the role of private equity and debt funds in sme and...

TRANSCRIPT

THE ROLE OF PRIVATE EQUITY

AND DEBT FUNDS IN SME AND

INFRASTRUCTURE FINANCE

December 7, 2015

101672

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Outline

Section 1: Overall Evolution of PE Funds

Section 2: Emergence of Private Debt Funds

Section 3: Venture Capital Funds

Section 4: Infrastructure Funds

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance1

Section 1: Private equity funds assets under management (AUM)

have grown from US$ 963 billion in 2004 to US$ 3.4 trillion in 2013.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance2

298 377 407 402 409563

8061,011 1,075 1,067 993 1,007 941 1,046418 374 360 465 554

675

898

1,265 1,2041,413

1,7832,029

2,3322,420

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Dec-0

0

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Ju

n-1

3

Private Equity Assets under Management December 2004 - June 2013 (US$ billion)

Dry Powder Unrealized ValueSource: 2014 Preqin Global Private Equity Report

Section 1: By geographical area, the main areas of focus are the US

and Europe, followed by Asia. The rest of the world is at a low level,

but growing slowly.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance3

Source: 2014 Preqin Global Private Equity Report

0

100

200

300

400

500

600

700

Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

Dry

Po

wd

er

($b

n)

Private Equity Dry Powder by Primary Geographic Focus 2003 – 2013 (US$ billion)

North America Europe Asia Rest of World

Section 1: Among emerging markets, emerging Asia is the

main geographical focus area (with China and India leading),

followed by Latin America (with Brazil leading)

4 Presentation Title

-

5.00

10.00

15.00

20.00

25.00

2009 2010 2011 2012 2013

Evolution on PE investments in Emerging Markets by region, in US$ billion

Emerging Asia China India

CEE and CIS Russia Latin America

Brazil MENA Sub-Saharan Africa

Source: EMPEA Database

Section 1: By type of fund, buyout funds dominate, followed by real

estate, venture capital and infrastructure. Mezzanine debt represents

a small share of the total, but is growing.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance5

0

200

400

600

800

1,000

1,200

Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

Dry

Po

wd

er

($b

n)

Private Equity Dry Powder by Fund Type 2004 – 2013 (US$ billion)

Buyout Distressed Private Equity GrowthInfrastructure Mezzanine Real EstateVenture Capital Other

Source: 2014 Preqin Global Private Equity Report

Section 1: After dropping following the international financial crisis in

2008, private equity-backed exits have rebounded sharply in the

2010-2013 period.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance6

0

20

40

60

80

100

120

140

0

50

100

150

200

250

300

350

400

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2006 2007 2008 2009 2010 2011 2012 2013

Ag

gre

ga

te E

xit V

alu

e ($

bn

)

No

. o

f E

xit

s

Private Equity-Backed Exits by Type Q1 2006 - Q4 2013

IPO Restructuring Sale to GP Trade Sale Aggregate Exit Value ($bn)

Source: 2014 Preqin Global Private Equity Report

Section 1: The investor base for private equity funds has

undergone major transformation over the past 6 years.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance7

Source: 2014 Preqin Global Private Equity Report

27%

11%

6%

9%

7%

2%

10%

1% 1%

7%

9%10%

13%

14%

7%

11%

8%

10%

4%

6%

8%

6%

3%

10%

0%

5%

10%

15%

20%

25%

30%

Pub

lic P

ensio

nF

und

s

Fu

nd

of

Fu

nd

sM

an

ag

ers

Priva

te S

ecto

rP

en

sio

n F

un

ds

Hig

h-N

et-

Wo

rth

Ind

ivid

uals

Insu

ran

ce

Com

pan

ies

Gove

rnm

en

tA

ge

ncie

s

End

ow

me

nt

Pla

ns

Co

rpora

teIn

ve

sto

rs

Fa

mily

Off

ices

Ban

ks &

Inve

stm

ent

Ban

ks

Fo

un

datio

ns

Oth

er

Pro

po

rtio

n o

f C

ap

ital C

om

mit

ted

Investor Type

Make-up of LPs in the Average Fund by LP Type (Capital Committed to Funds Closed in 2008-2013)

