the secret truth about annuities guide

TRANSCRIPT

FIRST AMERICAN ADVISORS, INC.

Creators of AnnuityEducator.com

The Secret Truth about Annuities

Y O U R F R E E R E S O U R C E G U I D E F R O M A N N U I T Y E D U C A T O R . C O M

The Secret Truth about Annuities

First American Advisors, Inc. 18881 Von Karman Ave • Suite 1470

Irvine, CA 92612 Phone 949.398.2200 • Fax 949.679.0200

TABLE OF CONTENTS

Part 1

Questions .......................................................................................................... 2

The Income Guarantee ................................................................................... 2

Do I Fit the Annuity Criteria? ........................................................................ 3

Clearing up the Confusion .............................................................................. 3

The Facts ........................................................................................................... 4

The Rate Hype .................................................................................................. 5

Negative Opinions ........................................................................................... 6

Keep the Gains, Never the Losses ................................................................ 7

Using IRA / 401(k) Money for Annuities .................................................... 9

Are there “Hidden Fees”? ............................................................................. 10

Will my Money be Liquid? ............................................................................ 11

Who Keeps my Money when I Die? ........................................................... 11

What’s the “Bonus” Catch? .......................................................................... 13

How Surrender Charges Work? ................................................................... 14

Part 2

What you’ll Learn in Part 2 ........................................................................... 17

The Problem with Retirement Income ....................................................... 17

3 Methods to Solve the Income Problem ................................................... 18

The Solution to the Income Puzzle ............................................................. 21

Part 3

Do-It-Yourself Pension using an Annuity .................................................. 24

The Next Steps ............................................................................................... 27

A Note from the Author ............................................................................... 29

Index ................................................................................................................ 30

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 1

Introduction

Is what you currently know about “Hybrid Annuities” really the truth?

aybe some of you have previously owned an indexed annuity with an income rider (Hybrid Annuity) and you’re thinking, “of course I know the truth”. But it’s possible that most of

what you think you know about them is wrong.

“Hybrid Annuities” can be a perfect fit for some people and maybe less beneficial for others. After reading this guide you will know whether or not it is for you.

So, what brought you here, about to read this guide on Hybrid Annuities? Maybe you went to a dinner seminar and the speaker was talking about Hybrid Annuities. Or maybe you saw an ad on the internet for “8% Annuity Secret” or something like that. Or maybe you asked for some “Free Information” from a website and now you have an overly aggressive agent calling and

emailing you, trying to pressure you into buying an indexed annuity with an income rider. However you got here, you most likely have some questions or concerns about Hybrid Annuities.

There is a real lack of unbiased information out there on indexed annuities. It seems like it’s either over hyped sales pitches from insurance agents or, Wall Street people bashing the heck out of them.

Part

1

M

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 2

As with most things, the truth is somewhere in the middle. Hopefully this guide will clear the air on some of the confusion.

Questions

Let’s talk about some of the questions you might be asking yourself:

Is an annuity right for me?

What if I make a costly mistake?

Where can I get help to understand how annuities work?

Who can give me some unbiased, factual, honest information so

I can decide for myself?

Well I’ve got a simple question for you instead, that will really get to the heart of the matter. “Would you like to turn a portion of your savings into a guaranteed income for life when you retire?” If you answered “no” then an annuity is not for you. If you answered “yes”, or “I think so”, or “maybe”, then keep reading and you will find the answers to the questions you’re asking yourself.

The Income Guarantee

The #1 reason to put some money into an indexed annuity with an income rider (Hybrid Annuity) is the guaranteed income you will get at some point in the future. This helps people stop worrying about depleting their IRA or 401(k) balance too soon or running out of money.

If you don’t need or don’t want some level of guaranteed income from your IRA/401(k) or other savings at some point in the future, then you should not put one single penny into an index annuity with an income rider. An index

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 3

annuity by itself may be ok, but why pay for an income rider if you don’t need income? Buy a Hybrid Annuity based on what it will do for

you, not what it might do.

Do I Fit the Annuity Criteria?

Let’s look at the ideal person that a Hybrid Annuity might be a fit for.

1. You are between the ages of 40 and 70.

2. You have between $250,000 and $3,000,000 of investable assets.

3. Ideally you are still working (or just recently retired).

4. You will not be getting a huge pension when you retire.

5. You will need income from IRA/401(k) to supplement Social

Security .

If this describes you, and you want to see if one of these Hybrid Annuities could fit in your overall investment portfolio, I promise that this guide will help to point you in the right direction.

Clearing up the Confusion

So first let’s talk about the term “Hybrid Annuity”. The term Hybrid Annuity means exactly this:

“An Indexed Annuity with an optional Income Rider”.

They mean exactly the same thing. “Hybrid Annuity” is simply a hyped-up marketing term. It’s not an actual product and in fact the insurance company compliance departments usually don’t like the term Hybrid Annuity.

Note

The definition of the word “hybrid”; of mixed character or, composed of mixed parts.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 4

So put simply, here are the 3 “mixed parts” which composes a Hybrid Annuity:

1. Immediate Annuity (an annuity that pays you income immediately)

2. Fixed Rate Annuity (an annuity that pays you a fixed rate of return like a Bank CD)

3. Index Annuity (an annuity that links your interest to a stock market index)

The Insurance companies developed and combined these products a few years ago because retirees like you were looking for these top 3 types of annuity products:

1. An annuity that guarantees income for life but allows you to maintain control of your money in case your needs change.

2. An annuity that allows the chance to earn more than the bank with no risk to your principle.

3. An annuity that distributes an exact income amount every year for life.

Hence the term “Hybrid” ….

The Facts

So setting aside the confusion, here are the facts about what a Hybrid Annuity is:

It’s an indexed annuity with an optional income rider.

Your actual annuity value earns interest by being linked to a market index.

Your Income Account grows independently of your actual annuity value (growth rate varies).

At some point in the future you can turn on your guaranteed lifetime income.

The longer you wait the more guaranteed income you get.

The income is guaranteed for life.

