the role of sukuk in islamic capital markets - comcec.org · global development of sukuk issuances...

TRANSCRIPT

The Role of Sukuk in Islamic Capital MarketsPresented by Dr Marjan Muhammad (ISRA) and Ruslena Ramli (RAM Ratings)

The Role of Sukuk in Islamic Capital Markets (ICM)

10th MeetingCOMCEC Financial Cooperation Working Group

29 March 2018

Dr. Marjan Muhammad and Ruslena Ramli

2

1 INTRODUCTION: SCOPE & METHODOLOGY

2 ROLE OF SUKUK IN ISLAMIC CAPITAL MARKETS

3 KEY SUCCESS FACTORS IN DEVELOPING A SUKUK MARKET

4 GLOBAL DEVELOPMENT OF SUKUK STRUCTURES, ISSUANCES & INVESTMENT

PART 1: OVERVIEW OF SUKUK AND ICM

5 KEY ISSUES & CHALLENGES IN DEVELOPING SUSTAINABLE SUKUK MARKETS

Scope of the study

3

Objective: To analyse the role of sukuk as an instrument for capital market development and resource mobilisation, and as an alternative financing tool for the economic development of the public and private sectors

Theoretical and legal natures of sukuk Parties involved in developing & issuing

sukuk Requisites of a successful sukuk market

Sukuk growth, analysis of issuances, structures and investments

Factors & challenges affecting sukuk and policy recommendations

SUKUK STRUCTURES, ISSUANCES &

INVESTMENTS

Legal, regulatory, Shariah governance, and tax frameworks

Innovations Developmental challenges

CASE STUDIES & POLICY RECOMMENDATIONS

Scope:

KEY BUILDINGBLOCKS

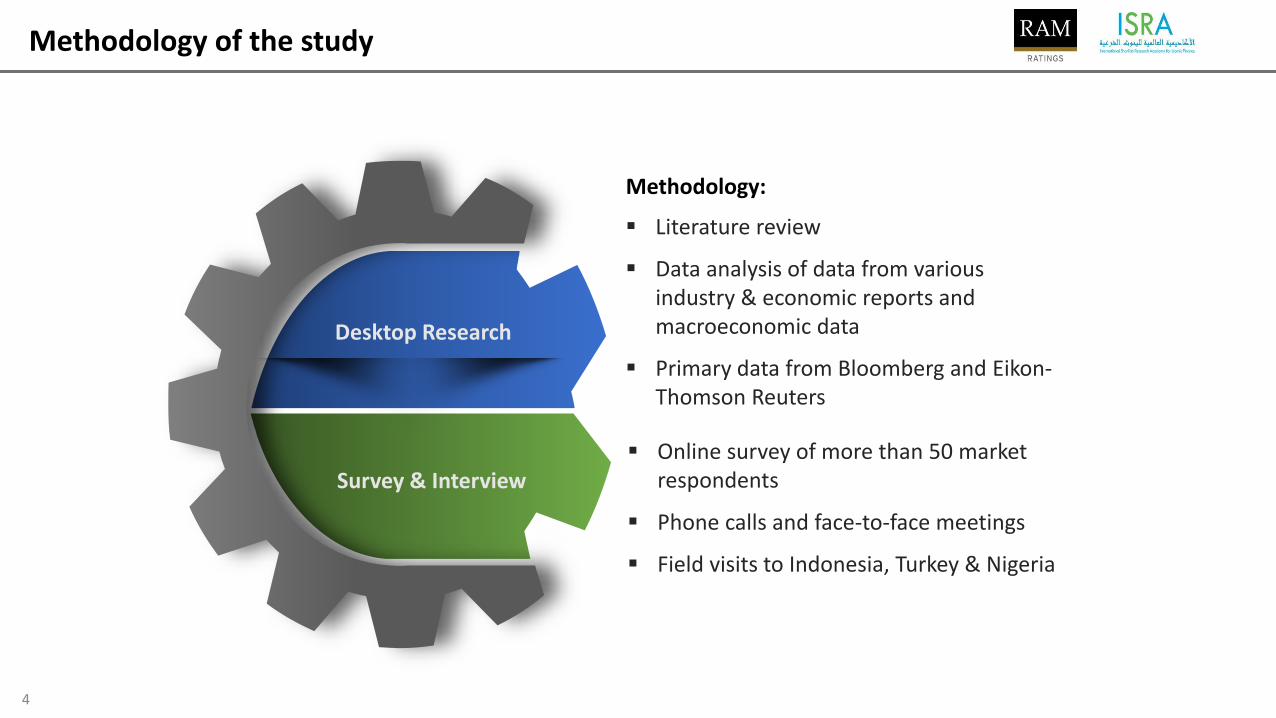

Methodology of the study

4

Methodology:

Desktop Research

Survey & Interview

Literature review

Data analysis of data from various industry & economic reports and macroeconomic data

Primary data from Bloomberg and Eikon-Thomson Reuters

Online survey of more than 50 market respondents

Phone calls and face-to-face meetings

Field visits to Indonesia, Turkey & Nigeria

Evolution of the sukuk industry

5

Initial attempts to develop sukuk- Muqaradah

bonds- Participation

terms cert- GII

Early sukuk issuance

- Shell MDS sukuk

- Period of theory and model building

Emergence of sukuk markets

- Bahrain government ijarah sukuk

- Malaysian global sukuk

Expansion of sukuk markets

- Green sukuk- More

jurisdictions issuing sukuk

Historical Pre-1990 1990 -2000 2001 -2016 2017 - Future

Classical use of sukuk

- Commodity/ grain coupon

- Esham

Global outlook of Islamic finance industry as at December 2017

6

Source: ICD-Thomson Reuters Report 2017

“The CAGR of Islamic finance assets from 2012 to 2017 stood at 7.4% with total assets of USD2.4 trillion as at end-2017 (projected)”