2008-2010

2011-2013

Section 1: In terms of performance, private equity horizon IRR

outperformed major market indices in 2013. However, this

performance was driven by buyout fund, while venture capital

underperformed market indices.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance8

-5%

0%

5%

10%

15%

20%

25%

30%

1 Year to Jun-13 3 Years to Jun-13 5 Years to Jun-13 10 Years to Jun-13

An

nu

ali

ze

d R

etu

rns

Private Equity Horizon IRRs vs. Public Indices as of 30 June 2013

All Private Equity

Buyout

Venture Capital

S&P 500

MSCI Europe

MSCI EmergingMarkets

Source: 2014 Preqin Global Private Equity Report

Outline

Section 1: Overall Evolution of PE Funds

Section 2: Emergence of Private Debt Funds

Section 3: Venture Capital Funds

Section 4: Infrastructure Funds

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance9

Section 2: Since the international financial crisis in 2008, private

debt funds (including mezzanine funds) have grown rapidly.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance10

Source: Preqin Special Report: Private Debt Report, November 2014

60

8388

94

137

69

23

4145

60

77

37

0

20

40

60

80

100

120

140

160

2009 2010 2011 2012 2013 2014 YTD

Year of Final Close

Annual Private Debt Fundraising 2009 - 2014 YTD (As at 20 October 2014)

No. of Funds Closed

Aggregate CapitalRaised ($bn)

Section 2: By geographical area, the main areas of focus are North

America, followed by Europe and Asia and the rest of the world.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance11

Source: Preqin Special Report: Private Debt Report, November 2014

17%17%

15% 17% 13% 14%

22%

22%

20%26%

21%

33%

62%

31%

65%57%

66%

52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014 YTD

Pro

po

rtio

n o

f F

un

ds

Year of Final Close

Breakdown of the Number of Private Debt Funds Closed by Primary Geographic Focus 2009 - 2014 YTD (As at 11.20.2014)

North America

Europe

Asia & Rest ofWorld

Section 2: By type of fund, direct lending funds dominate,

followed by mezzanine and distressed debt.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance12

Source: Preqin Special Report: Private Debt Report, November 2014

40%

36%

12%

9%3%

Primary Strategy of Private Debt Fund Managers Established Since 2008

Direct Lending

Mezzanine

Distressed Debt

Special Situation

Venture Debt

Outline

Section 1: Overall Evolution of PE Funds

Section 2: Emergence of Private Debt Funds

Section 3: Venture Capital Funds

Section 4: Infrastructure Funds

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance13

Section 3: After reaching a peak in 2008, venture capital fund raising

dropped significantly following the international financial crisis in

2009 and 2010. It rebounded significantly in 2011, but has tapered off

since then.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance14

Source: 2014 Preqin Global Private Equity Report

31

1417

2216

7

9

54

3

6

5

12

6 5

1515

15

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013

Ag

gre

ga

te C

ap

ital

Rais

ed

($b

n)

Year of Final Close

Annual Venture Capital Fundraising by Primary Industry Focus 2008 – 2013 (US$ billion)

InformationTechnology

Healthcare

Other Industries

Section 3: By stage, venture capital deal flow is led by angel/seed

deals, followed by round 1 deals and round 2 deals, showing the

critical role played by private equity at early stages of development of

SMEs. Venture debt represents less than 7% of the total.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance15

Source: 2014 Preqin Global Private Equity Report

22%

2%

22%

2%

13%

10%

15%

11%

8%

12%

9%

12%

4%

12%

4%

10%

3%

13%

3%

14%

2% 5%2%

3%1% 2% 1%

1%

32%27%

33%31%

6%

5%

4%7%

8%13%

7% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No. of Deals Aggregate Deal Value No. of Deals Aggregate Deal Value

2012 2013

Pro

po

rtio

n o

f To

tal

Proportion of Number and Aggregate Value of Venture Capital Deals by Stage 2012 – 2013