You maintain control. You can start and stop the income if you need to.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 5

The Rate Hype

Have you ever seen this ad on Google search? “8% Annuity Secret” or “Earn 8% Guaranteed For Life” This ad suggests that you are going to earn 8% on your money, safe and guaranteed. But that’s not the truth because there is more to it than that. Don’t be misled by these ads and these agents! I will tell you the truth about what this 8% number really is.

First, what it’s not. This 8% growth is not the growth rate on your lump sum amount. It is never an amount that you can walk away with. You are not earning 8% guaranteed on your actual annuity value. So what is the 8% then? It’s called the Roll-up Rate and it only applies to the Income Account Value.

A basic index annuity has an “Annuity Account Value”. This is your lump sum amount and the amount that is linked to a market index. When you add an income rider onto an index annuity you get

what’s called an “Income Account Value.” So there are two different terms here: 1) Annuity Account Value 2) Income Account Value The 8% refers to the growth rate of the Income Account Value that is used to calculate your income at some point in the future. Income Accounts work kind of like Social Security. The longer you wait, the more the income you get in the future. There is no lump sum on Social Security. Similarly, there is no lump sum of your Income Account Value.

Note: Different

companies may

have different

names for this.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 6

So when you see ads or have someone telling you, “You will earn 8% guaranteed”, now you understand that it applies to the growth of the income account value only.

That doesn’t make it good or bad, it just is what it is, and you need to know what you are buying, before you buy it having the wrong expectations.

Negative Opinions

Have you ever seen this headline ad from a Wall Street or Mutual Fund money manager? “I Hate Annuities and You Should Too” Which is interesting if you read one of these reports because one of the first sentences is something like: “One of the biggest risks an investor faces is running out of money in retirement.” The common theme on the anti-annuity websites and anti-annuity advertising seems to be:

You can make more in the stock market

Annuities are not 100% liquid all the time without penalty

Some annuities have high fees

But here’s what they don’t say!

They don’t tell you that all your annuity money grows from interest credited from the growth of a stock index like the S&P 500 without a dime of your savings actually being in the market. You only keep the gains, never the losses. There are also stock brokers and financial planners standing in the way of annuities. Once money goes into an annuity they can’t earn commissions from trading it anymore and may not be able to charge fees for managing it. Financial advisers have a charming term for this phenomenon ~ annuicide. You insure, and their revenue dies. So, many of them will try and talk you out of it.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 7

So the word is only slowly getting out to consumers that they do have another choice. Safe growth that gives back without the added risk of loss in the stock market. It’s called a fixed-indexed annuity, or “Hybrid Annuity”.

Keep the Gains, Never the Losses

Indexed annuities should not be presented as, or thought of as a direct substitute for stock market or mutual fund investments. Index annuities are a savings vehicle designed to compete with other fixed accounts like bank CDs. You don’t lose value

in a “bad” year and you capture some growth in a “good” year.

Let’s look at the example graph below.

This is a screen shot from an annuity brochure. Copies and complete details are available upon request.

Indexed interest accounts give you the potential to receive higher interest than might be the case with traditional fixed rate annuities but without subjecting your retirement savings to market risk. Indexed interest is credited annually based in part, by indexes such as the S&P 500 or the Dow Jones Industrial Average. The S&P 500 Index contains stocks from 500 various industry leaders and is widely regarded as the premier benchmark for the U.S. stock market performance. The Dow Jones Industrial Average is the oldest continuing stock market index in the world. Many of the stocks represented in the DJIA are leaders in their industries. Some insurance

Sound too good to

be true? That

would be the

perfect

investment!

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 8

companies use other indexes but the S&P 500 & the DJIA are the most common. But there are limits you should know about:

1. Caps: Means there is an upper ceiling on how much you can earn 2. Participation Rate: Means you get a percentage of the market

gains

3. Spread: A percentage the Insurance company retains if the market is positive

This isn’t good or bad. Again, it just is what it is. Indexed annuities are designed to be the “middle ground” between low rate bank products and having to put your money at risk in the market. Let me break them down for you:

CAPS - So let’s say you have an annuity with an annual cap of 5%. And the stock market index goes up 30% this year. You will make 5% because that’s your cap, even though the market was up 30%. Making 5% is pretty good compared to what the bank is paying right now. Plus you automatically lock that gain in so you won’t lose it if the market goes down the next year. But is making 5% when the market is up 30% really “Stock Market Gains Without The Risk?” You decide.

Another thing to watch for is Exaggerated Monthly Caps. There are annuities that have a monthly cap instead of an annual cap. For example let’s say the monthly cap is 2%. Many agents will say to you. “So your upside in a good year is 24%. 2% X 12 months = 24%.

While technically true, it is very unlikely and if you go into an indexed annuity expecting double digit returns every year you will be disappointed.

PARTICIPATION RATE: Participation rate is the stated percentage of any index increase credited to an annuity contract. Participation rates are also subject to change, declared annually and are guaranteed not to fall below a minimum. Most common is 100%

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 9

participation which means that if the S&P 500 goes up 5% that 100% of the growth is credited to your policy subject only to a cap. SPREAD: A spread is a percentage that the insurance company retains if the market is positive. The participation in the market index growth can be up to 100%. There are no caps. The upside growth to the policyholder is only limited by the spread or in some instances a combination of participation and spread. In summary, the most honest marketing statement to your potential gains with indexed annuities would be something like …

“You link your interest to a market index, and over time you have a pretty good shot of beating what the bank or other fixed accounts are paying, all while keeping

your money safe.”

Using IRA / 401(k) Money for Annuities

There are many “experts” out there who are very smart and they manage millions of dollars for other investors. Sometimes these “experts” will advise investors not to use IRA/401(k) money for an annuity “because it’s already tax deferred.” That may be obvious and sound advice for some investors, but not-so-smart advice for others! Before listening to that generic advice, ask yourself these questions: Obviously tax deferral would not be the smartest idea if I’m

putting my IRA into an annuity because the IRA is already tax deferred. BUT, how about if I want to make sure I will get guaranteed income without any market risk? Would that be a

good enough reason?

Or, how about if my biggest fear is losing money again and I want an option that will give me the chance to earn more than the bank without putting my money at risk? Would that be a

good enough reason?