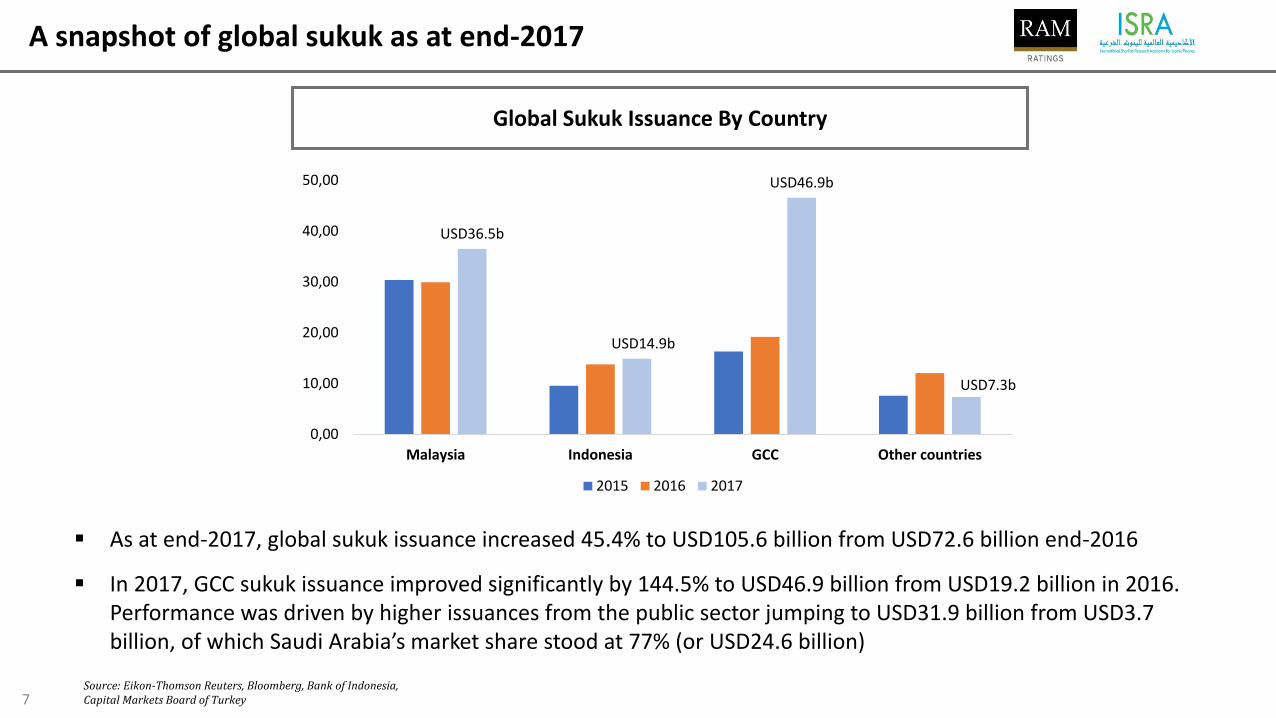

A snapshot of global sukuk as at end-2017

7

Global Sukuk Issuance By Country

As at end-2017, global sukuk issuance increased 45.4% to USD105.6 billion from USD72.6 billion end-2016

In 2017, GCC sukuk issuance improved significantly by 144.5% to USD46.9 billion from USD19.2 billion in 2016. Performance was driven by higher issuances from the public sector jumping to USD31.9 billion from USD3.7 billion, of which Saudi Arabia’s market share stood at 77% (or USD24.6 billion)

USD36.5b

USD14.9b

USD46.9b

USD7.3b

0,00

10,00

20,00

30,00

40,00

50,00

Malaysia Indonesia GCC Other countries

2015 2016 2017

Source: Eikon-Thomson Reuters, Bloomberg, Bank of Indonesia, Capital Markets Board of Turkey

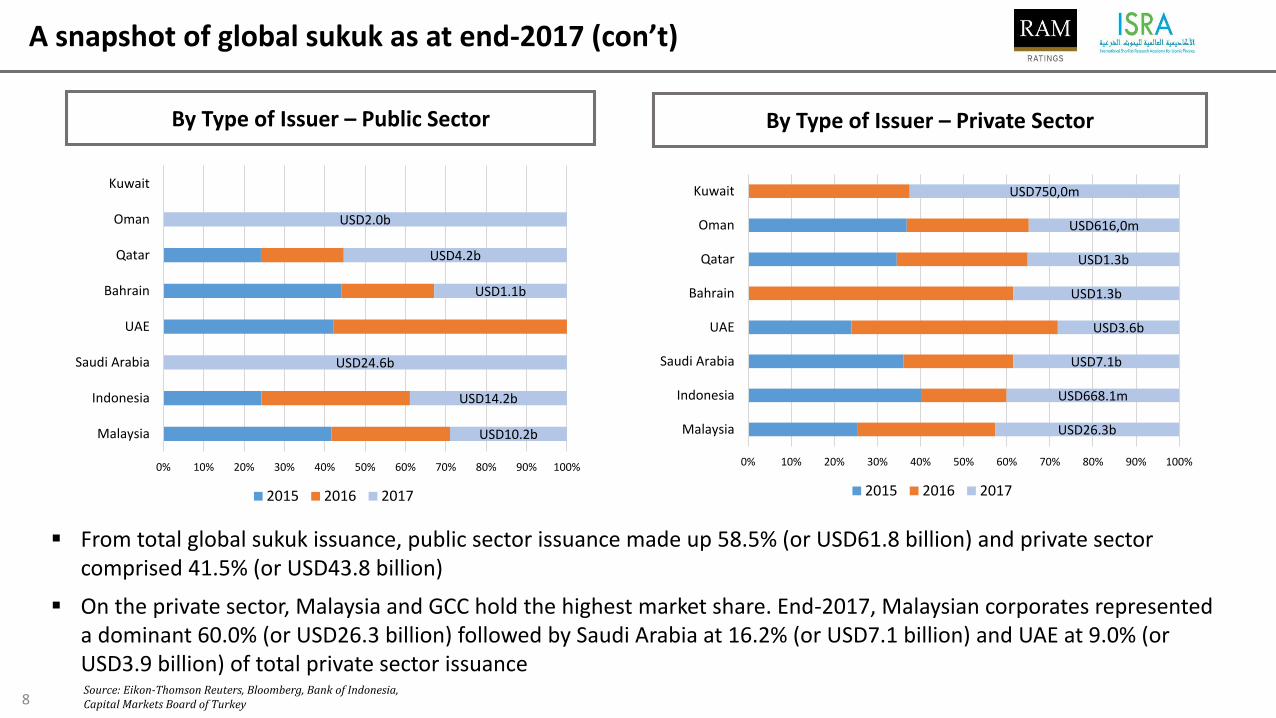

A snapshot of global sukuk as at end-2017 (con’t)