Angel/Seed Series A/Round 1 Series B/Round 2 Series C/Round 3

Series D/Round 4 and Later Growth Capital/Expansion PIPE Unspecified Round

Venture Debt Add-on & Other

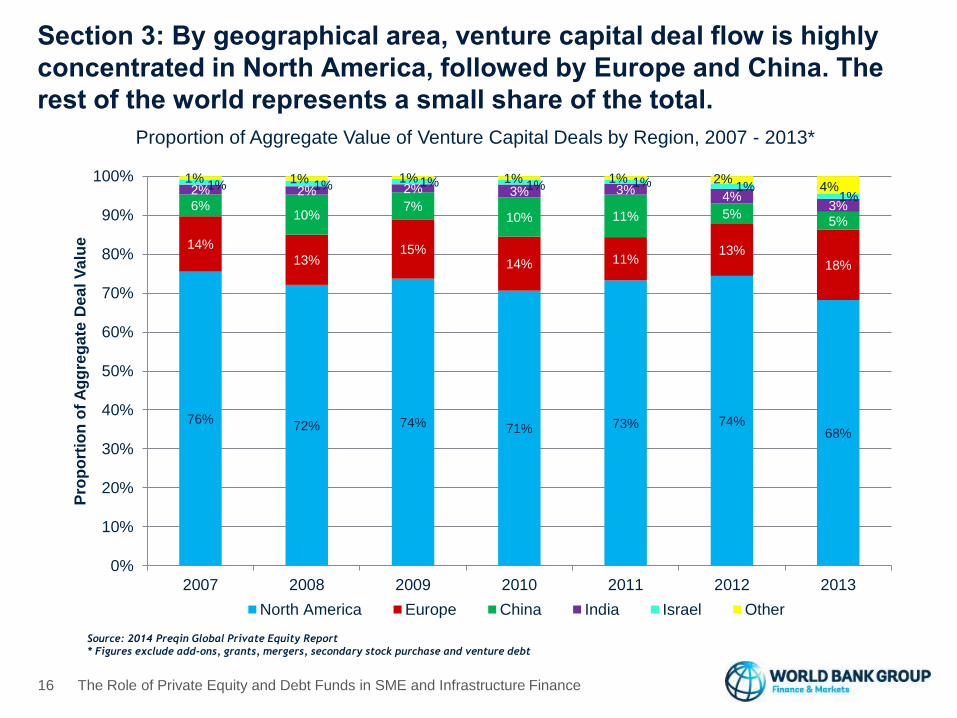

Section 3: By geographical area, venture capital deal flow is highly

concentrated in North America, followed by Europe and China. The

rest of the world represents a small share of the total.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance16

Source: 2014 Preqin Global Private Equity Report

* Figures exclude add-ons, grants, mergers, secondary stock purchase and venture debt

76%72% 74% 71% 73% 74%

68%

14%

13%15%

14% 11%13%

18%

6%10%

7%10% 11% 5%

5%

2% 2% 2% 3% 3%4%

3%

1% 1% 1% 1% 1% 1%1%

1% 1% 1% 1% 1% 2%4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013

Pro

po

rtio

n o

f A

gg

reg

ate

Dea

l V

alu

e

Proportion of Aggregate Value of Venture Capital Deals by Region, 2007 - 2013*

North America Europe China India Israel Other

Section 3: By industry, venture capital deal flow is led by

internet, followed by software, healthcare and telecoms.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance17

Source: 2014 Preqin Global Private Equity Report

27%22% 25% 23%

18%

14%

22%21%

18%

25%

16% 22%

12%9%

14% 10%

8%

8%

8% 9%2%

2%

3% 3%4%9%

3% 4%4% 2% 3% 2%3% 2%2% 1%3% 3% 2% 3%3% 3% 3% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No. of Deals Aggregate DealValue

No. of Deals Aggregate DealValue

2012 2013

Pro

po

rtio

n o

f To

tal

Proportion of Number and Aggregate Value of Venture Capital Deals by Industry 2012 – 2013

Internet Software & Related Healthcare

Telecoms Other IT Business Services

Clean Technology Consumer Discretionary Industrials

Semiconductors & Electronics Other

Outline

Section 1: Overall Evolution of PE Funds

Section 2: Emergence of Private Debt Funds

Section 3: Venture Capital Funds

Section 4: Infrastructure Funds

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance18

Section 4: Unlisted infrastructure funds AUM have grown from

US$ 17 billion in 2004 to US$ 244 billion in 2013.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance19