The truth is: There are reasons why people use their IRA or

401(k) money to purchase a Hybrid Annuity. And it’s not because

of the tax deferral.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 10

Now, with all of that being said … If you have non-IRA/401(k) money (also known as non-qualified money) then yes, maybe the benefits of tax deferral would influence your decision. But with IRA and 401(k) type money, it’s the safety, the guarantees, and the income that would be the great reasons to do it, not tax-deferral. You be the judge!

Are there “Hidden Fees”?

Here are the facts:

Some annuities have very high fees

Some annuities have no fees at all

Some annuities only have fees only if you

choose an optional rider

Saying all annuities have high fees is like saying all sandwiches have roast beef on them. In reality, some sandwiches do and some don’t. So don’t make the mistake of lumping them all together to make an incorrect blanket statement. Here is a general breakdown:

Variable Annuities – Always has several fees

Immediate Annuities -- No fees

Fixed Rate Annuities -- No fees

Indexed Annuities -- Typically no fees for just the annuity.

You can add on income or death benefit riders for a fee.

So 9 times out of 10 when someone says annuities have high fees they are talking about Variable Annuities. Variable Annuities are Wall Street products. Some of the fees associated with Variable Annuities are:

1. Mortality and Expense Charge 2. Surrender Charge 3. Investment Management Fees 4. Rider Fees 5. Flat Contract Fees

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 11

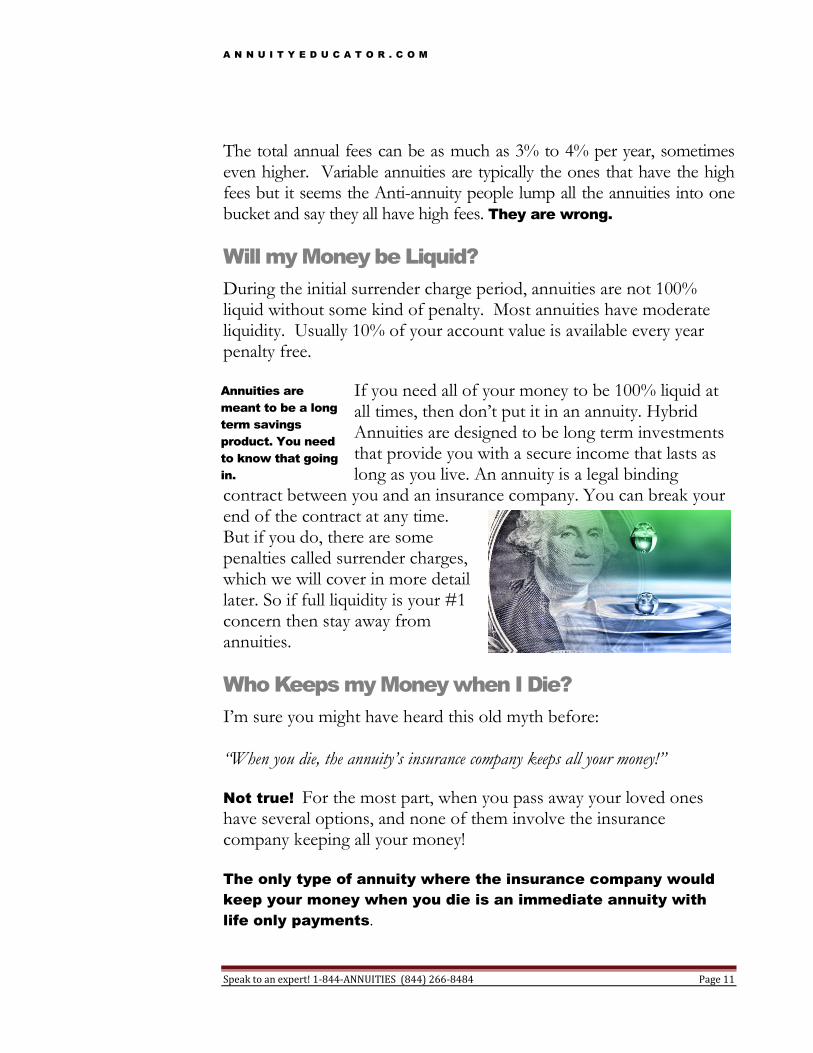

The total annual fees can be as much as 3% to 4% per year, sometimes even higher. Variable annuities are typically the ones that have the high fees but it seems the Anti-annuity people lump all the annuities into one bucket and say they all have high fees. They are wrong.

Will my Money be Liquid?

During the initial surrender charge period, annuities are not 100% liquid without some kind of penalty. Most annuities have moderate liquidity. Usually 10% of your account value is available every year penalty free.

If you need all of your money to be 100% liquid at all times, then don’t put it in an annuity. Hybrid Annuities are designed to be long term investments that provide you with a secure income that lasts as long as you live. An annuity is a legal binding

contract between you and an insurance company. You can break your end of the contract at any time. But if you do, there are some penalties called surrender charges, which we will cover in more detail later. So if full liquidity is your #1 concern then stay away from annuities.

Who Keeps my Money when I Die?

I’m sure you might have heard this old myth before: “When you die, the annuity’s insurance company keeps all your money!”

Not true! For the most part, when you pass away your loved ones have several options, and none of them involve the insurance company keeping all your money!

The only type of annuity where the insurance company would

keep your money when you die is an immediate annuity with

life only payments.

Annuities are

meant to be a long

term savings

product. You need

to know that going

in.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 12

Otherwise, here are your options:

1. Your spouse can continue the contract if you die provided he/she is listed as the primary beneficiary.

2. Your beneficiaries can opt to take a full lump sum payout of the remaining accumulation value (Death Benefit).

3. Your beneficiaries can opt to receive the death benefit (accumulation value) in a series of payments over a few years.

4. Some Hybrid Annuities allow your beneficiaries to take the Income Account Value over a period of 5 years or longer. This might make sense if the Income Account Value is much higher that your actual annuity value.

The guaranteed monthly payout on the immediate annuity is used to fund life insurance. The life insurance is guaranteed not to lapse if you make the premium payment.