8

From total global sukuk issuance, public sector issuance made up 58.5% (or USD61.8 billion) and private sector comprised 41.5% (or USD43.8 billion)

On the private sector, Malaysia and GCC hold the highest market share. End-2017, Malaysian corporates represented a dominant 60.0% (or USD26.3 billion) followed by Saudi Arabia at 16.2% (or USD7.1 billion) and UAE at 9.0% (or USD3.9 billion) of total private sector issuanceSource: Eikon-Thomson Reuters, Bloomberg, Bank of Indonesia, Capital Markets Board of Turkey

By Type of Issuer – Public Sector

USD10.2b

USD14.2b

USD24.6b

USD1.1b

USD4.2b

USD2.0b

Malaysia

Indonesia

Saudi Arabia

UAE

Bahrain

Qatar

Oman

Kuwait

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2015 2016 2017

By Type of Issuer – Private Sector

USD26.3b

USD668.1m

USD7.1b

USD3.6b

USD1.3b

USD1.3b

USD616,0m

USD750,0m

Malaysia

Indonesia

Saudi Arabia

UAE

Bahrain

Qatar

Oman

Kuwait

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2015 2016 2017

Key domestic stakeholders in developing a sukuk market

9

Stimulate activity and product development in both the sell and

buy sides

SERVICE PROVIDERS

SIX KEY DOMESTIC MARKET STAKEHOLDERS

Attract foreign investors and strengthen the liquidity structure

REGULATORS

Generate investor confidence

EXCHANGES

Facilitate issuance of infrastructure-based sukuk

with long tenures

NBFIs

Promote the efficient use of domestic wealth through financial intermediaries

GOVERNMENT

Promote value creation through capital-market activities

FINANCIAL INSTITUTIONS

A SUSTAINABLE

SUKUK MARKET

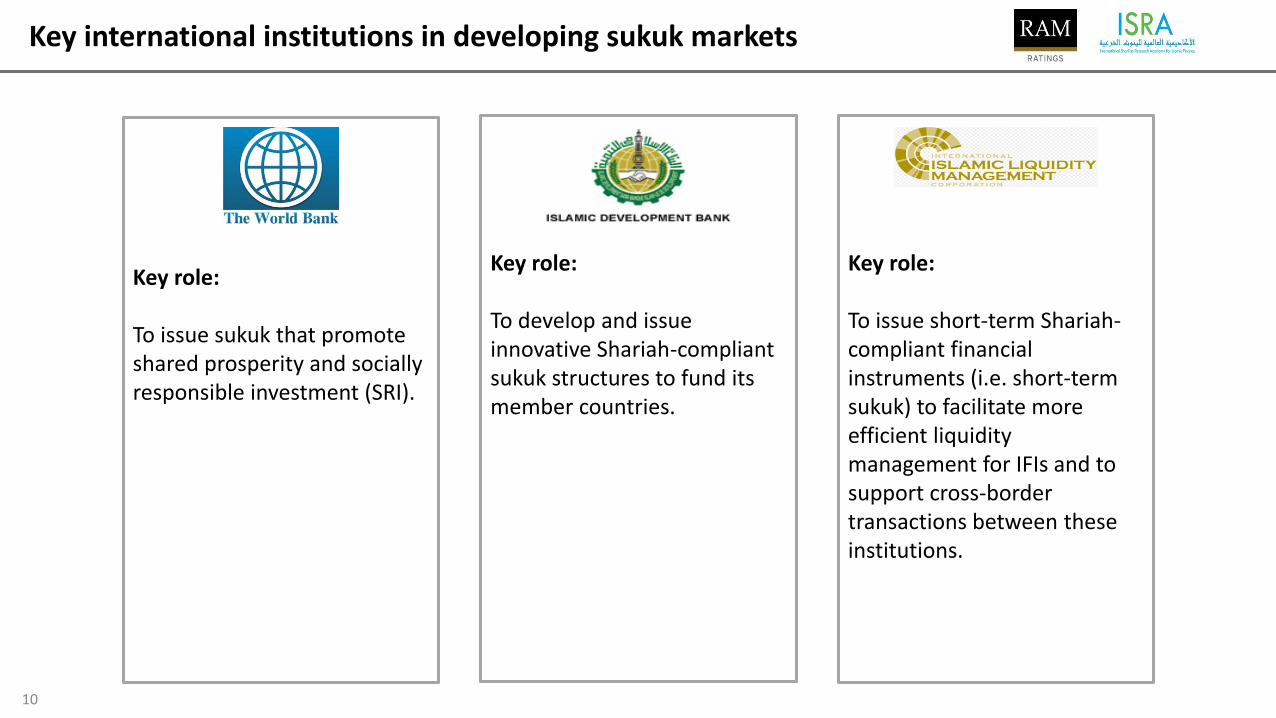

Key international institutions in developing sukuk markets

10

Key role:

To issue short-term Shariah-compliant financial instruments (i.e. short-term sukuk) to facilitate more efficient liquidity management for IFIs and to support cross-border transactions between these institutions.

Key role:

To develop and issue innovative Shariah-compliant sukuk structures to fund its member countries.

Key role:

To issue sukuk that promote shared prosperity and socially responsible investment (SRI).

