Use of Customer Personal Data.

2.2. Promote Consumer EducationPromote Consumer EducationEstablish “Banking Education Working Group”Launching “Blue Print Financial Consumer

Education”etc

Customer Due Diligence (CDD)/Know Your Customer

22

To prevent the banking industry from becoming a vehicle or objective of criminal activities directly or indirectly conducted by criminal, as an international initiative recommendation of:

Basel Committee on Banking Supervision Core Principles for Effective Banking Supervision;Financial Action Task force (FATF) 40 recommendation and 9 special recommendation (SR).

To implement the international initiative of prudential principles, Bank Indonesia regulate the application of Know Bank Indonesia regulate the application of Know Your CustomerYour Customer’’s Principles (KYC) for commercial banks and s Principles (KYC) for commercial banks and rural banks; rural banks;

Know Your Customer Principles (KYC)

23

Know Your Customer Principles (KYC) Know Your Customer Principles (KYC) are principles should implemented by bank in order to know and recoqnize the customer’s identity, monitor its customer’s transaction including to report suspicious transaction (STR)

Bank Indonesia as supervisor should ensureBank Indonesia as supervisor should ensure:banks have adequate controls and procedures to know the

customers with whom they are has a dealing;evade banks become subject to reputational, operasional, legal and concentration risk, which can result in significant cost;

24

Bank Should Implement the KYC Bank Should Implement the KYC

Bank shall establish: • policy on customer

acceptance;• Policy and procedure for

customer’s identification;• Policy and procedure for

monitoring customer’s account and transaction;

• Policy and procedure of risk management in line with the implementation of KYC principles.

The Board of Director is responsible for implementation of KYC;Bank shall establish a special unit or appoint an officer who is responsible for the implementation of KYC;The special unit or officer shall be directly reponsible to the Compliance Director.

Policy on Customer Acceptance and Identification

Perspective customer

Bank

Identification of legal document

Verify the authenticity of authenticity of supporting documentssupporting documents;If bank provide electronic banking service shall meet the meet the prospective customerprospective customer at least at the time of account opening;If necessary, bank may conduct an interview with the interview with the prospective customer. prospective customer.

identificationidentification document;Purposes and objectives of Purposes and objectives of businessbusiness relationship the prospective customer intends to have with the banks;prospective customercustomer’’s profiles profile;beneficial owner beneficial owner

identificationidentification, incase the prospective customer acts for and on behalf of other party.

Individual Customer:Description: name, permanent

residential address, date and place of birth & nationality;Occupation;Speciment of signature;Source of fund & purpose of

fund.

Corporate Customer

Small company;Bigger company;Government institution;Bank.

Policy on Customer Acceptance and Identification

Customer Acceptance Procedur

Policy on Customer Acceptance and IdentificationPolicy on Customer Acceptance and Identification

27

Bank would refuse to open an account and/or refuse to Bank would refuse to open an account and/or refuse to conduct transactions, if prospective customerconduct transactions, if prospective customer:not complying with the provisions;using false identity and/or providing false information;incorporated as a shell bank or with any bank permitting

its accounts to be used by shell banks.

Banks can refuse to conduct transactions and/or may terminate business dealings with existing customers in the event that:

if the criteria customers acceptance aren’t met;an account is un-used in departure from the purpose of

opening the account.

Bank shall maintain Bank shall maintain customercustomer’’s profile at s profile at least:least:• Occupation or

business sector;• Total earning;• Other customer’s

account;• Activity of normal

transaction;• Purpose of account

opening

Bank shall:Bank shall:•• maintain the documents maintain the documents

customercustomer’’s identity at least s identity at least 5 years after the customer5 years after the customer’’s s account has been closed;account has been closed;

•• up date the document (data up date the document (data base) in case of any changesbase) in case of any changes

BBank requiredank required::• to have information system information system

effectivelyeffectively capable of identifying, analyzing, monitoring and providing report on the characteristics of transactions;