A 65 year old male non-smoker is in good health. He's rated standard but not quite preferred because he's had some health issues in the past. He wants to transfer $1,000,000 at death to his children tax-free. To do this he purchases a $1,000,000

universal life insurance policy with a no lapse guarantee. The premium is level and is guaranteed not to go up and the policy will not lapse if the premium is paid. The cost for this policy is $2,260.00 per month as quoted from an Insurance Company with no lapse policies. In order to pay this premium he purchases a life only immediate annuity for $367,827.11 that will begin monthly payout of $2,269. The annuity payout will be used to pay the life insurance premium. At death, the beneficiaries of the life insurance policy will receive $1,000,000 tax-free. The owner leveraged taxable annuity money into tax-free money for his beneficiaries.

A fixed indexed annuity with a lifetime income rider (hybrid Annuity) could be used instead of an immediate annuity. The FIA accumulation account grows and is credited with market type gains. The lifetime income rider guarantees annual payments

beginning in one year. An FIA with an original deposit of

Here’s an example

of how to fund a life

insurance policy

using an immediate

annuity.

Another option

using a Hybrid

Annuity to transfer

tax-free money to

your beneficiaries.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 13

approximately $470,000 would be required to generate annual payments of $27,000 to cover the life insurance premiums. Unlike the immediate annuity when the owner dies any money remaining in the cash accumulation side of his FIA goes to the beneficiaries. The beneficiaries could then receive both the death benefit from the life insurance policy and any remaining account value in the FIA. The FIA also has liquidity. Taking cash from the FIA would reduce the guaranteed payout and might compromise the ability to continue the life insurance premium but liquidity is still a feature of the FIA. Whether you choose an immediate annuity or a FIA to fund your life insurance policy you will achieve the end result of transferring money tax-free to your beneficiaries.

What’s the “Bonus” Catch?

Fixed-Indexed annuities can offer you a 5% - 10% bonus on all deposits, rollovers or transfers for up to 10 years. The insurance company provides you with an incentive to save your money with safety. And the interest that you receive on your savings and the bonus is tax deferred. You pay no taxes on

the money until you start receiving your income at retirement. Insurance companies can pay a bonus when you make a long term commitment (usually 10 years or more) to let them use your money. Taking the upfront bonus is like having an immediate guaranteed interest growth of your savings. You also receive interest on your bonus. If you put in $100,000 then your immediate balance would be $110,000 and interest would be credited on the $110,000 balance. If you leave the money with the insurance company for 10 years you can walk away with your money, the bonus, the accumulated interest on your money, and the interest on your bonus! So what’s the catch? Well, bonus products are typically longer term contracts (10 years or more) and it’s possible that since they’re giving you an upfront bonus they may offer less downside potential than other products. This information is clearly laid out in the contract.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 14

Make sure you know the details and ask questions before you sign anything.

How Surrender Charges Work?

Surrender charges are often cited by the Anti-annuity people as the reason annuities are horrible investments. But are the criticisms legitimate?

Hybrid annuities have what’s called “Surrender Charges”. Or, you could think of it like an early exit penalty. Saving for retirement is a long term commitment.

The insurance company rewards saver's with a bonus when annuities often require 9 or 10 years until maturity. When evaluating surrender charges you should consider that you are getting a higher rate for the longer time that you have your money with the insurance company. Therefore, think about when you want or might need your money. How much do you need and when? If the insurance company has 10% free withdrawals without penalty, decide if that amount is enough for you. You might consider putting some of your money into a fixed-indexed annuity with a shorter period of surrender charges. That type of fixed-indexed annuity may not have a bonus but access to more of your money might be more important than the higher rate of return. Remember that your fixed-indexed annuities grow tax deferred with triple compounding so, irrespective of the length of your annuity, you are safely building your retirement income. A 10 year fixed-indexed annuity might have a 10% surrender charge. The surrender charge decreases by 1% per year. After the 10 years you can withdraw all of your money without a surrender charge. If you received a 5% -10% bonus at inception on your annuity the surrender charge may be higher. In essence the insurance company is taking some of the bonus back if you don't stay in the contract for the full term.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 15