Capital Markets

Government bonds Corporate and financial

institution bonds

Equity Securitised products

1 Foundational policies

Benchmarkassets

Supply of capital

Demand for capital

Intermediation Free markets Price discovery

2

Regulatory framework

3

Cornerstoneinstitutions

4

Regulations and standards

5

Taxation

6

Market infrastructure and technology

Regulatory bodies and their architecture

Governance and ownership

Institutional setup

Transparent regulations

Predictable enforcement

Tax policies

Tax incentives

Market infrastructure

Technology

Po

licym

akin

gM

arke

t ar

chit

ect

ure

an

d d

esi

gn

Basic Pillars of a Domestic Capital Market

11

McKinsey’s building blocks…

Source: McKinsey & Company (2017)

Critical success factors for establishing a sustainable sukuk market

12

4. Sustainable supply of private sector:

The best yardstick in tracking the pulse of a local sukuk market is the performance of the private sector (i.e.quasi-government and corporate issuance)

1. Cohesive collaboration with key market stakeholders:

A specific roadmap for the inclusion of ICM, interlinking sukuk as a core component is key to guide andmeasure the effectiveness of participation level

2. Vibrant ecosystem:

Amalgamation of a strong legal and regulatory regime, coupled with a conducive tax environment androbust market infrastructure and technology

3. Intermediation of domestic financial resources:

Effective mobilisation of domestic financial resources through cornerstone institutional investors such aspension funds, insurance/takaful companies, etc.

5. Shariah governance framework:

Harmonistion of Shariah principles and interpretations adds clarity to product development, builds marketconfidence and creates awareness of the benefits of Islamic finance

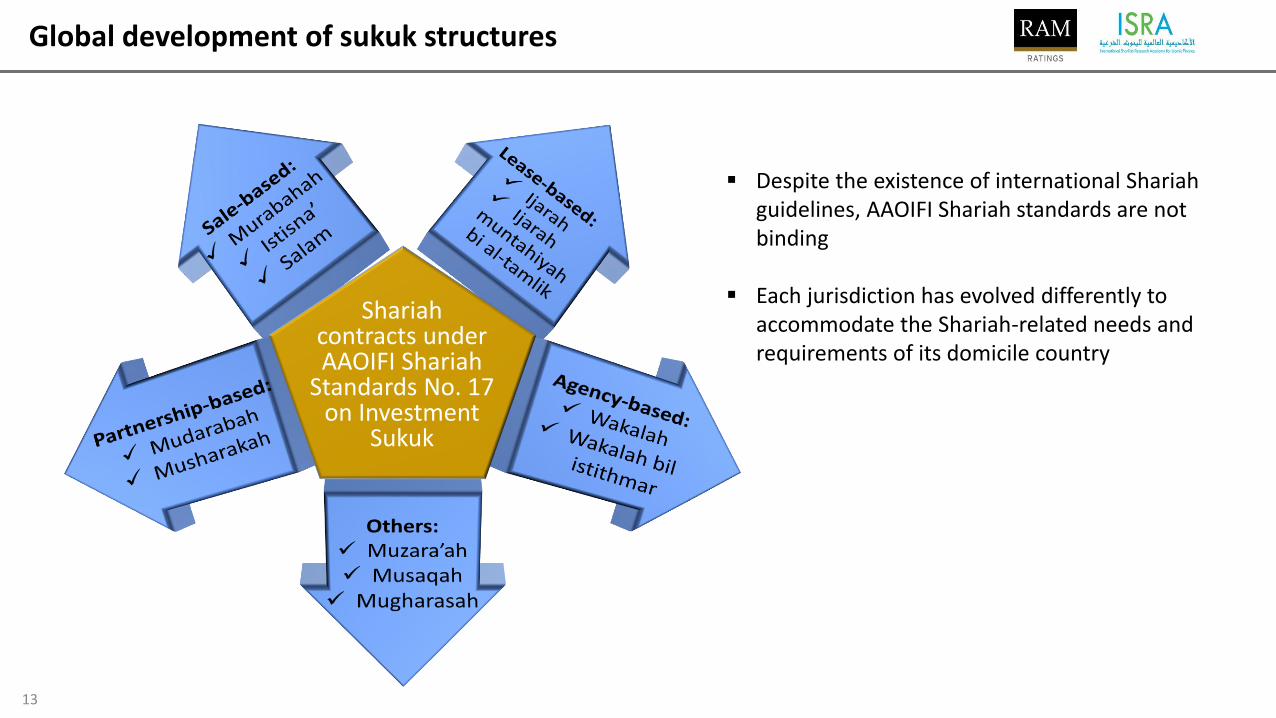

Global development of sukuk structures

13

Shariah contracts under AAOIFI Shariah

Standards No. 17 on Investment

Sukuk

Despite the existence of international Shariah guidelines, AAOIFI Shariah standards are not binding

Each jurisdiction has evolved differently to accommodate the Shariah-related needs and requirements of its domicile country

Global development of sukuk structures (con’t)

14

0%

20%

40%

60%

80%

100%

United Arab Emirates Saudi Arabia Qatar Oman Bahrain *Jordan

Types of Shariah contracts for sovereign issuances by selected Arab countries (2011 - June 2017)

Wakalah bil istithmarIjarahMurabahahSalamHybridOthers

“Ijarah-based sukuk constitute a large portion of sovereign issuances in most jurisdictions”