Source: 2014 Preqin Global Infrastructure Report

3 4 11 15

37

61 63 64 6890 82 87

4 56 9

16

3349

60

92

127 149157

0

50

100

150

200

250

300

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Ju

n-1

3

As

se

ts u

nd

er

Ma

na

ge

me

nt

($b

n)

Unlisted Infrastructure Assets under Management December 2004 - June 2013

UnrealizedValue ($bn)

Dry Powder($bn)

Section 4: By project stage, infrastructure fund deals are led

by secondary stage, followed by greenfield and brownfield.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance20

Source: 2014 Preqin Global Infrastructure Report

59%

28%

13%

Breakdown of Unlisted Infrastructure Deals by Project Stage 2008 – 2013

Secondary Stage

Greenfield

Brownfield

Section 4: By geographical area, the main areas of focus are

North America, followed by Europe and Asia.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance21

Source: 2014 Preqin Global Infrastructure Report

36 31

11 8

73

52

1616

0

20

40

60

80

100

120

North America Europe Asia Rest of World

As

se

ts u

nd

er

Ma

na

ge

me

nt

($b

n)

Fund Primary Geographic Focus

Unlisted Infrastructure Assets under Management by Fund Primary Geographic Focus as of June 2013

Unrealized Value($bn)

Dry Powder ($bn)

Section 4: By industry, infrastructure fund deal flow is led by

renewable energy, followed by transport, social infrastructure and

energy.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance22

Source: 2014 Preqin Global Infrastructure Report

29%

18%

18%

15%

14%

3% 3%

Breakdown of Infrastructure Deals by Industry, 2008 – 2013

Renewable Energy

Transport

Social

Energy

Utilities

Telecoms

Other

Section 4: By type of investor, private pension funds dominate,

followed by public pension funds, insurance companies and

foundations.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance23

Source: 2014 Preqin Global Infrastructure Report

19%

16%

10%

8%

6% 6% 6%

4% 4% 4% 4%

3% 3%2%

5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Private

Secto

rP

ensio

n F

unds

Public

Pensio

nF

un

ds

Insu

rance

Co

mpa

nie

s

Fou

nda

tio

ns

Asset

Man

age

rs

Banks

Endo

wm

ent

Pla

ns

Fun

d o

f F

und

sM

anag

ers

Inve

stm

ent

Co

mpa

nie

s

Wealth

Ma

nag

ers

Fam

ily O

ffic

es

Supe

rannu

ation

Sch

em

es

Govern

ment

Agen

cie

s

Sovere

ign

Wealth F

unds

Oth

er

Pro

po

rtio

n o

f In

ve

sto

rs

Investor Type

Breakdown of Infrastructure Investors by Type, 2013

Section 4: Since 2007, infrastructure investment funds have

outperformed the private equity class.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance24

Source: 2014 Preqin Global Infrastructure Report

0

20

40

60

80

100

120

140

160

Ind

ex R

etu

rns

(R

eb

ase

d t

o 1

00

as o

f 3

1 D

ece

mb

er

200

7) PrEQIn Index: Infrastructure vs. All Private Equity December 2007 – June 2013

PrEQIn AllPrivate EquityIndex

PrEQInInfrastructureIndex

Section 4: Following low levels of activity until 2005, unlisted private

infrastructure debt funds increased rapidly until the financial crisis in

2008. Following a sharp drop in 2009, infrastructure debt funds

recovered quickly, raising US$ 7.5 billion in 2013.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance25

Source: 2014 Preqin Global Infrastructure Report

5

3

6

9

1

6

7

10

7

1.81.2

3.5 3.6

0.2

1.3

6.2

3.4

7.5

0

2

4

6

8

10

12

199

8-2

00

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

Year of Final Close

Annual Infrastructure Debt Fund Raising, 1998-2013

No. of FundsClosed

Aggregate CapitalRaised ($bn)

Section 4: By geographical area, the main areas of concentration are

North America, followed by Europe and the rest of the world

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance26

Source: 2014 Preqin Global Infrastructure Report

15

19 19

21

18.3

10.9

6.3

8.2

0

5

10

15

20

25

North America Europe Asia Rest of World

Breakdown of Unlisted Infrastructure Debt Fund Universe by Primary Geographic Focus, 2013

No. of FundsClosed/Raising

Aggregate CapitalRaised/Targeted($bn)

Section 4: The number of listed infrastructure funds raised increased

from 2001 to 2009, but has remained stagnant since then.