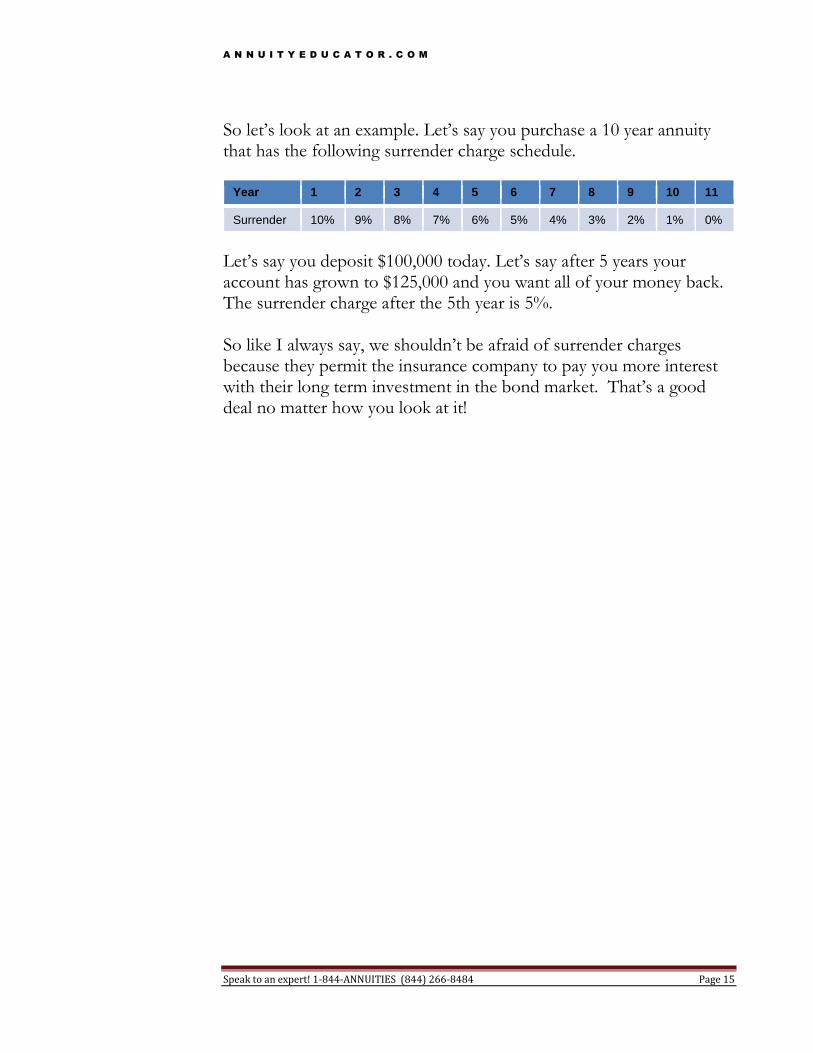

So let’s look at an example. Let’s say you purchase a 10 year annuity that has the following surrender charge schedule.

Year 1 2 3 4 5 6 7 8 9 10 11

Surrender 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0%

Let’s say you deposit $100,000 today. Let’s say after 5 years your account has grown to $125,000 and you want all of your money back. The surrender charge after the 5th year is 5%. So like I always say, we shouldn’t be afraid of surrender charges because they permit the insurance company to pay you more interest with their long term investment in the bond market. That’s a good deal no matter how you look at it!

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 16

What you’ll learn in Part 2

ere you are at age 45, 55, 65, or maybe even at 75 years old. You have worked your whole life to save up a nest egg, and every day you are getting closer and closer to retiring and not

getting a paycheck anymore.

How do you know if you have enough to retire? How do you make sure you and your spouse will have enough income coming in every month to pay the bills and have some fun for 20-30 years of retirement? Unfortunately, most people don’t get

much of a pension these days. Social Security is really nice, but it barely keeps pace with inflation and it’s not enough to cover all of your expenses.

So most likely you’ll be relying on your IRA’s, 401(k)’s, bank accounts etc., to provide you with income to supplement your Social Security.

Getting secure and predictable retirement income is what we

will cover in Part 2. It’s easier than you think. Part 2 talks about where Hybrid Annuities can fit in an overall financial plan. Retirement Income planning is just one issue you face when planning your retirement, but we feel it’s the most important because if you don’t have enough secure, predictable income coming in every month, for your whole retirement, all the little problems seem to get even worse.

Part

2

H Will your Social

Security or Pension

be enough to pay

your bills and have

fun?

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 17

First, I’ll define why income is a problem. Next, I’ll describe 3 methods that people use trying to set their accounts up to get that income. Finally, I’ll explain a simple way to look at your money that solves this problem once and for all, so you can stop thinking about.

The Problem with Retirement Income

I truly believe that, despite press reports to the contrary, we don't have a Social Security problem in America: We have a retirement problem.

As a Retirement Income Expert, I want to ensure that I produce the right retirement outcome for ALL my clients – not just the wealthy ones. It would be great if we could call on our leaders to recognize and elevate the Social Security problem and take steps to address it. But let’s face it, we can’t. I don’t claim to have all the answers, but I believe that compelling everyone to save more and save smarter has to be part of the solution.

First, the facts: We are living longer -- the average 65-year-old has nearly two decades of life ahead, and one in every four will live past 90 -- but producing fewer workers. That combination is producing a big bill for longer retirements that we're already struggling to pay.

Meanwhile, some of us are relying on Social Security to be the primary source of income in retirement when in fact it was always intended to be part of a three-legged stool that includes private pensions and savings. But more than one-third of retirees are getting 90% or more of their income from Social Security.

We depend too much on Social Security, private pensions are less available, too few workers have 401(k)s, and Americans aren't saving enough or appropriately for retirement.

So what can we do?

If you are one of the millions of people who will need income

from your IRA, 401(k) to supplement Social Security after you

retire, you might want to consider setting up your own “Personal Pension Plan” to insure you have income security.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 18

3 Methods to Solve the Income Problem

So let’s look at the 3 most common ways people solve the secure retirement income problem by using my sample clients “Tom and Martha”: Tom is a 63-year-old Chief Tech Officer at a bustling software company. He and his wife Martha are both hoping to retire in 4 years. They have been diligently contributing to their 401(k)’s and have put $600,000 aside in savings. Tom tends to prefer the safety of his savings account but isn't sure if that combined with his 401(k) will be enough to last throughout retirement. His friends are telling him to invest in more stocks or to purchase a foreclosed home to build up equity, but in the current market Tom feels all of these options seem a little too risky. Their estimated income and expenses at retirement are: $3,300 Income per month (Combined Social Security) $5,000 Expenses per month (Taxes, Insurance, Food, etc.) So it looks like they are $1,700 short per month. This shortage is your Income Gap.

When it comes to your base retirement income, you must solve for your Income Gap with as much certainty and guarantees as possible because you want to be 100% certain that

no matter how bad the economy gets, or what happens in the stock market, that you keep getting your retirement income month after month and year after year. So how do you do it? How are you going to set up your accounts to generate the income you need? Here are three common ways that

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 19

people do it. But ... will they pass the “Safe and Predictable”

income test?

1. THE BANK:

Keep your money in the bank and withdraw the interest. Never touch the principal. This could work out fine if interest rates are at 6%, but with interest rates around 0-2% it’s tough to generate enough income. So that means you have to start dipping into principal. This creates a downward spiral because then you have less money earning interest and you are taking out more than what you are earning which further depletes the principal. You could wind up in a situation where you run out of money. Also, it’s impossible to predict where interest rates will be in 5, 10, 20 years.

Does the Bank pass the “Safe and Predictable” income test?

No.