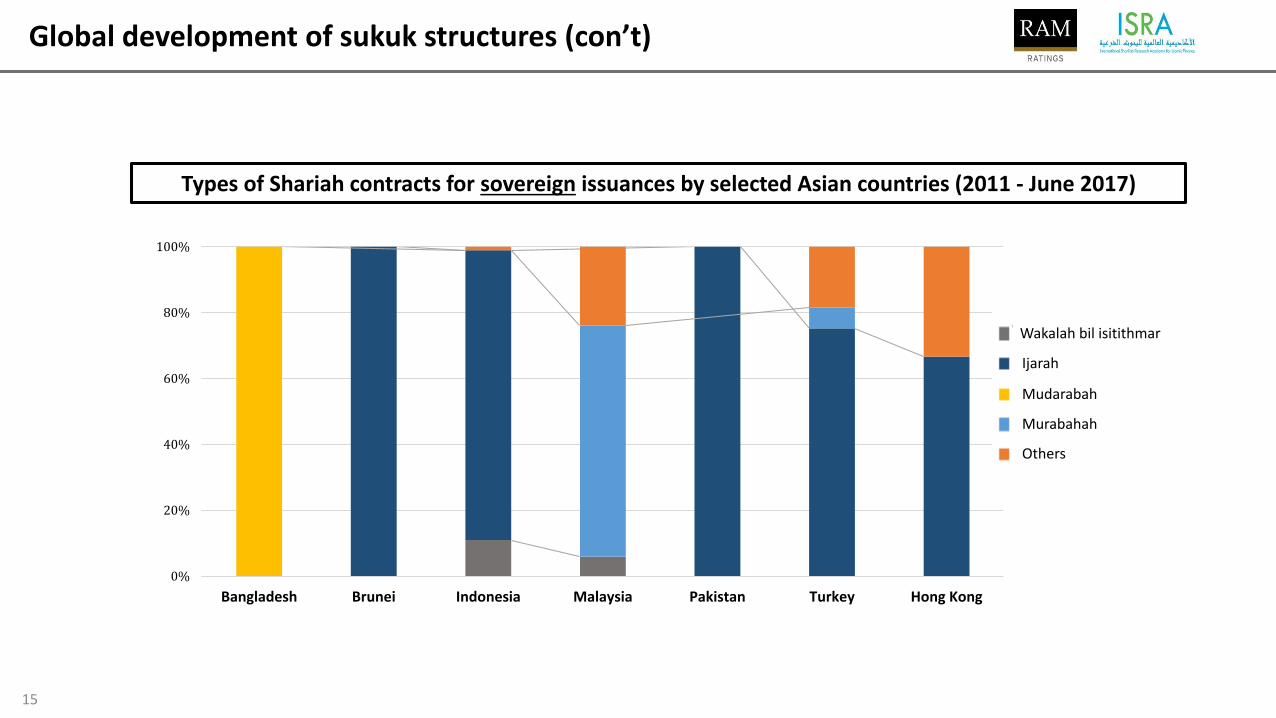

Global development of sukuk structures (con’t)

15

Types of Shariah contracts for sovereign issuances by selected Asian countries (2011 - June 2017)

0%

20%

40%

60%

80%

100%

Bangladesh Brunei Indonesia Malaysia Pakistan Turkey Hong Kong

Ijarah

Wakalah bil isitithmar

Mudarabah

Murabahah

Others

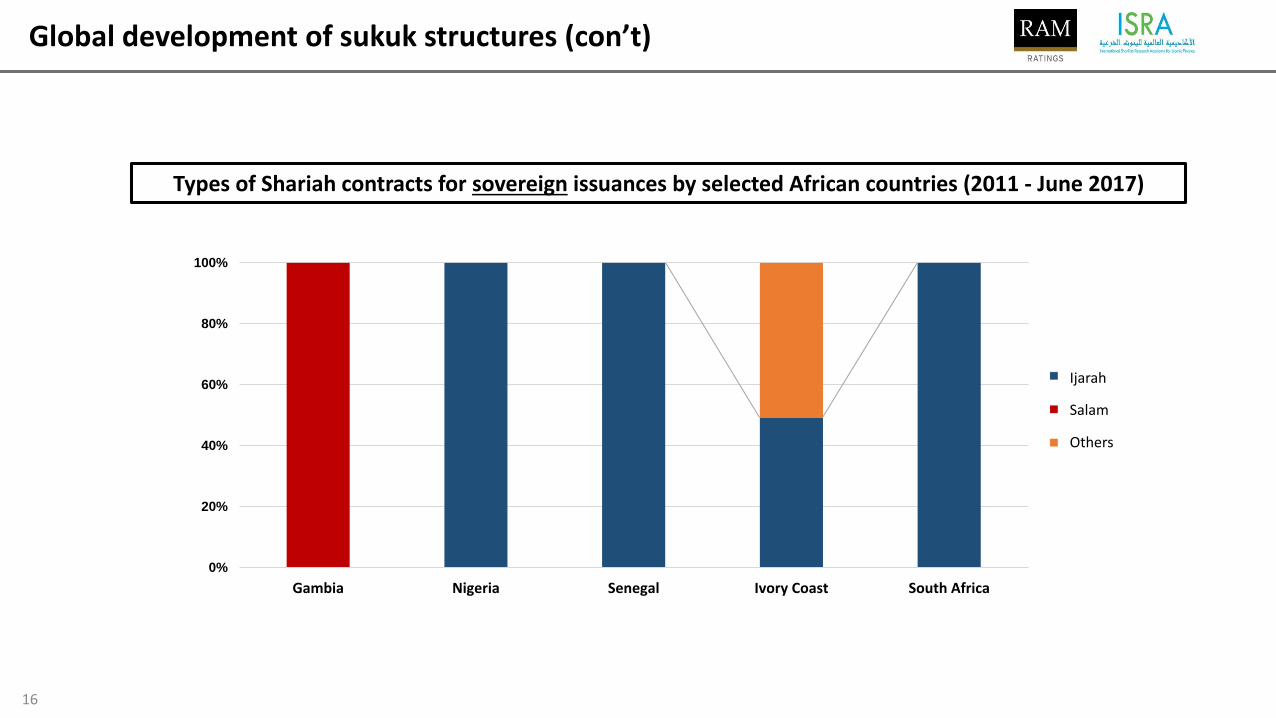

Global development of sukuk structures (con’t)

16

Types of Shariah contracts for sovereign issuances by selected African countries (2011 - June 2017)

0%

20%

40%

60%

80%

100%

Gambia Nigeria Senegal Ivory Coast South Africa

Salam

Others

Ijarah

Global development of sukuk structures (con’t)