• to conduct monitoring of bank conduct monitoring of bank customer transactionscustomer transactions, including identification of any occurrence of STR----> transaction instruments, dates, amount & denomination of transaction-

Monitoring, CustomerMonitoring, Customer’’s Account and s Account and TransactionTransaction

Bank

Risk Management Policy AssessmentRisk Management Policy Assessment

29

Assessment of risk management policy and prosedure Assessment of risk management policy and prosedure shall based on the results of examination conducted by shall based on the results of examination conducted by Bank Indonesia that covers risk management factors as Bank Indonesia that covers risk management factors as followsfollows:Bank’s management oversight;Policies and procedures;Internal Control and internal audit function;Management information system; andHuman resources and training.

KYC Impact in Bank Rating KYC Impact in Bank Rating

30

The rating on the implementation of KYC and the AML law shall be calculated into soundness rating soundness rating of commercial banks under the management factormanagement factor.

If the rating on the implementation of KYC and the AML is 5, the rating shall not only be calculated into soundness ratingsoundness rating, but also tied to imposition of imposition of administrative sanctions in the form of downgrading of administrative sanctions in the form of downgrading of the soundness rating and order for dismissal of the the soundness rating and order for dismissal of the managementmanagement of the commercial bank under the mechanism of the fit and proper testfit and proper test.

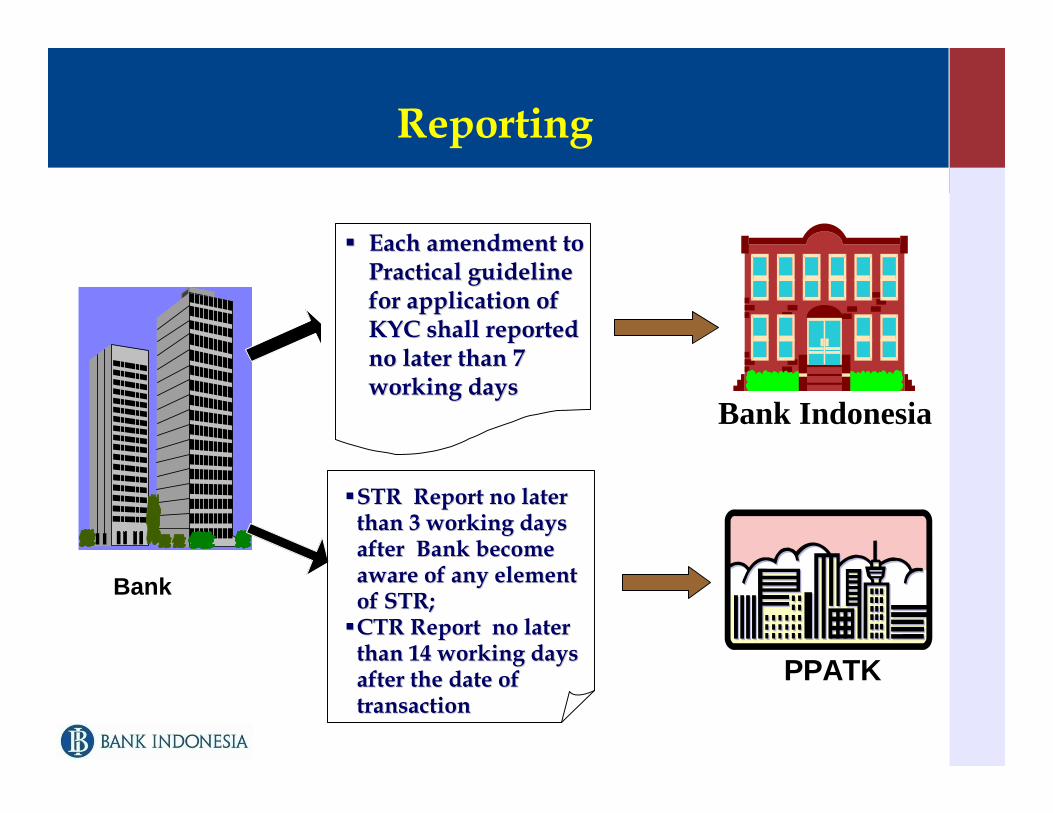

Reporting

Each amendment to Each amendment to Practical guideline Practical guideline for application of for application of KYC shall reported KYC shall reported no later than 7 no later than 7 working daysworking days