2. MUTUAL FUNDS: Keep your IRA/401(k) in a diversified basket of mutual funds and withdraw 4% per year. This was the old model that advisors used for quite a few years. It can work well if the market keeps going up. You can take your income and have a nice nest egg. However, many academics have discredited the 4% model because it doesn’t always work. In fact it can fail quite often. The 4% model is not a secure and predictable way to set up your “Personal Pension”. There are a couple of reasons why the 4% rule isn’t working. Interest rates are really low and that is making it really tough for the bond portion of your portfolio to do its job. Just take a look at this excerpt “Say Goodbye to The 4% Rule for Retirement” Wall Street Journal – March 3, 2013 Can your nest egg last your whole lifetime? It's getting tougher to tell. Conventional wisdom says you can take 4% from your savings the first year of retirement, and then that amount plus more to account for inflation each year, without running out of money for at least three decades.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 20

This so-called 4% rule was devised in the 1990s by California financial planner William Bengen and later refined by other retirement-planning academics. Mr. Bengen analyzed historical returns of stocks and bonds and found that portfolios with 60% of their holdings in large-company stocks and 40% in intermediate-term U.S. bonds could sustain withdrawal rates starting at 4.15%, and adjusted each year for inflation, for every 30-year span going back to 1926-55. Well, it was beautiful while it lasted. In recent years, the 4% rule has been thrown into doubt, thanks to an unexpected hazard: the risk of a prolonged market rout the first two, or even three, years of your retirement. In other words, timing is everything. If your nest egg loses 25% of its value just as you start using it, the 4% may no longer hold, and the danger of running out of money increases. If you had retired Jan. 1, 2000, with an initial 4% withdrawal rate and a portfolio of 55% stocks and 45% bonds rebalanced each month, with the first year's withdrawal amount increased by 3% a year for inflation, your portfolio would have fallen by a third through 2010, according to investment firm T. Rowe Price Group. And you would be left with only a 29% chance of making it through three decades, the firm estimates. That sort of scenario has left many baby boomers who are in the midst of retiring riddled with angst. "The mind-blowing aspect of retiring is all these years you're accumulating and accumulating, and then you need to start drawing down, and you have no idea how to do that," says Al Starzyk, a 66-year-old retired printing executive in Williamsburg, Va. So, if you can't safely withdraw at least 4% a year from a balanced portfolio of equity and bond funds, what do you do? …..

Do Mutual Funds pass the “Safe and Predictable” income test?

No.

3. ANNUITIES:

Move some of your money into an annuity and let it pay out when you need it. There a quite a few different types of annuities. They each work a little differently and they each have their own set of pro’s and con’s. For purposes of “Secure & Predictable” income there are two types you could look at. The first is called an immediate annuity. You deposit a lump sum with an insurance company and in exchange, the insurance company will

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 21

make payments to you for the rest of your life. The good part is you get income for life, but the bad part is you give up control in case your needs change down the road. It’s irrevocable. Another type of annuity that provides you more flexibility is what we have been talking about in this report. An Index Annuity with an income rider, also known as “Hybrid” annuities. They combine a growth account with an income account. You’ll know 2, 5, 10 years in advance exactly how much income you’ll get when you need it.

Do Annuities pass the “Safe and Predictable” income test?

Yes!

They are the only financial product that provides “Secure & Predictable” income.

The Solution to the Income Puzzle

Here is a simple way to fix the secure retirement income problem. Let’s look again at the money tools we have to work with:

Bank Accounts - Really good at being liquid and paying bills

Mutual Funds - Really good at long term potential growth

Annuities - Really good at providing secure and predictable

income

If we want “Secure &

Predictable” income

… then we need to

move a portion of

your money into the

right type of account

to do that!

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 22

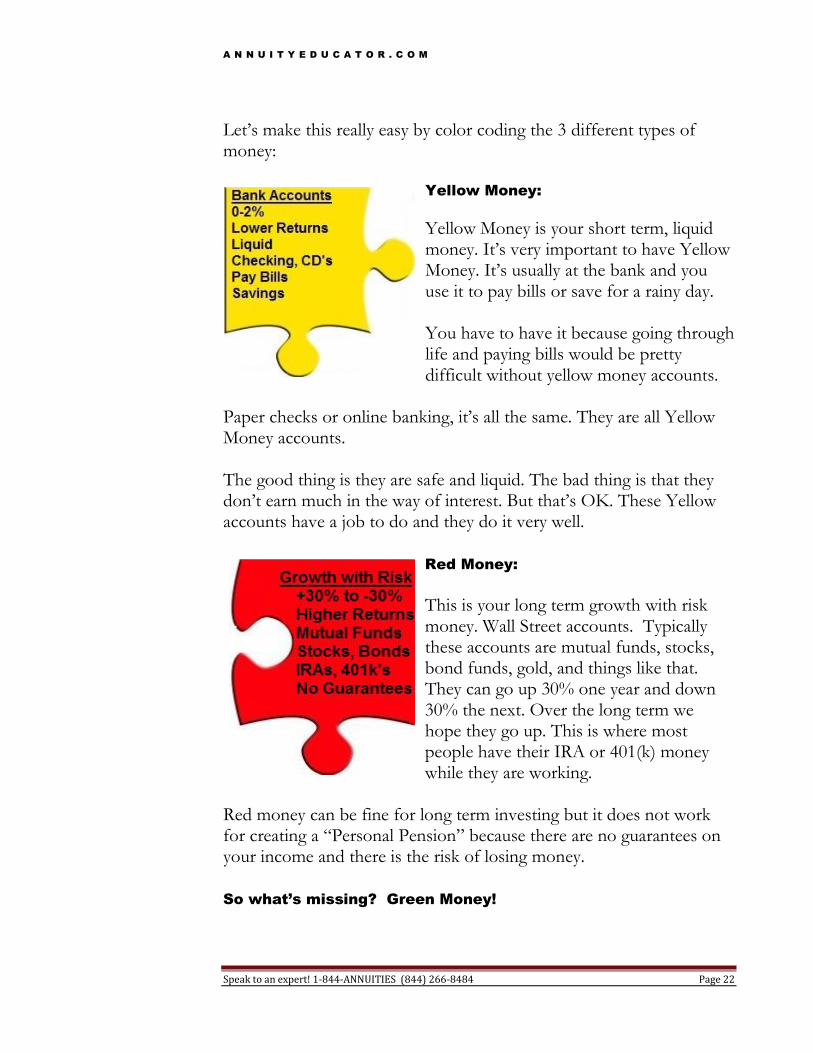

Let’s make this really easy by color coding the 3 different types of money:

Yellow Money:

Yellow Money is your short term, liquid money. It’s very important to have Yellow Money. It’s usually at the bank and you use it to pay bills or save for a rainy day. You have to have it because going through life and paying bills would be pretty difficult without yellow money accounts.