17

Types of Shariah contracts for quasi-government and corporate issuances by selected Arab countries (2011 - June 2017)

0%

20%

40%

60%

80%

100%

United Arab Emirates Saudi Arabia Kuwait Qatar Oman Bahrain *Jordan

Wakalah bil istithmar

IjarahMudarabahMurabahahMusharakahHybridOthers

“Requirement of having to secure available unencumbered assets has pushed the commercial decision by governments and corporates to adopt wakalah contracts”

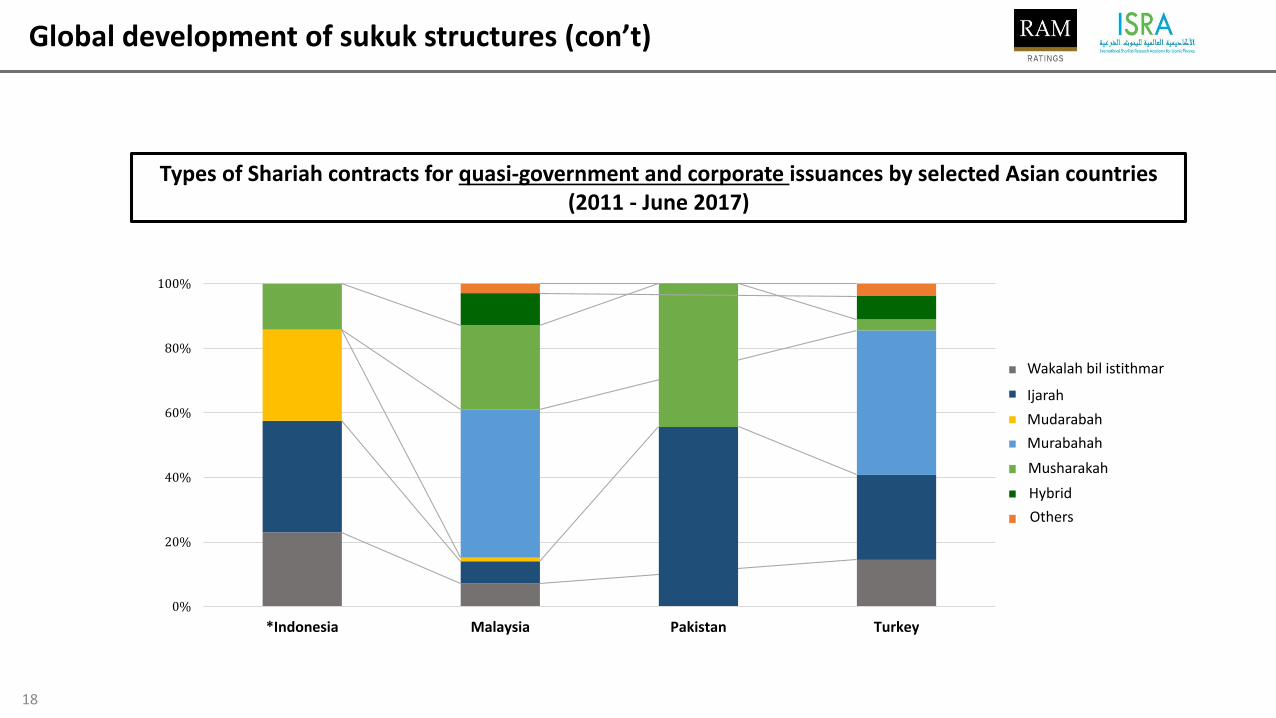

Global development of sukuk structures (con’t)

18

Types of Shariah contracts for quasi-government and corporate issuances by selected Asian countries (2011 - June 2017)