STR Report no later STR Report no later than 3 working days than 3 working days after Bank become after Bank become aware of any element aware of any element of STR;of STR;CTR Report no later CTR Report no later than 14 working days than 14 working days after the date of after the date of transactiontransaction

Bank Indonesia

PPATK

Bank

Customer Due Diligence (CDD) Customer Due Diligence (CDD)

32

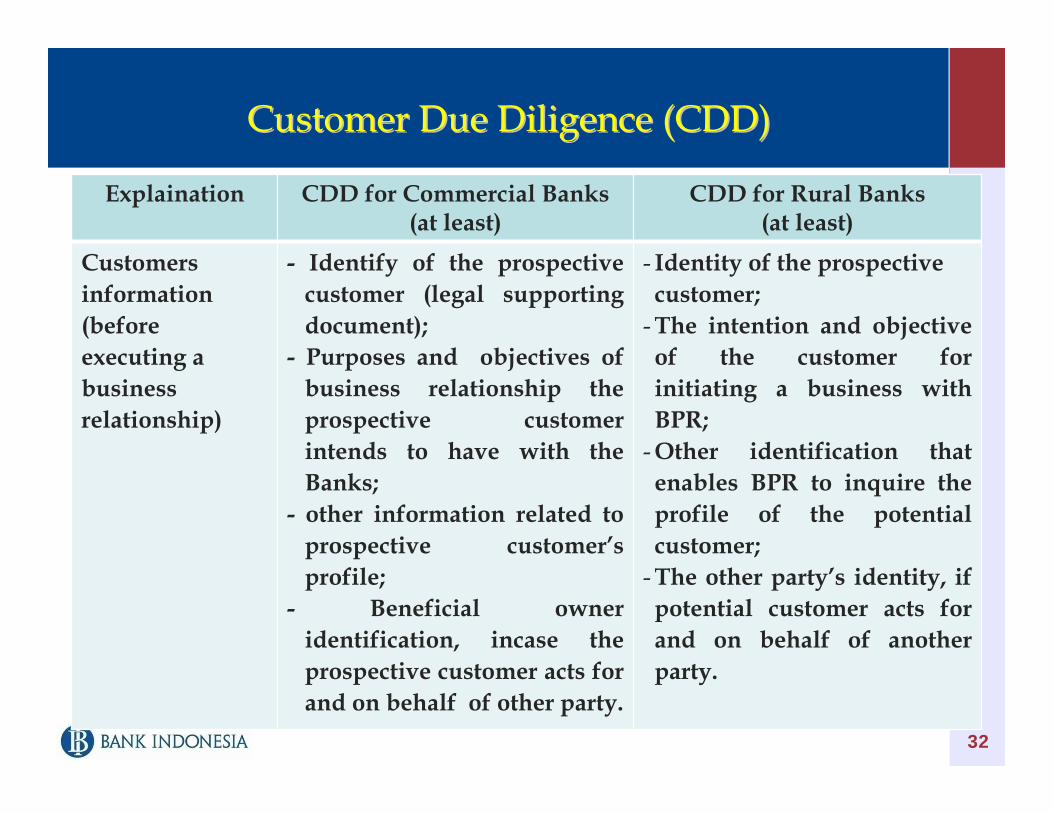

Explaination CDD for Commercial Banks (at least)

CDD for Rural Banks(at least)

Customers information (before executing a business relationship)

- Identify of the prospective customer (legal supporting document);

- Purposes and objectives of business relationship the prospective customer intends to have with the Banks;

- other information related to prospective customer’s profile;

- Beneficial owner identification, incase the prospective customer acts for and on behalf of other party.