Paper checks or online banking, it’s all the same. They are all Yellow Money accounts. The good thing is they are safe and liquid. The bad thing is that they don’t earn much in the way of interest. But that’s OK. These Yellow accounts have a job to do and they do it very well.

Red Money:

This is your long term growth with risk money. Wall Street accounts. Typically these accounts are mutual funds, stocks, bond funds, gold, and things like that. They can go up 30% one year and down 30% the next. Over the long term we hope they go up. This is where most people have their IRA or 401(k) money while they are working.

Red money can be fine for long term investing but it does not work for creating a “Personal Pension” because there are no guarantees on your income and there is the risk of losing money. So what’s missing? Green Money!

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 23

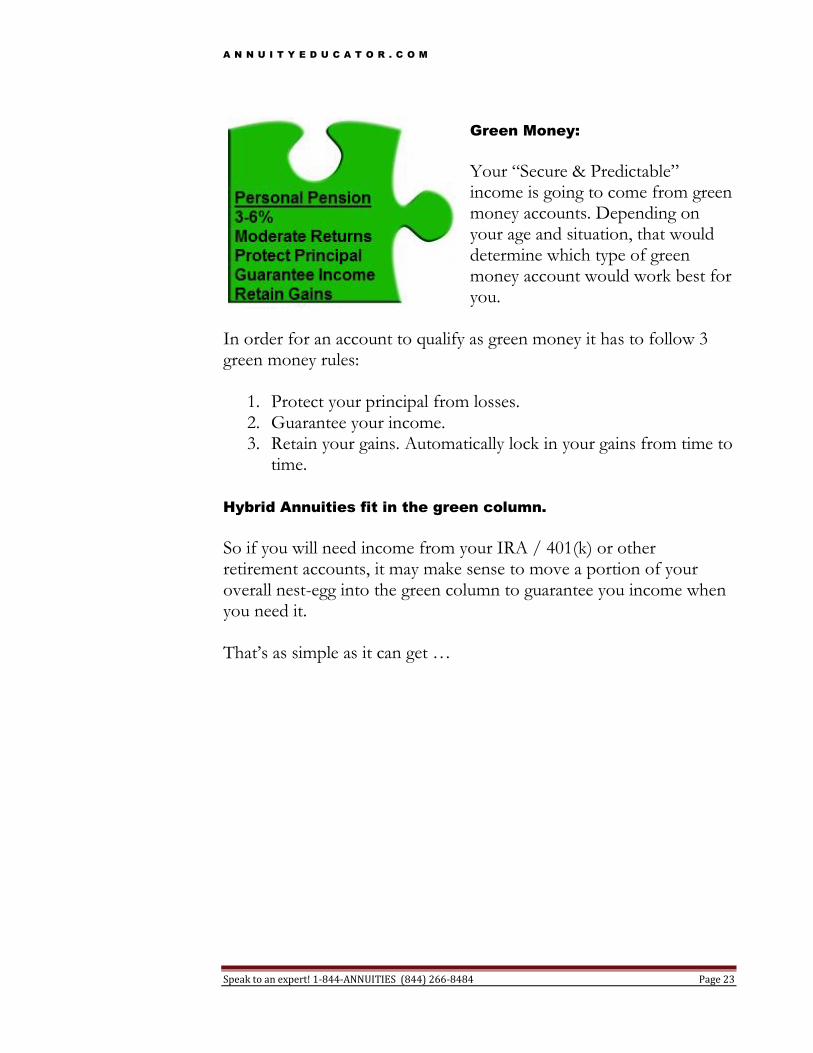

Green Money:

Your “Secure & Predictable” income is going to come from green money accounts. Depending on your age and situation, that would determine which type of green money account would work best for you.

In order for an account to qualify as green money it has to follow 3 green money rules:

1. Protect your principal from losses. 2. Guarantee your income. 3. Retain your gains. Automatically lock in your gains from time to

time. Hybrid Annuities fit in the green column.

So if you will need income from your IRA / 401(k) or other retirement accounts, it may make sense to move a portion of your overall nest-egg into the green column to guarantee you income when you need it. That’s as simple as it can get …

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 24

Do-It-Yourself Pension using an Annuity

o how can we use a “Hybrid Annuity” to set up your own personal pension? It’s actually easier than you think!

As we saw earlier, many people continue to use mutual funds to get their income when they retire. They continue to use the same investments that attempted to grow their money when they were younger, to now get their retirement income. But in my opinion it’s the wrong tool for the job and can get risky! Perhaps you are reading this guide about Hybrid Annuities because you are already thinking that an annuity might be a good fit for some of your money. So let’s look at how you can use a Hybrid Annuity to set up your own “Personal Pension Plan”. First of all, we like the benefits of a pension because:

You get steady income every month

It will last as long as you live

You don’t really have to worry about it too much Next, there are typically two phases to a personal pension plan:

1. “Grow Period” - This is when you are still working and the longer you work and the longer you wait, the more income you will get when you finally draw on it.

2. “Draw Period” - This is when you actually retire and start getting the income that you waited for.

So how do you set up your 401(k) or IRA now, so it works like

your own “Personal Pension Plan” when you retire?

Part

3

S

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 25

Let’s look at a simple illustration:

You are 60 right now and want to retire at 65

Your combined IRA/401(k) and other savings are $400,000

You will get $2,000 a month from Social Security when you retire in 5 years

You anticipate your expenses to be $3,000 a month Given the information above, you will be short $1,000 a month. This is your Income Gap. So let’s set up a “Personal Pension Plan” with a portion of your money now, so when you retire in 5 years, you know for certain that you will solve your Income Gap with contractual

guarantees. For this example we are going see if a Fixed Index Annuity with an Income Rider (Hybrid Annuity) can solve your problem.