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance27

Source: 2014 Preqin Global Infrastructure Report

32

1 39

3537

132

5

3

4

6

5

7

5 1

7

0

0

0

0

0

0

10

4 35

0

2

0

5

10

15

20

25

30

35

40

45

50

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

Listed Infrastructure Fund Launches, 2004 – 2013

No. of Funds Already Trading No. of Funds Launched

No. of Funds Delisted No. of Funds Liquidated

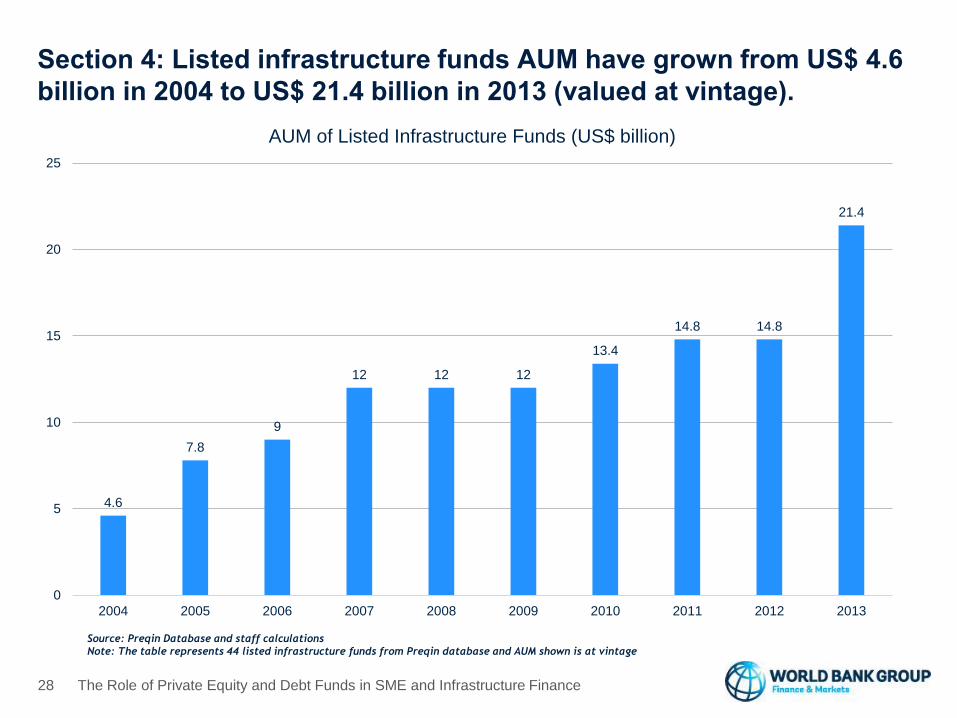

Section 4: Listed infrastructure funds AUM have grown from US$ 4.6

billion in 2004 to US$ 21.4 billion in 2013 (valued at vintage).

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance28

Source: Preqin Database and staff calculations

Note: The table represents 44 listed infrastructure funds from Preqin database and AUM shown is at vintage

4.6

7.8

9

12 12 12

13.4

14.8 14.8

21.4

0

5

10

15

20

25

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

AUM of Listed Infrastructure Funds (US$ billion)

Investment Funds Group Team

The Role of Private Equity and Debt Funds in SME and Infrastructure Finance29

Contact information:

Michel Noel

202-203-0874

Nikoloz Anasashvili

Consultant

Patrick J. McGinnis

ConsultantSevara Atamuratova

Research Analyst

Shanthi Divakaran

Sr. Financial Sector Specialist

Michel Noel

Head

Thelma Ayamel

Program Assistant