- Identity of the prospective customer;

- The intention and objective of the customer for initiating a business with BPR;

- Other identification that enables BPR to inquire the profile of the potential customer;

- The other party’s identity, if potential customer acts for and on behalf of another party.

Customer Due Diligence (CDD) Customer Due Diligence (CDD)

33

Explaination CDD for Commercial Banks

(at least)

CDD for Rural Banks(at least)

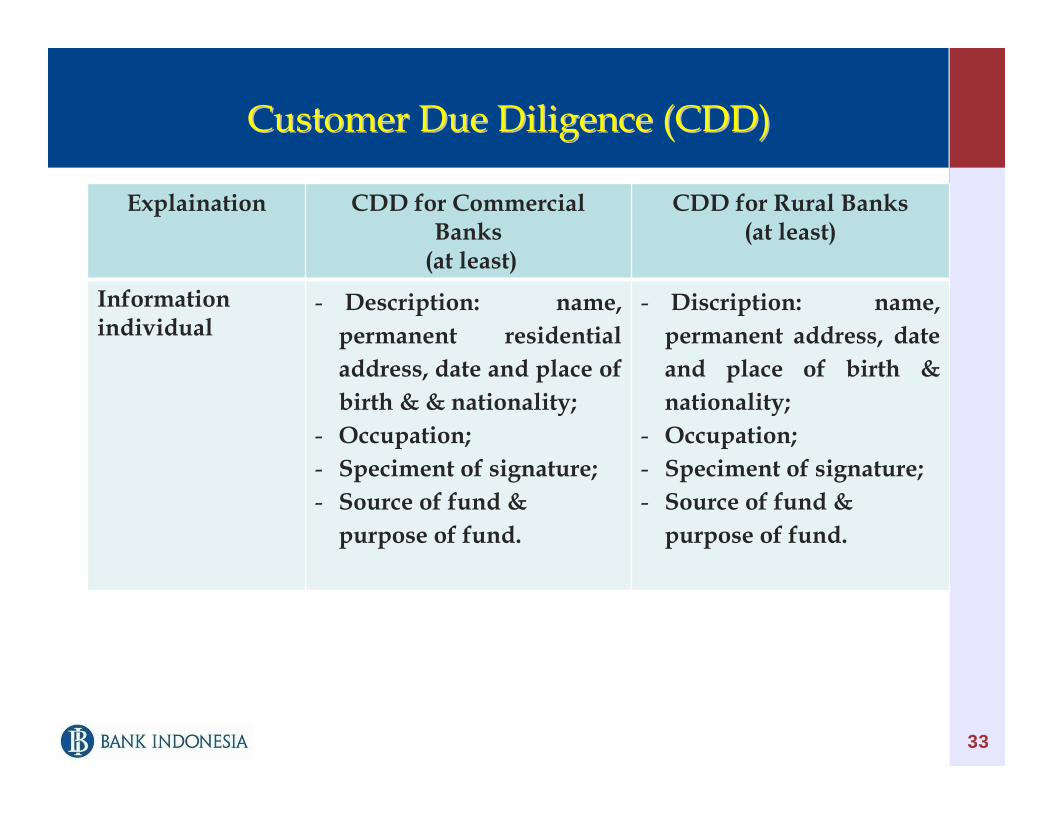

Information individual

- Description: name, permanent residential address, date and place of birth & & nationality;

- Occupation;- Speciment of signature;- Source of fund &

purpose of fund.

- Discription: name, permanent address, date and place of birth & nationality;

- Occupation;- Speciment of signature;- Source of fund &

purpose of fund.