1) “The Grow Period” - With Hybrid Annuities, this is called your Roll Up period. There is a Roll Up Percentage, which is the amount that your Income Account grows at. Let’s say your Roll Up is 7%, just for an example. That means if you put in $100,000, after one year, your income account will be $107,000. After two years it’s at $114,490 and so on. This Income Account is what your lifetime income is going to be based on. Think about Social Security. The longer you wait, the more income you get when you take it. The Roll Up works the same way. The younger you are when putting money into one of these and the longer time it has to grow, the more income you will get when you finally need it.

2) “The Draw Period” - At some point in the future, you decide to start your guaranteed lifetime income. This is where The Withdrawal Percentage comes into play. The Withdrawal Percentage is a withdrawal rate that the insurance company contractual guarantees you for the rest of your life. It varies from company to company. It is also age based. So the older you are when you start your income, the higher percentage withdrawal you get.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 26

Let’s look at this typical withdrawal rate table:

4.5% At age 60

5.0% At age 65

5.5% At age 70

So now let’s figure out how much you need to put into a Hybrid Annuity today to meet your goals for the future. Let’s go back to

our example and do the math:

You are 60 right now.

You need $1,000 a month starting in 5 years when you retire

at 65.

You have $400,000 to work with.

If you put $175,000 into our example annuity right now, in 5

years your income account value will grow to $245,446

(Using 7% growth rate).

At age 65 your withdrawal percentage is 5.0%.

So $245,446 x 5.0% = $12,272 per year. Or just over $1,000

per month.

Age Income Account Growing at 7%

Withdraw Percentage

Guaranteed Lifetime Income

60 $175,000 4.50% $7,875

61 $187,250 4.60% $8,613

62 $200,357 4.70% $9,416

63 $214,382 4.80% $10,290

64 $229,389 4.90% $11,240

65 $245,446 5.00% $12,272

66 $262,627 5.10% $13,393

67 $281,011 5.20% $14,612

68 $300,682 5.30% $15,936

69 $321,730 5.40% $17,373

70 $344,251 5.50% $18,933

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 27

So to summarize our case example:

Starting in 5 years, you will get $12,272 a year for the rest of your life. Guaranteed!! Also, there is $225,000 left over that you can invest however you like. We didn’t need to use all of your money to create your “Personal Pension Plan” so you are free to invest the remaining

$225,000 however you want, because you have the peace of mind that you will get the income you need when you retire in 5 years, and that income won’t be affected by ups and downs in the market.

The Next Steps

Choose Wisely! Don't forget that once you've chosen your

annuity provider and set up your annuity you cannot change it for the duration of your contract, so you must take your time and choose the best annuity for you and your family's needs.

Before you apply, double check your annuity quote to ensure all the details are correct (such as your postcode, marital status and date of birth). Changes to these details may change the amount and type of annuity payable. Read all the information carefully including the Key Features and Terms & Conditions of your chosen annuity provider.

Ask Questions! Got an annuity query? Call our experts. Remember, we're always here to help you. If you have any questions about your retirement options, please contact our annuity experts at 1-(844)-ANNUITIES or (844) 266-8484.

Make the Time! The time it takes to set up your annuity will depend upon if you are transferring your funds from your current IRA or 401(k), etc. This transfer will depend on the efficiency of your existing investment provider and how quickly they will forward your

Congratulations! You

just solved your future

income needs with

contractual guarantees.

(And it only took a

portion of your overall

nest egg).

T H E K E Y

Choose Wisely!

Ask Questions!

Make the Time!

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 28

funds to your new annuity company. Most transfers take two or three weeks.

Our experienced team will speak to your investment provider and your new annuity company on a regular basis and keep you up-to-date to ensure the process is as quick and seamless as possible.

How much does it cost to set up an annuity?

The annuity rate comparison and all of our consultation service is free. If you decide to go ahead, we get paid a one-time commission directly from the annuity insurance company. It's simple - we'll find you a competitive annuity, we’ll do all the work for you to get you a better retirement income, and you never pay us a dime.

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 29

A Note from the Author

Dear Reader,

Although I did my best at offering accurate, educational content, I must disclaim that I am not responsible for any mistakes that might have been overlooked. This guide is not intended to be investment advice or a recommendation to buy or sell anything.

Please consult the Insurance Company’s Statement of Understanding and Disclosure documents before buying an annuity and always consult the appropriate tax, legal or investment advice before buying or selling anything.

Sincerely,

David Novak

President, First American Advisors, Inc.

Founder, AnnuityEucator.com

License # 0H73574

18881 Von Karman Ave., Suite 1470

Irvine, California 92612

949.398.2200 | 800.823.9872 | Fax: 949.679.0200

Email: [email protected]

Website: www.annuityeducator.com Facebook: www.facebook.com/pages/First-American-Advisors-Inc/

LinkedIn: www.linkedin.com/in/invitedavidnovak/

A N N U I T Y E D U C A T O R . C O M

Speak to an expert! 1-844-ANNUITIES (844) 266-8484 Page 30

Index

401(k) Money, 9 annuicide, 7 Annuity Account Value, 5 Bank Money, 19 Beneficiary(s), 12 Bonus Incentive, 13 Caps, 8 Death Benefit, 12 Dow Jones Industrial Average, 7 Draw Period, 24 Exaggerated Monthly Caps, 8 Fees, 10 FIA, 13 Fixed Rate, 4 Flat Contract Fees, 11 Green Money, 23 Grow Period, 24 Hybrid Annuities, 3 Immediate Annuity, 4 Income Account Value, 5 Income Gap, 18

Index Annuity, 4 Investment Management Fees, 11 IRA, 9 Life Insurance, 12 Liquid Money, 11 Mortality and Expense Charge, 11 Mutual Funds, 19 Non-Qualified Money, 10 Participation Rate, 9 Personal Pension Plan, 18 Qualified Money, 10 Red Money, 22 Rider Fees, 11 Roll-Up Rate, 5 S&P 500 Index, 7 Social Security, 17 Spread, 9 Surrender Charges, 14 Tax Deferral, 9 Yellow Money, 22