0%

20%

40%

60%

80%

100%

*Indonesia Malaysia Pakistan Turkey

Wakalah bil istithmar

Ijarah

Mudarabah

Murabahah

Musharakah

Hybrid

Others

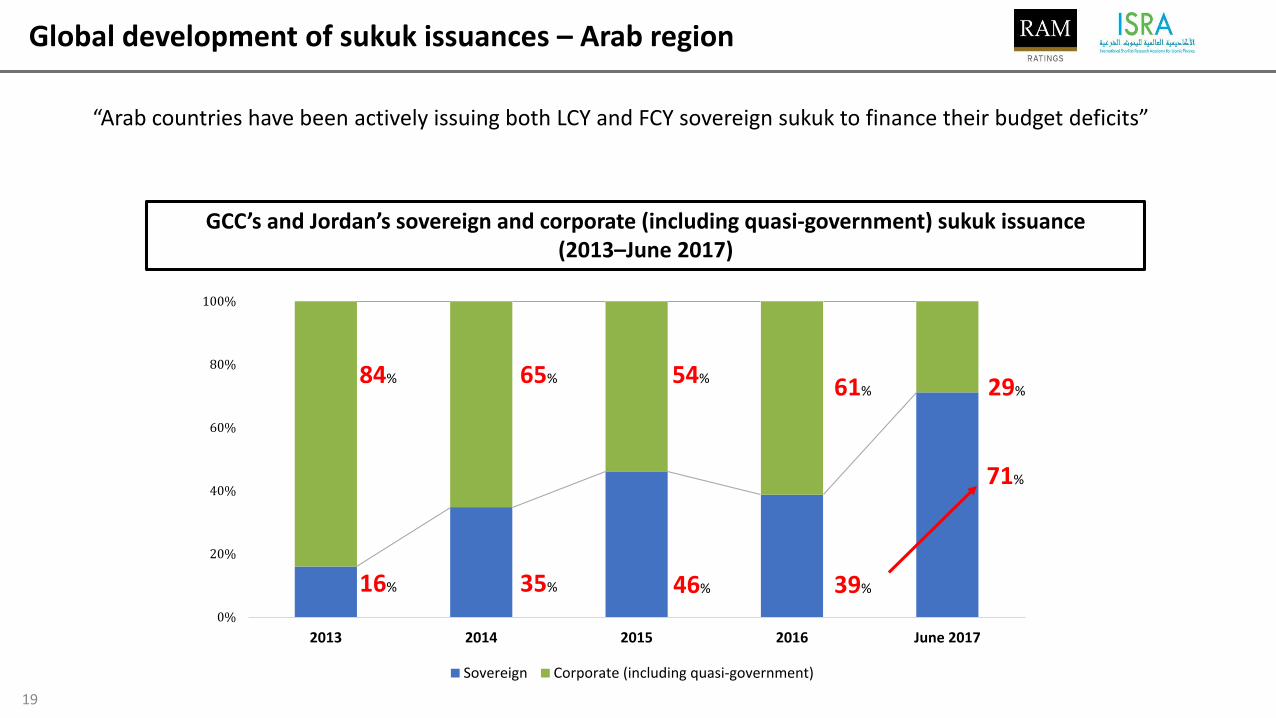

Global development of sukuk issuances – Arab region

19

GCC’s and Jordan’s sovereign and corporate (including quasi-government) sukuk issuance (2013–June 2017)

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 June 2017

Sovereign Corporate (including quasi-government)

16%

84% 65%

35%

54%

46% 39%

61%

71%

29%

“Arab countries have been actively issuing both LCY and FCY sovereign sukuk to finance their budget deficits”

Global development of sukuk issuances – Arab region (con’t)

20

Water and Sanitation

Transport

Information and Communications

Technology

5%

Electricity

9%

43%

43%

Annual funding gap of USD60.0 billion

Investment Requirements

Current Spending

USD40.0 billion

USD100.0 billion

Infrastructure financing gaps Priority sectors for the next 5 years

Arab countries’ infrastructure spending

“In developing Arab countries’ sukuk markets, consideration should be given to the large infrastructure funding gap that has historically been funded by governments and commercial banks”

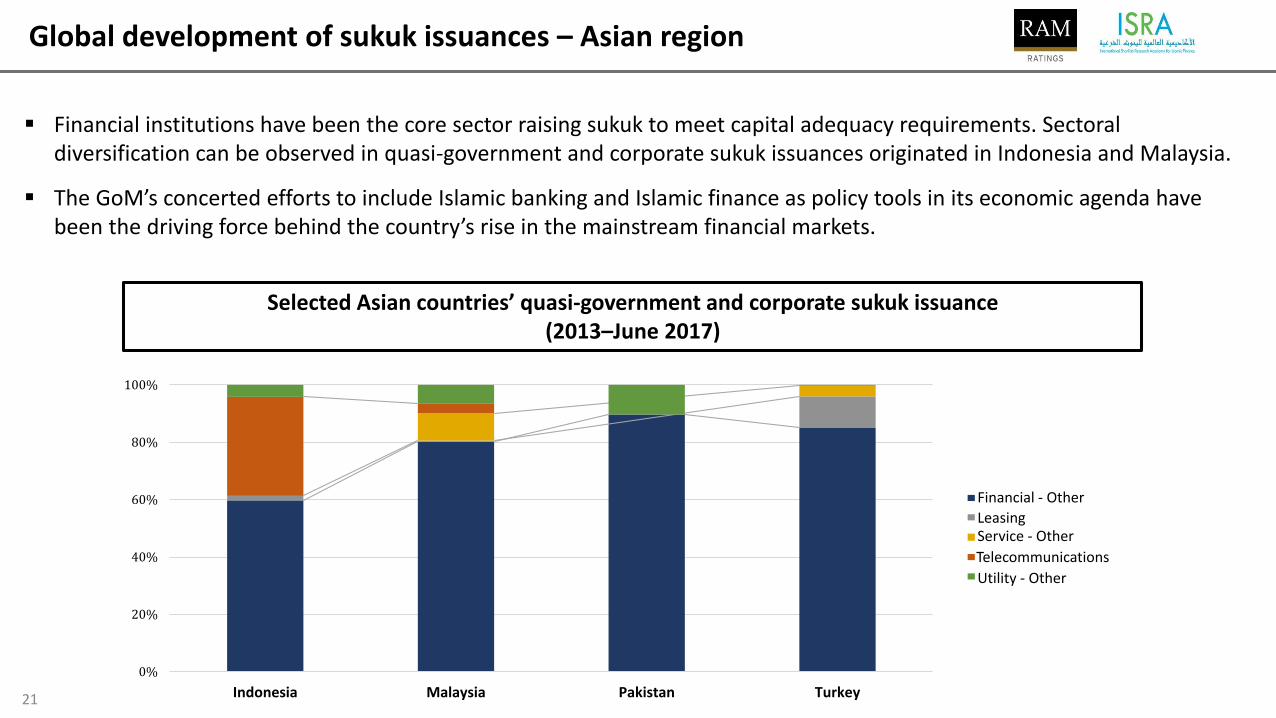

Global development of sukuk issuances – Asian region

21

Financial institutions have been the core sector raising sukuk to meet capital adequacy requirements. Sectoral diversification can be observed in quasi-government and corporate sukuk issuances originated in Indonesia and Malaysia.

The GoM’s concerted efforts to include Islamic banking and Islamic finance as policy tools in its economic agenda have been the driving force behind the country’s rise in the mainstream financial markets.