Customer Due Diligence (CDD) Customer Due Diligence (CDD)

34

Explanation CDD for Commercial Banks(at least)

CDD for Rural Banks(at least)

Small company information

Small company informationSmall company information- Article of association/ corporation;

- Business license or other license from authorized institution;

- Company description: name, speciment of signature, and power of attorney of any having authority to act on behalf of the company for conducting business relationship with the bank;

- Source and purpose of fund

Company customer information:-Arcitle of association/ corporation;-Business license from authorized institution;-Company disciption: name, specimen of signature, and power of attorney of any having authority to act on behalf of the company for conducting business relationship with the BPR;-Source and purpose of fund; -Tax number (NPWP);-Identity of the manager who represents the company.

Customer Due Diligence (CDD) Customer Due Diligence (CDD)

35

Explaination CDD for Commercial Banks (at least) CDD for Rural Banks(at least)

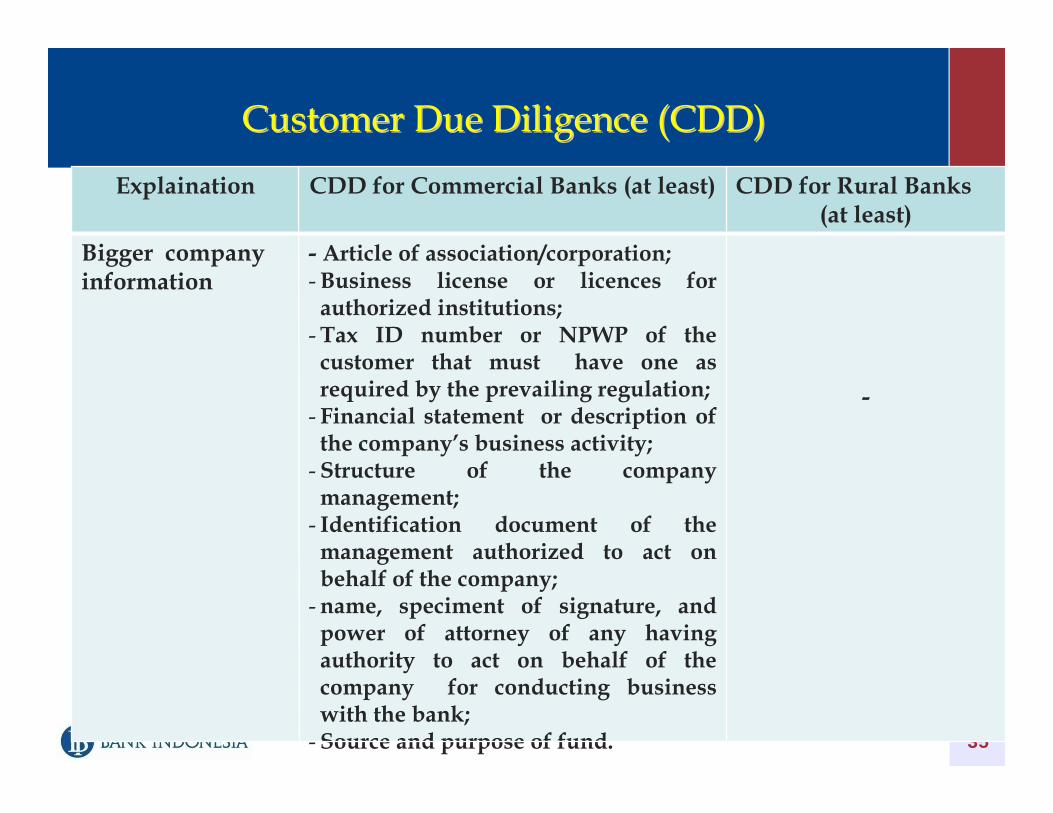

Bigger company information

- Article of association/corporation;- Business license or licences for

authorized institutions;- Tax ID number or NPWP of the

customer that must have one as required by the prevailing regulation;

- Financial statement or description of the company’s business activity;

- Structure of the company management;

- Identification document of the management authorized to act on behalf of the company;

- name, speciment of signature, and power of attorney of any having authority to act on behalf of the company for conducting business with the bank;

- Source and purpose of fund.

-

Thank youThank you

http :www.bi.go.id