0%

20%

40%

60%

80%

100%

Indonesia Malaysia Pakistan Turkey

LeasingService - Other

Telecommunications

Utility - Other

Financial - Other

Selected Asian countries’ quasi-government and corporate sukuk issuance (2013–June 2017)

Global development of sukuk investment – Arab region

22

A snapshot of selected GCC’s credit investors profile

“Investors in GCC’s recent bond issuances (including sukuk) shows a high reliance on foreign investors”

Masjid Al Futtaim Perp

Qatar Reinsurance Perp

Dubai Islamic Bank Sukuk 5Y

Gulf International Bank 5Y

Ahli Bank Qatar 5Y

NBAD Green bond 5Y

Inv. Corp of Dubai Sukuk 10Y

Oman 30Y

Oman 10Y

Oman 5Y

Kuwait 10Y

Kuwait 5Y

KIPCO 10Y

Equate Petro Sukuk 7Y

Country NBFIs assets as %

to GDP

Pension fund assets

as % to GDP

Bahrain 31.5% (2014) 20.5% (2006)

Kuwait 2.44% (2014) n/a

Oman n/a n/a

Qatar n/a n/a

Saudi Arabia 14.4% (2014) 26.0% (2016)

UAE n/a 2.7% (2007)

Financial Intermediation by NBFIs as a Percentage of GDP (Arab)

Global development of sukuk investment – Asian region

23

McKinsey Asian Capital Markets Development Index

“Hong Kong and Malaysia have undergone healthy developments in terms of the composition of their financial markets. Indonesia is still attempting to establish a higher ratio of its outstanding bond market against its GDP. ”

Financial Intermediation by NBFIs as a Percentage of GDP (Asian)

CountryFunding at scale1

Investment opportunities2

Pricing efficiencies3 Total score (out of 5)

1 Weight allocated: 50% while arriving at total score

2 Weight allocated: 40% while arriving at total score

3 Weight allocated: 10% while arriving at total score

Very deep

Deep Moderate Shallow Very Shallow

Country NBFIs assets as %

to GDP

Pension fund assets

as % to GDP

Hong Kong n/a 37.4% (2014)

Indonesia 3.3% (2014) 1.69% (2011)

Malaysia n/a 57.9% (2014)

Pakistan n/a 0.02% (2012)

Global development of sukuk investment – African region

24

Based on the composite mix of investors, Africa’s debt securities are mainly held by foreign holders.

Although African governments have implemented measures to heighten the development of NBFIs, challenges such as financial inclusion and a low savings rate have been hampering progress.

Country NBFIs assets as % to GDP Pension fund assets as % to GDP

The Gambia n/a n/a

Nigeria n/a 4.4% (2012)

Senegal n/a n/a

Ivory Coast n/a n/a

South Africa 120.3% (2014) 40.8% (2014)

Sudan n/a n/a

Financial Intermediation by NBFIs as a Percentage of GDP (African)

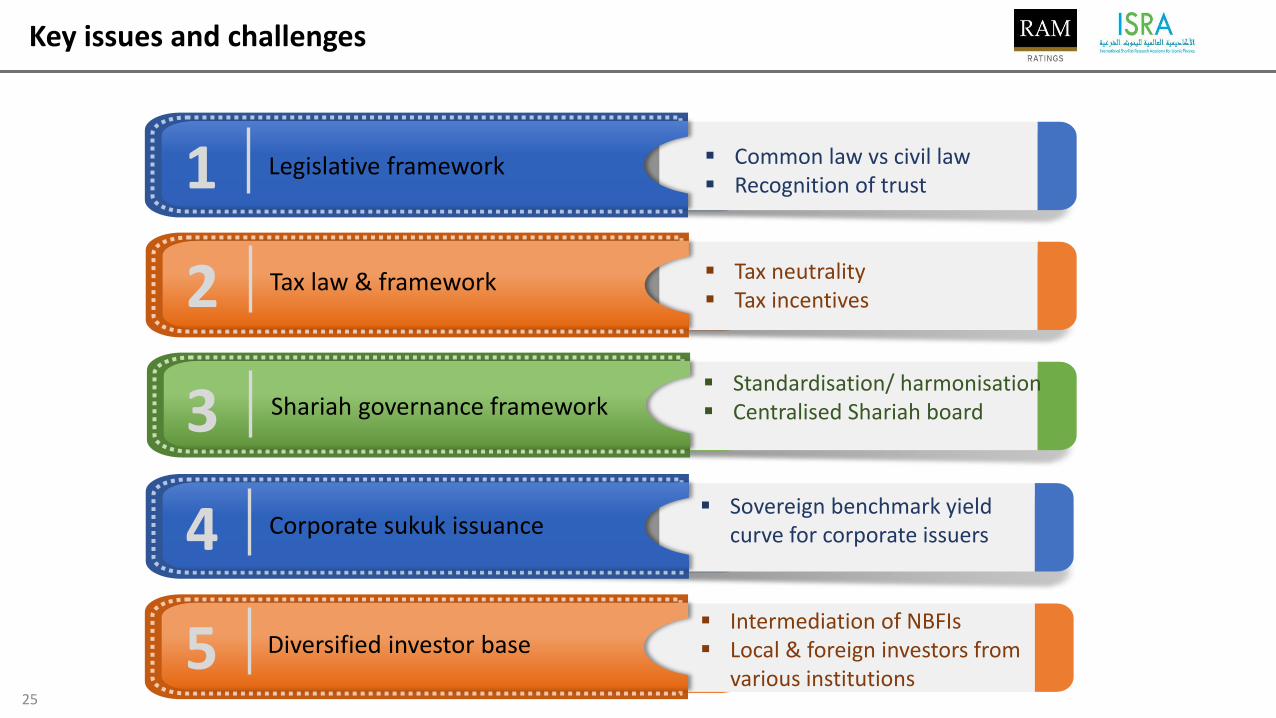

Key issues and challenges

25

Common law vs civil law Recognition of trust1 Legislative framework

Tax neutrality Tax incentives2 Tax law & framework

Standardisation/ harmonisation Centralised Shariah board 3 Shariah governance framework

Sovereign benchmark yield curve for corporate issuers4 Corporate sukuk issuance

Intermediation of NBFIs Local & foreign investors from

various institutions5 Diversified investor base

Thank you

Lorong Universiti A, 59100 Kuala Lumpur, Malaysia

Tel: +603-7651 4200Fax: +603-7651 4242ISRA: www.isra.my

I-FIKR: www.ifikr.isra.my

Suite 20.01, Level 20, The Gardens South Tower, Mid Valley City,

Lingkaran Syed Putra, 59200 Kuala Lumpur, Malaysia

Tel: +603-7628 1010Fax: +603-7620 8251

www.ram.com.my